Sample Category Title

AUD Forecast Unclear Ahead Of Consumer Sentiment Data

Key Points:

- Weak technical bias could see a ranging phase occur.

- Fundamentals likely to be more important as we move ahead.

- Consumer Sentiment data likely to be the key risk event.

The AUDUSD was all over the show last week which now begs the question, where is it off to in the week to come? Due to this, it's worth taking a look at exactly what happened and how this has positioned the pair for what's coming down the line fundamentally. However, we should also take a look at the technical forecast to try gauge whether the bulls or bears are going to be in command moving forward.

Starting with lasts week's performance, the Aussie Dollar had a fairly torrid few sessions of trading as it initially sank sharply before correcting as the week came to an end. This initial bearishness was a symptom of the 0.1% contraction in the Australian Retail Sales figure which revived the only recently allayed fears of a recession. The subsequent reversal stemmed primarily from some weaker US data, including the softer than expected Core CPI result of only 0.1% and a Core Retail Sales figure of 0.3%. Overall, the two swings largely offset one another and the pair closed only fractionally lower at 0.7384.

On the technical front, the AUD remained bound by its narrowing wedge last week but it is now equidistant from either constraint which leaves its technical outlook somewhat uncertain. Nevertheless, the EMA bias and the Parabolic SAR reading continue to favour the downside which means we are now poised to see more losses. This bearish outlook is only reinforced by the long wick on Friday's candle which seems to suggest that the bulls are fairly thin on the ground.

As for what lies ahead on the news front, the Australian Consumer Sentiment data will be worth monitoring this week as it could generate a much larger move than is typical of the release. This is primarily due to the fact that it is the first reaction we have to the recently presented federal budget which has had a mixed reception in the online commentary space. If we have a solid uptick in the sentiment result, we could see the pair hold onto the prior few session's gains as they are currently in danger of being eroded. However, also keep half an eye on the Aussie Unemployment Rate, even though it's expected to remain flat at 5.9%.

Ultimately, the relatively weak technical bias and the unclear fundamental outlook make the AUD a risky bet moving ahead. Ideally, we would need to see the pair move closer to the constraints of its wedge before we can forecast a strong reversal which likely means a ranging phase should take hold this week. As a result, we don't expect to see price action break out of the 0.7420 – 0.7367 levels this week unless we see some major fundamental upsets.

Cable Likely To Remain Bearish In The Week Ahead

Key Points:

- Cable likely to remain bearish in the coming session.

- Support at 1.2830 will be relatively critical.

- Technical factors currently suggesting a corrective move ahead.

The Cable had a week in the red as the pair experienced a sentiment swing towards the greenback following the release of a range of stronger U.S. economic data. In addition, the Bank of England also impacted the Cable's prospects following the release of the latest MPC statement that proved to be significantly more dovish than expected. Subsequently, the pair continued to slip lower during the trading week and closed the final session out around the 1.2883 mark. Subsequently, we take a look at what occurred last week with a view to discovering some insight for the coming session.

The Cable provided a relatively poor performance last week as the currency reacted to a range of stronger U.S economic data as well as a relatively dovish central bank. In particular, the U.S. JOLTS figures sent the pair reeling, as did the surprisingly strong Unemployment Claims result at 236k. However, it was largely the Bank of England and their dovish outlook on interest rates that did the pair the most damage. The decision was always going to be to keep the official bank rate on hold at 0.25%, but the dovish rhetoric was largely unexpected and saw the Cable give up around 60 pips just from the central bank's statement. Subsequently, the pair closed the trading week out around the 1.2883 mark.

Looking ahead, the Cable is in for an exceedingly busy week with the primary focus to fall upon the UK CPI and Core Retail Sales data. In fact, the CPI figures are likely to be very closely watched because of the building inflation that has been evident within the UK economy. Subsequently, this is likely to inform on potential action from the Bank of England incoming MPC meetings. Additionally, the Core Retail Sales figures could also prove illuminating given that they are a good gauge of consumer spending and demand. The forecast has the benchmark rising to 1.0% but we could potentially see a slight uptick in that result. On the U.S. side of the ditch, watch out for the Philly Fed Manufacturing Index, estimated to come in at 19.8.

From the technical perspective, the pair's recent decline has relieved some pressure from the overbought RSI and Stochastic Oscillator's. However, the trend is still downward in nature and the 1.2830 support zone could be challenged in the coming week. Subsequently, our bias is bearish given that we are no longer forming higher highs.Support is currently in place for the pair at 1.2830, 1.2754, and 1.2625. Resistance exists on the upside at 1.2986, 1.3121, and 1.3335.

Ultimately, the UK CPI figures are likely to set the fundamental trend for the pair in the week ahead. However, even a strong result will need to contend with the various technical indicators which are all suggesting that the coming week could prove relatively negative for the pair.

European Open Briefing: Asian Stock Markets Had A Solid Performance

Global Markets:

- Asian stock markets: Nikkei down 0.20 %, Shanghai Composite gained 0.30 %, Hang Seng rose 0.70 %, ASX 200 lost 0.10 %

- Commodities: Gold at $1230 (+0.20 %), Silver at $16.52 (+0.70 %), WTI Oil at $48.65 (+1.70 %), Brent Oil at $51.70 (+1.70 %)

- Rates: US 10-year yield at 2.33, UK 10-year yield at 1.10, German 10-year yield at 0.39

News & Data

- China Industrial Production 6.5 % vs 7.1 % expected

- China Retail Sales 10.7 % vs 10.6 % expected

- China Fixed Asset Investment 8.9 % vs 9.1 % expected

- New Zealand Retail Sales q/q 1.5 % vs 1.1 % expected

- New Zealand Core Retail Sales q/q 1.2 % vs 0.9 % expected

- Japan PPI m/m 0.2 % vs -0.1 % expected

- Japan PPI y/y 2.1 % vs 1.8 % expected

- Australia Home Loans -0.5 % vs 0.1 % expected

- PBOC sets USD/CNY central rate at 6.8852 (vs. Friday at 6.8948)

- Russia's Novak: Russia And Saudi Agree Output Cuts Need to Be Extended Until March 2018

CFTC Positioning Data:

- EUR long 22K vs 2K short last week. Longs increased by 24K

- GBP short 47K vs 81K short last week. Shorts trimmed by 34K

- JPY short 36K vs 30K short last week. Shorts increased by 6K

- CHF short 15K vs 18K short last week. Shorts trimmed by 3K

- CAD short 86K vs 48K short. Shorts increased by 38K

- AUD long 26K vs 43K long. Longs cut 17K

- NZD short 11K vs 12K short last week. Shorts trimmed by 1K

Markets Update:

Markets did not react to the news about another North Korean missile test. Asian stock markets had a solid performance overall, and commodity currencies rose overnight, indicating that risk appetite remains intact for now.

EUR/USD opened in Asia around 1.0930, unchanged from Friday's close. The currency rose on Friday on rumours that the ECB might signal the end of its ultra-loose monetary policy this summer. However, those are still only rumours. EUR/USD faces resistance at 1.0950, followed by 1.10.

USD/JPY recovered slightly overnight. Resistance is now seen at the former support area between 113.70 and 113.80. Key support is noted at 113. Should USD/JPY break below it, further losses towards 112.20 seem likely.

AUD/USD traded in a 0.7385-0.74 range overnight. Resistance at 0.7420/25 has proven to be strong. A clear break above it would then signal a move towards 0.75 though.

Upcoming Events:

- 10:00 BST – Italian CPI

- 13:30 BST – US NY Empire State Manufacturing Index

- 15:00 BST – US NAHB Housing Market Index

The Week Ahead:

Tuesday, May 16th

- 02:30 BST – RBA Meeting Minutes

- 07:45 BST – French CPI

- 09:00 BST – Italian GDP

- 09:30 BST – UK GDP

- 10:00 BST – German ZEW Economic Sentiment

- 10:00 BST – Euro Zone GDP

- 10:00 BST – Euro Zone ZEW Economic Sentiment

- 13:30 BST – US Housing Starts

- 13:30 BST – US Building Permits

- 14:15 BST – US Industrial Production

- 14:15 BST – US Manufacturing Production

Wednesday, May 17th

- 01:30 BST – Australian Westpac Consumer Sentiment

- 09:30 BST – UK Claimant Count Change

- 09:30 BST – UK Unemployment Rate

- 10:00 BST – Euro Zone CPI

- 15:30 BST – US Crude Oil Inventories

Thursday, May 18th

- 00:50 BST – Japanese GDP

- 02:30 BST – Australian Unemployment Rate

- 02:30 BST – Australian Employment Change

- 09:30 BST – UK Retail Sales

- 13:30 BST – US Philadelphia Fed Manufacturing Index

- 15:00 BST – US CB Leading Index

- 18:00 BST – ECB President Draghi speaks

Friday, May 19th

- 07:00 BST – German PPI

- 09:00 BST – Euro Zone Current Account

- 13:30 BST – Canadian CPI

- 13:30 BST – Canadian Retail Sales

- 15:00 BST – Euro Zone Consumer Confidence

Aussie Trading A Tad Higher In The Morning Session

For the 24 hours to 23:00 GMT, the AUD rose 0.3% against the USD and closed at 0.7393 on Friday.

LME Copper prices declined 1.1% or $60.5/MT to $5520.0/MT. Aluminium prices declined 0.4% or $7.0/MT to $1880.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7395, with the AUD trading slightly higher against the USD from Friday's close.

Early morning data revealed that Australia's seasonally adjusted home loan approvals unexpectedly eased 0.5% in March, compared to a revised fall of 0.8% in the previous month, while markets were anticipating for a flat reading.

Elsewhere, in China, Australia's largest trading partner, industrial production rose less-than-anticipated by 6.5% YoY in April, compared to an advance of 7.6% in the previous month. Markets participants had envisaged industrial production to rise 7.0%. Moreover, the nation's retail sales climbed less-than-anticipated by 10.7% on an annual basis in April, compared to market consensus for an advance of 10.8%. In the prior month, retail sales had risen 10.9%.

The pair is expected to find support at 0.7368, and a fall through could take it to the next support level of 0.7340. The pair is expected to find its first resistance at 0.7422, and a rise through could take it to the next resistance level of 0.7448.

Looking ahead, investors will look forward to minutes of the Reserve Bank of Australia's (RBA) latest meeting, scheduled to release in the early hours of tomorrow.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

German Economic Growth At A 12-Month High Level In 1Q 2017

For the 24 hours to 23:00 GMT, the EUR rose 0.61% against the USD and closed at 1.0928 on Friday, after Germany's seasonally adjusted preliminary gross domestic product (GDP) rose 0.6% on a quarterly basis in the first quarter of 2017, meeting market expectations and charting its strongest quarterly growth in a year, thus suggesting that the common currency region's largest economy started the year on a stronger footing. In the prior quarter, GDP had climbed 0.4%. Moreover, the nation's final consumer price index advanced 2.0% on an annual basis in April, confirming the preliminary print and compared to an advance of 1.6% in the previous month.

Separately, the Euro-zone's seasonally adjusted industrial production unexpectedly fell 0.1% on a monthly basis in March, defying market expectations for a rise of 0.3% and compared to a revised fall of 0.1% in the previous month.

The greenback traded lower against its major peers on Friday, as disappointing US inflation and retail sales data raised concerns about the health of the nation's retail sector and the broader economy.

Data showed that advance retail sales in the US recorded a rise of 0.4% on a monthly basis in April, undershooting market expectations for a rise of 0.6%. Advance retail sales had risen by a revised 0.1% in the previous month. Moreover, the nation's consumer price index (CPI) rose less-than-anticipated by 2.2% on an annual basis in April, compared to market expectations for an advance of 2.3%. In the prior month, the CPI had risen 2.4%. Meanwhile, on a monthly basis, the CPI climbed 0.2% in April, meeting market expectations and following a drop of 0.3% in the prior month.

On the other hand, the nation's flash Reuters/Michigan consumer sentiment index surprisingly jumped to a level of 97.7 in May, highlighting that Americans are getting increasingly optimistic over the nation's economic outlook. The index had registered a reading of 97.0 in the prior month, while markets expected for a steady reading. Meanwhile, the nation's business inventories registered a rise of 0.2% in March, at par with market expectations and after recording a revised similar rise in the prior month.

Separately, the Philadelphia Fed President, Patrick Harker, called for an additional two interest rate hikes this year.

In the Asian session, at GMT0300, the pair is trading at 1.0927, with the EUR trading marginally lower against the USD from Friday's close.

The pair is expected to find support at 1.0876, and a fall through could take it to the next support level of 1.0825. The pair is expected to find its first resistance at 1.0956, and a rise through could take it to the next resistance level of 1.0985.

Moving ahead, investors will await the release of German Buba monthly report, slated to release in a few hours. Moreover, the US NAHB housing market index for May, set to release later in the day, will be on investors' radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Pound Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the GBP declined 0.06% against the USD and closed at 1.2880 on Friday.

In the Asian session, at GMT0300, the pair is trading at 1.2892, with the GBP trading 0.09% higher against the USD from Friday’s close.

The pair is expected to find support at 1.2856, and a fall through could take it to the next support level of 1.2821. The pair is expected to find its first resistance at 1.2913, and a rise through could take it to the next resistance level of 1.2935.

In absence of any relevant economic releases in the UK today, market participants will look forward to global macroeconomic events for direction.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Japanese Yen Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.41% against the JPY and closed at 113.29 on Friday.

In the Asian session, at GMT0300, the pair is trading at 113.37, with the USD trading 0.07% higher against the JPY from Friday’s close.

The pair is expected to find support at 113.05, and a fall through could take it to the next support level of 112.74. The pair is expected to find its first resistance at 113.80, and a rise through could take it to the next resistance level of 114.24.

Going ahead, traders would focus on Japan’s tertiary industry index for March, slated to release tomorrow.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Marginally Lower In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.67% against the CHF and closed at 1.0009 on Friday.

In the Asian session, at GMT0300, the pair is trading at 1.0013, with the USD trading a tad higher against the CHF from Friday’s close.

The pair is expected to find support at 0.9972, and a fall through could take it to the next support level of 0.9930. The pair is expected to find its first resistance at 1.0070, and a rise through could take it to the next resistance level of 1.0126.

Ahead in the day, investors will keep a close watch on Switzerland’s producer and import prices for April.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Loonie Trading Higher This Morning, Ahead Of Canada’s Existing Home Sales Data

For the 24 hours to 23:00 GMT, the USD slightly rose against the CAD and closed at 1.3709 on Friday.

On the data front, Canada's Teranet/National Bank house price index rose 1.2% in April, following a gain of 0.9% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.3680, with the USD trading 0.21% lower against the CAD from Friday's close.

The pair is expected to find support at 1.3649, and a fall through could take it to the next support level of 1.3618. The pair is expected to find its first resistance at 1.3726, and a rise through could take it to the next resistance level of 1.3772.

Going ahead, all eyes will be on Canada's existing home sales data for April, due to release later in the day.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

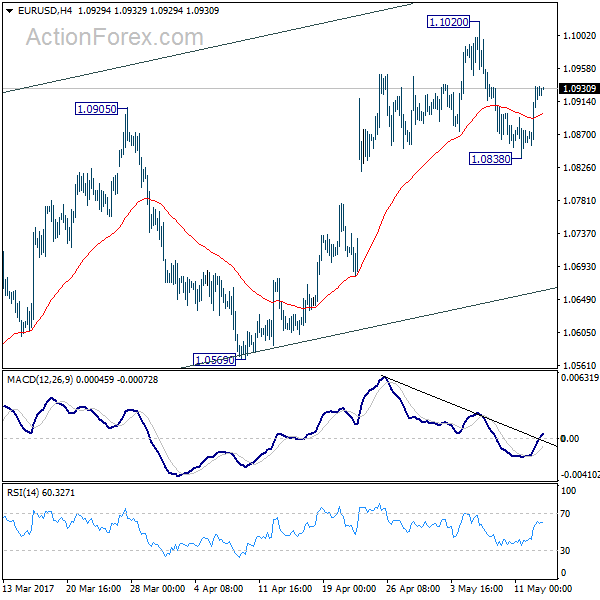

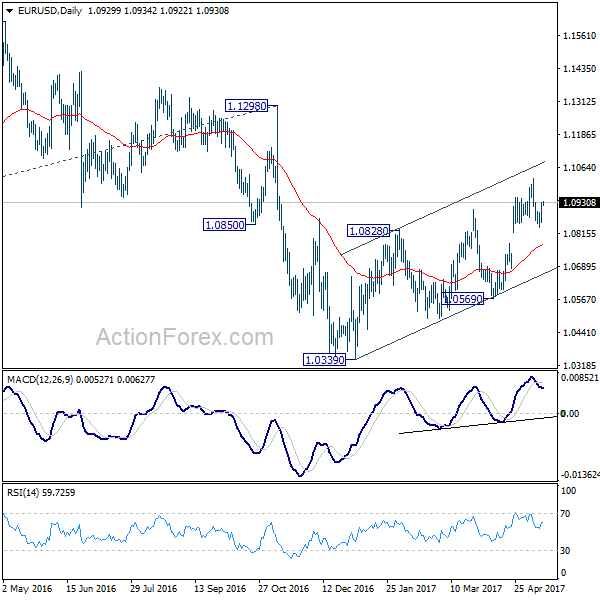

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0878; (P) 1.0906 (R1) 1.0957; More....

Intraday bias in EUR/USD remains neutral for the moment. Overall outlook is unchanged, choppy rise from 1.0339 is seen as a corrective move. In case, of another rally, we'll look for reversal signal again above 1.1020. Break of 1.0838 will turn bias to the downside for 55 day EMA (now at 1.0770). Break there will argue that the corrective rise from 1.0339 is completed and target 1.0569 support for confirmation.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate long term reversal.