Sample Category Title

Trade Idea: USD/CAD – Buy at 1.3600

USD/CAD - 1.3735

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

Original strategy :

Buy at 1.3600, Target: 1.3750, Stop: 1.3540

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.3600, Target: 1.3750, Stop: 1.3540

Position: -

Target: -

Stop:-

As the greenback has continued trading with a firm bias after recent rally above 1.3599 resistance, adding credence to our view that recent upmove is still in progress and bullishness remains for further gain to 1.3760-70, however, near term overbought condition should prevent sharp move beyond 1.3800-10 and reckon 1.3840-50 would hold on first testing, risk from there is seen for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy again on pullback as 1.3600 should limit downside. Only below said support at 1.3530 would abort and signal a temporary top is formed instead, risk correction to 1.3500 and later towards 1.3450-60 but support at 1.3411 should remain intact, bring another upmove later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

French Election Monitor: Le Pen’s Chances of Winning Presidency Increasingly Slim

On Sunday 7 May, the final round of the French presidential election will take place between the far-right candidate Marine Le Pen and independent Emmanuel Macron. As opinion polls have accurately predicted the first round result and pointed consistently towards a Macron win (see Chart 1), markets have largely priced out any French election risk premium over recent weeks. Yesterday's TV debate marked the final decisive battle between the candidates. Importantly, 63% of viewers saw Macron as the most convincing candidate in a snap poll conducted by Elabe afterwards (see Chart 2).

As with the first round, exit polls by the main TV and radio channels will be released once voting stations close at 20:00 CEST on Sunday and watched closely by the market. Official election results will be released by the Ministry of the Interior over the course of the night and updated continually. Turnout estimations released during the day could give an early indication of how close the race will be, as lower participation would increase Le Pen's chances of winning. By depicting Macron as the candidate of the political and financial elite over the past two weeks, Le Pen has already tried to convince previous Mélenchon supporters to abstain in the run-off. On Saturday, she also chose defeated first-round candidate Nicolas Dupont-Aignan as her Prime Minister, in a bid to attract his voters and broaden her support.

The election outcome will to a large degree depend on which candidate the previous François Fillon and Jean-Luc Mélenchon voters (some 14m) will support in the run-off. Both Fillon and Benoît Hamon have endorsed Macron since the first round and according to polls, Macron is the preferred choice over Le Pen for voters who have supported other candidates in the first round (see Chart 3). However, the great unknown remains how many of these will abstain in the second round due to dissatisfaction with the candidate choice available to them in the run-off. For now, Le Pen's chances of winning look increasingly slim, and she can only hope for a large abstention rate on Sunday to swing the vote in her favour. Following the run-off, focus will turn quickly to the parliamentary elections in June, which will determine the legislative support of the new President (see Chart 4).

CAC Edges Higher as TV Bout Goes to Macron

The CAC has posted slight gains in the Thursday session. Currently, the index is trading at 5,355.27. On the release front, German and Eurozone Services PMIs continued to show expansion and were above expectations. Eurozone Retail Sales posted a gain of 0.3%, above the estimate of 0.1%. Later in the day, ECB President Mario Draghi will speak at an event in Switzerland. On Friday, the Eurozone publishes Retail PMI, and the US releases wage growth and nonfarm payrolls reports.

The eurozone has enjoyed a solid first quarter, and more growth has meant more jobs and lower unemployment figures. Just a year ago, the eurozone unemployment rate was at 10.3%, but the rate has been steadily decreasing since then. The March release remained unchanged at 9.5%, within expectations. Germany has led the way, with the unemployment rate dropping to 5.9% in February. Unemployment rolls continue to shrink in Germany, and the decline of 15,000 unemployed persons was better than the estimate of 10,000. Services PMI reports for March have also looked solid, with the Eurozone and Germany releases pointing to expansion.

As widely expected, the Federal Reserve stayed on the sidelines on Wednesday, holding the benchmark rate at 0.75 percent. However, the Fed rate statement was hawkish, as policymakers emphasized the positives and donwplayed a soft first quarter for the US economy. The statement noted that consumer spending remains strong and that inflation was "running close" to the Fed's 2 percent target. The Fed's message is clearly one of optimism, as the central bank remains on track to raise interest rates twice more in 2017. The Fed's bullish statement immediately raised the likelihood of a rate hike at June meeting, which jumped to 74 percent after the statement, up from 63% before meeting. The Fed has two key goals which have been achieved, namely full employment and an inflation rate of 2%. One area of concern is the balance sheet, which stands at $4.5 trillion. The minutes of the March meeting stated that policymakers want to start reducing this figure before the end of 2017, and we could see another reference to the balance sheet in the April minutes.

Just a few days ahead of the French election, Emmanuel Macron and Marie Le Pen faced off in a highly-anticipated television debate on Wednesday. Polls taken after the feisty debate showed that 64% of viewers felt Macron won the debate. With a 20-point lead in the polls, Macron had the most to lose from the debate, but he kept his cool and acted presidential, in contrast to Le Pen. Barring a dramatic event in the next few days, such as a terror attack, all signs are pointing to Macron becoming France's next president. Parliamentary elections are scheduled for June, so the French political landscape will remain uncertain until then. Macron's En Marche! party is expected to win the most seats, and has an outside short at forming a majority in parliament.

Gold Edges Down Ahead of NFP

The crucial US labour market data for April will be released this Friday May 5, at 13:30 BST. It includes non-farm payrolls, unemployment rate and average hourly earnings.

Please note that the release of US labour market data will likely cause volatility for USD, USD crosses and commodities.

Spot gold has retraced around 3.6% since mid-April as it neared a significant resistance level at $1300.

Following the first-round of the French presidential election market concerns about a collapse of the EU have eased somewhat and thus further weighed on the price of gold.

The recent FOMC meeting has left the door open for a June rate hike which has pushed USD higher and resulted in spot gold falling below a significant psychological level at $1250.

On the 4-hourly chart the current price is still trading along the lower band of the Bollinger Band indicator suggesting the trend remains bearish. The downtrend is likely to test the support line at $1230.

If the upcoming non-farm payrolls for April is in line with, or above, expectations of 180K and accompanied by an upward revision of the previous figure, along with rising wages and a stable unemployment rate – then the support at $1230 will likely be broken.

Conversely, if the upcoming non-farm payrolls is far below expectations, accompanied by a downward revision of the previous figure, low wage growth and a rising unemployment rate -then it will likely result in a weaker USD and a rebound in gold prices.

The resistance level is at $1237.00, followed by $1240 and $1244.

The support line is at $1230, followed by $1225 and $1220.

Be aware that, based on prior experience, market trends sometimes reverse within 1-2 hours after the initial move.

Canada’s Trade Deficit Narrowed in March

Canada's trade deficit narrowed to $135 million in March (previously $1.1 billion), as a 3.8% rise exports outpaced the 1.7% increase in imports. In real terms, the picture was even better, as export volumes were up 2.5% and imports slipped 0.2%.

The rise in exports was widespread, led by energy, consumer goods and metal and non-metallic mineral products which were all up by 7% during the month. The jump in energy exports was driven largely by higher natural gas and coal exports. A decline in motor vehicle and metal ores and non-metallic minerals provided some offset.

Canada's trade surplus with the U.S. narrowed to $4 billion in March (previously $4.5 billion), while its deficit with the rest of the world narrowed to $4.1 billion (previously $5.6 billion).

Key Implications

The bounce back in export volumes is certainly a welcome development, but strong imports and weak exports earlier in the year means that net trade will weigh on economic growth in the first quarter of this year. Even with this drag, the Canadian economy is still on track to advance by a robust 3.4% in Q1. Moreover, March's trade data will provide a solid hand off for the second quarter.

Going forward, the recent momentum in exports should continue, as the Canadian dollar remains under pressure - the loonie fell below 73 US cents this week for the first time in over a year - and economic activity in the U.S. is set to pick up after a slow start to the year.

The key risk to the outlook remains any potential changes to trade policy with the United States. Last week's (preliminary) announcement that Canadian softwood lumber exports will be hit with a hefty tariff shows that the new President intends to make good on his promise to ensure fair trade for America. While a NAFTA re-negotiation is almost certain to come, we suspect that the agreement will remain largely intact given the close trading relationship between these two countries and effectively balanced trading relationship when services are accounted for.

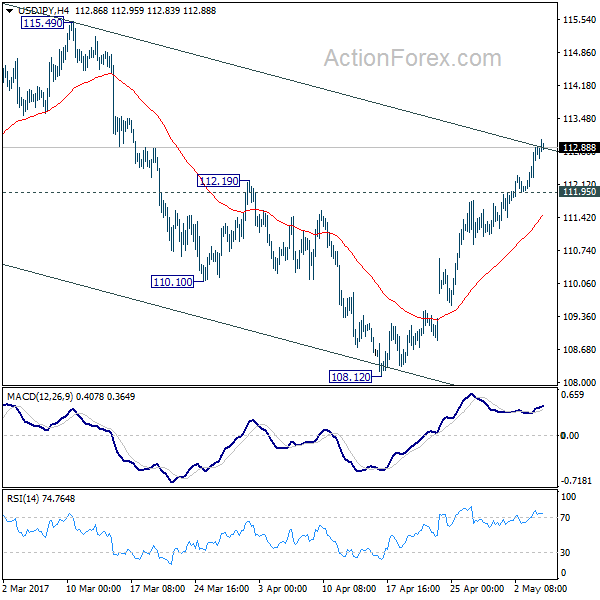

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.22; (P) 112.49; (R1) 113.04; More...

Intraday bias in USD/JPY remains on the upside as rise from 108.12 continues and is picking up momentum again. As noted before, corrective fall from 118.65 has completed with three waves down to 108.12 already. Current rise should target 115.49 resistance. Break of 115.49 will resume larger rally from 98.97 to 125.85 high. On the downside, below 111.95 minor support will turn bias neutral and bring consolidations first.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

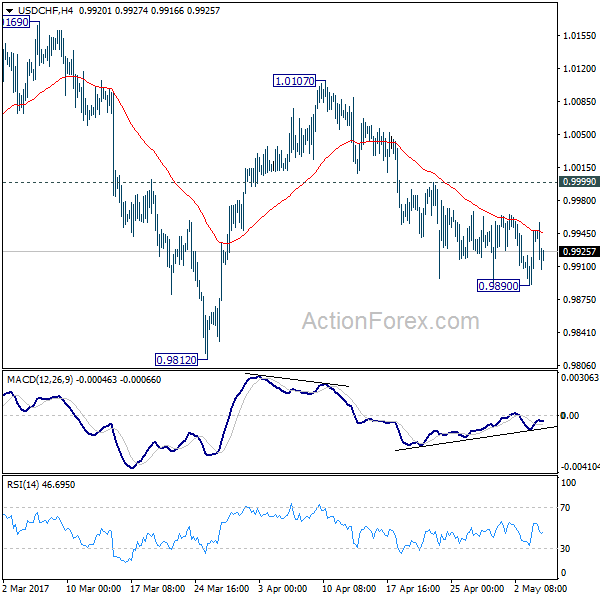

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9908; (P) 0.9928; (R1) 0.9965; More.....

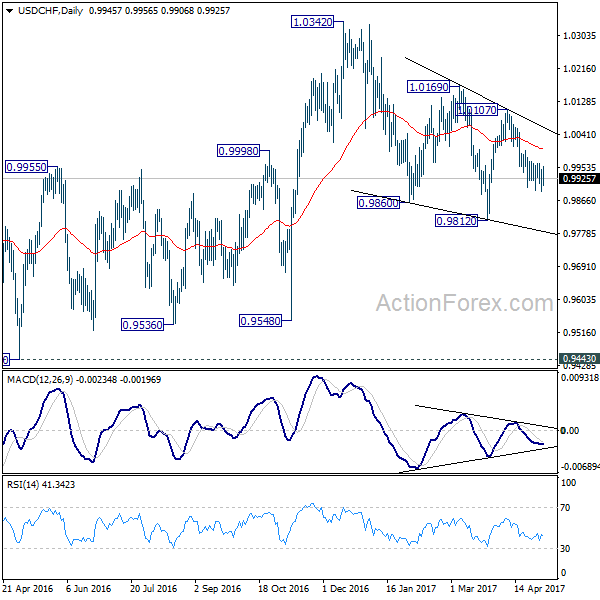

Intraday bias in USD/CHF remains neutral for the moment. With 0.9999 minor resistance holds, deeper decline is mildly in favor. Below 0.9890 will target 0.9812 and below to extend the correction from 1.0342. But break of 0.9812 should be brief and we will look for bottoming signal below there. On the upside, above 0.9999 minor resistance argues that fall from 1.0107 is finished, with bullish convergence condition in 4 hour MACD. In that case, intraday bias will be flipped back to the upside for 1.0107 resistance first.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

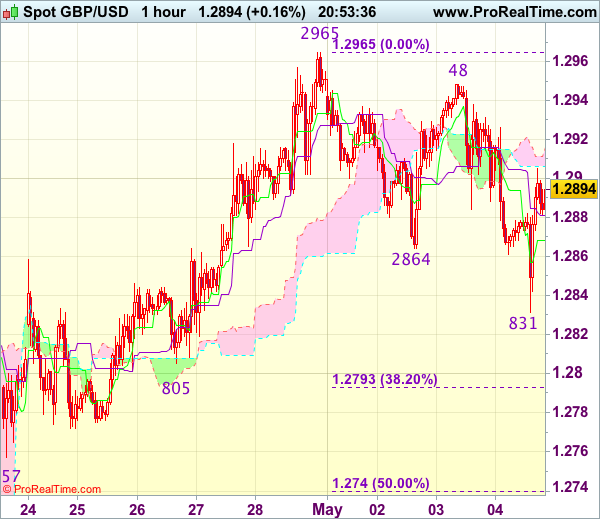

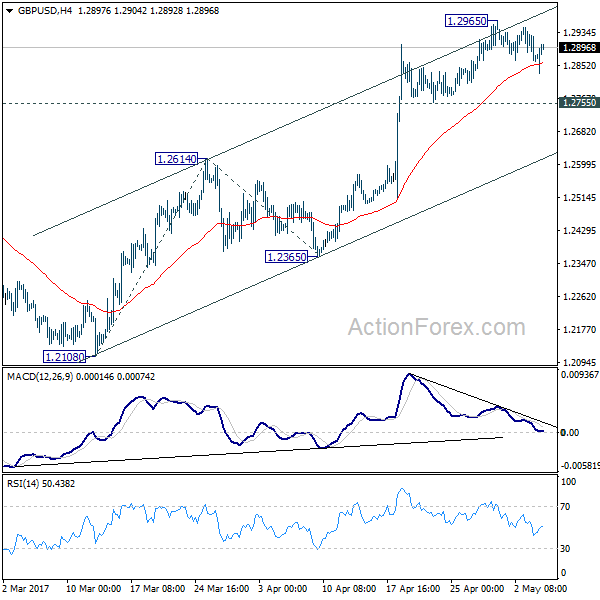

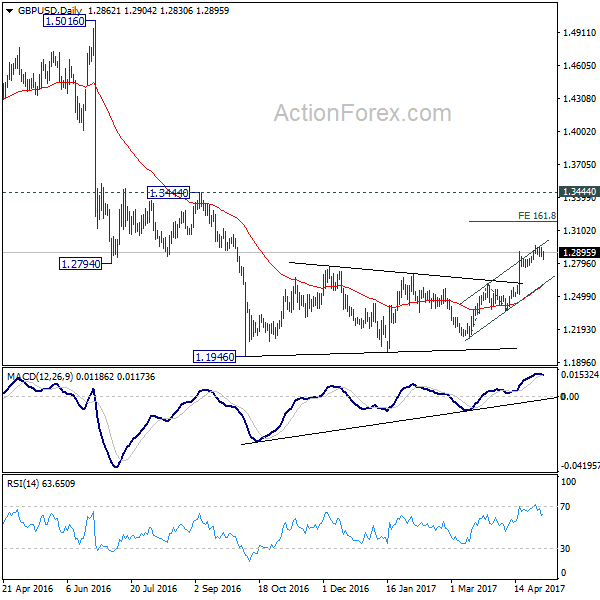

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2838; (P) 1.2893; (R1) 1.2921; More...

GBP/USD is still staying in consolidative trading in range of 1.2755/2965 and intraday bias remains neutral. Another rise is mildly in favor with 1.2755 support intact. Break of 1.2965 will target 161.8% projection of 1.2108 to 1.2614 from 1.2365 at 1.3184. At this point, price actions from 1.1946 are still seen as a correction pattern. Therefore, we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2755 minor support will turn bias to the downside. Further break of 1.2614 resistance turned support will now indicate near term reversal.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

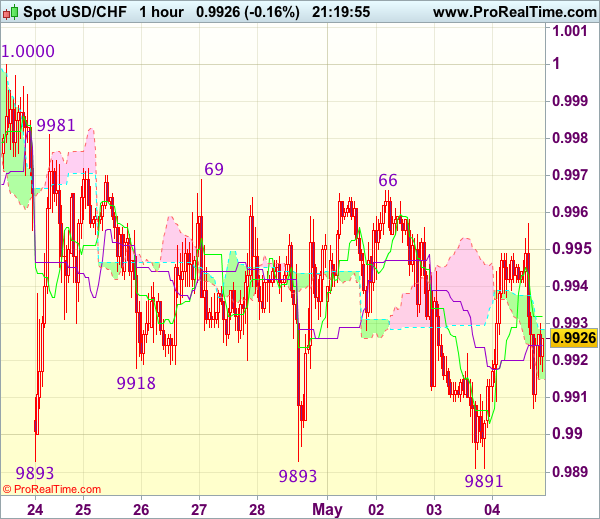

Trade Idea Update: USD/CHF – Stand aside

USD/CHF - 0.9923

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s brief fall to 0.9891, lack of follow through selling on break of previous support at 0.9893 and the subsequent rebound has retained our view that further consolidation is in store and test of 0.9966-69 resistance cannot be ruled out, however, a break of 0.9981 is needed to signal low is formed, bring a stronger rebound to 1.0000-08 resistance, above there would confirm a temporary low has been formed at 0.9891, bring retracement of recent decline to 1.0020-30 (61.8% Fibonacci retracement of 1.0108-0.9891) but price should falter well below resistance at 1.0067.

On the downside, below 0.9905-10 would bring retest of 0.9891 but break there is needed to confirm recent decline from 1.0108 top has resumed and extend weakness to 0.9865-70 (2 times extension of 1.0108-1.0008 measuring from 1.0067), however, support at 0.9831 would hold from here, bring rebound later. As near term outlook is still mixed, would be prudent to stand aside for now.

Trade Idea Update: GBP/USD – Buy at 1.2790

GBP/USD - 1.2900

Original strategy :

Buy at 1.2790, Target: 1.2910, Stop: 1.2755

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2790, Target: 1.2910, Stop: 1.2755

Position : -

Target : -

Stop : -

Although cable has rebounded after intra-day brief fall to 1.2831, reckon upside would be limited to 1.2910-15 and near term downside risk remains for the corrective fall from 1.2965 to bring retracement of recent upmove, below said support at 1.2831 would extend weakness to 1.2790-95 (38.2% Fibonacci retracement of 1.2515-1.2965) where renewed buying interest should emerge, bring another rise later. Above 1.2948 would bring retest of 1.2965, break there would confirm upmove has resumed for headway towards 1.2990-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance).

In view of this, would not chase this rise here and would be prudent to buy cable on further subsequent pullback as downside should be limited to 1.2790-95. A drop below previous support at 1.2757 would abort and signal top is formed instead, bring correction to 1.2740 (50% Fibonacci retracement of 1.2515-1.2965) first.