Sample Category Title

Technical Outlook: EURUSD – Near-Term Picture Is Bullishly Aligned, Fed In Focus

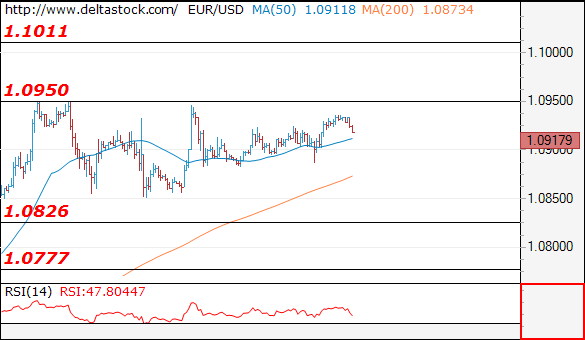

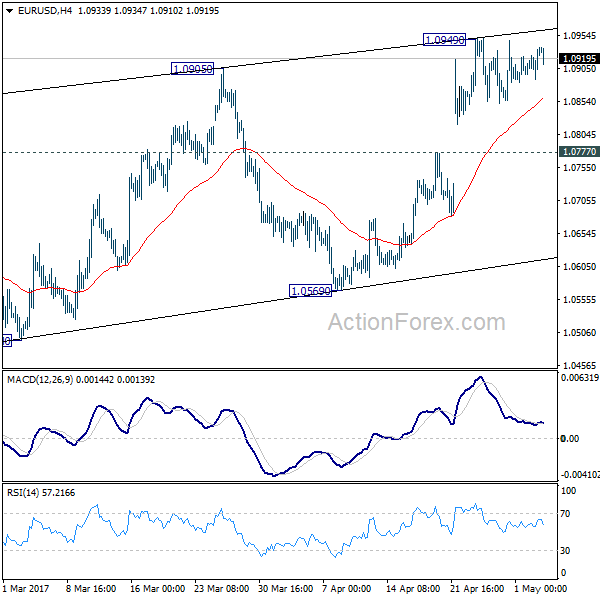

The Euro is holding in the upper side of seven-day 1.0850/1.0950 congestion in early Wednesday, following Tuesday's bullish close. Bullish near-term technicals keep focus at the upside, as multiple bullish crosses of daily MA's (the latest were 10/200 and 20/30) and north-heading 10SMA/thick 4-hr cloud (1.0858/1.0775) continue to underpin.

Eventual break above 1.0950 trigger would open psychological 1.1000 barrier (also 50% of larger 1.1614/1.0339 descend) and Fibo 138.2% projection at 1.1033.

Lows of Mon/Tue at 1.0885 offer initial support, followed by rising 10SMA (currently at 1.0864) and range floor at 1.0850, loss of which would weaken near-term structure and risk test of next pivots at 1.0832 (200SMA) and 1.0804 (Fibo 38.2% of 1.0568/1.0950 upleg). Markets are awaiting the Fed's policy statement, due later today, for more clues about interest rate outlook which would give stronger direction signals for the pair..

Res: 1.0950, 1.1000, 1.1033, 1.1067

Sup: 1.0914, 1.0885, 1.0864, 1.0850

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 10917

Nothing interesting here, as any upward attempt is still capped at 1.0950 and only a violation of the latter will challenge 1.1010 area. Key support lies at 1.0826.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.0950 | 1.0950 | 1.0826 | 1.0780 |

| 1.1010 | 1.1010 | 1.0780 | 1.0676 |

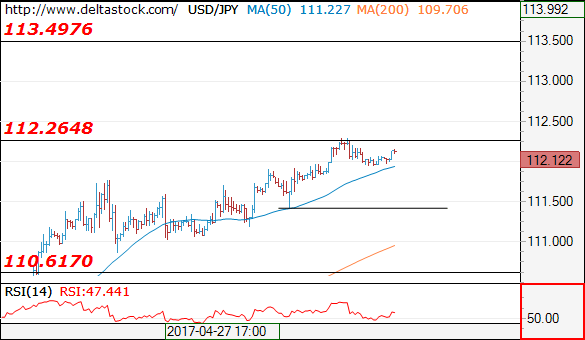

USD/JPY

Current level - 112.12

The overall bias remains positive, for a break through 112.26 resistance, towards 112.90 dynamic hurdle. Crucial on the downside is 111.40 low.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 112.26 | 112.26 | 111.42 | 109.40 |

| 112.90 | 113.50 | 110.60 | 108.12 |

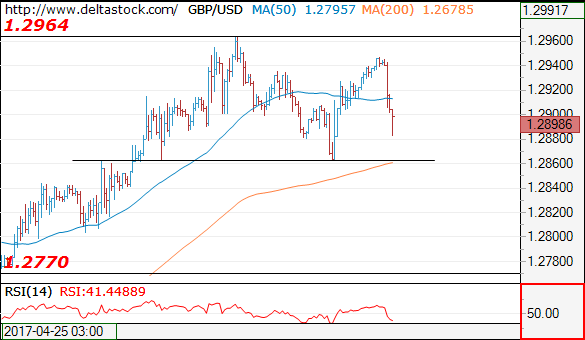

GBP/USD

Current level - 1.2898

Yesterday's failure at 1.2860 support led to a massive rebound all the way up to 1.2945 and the pair is currently getting ready for another test of the mentioned static area. Only a violation of the latter will expose 1.2770.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2945 | 1.3120 | 1.2860 | 1.2610 |

| 1.3000 | 1.3500 | 1.2770 | 1.2510 |

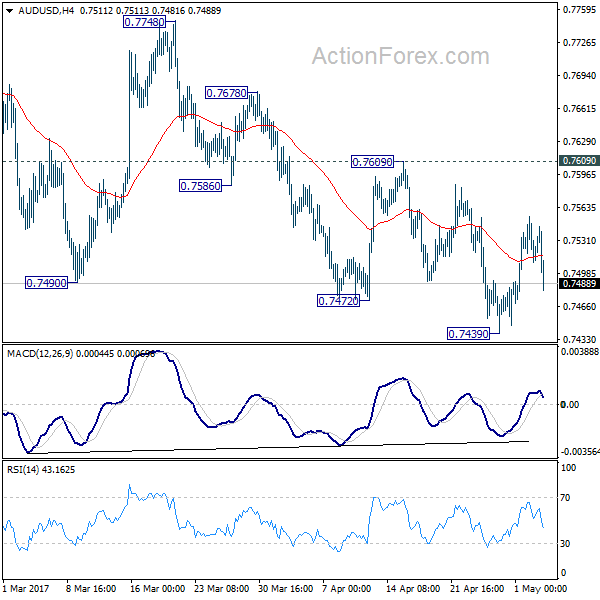

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7479; (P) 0.7509; (R1) 0.7555; More...

AUD/USD is staying in range of 0.7439/7609 and intraday bias remains neutral for the moment. We're favoring the case that rise from 0.7158 has completed at 0.7748 already. And deeper decline is expected. Break of 0.7439 will turn bias to the downside and target a test on 0.7144/7158 support zone. At this point, there is no clear sign of larger down trend resumption yet. Hence we'll be cautious on strong support from 0.7144/58 to contain downside and bring rebound. On the upside, break of 0.7609 will argue that the fall from 0.7748 has completed. In such case, bias will be turned back to the upside for 0.7748 resistance.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8118) and above.

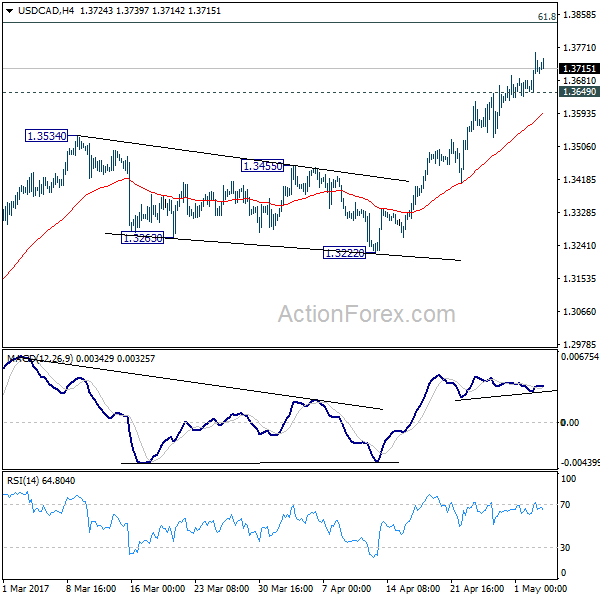

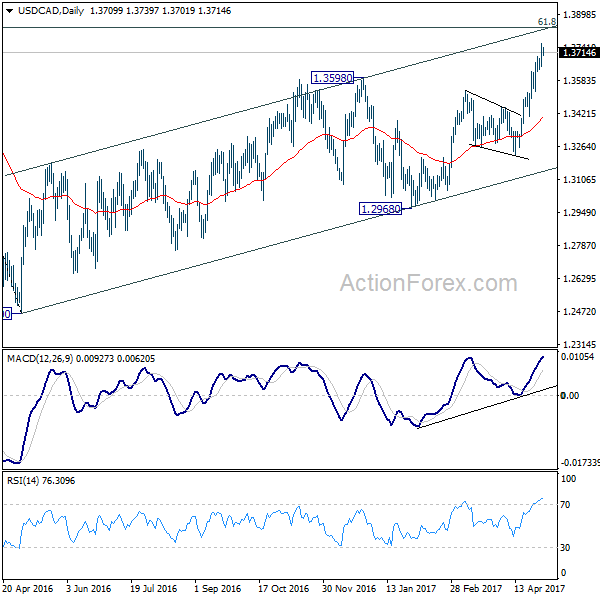

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3652; (P) 1.3704; (R1) 1.3760; More....

USD/CAD's rally continues and reaches as high as 1.3757 so far. Intraday bias remains on the upside for the moment. Current rally is part of the larger rise from 1.2460 and should target next medium term fibonacci level at 1.3838 ahead. We'd be cautious on topping there. On the downside, below 1.3649 minor support will turn bias neutral and bring retreat first.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. However, break of 1.3222 support will argue that the third leg has already started and should at least bring a retest of 1.2460 low. Meanwhile, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

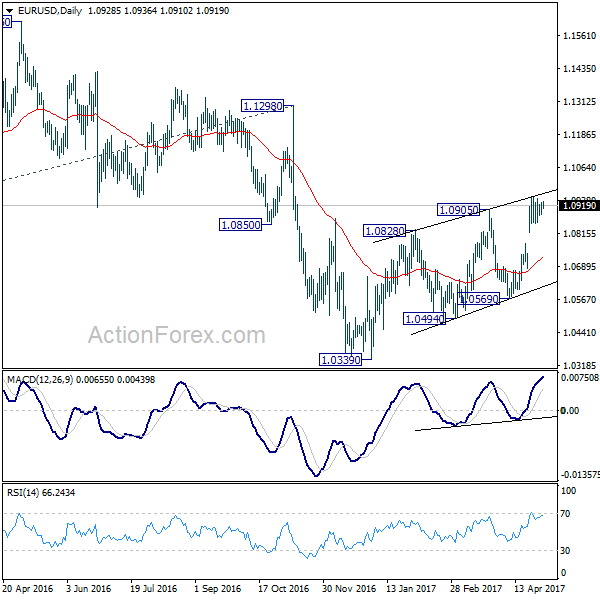

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0902; (P) 1.0917 (R1) 1.0946; More....

EUR/USD continues to be bounded in consolidation below 1.0949 temporary top. And, intraday bias remains neutral at this point. With 1.0777 minor support intact, further rise is expected. But still, choppy rebound from 1.0339 is seen as a correction. Hence we'd look for topping again on next rise. Meanwhile, on the downside, break of 1.0777 will turn turn bias to the downside for 1.0569 support first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. This would also be supported by sustained trading above 55 week EMA.

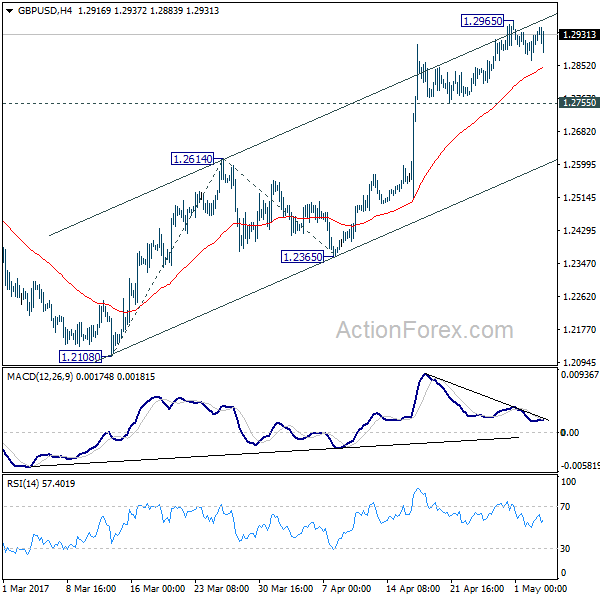

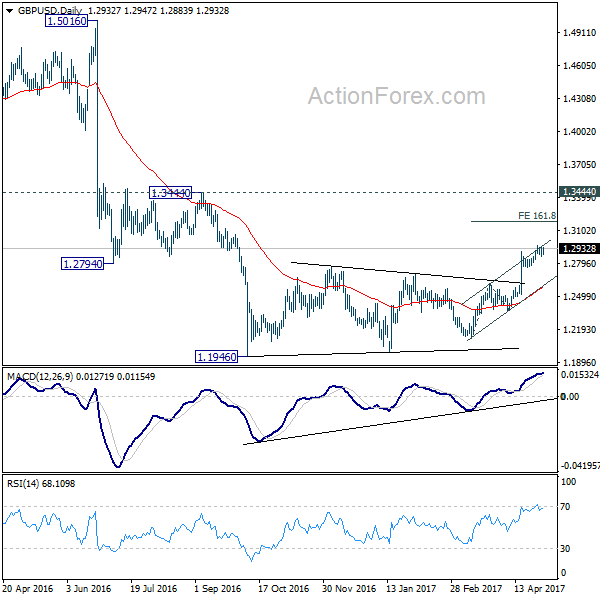

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2888; (P) 1.2913; (R1) 1.2963; More...

GBP/USD continues to engage in consolidative trading below 1.2965 temporary top. Intraday bias remains neutral at this point. With 1.2755 support intact, further rise is expected. Break of 1.2965 will target 161.8% projection of 1.2108 to 1.2614 from 1.2365 at 1.3184. At this point, price actions from 1.1946 are still interpreted as a correction pattern. Therefore, we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2755 minor support will turn bias to the downside. Further break of 1.2614 resistance turned support will now indicate near term reversal.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

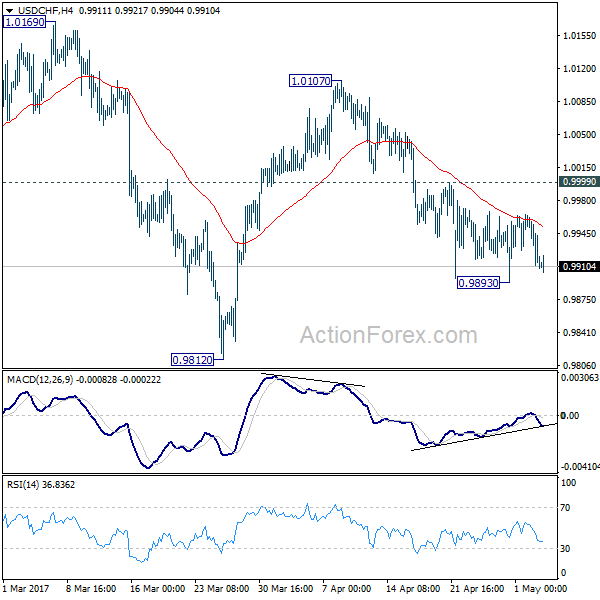

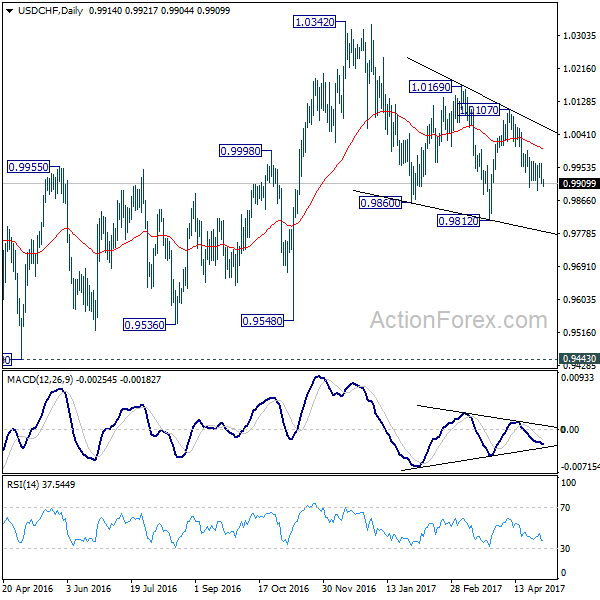

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9897; (P) 0.9930; (R1) 0.9948; More.....

USD/CHF is still staying in consolidation above 0.9893 temporary low. Intraday bias remains neutral for the moment. As 0.9999 resistance stays intact, deeper decline is still mildly in favor. Below 0.9893 will target 0.9812 and below to extend the correction from 1.0342. But break of 0.9812 should be brief and we will look for bottoming signal below there. On the upside, above 0.9999 minor resistance argues that fall from 1.0107 is finished, with bullish convergence condition in 4 hour MACD. In that case, intraday bias will be flipped back to the upside for 1.0107 resistance first.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.74; (P) 112.02; (R1) 112.27; More....

Upside momentum is seen as diminishing in 4 hour MACD after breaching 112.19 resistance. But there is no clear sign of topping in USD/JPY yet. Further rise is expected to 115.49 resistance next. Corrective fall from 118.65 should have completed with three waves down to 108.12 already. Break of 115.49 will resume larger rally from 98.97 to 125.85 high. On the downside, break of 110.86 will bring lengthier consolidation before staging another rise.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

No Shortage Of Economic Events On Wednesday

European equity markets are expected to open relatively flat on Wednesday as we await the release of GDP data from the eurozone, unemployment data for Germany and Spain and the construction PMI for the UK.

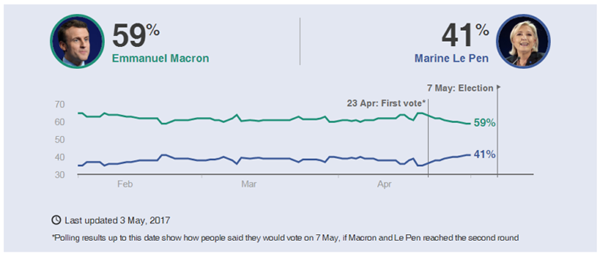

Needless to say, it should be quite a lively morning in Europe, despite the uninspiring open. The eurozone is expected to have grown 0.5% in the first quarter, a decent number given the ongoing challenges facing the region. One challenge that it appears to be overcoming is the rise of populist parties, with the French looking to follow in the footsteps of the Dutch this year in selecting a pro-EU candidate for President. Emmanuel Macron still holds a commanding lead over Marine Le Pen in the polls ahead of voting this Sunday.

The polling average line looks at the five most recent national polls and takes the median value, ie, the value between the two figures that are higher and two figures that are lower.

Source – BBC

French Election Timeline

May 3 – TV debate between the two remaining candidates

May 5 – [from midnight] Poll blackout

May 7 – Second round of French presidential elections. Last polls close at 19:00 BST / 14:00 EDT, with an exit poll result announced immediately.

May 11 – Official proclamation of the new President.

May 14 – [from midnight] End of Francois Hollande's mandate

June 11 – First round of legislative elections

June 18 – Second round of legislative elections.

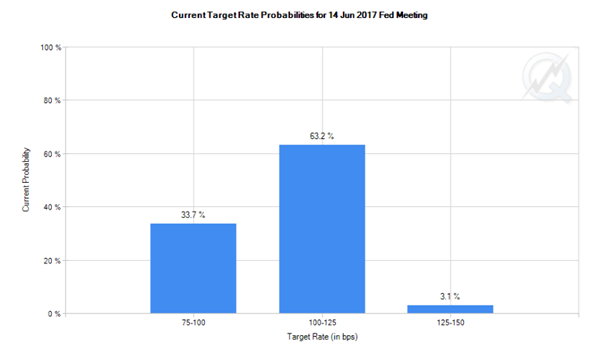

While the Fed decision itself may not surprise anyone – with markets pricing in only a 5% chance of a rate hike this evening – the statement could offer important clues on the central banks intentions at upcoming meetings. In the absence of a press conference with Chair Janet Yellen, the statement is all we have to go off and if the Fed is aiming to raise rates again in June, it may signal its intention to do so.

Fortunately, with markets already pricing in a June rate hike at 66%, the Fed doesn't have to work as hard to manage expectations as it did earlier this year and so any signal may be fairly subtle.

While I expect the central bank to see through the first quarter weakness in the economy, it may refrain from sending a stronger signal in order to give itself room to manoeuvre, should the data not improve between now and the June meeting.

Given the trend that we've seen in recent years of the first quarter disappointing, I would expect to see a similar rebound in the data over the coming months. The jobs data on Friday is expected to report a rebound in hiring following March's surprising increase of only 98,000. Today's ADP release may offer some insight into what we could see here on Friday, although it should be noted that last month it indicated that 263,000 jobs were added in March, not quite in line with the official data. The final services and non-manufacturing PMIs will also be released this afternoon to wrap up a busy session for the US.

UP Down Turnaround

This afternoon we'll also get the latest inventory data from EIA, a day after API reported a 4.15 million barrel drawdown helping oil prices bounce off their lowest levels since November. With Brent crude testing the psychologically significant $50 level, the inventory data could be a big test of sentiment in crude, with a break of this being rather bearish.

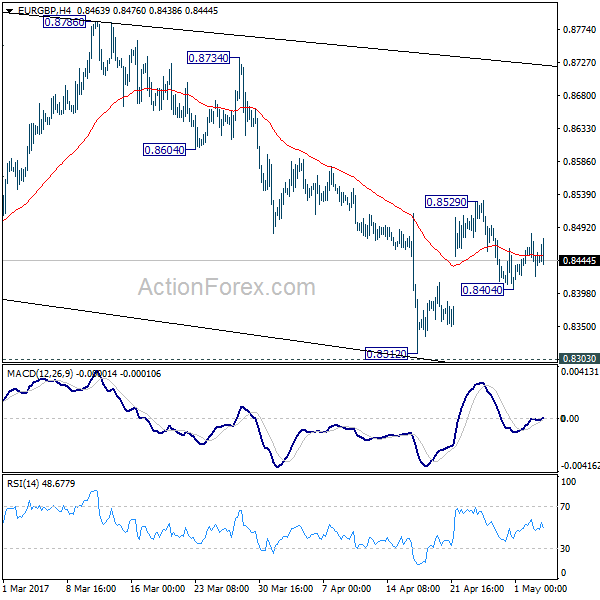

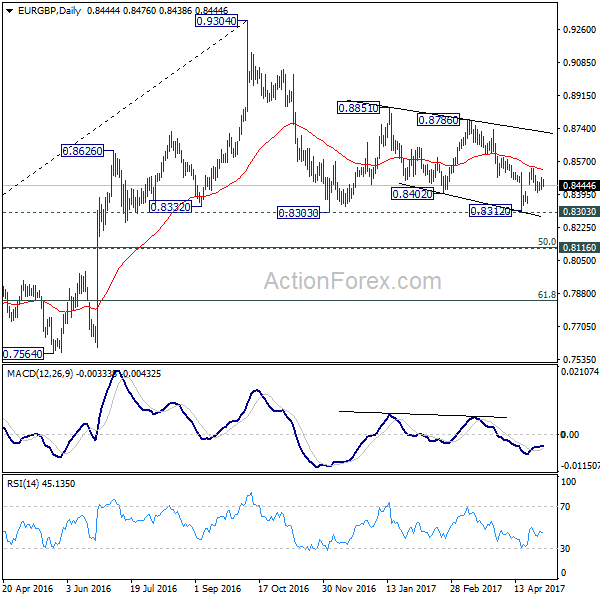

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8430; (P) 0.8444; (R1) 0.8473; More...

EUR/GBP's recovery from 0.8404 was weak and intraday bias is turned neutral first. On the downside, below below 0.8404 will turn focus back to 0.8303 low. Break there will extend the whole corrective pattern from 0.9304. On the upside, above 0.8529 will resume the rebound from 0.8312 towards 0.8786 resistance. Overall, price actions form 0.9304 are seen as a corrective pattern and is extending.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. In case of deeper fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.