Sample Category Title

Trade Idea: EUR/GBP – Stand aside

EUR/GBP - 0.8448

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite intra-day bounce to 0.8485, lack of follow through buying and current retreat has retained our view that further consolidation would be seen and weakness to 0.8400-05 cannot be ruled out, however, break there is needed to signal the rebound from 0.8312 has ended, bring further fall to 0.8370-75 but support at 0.8351 should remain intact, bring another rebound later.

On the upside, above said resistance at 0.8485 would bring a stronger rebound to 0.8505 but break of indicated resistance at 0.8531 is needed to add credence to our view that a temporary low has been formed at 0.8312 and extend the rebound from there for retracement of recent decline to 0.8550, however, reckon resistance at 0.8580 would limit upside and 0.8600-10 would hold from here. As near term outlook is mixed, would be prudent to stand aside in the meantime.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Buy at 1.3600

USD/CAD - 1.3700

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

Original strategy :

Buy at 1.3600, Target: 1.3750, Stop: 1.3540

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.3600, Target: 1.3750, Stop: 1.3540

Position: -

Target: -

Stop:-

As the greenback has continued trading with a firm undertone, adding credence to our view that recent upmove is still in progress and bullishness remains for further gain to 1.3740-50, however, near term overbought condition should prevent sharp move beyond 1.3790-00 and reckon 1.3840-50 would hold on first testing, risk from there is seen for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy again on pullback as 1.3600 should limit downside. Only below said support at 1.3530 would abort and signal a temporary top is formed instead, risk correction to 1.3500 and later towards 1.3450-60 but support at 1.3411 should remain intact, bring another upmove later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

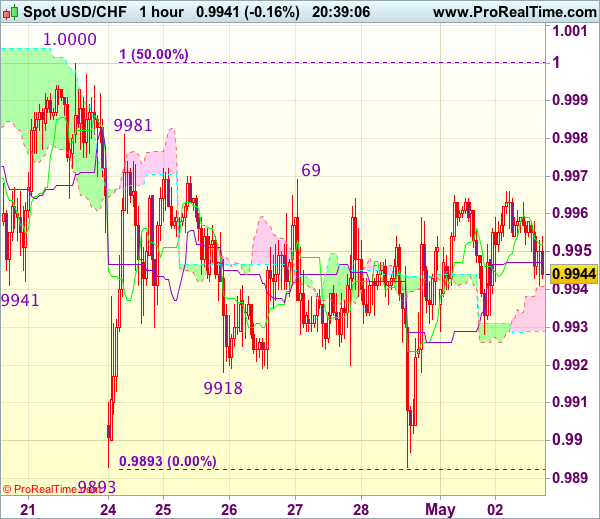

Trade Idea Update: USD/CHF – Stand aside

USD/CHF - 0.9945

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite last week’s late fall to 0.9893, failure to penetrate this last week’s low and the subsequent strong rebound to 0.9961 has retained our view that further choppy trading above said support would take place, above 0.9969 would bring test of resistance at 0.9981 but only break of 1.0000-08 resistance would confirm a temporary low has been formed at 0.9893, bring retracement of recent decline to 1.0025-30 (61.8% Fibonacci retracement of 1.0108-0.9893) but price should falter well below resistance at 1.0067.

On the downside, below 0.9915-20 would bring another test of said strong support at 0.9893 but break there is needed to revive bearishness and signal the decline from 1.0108 top has resumed and extend weakness to 0.9865-70 (2 times extension of 1.0108-1.0008 measuring from 1.0067), however, support at 0.9831 would hold from here, bring rebound later. As near term outlook is mixed, would be prudent to stand aside for now.

Trade Idea Update: GBP/USD – Buy at 1.2790

GBP/USD - 1.2894

Original strategy :

Buy at 1.2790, Target: 1.2910, Stop: 1.2755

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2790, Target: 1.2910, Stop: 1.2755

Position : -

Target : -

Stop : -

As cable has finally retreated after rising to 1.2965 late last week, suggesting consolidation below this level would take place and initial downside risk is seen for correction to 1.2840-45, then towards support at 1.2805, however, reckon downside would be limited to 1.2790-95 (38.2% Fibonacci retracement of 1.2515-1.2965) and bring rebound later. Above 1.2910 resistance would bring test of 1.2937 but break there is needed to signal the pullback from 1.2965 has ended, bring retest of this level first, then towards 1.2990-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance).

In view of this, would not chase this rise here and would be prudent to buy cable on further subsequent pullback as downside should be limited to 1.2790-95. A drop below previous support at 1.2757 would abort and signal top is formed instead, bring correction to 1.2740 (50% Fibonacci retracement of 1.2515-1.2965) first.

Trade Idea Update: EUR/USD – Stand aside

EUR/USD - 1.0912

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the single currency rose to as high as 1.0948 late last week, the subsequent retreat after faltering below last week’s high at 1.0951 has retained our view that further consolidation below this level would be seen and test of support at 1.0883 cannot be ruled out, however, reckon downside would be limited to support at 1.0851 and price should stay above 1.0821 support, bring another rise later.

On the upside, above said resistance at 1.0948-51 would revive bullishness and signal recent upmove from 1.0340 low has resumed for headway to 1.0975-80 and possibly towards 1.1000 which is likely to hold on first testing due to loss of momentum. As near term outlook is still mixed, would be prudent to stand aside in the meantime.

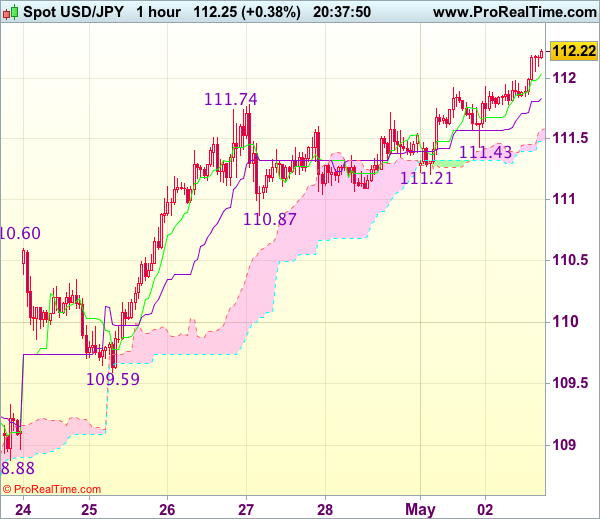

Trade Idea Update: USD/JPY – Buy at 111.55

USD/JPY - 112.22

Original strategy :

Buy at 111.55, Target: 112.55, Stop: 111.20

Position : -

Target : -

Stop : -

New strategy :

Buy at 111.55, Target: 112.55, Stop: 111.20

Position : -

Target : -

Stop : -

As the greenback has surged again after brief pullback and broke above previous resistance at 111.74, adding credence to our view that recent upmove is still in progress and bullishness remains for further subsequent gain to 112.50-60 but near term overbought condition should limit upside to 112.80 and price should falter below 113.00-10, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on subsequent pullback as 111.50-55 should limit downside. Below support at 111.21 (yesterday’s low) would abort and suggest a temporary top is formed instead, bring correction towards 110.87 support.

USDJPY: Targets Further Upside Pressure With Eyes On Key Resistance

USDJPY: The pair continues to hold on to its upside pressure leaving more strength expected. On the downside, support comes in at the 112.00 level where a break if seen will aim at the 111.50 level. A cut through here will turn focus to the 111.00 level and possibly lower towards the 110.50 level. On the upside, resistance resides at the 112.50 level. Further out, we envisage a possible move towards the 113.00 level. Further out, resistance resides at the 113.50 level with a turn above here aiming at the 114.00 level. On the whole, USDJPY looks to recover further higher.

Sterling Dragged Back into the Spotlight

The potential threat of complications and confrontations during Brexit negotiations could rekindle hard Brexit fears and expose Sterling to downside risks this quarter. Some difficulties have already materialized in the early stages of Brexit talks with European Commission President, Jean-Claude Juncker recently commenting that Theresa May is "living in another galaxy", leaving investors anxious. Theresa May repeating her threats of walking away from the European Union without a deal has contributed to uncertainty, and as such Sterling vulnerability could become a dominant theme.

There is a growing suspicion that the European Union may exploit the complicated process of Brexit negotiations to demonstrate to other members that leaving the single bloc may come with heavy consequences. With Brexit developments and ongoing political instability likely to weigh on sentiment, sellers may attack the Pound moving forward.

Focusing on the macro fundamentals, Sterling popped higher during Tuesday's trading session after UK manufacturing surged to a three-year high in April at 57.3. A vulnerable Pound boosted the competitiveness of British products globally, and with manufacturing accounting for 10% of the economy, a solid release was warmly received. Although Sterling could find itself supported in the short term, the upside may be limited, especially when considering how the toxic combination of accelerating prices and Sterling weakness continues to impact consumers.

From a technical standpoint, Sterling/Dollar is bullish in the short term with the breakout above 1.2875 opening a path towards 1.3000. If bulls fail to conquer the 1.3000 level, then prices may descend back towards 1.2875 and 1.2775 respectively.

Stock markets buoyed by earnings

Global stocks crept higher on Tuesday as investors looked beyond the ongoing geopolitical tensions and uncertainty, focusing on stronger corporate earnings. Asian stocks concluded mixed during early trading on Tuesday with some investors on the fence after soft economic data from China rekindled concerns about the global economy. In Europe, equities opened cautiously higher as participants prepared for an explosive data-packed week with the Fed meeting, U.S Jobs data and the French presidential elections in the limelight.

Although Wall Street may find itself supported by earnings, an air of caution permeating the financial markets may cap gains. With uncertainty still lingering over Trump's economic policies, geopolitical tensions in the background, and depressed oil prices weighing on sentiment, the "sell in May and go away" strategy could become attractive to anxious investors.

Dollar losing its attitude

Dollar bears have been unleashed by the recent string of soft economic data from the U.S, leaving investors questioning whether the Federal Reserve will raise U.S interest rates again this year. The Trump rally continues to display signs of exhaustion as scepticism mounts over Donald Trump's ability to move forward with the proposed fiscal spending. Although markets reacted to a big tax announcement last week that offered little detail on the tax reform, it must be kept in mind that support for the proposed reforms does not mean they will be passed through congress.

Much attention may be directed towards the Federal Reserve meeting and U.S jobs data this week which could create some Dollar volatility. While markets widely expect the Federal Reserve to leave interest rates unchanged in May, investors may scrutinize the meeting's tone for any clues or confirmation of a June interest rate increase.

Commodity spotlight - Gold

Gold bulls have succumbed to selling pressure by losing the battle to defend the $1260 support. While the metal could still be supported by risk aversion in the medium to longer term, the break below $1260 may entice sellers to send prices towards $1240. The metal may be subject to volatility this week with the Federal Reserve meeting on Wednesday, and NFP on Friday acting as prime drivers. From a technical standpoint, previous support around $1260 may transform into a dynamic resistance that opens a path towards $1240. In an alternative scenario, a daily break back above $1260 could provide bulls the opportunity to challenge $1280.

AUD/USD Bulls Retreat After Testing Downtrend Resistance

This morning, the Reserve Bank of Australia (RBA) announced interest rates on hold at 1.5%, which was in line with market expectations.

The RBA sees an upswing in the global economy, and foresees the Australian economic growth to increase gradually around 3% over the next couple of years, helped by the rising mining investment and exports of resources.

In terms of labour market, the unemployment rate is expected to drop over time. However, wage growth remains slow.

Overall, the economic outlook is sound, nevertheless, the bullish momentum of the Aussie will likely be restrained due to the concern over the slow wage growth.

AUD/USD has rebounded after hitting the lowest level of 0.7439 since January 12 on April 27.

The RBA's sound economic outlook lifted AUD/USD touching a 1-week high of 0.7555 in early hours of this morning, testing the near-term major downtrend line resistance.

However, the price has retraced as the pressure at the level is heavy.

The 4-hourly Stochastic Oscillator Is heading downward, suggesting further retracement.

The resistance level is at 0.7530, followed by 0.7550 and 0.7560.

The support line is at 0.7510, followed by the psychological level at 0.7500 and 0.7485.

The FOMC meeting will be held on Wednesday May 3. Markets expect the Fed to raise rates in June instead of May. Nevertheless, we might get further clues about the probability of a rate hike in June from Fed Chair Yellen's tone of her speech. The recent weak US economic data might make Yellen's speech less hawkish. Per the CME's FedWach tool, the probability for a rate hike in June is 67.4%.

Be aware that Yellen's speech will likely cause volatility for USD and the USD crosses. With a dovish statement, it will likely weigh on USD and push AUD/USD up. With a hawkish statement, it will likely strengthen USD and weigh on AUD/USD.

Technical Outlook: USDTRY – Bears May Extend To 3.5000

The pair continues to head lower following last week's break below key med-term support at 3.5555 (23 Feb low) and break below pivot at 3.5487 (Fibo 38.2% of 2.9135/2.9414 ascend) which are signaling further extension of corrective phase from 3.9414 (11 Jan record high). Multiple bear-crosses of daily MA's as well as Tenkan-sen/Kijun-sen lines maintain strong downside pressure, which is reinforced by completion of bearish pennant pattern. Further weakness may test psychological 3.5000 support, however, bears could be interrupted by correction on strongly oversold slow stochastic on daily chart, which is so far lacking firmer bullish signal. Falling daily Tenkan-sen offers solid barrier (currently at 1.6019) which should ideally cap and keep intact last week's high at 3.6244 (posted after gap-lower opening).

Res: 3.5553, 3.5850, 3.6000, 3.6244

Sup: 3.5300, 3.5124, 3.5000, 3.4850