Sample Category Title

Technical Outlook: Cable – UK Jobs Data Eyed For Fresh Signals

Cable is trading within 1.2900/40 range in early Wednesday's trading after failing to capitalize stronger on Monday's upbeat UK inflation data. The pair spiked to 1.2955 but was unable to sustain gains, closing at 1.2914 (the second daily close below cracked 10SMA pivot). The action remains underpinned by rising 20SMA (currently at 1.2890) and may be dragged higher by fresh strength of the Euro. Bullish technicals are supportive for another attempt at psychological 1.3000 barrier, however, gains may be limited as falling thick weekly cloud heavily weighs on the market. Repeated rejections under 1.3000 pivot and extension below 20SMA would weaken bullish structure and risk retest of lower pivots at 1.2840/30 zone. Sterling is eyeing today's UK jobs data for fresh signals. Unemployment rate is expected to stay unchanged at 4.7% in March, but forecast for Apr jobless claims and average earnings are very good (7.5K f/c vs 25.5K in Mar and 2.4% f/c for Apr vs 2.3% in Mar respectively) and could further support pound on forecasted or better releases.

Res: 1.2940, 1.2955, 1.2986, 1.3000

Sup: 1.2904, 1.2890, 1.2864, 1.2843

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

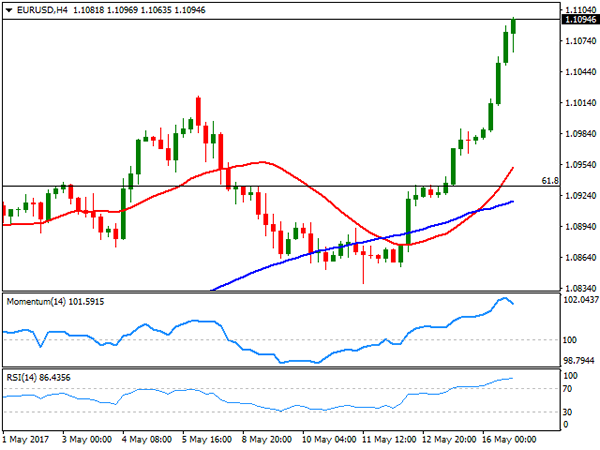

EUR/USD

EUR/USD's rally extended to fresh 2017 highs this Tuesday, fueled intraday by another batch of soft US data and the scandal surrounding US President Trump, involving classified information being unveiled to Russian diplomats. The news came after Trump fired FBI's director, James Comey, on the back of Russia supposed involvement in the latest election, fueling political unrest in the world's largest economy. Greenback's slide was uneven across the board, yet that the currency is being dropped by investors, is undeniable.

Macroeconomic data released at both shores of the Atlantic backed the rally, as in the EU, preliminary Q1 GDP matched expectations, with economic growth advancing 0.5% in the three months to March, whilst German ZEW survey showed that local business confidence continued to improve in May, although less than market's forecast. The index rose to 20.6 from 19.5 points in the previous month, missing expectations of a rise to 22.0. In the US, housing data surprised to the downside, with building permits down to 1.229M from previous 1.26M, and housing starts also down in April, accounting for 1.172M vs. previous 1.203M. Industrial output, however, improved, up in April by 1.0%, the fastest rate in more than three years.

From a technical point of view, the pair has reached extreme overbought conditions in the short term, but with the price pressuring the daily high, betting on a decline seems too risky. In the 4 hours chart, technical indicators have barely retreated from extreme readings, with the RSI indicator standing at 85, whilst the price accelerated further beyond a bullish 20 SMA. The rally could meet some profit taking on an initial approach to the 1.1100 figure, yet further gains can be expected, as long as the pair holds now above the 1.1000 critical figure.

Support levels: 1.1045 1.1000 1.0965

Resistance levels: 1.1130 1.1180 1.1220

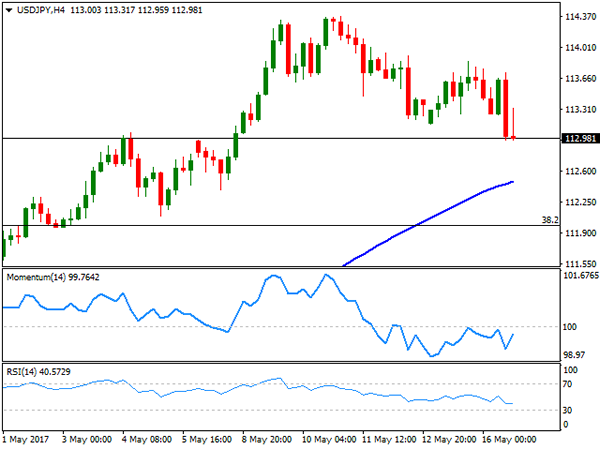

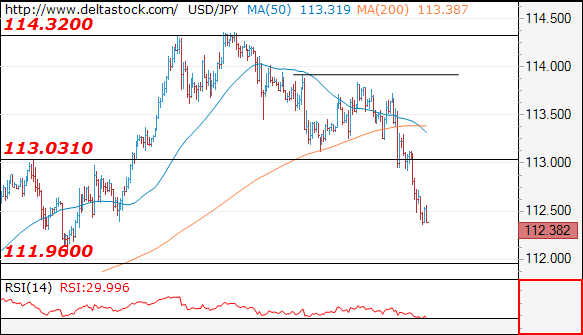

USD/JPY

The USD/JPY pair fell to a fresh 2-week low of 112.96, undermined in the US afternoon by a decline in US yields, which remain a driving force for the safe-haven currency. Treasury yields have been stable for most of the week, but fell in the latest hour following an auction. The 10-year benchmark now stands at 2.33%, down from previous 2.34%, while the 30-year yield retreated to 2.99% from 3.01%. Comments from BOJ's Governor Kuroda confident stance on withdrawing stimulus in the future, is also yen supportive, as the Central Bank's leader said earlier today that he is "quite sure" that they can smoothly exit monetary stimulus when the time comes. Entering the Asian session barely holding around 113.00, the pair has an immediate support around 112.50, where in the 4 hours chart stands a bullish 100 SMA, followed by 112.00, the 38.2% retracement of the November/December rally. In the same chart, the RSI indicator aims higher within negative territory, but the RSI indicator anticipates some further declines, heading south around 40.

Support levels: 113.20 112.75 112.40

Resistance levels: 114.00 114.50 114.85

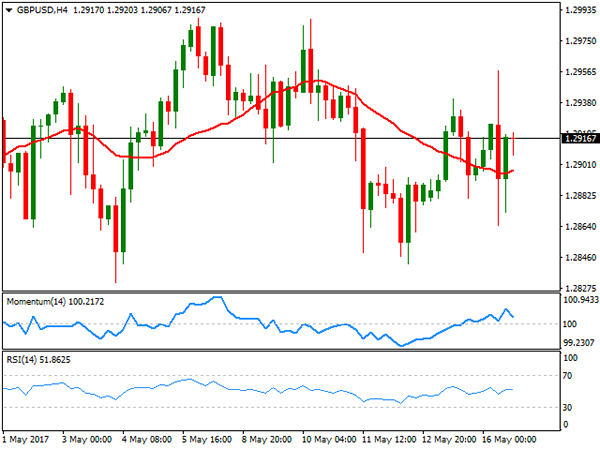

GBP/USD

The British Pound failed to gather momentum from higher-than-expected April inflation figures, ending the day anyway with modest gains at 1.2917. UK inflation surpassed market's consensus in beyond, printing a whopping 2.7% yearly basis, above the 2.6% expected and previous 2.3%. When compared to the previous month, inflation advanced 0.5%, surpassing the 0.4% forecast. Producer prices inflation was also higher than expected, with factory output prices up by 0.5% in the same month, and by 3.6% yearly basis, matching previous month's figures, but above the 3.4% expected. Higher inflation usually means that the BOE would be a step closer to rising rates, triggering a rally in the GBP, but uncertainty surrounding the Brexit and the upcoming elections maintained investors side-lined this time. The pair has traded as high as 1.2957 and as low as 1.2865, with the daily candle presenting a limited body, a sign of the uncertainty surrounding the pair. Short term, the pair retains the neutral stance seen on previous updates, as in the 4 hours chart, technical indicators keep hovering around their mid-lines with no certain directional strength, whilst the price settled a few pips above a modestly bearish 20 SMA.

Support levels: 1.2900 1.2865 1.2830

Resistance levels: 1.2960 1.2995 1.3040

GOLD

Stop gold settled at $1,237.50 a troy ounce, extending its weekly advance by a few cents as the greenback remains in sell mode, while market's mood remains high. The bright metal has posted a limited recovery ever since bottoming at a two-month low of 1,214.24 earlier this month, as odds for a US rate hike next June limit chances of a steeper advance. From a technical point of view, the pair has pared its advance right below a horizontal 100 DMA, but advanced above its 200 DMA for the first time in over a week, while it remains below a strongly bearish 20 DMA, this last at 1,243.30. Technical indicators in the mentioned time frame remain within negative territory, with the RSI heading higher around 45, but the Momentum showing no certain directional strength. In the 4 hours chart, a positive tone prevails, with the price above a bullish 20 SMA, and indicators presenting a neutral-to-bullish stance within positive territory.

Support levels: 1,233.20 1.226.60 1,214.25

Resistance levels: 1,243.30 1,251.30 1,262.10

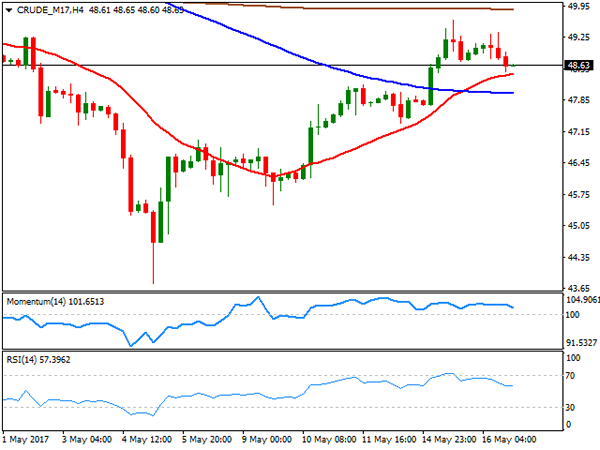

WTI CRUDE OIL

Crude oil prices retreated this Tuesday, with West Texas Intermediate crude futures settling at $48.63 a troy ounce. Despite broad dollar's weakness, the commodity was unable to extend its upward momentum, as investors turned cautious ahead of the weekly US stockpiles release. Inventories are expected to have decreased by around 2.3 million barrels in the week ended May 12th. The API report to be released at the beginning of the Asian session, may hint what the EIA will bring later on the day. From a technical point of view, the daily cart shows that the price remained within the higher end of Monday's range and above a modestly bearish 20 DMA, but also that technical indicators have lost their upward momentum and turned flat within neutral territory. Shorter term and according to the 4 hours chart, technical indicators have eased within positive territory, with the price resting a few cents above a bullish 20 SMA, providing an immediate support at 48.45.

Support levels: 48.45 47.30 46.60

Resistance levels: 48.95 49.60 50.10

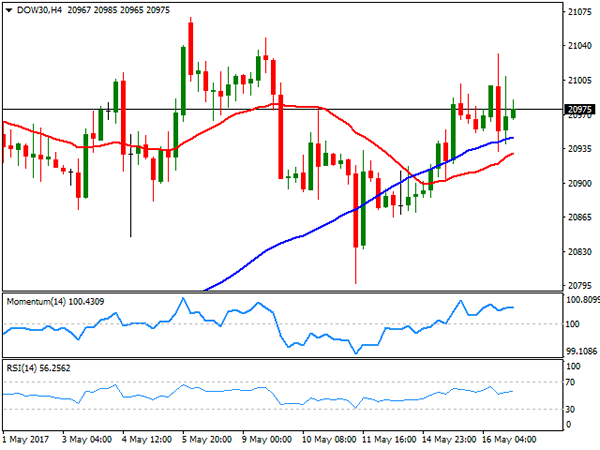

DJIA

Wall Street closed mixed, with the Nasdaq Composite ending the day 20 points higher at 6,169.87, but the Dow and the S&P trimming all of its daily gains ahead of the close, both ending the day with marginal losses. The DJIA shed 2 points, to 20,979.68, while the S&P lost 0.07% and ended at 2,400.67. Techs were the best performers, with Microsoft leading winners' list within the Dow, up 2.01% and followed by IBM which added 1.43%. UnitedHealth Group was the worst performer, down 1.99% while Nike shed 1.84%. From a technical point of view, the index maintains a neutral stance, as investors stand clueless on political woes, although confident on a brighter future. In the daily chart, technical indicators stand pat around their mid-lines, whilst the index barely ended a couple of points above a modestly bullish 20 DMA. In the 4 hours chart, the technical picture is neutral-to-bullish as indicators hold flat within positive territory, whilst intraday declines were contained by a bullish 100 SMA, currently at 20,945.

Support levels: 20,865 20,822 20,797

Resistance levels: 20,900 20,941 20,977

FTSE100

The FTSE 100 rallied to fresh record highs, adding 68 points at the end of the day to settle at 7,522.03. Advancing mining-related equities alongside with a soft Pound, supported once again the advance in the Footsie. Vodafone was the best performer after the telecoms group raised its forecasts for profits for the coming year, posting a 3.96% intraday gain. Fresnillo followed through with a 2.90% advance, whilst Rio Tinto added 2.68%. Hargreaves Lansdown plunged 8.50% leading losers list after competitor Vanguard announced plans to launch an online service to sell its funds directly to UK investors, spurring concerns over an upcoming price war. EasyJet followed, down by 7.25% after reporting a £212 million loss for the first half of its financial year. The index holds around the mentioned close early Asia, and the daily chart shows that the RSI indicator maintains its upward slope at 71, while the Momentum indicator resumed its advance after a modest downward correction, indicating that further gains are likely, despite a downward corrective move can't be dismissed. In the 4 hours chart, technical indicators are also biased higher within extreme overbought territory, as the 20 SMA keeps advancing far above the larger ones and below the current level.

Support levels: 7,508 7,465 7,410

Resistance levels: 7,535 7,570 7,600

DAX

European equities closed mixed around their opening levels, with the German DAX pretty much unchanged, down 2 points to 12,979.53, weighed by a decline in the automotive sector. In Germany, confidence remained strong, but the positive sentiment has grown at a slower-than-expected pace, denting local sentiment, alongside with a non-motivating EU Q1 GDP. Only nine components managed to advance, with ThyssenKrupp adding 4.03%, followed by Deutsche Telekom that gained 1.08%. The worst performer was Linde, down 1.22% followed by BASF that closed -1.09%. The index closed the day with a small doji, having held within the upper end of Monday's range, overall retaining the positive stance, as in the daily chart, the RSI indicator continues consolidating in overbought levels, whilst the Momentum indicator turned flat above its 100 line as moving averages keep advancing well below the current level. In the 4 hours chart, a modest positive tone is present, as indicators bounced from their mid-lines, while the index holds above its 20 SMA.

Support levels: 12,801 12,755 12,718

Resistance levels: 12,839 12,870 12,920

Technical Outlook: The Euro Broke Above 1.1100 On Political Turmoil In The US

The Euro surged above 1.1100 barrier during Asian session on Wednesday, extending strong rally on Tuesday when the single currency was up nearly 1% against the dollar in the biggest one-day rally since 03 Mar. The greenback fell sharply against the basket of major currencies on Tuesday, driven by report that President Trump shared sensitive information with Russia at last week's meeting. The latest political turmoil in the US comes a week after President Trump dismissed his FBI Chief and deepened after news that came out overnight showed that President Trump asked then FBI Director to end a probe into Trump's former national security advisor. The reports significantly weakened confidence in implementation of US president's plan for aggressive stimulus program that had been focused since Trump stepped in the White House. Raising questions over whether Trump's latest actions could be seen as obstruction of justice and may trigger charges against Trump put the US dollar under strong pressure. The EURUSD pair extends strong rally in the fourth straight day, taking out important resistances at 1.1000/20 (psychological barrier/former high of 07 May), as fresh acceleration higher emerged above weekly cloud and broke above 1.1100 (round-figure barrier). The pair is focusing at next pivotal barrier at 1.1127 (Fibo 61.8% of 1.1614/1.0339 descend), break of which is needed to generate another strong bullish signal. Fresh bullish sentiment on political turmoil in the US is reinforced by bullish technical studies, seeing scope for further upside action which may extend towards 1.1300 zone (09 Nov 2016 spike high). Meantime, corrective easing could be anticipated on overbought slow stochastic on daily chart, which so far did not show signs of turning lower. Broken weekly cloud top now acts as good support at 1.1067 with extended dips expected to remain above former key barriers, now supports at 1.1020/00.

Res: 1.1127, 1.1201, 1.1250, 1.1300

Sup: 1.1078, 1.1067, 1.1020, 1.1000

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

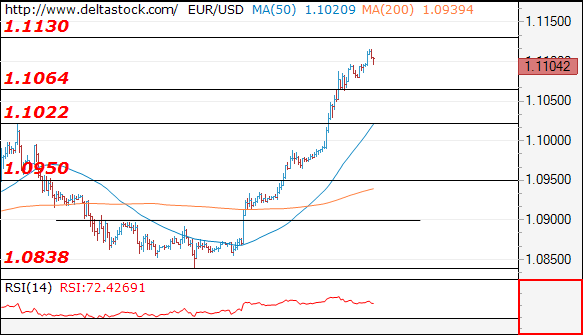

Current level - 1.1104

The uptrend is still intact, heading for a test of 1.1130 resistance area. Initial minor support lies at 1.1094 and crucial on the downside is 1.1064. Only a break through the latter will signal a completion of the whole upmove since 1.0838 low.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1130 | 1.1130 | 1.1094 | 1.1022 |

| 1.1200 | 1.1300 | 1.1022 | 1.0838 |

USD/JPY

Current level - 112.38

The pair did break through 113.00 support and the bias is bearish, for a tight test of 111.90 area. The latter should provide a reliable base for another upswing towards 114.30 peak.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 113.00 | 114.30 | 112.00 | 109.40 |

| 114.30 | 115.60 | 112.00 | 108.12 |

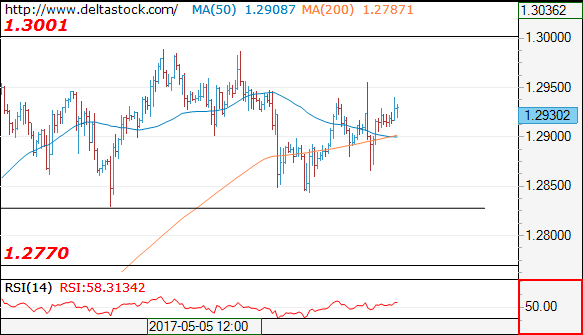

GBP/USD

Current level - 1.2930

Nothing interesting here and the outlook remains absolutely neutral. Only a violation of the range boundaries at 1.3000 and 1.2830 will signal trend dynamics.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2950 | 1.3120 | 1.2830 | 1.2770 |

| 1.3000 | 1.3500 | 1.2770 | 1.2610 |

Currencies: US Political Risk Hammers US Dollar

Sunrise Market Commentary

- Rates: Trump affaire deteriorates risk sentiment

Risk sentiment deteriorated overnight as the Russia-related Trump affaire took on bigger proportions. Safe havens like US Treasuries, gold and JPY gained ground. The absence of eco data suggests that risk sentiment will be today's key driver for trading. A break from the US Note future above 125-26+ would suggest return action to the contract high short term. - Currencies: US political risk hammers US dollar

Yesterday, EUR/USD was propelled both by euro strength and USD softness on recent poor US eco data. A flaring up of political issues in the US is putting additional pressure on the dollar. Especially USD/JPY is vulnerable if risk sentiment deteriorates. The UK labour data are in focus for sterling trading. The UK currency recently lost its positive spin

The Sunrise Headlines

- Wall Street ended unchanged (Dow, S&P) with Nasdaq outperforming (+0.33%), marching to a new record high. Overnight, risk sentiment deteriorated as the latest Trump-scandal escalates.

- President Trump asked then-FBI Director Comey to back off the investigation of former National Security Adviser Flynn shortly after Mr. Flynn had resigned, according to two people close to Mr. Comey.

- Austrian centre-left Chancellor Kern said leaders of the parties in Parliament had agreed on snap elections Oct. 15, a year earlier than scheduled and giving the anti-immigrant Freedom Party a strong chance to enter the government.

- The ECB is not concerned by a recent rise in EMU bond yields as they reflect improved growth prospects, receding fears of deflation, improved inflation expectations and increased risks from outside the bloc, governor Coeure said.

- The US economy is forecast to expand at a 4.1% annualized pace in Q2 according to the latest update of the Atlanta Fed's GDP Now forecast model. Our in-house model currently expects 3.1% Q/Qa growth.

- Australia had its AAA credit rating affirmed by S&P after the government's latest budget projected a return to surplus by 2021.S&P kept a negative outlook, issued in the wake of a knife-edge federal election last July.

- Today's eco calendar is thin with UK labour market data and final EMU CPI figures. Germany sells its 30-yr Bund and Greek parliament is expected to vote on additional reform measures.

Currencies: US Political Risk Hammers US Dollar

US political uncertainty hammers US dollar

On Tuesday, EUR/USD cleared the 1.1023 resistance. The move was due to USD weakness on recent Trump-related issues and on disappointing US data. At the same time, sentiment on the euro remained constructive. EUR/USD closed the session at the 1.1083. The loss of USD/JPY remained modest as US equities remained resilient despite the political noise, at least during the regular hours. USD/JPY finished the day at 113.12.

Overnight, sentiment turned risk-off on headlines that president Trump asked FBI director Comey to stop an investigation against Trump's former national security adviser. The Asian equity losses are modest, but the decline in US equity futures suggests that this case might have more impact than recent ones. The yen plays its safe haven roll. USD/JPY declined to the mid 112 area. Japanese machine orders were weaker than expected, but the focus for yen trading was on US politics. Dollar weakness propelled EUR/USD north of 1.11.

There are no US eco data today. In EMU, only the final HICP inflation report will be released. The impact on FX trading will be limited. The focus for global trading will be on the last flaring up of political turmoil in the US. There were already several 'issues' on Trump that caused high profile press headlines, but until now, the impact on markets was negligible. The jury is still out, but we think that the overnight report of the NYT might be more important than previous incidents. It risk delaying or even aborting the implementation of a coherent policy an tax, deregulation on other issues that are important for markets. US equities were incredibly resilient of late, but this might be the trigger for a more bumpy ride.

On the currency markets, such a scenario should favour the safe havens like the yen and, to a less extent, the Swiss franc. The USD negative sentiment also support more EUR/USD gains. There is no reason to row against EUR/USD uptrend, but a reversal in the EUR/JPY rally might also slow the rebound of EUR/USD. So, even if political tensions in the US deepen, the EUR/USD rally might slow.

Short term assessment

From a technical point of view, the USD/JPY rebound ran into resistance last week. Till yesterday it was not more than a correction on a 6-big figure rally. However, the pair is nearing the previous top/break-up area at 112.20 Return action below this level would indicate that the recent uptrend is aborted and that further return action in the 108.13/114.37 range is possible. We amend our short-term assessment on USD/JPY from positive (buy-on-dips) to neutral with downside risks.

Last week, it looked that EUR/USD could revisit the 1.0821/1.0778 support (gap). However, Friday's US data and political uncertainty finally propelled EUR/USD north of the 1.0821/1.0778 to 1.1023 range. This break improved the technical picture. Next resistance stands at 1.1120 (62% retracement) and at 1.1366 (correction top).

EUR/USD: euro breaks topside of the ST range as US political uncertainty weighs on the dollar

EUR/GBP

EUR/GBP jumps on broad based euro strength

Yesterday, UK April inflation (2.7% Y/Y) and core inflation (2.4% Y/Y) rose more than expected. However, the data didn't help sterling. EUR/GBP pierced the 0.8509/31 resistance after the CPI data. The technical break and broad-based euro strength reinforced EUR/GBP buying. There was probably also an aspect of sterling weakness. A decision of the EU Court of Justice that the free-trade agreement between the EU and Singapore needs approval of the national parliaments, raising the chance that national parliaments will have an important say in the approval of a post-Brexit EU-UK trade deal. EUR/GBP closed the session at 0.8593 (from 0.8510). Cable showed no clear trend and closed the session at 1.2917. However, sterling hardly gaining ground against a struggling dollar is a sign of sterling weakness.

Today, UK labour market data will be published. For now, there is no big impact expected of cooling growth on the labour market. The markets is still a bit more sensitive to negative rather than to a positive news. The wage data are a wildcard. A substantial positive surprise in wages might be slightly supportive for sterling. However, this is not our favoured scenario. Of late, the positive sterling sentiment eased and euro strength prevailed in EUR/GBP trading. For now, we don't row against the EUR/GBP uptrend. Recently, EUR/GBP was locked in a ST sideways range (0.83/0.85) after a substantial decline in March/April. The pair developed a bottoming out pattern with 0.84/0.8330 as a solid bottom. The breach of 0.8509/31 (previous ST tops) improved the technical picture. We continue to prefer a EUR/GBP buy-on-dips approach. Longer term, Brexit remains potentially negative for sterling.

EUR/GBP: jumps north of ST range top

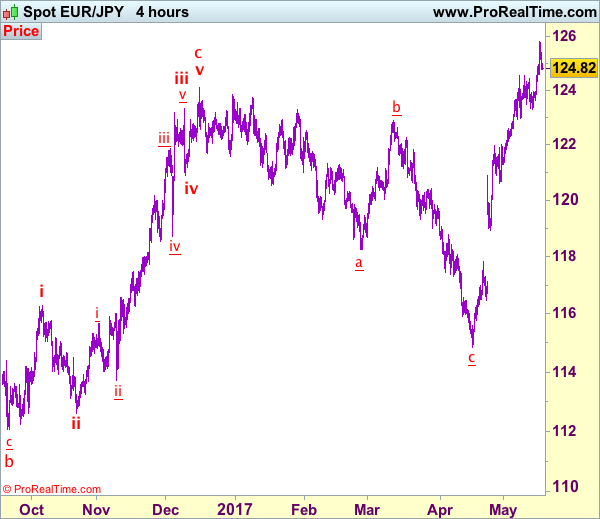

Trade Idea: EUR/JPY – Stand aside

EUR/JPY - 124.75

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term up

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Although the single currency surged to as high as 125.82 yesterday, the subsequent retreat suggests consolidation below this level would be seen and initial downside risk is for weakness to previous resistance at 124.55, break there would bring retracement to 124.00-10, however, reckon downside would be limited to 123.60-65 and previous support at 123.32 should hold, bring another rise later.

In view of this, would not this rise here and would be prudent to stand aside in the meantime. Above 125.50-55 would bring retest of 125.82 but break there is needed to revive bullishness and extend recent upmove to 126.00-10, then 126.40-50, however, near term overbought condition should limit upside to 126.90-00, risk from there has increased for another retreat to take place.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Oil Prices Retreated

Market movers today

Today is a quiet day in terms of economic data releases. In the UK, the labour market report for March is due. Weestimate the unemployment rate (3M average) was unchanged, as there is still no evidence that Brexit uncertainties and slower growth have hit the labour market. Weestimate the annual growth rate in average weekly earnings ex bonuses (3M average) fell from 2.2% to 2.1%, meaning that nominal wage growth continues to be subdued despite higher inflation.

The euro area final HICP figures for April are due out . The details should be especially interesting for April, as they should reveal to what extent Easter drove the inflation figure up.

The Polish cent ral bank is expected to keep the policy rate unchanged at 1.50%.

There are no market movers in Scandi today.

Selected market news

US President Donald Trump faced a new headwind on Tuesday after a source said Trump had asked former FBI Direct or James Comey to end the agency's investigation into ties between former White House national security adviser Michael Flynn and Russia. The growing concerns over US politics weighed on equity markets overnight with the S&P futures down around 0.5% overnight . The USD has also weakened and EUR/USD moved above 1.11 for the first time since November 2016 prior to the election. Following market concerns over European politics for some time, the worry seems to be moving in the direction of US politics. The decline in risk appet ite has pushed US bond yields a bit lower in Asian trading hours.

Oil prices retreated yesterday, breaking the rising trend over the past week. Brent crude oil fell USD1 per barrel on weaker risk sentiment and US data showing an increase in US crude stockpiles.

Data for US manufacturing production for April surprised on the upside yesterday, rising 1.0% m/m versus consensus of 0.4% m/m. Hence, hard data is catching a bit up with the stronger soft data seen in Q1. However, regional business surveys and ISM continue to show some weakening of the US cycle in the months ahead.

In Sweden, the Riksbank has proposed changes to the inflation framework to target the previous policy variable CP IF (still 2% target ) and introduce a ‘variation band' of +/-1%. The change should have no implicat ions for monetary policy though (see Riksbank Comment: Much ado about nothing, 16 May 2017).

Trade Idea: AUD/USD – Buy at 0.7370

AUD/USD – 0.7429

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term down

Original strategy :

Buy at 0.7370, Target: 0.7520, Stop: 0.7320

Position: -

Target: -

Stop: -

New strategy :

Buy at 0.7370, Target: 0.7520, Stop: 0.7320

Position: -

Target: -

Stop:-

As aussie found good support at 0.7329 and has staged a rebound, suggesting a temporary low is possibly formed there and consolidation with mild upside bias is seen for further gain to 0.7470-75, then 0.7500-10 but break of latter level is needed to add credence to this view, bring subsequent rise towards resistance at 0.7556 which is likely to hold from here due to near term overbought condition.

In view of this, we are looking to buy aussie on dips as 0.7360-70 should limit downside. A break of said support at 0.7329 would abort and signal recent decline is still in progress for weakness to 0.7295-00 (76.4% retracement of 0.7158-0.7750), however, loss of downward momentum should prevent sharp fall below 0.7300 and reckon 0.7245-50 would remain intact, bring another rebound later.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

Australia’s Consumer Confidence Declined In May

For the 24 hours to 23:00 GMT, the EUR rose 1.04% against the USD and closed at 1.1093, on the back of upbeat economic data from across the Euro-zone.

Data indicated that the Euro-zone's ZEW economic sentiment index jumped to a level of 35.1 in May, following a reading of 26.3 in the prior month, as concerns over political turmoil across the common currency region receded. Additionally, the region's second estimate of gross domestic product (GDP) advanced 0.5% on a quarterly basis in the first quarter of 2017, confirming the flash estimate. In the prior quarter, GDP had registered a similar rise. Further, the region's seasonally adjusted trade surplus widened to a level of €23.1 billion in March, from a revised surplus of €18.8 billion recorded in the prior month, while market participants expected the region to post a surplus of €18.7 billion.

Separately, confidence among German investors strengthened to a nearly two-year high level of 20.6 in May, compared to a reading of 19.5 in the prior month. Investors had envisaged the index to climb to a level of 22.0. Also, the nation's ZEW current situation index rose more-than-anticipated to a level of 83.9 in May, compared to a level of 80.1 in the previous month.

The greenback lost ground against a basket of major currencies, on reports that the US President, Donald Trump, disclosed highly classified information to Russia's Foreign Minister about a planned Islamic State operation in a meeting last week.

Earlier in the session, the US Dollar fell against its major peers, after disappointing building permits and housing starts data in the US dampened optimism over the health of the nation's housing sector.

Housing starts in the US unexpectedly dropped 2.6% on monthly basis, to an annual rate of 1172.0K in April, hitting its lowest level in five months, led by a big drop in construction of apartments. Markets anticipated housing starts to advance to a level of 1260.0K, after recording a revised level of 1203.0K in the previous month. Further, the nation's building permits surprisingly fell 2.5% on a monthly basis, to an annual rate of 1229.0K in April, compared to market consensus for a rise to a level of 1270.0K and following a level of 1260.0K in the prior month.

On the contrary, the US manufacturing production surged to a more than three-year high level, after it jumped 1.0% in April, surpassing market expectations for an advance of 0.4%. In the previous month, manufacturing production had dropped 0.4%. Moreover, the nation's industrial production climbed more-than-expected by 1.0% in April, notching its highest level since February 2014. Market participants expected industrial production to gain 0.4%, following a revised rise of 0.4% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.1109, with the EUR trading 0.14% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1022, and a fall through could take it to the next support level of 1.0936. The pair is expected to find its first resistance at 1.1154, and a rise through could take it to the next resistance level of 1.1200.

Moving ahead, all eyes would be on the Euro-zone's final consumer price index for April, slated to release in a few hours. Moreover, in the US, weekly mortgage applications data will also be on investors' radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s GDP Growth Confirmed At 0.5% In 1Q 2017

For the 24 hours to 23:00 GMT, the EUR rose 1.04% against the USD and closed at 1.1093, on the back of upbeat economic data from across the Euro-zone.

Data indicated that the Euro-zone's ZEW economic sentiment index jumped to a level of 35.1 in May, following a reading of 26.3 in the prior month, as concerns over political turmoil across the common currency region receded. Additionally, the region's second estimate of gross domestic product (GDP) advanced 0.5% on a quarterly basis in the first quarter of 2017, confirming the flash estimate. In the prior quarter, GDP had registered a similar rise. Further, the region's seasonally adjusted trade surplus widened to a level of €23.1 billion in March, from a revised surplus of €18.8 billion recorded in the prior month, while market participants expected the region to post a surplus of €18.7 billion.

Separately, confidence among German investors strengthened to a nearly two-year high level of 20.6 in May, compared to a reading of 19.5 in the prior month. Investors had envisaged the index to climb to a level of 22.0. Also, the nation's ZEW current situation index rose more-than-anticipated to a level of 83.9 in May, compared to a level of 80.1 in the previous month.

The greenback lost ground against a basket of major currencies, on reports that the US President, Donald Trump, disclosed highly classified information to Russia's Foreign Minister about a planned Islamic State operation in a meeting last week.

Earlier in the session, the US Dollar fell against its major peers, after disappointing building permits and housing starts data in the US dampened optimism over the health of the nation's housing sector.

Housing starts in the US unexpectedly dropped 2.6% on monthly basis, to an annual rate of 1172.0K in April, hitting its lowest level in five months, led by a big drop in construction of apartments. Markets anticipated housing starts to advance to a level of 1260.0K, after recording a revised level of 1203.0K in the previous month. Further, the nation's building permits surprisingly fell 2.5% on a monthly basis, to an annual rate of 1229.0K in April, compared to market consensus for a rise to a level of 1270.0K and following a level of 1260.0K in the prior month.

On the contrary, the US manufacturing production surged to a more than three-year high level, after it jumped 1.0% in April, surpassing market expectations for an advance of 0.4%. In the previous month, manufacturing production had dropped 0.4%. Moreover, the nation's industrial production climbed more-than-expected by 1.0% in April, notching its highest level since February 2014. Market participants expected industrial production to gain 0.4%, following a revised rise of 0.4% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.1109, with the EUR trading 0.14% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1022, and a fall through could take it to the next support level of 1.0936. The pair is expected to find its first resistance at 1.1154, and a rise through could take it to the next resistance level of 1.1200.

Moving ahead, all eyes would be on the Euro-zone's final consumer price index for April, slated to release in a few hours. Moreover, in the US, weekly mortgage applications data will also be on investors' radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.