Sample Category Title

US Futures Shrug Off Moderate Gains In Europe

- EUR and GBP gain on multi-year highs for UK and eurozone manufacturing PMIs;

- French election to remain in focus ahead of this weekend's vote;

- Fed decision key this week despite rate hike being all but priced out.

US equity markets are on course to open flat on Tuesday following a decent start in Europe where indices are currently posting moderate gains.

Europe has been given a boost this morning by the better than expected April manufacturing PMI data for the eurozone and the UK. The final eurozone PMI release hit a six year high while the UK rebounded from three months of declines to record its fastest growth in three years. Both currencies are making decent gains this morning on the back of the data and could test last week's highs, with both trading near key technical resistance levels. A break of these could spur further gains in the coming weeks.

While traders continue to have one eye on the data, the French election is likely to remain at the forefront of their minds this week, with the second round of voting taking place this weekend. Emmanuel Macron remains the runaway favourite in the polls which is supporting risk appetite at the moment but traders may retain a slightly cautious approach given the experience of last year's voting in the UK and the US.

Earnings season continues to be another key focus for investors and this week we'll also get the latest monetary policy decision from the Federal Reserve as well as the April jobs report. While a rate hike at the meeting tomorrow is all but priced out, the probability of one at the meeting in June is currently just shy of the 70% level that is widely seen as the threshold for such a move. Tomorrow's statement will therefore be very closely monitored in the absence of a press conference from Chair Janet Yellen.

Chinese Growth Probably Peaked In March, ‘Prudent And Neutral’ Policy Maintained

China's latest set of PMI data indicated slowdown in the country's activity growth. The official manufacturing index was reported to have dropped -0.6 point to 51.2 in April, whist the non-manufacturing PMI declined -1.1 points to 54 for the month. The slowdown was broadly based: the 'output' index slipped -0.4 point to 53.8 and the 'new orders' index dropped -1point to 52.3. The 'new export orders' index fell for the first time in 4 months, losing -0.3 point to 50.5, although the three-month moving average remained up. The 'input price' index sank -7.5 points to 51.8. The trend indicates that PPI inflation should have slowed more sharply in April. Recall that the March reading was +7.6% and the February reading was a record higher of +7.8%. The only sub-index that has shown improvement was the 'stock of finished goods' index, which gained +0.9 point to 48.2.

Activity Growth in Small- and Medium- Sized Firms Also Moderated

Separately, the Caixin/ Markit manufacturing PMI fell -0.9 point to 50.3, the lowest point since September, in April. The market had anticipated a modest rise to 51.4. As the accompanying statement suggested, "the sub-indexes of output and new business both fell to the weakest levels since September, while the employment index dropped to the lowest in three months". It added that "the downward pressure on manufacturing gradually emerged in April, with all indicators weakening. The Chinese economy may be starting to embrace a downward trend in the near term as prices of industrial products decline and active restocking comes to an end".

Both reports indicated that activity growth in China has peaked in March. Weakness in trade expansion and the government's tightening in the monetary were likely the causes. Inflationary pressure in the manufacturing sector also eased in April, from the peak in the first quarter of the year. We would get more insight after the trade balance report is released on May 8.

PBOC Trimmed Liquidity Injection in April

In a separate note, PBOC injected RMB590.3B to the market in April, down -18% from the previous month. Of which, RMB495.5B was from the medium-term lending facility (MLF) while the rest from standing lending facility (SLF). Looking into the composition of MLF, RMB 128B was 6-month loan and RMB367.5B was 1-year loan. Outstanding SLF loans were at RMB10.27B at the end of April, down from RMB70B at end-March. This represents a net drain of RMB59.7B. The central bank also injected RMB 83.9B of pledged supplementary lending (PSL) facility to a number of commercial, sending the total of PSL to about RMB2.3 trillion at the end of April, up from RMB2.22 trillion the same period last month. PBOC has been reliant on open market operation, rather than adjustments of interest rate and required reserve ratio, to achieve its monetary policy stance. The overall trend of liquidity injection remains in line with the government's 'prudent and neutral' policy, which aims at cooling the excessive credit growth but not harming economic stability.

Fed In Focus, Risk On

With May Day over, capital markets are back in full swing and despite some weaker than expected economic data in the U.S of late, investors are returning to risky assets.

Global stocks are heading for a fresh high as investors focus on stronger corporate earnings. The yen has extended it losses while Treasury prices maintain its price declines.

Dealers will be focusing on the Fed and the U.S yield curve with the FOMC beginning its two-day policy meet today.

Yesterday, the VIX closed at its lowest level in a decade, which suggests that investor fears are easing, despite North Korea's saber rattling.

1. Global equities trade atop record highs

In Asian overnight, shares rose to near two-year highs as growing optimism over tech industry earnings and easing concerns over North Korea offset softer-than-expected factory readings in China and the U.S.

In Japan, the Nikkei climbed (+0.7%) to a six-week high on earnings optimism, while the broader Topix index rose +0.6% to the highest since March 21.

Note: Japanese markets will be closed for holidays over the next three-days.

In South Korea, the Kospi index advanced +0.7% to trade atop of its six-year high. In Singapore, the Straits Times Index added +0.9%, while in China the Shanghai Composite Index declined -0.4%, following four straight days of gains.

Down-under, the Aussie S&P/ASX 200 Index slipped -0.1%, breaking a seven-day rally, as banks declined.

In Europe, indices are trading higher on generally positive PMI data out of Eurozone. Elsewhere, stronger earning from BP is helping the FTSE to slightly outperform.

U.S stocks are to open little changed (-0.1%).

Indices: Stoxx50 0.1% at 3564, FTSE +0.4% at 7232, DAX 0.1% at 12447, CAC-40 0.3% at 5280, IBEX-35 0.6% at 10776, FTSE MIB 0.5% at 20710, SMI 0.4% at 8852, S&P 500 Futures -0.1%

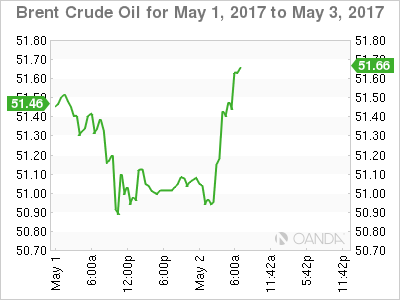

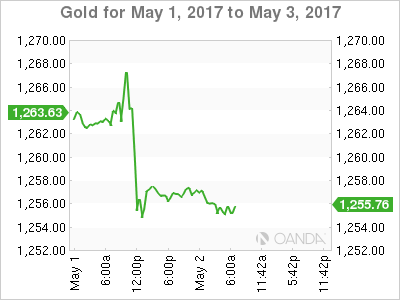

2. Oil prices rise, gold falls

Crude ‘bulls' are getting the better of the “bears” rising production concerns in the U.S, Canada and Libya as oil prices are on the rise ahead of the U.S open, supported by market expectations that OPEC will extend last November's output cut quotas into H2. OPEC is to meet on May 25.

Brent crude oil futures are up +30c at +$51.82 a barrel – the contract hit a one-month low of +$50.45 last week after the restart of two Libyan oilfields – while U.S light crude (WTI) is up +20c at +$49.04 a barrel.

Note: Libya's National Oil Company said yesterday that production had risen above the +760k bpd to its highest in three-years, with plans to keep boosting production. Offsetting some of the market prices losses is data from Russia showing that oil output fell slightly to +11m bpd in April from +11.05m in March.

Gold trades near its three-week lows on surging equities and on the dollar's strength. Bullion prices dropped -1% yesterday to +$1,253.66 an ounce, its weakest since April 11.

3. Global yields back up

A number of factors are boosting demand for U.S treasuries on price pullbacks -investors are sceptical over Trump's capability to push through his fiscal agenda anytime soon and a number of economic releases over the past month have been disappointing.

U.S 10's have backed up +1 bps to +2.33% overnight on market belief that the Treasury department may raise the size of its longer-dated bond issuance from its quarterly refunding release tomorrow – 10-year note and 30-year bonds to increase by perhaps +$2B apiece.

The Fed is to start its two-day policy meeting today, and is widely expected to hold short-term interest rates steady tomorrow after a rate increase in March. Some Fed officials have signalled in recent weeks that the door remains open for the Fed to raise rates again in June. Fed fund futures see a +66% chance for a hike next month.

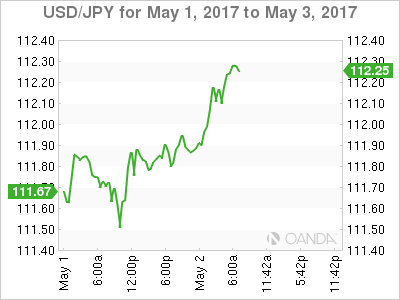

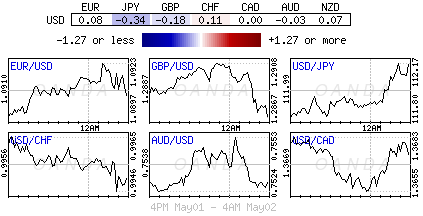

4. Dollar majors trade in narrow range

The dollar majors are trading in a narrow range. The EUR (€1.0910) continues to find support on pullback outright, helped by expectations that Macron will beat far-right candidate Marine Le Pen in this weekend's French presidential elections. Euro GDP data out tomorrow is expected to show the economy picking up.

Sterling falls, with GBP down -0.1% at £1.2877 as U.S Congress reached a deal to avoid a government shutdown helps the dollar. It's off its overnight lows after the U.K manufacturing PMI data beat consensus – 57.3 in April, bouncing from March's four-month low of 54.2.

USD/JPY (¥112.21) is now trading atop its one-month highs, with yen ‘bears' looking for further extensions for the dollar.

Note: The yen remains vulnerable to rising political tensions over North Korea as it is as safe-haven.

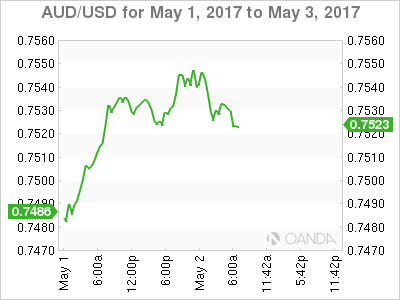

The AUD/USD (A$0.7531) was most volatile overnight, sliding after a disappointing China Caixin Manufacturing PMI (see below), before lifting to its overnight highs after an upbeat RBA policy statement.

Emerging markets FX gains are being supported by optimism that the Fed will ‘not' raise interest rates this week, and that there wont not be any negative surprises from this weekends second round French Presidential election.

5. RBA holds steady, China data disappoints

Overnight, RBA held rates steady at +1.50% as expected, but the policy statement was definitely more upbeat after last month's grim assessment of employment.

Aussie policy makers noted improvement in global growth boosting demand for exports, noted employment was now a bit stronger and forecasted growth reaching +3% over the next few years. As to be expected, they are also anticipating further increase to underlying inflation.

In China, the Caixin Manufacturing PMI came in below estimates at 50.3 vs. 51.3E, which is also its seven-month low.

Analysts noted that slower increases in output and new orders endorsed the decline, along with softer growth in new-orders that forced companies to cut jobs at the fastest pace in four-months. Slowing growth was also felt in the prices components.

Technical Outlook: USDCAD – Signals Of Correction On O/B Studies, Fed In Focus

The pair is holding softer tone on Tuesday, following uninterrupted rally that lasted for seven straight days and peaked at 1.3695 (fourteen–month high).

Fresh boost has been received on break above former tops at 1.3586/96 (14 Nov / 28 Dec 2016 peaks) which also mark the top of thick weekly cloud and now act as supports.

Initial signs of correction are seen on overbought daily RSI / slow stochastic which would generate stronger bearish signal on reversal.

First support at 1.3634 (Monday's low) is still holding with break lower and daily close in red, expected to signal further easing.

Weekly cloud top and former peaks, together with Fibo 38.2% of 1.3409/1.3695 upleg, mark a cluster of strong supports loss of which would signal deeper correction and expose rising daily Tenkan-sen at 1.3552.

With no releases from Canada scheduled, focus will turn towards tomorrow's comments from Fed after policy meeting ends, which are expected to stronger influence performance of the US dollar.

Res: 1.3681, 1.3694, 1.3726, 1.3845

Sup: 1.3634, 1.3585, 1.3552, 1.3518

Market Update – European Session: Greece Moves Closer To Concluding Its 2nd Bailout Review

Notes/Observations

European Manufacturing PMI data remains in expansion territory (beats: UK, Italy, Spain, Sweden, Czech, Poland; misses: Swiss, Russia, Hungary; in-line: France, Germany, Euro Zone)

Greece moves closer to concluding its 2nd bailout review

Risk appetite building momentum aided by declining global headwinds and prospects of an increasing pace of reform in the US; no surprises seen by Fed or in 2nd round of French elections

Wed's FOMC meeting likely to guide markets towards a June rate hike

Overnight:

Asia:

Reserve Bank of Australia (RBA) left its Cash Rate Target unchanged at 1.50% (as expected)

China Apr Caixin Manufacturing PMI registers its 10th straight month of expansion but hits a 7-month low (50.3 v 51.3e)

Japan Fin Min Aso: North Korea is the most urgent matter for Japan; China has capability and capacity to fix situation; Want to eliminate nuclear capability. JPY currency (yen) is vulnerable to rising political tensions over North Korea as it is a safe-haven currency

South Korea Apr CPI data saw annual its pace move back below target for 1st time in 2017 (Y/Y: 1.9% v 2.1%e)

Europe:

Greece Finance Ministry: Negotiators of Greece govt and its creditors said to have concluded an agreement on bailout mandated reforms in Athens. Greece needs to legislate measures before Eurogroup meeting scheduled for May 22nd before any disbursement of loans

Americas:

Treasury Sec Mnuchin: Could take two years to get GDP growth up to 3%; will be achievable and sustainable because of tax and regulatory reform and trade renegotiations. Q1 GDP was weak due to seasonality issues and because the economy is being held back. Will release details of the tax plan as soon as we can, but still working on it with Congress

Economic Data

(IE) Ireland Apr Manufacturing PMI: 55.0 v 53.6 prior (47 straight month of expansion)

(IN) India Apr PMI Manufacturing: 52.5 v 52.5 prior (4th month of expansion)

(RU) Russia Apr Manufacturing PMI: 50.8 v 52.6e (9th month of expansion)

(SE) Sweden Apr PMI Manufacturing: 62.5 v 62.3e

(NO) Norway Apr Manufacturing PMI: 54.7 v 54.3e

(HU) Hungary Apr Manufacturing PMI: 55.9 v 56.5e (16th month of expansion)

(PL) Poland Apr Manufacturing PMI: 54.1 v 53.9e (29th month of expansion)

(TR) Turkey Apr PMI Manufacturing: 51.7 v 52.2e

(ES) Spain Apr Manufacturing PMI: 54.5 v 54.4e

(CH) Swiss Apr PMI Manufacturing: 57.4 v 58.2e

(CZ) Czech Apr PMI Manufacturing: 57.5 v 57.0e (9th month of expansion)

(IT) Italy Apr Manufacturing PMI: 56.2 v 56.0e (8th month of expansion and the highest since Mar 2011)

(FR) France Apr Final Manufacturing PMI: 55.1 v 55.1e (confirmed 7th month of expansion and highest since Apr 2011)

(DE) Germany Apr Final Manufacturing PMI: 58.2 v 58.2e (confirmed its 29th month of expansion

(EU) Euro Zone Apr Final Manufacturing PMI: 56.8e v 56.8 prelim (confirmed 45th straight month of growth and highest since April 2011)

(GR) Greece Apr Manufacturing PMI: 48.2 v 46.7 prior (8th month of contraction)

(IT) Italy Mar Preliminary Unemployment Rate: 11.7% v 11.5%e

(CH) SNB Total Sight Deposits for Week Ended Apr 28th (CHF): 571.4B v 569.1B prior

(UK) Apr PMI Manufacturing: 57.3 v 54.0e (9th month of expansion and highest since Apr 2014)

(EU) Euro Zone Mar Unemployment Rate: 9.5% v 9.4%e (matches lowest level since 2009)

(BE) Belgium Mar Unemployment Rate: 6.9% v 7.0% prior

(ZA) South Africa Apr Manufacturing PMI: 44.7 v 51.4e (1st contraction in 4 months)

Fixed Income Issuance:

(ID) Indonesia sold total IDR4.075T vs. IDR6.0T target in 2-year,4-year,7-year and 15-year Project-based Sukuks (PBS)

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 0.1% at 3564, FTSE +0.4% at 7232, DAX 0.1% at 12447, CAC-40 0.3% at 5280, IBEX-35 0.6% at 10776, FTSE MIB 0.5% at 20710, SMI 0.4% at 8852, S&P 500 Futures -0.1%] Market Focal Points/Key Themes

European indices trade up after the majority of indices come back from the long weekend, continuing the upward momentum that has been seen this year. Generally positive PMI data out of Europe is helping underpin the move with strong earnings from BP helping the FTSE slightly outperform.

Earnings during the day continue with notable earners out of the US to include Merck, Pfizer and MasterCard and after the close Tech giant Apple is due to report.

Equities

Consumer discretionary [Just Eat [JE.UK] -4.2% (Q1 orders), Ocado [OCDO.UK] +7.2% (potential tie up with Marks and Spencer), Dufry [DUFN.CH] -3.0% (Earnings), Accel Grp [ACCEL.NL] -5% (Discontinues talks with Pon Holdings)]

Consumer Staples [PureCircle [PURE.UK] -10% (Cuts outlook)]

Materials: [DSM [DSM.NL] +1.1% (Earnings)]

Industrials: [Geberit [GEBN.CH] -1.3% (Earnings), DSV [DSV.DK] +3% (Earnings)]

Financials: [Aberdeen Asset Mgt [ADN.UK] +3.8% (Earnings),

Healthcare: [Abivax [ABVX.FR] +85% (ABX464 demonstrated the first reduction in HIV reservoirs)]

Energy: [BP [BP.UK] +1.5% (Earnings)]

Speakers

ECB's Nowotny (Austria) stated that the : General Council to hold a discussion at the Jun policy meeting about its strategy for 2018 and an eventual exit from its ultra-easy policy.

EU Institutions: Agreement with Greece with creditors sets the basis for conclusion of the 2nd bailout review

European Stability Mechanism (ESM) Statement: Staff teams from the EU Commission, ESM, ECB and the IMF have reached a preliminary agreement with the Greek authorities on a policy package to support the recovery in Greece

German Finance Ministry: Greek agreement is an important interim step; more clarity still needed on Greek primary budget surplus

Eurogroup chief Dijsselbloem: Welcomes preliminary agreement on Greece package

Greece New Democracy Party (opposition): Will not support new bailout agreement with creditors

French presidential candidate Macron: Will not change his campaign promises to win the backing of Melenchon

Bank of Korea (BOK) Apr minutes: One member sees upside risks for growth projections; economic recovery could be temporary One member: Consumption unlikely to fall more than expected (**Note: Only dissenters are identified in minutes)

China govt reiterated its call for dialogue and consultation to resolve the North Korea issue

China said to be prepared to reach Code of Conduct in the South China Sea at an early date

Currencies

Dealers noted that EUR/USD was likely to stay within a tight range ahead of the French 2nd round of its Presidential election next weekend. The pair stayed above the 1.09 during the session with 1.10 seen as formable resistance for the time being.

USD/JPY was at 1-month high above the 112 handle. Dealers attributed Treasury Sec Mnuchin hint of using the very long end of the US yield curve for funding as rationale for the greenback's strength as it added to the steepening of US yield curve

GBP received a small boost after UK Apr PMI Manufacturing registered its 9th month of expansion and highest level since Apr 2014)

Emerging markets FX saw gains buoyed by optimism the Fed will not raise interest rates this week and there won't be any negative surprises from the 2nd round of the French Presidential election

Fixed Income

Bund futures trade at 161.65 down 17 ticks falling slightly lower following Monday's slide in Treasuries on heavy corporate supply and Treasury Sec Mnuchin comments on ultra-long bond issuance. A break of 161.54 support level could see lows target 161.26 followed by 160.15. Resistance moves to 161.88 level followed by 163.54.

Gilt futures trade at 127.95 down 30 ticks falling after UK Manufacturing PMI beat expectations and rose to the highest since Apr 2014. The move lower was also supported by the decline in US treasuries and German Bunds. Continuation to the downward trend eyes 127.74 followed by 125.83. Resistance stands at 128.58 then 128.81 followed by 129.14.

Tuesday's liquidity report showed Friday's excess liquidity rose to €1.588T a gain of €1B from €1.587T prior. Use of the marginal lending facility climbed to €361M from €259M prior.

Corporate issuance saw over $4.35B come to market via 2 issues headlined by United Technologies $4.0B 5-part senior unsecured notes and Kimberly Clark $350M 30 year senior notes.

Looking Ahead

(RO) Romania Apr International Reserves: No est v $38.6B prior

(RU) Russia Apr Sovereign Wealth Fund Balances: Reserve Fund: No est v $16.2B prior; Wellbeing Fund: No est v $73.3B prior

(IT) Italy Apr Budget Balance: No est v -€22.9B prior

(NG) Nigeria Apr Manufacturing PMI:

(ZA) South Africa Apr Naamsa Vehicle Sales Y/Y: 1.5%e v 2.1% prior

05:30 (EU) ECB allotment in 7-Day Main Refinancing Tender (prior €14.4B with 43 bids recd)

05:30 (HU) Hungary Debt Agency (AKK) to sell 3-month Bills

05:30 (BE) Belgium Debt Agency (BDA) to sell €1.3-1.7B in 3-month and 6-month bills

05:30 (NL) Netherlands Debt Agency (DSTA) to sell 6-Month Bills

06:45 (US) Daily Libor Fixing

07:25 (BR) Brazil Central Bank Weekly Economists Survey

07:30 (CL) Chile Central Bank (BCCh) Apr Minutes

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (CZ) Czech Apr Budget Balance (CZK): No est v 4.7B prior

08:00 (BR) Brazil Apr PMI Manufacturing: No est v 49.6 prior

08:15 (UK) Baltic Dry Bulk Index

08:50 (FR) France Debt Agency (AFT) to sell combined €5.-6.2B in 3-month, 6-month and 12-month BTF Bills

08:55 (US) Weekly Redbook Sales

09:00 (EU) Weekly ECB Forex Reserves

09:00 (NZ) Fonterra Global Dairy Trade Auction

09:00 (SG) Singapore Apr Purchasing Managers Index: 51.2e v 51.2 prior, Electronics Sector Index: No est v 51.8 prior

09:00 (RU) Russia announces upcoming weekly OFZ bond auction

09:30 (EU) ECB announces Covered-Bond Purchases

10:00 (DK) Denmark Apr Foreign Reserves (DKK): 464.1Be v 464.1B prior

10:00 (BR) Brazil Mar CNI Capacity Utilization: 77.2%e v 77.3% prior

10:00 (MX) Mexico Central Bank Economist Survey

10:00 (MX) Mexico Mar Total Remittances: $2.3Be v $2.1B prior

10:30 (MX) Mexico Apr PMI Manufacturing: No est v 51.5 prior

11:00 (BR) Brazil to sell I/L 2022, 2026, 2035 and 2055 Bonds

11:30 (US) Treasury to sell 4-Week Bills

12:00 (IT) Italy Apr New Car Registrations Y/Y: No est v 18.2% prior

13:00 (MX) Mexico Apr IMEF Manufacturing Index: 46.5e v 45.9 prior; Non-Manufacturing Index: 48.2e v 48.0 prior

13:00 (NZ) New Zealand Apr QV House Prices Y/Y: No est v 12.9% prior

14:00 (BR) Brazil Apr Trade Balance: $7.0Be v $7.1B prior; Total Exports: $18.1Be v $20.1B prior; Total Imports: $10.9Be v $12.9B prior

16:30 (US) Weekly API Oil Inventories

GOLD Going Lower, SILVER Continued Weakness, CRUDE OIL Pushing Towards $48.

GOLD Going lower.

Gold continues its decline after the yellow metal has faded near the hourly resistance at 1295 (18/04/2017 high). Hourly support can be located at 1260 (26/04/2017 low). The road is wide-open for further decline.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Continued weakness.

Silver has broken strong support at 18.16 (rising trendline) indicating further downside risk. Strong support given at 16.82 (15/03/2017 low) has been broken. Strong resistance is given at a distance at 19.00 (09/11/2017 high). Expected to see continued bearish pressures.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Pushing towards $48.

Crude oil is trading mixed, breaking the support at 50.71, yet now has paused. Support now lies at 48.87 (25/04/2017 low). Resistance for a short-term bounce can be found at 50.71 (old support) and 53.70 (12/04/2017 high).

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

EUR/JPY Pushing Higher, EUR/GBP Slight Increase., EUR/CHF Targeting Key Resistance.

EUR/JPY Pushing higher.

EUR/JPY's buying pressures are there. Key resistance area given around 122.00 has been broken and stronger resistance stands at 123.31 (27/01/0217 high). Major support is given at 114.90 (18/04/2017low). Expected to see shortterm consolidation before seeing another leg higher.

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Slight increase.

EUR/GBP is getting higher. The technical structure is negative as long as the resistance at 0.8596 holds. Expected to show continued weakness until resistance given at 0.8304 (05/12/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

EUR/CHF Targeting key resistance.

EUR/CHF is pushing higher. Despite the sharp increase and the recent bullish breakout which is very likely psychological, we believe that the medium-term pattern suggests us to see at some point renewed bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low).

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

USD/CHF Sideways Price Action, USD/CAD Targeting 1.3700, AUD/USD Monitoring Downtrend.

USD/CHF Sideways price action.

USD/CHF is trading mixed. Yet, the volatility is getting higher. The short-term technical structure is turning positive as long as prices remain below the hourly resistance at 1.0171 (07/03/2017). Monitor strong support given at 0.9814 (27/03/2017 low).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015

USD/CAD Targeting 1.3700.

USD/CAD has broken key resistance given at 1.3599 (28/12/206 high). The pair keeps on pushing higher. Hourly support can be found at 1.3411 (24/04/2017 high) then 1.3353 (20/01/2017 high). Expected to show continued bullish pressures as long as the pair remains above 1.3411.

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Monitoring downtrend.

AUD/USD is pushing higher . As long as prices remain below the resistance at 0.7608 (17/04/2017 high), the short-term technical structure is negative. Key resistance stands at 0.7681 (30/03/2017 high). Expected to show further weakness.

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Pausing Above 1.0900, GBP/USD Bearish Consolidation, USD/JPY Testing 112.20.

EUR/USD Pausing above 1.0900.

EUR/USD is trading sideways. Hourly support is given at 1.0852 (27/04/2017 low) then 1.0682 (21/04/2017 base). Stronger support can be found at 1.0494 (22/02/2017 low). Hourly resistance is given at 1.0951 (26/04/2017 high). Expected to show another leg higher towards 1.10.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Bearish consolidation.

GBP/USD keeps pushing higher despite ongoing consolidation. Hourly resistance can be found at 1.2966 (30/04/2017 high). The pair has exited the short-term bearish momentum. Hourly support can be found at 1.2757 (21/04/2017 low). An unlikely break of this support would indicate further weakness.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Testing 112.20.

USD/JPY is consolidating. Strong resistance can be found at 112.20 (31/03/2017 high). Closest support can be located at 108.13 (17/04/2017 low). Other key supports lie at a distant 106.04 (11/11/2016 low). Expected to show continued bullish pressures.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

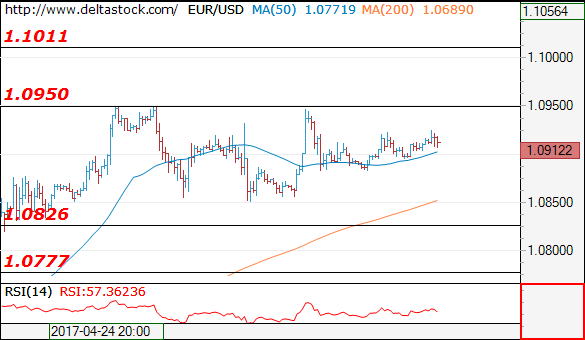

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 10912

The bias here remains neutral, as the pair is caught in a tight trading range between 1.0950 and 1.0826. Intraday allow another swing to the lower boundary.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.0950 | 1.0950 | 1.0826 | 1.0780 |

| 1.1010 | 1.1010 | 1.0780 | 1.0676 |

USD/JPY

Current level - 112.07

The uptrend here is intact, heading towards 112.90 dynamic resistance. Crucial on the downside is 111.42 low.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 112.26 | 112.26 | 111.42 | 109.40 |

| 112.90 | 113.50 | 110.60 | 108.12 |

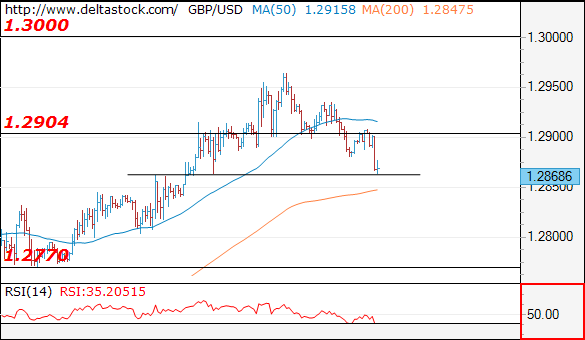

GBP/USD

Current level - 1.2868

There is a reversal at 1.2965 peak and the intraday bias is bearish, currently struggling above 1.2860 support zone. A break through the latter will challenge 1.2770. Crucial on the upside is 1.2904.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2904 | 1.3120 | 1.2860 | 1.2610 |

| 1.3000 | 1.3500 | 1.2770 | 1.2510 |