Sample Category Title

Yen Edges Lower in Thin Holiday Trade, Fed Statement Ahead

USD/JPY has edged upwards in the Wednesday session. In North American trade, the pair is trading at 112.40. Japanese banks are closed for Greenery Day. On the release front, BoJ Core CPI disappointed with a decline of 0.1%, short of the forecast of 0.2%. In the US, ADP Nonfarm Payrolls fell to 177 thousand, very close to the forecast of 178 thousand. The ISM Non-Manufacturing PMI improved to 57.5, beating the estimate of 56.1 points. Today's key event is the Federal Reserve's policy statement, with no change expected in the benchmark interest rate. On Thursday, the US will release unemployment claims.

Japanese inflation continues to underwhelm, and BoJ Core CPI was soft, posting a rare decline. A year ago, the indicator posted a solid gain of 1.1%, but since then consumer inflation has steadily weakened. The BoJ released its minutes from the March meeting last week, and policymakers focused on consumer inflation, which remains well below the central bank's target of two percent. The minutes indicated that the BoJ will closely track consumer prices, but in the meantime will continue with its quantitative easing scheme, in which the central bank purchases JPY 80 trillion per year. The BoJ's prescription for curing weak inflation is to continue its ultra-accommodative monetary policy, so we're unlikely to see policymakers contemplate tightening policy unless inflation moves reverses direction and moves upwards.

All eyes are on the Federal Reserve, which holds its monthly policy meeting on Wednesday. A rate hike is extremely unlikely, with the CME Group pricing in a hike at just 5%. This means that the markets will be focusing on the rate statement and the views of policymakers concerning economic conditions. The Fed has two key goals which have been achieved, namely full employment and an inflation rate of 2%. One area of concern which policymakers have circled is the Fed's balance sheet, which stands at $4.5 trillion. The minutes of the March meeting stated that policymakers want to start reducing this figure before the end of 2017, so the markets will be looking for another reference to the balance sheet in the rate statement or the minutes of the meeting. The markets are fairly confident that the Fed will press the rate trigger in June, as the odds for a hike have improved to 63%. If the rate statement is more hawkish than expected, we could see these odds increase.

Eurozone Q1 GDP Meets Expectations

Eurozone Q1 GDP expanded 0.5 percent in Q1 (not annualized), matching the consensus forecast. While the Eurozone appears to be on solid footing, economic growth is not likely to break out any time soon.

Steady as She Goes

Data released this morning revealed that GDP in the Eurozone expanded 0.5 percent in Q1 (2.0 percent annualized) and is up 1.7 percent from a year ago (top chart). This now marks the ninth consecutive quarter in which the year-over-year growth rate has fallen in the range of 1.5 percent to 2.0 percent. Although a breakdown of GDP into its demand components is not yet available, inferences can be made from the monthly data.

Looking at spending patterns, it is likely that growth in personal consumption contributed positively to the headline figure. Retail sales, by volume, were up 0.2 percent in the first two months of 2017 compared to the Q4 average. Likewise, car registrations have trended higher recently and have eclipsed the 900K mark per month for the first time since January 2010 (middle chart). Export volumes are also starting to trend higher, reaching 3.0 percent growth in January, on a year-over-year basis, for the first time since May 2015. The monthly data, although not jawdropping, is consistent with a gradual expansion that is becoming increasingly self-sustaining.

Perhaps the greatest threat to continued economic improvement in the Eurozone is the French Presidential election on May 7. However, if Emmanuel Macron, the candidate of the centrist En Marche! party is elected president, as is widely expected, then a downside risk to the French economy, and the Eurozone will have faded.

With GDP growth in the Eurozone relatively tame, it is no surprise that CPI inflation has been somewhat subdued (bottom chart). The overall rate of inflation currently stands just below 2 percent. Although the core rate of inflation is lower, it did jump to 1.2 percent in April from 0.7 percent in March. On Thursday of last week, the European Central Bank (ECB) held a regularly scheduled policy meeting in which the Governing Council kept its main policy rates unchanged, which was universally expected. In the subsequent press conference, ECB President Draghi stated that risks to the Eurozone outlook "are still tilted to the downside." The Governing Council did, however, acknowledge that risks were "moving toward a more balanced configuration."

In our view, the ECB will continue to buy €60 billion worth of bonds each month for the next few months. However, our expectation is that at some point this summer, the Governing Council could announce plans to "taper" its bond purchases further if the economic outlooks remains upbeat and/or inflation continues to trend higher. Against the backdrop of the Federal Reserve, which is expected to hike rates two more times this year, and the ECB, which is likely to remain on hold, our currency strategy team looks for the euro to depreciate modestly against the dollar in coming months.

Trade Idea: EUR/GBP – Stand aside

EUR/GBP - 0.8445

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Euro’s retreat after yesterday’s bounce to 0.8485 has retained our view that further consolidation would be seen and weakness to 0.8400-05 cannot be ruled out, however, break there is needed to signal the rebound from 0.8312 has ended, bring further fall to 0.8370-75 but support at 0.8351 should remain intact, bring another rebound later.

On the upside, above said resistance at 0.8485 would bring a stronger rebound to 0.8505 but break of indicated resistance at 0.8531 is needed to add credence to our view that a temporary low has been formed at 0.8312 and extend the rebound from there for retracement of recent decline to 0.8550, however, reckon resistance at 0.8580 would limit upside and 0.8600-10 would hold from here. As near term outlook is mixed, would be prudent to stand aside in the meantime.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

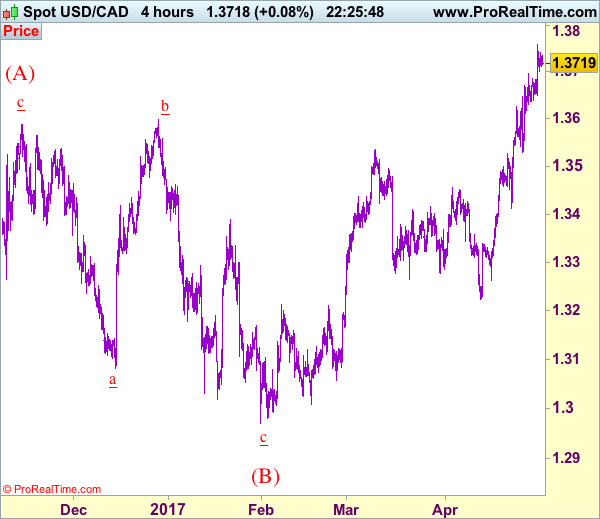

Trade Idea: USD/CAD – Buy at 1.3600

USD/CAD - 1.3725

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

Original strategy :

Buy at 1.3600, Target: 1.3750, Stop: 1.3540

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.3600, Target: 1.3750, Stop: 1.3540

Position: -

Target: -

Stop:-

As the greenback has maintained a firm undertone after recent rally above 1.3599 resistance, adding credence to our view that recent upmove is still in progress and bullishness remains for further gain to 1.3760-70, however, near term overbought condition should prevent sharp move beyond 1.3800-10 and reckon 1.3840-50 would hold on first testing, risk from there is seen for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy again on pullback as 1.3600 should limit downside. Only below said support at 1.3530 would abort and signal a temporary top is formed instead, risk correction to 1.3500 and later towards 1.3450-60 but support at 1.3411 should remain intact, bring another upmove later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

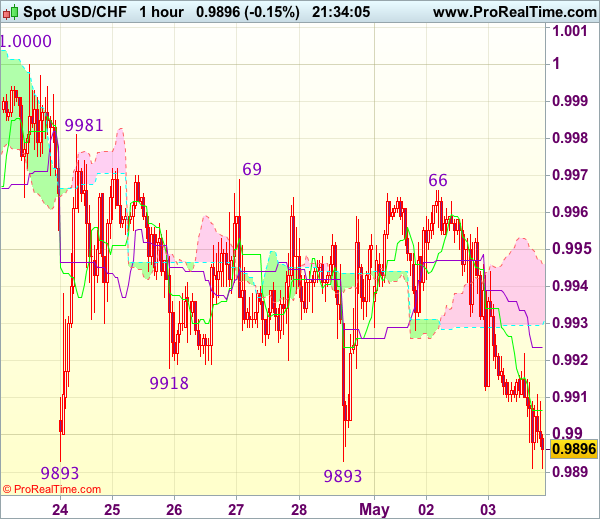

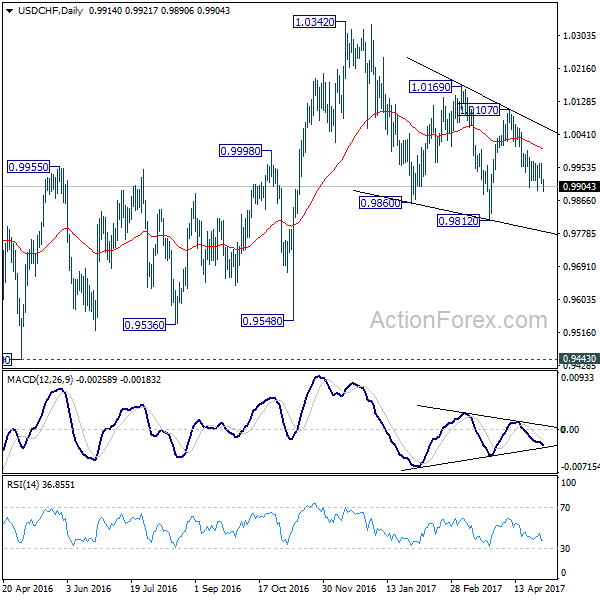

Trade Idea Update: USD/CHF – Stand aside

USD/CHF - 0.9905

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback retreated after faltering below resistance at 0.9969 and retest of indicated strong support at 0.9893 cannot be ruled out, a firm break below there is needed to confirm recent decline from 1.0108 top has resumed and extend weakness to 0.9865-70 (2 times extension of 1.0108-1.0008 measuring from 1.0067), however, support at 0.9831 would hold from here, bring rebound later.

If said support at 0.9893 continues to hold, then further choppy trading within 0.9893-0.9981 range would take place and another bounce to 0.9966-69 cannot be ruled out but said upper range at 0.9981 should limit upside, bring retreat. Only a break of 1.0000-08 resistance would confirm a temporary low has been formed at 0.9893, bring retracement of recent decline to 1.0025-30 (61.8% Fibonacci retracement of 1.0108-0.9893) but price should falter well below resistance at 1.0067. As near term outlook is still mixed, would be prudent to stand aside for now.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.74; (P) 112.02; (R1) 112.27; More....

USD/JPY rises further to as high as 112.47 so far today and intraday bias remains on the upside. As noted before, corrective fall from 118.65 should have completed with three waves down to 108.12 already. Break of 115.49 will resume larger rally from 98.97 to 125.85 high. On the downside, break of 110.86 will bring lengthier consolidation before staging another rise.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

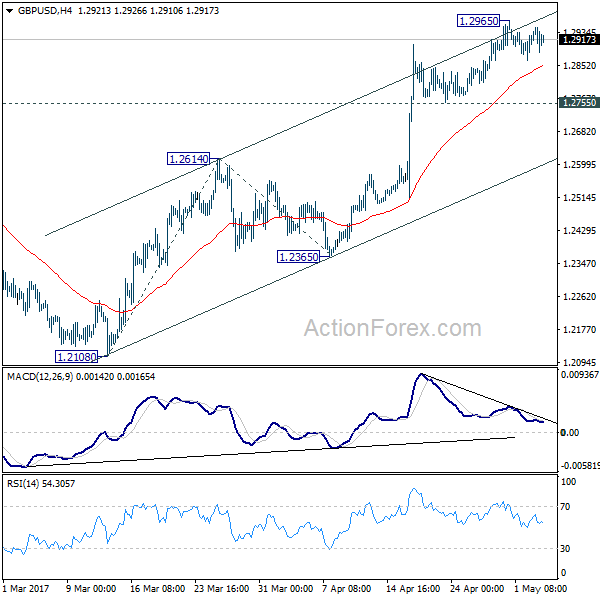

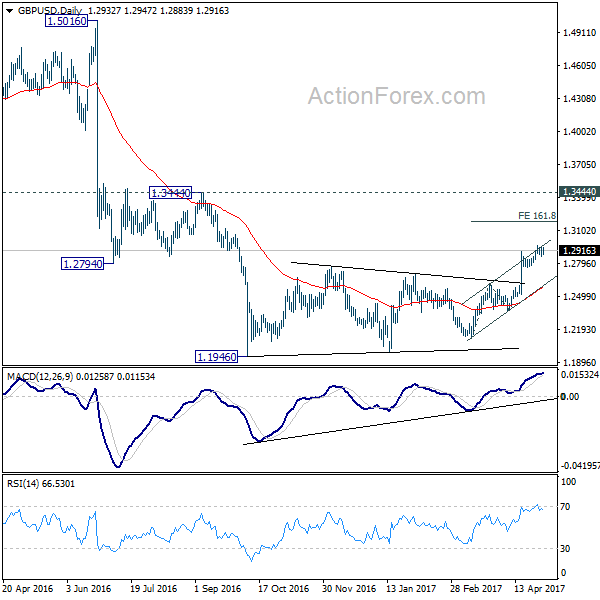

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2888; (P) 1.2913; (R1) 1.2963; More...

GBP/USD continues to engage in consolidative trading below 1.2965 temporary top. Intraday bias remains neutral at this point. With 1.2755 support intact, further rise is expected. Break of 1.2965 will target 161.8% projection of 1.2108 to 1.2614 from 1.2365 at 1.3184. At this point, price actions from 1.1946 are still interpreted as a correction pattern. Therefore, we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2755 minor support will turn bias to the downside. Further break of 1.2614 resistance turned support will now indicate near term reversal.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

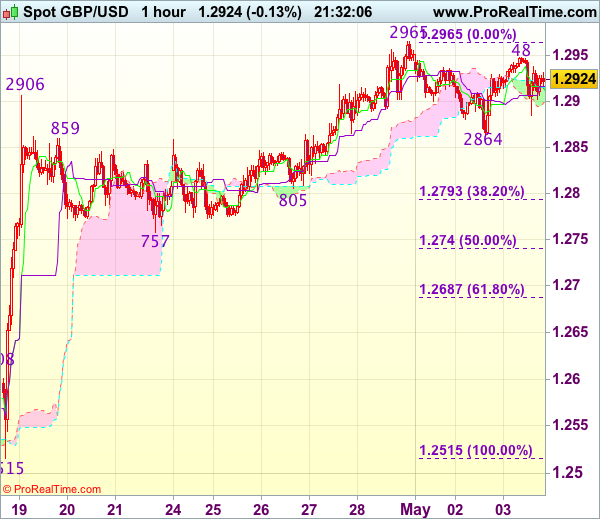

Trade Idea Update: GBP/USD – Buy at 1.2790

GBP/USD - 1.2912

Original strategy :

Buy at 1.2790, Target: 1.2910, Stop: 1.2755

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2790, Target: 1.2910, Stop: 1.2755

Position : -

Target : -

Stop : -

Although cable rebounded to 1.2948, the subsequent retreat after faltering below resistance at 1.2965 has retained our view that further consolidation below this level would be seen and another corrective fall to 1.2864 support is likely, below there would bring retracement of recent rise to 1.2840-45, then towards support at 1.2805 but reckon downside would be limited to 1.2790-95 (38.2% Fibonacci retracement of 1.2515-1.2965) and bring another rise later. Above 1.2948 would bring retest of 1.2965, break there would confirm upmove has resumed for headway towards 1.2990-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance).

In view of this, would not chase this rise here and would be prudent to buy cable on further subsequent pullback as downside should be limited to 1.2790-95. A drop below previous support at 1.2757 would abort and signal top is formed instead, bring correction to 1.2740 (50% Fibonacci retracement of 1.2515-1.2965) first.

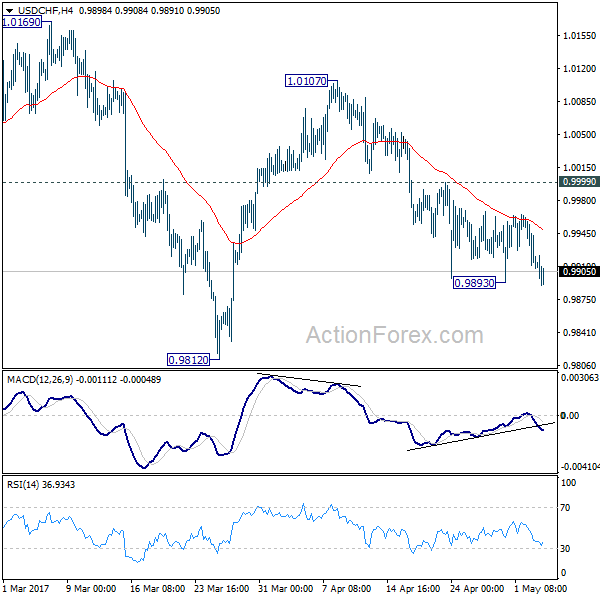

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9897; (P) 0.9930; (R1) 0.9948; More.....

Intraday bias in USD/CHF remains neutral for the moment. As 0.9999 resistance stays intact, deeper decline is still mildly in favor. Below 0.9893 will target 0.9812 and below to extend the correction from 1.0342. But break of 0.9812 should be brief and we will look for bottoming signal below there. On the upside, above 0.9999 minor resistance argues that fall from 1.0107 is finished, with bullish convergence condition in 4 hour MACD. In that case, intraday bias will be flipped back to the upside for 1.0107 resistance first.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

Trade Idea Update: EUR/USD – Stand aside

EUR/USD - 1.0910

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the single currency rebounded after holding above support at 1.0883, break o indicated resistance at 1.0951 (last week’s high) is needed to signal recent upmove from 1.0340 low has resumed for headway to 1.0975-80 and possibly towards 1.1000 which is likely to hold on first testing due to loss of momentum.

In view of this, would not chase this rise here, below 1.0883-88 support would prolong consolidation below said resistance at 1.0951, bring correction towards support at 1.0851 but price should stay above 1.0821 support, bring another rise later. As near term outlook is still mixed, would be prudent to stand aside in the meantime.