Sample Category Title

Trade Idea Wrap-up: USD/JPY – Buy at 111.55

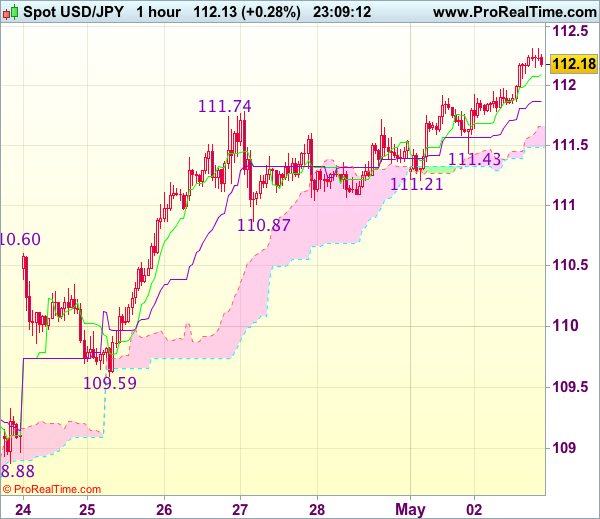

USD/JPY - 112.18

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 112.09

Kijun-Sen level : 111.87

Ichimoku cloud top : 111.66

Ichimoku cloud bottom : 111.48

Original strategy :

Buy at 111.55, Target: 112.55, Stop: 111.20

Position : -

Target : -

Stop : -

New strategy :

Buy at 111.55, Target: 112.55, Stop: 111.20

Position : -

Target : -

Stop : -

As the greenback has surged again after brief pullback and broke above previous resistance at 111.74, adding credence to our view that recent upmove is still in progress and bullishness remains for further subsequent gain to 112.50-60 but near term overbought condition should limit upside to 112.80 and price should falter below 113.00-10, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on subsequent pullback as 111.50-55 should limit downside. Below support at 111.21 (yesterday’s low) would abort and suggest a temporary top is formed instead, bring correction towards 110.87 support.

USD/JPY Testing the 112.20 Neckline

Headlines

European equity markets gained up to 0.75% with the Athens stock exchange outperforming after the reform agreement between Greece and international creditors. US stock markets opened slightly firmer as well.

Growth in the UK's manufacturing sector unexpectedly rebounded in April (from 54.2 to 57.3), confounding expectations of a slide to push the PMI to a three-year high. The forward looking overall new orders balance rose sharply from 56.1 to 60.7.

The eurozone's unemployment rate was steady at 9.5% in March, falling short of economists' expectations it would improve to 9.4%. This kept the rate at its lowest level since May 2009, after a downward trend from 2013′s peak at 12.1%. The final EMU manufacturing PMI was marginally downwardly revised from 56.8 to 56.7.

The ECB will have to hold a discussion next month about its strategy for 2018 and the eventual exit from its ultraeasy monetary policy, ECB Governing Council member Ewald Nowotny said.

Czech PM Sobotka said he will submit the resignation of his government to President Zeman this week. The move follows last week's comments by PM Sobotka that FM Babis may have engaged in "tax tricks or even tax evasion" as he built his empire, allegations that the minister has rejected. The premier said early elections were one option. A regularly scheduled ballot is set for October.

Rates

Greek assets outperform on reform agreement

Global core bonds lost marginally ground today in an uneventful session. This week's back-loaded eco calendar keeps many investors at bay with Apple earnings (tonight), the Fed meeting (tomorrow), US payrolls (Friday) and a potential new vote on a health care bill in US congress lining up. At the time of writing, the German yield curve shifts 0.6 bps (2-yr) to 1.3 bps (10-yr) higher. Changes on the US yield curve vary between +0.4 bps (2-yr) and +0.9 bps (10-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany range between -2 bps and + 4 bps with Greece outperforming (-29 bps).

The Bund opened slightly weaker but trading flat lined afterwards. EMU eco data printed to close to consensus to trigger market reaction and the US eco calendar is empty. The initial move was some catching up with the US after yesterday's European banking holiday. US Treasuries lost ground after US Treasury Secretary Mnuchin repeated that issuing bonds with tenors +30y was a realistic possibility.

Apart from the catch-up move, European stock markets reacted positively on the reform agreement between Greece and international creditors. Greeks assets outperformed today. The Athens stock exchange gained around 3% and Greek spreads vs Germany narrowed up to 40 bps at the front end of the curve.

If the Greek parliament approves the measures agreed with EU/IMF, the Eurogroup can rubberstamp a new aid tranche at its May 22 meeting, avoiding a Greek default in July when €6B bonds are due. Yesterday's deal is also a first necessary requirement to get the IMF financially on board for the third bailout package and to start debt relief talks.

ECB Nowotny said that the ECB will have to hold a discussion about its strategy for 2018 and the eventual exit from its ultra-easy monetary policy at the June 8 meeting. "It is clear that the (asset-purchasing) programme has been and is a success. But on the other hand it is also clear that it must not become a permanent facility... That is the challenge we face," he added. "The longer such a programme continues, the more one must think about its consequences." Nowotny's comments didn't trigger market reaction, contrary to the ECB exit speculation we've witnessed after the March meeting.

Currencies

USD/JPY testing the 112.20 neckline

There were few eco data with potential to move the euro or the dollar. Especially EUR/USD again held a very tight range in the low 1.09 area. Greece's agreement with international creditors and hawkish comments of ECB's Nowotny didn't help the euro. USD/JPY (currently 112.25). tries to regain 112.20 resistance. The pair is supported by an ongoing positive risk sentiment and slightly higher core bond yields

Overnight, Asian markets partially joined the tech-driven rally from the US yesterday. China underperformed as the Caixin manufacturing PMI unexpectedly declined to 50.3 from 51.2. USD/JPY stabilized in the high 111 area, near the recent correction top. EUR/USD still didn't go anywhere in the low 1.09 area.

European equities also started the shortened week with a positive bias. Positive spill-over effects from the US were at play. Greece's agreement with its creditors on additional reforms was also positive for sentiment on European markets. However, it didn't help the euro. EUR/USD showed no dynamics at all and was locked in a very tight range in the low 1.09 area. ECB's Nowotny in a press interview again indicated that the ECB might discuss the future strategy at the June meeting. However, these Nowotny headlines had little impact on the euro. Interest rate differentials between the US and Europe were also little changed. Investors apparently await more important US data/events later this week before engaging in directional bets on the dollar. USD/JPY profited from the rise in core yields and the ongoing risk-on sentiment. The pair returned to the 112.20 resistance/neckline.

There were no important data in the US. The focus for trading over there is currently on the corporate earnings for the first quarter. US indices remain at/within reach of record levels going into the results of Apple after tonight's close. The dollar maintains a cautious bid. EUR/USD trades in the 1.0910 area. The test of USD/JPY 112.20 is ongoing (currently 112.25).

Sterling profits modestly from strong manufacturing PMI

Sterling remained under pressure early in Europe. The harsh comments from EU commission President Juncker on the Brexit negotiation after this weekend's meeting of EU leaders caused some further follow-through sterling selling. EUR/GBP rebounded to the 0.8480/85 area. Mid-morning, the UK April manufacturing PMI came out surprisingly strong at 57.3 from 54.2 in March. The report suggests that the sector profits, at least temporary, from the post-Brexit decline of sterling and from better economic conditions in Europe and at other UK trading partners. Initially, the gains of sterling remained very modest, but the UK currency gradually received a better bid later in the session. EUR/GBP trades currently in the 0.8450/55 area. Cable is again trading in the 1.29 area. Of late, sterling performed quite well, even as there was no important news. In this context, sterling gains to the UK PMI might be seen as slightly disappointing for sterling bulls.

EUR/GBP Rounding Bottom Uptrend Continuation

The EUR/GBP has formed a rounding bottom shaped pattern at the support and is rejecting from W H3 camarilla pivot. 0.8435-50 is POC zone (D L3, ATR pivot, EMA 89, 50.0, trend line) and rejection from POC could target 0.8510. Have in mind that if target is reached, the pair could possibly spike to 0.8550 during next few days. This bullish scenario is negated if the pair drops and stays below 0.8400, rounded bottom low.

Gold Short Term Weakness Likely

Daily chart of Gold-to-Silver ratio above suggests that the ratio is correcting cycle from 2/29/2016 peak (83.68) before the decline resumes later, provided that pivot at 83.68 high stays intact. Short term, cycle from 7/4/2016 low (64.37) is showing a 5 swing incomplete sequence, favoring further upside in the short term. Expect the ratio to extend higher towards 76.55 – 78.68 area to end the rally from 7/4/2016 low, then it should at least pullback in 3 waves if not continue the next leg lower.

As the Ratio is inversely correlated with the underlying physical metals, this suggests that a higher ratio implies a lower XAUUSD and XAGUSD. Thus, we could expect short term weakness in both metals to persist until the Ratio reaches the target of 76.55 – 78.68, then when the Ratio turns lower, both metals can get support and start rallying also.

Elliott Wave Analysis: GBPUSD Undergoing A Possible Reversal

GBPUSD made a sharp bounce in the last couple of hours, which we see as wave B as part of a three wave decline. That said current wave B may see limited upside in the next few trading sessions around the Fibonacci ratio of 61.8, before making a new drop towards wave C).

GBPUSD, 1H

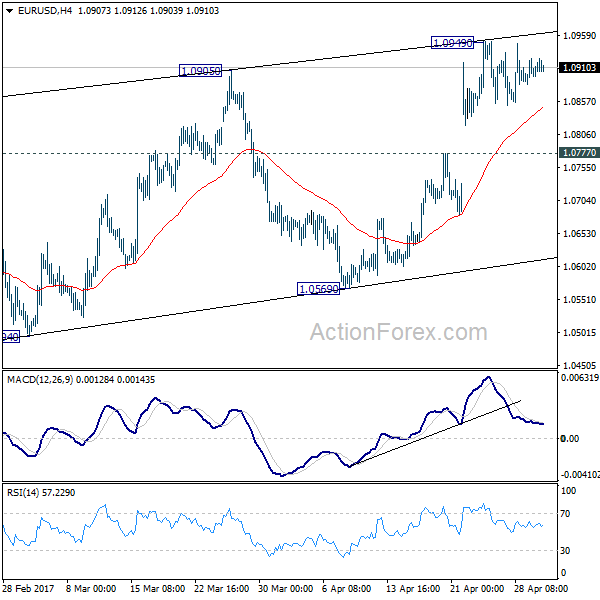

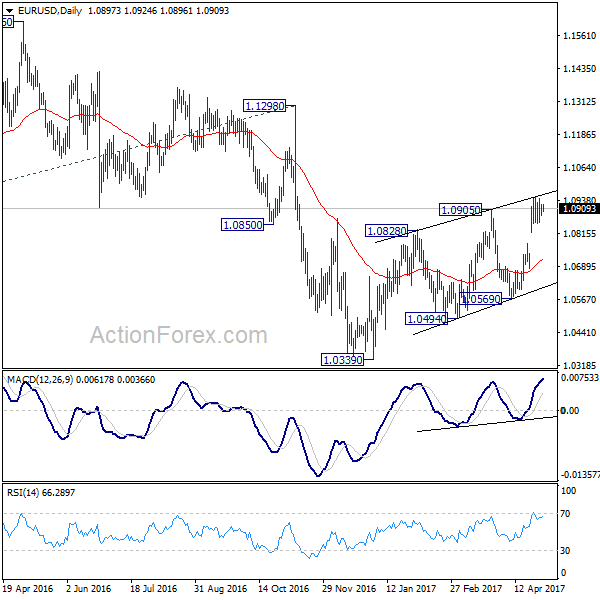

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0880; (P) 1.0901 (R1) 1.0920; More....

Intraday bias in EUR/USD remains neutral as consolidation from 1.0949 temporary top continues. With 1.0777 minor support intact, further rise is still expected. But still, choppy rebound from 1.0339 is seen as a correction. Hence we'd look for topping again on next rise. Meanwhile, on the downside, break of 1.0777 will turn turn bias to the downside for 1.0569 support first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. This would also be supported by sustained trading above 55 week EMA.

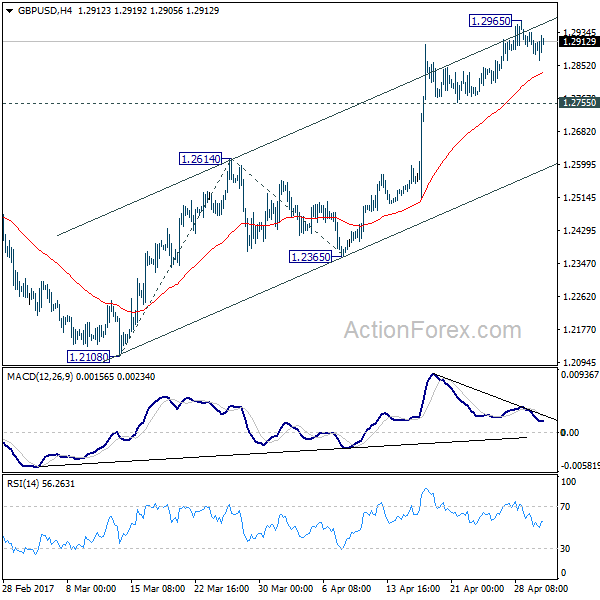

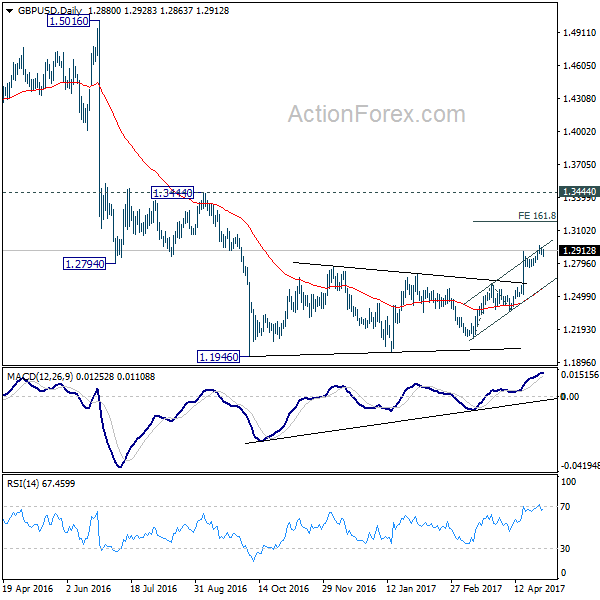

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2863; (P) 1.2903; (R1) 1.2923; More...

Intraday bias in GBP/USD remains neutral as it's staying in consolidation below 1.2965 temporary top. Further rally is expected as long as 1.2755 minor support holds. Break of 1.2965 will target 161.8% projection of 1.2108 to 1.2614 from 1.2365 at 1.3184. At this point, price actions from 1.1946 are still interpreted as a correction pattern. Therefore, we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2755 minor support will turn bias to the downside. Further break of 1.2614 resistance turned support will now indicate near term reversal.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

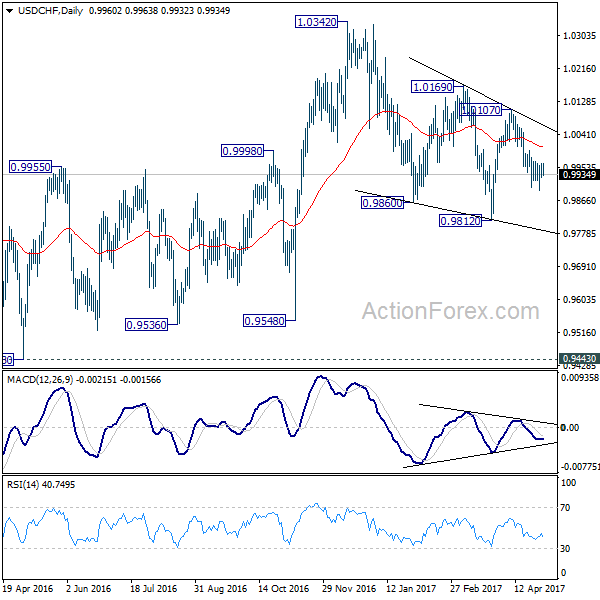

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9939; (P) 0.9952; (R1) 0.9975; More.....

Intraday bias in USD/CHF remains neutral as it's bounded in tight range above 0.9893 temporary low. With 0.9999 minor resistance intact, deeper decline is mildly in favor. Below 0.9893 will target 0.9812 and below to extend the correction from 1.0342. But break of 0.9812 should be brief and we will look for bottoming signal below there. On the upside, above 0.9999 minor resistance argues that fall from 1.0107 is finished, with bullish convergence condition in 4 hour MACD. In that case, intraday bias will be flipped back to the upside for 1.0107 resistance first.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.37; (P) 111.65; (R1) 112.09; More....

USD/JPY rises to as high as 112.30 so far as the rebound from 108.12 resumes. The current development indicates that corrective decline from 118.65 has completed with three waves down to 108.12. Further rally would be seen to 115.49 resistance first. Break will target 118.65 high. On the downside, break of 110.86 minor support will turn bias neutral and bring consolidations first.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

Yen Broadly Lower as US Yield Strengthens, Also on North Korea Concerns

Yen weakens broadly as concerns over North Korea tensions continue. Japan Finance Minister spoke in a conference in California, US, yesterday. He warned that while yen is always "said to be a safe-haven currency", the situation in North Korea made it "extremely unstable". And he emphasized that "we should always think about what the yen would be like if something happens in North Korea." Regarding trade relationship, Aso said Japan and 10 other countries should push ahead with the Trans-Pacific Partnership with the involvement of the US. But he is optimistic that US will eventually find it better to rejoin. He said that "it's not a fact that the U.S. will be able to gain more from bilateral framework than TPP." The Japanese currency is also weighed down by renewed strength in US treasury yields. US Treasury Secretary Steven Mnuchin said yesterday that ultra-long bonds are "something that could absolutely make sense for us at Treasury."

UK PMI manufacturing surged to three year high

UK PMI manufacturing jumped sharply to 57.3 in April, up from 54.2 and well above expectation of 54.0. That's also the highest level in three years. Markit economist Rob Dobson noted that "although only accounting for 10% of the economy, the upturn in the manufacturing sector represents some welcome good news after the sharp slowing in GDP seen in the first quarter." And, "the big question is whether this growth spurt can be maintained, especially given the backdrop of ongoing market volatility and a number of political headwinds such as elections at home and abroad. Other surges seen since the middle of last year have generally proved short-lived, as weak wage growth sapped consumer spending."

Release from Eurozone, unemployment rate was unchanged at 9.5% in March. Eurozone manufacturing PMI was revised down to 56.7 in April. Germany manufacturing PMI was finalized at 58.2, unchanged. France manufacturing PMI was finalized at 55.1, unchanged. Italy manufacturing PMI rose to 56.2, up from 55.7 and beat expectation of 55.9. From Swiss, SVME PMI dropped to 57.4 in April, below expectation of 58.2, down from 58.6.

RBA left cash rate unchanged at 1.50%.

As widely anticipated, RBA left its cash rate, for an 8th meeting, at 1.50% in April. While headline CPI has more or less reached the central bank's target level, the core reading has remained subdued. Policymakers have decided to take more time to gauge the inflation outlook before action. Meanwhile, the unemployment rate has remained elevated while excess capacity in the job market has rendered wage growth weak. More in RBA On Hold, Cautious Over Housing Market Despite Price Growth Slowdown In April.

China data points to loss of momentum

China's latest set of PMI data indicated slowdown in the country's activity growth. The official manufacturing index was reported to have dropped -0.6 point to 51.2 in April, whist the non-manufacturing PMI declined -1.1 points to 54 for the month. The slowdown was broadly based: the 'output' index slipped -0.4 point to 53.8 and the 'new orders' index dropped -1point to 52.3. The 'new export orders' index fell for the first time in 4 months, losing -0.3 point to 50.5, although the three-month moving average remained up. The 'input price' index sank -7.5 points to 51.8. The trend indicates that PPI inflation should have slowed more sharply in April. Recall that the March reading was 7.6% and the February reading was a record higher of 7.8%. The only sub-index that has shown improvement was the 'stock of finished goods' index, which gained 0.9 point to 48.2. More in Chinese Growth Probably Peaked In March, 'Prudent And Neutral' Policy Maintained.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.37; (P) 111.65; (R1) 112.09; More....

USD/JPY rises to as high as 112.30 so far as the rebound from 108.12 resumes. The current development indicates that corrective decline from 118.65 has completed with three waves down to 108.12. Further rally would be seen to 115.49 resistance first. Break will target 118.65 high. On the downside, break of 110.86 minor support will turn bias neutral and bring consolidations first.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Minutes of March 15-16 Meeting | ||||

| 23:50 | JPY | Monetary Base Y/Y Apr | 19.80% | 21.20% | 20.30% | |

| 1:45 | CNY | Caixin Manufacturing PMI Apr | 50.3 | 51.4 | 51.2 | |

| 4:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 7:30 | CHF | SVME PMI Apr | 57.4 | 58.2 | 58.6 | |

| 7:45 | EUR | Italy Manufacturing PMI Apr | 56.2 | 55.9 | 55.7 | |

| 7:50 | EUR | France Manufacturing PMI Apr F | 55.1 | 55.1 | 55.1 | |

| 7:55 | EUR | Germany Manufacturing PMI Apr F | 58.2 | 58.2 | 58.2 | |

| 8:00 | EUR | Eurozone Manufacturing PMI Apr F | 56.7 | 56.8 | 56.8 | |

| 8:30 | GBP | PMI Manufacturing SA Apr | 57.3 | 54 | 54.2 | |

| 9:00 | EUR | Eurozone Unemployment Rate Mar | 9.50% | 9.40% | 9.50% |