Sample Category Title

Elliott Wave View: Nikkei Ending Impulsive 5 Waves

Short term Elliott Wave view in Nikkei ( NKD_F) suggests that the decline to 4/16 low (18255) ended primary wave ((4)). Up from there, the rally is unfolding as an impulse Elliott wave structure where Minute wave ((i)) ended at 18590, Minute wave ((ii)) ended at 18315, Minute wave ((iii)) ended at 19355, and Minute wave ((iv)) ended at 19170 low. Near term index has reached the minimum extension area in Minute wave ((v)) already, however another push higher towards 19579 area can be seen before index ends cycle from 4/17 lows in Minor wave A. Afterwards index is expected to see a pullback in 3, 7 or 11 swings within Minor wave B before further upside is seen. We don’t like selling the proposed pullback and expect buyers to appear again once Minor wave X pullback is complete in 3, 7, or 11 swing provided that pivot at 4/16 low (18255) remains intact.

Nikkei 1 Hour Elliott Wave Chart

EUR/JPY Targeting Resistance At 123.31, EUR/GBP Trading Sideways, EUR/CHF Failed To Break Key Resistance.

EUR/JPY Targeting resistance at 123.31.

EUR/JPY's buying pressures are there. Key resistance area given around 122.00 has been broken. Strong resistance stands at 123.31 (27/01/0217 high). Major support is given at 114.90 (18/04/2017low). Expected to see further increase.

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Trading sideways.

EUR/GBP is trading mixed. The technical structure remains negative as long as the resistance at 0.8596 holds. Expected to show continued weakness until resistance given at 0.8304 (05/12/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

EUR/CHF Failed to break key resistance.

EUR/CHF has bounced back lower. Despite the sharp increase and the recent bullish breakout which is very likely psychological, we believe that the medium-term pattern suggests us to see at some point renewed bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low).

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

Technical Outlook: Gold Spot – Bears Found Footstep At 200SMA, Fed Statement In Focus

Spot Gold maintains negative tone as dollar is firmer on expectation that the Fed may raise interest rates in June. Gold is sensitive to the US rate changes and is eyeing comments from Fed after two day policy meeting ends today, for more clues about possible action in June.

The price is holding near three-week low for the second day, as 200SMA offered solid support at $1252 and so far contained bear-leg from $1295 (17 Apr high).

Gold price is expected to remain within narrow range until release of FOMC statement which is expected to give fresh direction signals.

Hawkish tone from Fed would put gold price under fresh pressure and break below 200SMA would open next layers of supports at $1247/46 (rising 55SMA / 50% retracement of $1197/$1295) and $1241 (bull-trendline connecting lows at $1122/97).

Stronger bearish acceleration may extend towards $1234 (Fibo 61.8% of $1197/$1294 upleg).

Conversely, softer tone from Fed that may signal June rate hike on hold, would boost the yellow metal’s price for retest of pivotal barriers at $1267/$1270 (daily Kijun-sen / Tenkan-sen lines) respectively and shift near-term focus higher on break.

Res: 1257, 1260, 1267, 1270

Sup: 1252, 1247, 1246, 1241

Market Update – European Session: Markets Await The Fed, Euro Zone Q1 GDP In-Line

Notes/Observations

Fed widely expected to keep interest rates unchanged today with focus on language for its next move in June

Euro Zone Q1 GDP data in-line with upward back quarter revision

Overnight:

Asia:

PBoC will prevent liquidity from fluctuating beyond tolerance level to create appropriate monetary environment. China is unlikely to loosen monetary policy, while significant tightening is also unnecessary

Europe:

ECB's Nouy (SSM Chief): concerned about a race to the bottom among regulators following Brexit; ECB will not compromise its high standards

Americas:

President Trump and Russia President Putin agree in phone discussion that all parties must do all they can to end violence in Syria

Energy:

Weekly API Oil Inventories: Crude: -4.2M v +0.9M prior; (largest draw since Jan 18th 2017)

Russia govt reportedly favors extension of OPEC deal by six months

Economic Data

(TR) Turkey Apr CPI M/M: 1.3% v 1.3%e; Y/Y: 11.9% v 11.7%e; CPI Core Y/Y: 9.4% v 9.9%e

(DE) Germany Apr Unemployment Change: -15K v -11Ke; Unemployment Rate: 5.8% v 5.8%e

(UK) Apr Construction PMI: 53.1 v 52.0e (8th month of expansion)

(EU) Euro Zone Q1 Advance GDP Q/Q: 0.5% v 0.5%e; Y/Y: 1.7% v 1.7%e

Fixed Income Issuance:

(IN) India sold total INR140B vs. INR140B indicated in 3-month and 6-month Bills

(DK) Denmark sold total DKK2.24B in 2021 and 2027 bonds

(SE) Sweden sold total SEK2.5B vs. SEK2.5B indicated in 2023 and 2028 Bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 -0.1% at 3573, FTSE -0.3% at 7226, DAX -0.2% at 12481, CAC-40 -0.3% at 5287, IBEX-35 -0.1% at 10810, FTSE MIB -0.2% at 20689, SMI 0.0% at 8873, S&P 500 Futures -0.2%]

Market Focal Points/Key Themes European Indices trade slightly lower across the board pausing from the recent run up, with slightly underwhelming results from Apple, weighing on sentiment. Hugo Boss shares one of the leading decliners in Europe following their results with 3% decline in LFL sales in own retail stores said to weigh on the stock, and UK home builder Galliford Try down sharply after taking £98M in charges. Another busy earnings day in the US with notable earners including Time Warner, Sprint and Reynolds American.

Equities

Consumer discretionary: [Galliford Try [GFRD.UK] -9% (trading update), Halfords [HFD.UK] -3.3% (CEO steps down), Hugo Boss [BOSS.DE] -5.2% (Earnings), JD Weatherspoons [JDW.UK] +2.6% (Trading update)]

Consumer Staples: [Sainsbury's [SBRY.UK] -2.5% (Earnings)]

Materials: [Centamin [CEY.UK] -4.5% (Earnings)]

Industrials: [Volkswagen [VOW3.DE] -1.0% (Earnings)]

Financials: [Allianz [ALV.DE] +0.6% (prelim Q1), BNP Paribas [BNP.FR] +0.5% (Earnings)]

Technology: [Eltel [ELTEL.SE] -12% (Earnings, rights issue, CFO to step down)]

Healthcare: [Fresenius SE [FRE.DE] +3.4% (Earnings), Novo Nordisk [NOVOB.DK] +5% (Earnings)]

Speakers

Brexit Min Davis: Brexit bill would be a matter of negotiation; would be no bill if UK walked away without an agreement with EU. UK would not pay €100B EU exit bill

EU's Barnier unveiled the draft negotiating mandate for Brexit talks and noted that EU citizens in Britain who lived there for 5 years should have right to permanent residence. Britain must honor its share of obligations undertaken as a EU member. Britain's obligations should cover liabilities, contingent liabilities and costs related to moving agencies out of Britain

Chancellor Hammond reiterated view that economic risks and uncertainty remain in the country

China Foreign Ministry called for calm and restraint on all sides after a US bomber flew over Korean peninsula as part of joint exercises with South Korea

China FX Regulator SAFE: Govt to intensify crackdown on Forex violations

Currencies

FX relatively quiet with the USD steady ahead of the FOMC rate decision. Fed is widely expected to keep interest rates unchanged at the end of its two-day policy meeting on Wednesday, but traders will be looking to see whether the central bank downplays the recent soft patch in the economy to leave the door open for a move next month. Currently markets are pricing approx. 70% for a move in June.

EUR/USD was holding above the 1.09 level but holding below last week's 5-month high of 1.0950. Little reaction to the in-line GDP data for the Euro Zona

GBP/USD was steady despite a beat on its PMI Construction data. Pair holding above the 1.29 handle just ahead of the NY morning.

USD/JPY steady at 112.20 area

Fixed Income

Bund futures trade at 161.76 down 2 ticks falling slightly lower following light participation as cash Treasuries were closed in Asian hours due to Japan holiday. The German curve trade is flat ahead of German 2027 Bund auction. A break of 161.54 support level could see lows target 161.26 followed by 160.15. Resistance remains near the 161.88 level followed by 163.54.

Gilt futures trade at 128.15 marginally lower following UK April construction PMI beat. Continuation to the downward trend eyes 127.74 followed by 125.83. Resistance stands at 128.49 then 128.81 followed by 129.14.

Wednesday's liquidity report showed Tuesday's excess liquidity rose to €1.641T a gain of €52.9B from €1.588T prior. Use of the marginal lending facility dropped to €356M from €361M prior.

Corporate issuance saw over $16.7B come to market via 9 issues headlined by Barclays Plc $6.8B 11-year subordinated notes and Constellation Brands $1.5B in a 3-part senior unsecured note offering

Looking Ahead

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month Bills

05:30 (DE) Germany to sell €3.0B in 0.25% Feb 2027 Bunds

06:00 (RU) Russia to sell combined RUB45Bin 2024 and 2026 OFZ bonds

06:00 (IE) Ireland Apr Unemployment Rate: No est v 6.4% prior

06:45 (US) Daily Libor Fixing

07:00 (US) MBA Mortgage Applications w/e Apr 28th: No est v 2.7% prior

07:00 (UK) PM May weekly question time in House of Commons

07:30 (US) Treasury Sec Mnuchin in DC

08:00 (CL) Chile Mar Retail Sales Y/Y: No est v -0.3% prior

08:00 (BR) Brazil Mar Industrial Production M/M: -0.8%e v +0.1% prior; Y/Y: +2.0%e v -0.8% prior

08:15 (US) Apr ADP Employment Change: +175Ke v +263K prior

08:15 (UK) Baltic Dry Bulk Index

09:00 (MX) Mexico Mar Leading Indicators M/M: No est v -0.13 prior

09:45 (US) Apr Final Markit Services PMI: 52.5e v 52.5 prelim, Composite PMI: No est v 52.7 prelim

10:00 (US) Apr ISM Non-Manufacturing Composite: 55.8e v 55.2 prior

10:00(BR) Brazil Mar CNI Capacity Utilization: 77.2%e v 77.3% prior

10:30 (US) Weekly DOE Crude Oil Inventories

11:00 (CO) Colombia Mar Exports: $3.1Be v $2.7B prior

14:00 (US) FOMC Interest Rate Decision: Expected to leave Interest Rates unchanged

Trade Idea: GBP/USD – Buy at 1.2770

GBP/USD – 1.2913

Recent wave: Wave V of larger degree wave (III) has ended at 1.1986 and major correction has commenced from there for gain to 1.3000 and 1.3140-50

Trend: Near term up

Original strategy :

Buy at 1.2770, Target: 1.2960, Stop: 1.2710

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.2770, Target: 1.2960, Stop: 1.2710

Position: -

Target: -

Stop:-

As cable has retreated again after faltering below indicated resistance at 1.2965 (last week’s high), retaining our view that a minor top is formed there and consolidation below this level would be seen with initial downside bias for correction to 1.2860-65, then 1.2800-10, however, reckon support at 1.2757 would contain downside and bring another rise later, above said resistance at 1.2965 would confirm recent upmove has resumed and extend gain to psychological resistance at 1.3000 but overbought condition should limit upside and 1.3050 and price should falter below 1.3100. We are keeping our view that the wave c as well as larger degree wave B has ended at 1.2109, hence impulsive wave C has commenced from there with wave i of C ended at 1.2616, follow by a correction to 1.2365 (end of wave ii) and wave iii rally is unfolding, hence further gain to indicated upside targets would be seen.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

On the downside, whilst initial pullback to 1.2845-55 and possibly support at 1.2805 cannot be ruled out, price should stay above support at 1.2757 and bring another rise later. A drop below this level would defer and signal a temporary top is formed instead, risk correction of recent upmove to 1.2700-10 later.

Trade Idea: GBP/JPY – Buy at 142.55

GBP/JPY - 144.85

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term up

Original strategy:

Buy at 142.55, Target: 145.00, Stop: 141.95

Position: -

Target: -

Stop: -

New strategy :

Buy at 142.55, Target: 145.00, Stop: 141.95

Position: -

Target: -

Stop:-

As sterling has maintained a firm undertone after recent rally, adding credence to our bullish count that recent upmove from 135.60 has resumed and upside bias remains for this move to extend further gain to 145.35-40, however, near term overbought condition should prevent sharp move beyond 146.00-10 and reckon 147.00-10 would hold, price should falter well below previous chart resistance at 148.45, bring retreat later.

In view of this, would not chase this rise here and would be prudent to buy sterling on pullback as 142.50-55 should limit downside. Below previous resistance at 142.10-15 would defer and suggest top is possibly formed, bring correction to 141.60-65, then 141.20-25, however, reckon downside would be limited to 140.55-60 and support at 140.10 should remain intact, bring another upmove later.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

Euro Shrugs As Eurozone Preliminary GDP

The euro continues to have a quiet week, as EUR/USD trades just above the 1.09 line in the Wednesday session. On the release front, German Unemployment Claims came in at -15 thousand, beating the estimate of -10 thousand. Eurozone Preliminary Flash GDP remained unchanged in the first quarter at 0.5%, matching the forecast. In the US, the Federal Reserve is expected to maintain interest rates at 0.75%. Other major events include ADP Nonfarm Employment Change and ISM Non-Manufacturing PMI. On Thursday, the US releases unemployment claims, and ECB President Mario Draghi will speak at an event in Switzerland.

The Federal Reserve holds a policy meeting later on Wednesday. A rate hike is extremely unlikely, with the CME Group pricing in a hike at just 5%. This means that the markets will be focusing on the rate statement and the views of policymakers concerning economic conditions. The Fed has two key goals which have been achieved, namely full employment and an inflation rate of 2%. One area of concern is the balance sheet, which stands at $4.5 trillion. The minutes of the March meeting stated that policymakers want to start reducing this figure before the end of 2017, so the markets will be looking for another reference to the balance sheet in the rates statement or the minutes of the meeting. The markets are fairly confident that the Fed will press the rate trigger in June, as the odds for a hike have improved to 63%. If the rate statement is more hawkish than expected, we could see these odds increase.

High unemployment was long the bane of a sputtering Eurozone economy, but the labor situation has improved considerably. The eurozone economy continues to expand, and more growth has meant more jobs and lower unemployment figures. Just a year ago, the eurozone unemployment rate was at 10.3%, but the rate has been steadily decreasing since then. The March release remained unchanged at 9.5%, within expectations. Germany has led the way, with the unemployment rate dropping to 5.9% in February. Unemployment rolls continue to shrink in Germany, and the decline of 15,000 unemployed persons was better than the estimate of 10,000. US employment numbers will also be in the spotlight this week, with ADP Nonfarm Payrolls kicking things off on Wednesday. The indicator is expected to drop sharply to 178 thousand in March compared to 263 thousand a month earlier. On Friday, we'll get a look at wage growth and the official nonfarm payrolls report. If these indicators are not close to the estimates, we're likely to see some movement from the euro.

It's Election Day (again) in France on Sunday, with Emmanuel Macron and Marine Le Pen vying for the next president of France. The euro and European stock markets have been very steady in the second round of the campaign, as opinion polls continue to show a comfortable majority for Macron:

The polling average line looks at the five most recent national polls and takes the median value, ie, the value between the two figures that are higher and two figures that are lower.

Source – BBC

French Election Timeline

May 3 – TV debate between the two remaining candidates

May 5 – [from midnight] Poll blackout

May 7 – Second round of French presidential elections. Last polls close at 19:00 BST / 14:00 EDT, with an exit poll result announced immediately.

May 11 – Official proclamation of the new President.

May 14 – [from midnight] End of Francois Hollande’s mandate

June 11 – First round of legislative elections

June 18 – Second round of legislative elections.

USD/CHF Continued Decline, USD/CAD Bullish Breakout, AUD/USD Bearish Trend.

USD/CHF Continued decline.

USD/CHF is trading mixed. Yet, the volatility is getting higher. The short-term technical structure is turning positive as long as prices remain below the hourly resistance at 1.0171 (07/03/2017). Monitor strong support given at 0.9814 (27/03/2017 low).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Bullish breakout.

USD/CAD has broken resistance level at 1.3700. The pair keeps on pushing higher. Hourly support can be found at 1.3411 (24/04/2017 high) then 1.3353 (20/01/2017 high). Expected to show continued bullish pressures as long as the pair remains above 1.3411.

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Bearish trend.

AUD/USD is back below 0.7500. As long as prices remain below the resistance at 0.7608 (17/04/2017 high), the short-term technical structure is negative. Key resistance stands at 0.7681 (30/03/2017 high). Expected to show further weakness.

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Pausing Above 1.0900, GBP/USD Continued Bearish Consolidation, USD/JPY Breaking Resistance At 112.20.

EUR/USD Pausing above 1.0900.

EUR/USD is trading sideways. Hourly support is given at 1.0852 (27/04/2017 low) then 1.0682 (21/04/2017 base). Stronger support can be found at 1.0494 (22/02/2017 low). Hourly resistance is given at 1.0951 (26/04/2017 high). Expected to show another leg higher towards 1.10.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Continued bearish consolidation.

GBP/USD keeps pushing higher despite ongoing consolidation. Hourly resistance can be found at 1.2966 (30/04/2017 high). The pair has exited the short-term bearish momentum. Hourly support can be found at 1.2757 (21/04/2017 low). An unlikely break of this support would indicate further weakness.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Breaking resistance at 112.20.

USD/JPY keeps on pushing higher. Strong resistance given at 112.20 (31/03/2017 high) has been broken. Closest support can be located at 108.13 (17/04/2017 low). Other key supports lie at a distant 106.04 (11/11/2016 low). Expected to show continued bullish pressures.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

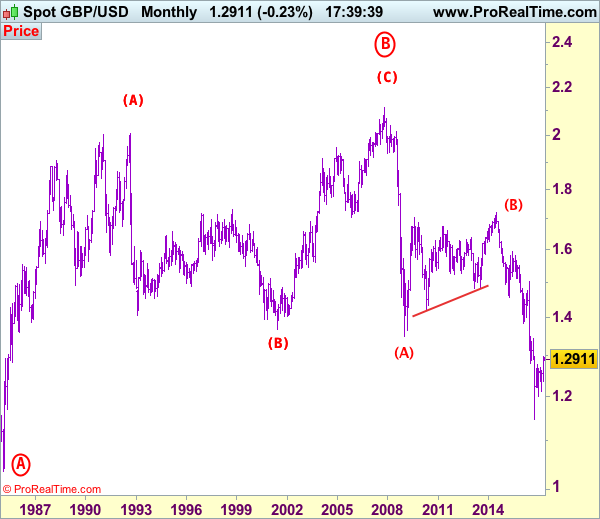

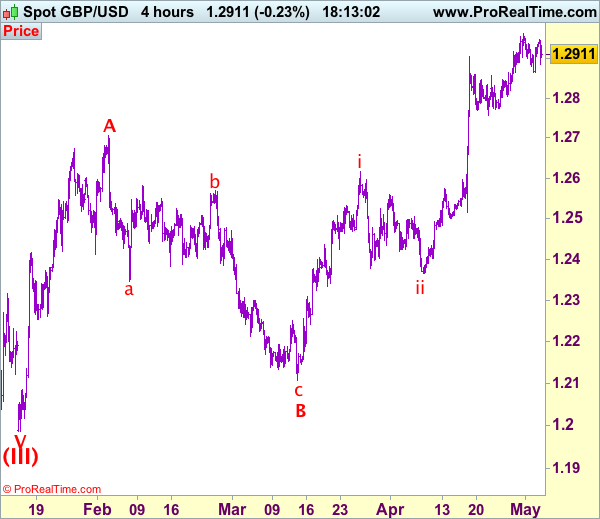

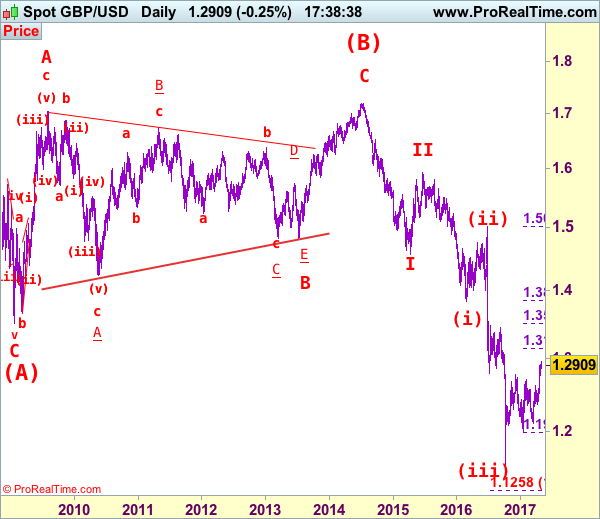

GBP/USD Elliott Wave Analysis

GBP/USD – 1.2911

GBP/USD – Wave 4 is unfolding as an (A)-(B)-(C) and could have ended at 1.7192

Cable has continued trading with a firm undertone after recent rally above indicated previous resistance at 1.2775, adding credence to our view that low has indeed been formed at 1.1986 earlier and bullishness remains for the erratic rise from there to bring retracement of medium term decline, hence further gain to psychological resistance at 1.3000 and then 1.3050-55 would be seen, however, loss of near term upward momentum should prevent sharp move beyond 1.3100 and price should falter below 1.3140-50 (38.2% Fibonacci retracement of 1.5018-1.1986), risk from there has increased for a retreat later.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has possibly ended at 1.7192, below support at 1.4232 would add credence to this count, then further fall to 1.4000 level would follow but reckon downside would be limited to 1.3655 support and price should stay above previous support at 1.3500.

On the downside, whilst initial pullback to 1.2845-50 cannot be ruled out, reckon downside would be limited to 1.2757 support and previous resistance at 1.2706 would turn into support and contain downside, bring another rise later. Only below previous resistance at 1.2616 (tentatively wave i top) would abort and suggest top is possibly formed, risk weakness to 1.2550-60 but break of 1.2500 support is needed to provide confirmation.

Recommendation: Buy at 1.2710 for 1.2960 with stop below 1.2610.

Longer term - Cable's rise from 1.0520 (Feb 1985) to 2.0100 (September 1992) is seen as [A], the decline to 1.3682 is labeled as (B) and (C) wave rally has ended at 2.1162 (9 Nov, 2007) which is also the top of larger degree wave B with circle. The selloff from there is a 5-waver with wave (A) ended at 1.3500 (23 Jan 2009), wave (B) itself is labeled as A: 1.6733, triangle wave B: 1.4813 and wave C as well as top of wave (B) ended at 1.7192 (2014), hence the selloff from there is an impulsive wave (C) with wave I : 1.4566, wave II 1.5930, an extended wave III is unfolding and already exceeded our downside target at 1.3500 and 1.3000, hence weakness to 1.2500 and possibly 1.2000 cannot be ruled out, however, price should stay well above psychological level at 1.0000.