Sample Category Title

Trade Idea Wrap-up: EUR/USD – Stand aside

EUR/USD - 1.1244

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1213

Kijun-Sen level : 1.1213

Ichimoku cloud top : 1.1145

Ichimoku cloud bottom : 1.1137

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the single currency has surged again after brief pullback to 1.1161 and initial upside bias remains for recent upmove to extend gain to 1.1260-65, reckon upside would be limited to 1.1280-85 (61.8% projection of 1.0839-1.1172 measuring from 1.1076) and loss of near term upward momentum should limit upside to 1.1300-10, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below the Kijun-Sen (now at 1.1206) would bring pullback towards said support at 1.1161 but break there is needed to signal top is formed, bring retracement of recent rise to 1.1125-30 first.

Trade Idea Wrap-up: USD/JPY – Sell at 112.05

USD/JPY - 111.10

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.26

Kijun-Sen level : 111.27

Ichimoku cloud top : 111.36

Ichimoku cloud bottom : 111.29

Original strategy :

Sell at 112.05, Target: 110.85, Stop: 112.40

Position : -

Target : -

Stop : -

New strategy :

Sell at 112.05, Target: 110.85, Stop: 112.40

Position : -

Target : -

Stop : -

As the greenback found support at 110.24 last week and rebounded, retaining our view that further consolidation above this level would be seen and corrective bounce to 112.00-05 (50% Fibonacci retracement of 113.85-110.24) cannot be ruled out, however, reckon upside would be limited and bring another decline later, below 110.70-75 would suggest the rebound from 110.24 has ended, bring retest of this level first.

In view of this, would be prudent to sell dollar on further subsequent recovery as 112.05-10 should limit upside and bring another decline. Above 112.35-40 would defer and signal low is formed instead, risk a stronger rebound to 112.65-70.

CAC Unchanged Ahead of Eurozone, French Manufacturing PMIs

It's a quiet start to the week for European stock markets, and the France CAC 30 is almost unchanged. In the North American session, the CAD is trading at 5329.90. There are French or Eurorozone economic releases on the schedule. On Tuesday, we'll get a look at eurozone and French Manufacturing and Services PMIs.

The continuing political crisis in Washington weighed on global stock markets. The CAC dropped 1.4% last week, as nervous investors have dumped US-denominated assets, boosting the euro, the Japanese yen and gold. Will the downward spiral in the stock markets continue? Much will depend on whether the beleaguered Trump administration can regain its footing after a week to forget. Trump's administration was rocked by reports that he had asked former FBI director James Comey to end an investigation into connections between Russia and the Trump campaign team during the US election. If these accusations are true, Trump could be charged with committing obstruction of justice. Trump is no doubt delighted to have left town as he wings through the Middle East and Europe, to warm receptions everywhere he goes. With Democrats smelling a bona fide scandal and the noxious term of "impeachment" being thrown around, Trump may face a chilly reception in Congress when he returns from his trip abroad.

EU finance ministers are meeting on Monday, with debt relief for Greece a key issue on the agenda. Greece has undergone a severe austerity plan and understandably, the Greek government is reluctant to adopt further painful measures. However, Greece could be headed on a collision course with the EU, if the latter insists that the further reforms are needed. German Finance Minister Wolfgang Schaeuble praised the reforms implemented by Greece as "remarkable", but insisted that Greece must take further steps before the EU provides further financial aid. Greek's debt woes once resulted in the country almost leaving the eurozone, and if the EU holds up debt relief, European stock markets could drop sharply.

Trade Idea: EUR/GBP – Target met and stand aside

EUR/GBP - 0.8639

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Bought at 0.8530, met target at 0.8630

Position : - Long at 0.8530

Target : - 0.8630

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the single currency has surged again after finding renewed buying interest at 0.8524 last week, adding credence to our bullishness and our long position entered at 0.8530 met our upside target at 0.8630 (with 100 points profit), having said that, as this move from 0.8312 low is viewed as retracement of recent decline, reckon upside would be limited to 0.8670 and price should falter below 0.8700, risk from there is seen for a retreat later.

As we have taken profit on our long position entered at 0.8530, would not chase this rise here and would be prudent to stand aside for now. Below 0.8595-00 would bring pullback to 0.8565-70 but break there is needed to signal top is possibly formed, bring subsequent test of said support at 0.8524, once this level is penetrated, this would provide confirmation.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Hold long entered at 1.3530

USD/CAD - 1.3493

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

Original strategy :

Bought at 1.3530, Target: 1.3730, Stop: 1.3470

Position: - Long at 1.3530

Target: - 1.3730

Stop: - 1.3470

New strategy :

Hold long entered at 1.3530, Target: 1.3730, Stop: 1.3470

Position: - Long at 1.3530

Target: - 1.3730

Stop:- 1.3470

Although the greenback has remained under pressure and marginal weakness from here cannot be ruled out, reckon downside would be limited to 1.3470 and bring rebound, above 1.3540-45 would bring test of 1.3580-85 but break of latter level is needed to signal low is formed, bring subsequent rise to 1.3670, however, only break there would confirm and suggest the the fall from1.3794 has ended, bring further gain to 1.3700 and later towards 1.3740-45.

In view of this, we are holding on to our long position entered at 1.3530. Below 1.3470 would signal the fall from 1.3794 top is still in progress and may extend weakness to previous support at 1.3411, however, loss of downward momentum should previous sharp fall below there today and reckon 1.3370 would remain intact.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

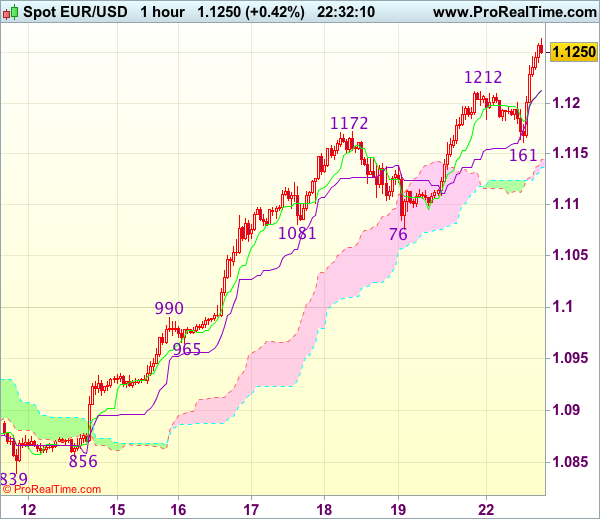

Merkel Comments Push Euro Beyond EUR/USD 1.12

- European equities had a uneventful session, mostly spend in negative territory, but now approaching opening levels.US equities take a strong start, suggesting that a stronger euro is starting to take its toll on EMU equities.

- The euro rose as much as 0.4% to $1.1250 -its highest level since November 9 -having declined as much as 0.4% to $1.1262 earlier in the day. The moves came after Angela Merkel, the German chancellor, told school students in Berlin that "the euro is too weak", which she attributed to European Central Bank policy.

- EU ministers have unanimously agreed to hand the European Commission a tough negotiating mandate for the Brexit talks, pencilling in the start of withdrawal discussions with the UK around June 19.

- Theresa May has dramatically rewritten her controversial "dementia tax" plans, announcing that she will put a cap on total care costs to protect homeowners from the risk of losing nearly all of their assets. The original Tory policy stipulated that people would have to pay all of their care costs – whether at home or in a care home – apart from their last £100,000 of assets.

- Germany and France are considering boosting cooperation between their top companies under an initiative launched last week by chancellor Angela Merkel and president Emmanuel Macron to strengthen bilateral relations and revive the euro area economy.

Modest downward pressure on bonds continues

In a thinly traded, data-poor session, German bonds came under modest selling pressure mid-morning, that accelerated around noon. There was a quote of Merkel that the euro was too cheap and lots of talk of Weidmann replacing Draghi as ECB chief…. in October 2019 when Draghi's term ends. US Treasuries fell slightly in the overnight session to stabilize further out. European equities traded mixed with Italy underperforming, while oil was slightly up around $54/barrel. We shouldn't draw conclusions from today's price action that may have been nothing more than noise. At the time of writing, US yields rise an insignificant 0.8 bps (2-yr) to 1.2 bps (5-10-30-yr). The German yields rise by 0.8 to 3.5 bps, steepening the curve a tad.

The Spanish socialist party elected Mr. Sanchez, a left oriented politician, as their leader. He promised a tough opposition to PM Rajoy's minority government, which might cause problems for Mr. Rajoy further down the road and new elections are not excluded. The socialists abstained to make Rajoy's minority government possible. Spanish equities didn't underperform (contrary to the Italian ones), but the 10-yr yield spread with Germany widened 1 bps while Italy and Portugal saw their spread drop 3 to 4 bps. Greece outperformed (-8 bps) as the Euro group discusses the Greek situation.

Merkel comments push euro beyond EUR/USD 1.12.

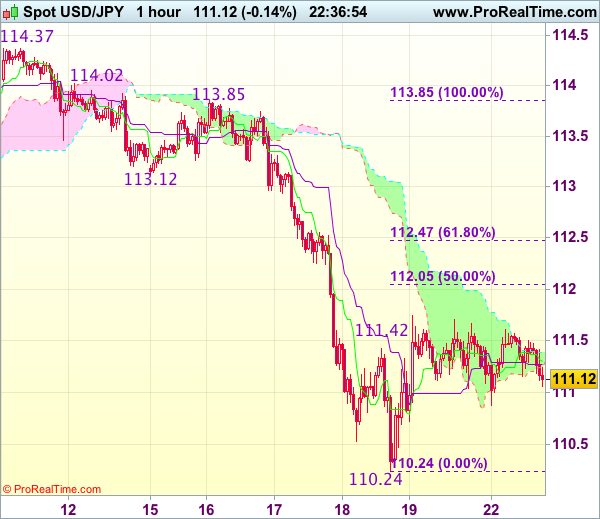

Today, the euro dropped temporary early in Europe, but the dip was short-lived. Later in the session, the euro set new highs after comments from German Chancellor Merkel that the euro is too weak. EUR/USD trades currently in the mid 1.12 area. At the same time, the dollar struggles not to lose ground against other majors. USD/JPY trades in the 111.25/30 area.

Overnight, Asian equities joined Friday's US rebound. A further rise in the oil price supported commodity related assets. The focus turned to the visit of the President Trump to the Middle East, easing market uncertainty. Still the risk-on sentiment didn't help the dollar. EUR/USD held just below 1.12, within reach of Friday's top. USD/JPY gains remained modest and rebounded to about 111.50.

European equities took a uninspiring start and soon reversed opening gains. This hesitant start caused a tempering decline in EUR/JPY, EUR/USD and USD/JPY. Rising political uncertainty in Spain (new socialist leader) maybe provided an excuse for some euro profit taking, but the euro dip was short-lived. Just before noon, the euro (and European yields) jumped higher on comments from German Chancellor Markel. Elaborating on the German trade surplus, she said that the euro was too weak due to ECB monetary policy, making German products cheap. It is a bit 'strange' to see the euro and the German/EMU yields rising in lockstep due to these comments as a strong euro might make it more difficult for the ECB to raise rates. Even so, interest rate differentials between the dollar and the euro narrowed. EUR/USD set a new recovery top just below 1.1250. The euro was maybe also supported by press comments that German Chancellor Merkel will push for Weidnann as ECB president.

The combination of USD weakness and euro strength continued as US traders joined the fray. US equities opened narrowly mixed. EUR/USD (currently 1.1245) is holding within reach of the correction top. USD/JPY also struggles not to drift south. The pair is changing hands in the 111.30 area.

EUR/GBP testing 0.8650 barrier on euro strength

Euro strength is also the dominant factor for EUR/GBP trading. The Merkel comments on a weak euro pushed EUR/GBP further beyond the 0.86 big figure. The pair trades currently near 0.8650. At the same time, sterling also tried to regain ground against an overall weak dollar. The pair returned to the 1.30 area, but Friday's top (1.3040 area) stayed out of reach. Some factors weighed on the UK currency. The lead of the conservative party over labour in the polls for the Parliamentary election is still big, but declining. This causes some unease for sterling. Today, the EU rubberstamped its Brexit negotiation position. The EU still wants an agreement on the UK financial commitments first. The EU starting point suggests a difficult start for the Brexit negotiations. At least for now, this uncertainty weighs more on the sterling than on the euro.

Canadian Dollar Quiet in Thinned Holiday Trade

The Canadian dollar has edged lower in the Monday session. In North American trade, USD/CAD is trading at the 1.35 line. Canadian banks and stock markets are closed for the Victoria Day holiday. In the US, there are no economic releases. We'll hear from four FOMC members, and the markets will be looking for clues as to the Fed's plans with regard to future rate hikes. On Tuesday, Canada releases Wholesale Sales and the US will publish New Home Sales.

There are no economic numbers out of Canada or the US on Monday, so the markets will have a chance to focus on the Federal Reserve, with four FOMC members delivering speeches. The Fed has been keeping the markets guessing in recent weeks regarding a rate hike. The central bank is expected to announce a rate hike at its June 14 meeting, but the odds of a hike have shown strong volatility. In late April, a rate hike was priced in at just 50%. The odds jumped higher in May but continue to show movement. Currently, the markets have priced in a hike at 78%, up from 73% on Friday. If the likelihood of a June move continue to fluctuate, the US dollar could also show some movement, as a rate hike will make US-dollar assets more attractive to investors.

The Canadian dollar enjoyed strong gains last week, as the currency climbed 1.4%. Although Canadian consumer numbers were lukewarm last week, the Canadian dollar was buoyed by rising oil prices, as Brent crude soared 4.7% last week. However, investors are nervous about the ongoing political turmoil in Washington, and that could spell trouble for minor currencies like the Canadian dollar. President Trump must have been happy to head to the Middle East and Europe, as last week was perhaps his most difficult since taking office. Trump's administration was rocked by reports that he had asked former FBI director James Comey to end an investigation into connections between Russia and the Trump campaign team during the US election. If these claims are true, Trump could be charged with committing obstruction of justice. President Trump fired back last week, angrily denouncing this move as a "witch hunt". With Washington preoccupied with Trump's alleged connections with Russia, Trump's administration could find itself immersed with damage control, rather than moving ahead with its agenda of tax reform and increased fiscal spending.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9694; (P) 0.9749; (R1) 0.9778; More.....

USD/CHF's fall extends to as low as 0.9694 so far today. Intraday bias remains on the downside. Current decline from 1.0342 should target 100% projection of 1.0342 to 0.9860 from 1.0099 at 0.9617. We'll start to look for bottoming signal again below there. On the upside, above 0.9765 minor resistance will turn intraday bias neutral again and bring consolidations first, before staging another fall.

In the bigger picture, USD/CHF is bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level.

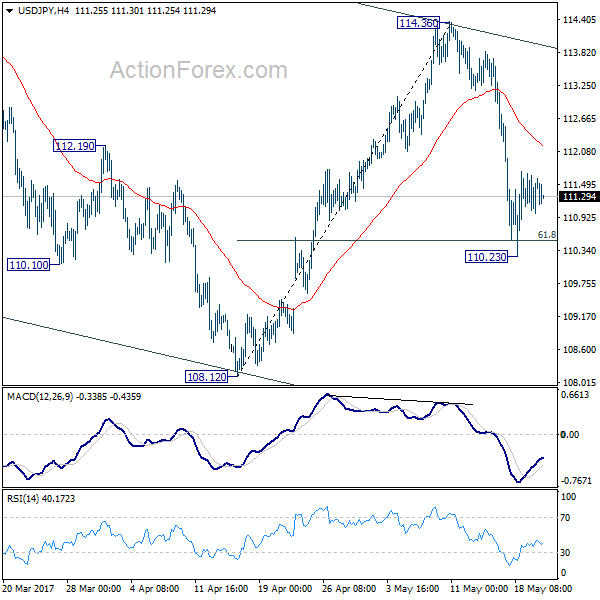

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.95; (P) 111.32; (R1) 111.62; More...

USD/JPY is staying in range above 110.23 and intraday bias remains neutral for the moment. Overall, the development suggests that whole corrective decline from 118.65 is going to extend lower. Below 110.23 turn bias back to the downside and send USD/JPY through 108.12 low. In that case, we'll look for bottoming signal again at 61.8% retracement of 98.97 to 118.65 at 106.48.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

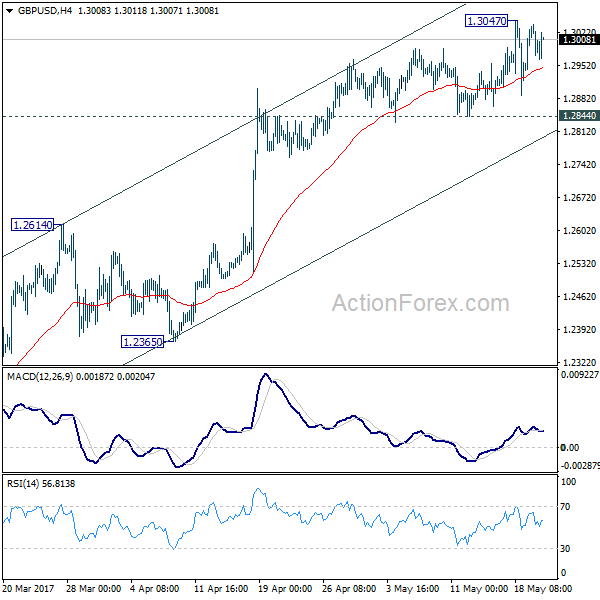

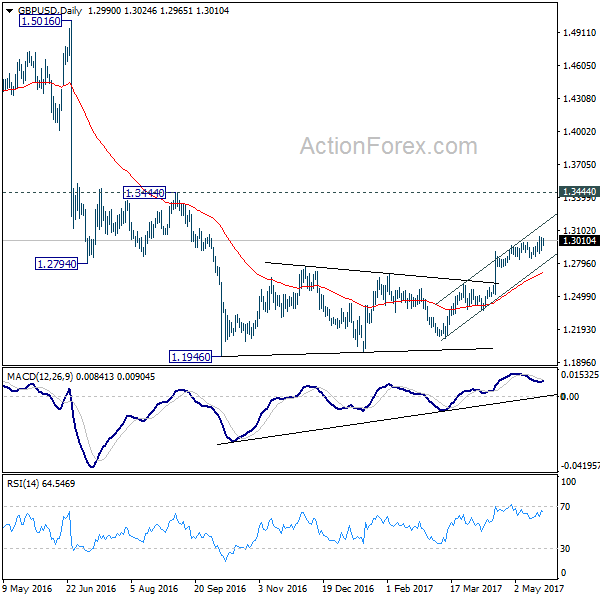

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2952; (P) 1.2995; (R1) 1.3075; More...

GBP/USD is still staying in tight range below 1.3047 and intraday bias remains neutral. With 1.2844 minor support intact, further rise remains mildly in favor. Nonetheless, as we are still viewing price actions from 1.1946 as a corrective move, we'd expect upside to be limited below 1.3444 resistance to bring near term reversal. On the downside, break of 1.2844 will indicate short term topping and turn bias back to the downside for 1.2614 resistance turned support first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There are signs of reversal, like breaking of 55 week EMA, weekly MACD turned positive, and monthly MACD crossed above signal line. But still, break of 1.3444 resistance is need to confirm medium term bottoming. Otherwise, outlook will remains bearish for extend the down trend through 1.1946 low.