Sample Category Title

Trade Idea Update: USD/CHF – Hold long entered at 0.9700

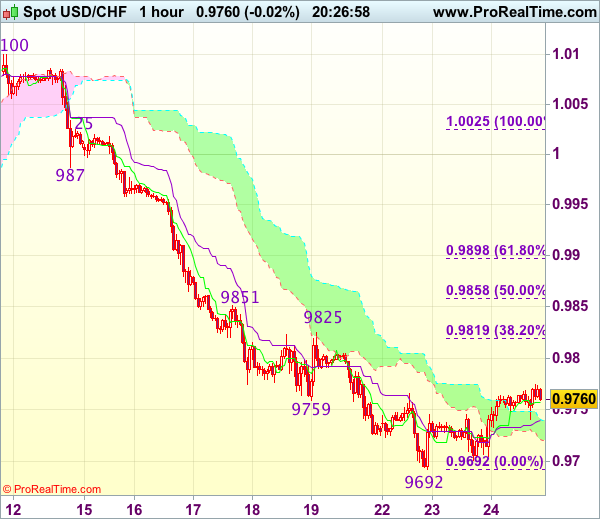

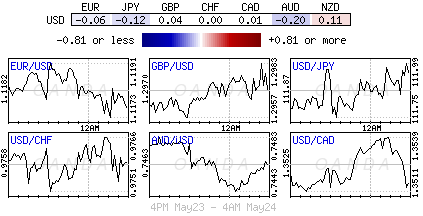

USD/CHF - 0.9756

Original strategy :

Bought at 0.9700, Target: 0.9800, Stop: 0.9700

Position : - Long at 0.9700

Target : - 0.9800

Stop : - 0.9700

New strategy :

Hold long entered at 0.9700, Target: 0.9800, Stop: 0.9700

Position : - Long at 0.9700

Target : - 0.9800

Stop : - 0.9700

As the greenback has rebounded after holding above this week’s low at 0.9692, retaining our view that further consolidation above this level would be seen and mild upside bias remains for another rebound to 0.9790-00, however, break of resistance at 0.9825 is needed to low is formed, bring retracement of recent decline to previous resistance at 0.9851 which is likely to hold from here.

In view of this, we are holding on to our long position entered at 0.9700. Below said support at 0.9692 would signal recent decline has resumed and extend weakness to 0.9670-75 but reckon downside would be limited to 0.9650 and 0.9620-25 should hold, bring another rebound later.

Trade Idea Update: GBP/USD – Stand aside

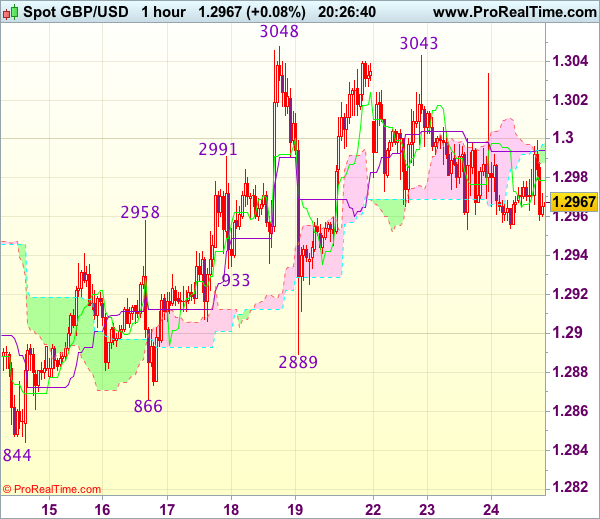

GBP/USD - 1.2965

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Cable’s retreat after faltering below indicated resistance at 1.3048 (last week’s high) has retained our view that further choppy trading below this level would be seen and pullback to 1.2950 cannot be ruled out, however, reckon downside would be limited to 1.2920-25 and said support at 1.2889 should remain intact, bring another rebound later.

On the upside, although recovery to 1.3000-10 cannot be ruled out, reckon said resistance at 1.3048 would hold, bring further consolidation. Only a break of said resistance at 1.3048 would confirm recent upmove has resumed an extend further gain to 1.3075-80 and possibly towards 1.3100-10 later. As near term outlook is mixed, would be prudent to stand aside in the meantime.

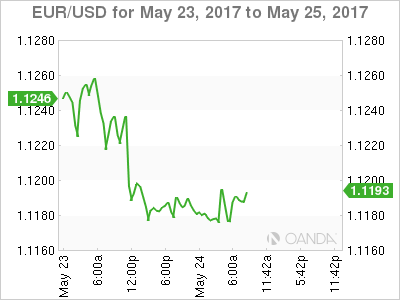

Trade Idea Update: EUR/USD – Stand aside

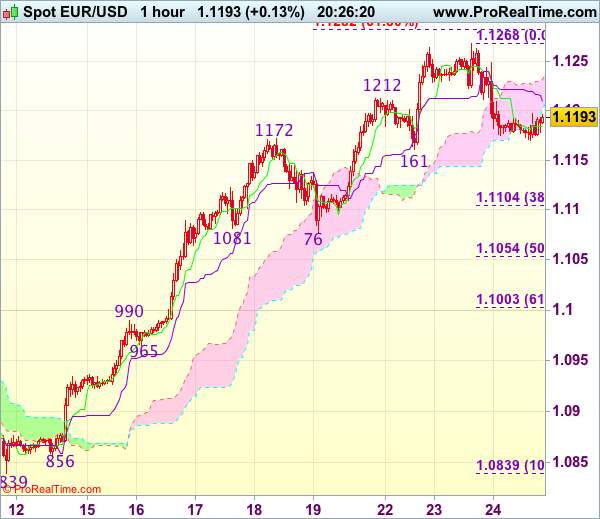

EUR/USD - 1.1197

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s marginal rise to 1.1268, the subsequent retreat suggests a temporary top is possibly formed and test of support at 1.1161 cannot be ruled out, however, break there is needed to add credence to this view, bring further fall to 1.1130 but reckon downside would be limited to 1.1100-05 (38.2% Fibonacci retracement of 1.0839-1.1268) and price should stay well above support at 1.1076, bring rebound later.

On the upside, whilst recovery to 1.1200 cannot be ruled out, reckon the Kijun-Sen (now at 1.1220) would limit upside and 1.1250 should hold, bring retreat later. Only break of said resistance at 1.1268 would extend recent upmove to extend further gain to 1.1280-85 (61.8% projection of 1.0839-1.1172 measuring from 1.1076) and possibly towards 1.1300-10.

Trade Idea : USD/JPY – Sell at 112.40 or buy at 111.50

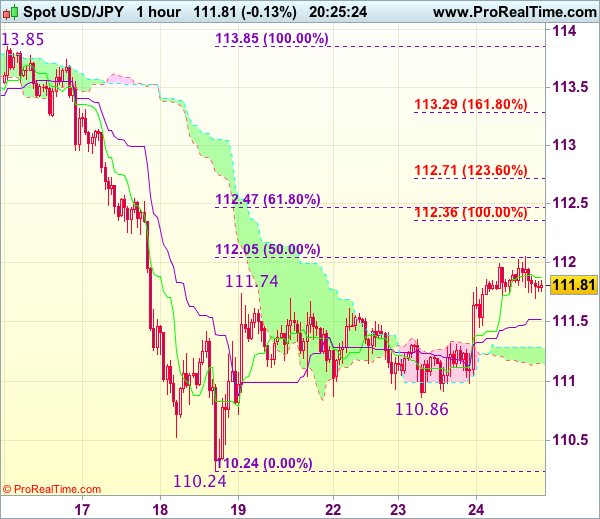

USD/JPY - 111.81

Original strategy :

Sell at 112.40, Target: 111.00, Stop: 112.75

Position : -

Target : -

Stop : -

New strategy :

Sell at 112.40, Target: 111.00, Stop: 112.75

O.C.O.

Buy at 111.50, Target: 112.50, Stop: 111.15

Position : -

Target : -

Stop : -

The greenback has rebounded after holding above support at 110.86, suggesting near term upside risk remains for the corrective rise from 110.24 low to extend gain to 112.05 (50% Fibonacci retracement of 113.85-110.24), then 112.36 (100% projection of 110.4-11174 measuring from 110.86) but upside should be limited to 112.45-50 (61.8% Fibonacci retracement) and bring another decline later, below 111.30-35 would bring test of said support at 110.86 but break there is needed to signal the rebound from 110.24 has ended, bring further fall to 110.50 first.

In view of this, whilst we are still looking to sell dollar on further recovery, we would turn long on dips as the Kijun-Sen (now at 111.50) should limit downside and bring another rebound. Above 112.70-75 would abort and signal recent decline has ended, bring further gain to 113.00.

Fed Focus Trumps Moody’s China Downgrade

Wednesday May 24: Five things the markets are talking about

It's been a busy overnight session for capital markets.

Global equities are mixed after China's sovereign credit rating is downgraded by Moody's (see below). The fallout has the AUD dollar being the worst performing G10 currency as the downgrade has spilled into a much weaker Dalian iron ore price, so the result is a softer Aussie (A$0.7456).

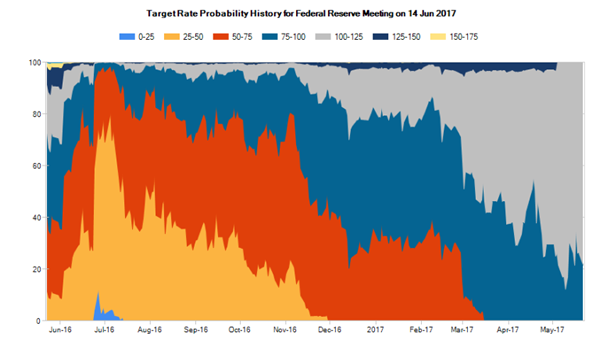

The 'mighty' USD and bond yields are steady, with fixed income dealers more confident that the Fed will raise U.S interest rates next month (June 13-14), while oil has rallied for a sixth consecutive day in anticipation of an OPEC-led output cut may be extended to the Q1 of 2018.

Note: OPEC officially meets in Vienna tomorrow, however, informal meeting are taking place today.

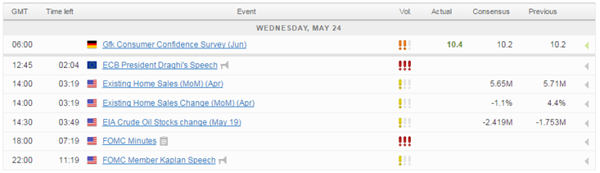

The markets focus is switching to today's FOMC minutes – even though inflation has been softer and other U.S economic data on the weak side, the minutes of the Fed's last meeting, will be released at 2 p.m. EST today, are expected to point to another rate hike in June.

Investors will also be looking for any new information about the Fed's plans to shrink its balance sheet.

Expect the Fed to emphasize that the economy remains on pretty solid footing, highlighting continued improvement in the labor markets, solid consumer confidence data, mostly positive data on housing along with some signs of improvement in the manufacturing sector.

Offsetting the positives, the FOMC may point to continued uncertainty in Washington, and modest gains in wages.

1. Equities produce mixed results

In Japan, the Nikkei share average (+0.7%) rallied to a one-week closing high helped by exporters after the USD gained against the yen (¥111.93), while financials outperformed as U.S Treasury yields backed up. The broader Topix index increased +0.6%.

Down-under, despite China's downgrade, Australia's S&P/ASX 200 Index rose +0.2%, while South Korea's Kospi index advanced +0.2%.

In China, the Shanghai Composite rose +0.1%, reversing an earlier drop of -1.3%. The Hang Seng slipped less than -0.1%.

In Europe, indices are trading mostly lower across the board with the exception of the FTSE 100 helped by strength of some Q1 earnings reports.

U.S stocks are set to open little changed (+0.1%).

Indices: Stoxx50 -0.1% at 3593, FTSE +0.2% at 7498, DAX -0.1% at 12643, CAC-40 flat at 5347, IBEX-35 flat at 10916, FTSE MIB -0.2% at 21363, SMI -0.1% at 9055, S&P 500 Futures +0.1%

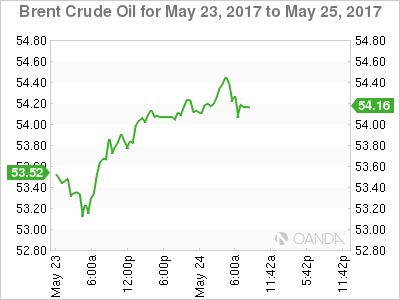

2. Oil prices rise as market awaits extended output cut

Oil prices have climbed in recent sessions on expectations that OPEC will extend their current production deal for a minimum of six months, to maybe nine months.

Ahead of the U.S open, Brent crude oil is up +40c a barrel at +$54.55, while U.S light crude (WTI) is up +35c at +$51.82.

Note: Both crude benchmarks have gained more than +10% from this months lows below +$50 a barrel, rebounding on a consensus that OPEC and other producers will maintain strict limits on oil production in an attempt to drain a global oversupply.

OPEC has promised to cut supplies by 1.8 million bpd until the end of June and is expected tomorrow to decide to prolong that cut to March 2018.

Crude bears are not expecting much of a price rally from current price levels. They point to U.S 'frackers' who are suddenly profitable again to increase production and there is an upside risk of U.S President Trump to take a fairly hard line on Iran by imposing sanctions.

Gold (+$1,250.52 per ounce) is holding steady ahead of the U.S open, after slipping in Tuesday's session. Investors await cues on the U.S Fed's rate hike stance from today's minutes. Higher interest rates tend to boost the dollar and push bond yields up, putting pressure on gold prices.

Nickel has slumped -1.7% and copper -0.6% after Moody's Investors Service cut China's sovereign credit rating for the first time since 1989.

3. Yields under pressure to back up from supply and data

In Europe, government bond yields are higher as improving consumer sentiment in Germany is viewed as the latest evidence that a brightening economy may encourage the ECB to wind back ultra-easy monetary policy. German 10-year Bund yields have climbed +2 bps to +0.43%. Also, a sale of 10-year Bunds is also adding upward pressure to yields.

Note: Euro data shows that German consumer morale is the highest in nearly 16 years.

In the U.S, despite there being a +$34B five-year note sale today and +$28B sale of seven-year notes tomorrow, the shape of the yield curve will take its cues from today's FOMC minutes. The market will focus on clues about the pace of interest-rate increases as well as discussions about how to wind down the Fed's balance sheet.

Currently, fed funds show a +79% chance that the Fed would raise short-term interest rates at its June 13-14 meeting – the odds was at +74% on Friday and +51% a month ago.

The yield on U.S 10's is holding at +2.28%, while Aussie 10-year yields have backed up +4 bps to +2.48%.

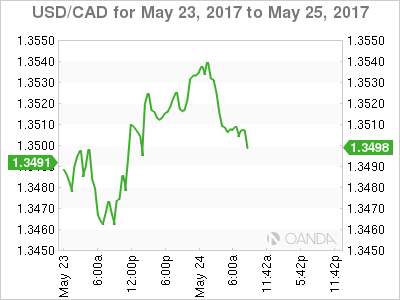

Note: The Bank of Canada (BoC) releases its monetary policy decision at 10 am EST – no change (+0.5%) is expected (C$1.3502).

4. Dollar contained until Fed minutes

The USD is steady in quiet trading as investors/dealers wait for the Fed minutes to see if the language could help to support the greenback.

The EUR/USD (€1.1179) continues to hover just under the psychological €1.12 handle. Many expect the 'single' unit pullbacks to be brief and shallow. The 'bulls' believe the EUR is in the process of going higher – the prospect of the ECB announcing a path to more tapering of its asset-purchase program at the June ECB meeting, improving eurozone economic activity, and rising eurozone capital inflows is expected to support the currency towards €1.1275.

The pound (£1.2972) is still within striking distance of testing the alleged option barriers at £1.3050. To many, £1.3000 is considered the key pivot and with any momentum through theses levels expect the structural shorts out there post-Brexit will be looking to wind back. Short-term sterling bulls are now targeting £1.3350/1.3400.

USD/JPY (¥111.79) probed the ¥112 area overnight, supported mostly by U.S Treasury yield backing up. JPY is also under pressure after Japan's Upper House approved government's two nominees for the BoJ board. The nominees would replace current dissenters of Kuroda's QQE policy.

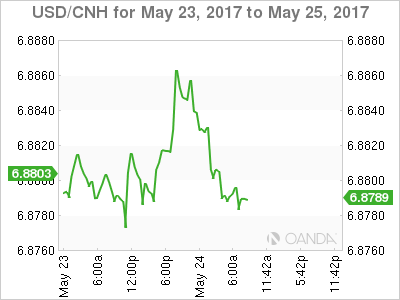

5. Moody's cuts China sovereign rating for the first time in 28-years

Overnight, Moody's Investor Service cuts China's sovereign rating from AA3 to A1 (one notch) and revised its outlook from negative to stable.

The rating agency noted that "China's financial strength will erode over the coming years, with economy-wide debt continuing to rise as potential growth slows", though the "stable outlook reflects our assessment that, at the A1 rating level, risks are balanced."

Moody's also forecast leverage across the China economy to increase in coming years and reform to slow, as sustained policy stimulus will lead to higher debt.

Note: China Finance Ministry responded that the assessment overestimated economic difficulties and underestimates ability to deepen supply side reform, maintaining that debt levels will be reasonable and government reform will help curb local debt risks.

Market Update – European Session: German Confidence At Highest Level Since Oct 2001, Focus On Fed Minutes

Notes/Observations

German GFK Confidence hits fresh 16-year high

Focus shifts from US politics to Fed minutes for clues on rate policy

Overnight:

Asia:

Moody's cuts China's sovereign rating from AA3 to A1 (one notch); revised outlook from negative to stable (**Note: 1st cut by first Moody's since 1989). Expectation that China's financial strength would erode somewhat over the coming years, with economy-wide debt continuing to rise as potential growth slows.

Japan Upper House approved government's two nominees for BoJ board (matter now goes to the lower house for confirmation). Nominees are Goushi Kataoka (economist at MUFJ Research and Consulting) and Hitoshi Suzuki (director for Bank of Tokyo-MUFJ) and would replace Kiuchi and Sato (both dissenters) when their respective 5 year terms end of July 23rd

Europe:

PM May: will temporarily increase terror threat level from severe to critical in UK following attack in Manchester; level increase suggests "further attack may be imminent" - ECB's Coeure (France) reiterated view that European growth was pretty strong; but no need to change policy exit sequencing at this time

Americas:

Fed's Harker (hawk, FOMC voter): reiterates support for two more rate hikes this year. June rate hike is a "distinct possibility" but downside inflation surprise could delay a move - Canada Foreign Min Freeland: NAFTA talks must be trilateral

Energy:

Weekly API Oil Inventories: Crude: -1.5M v +0.9M prior

UAE Oil Min: delegates still debating whether cut extension will be 6 months or 9 months

Oman Energy Undersecretary: Oman wants some discussion before supporting a 9-month OPEC extension, but not opposed to the idea

Algeria Oil Min Boutarfa: not ruling out deeper oil production cuts or maintaining the cuts longer than 9 months

Norway Q2 Oil Investment Survey raised 2017 exploration spending from NOK18.4B to NOK21.6B

Economic Data

(DE) Germany Apr Jun GfK Consumer Confidence: 10.4 v 10.2e (highest level since 2001)

(NO) Norway Mar AKU Unemployment Rate: 4.5% v 4.3%e

(FI) Finland Apr Unemployment Rate: 10.2% v 9.6% prior

(SE) Sweden May Consumer Confidence: 105.9 v 104.0e; Manufacturing Confidence: 117.0 v 121.0e, Economic Tendency Survey: 111.0 v 111.6e

(CZ) Czech May Business Confidence: 13.9 v 14.3 prior; Consumer Confidence: 6.0 v 6.0 prior

(TH) Thailand Central Bank (BOT) left its Benchmark Interest Rate unchanged at 1.50% (as expected)

(ZA) South Africa Apr CPI M/M: 0.1% v 0.3%e; Y/Y: 5.3% v 5.6%e (annual pace moved back within SARB target range for 1st time in 7 months)

(ZA) South Africa Apr CPI Core M/M: 0.2% v 0.3%e; Y/Y: 4.8% v 4.9%e

Fixed Income Issuance:

(IN) India sold total INR140B vs. INR140B indicated in 3-month and 12-month Bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 -0.1% at 3593, FTSE +0.2% at 7498, DAX -0.1% at 12643, CAC-40 flat at 5347, IBEX-35 flat at 10916, FTSE MIB -0.2% at 21363, SMI -0.1% at 9055, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes

European indices trade mostly lower across the board with the exception of the FTSE 100 helped by strength in Dixons Carphone following strong LFL sales numbers for the 4th quarter, and Marks and Spencer which reported Adj pretax ahead of consensus but down on the year. However shares of B&Q parent Kingfisher trades lower by over 6% after LFL sales fell for the quarter. Elsewhere in Europe shares of Safran and Zodiac are halted pending an announcement after earlier Safran was exploring options to lower Zodiac offer. Looking head to the US morning, notable earners include Lowe's, Advanced Autoparts and Chico Fas.

Equities

Consumer discretionary [Dixons Carphone [DC.UK] +4.2% (Q4 update), Kingfisher [KGF.UK] -6.2% (Earnings), Marks and Spencer [MKS.UK] +1.0% (Earnings) , Fiat Chrysler [FCA.IT] -0.8% (DOJ investigation)]

Materials: [Glencore [GLEN.UK] -1% (Makes informal takeover approach to Bunge)]

Industrials: [Babcock International [BAB.UK] -2.2% (Earnings), Vedanta Res [VED.UK] -1.5% (Earnings)]

Technology: [Sunrise Communications [SRCG.CH] +1.5% (Sells Towers to consortium, Raises dividend outlook)]

Energy: [Shell [RDSA.NL] +0.3% (Sells stake in Canadian Natrual Resources for C$4B)]

Speakers

ECB Financial Stability Report: Risks in the euro zone are contained but remain significant and have even increased in some areas over the past six months. Concerns over debt sustainability had risen, while the clean up of the banking sector was slow and the risk of a sudden repricing in bond markets remained significant, potentially leading to major capital losses. Repricing risks in fixed income markets remained significant, There were risks that euro area bond yields could increase abruptly without a simultaneous improvement in growth prospects

ECB's Praet (Belgium, chief economist) reiterated that economic recovery was becoming more solid and braid-based but underlying inflation remained subdued. June ECB meeting to draw on the latest information and have new projections and updated assessment of risks surrounding the economic outlook

ECB's Constancio (Portugal): Faster economic growth was good for financial stability. Must be cautious about premature withdrawal of stimulus; would rather err on side of removing stimulus too late than too early

France President Macron to ask Parliament to extend the current State of emergency and prepare new security measures

Sweden Central Bank (Riksbank) Financial Stability Report: Housing prices and household indebtedness are foremost risks and serious threat to stability. Measures were needed to increase household resilience. Higher leverage ratio of over 5% might be appropriate for major Swedish banks from Jan 2018. Necessary that Riksbank has sufficiently large FX reserves if liquidity requirement arose

China state planner NDRC: Chinese companies overall debt risks seen as controllable

Thailand Central Bank Policy Statement noted that decision to keep policy steady was again unanimous as current rate remained accommodative for economy. It reiterated that was ready to use appropriate policy mix. Economic outlook has improved but still subject to risks. Reiterated that THB currency (Baht) moving in-line with regional currencies

Japan Cabinet Office (Govt) Monthly Economic Report for May: reiterated view that domestic economy was continuing a moderate recovery although with a delay in some areas (**Note: 6th month of unchanged assessment)

IEA Head of Oil Atkinson: Almost certain there will be an extension on oil cuts in Vienna at the May 25th OPEC meeting. Saw oil demand rising to 1.3M bpd in 2017 and reiterated its view that if oil producers stay the course, the market would rebalance

Kuwait Oil Min Almarzooq stated that he saw market rebalancing by Q3

Iran Oil Min Zanganeh: OPEC ceiling will continue just not clear on duration of the extension of production cuts

Algeria Oil Min: Almost all countries agree on a 9-month extension of oil cuts

Currencies

USD steady in quiet trading on Wed. Dealers were awaiting the upcoming Federal Reserve minutes later today to see if the language could help to support the greenback.

EUR/USD hovered around just under the 1.12 in the session and consolidated its recent gains. Price action by the market may have become too enthusiastic in speculating about interest rates rising. Dealers has noted that the improved sentiment and growth outlook supported equity inflows in the Euro Area. The EUR was further aided by recent commentary by the German Fin Min Schauble and Chancellor Merkel noting that the EUR was too low for Germany.

GBP/USD still within striking distance of testing alleged option barriers at 1.3050.

USD/JPY probed the 112 area for the early part of the session. Dealers noted that US Treasury yield was supporting the pair (yield climbed several bps overnight). JPY currency also softer after Japan's Upper House approved government's two nominees for BoJ board. The nominees would replace current dissenters of Kuroda's QQE policy

Fixed Income

Bund futures trade at 160.93 up 24 ticks, trading in the middle of last week's trading range. Resistance lies near the April 27th high of 162.01 level followed by 163.68. A break of 160.01 support level could see lows target 159.01 followed by 157.50.

Gilt futures trade at 128.54 higher by 13 ticks and approaching last week's high of 128.95. Last week's rally respected both the 129.00 handle and the 129.14 April 18th high. Price is now tentatively above the 128.51 level and finds key support at the 127.52 support level. An acceleration lower could test the 126.74 region. Resistance stands at 129.14 followed by 132.80.

Wednesday's liquidity report showed Tuesday's excess liquidity rose to €1.6272T a slight gain of €0.2B from €1.6720T prior. Use of the marginal lending facility fell to €130M from €212M prior.

Corporate issuance saw over $13.1B come to market via 8 issues headlined by JP Morgan $3B in an 2-part deal consisting of 4-year non-call 3-year FRN and a 7.75-year non-call 6.75year fixed-to-floating note and Canadian Natural Resources $3B in a 3-part senior unsecured note offering

Looking Ahead

(CO) Colombia Apr Industrial Confidence: No est v -0.9 prior; Retail Confidence: No est v 18.6 prior

(BR) Brazil May FGV Consumer Confidence: No est v 82.2 prior

05:30 (DE) Germany to sell €3.0B in 0.25% 2027 bunds

06:00 (RU) Russia to sell combined RUB45B in 2019 and 2026 OFZ bonds

06:00 (EU) EU's Dombrovskis with Moscovici on Greece

06:30 (EU) EU Foreign Min Mogherini in Brussels

06:45 (US) Daily Libor Fixing

07:00 (EU) EU's Tusk and Juncker with NATO Sec Gen Stoltenberg in Brussels

07:00 (US) MBA Mortgage Applications w/e May 19th: No est v -4.1% prior

07:30 (CL) Chile Central Bank's Traders Survey - 08:15 (UK) Baltic Dry Bulk Index

08:45 (EU) ECB's Draghi in Madrid

09:00 (US) Mar FHFA House Price Index M/M: 0.5%e v 0.8% prior; Q/Q: No est v 1.5% prior

09:00 (BE) Belgium May Business Confidence: -0.5e v -0.8 prior

09:00 (BR) Brazil Apr Total Federal Debt (BRL): No est v 3.234T prior

09:00 (CL) Chile Apr PPI M/M: No est v 0.7% prior

10:00 (US) Apr Existing Home Sales: 5.65Me v 5.71M prior

10:00 (CA) Bank of Canada (BOC) Interest Rate Decision: Expected to leave Interest Rates unchanged at 0.50%

10:30 (US) Weekly DOE Crude Oil Inventories

11:30 (US) Treasury to sell 2-Year Floating Rate Notes Reopening

13:00 (US) Treasury to sell 5-Year Notes

14:00 (US) FOMC Minutes from May 3rd Meeting

18:00 (US) Fed's Kaplan (voter) in Toronto

18:30 (US) Fed's Kashkari (dissenter)

June Hike All But Priced In Ahead of FOMC Minutes

We're expecting a relatively flat open on Wall Street on Wednesday, as traders await the minutes from the FOMC meeting earlier this month having already strongly priced in a rate hike in June, with a second in December looking less certain.

Traders Convinced By June But What About December?

While the dollar's performance in recent months would suggest otherwise, traders have become increasingly convinced that we'll see a rate hike in June, the second this year, but questions are being asked about where the Fed will go from there. A lot of the expectation in the final couple of months of the year came from the expectation that President Donald Trump would announce huge spending and tax reform plans but as of yet, that's not happened.

The result is that the rally in both equity markets and the dollar have stalled, with other currencies making up ground as central banks elsewhere turn a little less dovish. The S&P and the Dow on the other hand have been range bound over the last few months and have failed each time they've tested their highs. While the Dow remains a little off its highs, the S&P appears to be eyeing another test having rebounded convincingly following last Wednesday's tumble.

Oil Climbs Ahead of Inventory Data on Anticipation of Output Extension

Brent and WTI crude are both trading in the green once again today and are headed for a sixth consecutive day of gains as we await the latest oil inventory data from EIA and the decision on whether there'll be an extension, and possible increase, to the output cut that came into effect this year. The rally in recent weeks would certainly suggest traders have bought into it already, leaving oil WTI and Brent very vulnerable to the downside should participating members fail to come to an agreement. With Saudi Arabia and Russia appearing on board though, the chance of a deal not materializing seems slim. The bigger question is whether they'll live up to market expectations. Another small reduction in inventories is expected to be reported today, in line with what API reported on Tuesday.

China Downgrade Shrugged Off by Markets

Markets have largely shrugged off Moody's downgrade of China's credit rating overnight, with even Chinese stocks and the yuan being relatively unfazed. We saw some initial weakness in Chinese stocks and the currency immediately following the announcement but both quickly reversed the moves to trade positive on the day. This sentiment has been shared by investors elsewhere who have also shrugged off the downgrade, with the possible surprise factor being offset by the fact that concerns about Chinese debt and growth are not exactly new.

While the FOMC minutes will likely attract the most attention today, we'll also get existing home sales data from the US and hear from a couple of Fed officials, with Robert Kaplan and Neel Kashkari both due to appear for the second time this week.

FTSE Rallied After Completing Elliott Wave FLAT

In this technical blog, we are going to take a look at the performance of past Elliott wave FTSE charts from April 2017, which we presented to the clients at elliottwave-forecast.com. Now lets take a look at the 4 hr chart from April 20,2017, which is showing the intermediate cycle in wave (A) in blue unfolded on March 17,2017 peak 7448, below from there intermediate pullback in wave (B) in blue was proposed be in progress as Elliott wave Flat structure. Where Minor wave A in red unfolded in 3 swings (labelled as W,X,Y structure) at 7251 and wave B in red also unfolded in 3 swings (labelled as W,X,Y structure) at 7404 peak. Below from there Minor wave C in red of a flat remained in progress and already showing the enough number of swings within the buying area from the peak. However another marginal push lower was expected within the blue box area (7100-7027) area to complete there as 5 waves structure.

FTSE 4 hour chart

Then we got the nice reaction higher from the mentioned blue box area as expected thus suggesting the intermediate cycle in wave (X) pullback should be completed as Flat structure at 7098 low and allowing our members at elliottwave-forecast,com to create a risk free position in the trade. Also the bounce from 7098 low looks to be unfolding as continuation pattern i.e. Elliott wave Zigzag pattern, where index was expected to trade higher towards 7403-7452 equal legs area of ((a))-((b)) next as far as pivot from 7098 low remains intact.

1 Hour FTSE Elliott Wave Chart

Since then index rallied as expected & has broken above the March 17,2017 peak 7448 already thus suggesting the next leg higher has already started. Index then did a full retest of 1.618% extension area of ((a))-((b)) 7530 before ending the cycle from 7098 low in Minor wave 1 and started the pullback in Minor wave 2 that should expected to find buyer’s against 7098 low in sequence of 3, 7 or 11 swings for further upside.

1 Hour FTSE Elliott Wave Chart

The index already did a 3 swings pullback in Minor wave 2, so the correction of cycle from 7098 low could be done in the index at yesterday’s low 7389, while above there and more importantly as far as pivot from 7098 low remains intact index has scope to resume the rally again.

FTSE Latest 1 Hour Chart

DAX Steady As German Consumer Confidence Remains High

The DAX index has inched lower in the Wednesday session. Currently, the DAX is trading at 12,641.00 points. On the release front, German Consumer Climate improved to 10.4, beating the estimate of 10.2 points. The ECB released its semi-annual Financial Stability Review, which was generally positive. Later in the day, ECB President Mario Draghi will speak at an event in Madrid. German Consumer Climate improved to 10.4, beating the estimate of 10.2 points. The ECB released its semi-annual Financial Stability Review, which was generally positive. Later in the day, ECB President Mario Draghi will speak at an event in Madrid. In the US, today's highlight is the Federal Reserve minutes from the May policy meeting

The Federal Reserve raised rates back in March, and the markets are expecting the Fed to press the rate trigger again in June. The odds of a rate hike have increased to 83%, according to the CME Group. Just last week, the likelihood of a rate increase stood at 73%. Despite the market speculation, Fed policymakers are keeping their cards close to their chest, at least in their public appearances. On Tuesday, Philadelphia Fed President Patrick Harker said that a June move was a 'distinct possibility', but cautioned that a weak inflation report could delay a rate hike. Earlier in the week, Robert Kaplan, President of the Dallas Fed, stated that three interest increases in 2017 was 'appropriate'. The Fed minutes are expected to underscore support for a June move, but may not shed much light on what happens after that. Still any clues about the Fed's rate plans could shake up the listless EUR/USD.

With President Trump out of town on his first overseas visit, the White House presented Trump's 2018 budget proposal to lawmakers in Congress. Trump is eager to pick up the axe and slash government spending, and the budget proposes major cuts to the Medicaid health program, disability benefits and food stamps. Trump has outlined an ambitious program to cut government spending by $3.6 trillion in the next 10 years and achieving a balanced budget by 2020. The budget includes $25 billion for paid leave after childbirth and some $200 billion for infrastructure programs. Trump's budget will face tough opposition on Capitol Hill, with both Democrats and Republicans likely to demand changes. Still, with the Trump administration beset by Congressional investigations, the White House can point to the budget as a step forward in his agenda to slash government spending.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD was corrected lower yesterday bottomed at 1.1175. The bias is bearish in nearest term. Price broke below a trend line support as you can see on my H1 chart below suggests a potential bearish pullback especially if price able to make a clear break below 1.1175 testing the H1 EMA 200 located around 1.1110 but overall I remain bullish and any downside pullback should be seen as a good opportunity to buy. Immediate resistance is seen around 1.1210. A clear break above that area could lead price to neutral zone in nearest term testing 1.1265 area which need to be clearly broken to the upside to continue the bullish scenario targeting 1.1300 – 1.1350 area.

GBPUSD

The GBPUSD attempted to push higher yesterday topped at 1.3033 but closed lower at 1.2960. The bias remains neutral in nearest term probably with a little bearish bias testing the trend line support and 1.2925/00 support area as you can see on my H1 chart below, which is a good place to buy with a tight stop loss. Immediate resistance is seen around 1.2985. A clear break above that area could trigger further bullish pressure testing 1.3050 key resistance which needs to be clearly broken to the upside to continue the bullish scenario testing 1.3185 area.

USDJPY

The USDJPY attempted to push lower yesterday bottomed at 110.86 but whipsawed to the upside and closed higher at 111.78 and hit 111.99 earlier today in Asian session. The bias is bullish in nearest term testing the trend line resistance and 112.00 area as you can see on my H4 chart below, which remains a good place to sell with a tight stop loss targeting 108.00 region. Immediate support is seen around 111.50. A clear break below that area could lead price to neutral zone in nearest term testing 111.00 or lower. On the upside, a clear break and daily close above 112.00 and the trend line resistance would activate my wait and see mode as direction would become unclear.

USDCHF

The USDCHF attempted to push lower yesterday bottomed at 0.9701 but whipsawed to the upside and closed at 0.9760. The bias is bullish in nearest term testing 0.9815 which is a good place to sell with a tight stop loss targeting 0.9650 as a part of the false breakout bearish scenario as you can see on my H4 chart below. Immediate support is seen around 0.9730. A clear break below that area could lead price to neutral zone in nearest term testing 0.9650 area.