Sample Category Title

Flash PMIs in focus

In focus today

Today all eyes are on the euro area December flash PMIs as the very large decline in November caused significant market moves. There was nothing positive in the November report where the services PMI fell below 50 to 49.5 for the first time since January, and the manufacturing PMI remained stuck at 45.2. We expect the economic situation to be little changed since November and forecast negative quarterly GDP growth in Q4. We thus expect the PMIs to decline slightly in December to 44.9 in the manufacturing sector and remain at 49.5 in the service sector.

We also receive the flash PMIs for November from the US and UK later in the day.

In France, the National Assembly will debate a "special law", which will allow the 2024 budget to be rolled over to 2025 to avoid a government shutdown. The National Rally has said that it will support the law, thereby allowing the current caretaker government to manage minimal state expenditures until a new government is formed. While it is our base case that the law will pass there is a risk that it is not passed, which will increase uncertainty in French politics. In this case, President Macron will need to use an unprecedented law by the constitution to pass budgetary measures without going through Parliament.

Economic and market news

What happened overnight

In China, activity remains weak as retail sales for November came in weaker than expected at 3.0% y/y (consensus: 5.0%, prior: 4.8%). Coupled with Chinese credit growth slowing and money supply growth posing a drag with M1 at -3.7% y/y, albeit up from -6.1% y/y in October, the data highlights the need for more stimulus from Chinese authorities. Chinese equities edged lower on the data releases out overnight.

What happened since Friday

In France, the veteran centrist politician Francois Bayrou was appointed the role as prime minister on Friday. Barou is a long-term ally of president Macron as head of the centrist Democratic Movement (MoDem). Barou has the tacit support from the far-right national rally who said they will not back a no-confidence vote against him by default. However, while the prime minister is new, he will face the same old hurdles as Barnier given the highly divided National Assembly. Because of this, markets did not react to the announcement on Friday. Additionally, Moody's downgraded France to Aa3 from Aa2 over the weekend since the outlook of the country's public finances will be substantially weakened over the coming years.

In the UK, monthly GDP for October surprised to the downside at -0.1% m/m (cons: 0.1%, prior: -0.1%). There is likely some negative sentiment effects from the Autumn statement as flagged by the past PMI reports. The downside surprise is broad-based but in particular driven by industrial and manufacturing production affected by weather disruptions.

Equities: Global equities were lower on Friday and throughout last week, though we are talking about smaller movements alongside some indications of Christmas trading commencing, despite being in a busy period for central banks. The most interesting aspect last week was the bond market, with yields rising across all five days. Nevertheless, equities reacted only marginally to the movement in bonds. Growth and technology sectors performed well, despite the increase in yields, while small-cap stocks lost almost 1% relative to large-cap stocks last week. In the US on Friday, the Dow fell by 0.20%, the S&P 500 remained unchanged, the Nasdaq rose by 0.1%, and the Russell 2000 declined by 0.6%. Most Asian markets are in the red this morning. European futures are also lower, while US futures are slightly positive.

FI: It was another eventful week in the European fixed income market given the bearish reaction to the ECB meeting last week and the unexpected downgrade of France from Moody's from Aa2 to Aa3. The 2Y and 10Y EUR swap rates rose some 10bp after the ECB meeting despite the dovish tone from Lagarde.

FX: Last week saw a generally stronger USD, only NOK outperformed, while we found JPY and CHF at the bottom. USD/JPY was rejected at 150 and instead closed the week 2.5% higher at above 153.50 as US yields soared. Meanwhile, EUR/USD gyrated between gyrated between 1.0450 and 1.0600, just to close the week around 1.0500. The CHF weakened after the surprise 50bp rate cut. EUR/CHF soared to a 1M high. EUR/SEK remained within a tight range just above 11.50. EUR/NOK dropped from 11.80 to around 11.70. This week, the central bank takes centre stage with five rates decisions within 17 hours on Wednesday and Thursday.

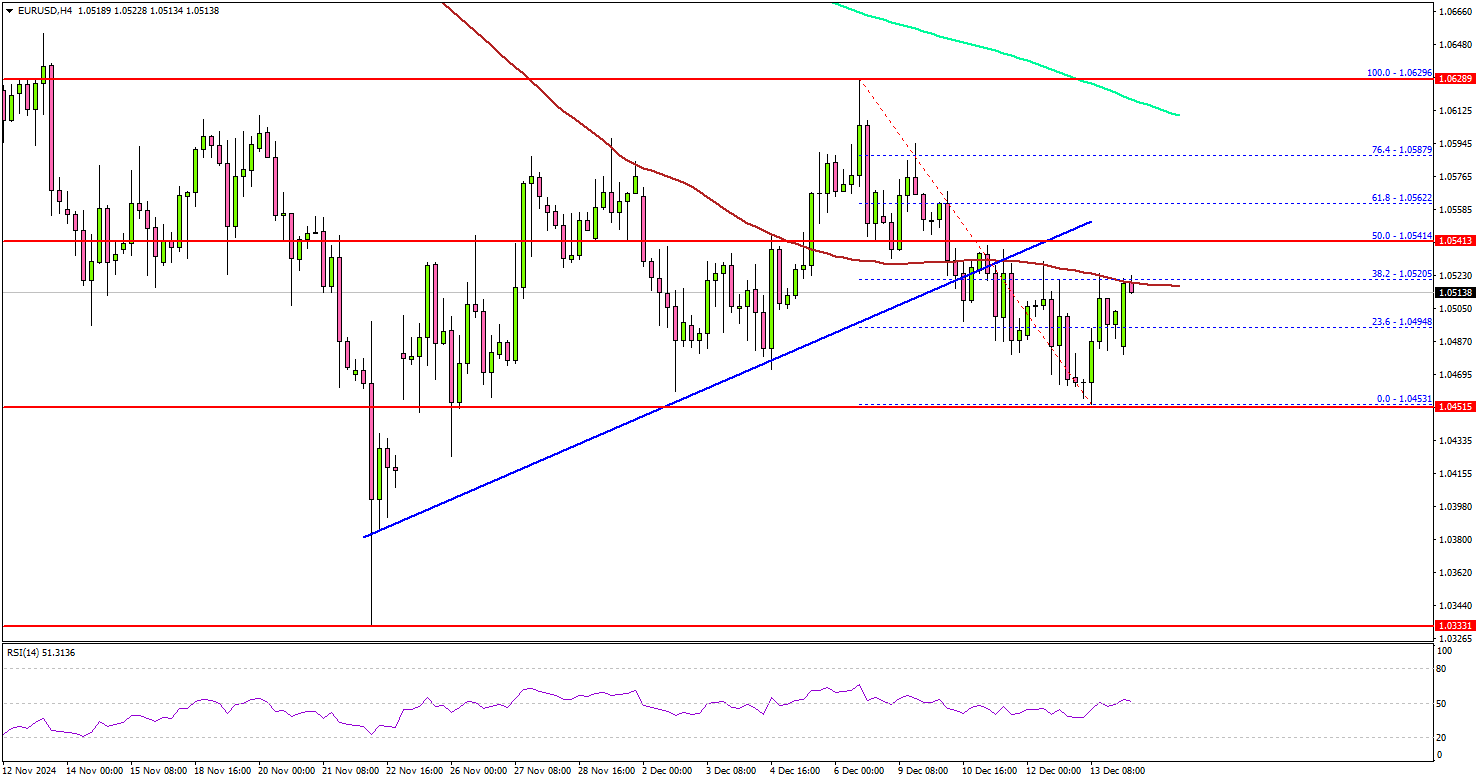

EUR/USD Wavers: A Tough Road Ahead for The Bulls

Key Highlights

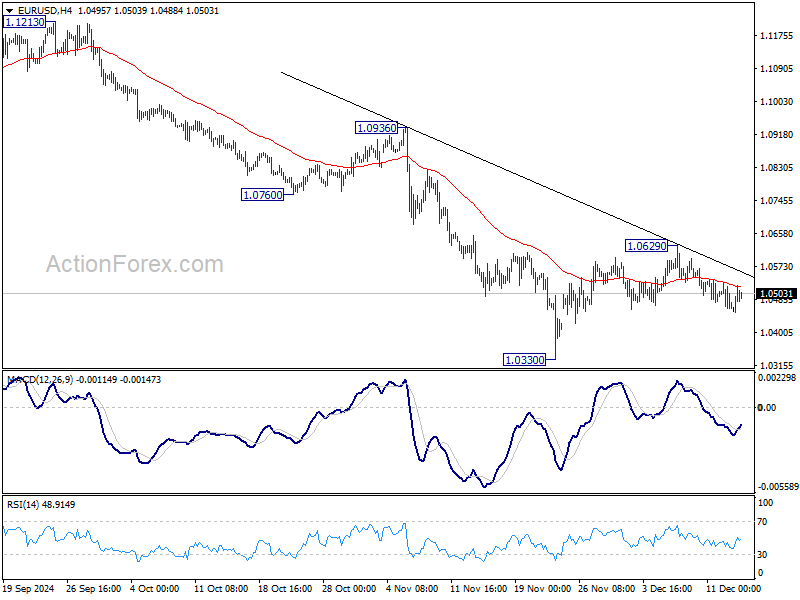

- EUR/USD struggled to extend gains above the 1.0620 resistance zone.

- It traded below a connecting bullish trend line with support at 1.0535 on the 4-hour chart.

- USD/JPY is attempting to climb above the 154.00 resistance zone.

- Bitcoin rallied to a new all-time high above $106,000.

EUR/USD Technical Analysis

The Euro failed to settle above 1.0620 against the US Dollar. EUR/USD started a fresh decline and traded below the 1.0550 support zone.

Looking at the 4-hour chart, the pair traded below a connecting bullish trend line with support at 1.0535. There was a move below 1.0480 and the pair traded as low as 1.0453. It is now consolidating losses and trading near the 38.2% Fib retracement level of the downward move from the 1.0629 swing high to the 1.0453 low.

The pair is now below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). On the upside, the pair could face resistance near the 1.0520 level.

The first major resistance is near the 1.0540 level. It is close to the 50% Fib retracement level of the downward move from the 1.0629 swing high to the 1.0453 low. A close above the 1.0540 level could set the tone for another increase.

The next major resistance could be the 1.0600 level, above which the price could climb higher toward the 1.0620 resistance.

On the downside, immediate support sits near the 1.0480 level. The next key support sits near the 1.0450 level. Any more losses could send the pair toward the 1.0410 level.

Looking at Bitcoin, the price started another increase and there was a move to a new all-time high above $106,000.

Upcoming Economic Events:

- Euro Zone Manufacturing PMI for Dec 2024 (Preliminary) – Forecast 45.0, versus 45.2 previous.

- Euro Zone Services PMI for Dec 2024 (Preliminary) – Forecast 49.9, versus 49.5 previous.

Inflation Pressures and Yield Surge Anchor Dollar as Top Performer

Dollar ended as the strongest performer last week, boosted by a surge in U.S. Treasury yields following persistent inflation data. Despite expectations of another 25bps rate cut at the upcoming FOMC meeting, stubborn price pressures are likely to slow the pace of policy easing next year. Adding to the caution, inflation uncertainties under the incoming administration's fiscal and trade policies will keep Fed on guard, discouraging aggressive action. Technically, the Dollar Index’s near-term bullishness remains intact, though another strong rally would hinge on whether 10-year yield can make significant new gains.

Among commodity-linked currencies, both the Australian and Canadian Dollars finished on firm footing. Aussie overcame RBA’s dovish shift, as robust domestic employment data tempered expectations of an early policy cut in February. Similarly, Canadian Dollar found support after BoC delivered a second 50bps rate cut but signaled a more measured approach moving forward. This shift in tone suggests that both central banks are not in a rush to push rates lower and are more inclined to respond thoughtfully to incoming data.

In Europe, Euro stood out, benefiting from the ECB’s modest 25bps rate cut and officials’ commitment to gradualism. By contrast, Swiss Franc lagged, ranking as the second weakest currency after SNB delivered a surprising 50bps reduction, raising the prospect of a return to zero or negative rates if inflation weakens further.

Nevertheless, Yen was the worst performer, weighed down by higher yields in both the US and European markets. Meanwhile, Sterling and New Zealand Dollar found themselves in middle positions.

Hawkish Fed Undertones Emerge, Treasury Yields Soar and Dollar Gains

Last week brought significant surge in US Treasury yields, fueled by consecutive inflation prints that reinforced the persistence of price pressures. Headline CPI rose to 2.7%, marking the second straight monthly re-acceleration, while core CPI held steady at 3.3%. Adding to this inflationary backdrop, PPI hit 4.7%, its highest since February 2023.

Although these figures won’t stop Fed from delivering another 25bps cut at its upcoming meeting, they underscore the likelihood of a "hawkish cut." Markets now anticipate Fed signaling a pause in January and slowing the pace of rate reductions through 2025.

The need for a measured easing path is becoming increasingly evident. Disinflation has shown little progress in recent months, and inflationary pressures could re-emerge under President-elect Donald Trump’s anticipated fiscal and trade policies, which remain to be fully detailed.

Current market pricing reflects expectations for just two additional rate cuts in 2025, bringing the federal funds rate to 3.75–4.00%, already higher than Fed’s September median projection of 3.4% for year-end 2025. This represents a marked shift from September when markets anticipated a more aggressive easing cycle. The market’s uncertainty, with roughly a third of participants expecting fewer cuts and a third expecting more, highlights the uncertainty around the outlook.

Technically, the strong rebound in 10-year yield not makes the dip to 4.126 a false break of 55 D EMA. The development suggests that rise from 3.603 is still in progress. Retest of 4.505 resistance should be seen next, and firm break there will target 61.8% projection of 3.603 to 4.505 from 4.126 at 4.683.

More importantly, the development in 10-year yield solidifies that case that whole medium term correction from 4.997 has completed with three waves down to 3.603. The strong support from 55 W EMA (now 4.133) also supports this view. There is prospect of resuming the up trend of 0.398 (202 low) through 4.997 to 38.2% projection of 0.398 to 4.997 from 3.603 at 5.359 next year.

Dollar Index followed yields higher last week, and the development suggest that pull back from 108.07 has completed. While the near term corrective pattern could still extend with another falling leg, it's now looking more likely that downside will be supported by 38.2% retracement of 100.15 to 108.07 at 105.04, which is slightly below 55 D EMA (now at 105.12). Rise from 100.15 should resume sooner or later through 108.07, but that would depends on when 10-year yield would power through 4.505 resistance.

Also, the next rally in Dollar Index through 108.07 would solidify that case of medium term bullish trend reversal. Upside acceleration could follow through 161.8% projection of 99.57 to 107.34 from 100.15 at 112.72.

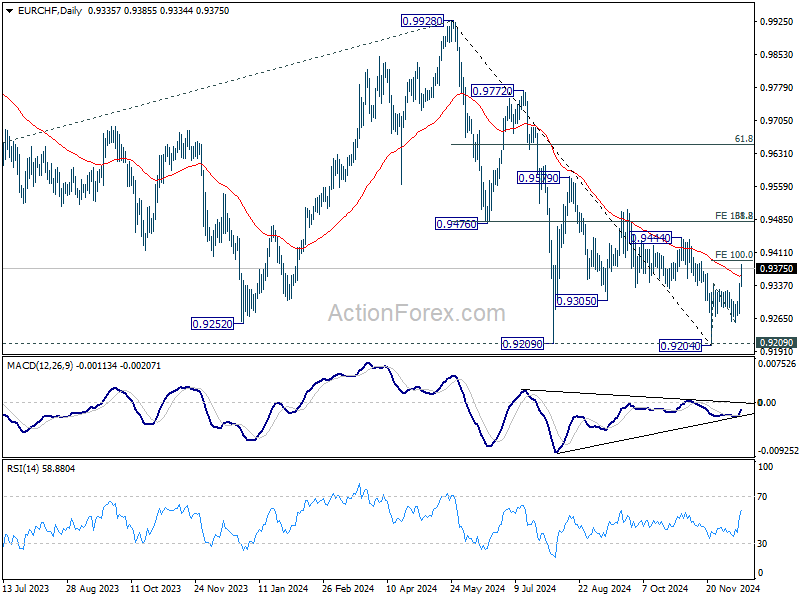

EUR/CHF Rises Sharply Amid SNB's Bold Cut and ECB's Gradualism

EUR/CHF climbed significantly, driven by divergent monetary policy decisions from SNB and the ECB. SNB delivered a hefty 50bps rate cut, pushing its policy rate down to 0.50%. This move was accompanied by revised inflation projections, which show inflation staying below the mid-point of SNB’s target range throughout the forecast horizon. While somewhat unexpected, the decision aligns with SNB’s historical pattern of bold actions, necessitated by Switzerland’s unique economic challenges as a small, open economy. The cut also brings Switzerland closer to the prospect of 0% rates and potentially negative territory if deflationary pressures continue to build.

In contrast, ECB implemented a more modest 25bps cut in its deposit rate, bringing it to 3.00%. Euro strengthened in the wake of commentary from ECB officials, who signaled a broad consensus for the gradual approach to easing. Policymakers expressed confidence in inflation returning to target levels without resorting to aggressive rate cuts, even as economic activity data remains weak. ECB’s preference for gradualism signals a desire to balance economic risks without triggering undue market anxiety.

Technically, EUR/CHF's rebound from 0.9204 resumed with strong acceleration last week. The firm break of 55 D EMA argues that a medium term bottom was already formed. Immediate focus is now on 100% projection of 0.9204 to 0.9343 from 0.9254 at 0.9393. Firm break there will be a strong sign of underlying bullish momentum, and pave the way to 161.8% projection at 0.9479. This level coincides with 38.2% retracement of 0.9928 to 0.9204 at 0.9481. Reaction there would reveal whether the cross is already in medium term trend reversal.

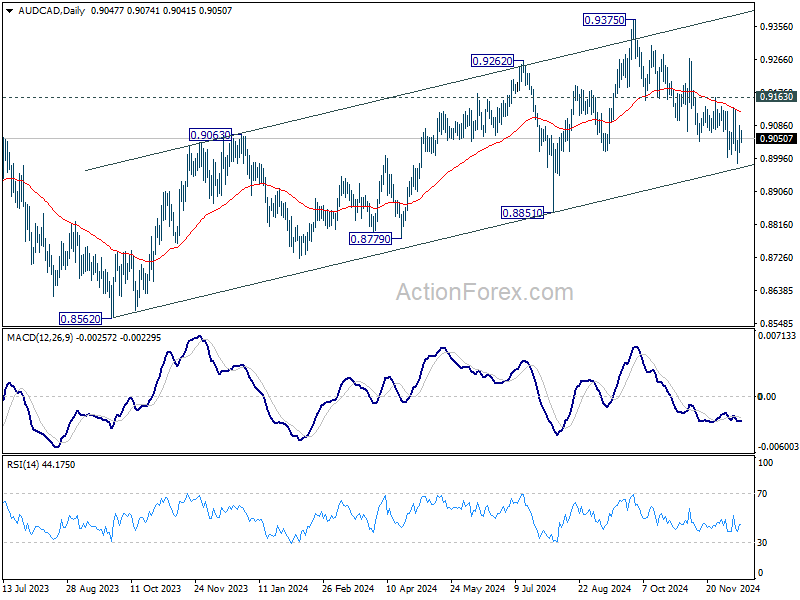

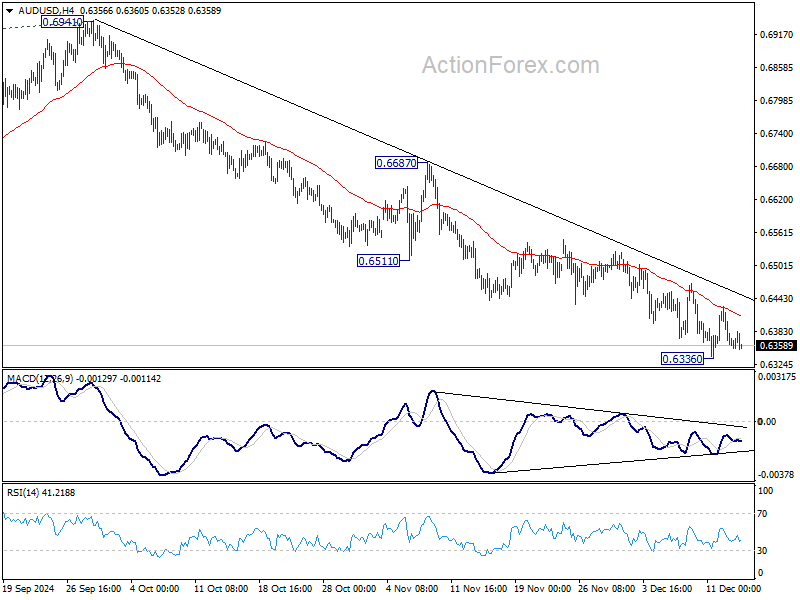

AUD/CAD Stays Indecisively Bearish after RBA and BoC

AUD/CAD remains on the defensive last week following developments in Australia and Canada, even though downside momentum has been indecisive.

RBA’s decision to keep rates unchanged at 4.35% was accompanied by a surprising dovish shift. Key in this shift was the central bank's move to drop the previously language of "not ruling anything in or out" regarding policy adjustments. This subtle but significant change signals a growing inclination toward rate cuts, contingent on further evidence of sustained disinflation. Governor Michele Bullock, when pressed on the likelihood of a February cut, candidly admitted she does not "actually know".

However, the case for imminent easing faced a setback with robust labor market data released just two days after the RBA meeting. November’s employment figures exceeded expectations, while unemployment rate fell unexpectedly to 3.9% from 4.1%. The persistently tight labor market could keep RBA cautious about prematurely easing policy.

In contrast, BoC moved decisively with a 50bps rate cut, bringing the overnight rate to 3.25%. This marks the second consecutive 50bps cut, placing policy at the top end of the neutral range. Governor Tiff Macklem signaled a shift toward a more measured easing approach, saying, “With the policy rate now substantially lower, we anticipate a more gradual approach to monetary policy if the economy evolves broadly as expected.” Market expectations for another cut in January stand at 70%, though a pause seems increasingly likely in the near term, as BoC evaluates the impact of its aggressive rate reductions.

Technically, AUD/CAD is now at a juncture. Near term outlook is staying bearish as the cross is held well below falling 55 D EMA. Yet, it's now in proximity to medium term rising channel support, which could limit downside in case of another fall. Indeed, break of 0.9163 resistance will argue that pull back from 0.9375 has completed, and was merely a correction. Rise from 0.8562 should then be ready to resume. However, sustained break of the channel support will argue that the trend has already reversed.

The pair’s trajectory in the near term hinges on the timing of RBA rate cuts and a BoC pause. Over the medium term, broader macroeconomic factors, including the impact of the US-China tariff war, will likely play a significant role. RBA Deputy Governor Andrew Hauser has just emphasized Australia’s "unique" vulnerability to global trade disruptions due to its heavy reliance on Chinese markets, a risk that could weigh on Australian Dollar further if tensions escalate.

USD/JPY Weekly Outlook

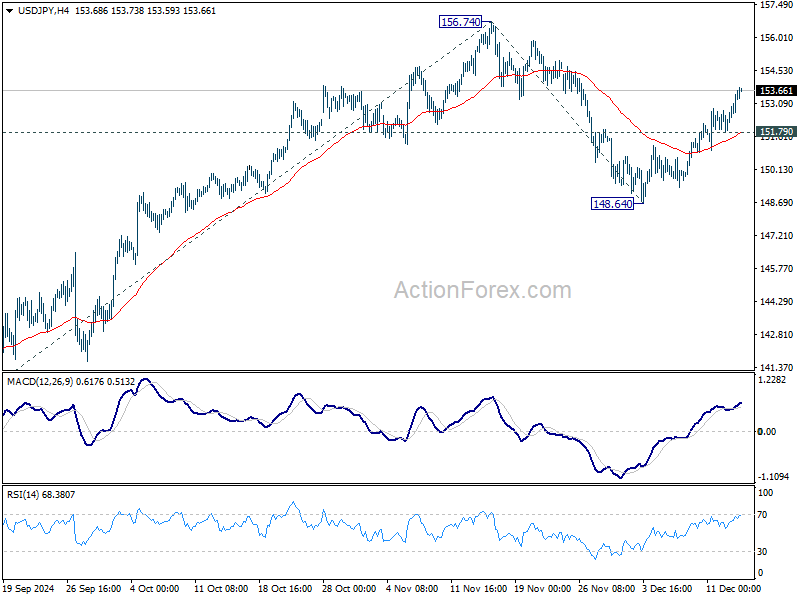

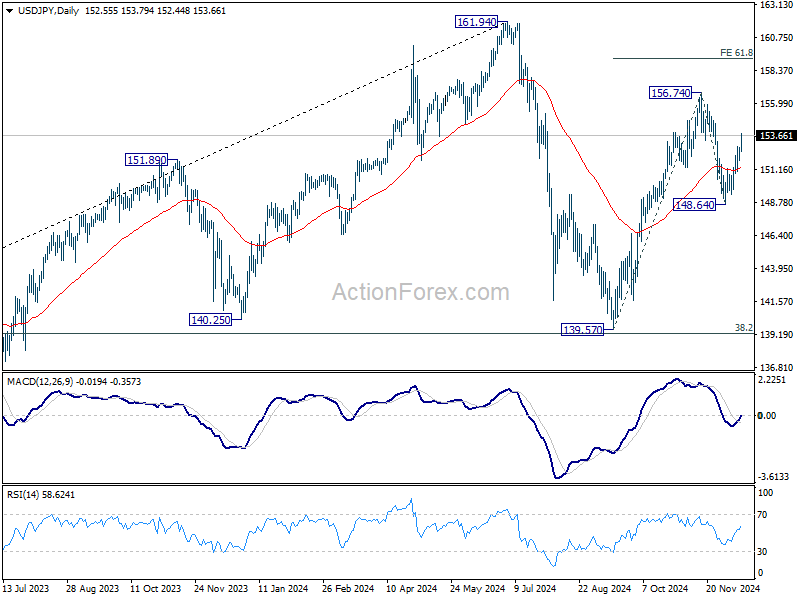

USD/JPY's stronger than expected rebound last week suggests that correction from 156.74 has completed at 148.64. Initial bias remains on the upside this week for retesting 156.74 first. Firm break there will resume whole rally from 139.57, and target 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next. On the downside, below 151.79 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 148.64 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

In the long term picture, it's still early to conclude that up trend from 75.56 (2011 low) has completed. However, a medium term corrective phase should have commenced, with risk of deep correction towards 55 M EMA (now at 134.98).

EUR/USD Weekly Outlook

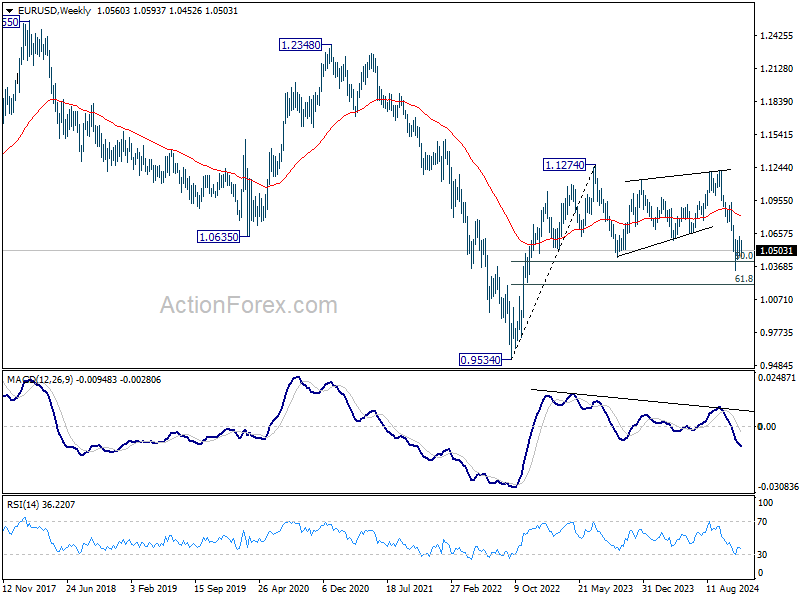

EUR/USD gyrated lower last week but recovered again after hitting 1.0452. Initial bias stays neutral this week first. Corrective pattern from 1.0330 might extend further. But outlook will stay bearish as long as 55 D EMA (now at 1.0678) holds. On the downside, below 1.0452 will bring retest of 1.0330 low.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

In the long term picture, down trend from 1.6039 remains in force with EUR/USD staying well inside falling channel, and upside of rebound capped by 55 M EMA (now at 1.0979). Consolidation from 0.9534 could extend further and another rising leg might be seem. But as long as 1.1274 resistance holds, downside breakout would be mildly in favor.

USD/JPY Weekly Outlook

USD/JPY's stronger than expected rebound last week suggests that correction from 156.74 has completed at 148.64. Initial bias remains on the upside this week for retesting 156.74 first. Firm break there will resume whole rally from 139.57, and target 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next. On the downside, below 151.79 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 148.64 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

In the long term picture, it's still early to conclude that up trend from 75.56 (2011 low) has completed. However, a medium term corrective phase should have commenced, with risk of deep correction towards 55 M EMA (now at 134.98).

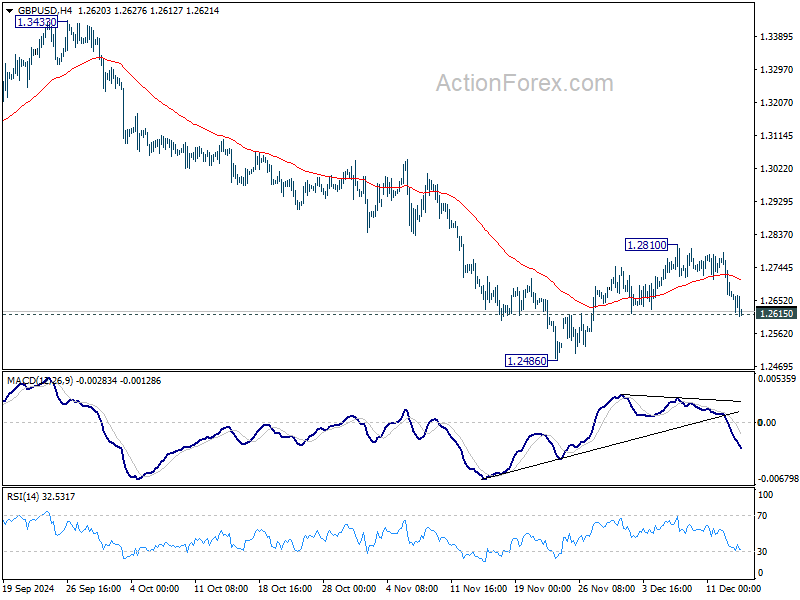

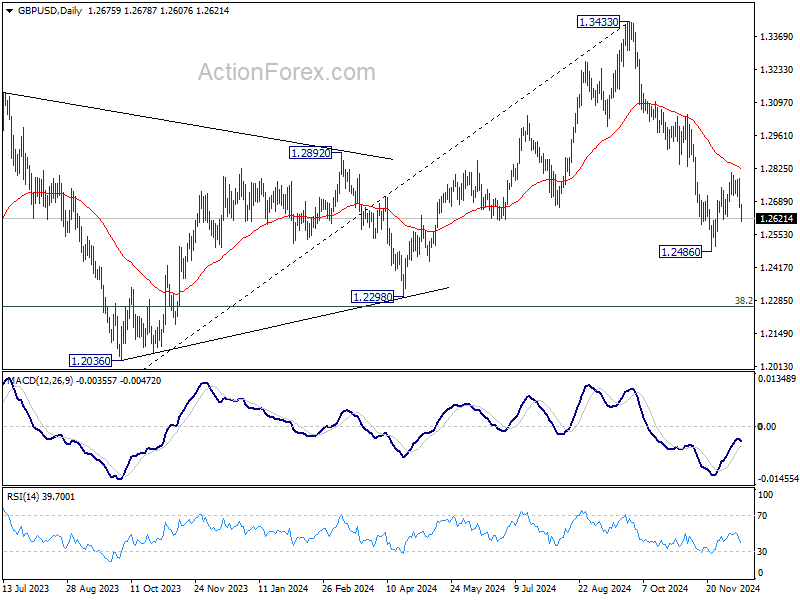

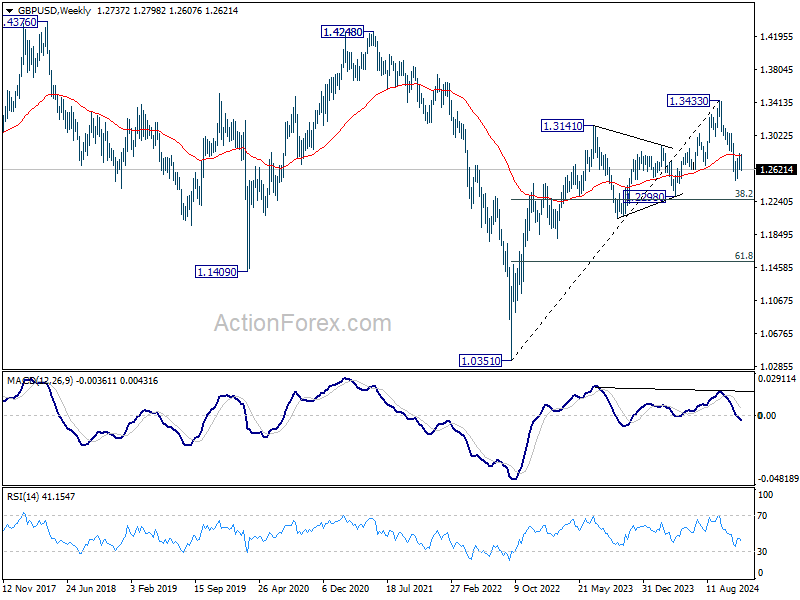

GBP/USD Weekly Outlook

GBP/USD's decline last week suggests that corrective recovery from 1.2486 might have completed at 1.2810 already. Break of 1.2615 should affirm this case, and bring deeper decline through 1.2486 to resume the whole fall from 1.3433. Next target will be 1.2298 cluster support zone.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

In the long term picture, as long as 1.2298 support holds, rise from 1.0351 long term bottom is expected to continue. But in any case, outlook is neutral at best as long as 1.4248 structural resistance holds.

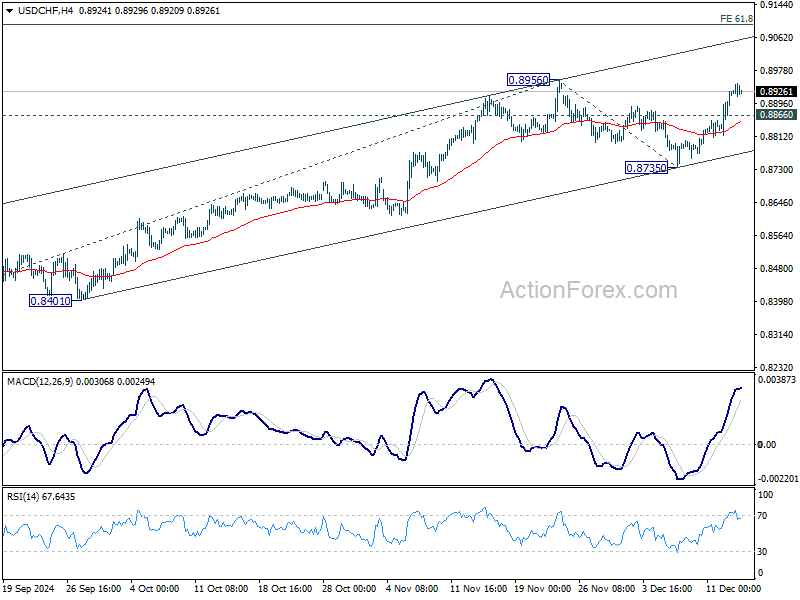

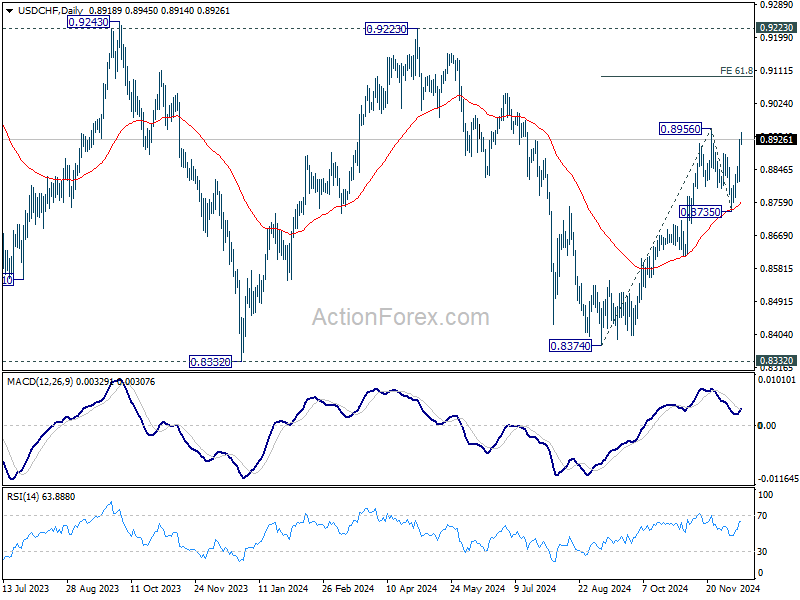

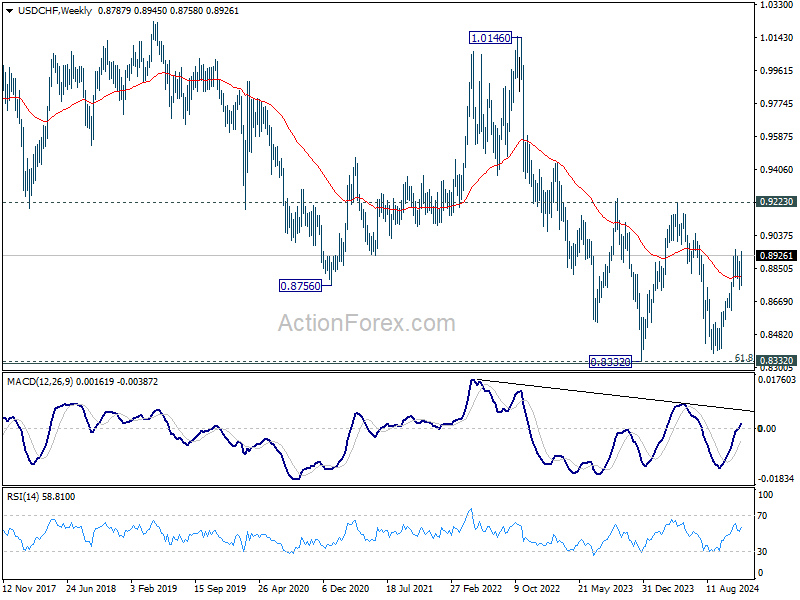

USD/CHF Weekly Outlook

USD/CHF's strong rebound last week suggests that correction from 0.8956 has already completed at 0.8735, and rise from 0.8374 is ready to resume. Initial bias stays on the upside this week. Break of 0.8956 will confirm this bullish case and target 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095. On the downside, below 0.8866 minor support will delay the bullish case and bring more consolidations first.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

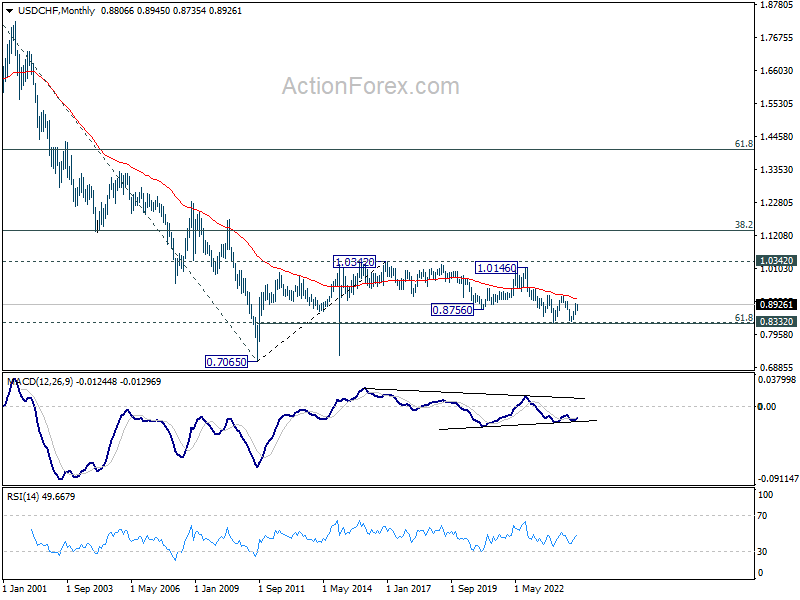

In the long term picture, price action from 0.7065 (2011 low ) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). Fall from 1.0342 (2016 high) is seen as the second leg. Rejection by 55 M EMA suggest that this fall is in progress. Break of 61.8% retracement of 0.7065 to 1.0342 at 0.8317 will pave the way back to 0.7065.

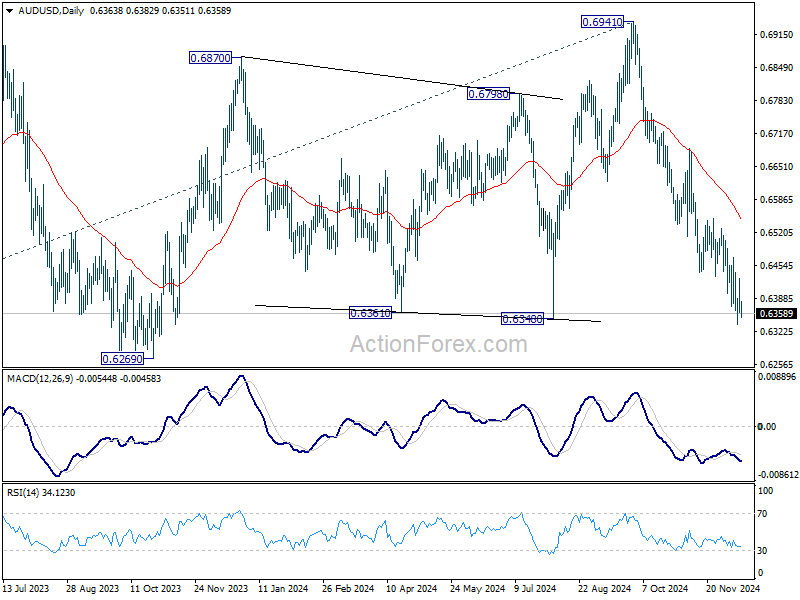

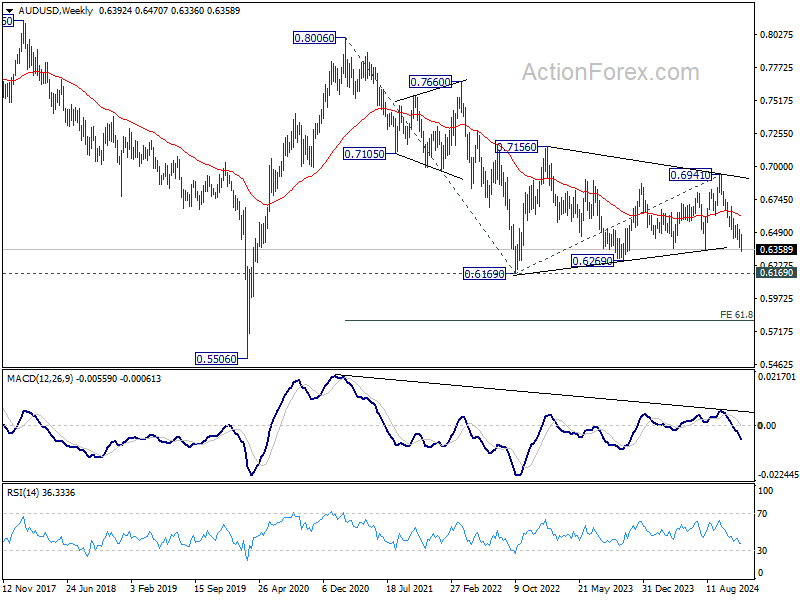

AUD/USD Weekly Report

AUD/USD edged lower last week but turned sideway after hitting 0.6336. Initial bias stays neutral this week for more consolidations. While another recovery cannot be ruled out, outlook will stay bearish as long as 55 D EMA (now at 0.6546) holds. Below 0.6336 will resume the fall from 0.6941 to 0.6269 support next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. More sideway trading could be seen above 0.6169, but overall outlook will stay bearish as long as 0.6941 resistance holds. Firm break of 0.6169 will resume the down trend to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next.

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen as the second leg of the pattern. Hence, even in case of deeper fall, strong support should emerge above 0.5506 to contain downside to bring reversal.

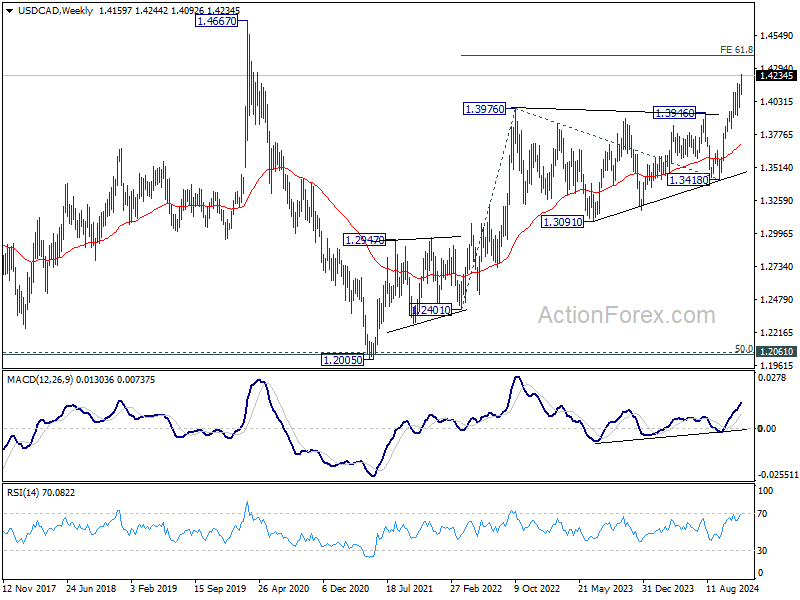

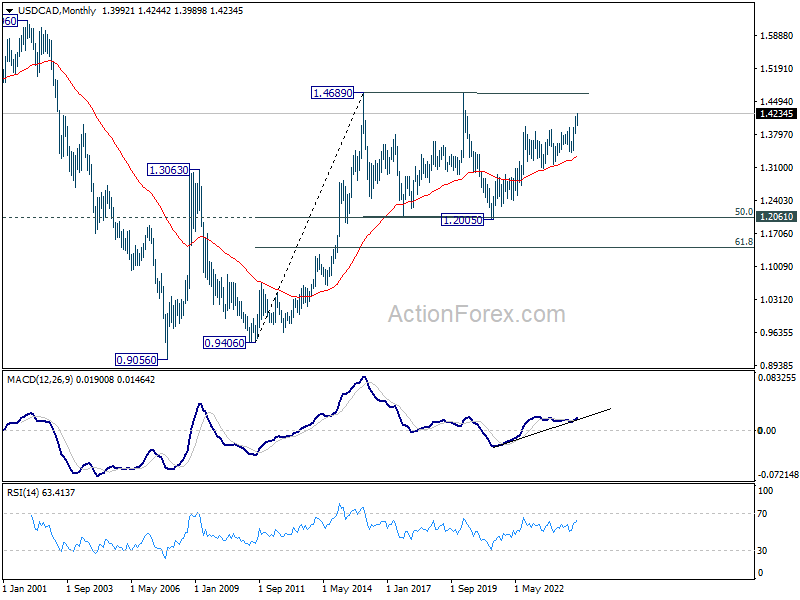

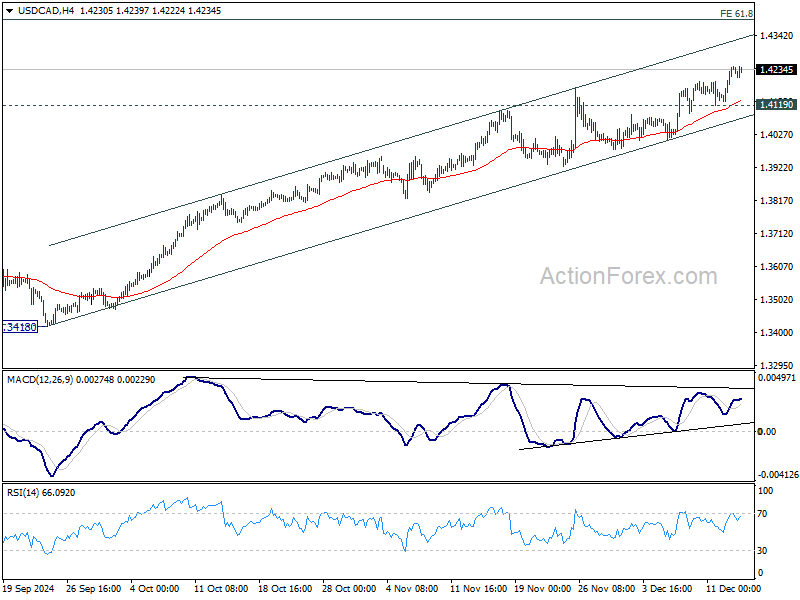

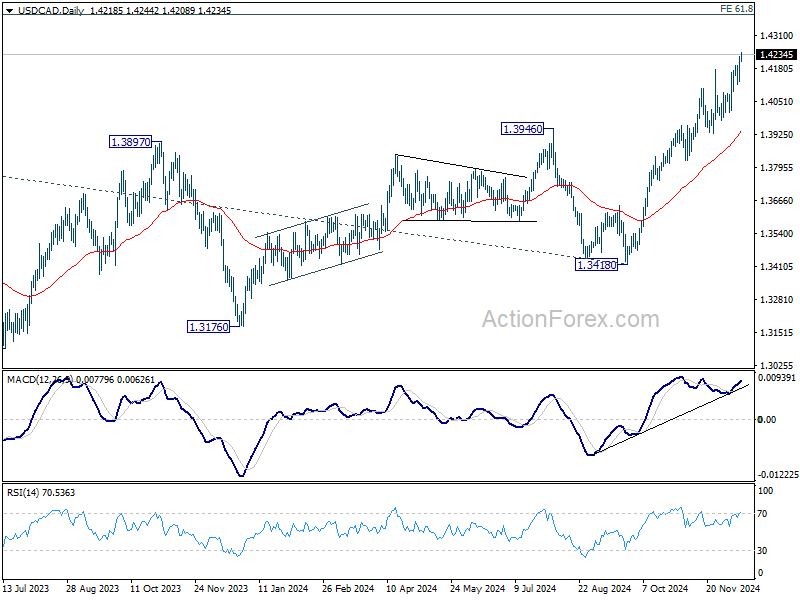

USD/CAD Weekly Outlook

USD/CAD's up trend continued last week and there is no sign of topping. Initial bias stays on the upside this week for 1.4391 projection level next. Considering bearish divergence condition in 4H MACD, break of 1.4119 support will indicate short term topping and bring correction.

In the bigger picture, up trend from 1.2005 (2021) is in progress. Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Medium term outlook will remain bullish as long as 55 W EMA (now at 1.3706) holds, even in case of deep pullback.

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.3418 support holds.