Sample Category Title

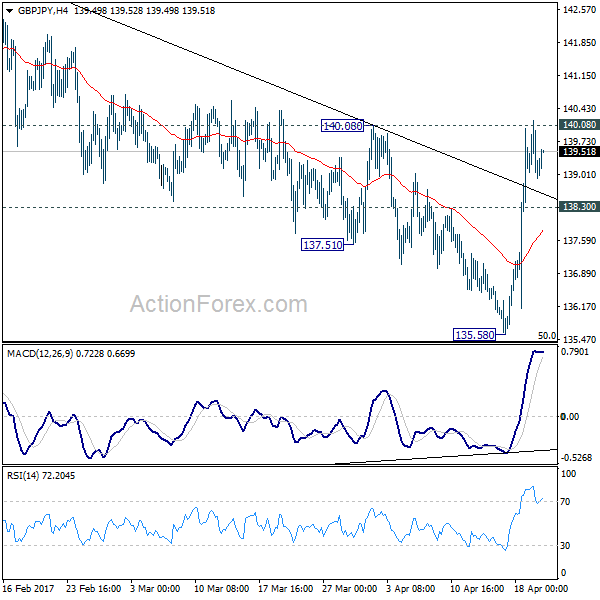

GBP/JPY Daily Outlook

Daily Pivots: (S1) 138.61; (P) 139.40; (R1) 139.88; More...

Intraday bias in GBP/JPY remains on the upside with cautiously bullish outlook. Current developments argues that consolidation pattern from 148.42 is possibly completed at 135.58, just ahead of 135.39 fibonacci level. Decisive break of 140.08 resistance will affirm this case. GBP/JPY should then target a test on 148.42 key resistance level. Meanwhile, this bullish case will be favored as long as 138.30 minor support holds, in case of retreat.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. As long as 50% retracement of 122.36 to 148.42 at 135.39 holds, another rising leg would be seen to 38.2% retracement of 195.86 to 122.36 at 150.42 and possibly above. However, firm break of 135.39 will bring retest of 122.36, with prospect of resuming the larger down trend from 195.86.

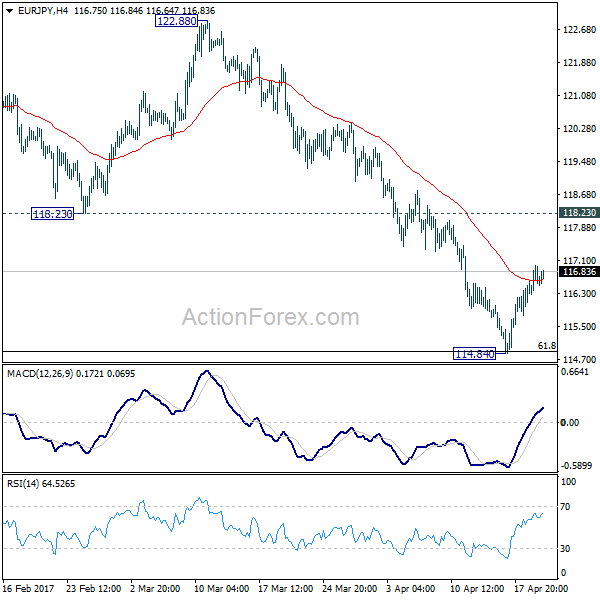

EUR/JPY Daily Outlook

Daily Pivots: (S1) 116.25; (P) 116.61; (R1) 116.96; More...

Intraday bias in EUR/JPY remains neutral as the correction from 114.84 continues. At this point, we'd still expect upside to be limited by 118.23 resistance and bring another fall. Corrective rise from 109.20 should have completed at 124.08. Sustained break of 61.8% retracement of 109.20 to 124.08 at 114.88 will pave the way to retest 109.20 low.

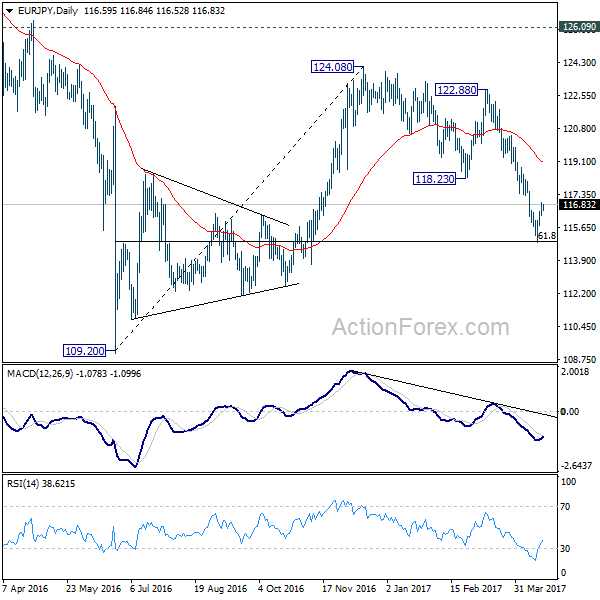

In the bigger picture, medium term corrective rise from 109.20 should have completed at 124.08, ahead of 126.09 support turned resistance. Medium term down trend from 149.76 is likely resuming. Break of 109.20 will target 94.11 low. In any case, break of 126.09 is needed needed to confirm medium term reversal. Otherwise, outlook will remain bearish in case of another rebound.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4214; (P) 1.4256; (R1) 1.4328; More...

Intraday bias in EUR/AUD remains on the upside for 1.4309 resistance. Current development affirmed the case of trend reversal after defending 1.3671 key support. Break of 1.4309 will target 1.4721 key resistance and firm break there will confirm our bullish view. On the downside, below 1.4183 minor support will turn bias neutral first. But we'll stay bullish as long as 1.3980 support holds.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after testing 1.3671 key support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn extend the fall from 1.6587 towards 1.1602 long term bottom.

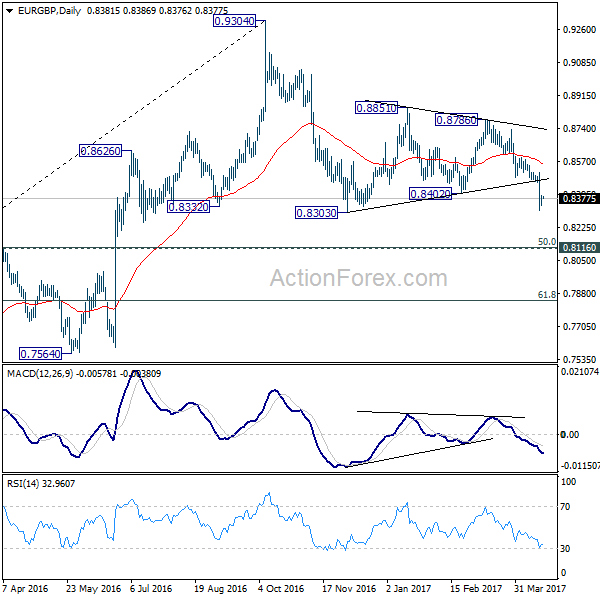

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8349; (P) 0.8369; (R1) 0.8401; More...

With 0.8511 resistance intact, deeper fall is expected in EUR/GBP through 0.8303 low. Current fall is seen as the third leg of the corrective pattern from 0.9034. Break of 0.8303 will target 0.8116.20 key cluster support. We'd expect strong support there to completion the correction and bring rebound. But for now, break of 0.8511 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Such decline is likely ready to resume and should make a new low below 0.8303. At this point, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

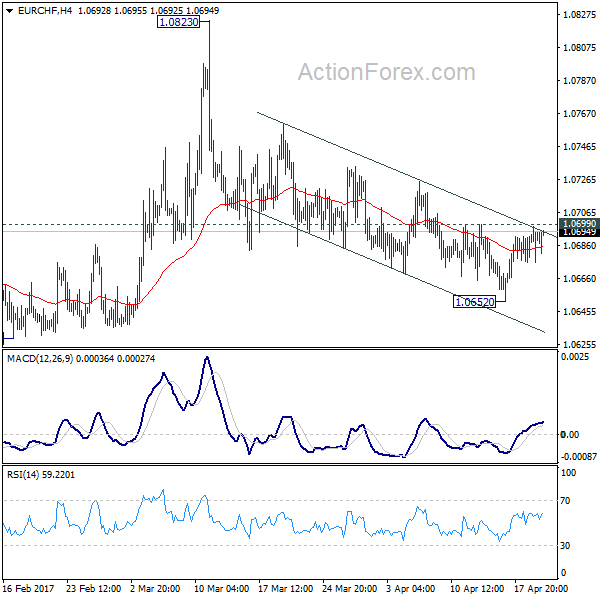

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0678; (P) 1.0688; (R1) 1.0700; More...

Intraday bias in EUR/CHF remains neutral as consolidation from 1.0652 continues. With 1.0699 minor resistance intact, deeper decline is still expected. Below 1.0652 will target 1.0620/0629 support zone. Decisive break there will confirm resumption of whole fall from 1.1198. In that case, EUR/CHF should target next long term fibonacci level at 1.0485. On the upside, break of 1.0699 minor resistance will argue that choppy fall from 1.0823 has completed and turn bias back to the upside.

In the bigger picture, the decline from 1.1198 is seen as a corrective move. Current development suggests that it's not completed yet. Sustained trading below 38.2% retracement of 0.9771 to 1.1198 at 1.0653 will target 50% retracement at 1.0485. In any case, break of 1.0823 resistance is needed to be the first indication of reversal. Otherwise, deeper fall is still expected even in case of recovery.

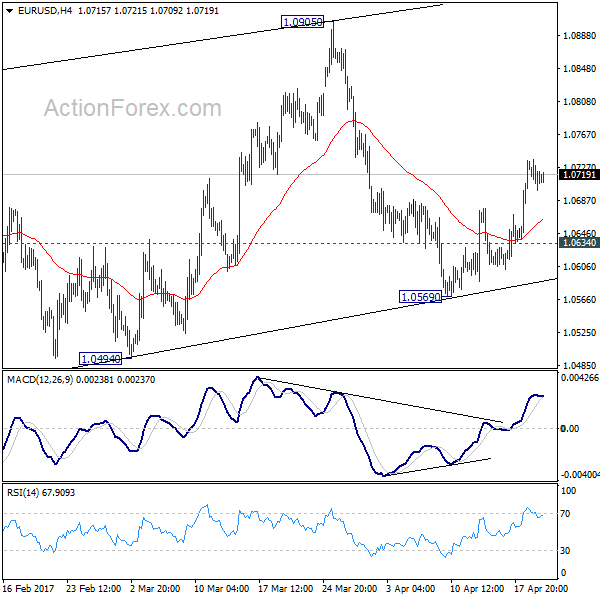

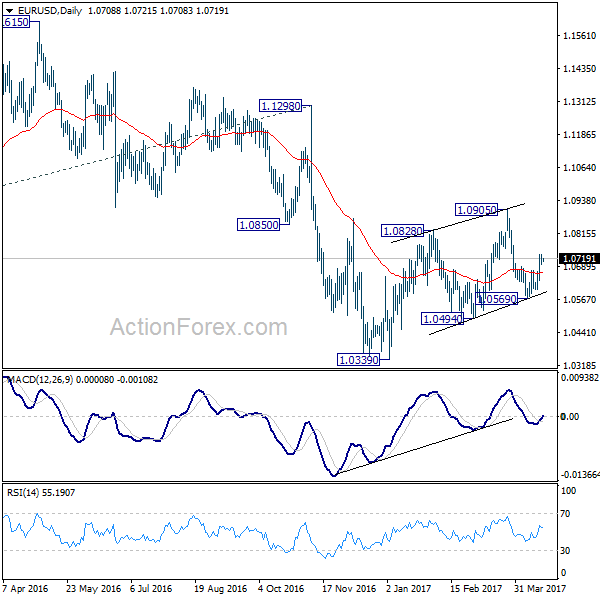

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0694; (P) 1.0715 (R1) 1.0732; More....

With 1.0634 minor support intact, further rise is expected in EUR/USD for 1.0905 resistance. As noted before, corrective rise from 1.0339 is still in progress with 1.0569 as another rising leg. Further rally would be seen to 1.0905 resistance and above. We'll pay attention to topping signal above 1.0905 again, as we'd expect larger down trend to resume later. On the downside, break of 1.0634 minor support will turn intraday bias back to the downside for 1.0569 instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

EUR/USD

In the early hours of yesterday's segment, the pair, as you can see, began to fade around the 1.0735 region. This consequently persuaded the shared currency to retest the 1.07 handle as support. In view of the somewhat compressed approach (little active demand – see H4 wicks) to this psychological band and the fact that daily candles are seen retesting a support area formed at 1.0714-1.0683, this may encourage buyers into the market today. Despite this, the main interest here remains around 1.0773-1.0751: a H4 supply zone that sits in between a H4 mid-level resistance at 1.0750/161.8% H4 Fib extension at 1.0743 (drawn from the low 1.0569) and a H4 61.8% Fib resistance at 1.0777 (taken from the high 1.0905). Also noteworthy is the daily resistance seen at 1.0772 located within the upper limits of the said H4 supply base.

Our suggestions: The above points all suggest that the single currency may find resistance within our green area drawn on the H4 chart at 1.0777/1.0743. Seeing as how the area is rather large and the weekly chart shows room to appreciate beyond the H4 sell zone, we'll wait for a reasonably sized H4 bearish candle to print within before looking to sell.

Data points to consider: US Philly Fed manufacturing survey report and US weekly unemployment claims at 1.30pm, US Treasury Sec Steven Mnuchin speaks at 6.15pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1.0777/1.0743 ([waiting for a reasonably sized H4 bear candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's wick).

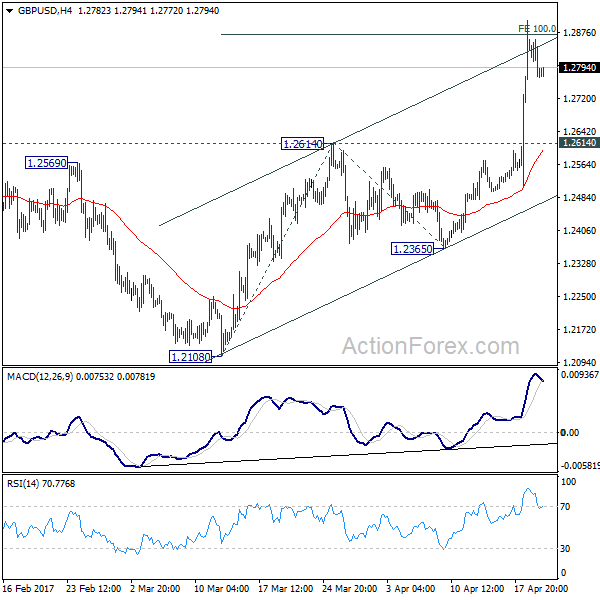

GBP/USD

During the course of yesterday's sessions, we saw the pair trim part of Tuesday's gains as price extended its downside move from the 1.29 handle. Bolstered by a daily resistance coming in at 1.2876 cable eventually managed to close below the 1.28 hurdle, and is now seen poised to test the H4 broken Quasimodo line penciled in at 1.2744. What Wednesday's move also accomplished was bringing weekly price back below resistance at 1.2789.

Although we believe a bounce is likely to be seen from the H4 broken Quasimodo line, trading long from here when both weekly and daily price are trading from structure is chancy, even with additional confirmation. Therefore, the best we feel we can do here is wait and see if the H4 candles retest the 1.28 line as resistance.

Our suggestions: In the event that H4 price retests 1.28 and manages to form a lower-timeframe sell signal (see the top of this report), a short from here is likely to achieve 1.2744, and quite possibly beyond should higher-timeframe sellers get involved.

Data points to consider: BoE Gov. Carney is scheduled to speak at 4.30pm and also 5.30pm in Washington DC. US Philly Fed manufacturing survey report and US weekly unemployment claims at 1.30pm, US Treasury Sec Steven Mnuchin speaks at 6.15pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1.28 region ([waiting for additional lower-timeframe confirming price action is advised] stop loss: dependent on where one confirms this area).

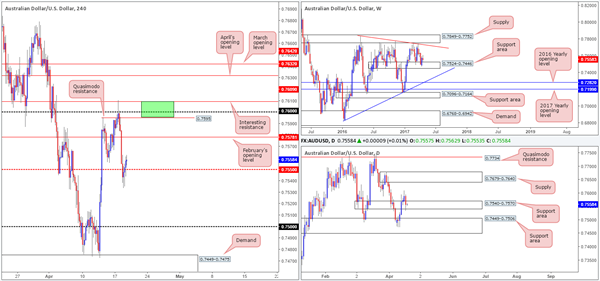

AUD/USD

The value of the Aussie weakened in aggressive fashion on Wednesday, ultimately clearing out bids around the 0.75 handle, which is currently being retested as resistance. Consequent to this, weekly price shows that the majority of last week's gains have been erased and the unit is now seen trading within the lower limits of a support area at 0.7524-0.7446. What's more, daily action is also now seen trading within the walls of a support area formed at 0.7449-0.7506, which happens to bolster the H4 demand at 0.7449-0.7475: the next downside target on the H4 scale.

Our suggestions: Given that the H4 demand is placed within both the said weekly and daily support areas, a long from here is a possibility. However, seeing as this would be considered the areas second time back, we would not feel comfortable pulling the trigger without additional confirmation in the form of a reasonably sized H4 bullish candle.

Data points to consider: US Philly Fed manufacturing survey report and US weekly unemployment claims at 1.30pm, US Treasury Sec Steven Mnuchin speaks at 6.15pm GMT+1.

Levels to watch/live orders:

- Buys: 0.7449-0.7475 ([waiting for a reasonably sized H4 bull candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

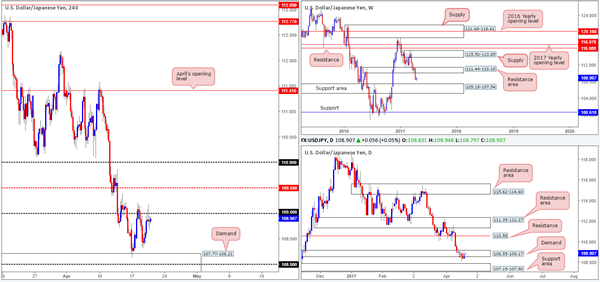

USD/JPY

Beginning with a look at the weekly timeframe this morning, we can see that candle action is hovering between a resistance area at 111.44-110.10 and a support area drawn from 105.19-107.54. Overall, the bears look to have control at the moment, and therefore a test of the said support zone is possible. The story on the daily chart, however, shows price to be trading within the walls of a demand base at 108.55-109.17. Technically speaking though, the bulls look drained here which could eventually spark further selling down to the support area lodged at 107.15-107.90.

Swinging across to the H4 candles, upside remains capped by the 109 handle following Monday's bounce from demand at 107.77-108.21. In view of the current H4 demand being bolstered by the said daily support area, which itself is supported by the aforementioned weekly support area, the 109 handle could be consumed today.

Our suggestions: In the event that a decisive H4 close is seen beyond 1.09 and price retests the boundary as support, we would, assuming that the retest is followed up with a lower-timeframe buy signal (see the top of the report), look to buy, targeting the H4 mid-level resistance at 109.50 and the 110 handle (represents the lower edge of the weekly resistance area mentioned above at 111.44-110.10).

Data points to consider: US Philly Fed manufacturing survey report and US weekly unemployment claims at 1.30pm, US Treasury Sec Steven Mnuchin speaks at 6.15pm GMT+1.

Levels to watch/live orders:

- Buys: Watch for H4 price to engulf 109 and then look to trade any retest seen thereafter ([waiting for additional lower-timeframe confirming price action to form following the retest is advised] stop loss: dependent on where one confirms this number).

- Sells: Flat (stop loss: N/A).

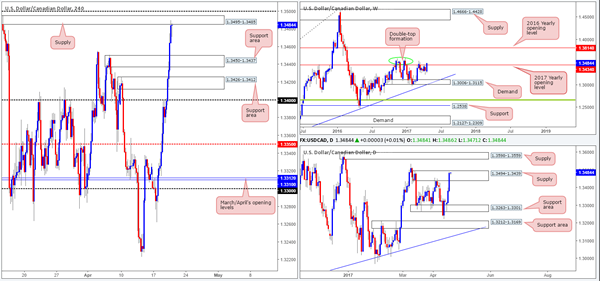

USD/CAD

The USD/CAD surged north for a third consecutive day on Wednesday, as oil prices took a hit to the mid-section. After running through multiple H4 resistances, the pair is now seen testing the underside of a supply zone at 1.3495-1.3485 that is positioned directly below the 1.35 handle.

Over on the daily picture, the buyers and sellers are seen battling for position within supply coming in at 1.3494-1.3439. Weekly price on the other hand, has recently crossed back above the 2017 yearly opening base line at 1.3434. Under normal circumstances, this would be considered a rather important bullish cue. However, since we know that there is a somewhat strong-looking double-top formation located nearby around the 1.3530 neighborhood (see green circle), the bulls could very well struggle here.

Our suggestions: Personally, shorting at the current H4 supply is risky given the round number 1.35 lurking just above. It has ‘fakeout' written all over it! As such, should price happen to print a H4 selling wick that pierces above the current H4 supply and taps 1.35, we would look to short this candle, targeting the support area seen at 1.3450-1.3437.

Data points to consider: US Philly Fed manufacturing survey report and US weekly unemployment claims at 1.30pm, US Treasury Sec Steven Mnuchin speaks at 6.15pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Look for price to print a H4 selling wick that pierces above the current H4 supply and taps 1.35 – this is a cue to sell (stop loss: beyond the selling wick).

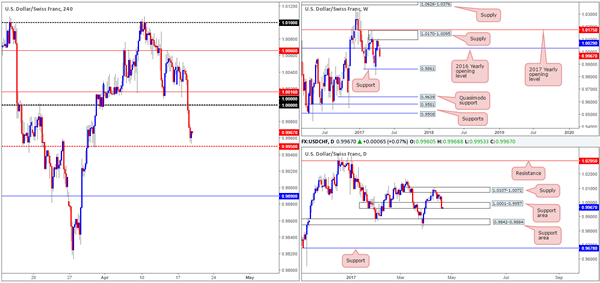

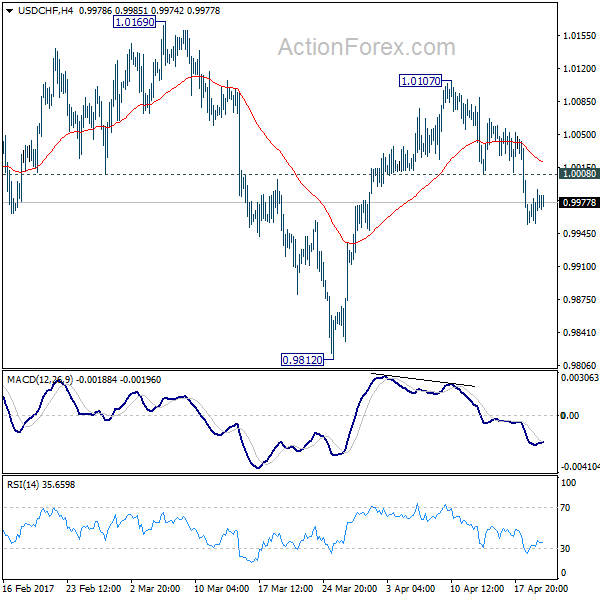

USD/CHF

With weekly price seen trading below the 2016 yearly opening level at 1.0029, the bears could potentially continue pumping the pair down to support penciled in at 0.9861. On the other side of the coin, however, we have fresh bids coming in on the daily chart from within the lower limits of a support zone drawn in at 1.0001-0.9957. Given the difference of opinion being seen on the bigger picture right now, let's see what we can wrinkle out of the H4 chart…

As you can see, the H4 candles are currently loitering between parity (1.0000) and a H4 mid-level support at 0.9950. Notable features on this scale is the nearby April opening level at 1.0016 plotted just above 1.0000, and the H4 demand seen located below 0.9950 at 0.9913-0.9927.

Our suggestions: A retest of 1.0016/1.0000 (green zone) would, if a reasonably sized H4 bearish candle took shape, be a relatively nice place to short from given weekly flow. The reason for requiring a confirming bearish candle prior to entry is simply due to the fact that daily buyers could push this market higher.

Data points to consider: US Philly Fed manufacturing survey report and US weekly unemployment claims at 1.30pm, US Treasury Sec Steven Mnuchin speaks at 6.15pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1.0016/1.0000 ([waiting for a reasonably sized H4 bear candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's wick).

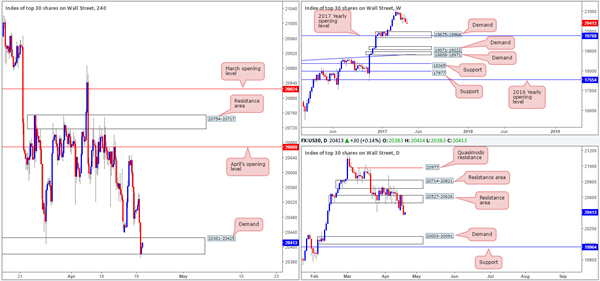

DOW 30

Although the index clocked fresh lows yesterday, the structure of this market remains unchanged. Weekly flow still looks poised to extend the pullback seen from record highs of 21170 down to 19675-19964: a demand area that's bolstered by the 2017 yearly opening level at 19769. Alongside this, daily bears are currently in a strong position right now. Assuming that the sellers remain in the driving seat here, the next downside target can be seen around demand at 20003-20091, which happens to sit directly above the said weekly demand.

As highlighted in Wednesday's report, before one looks to go about shorting this market it might be worth noting that there's a H4 demand area at 20381-20425 to contend with first. Once this area is cleared, the daily demand will likely be brought into the picture. As you can see, the H4 candles are seen testing this H4 demand base as we write. The bulls are showing some interest, but given the higher-timeframe picture it's unlikely going to amount to anything notable.

Our suggestions: Sit on your hands and wait for the H4 demand to be taken out (a H4 close). Once/if this comes to fruition, one can then look at shorting any retest seen to the underside of this zone (a reasonably sized H4 bear candle is required prior to pulling the trigger), targeting the daily demand mentioned above.

Data points to consider: US Philly Fed manufacturing survey report and US weekly unemployment claims at 1.30pm, US Treasury Sec Steven Mnuchin speaks at 6.15pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Watch for the H4 demand at 20381-20425 to be engulfed and then look to trade any retest seen thereafter ([waiting for a reasonably sized H4 bear candle to form following the retest is advised] stop loss: ideally beyond the candle's wick).

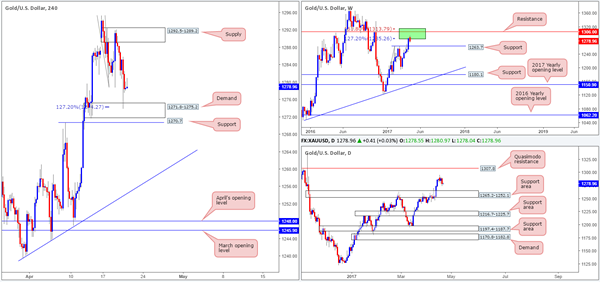

GOLD

In recent sessions, the yellow metal continued to drive lower after touching base with a H4 supply zone seen at 1292.5-1289.2. The move, as you can see, completed at a H4 AB=CD 127.2% ext. at 1274.2, which happens to be housed within a H4 demand area at 1271.8-1275.2. Although this zone has already done a fine job of supporting the bulls, both weekly and daily structure show that the bears could remain in control.

Weekly flow shows price trading nicely from two Fibonacci extensions 161.8/127.2% at 1313.7/1285.2 taken from the low 1188.1 (green zone), while daily action has room to stretch down to a support area marked at 1265.2-1252.1 (a weekly support line at 1263.7 is seen housed within this daily area – the next downside target on this scale).

Our suggestions: We do not see a lot to hang our hat on at the moment. Here's why:

A long would, of course, place one against potential weekly and daily sellers.

A short, although supported by higher-timeframe flow, is risky given the current H4 demand and nearby H4 support at 1270.7. Even with a H4 close seen beyond these two areas, price would then be too close to the top edge of the daily support area to consider a sell!

Maybe we're missing something here, but it seems like we're trapped at both ends!

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2743; (P) 1.2801; (R1) 1.2833; More...

Further rise is expected in GBP/USD as long as 1.2614 resistance turned support holds. Firm break of 100% projection of 1.2108 to 1.2614 from 1.2365 at 1.2871 will target 161.8% retracement at 1.3184. Still, price actions from 1.1946 are seen as a correction. Hence we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2614 resistance turned support will turn bias back to the downside for 1.2365 support first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9961; (P) 0.9976; (R1) 0.9997; More.....

With 1.0008 minor resistance intact, intraday bias in USD/CHF remains on the downside at this point. Rebound from 0.9812 has completed at 1.0107 and correction from 1.0342 is still in progress. Such correction should have started another falling leg. Deeper decline would be seen for 0.9812 support and possibly below. On the upside, above 1.0008 minor resistance will turn bias back to the upside for 1.0107 resistance instead.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the cross. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

European Open Briefing: Asian Stock Markets Recovered Slightly After Several Days Of Losses

Global Markets:

- Asian stock markets: Nikkei gained 0.20 %, Hang Seng rose 0.25 %, Shanghai Composite and ASX 200 both up 0.15 %

- Commodities: Gold at $1281 (-0.20 %), Silver at $18.15 (-0.10 %), WTI Oil at $51.20 (+0.60 %), Brent Oil at $53.35 (+0.75 %)

- Rates: US 10-year yield at 2.21, UK 10-year yield at 1.06, German 10-year yield at 0.20

News & Data:

- New Zealand CPI (QoQ) (Q1): 1.00% (est 0.80%, prev 0.40%)

- New Zealand CPI (YoY) (Q1): 2.20% (est 2.00%, prev 1.30%)

- Australia NAB Business Confidence (Q1): 6 (prev 6)

- PBOC fixes yuan at 6.8792, weakens most since March 29

- Asian stocks set for cautious start on weak U.S. cues – RTRS

- Oil prices claw back ground after sharp drop, buoyed by U.S. crude stock dip – RTRS

Markets Update:

Asian stock markets recovered slightly after several days of losses. However, sentiment remains mixed as investors are nervous ahead of the French election over the weekend. Further, geopolitical risks are also weighing on the market.

The US Dollar regained some strength. EUR/USD fell back to 1.0710 in Asia, while GBP/USD declined to 1.2770 after Tuesday's two percent rally. Support is now seen at 1.2750 and again ahead of 1.27. The Pound is likely to remain bid in the near-term.

Meanwhile, USD/JPY briefly broke back above 109, but momentum is still weak. Strong resistance is seen at 109.20/30, followed by 109.80.

The New Zealand Dollar was the strongest currency overnight. New Zealand inflation data beat expectations and NZD/USD rallied from 0.70 to 0.7045. The Australian Dollar managed to benefit a bit from the NZD flows as well, and rose from 0.7490 to 0.7510.

Upcoming Events:

- 13:30 GMT – US Initial Jobless Claims

- 13:30 GMT – US Philadelphia Fed Manufacturing Index