Sample Category Title

DAX Quiet as German Markets Closed for Good Friday

The DAX is steady on Friday, as the index trades at 12,109.00. German stock markets and banks are closed for the Good Friday holiday, and there are no eurozone releases on the schedule. In the US, it's a busy day, with the release of CPI and Retail Sales reports. CPI is expected to tread water at 0.0%, while the forecast for retail sales stands at 0.2%.

The DAX has enjoyed strong gains in the first quarter of 2017, buoyed by stronger growth data in Germany and the eurozone. However, the DAX has reversed directions in April, dropping 2.1 percent. North Korea and Syria have become flash-points for geopolitical tensions, and there is increasing speculation that the US and North Korea could find themselves at war if China does not succeed in de-escalating tensions and stabilizing a dangerous situation in the Far East. These events are weighing on jittery investors, many who have dumped their holdings in exchange for safe-assets such as gold, which is trading at 5-month highs.

The ECB appears in no hurry to make any changes to its loose monetary policy prior to 2018, or even later. Eurozone inflation levels have picked up in the first quarter, but March levels were softer than expected. This has eased the pressure on the ECB, which is not scheduled to reduce its asset-purchase program until December. In Germany, Wholesale Price Index dropped to a flat 0.0%, compared to 0.5% a month earlier. This was well short of the forecast of 0.4%. The downward trend continued with Final CPI, which dropped to 0.2%, down from 0.6% in February. Eurozone CPI made a big splash in February, when it hit the ECB's target of 2.0%, and raising speculation that the ECB might need to respond by tightening monetary policy. However, the key index softened in March to 1.5%, short of the forecast of 1.8%.

US consumer behavior has been perplexing analysts, displaying a "hard/soft discrepancy" with regard to consumer indicators. Consumer confidence levels have failed to translate into stronger consumer spending, a key driver of economic growth. Confidence levels are considered "soft" data, compared to actual spending numbers, which are termed "hard" data. Will this pattern continue in the March releases? On Thursday, UoM Consumer Sentiment improved to 98.0, beating expectations and hitting a 3-month high. However, the markets are expecting retail sales reports, the primary gauges of consumer spending, to remain at weak levels. Core Retail Sales and Retail Sales are expected to remain unchanged in March, with gains of 0.2% and 0.1%, respectively. On the business front, surveys are pointing to a similar trend, with weak orders despite high confidence levels. The Fed will be closely monitoring consumer spending reports, and if these numbers remain soft, it's unlikely that the Federal Reserve will press that trigger more than two more times in 2017.

Dollar Rebounds on Strong Jobless Claims, German Markets Closed for Holiday

EUR/USD is unchanged in Friday's European session, as the pair trades slightly above the 1.06 line. On Thursday, the euro lost ground as US unemployment claims were unexpectedly strong. In economic news, German banks and stock markets are closed for Good Friday, so we can expect thin trading in the currency markets as we wrap up the trading week. In the US, it's a busy day, with the release of CPI and Retail Sales reports. CPI is expected to tread water at 0.0%, while the forecast for retail sales stands at 0.2%. We'll also get a look at the Treasury Currency Report, which details currency practices of the United States's major trading partners. Earlier this week, President Trump said that China was not guilty of currency manipulation, contradicting what he had repeatedly declared onthe campaign trail.

The ECB appears in no hurry to make any changes to its loose monetary policy prior to 2018, or even later. Eurozone inflation levels have picked up in the first quarter, but March levels were softer than expected. This has eased the pressure on the ECB, which is not scheduled to reduce its asset-purchase program until December. In Germany, Wholesale Price Index dropped to a flat 0.0%, compared to 0.5% a month earlier. This was well short of the forecast of 0.4%. The downward trend continued with Final CPI, which dropped to 0.2%, down from 0.6% in February. Eurozone CPI made a big splash in February, when it hit the ECB's target of 2.0%, and raising speculation that the ECB might need to respond by tightening monetary policy. However, the key index softened in March to 1.5%, short of the forecast of 1.8%.

US consumer behavior has been perplexing analysts, displaying a "hard/soft discrepancy" with regard to consumer indicators. Consumer confidence levels have failed to translate into stronger consumer spending, a key driver of economic growth. Confidence levels are considered "soft" data, compared to actual spending numbers, which are termed "hard" data. Will this pattern continue in the March releases? On Thursday, UoM Consumer Sentiment improved to 98.0, beating expectations and hitting a 3-month high. However, the markets are expecting retail sales reports, the primary gauges of consumer spending, to remain at weak levels. Core Retail Sales and Retail Sales are expected to remain unchanged in March, with gains of 0.2% and 0.1%, respectively. On the business front, surveys are pointing to a similar trend, with weak orders despite high confidence levels. The Fed will be closely monitoring consumer spending reports, and if these numbers remain soft, it's unlikely that the Federal Reserve will press that trigger more than two more times in 2017.

The Weekly Bottom Line

HIGHLIGHTS OF THE WEEK

United States

- Economic data this week remained consistent with the theme of an economy nearing full employment.

- Headlines were dominated this week by rising tensions with North Korea and the increased odds that the French Presidential elections could result in the victory of an anti-EU candidate.

- Comments from President Trump's interview with the Wall St. Journal imply that tax reform is now secondary in importance to health care reform. Less scope for fiscal stimulus may imply a more gradual process of monetary policy normalization than previously anticipated.

Canada

- Manufacturing sales beat expectations in February, with volumes rising 0.1% to the highest level since September 2008.

- Housing starts surged to over 250k units (annualized) in March, marking the fastest pace of building activity in nearly a decade.

- The Bank of Canada left the overnight rate unchanged at 0.50% and upgraded its growth outlook for this year to 2.6% (previously 2.1%). Notwithstanding the upward revision to the numbers, its language emphasized downside risks and caution on the outlook for the Canadian economy.

UNITED STATES - REFLATION TRADE FIZZLES AS GEOPOLITICAL RISKS RISE

There was little in terms of data this holiday week to move financial markets. February data from the job opening and labor turnover survey (JOLTS) showed an uptick in job openings, a downtick in new hires, and a reversal of previous month's strength in the separations rate. Similarly, initial claims data for last week held near historic lows, further corroborating the theme of a healthy labor market. The key message permeating the data is that the job market is nearing full employment, yet more reason to look past last week's disappointing payrolls number.

In addition to the labor market data, updates on small business sentiment and producer prices were released. The NFIB's optimism index cooled for the second consecutive month, but small business remains highly optimistic by historical standards. Growth in core producer prices meanwhile, remains consistent with gradually rising price pressures. Although producer prices in March fell on a month-on-month (m/m) basis, the move was largely driven by energy prices, leaving prices for the final demand goods excluding food and energy category rising by a firm 0.4% m/m.

Overall, there was little change in economic fundamentals this week to motivate the shifts in financial markets, which were drowned out by geopolitical developments and apparent shifts in domestic policy.

News out of North Korea dominated headlines early this week, with fears of an imminent confrontation between the U.S. and the pariah state contributing to a selloff in risk assets and a strong bid on safe havens such as Treasuries and gold. There was initially hope that the meeting between the Presidents of China and the U.S. last week would reduce tensions, but the subsequent bolstering of America's military presence in the Korean peninsula has resulted in the opposite.

Markets also became concerned with the French Presidential election, which has seen a surge in another populist, anti-EU candidate in polls for the first round of elections set to take place in ten days. Jean-Luc Mélenchon, a far-left socialist candidate, is nipping at the heels of third placed Francois Fillon, and his momentous rise in the polls has raised the odds of a presidential runoff election in early May between two anti-EU candidates.

On this side of the Atlantic, President Trump's comments in an interview with the Wall St. Journal suggest a shift toward more conventional policy. For one, President Trump advocated for the need to accomplish healthcare reform before tax reform. President Trump also backed off on plans to label China a currency manipulator, and expressed concern that the strong U.S. dollar has been hurting American exporters. He also reversed his view of the Export-Import bank, suggesting that it was "... a very good thing. And it actually makes money, it could make a lot of money". Lastly, he appeared to soften his stance on the Federal Reserve's policy of low interest rates.

These statements altogether suggest that stimulus from tax cuts is less likely in the near term. Less scope for fiscal stimulus may imply a more gradual process of monetary policy normalization than previously anticipated. Add into the mix elevated geopolitical uncertainty and it looks more and more like the reflation trade's days are numbered.

CANADA - CENTRAL BANK STILL CAUTIOUS ON OUTLOOK

There were two Canadian data releases and a Bank of Canada announcement this week, which, combined with rising oil prices and remarks from Trump that the USD is too high, sent the loonie up to a 6-week high of 75½ US cents.

Both of the key data releases continued the trend of better-than-expected activity at the start of this year. Manufacturing sales beat expectations, with volumes rising by 0.1% in February. This marks the 4th consecutive increase and brings volumes to the highest level since 2008. Forward looking indicators suggest that this momentum could continue going forward. Combined with a strong hand off from the end of 2016, manufacturing output is on track to add favourably to growth during the first quarter of the year.

Ditto for residential construction. Housing starts surged to over 250k units (annualized) in March - the fastest pace of building activity in nearly a decade. For the quarter as a whole, construction was up by a whopping 15% q/q. This pace of building is unlikely to be sustained, however, with some payback likely in store in the coming months. Still, overall economic growth for the first quarter is set to come in quite strong, tracking a robust 3.4% annualized.

Perhaps the highlight of the week was Wednesday's Bank of Canada announcement and accompanying Monetary Policy Report. The remarkable performance of the Canadian economy in recent months, combined with the Federal Reserve in tightening mode stateside, had prompted some expectations for a more hawkish tone from the Bank of Canada. However, despite an improved outlook, Canada's central bank remains quite cautious.

As expected, the overnight rate was left unchanged at 0.50%. However, growth forecasts were indeed upgraded for this year, with the Bank now forecasting economic activity to advance by 2.6% (previously 2.1%). Accordingly, it also expects the output gap to close in the first half of 2018 - slightly earlier than the mid-2018 expected previously.

Despite these improvements, the Bank is clearly not convinced that the Canadian economy is out of the woods just yet. The communique struck a somber tone, noting that 'material slack' still exists in the economy, that soft spots remain - notably, hours worked, uneven export growth and challenges related to business investment - and that it is simply too early to declare the economy on a sustainable growth path. What's more, the Bank's growth profile suggests that it views the near term growth drivers - consumer spending and residential investment - as transitory and likely to slow in the coming quarters, while it awaits a more consistent improvement from exports and business investment. The cautious approach also reflects risks to the outlook, particularly those outside Canada's borders such as the implications from any new policy actions south of the border.

All told, the Bank has clearly not forgotten that the Canadian economy has endured a couple of false starts in recent years. While some pullback from the exceptionally strong start to the year is likely, we expect economic activity to chug along at a healthy clip of around 2% over the remainder of this year. This is unlikely to be enough to entice the Bank of Canada to pull the trigger on higher rates; however, it will allow economic slack to be absorbed and should pave the way for a rate hiking cycle to begin in 2018.

Turkey’s Constitutional Referendum: Too Close to Call?

On Sunday, Turkish citizens will head to the polls to vote on constitutional changes that could greatly expand the executive powers of President Erdogan The referendum will ask the question of whether to turn Turkey from a parliamentary to a presidential republic. The government and the President argue that a "yes" vote would reduce political deadlocks, thereby accelerating the pace of future reforms. On the other hand, critics of these changes argue that too much power would be concentrated in the hands of one person, which could increase the risk for an authoritarian government in the future.

Opinion polls suggest that this race is too close to call. A "yes" outcome is seen by most polls as being more likely, but marginally so. Importantly, the majority of polls show a high percentage of undecided voters, so surprises are definitely possible.

With regards to the Turkish lira, we see the case for the currency to strengthen under a "yes" outcome, and to weaken if the Turkish public votes against these reforms. Ever since the failed military coup last year, Turkey has remained in a state of emergency, which is still ongoing. Media reports suggest that in a "yes" scenario, the government could lift this state of emergency, which in our view could prove positive for the lira in the short-term, as some political uncertainty dissipates. In this scenario, USD/TRY could break below the crossroad of the 3.6400 (S1) support and a medium-term upside support line taken from the 13th of December. Such a break could pave the way for further downside extensions, towards the 3.5550 (S3) territory.

On the other hand, a "no" vote could heighten political uncertainty even further. The state of emergency could stay in place, and there seems to be no clear plan about what happens next. Some reports suggest that the nation could even go into early elections as soon as this year. In such a case, USD/TRY may surge and break above the resistance zone of 3.7050 (R1). A decisive break above that territory could initially target the 3.7400 (R2) level.

Today's highlights:

During the European day, markets will remain closed in G10 nations in celebration of the Good Friday holiday.

Even though US markets will stay closed too, we still get the nation's CPI and retail sales data, all for March. With regards to the CPIs, the headline rate is forecast to have ticked down, while the core rate is expected to have ticked up. In such a case, we think that an increase in the core CPI rate is likely to overshadow a decline in the headline, as policymakers tend to focus more on the core figure.

As for retail sales, both the headline and the core rates are expected to have declined somewhat. We see the risks surrounding these forecasts as skewed to the upside, perhaps for unchanged rates, considering the nation's consumer confidence indices for the month. Even though the U of M index rose only slightly, the Consumer Board figure skyrocketed, reaching a level last seen in 2000. This suggests that US consumers may be feeling increasingly more optimistic, something that may show up in the retail sales figures too. Considering our overall CPI and retail sales view, we think that the greenback could recover some of its recent losses on the news.

USD/JPY rebounded somewhat yesterday, after it found support near the 108.80 (S1) level. In case of encouraging US data today, this recovery could continue and perhaps aim for the 109.90 (R1) resistance area. However, bearing in mind the latest verbal FX intervention from the Trump administration, as well as the fact that geopolitical risks in the Korean Peninsula and the Middle East are far from diminished, we believe that any near-term rebounds in this pair are likely to remain limited. As such, even if the rate rises somewhat today on the aforementioned data, we would expect the bears to take back control soon and push the battle lower again, possibly for another test of the 108.80 (S1) support level.

USD/TRY

Support: 3.6400 (S1), 3.5900 (S2), 3.5550 (S3)

Resistance: 3.7050 (R1), 3.7400 (R2), 3.7700 (R3)

USD/JPY

Support: 108.80 (S1), 107.90 (S2), 107.00 (S3)

Resistance: 109.90 (R1), 111.00 (R2), 111.60 (R3)

Volatility Compressed ahead of Holiday Week with an Eye on Middle East and Korea

US Session Highlights

- (US) INITIAL JOBLESS CLAIMS: 234K V 245KE; CONTINUING CLAIMS: 2.03M V 2.02ME

- (US) MAR PPI FINAL DEMAND M/M: -0.1% V 0.0%E; Y/Y: 2.3% V 2.4%E

- (US) Pres Trump tweets: "I have great confidence that China will properly deal with North Korea. If they are unable to do so, the U.S., with its allies, will!"

- (US) APR PRELIMINARY UNIVERSITY OF MICHIGAN CONFIDENCE: 98 V 96.5E; Current conditions: 115.2 v 113.2 prior final reading (highest since 2000)

- (US) Forces in Afghanistan struck ISIS tunnels with "the mother of all bombs", largest conventional bomb ever used by the US military - press

US markets on close: Dow -0.7%, S&P500 -0.7%, Nasdaq -0.5%

- Best Sector in S&P500: Real Estate

- Worst Sector in S&P500: Energy

- Biggest gainers: ALXN +3.3%; INCY +1.9%; COTY +1.7%

- Biggest losers: SWN -5.0%; FTR -4.4%; CHK -4.2%

- At the close: VIX 16.0 (+0.2pts); Treasuries: 2-yr 1.21% (flat), 10-yr 2.23% (-7bps), 30-yr 2.89% (-4bps)

US movers afterhours

- STRP: Verizon said to consider topping AT&T bid - press; +9.4% afterhours

- SABR: To enter S&P MidCap 400 index, effective ahead of the open on April 19; +4.6% afterhours

Politics

- (FR) France IFOP daily presidential poll: Second round poll: Macron 58.5% (unchanged), Le Pen 41.5% (unchanged)

Key economic data

- (KR) South Korea Mar Import Price Index M/M: -2.0% v -2.1% prior (revised from -2.2%); Y/Y: 6.9% v 9.2% prior (revised from 9.1%)

- (CN) China Finance Ministry: Q1 Fiscal Rev rose 14.1% y/y at CNY4.44T - Chinese press

Asia Session Notable Observations, Speakers and Press

- Asian equity markets are trending lower, tracking continued selling in US that took its indices to 2-month lows. Despite the fairly constructive start to the US earnings season with a beat by JP Morgan and a mixed report from Wells Fargo, investors focus remained on geopolitical jitters around South Korea and the Middle East. Selling momentum picked up at the end of the US session after reports that US forces in Afghanistan struck ISIS tunnels with "the mother of all bombs" - the largest conventional bomb ever used by the US military - raising concerns of an expanded US involvement in other parts of the Middle East.

- In Asian trading hours, the focus is centered on North Korea as it approaches the key Apr 15th birthday of its founder Kim Il-sung. Overnight reports suggested that there's been new activity at its nuclear test cite, and today NBC reported that US would consider a preemptive strike against North Korea with conventional weapons if it believes Pyongyang will proceed with a nuclear test. In response, North Korea's Vice Foreign Minister said Pyongyang will conduct a nuclear test when it sees fit, adding that its military will not sit idly in the event of a US strike.

- Despite the ongoing saber-rattling, currency volatility is compressed going into Good Friday / Easter holidays. USD/JPY is not reacting to the news that would typically dictate safehaven flows, flat-lining just below 109.20. CME futures markets are also closed for holiday and not responding to developments.

- Toshiba remained in the corporate headlines, falling nearly 6% on press reports that it stopped meetings regarding sale of its chip unit due to contractual obligations to Western Digital, but pared half of that decline after reports of Apple interest in a joint bid for the division with Hon Hai.

China

- (CN) China Finance Ministry: Q1 Fiscal Rev rose 14.1% y/y - Chinese press

- (CN) Japan Coast Guard claims China Coast Guard vessels entered its waters - financial press

Japan

- (JP) Bank of Japan (BoJ) Exec Dir Amamiya: BOJ easing is not for financing govt debt - press

Australia/New Zealand

- (NZ) DairyNZ: Cyclone Cook may have an impact on the coming season's dairy production - NZ press

Korea

- (KR) North Korea Vice Foreign Min: Will conduct another nuclear test when HQ sees fit; Pres Trump is "making trouble" with aggressive tweets - press

- (KR) South Korea Deputy Fin Min Song In-chang: Pres Trump's remarks on China not being a currency manipulator reduce the risks of Korea being labeled one as well - press

Asian Equity Indices/Futures closed (23:000ET)

- Nikkei -0.3%, Hang Seng closed, Shanghai Composite -0.6%, ASX200 closed, Kospi -0.6%

FX ranges/Commodities/Fixed Income (23:00ET)

- EUR 1.0605-1.0625; JPY 109.00-109.20; AUD 0.7555-0.7575; NZD 0.6975-0.7000

- (US) Weekly Baker Hughes US Rig Count: 847 v 839 w/w (+1%) (13th straight weekly rise)

- SPDR Gold Trust ETF daily holdings rise 6.5 tonnes to 848.9 tonnes; highest since Dec 14th

- (CN) PBOC SETS YUAN MID POINT AT 6.8740 V 6.8651 PRIOR

- (CN) PBoC injects CNY90B combined in 7, 14, and 28-day reverse repos; Injects net CNY70B this week v drained CNY100B prior

Asia equities/Notables/movers

Japan

- 6502.JP Toshiba -5.7% (speculation to stop chip unit sale)

- 7974.JP Nintendo Co +3.4% (Switch becomes fast-selling video games system)

- 9983.JP Fast Retailing Co +1.0% (Q2 result)

Taiwan

- 2330.TW Taiwan Semiconductor Manufacturing Co -1.8% (Q1 result)

China

- 002143.CN Sichuan Gaojin Food Co -10.0%

- 000415.CN Bohai Leasing Co +5.3% (Xiongan new area momentum)

- 000338.CN Weichai Power +1.6% (guidance)

- 601898.CN China Coal Energy -1.3% (Mar result)

Elliott Wave View: Gold Pullback Starting

Short term Elliott Wave view in Gold (XAUUSD) suggests that cycle from 4/10 low (1246.92) is unfolded as an impulse Elliott wave structure where Minutte wave ((i)) ended at 1257.2, Minutte wave (ii) ended at 1250.8, Minutte wave (iii) ended at 1279.75, Minutte wave (iv) ended at 1271.69 and Minutte wave (v) of (a) could be done at yesterday's peak 1288.42 in Minutte wave (b), although another push higher in Minutte wave (v) of (a) towards 0.618-0.764% fibonacci extension area of Minutte (i)+(iii) 1291.84-1296.48, can't be ruled out yet before ending the 4/10 cycle. However while below the 1288.42 metal could have started the Minutte wave (b) pullback to correct the cycle from 4/10 lows. We don't like selling the proposed pullback and expect buyers to appear again in Minutte wave (b) in sequence of 3, 7, or 11 swings provided that pivot at 4/10 low (1246.92) remains intact.

Gold 1 Hour Elliott Wave Chart

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD,AUDUSD, GBPCAD, GOLD, WTI CRUDE, DJIA, FTSE 100, DAX

EUR/USD

The EURUSD pair fell on Thursday and pared most of gains from late Wednesday's rally, inspired by comments from the US President Trump. The rally stalled at 1.0675, capped by 55SMA and left double-top after repeated upside rejection followed by fresh bearish acceleration. Quick reversal was triggered by profit-taking action at the end of holiday-shortened week and retraced 76.4% of Wednesday's 1.0588/1.0675 rally. Also, fresh strength of the US dollar was sparked by solid US weekly jobless claims data that boosted the greenback which was previously hit by Trump's comments that the US currency is too strong and that he prefers low interest rates. US weekly jobless claims were unchanged from the previous week at 234K and holding near 44-year low at 227K, posted in February, signalling that US jobs sector is on the right path.

EURUSD's rally failed to regain pivotal 1.07 resistance zone to trigger stronger recovery and fell back below previous pivot at 1.0624 (100SMA), also denting the top of daily Ichimoku cloud at 1.0614 and bringing near-term technical studies back to negative mode that increases risk of further weakness.

Increased downside risk is also backed by negative daily studies.

Due to Good Friday holiday on Friday, money markets are expected in thin volumes environment, with release of US inflation and Retail Sales data, expected to move markets on releases away from forecasted levels.

Retail Sales are expected to fall in |March, according to -0.1% forecast against February's 0.1% increase, while annualized CPI is forecasted at 2.3% in March vs 2.2% in Apr, which could be good signal for Fed about decision of next rate hike.

Support: 1.0608; 1.0588; 1.0570; 1.0525

Resistance: 1.0623; 1.0663; 1.0675; 1.0700

USD/JPY

USD JPY currency pair ended Thursday's trading in green, but gains were limited after the pair extended strong fall of previous two days to 108.72, where 200SMA offered solid support and paused bear-leg from 111.57 (Apr 10 high). Technical studies remain bearish on daily chart, favouring break below 200SMA footstep and extension of the wave C ( the third wave of five-wave descend from 118.60 peak) towards its 100% Fibonacci expansion at 108.48 and 107.86 (Fibonacci 61.8% of broader bull-trend from 101.18 to 118.65) in extension.

Japanese yen remains well support by risk aversion and safe haven buying on growing geopolitical risk that sees potential for yen to gain further against the US dollar.

Recovery attempts on Thursday were limited at 109.38, keeping strong resistances at 110.00 zone (former base, reinforced by falling Tenkan-sen line) intact and keeping risk shifted to the downside, despite oversold daily studies.

Only firm break above 110.00 barrier would sideline downside risk in favour of stronger correction.

Support: 108.72; 108.48; 107.86; 106.73

Resistance: 109.38; 110.10; 110.48; 110.90

GBP/USD

GBPUSD pair ended Thursday's trading in red, leaving bearish daily candle with long upper wick, after strong three-day rally extended on Thursday to fresh two-weeks high at 1.2574, but failed to hold gains. Subsequent easing returned to 1.2500 zone (former pivotal barrier) where it ended trading for Thursday. Pullback was also boosted by fresh strength of the dollar, but pullback could be seen as correction of larger rally, as pound received strong support from solid economic data this week and technical studies remain in strong bullish setup. Correction faces good support at 1.2466 (20SMA) which is expected to ideally contain dips ahead of fresh push higher. However, extended downticks cannot be ruled out, with next set of solid supports at 1.2426/17 (converged 55/100SMA's) seen containing.

Bulls are still focusing targets at 1.2615/29 (27 Mar high / 200SMA) and only sustained break below 100SMA at 1.2617 would sideline bullish scenario and turn focus towards higher base at 1.2365 (lows of Apr 07/10).

Support: 1.2480; 1.2466; 1.2426; 1.2417

Resistance: 1.2548; 1.2574; 1.2615; 1.2629

AUDUSD

The Aussie dollar was among top winners on Thursday, as it rallied on fresh US dollar's weakness and accelerated further after upbeat Australian jobs data and better than expected Chinese export / import data which boosted Australian dollar as Australia is one of the biggest China's trading partners.

Australian employment data showed creation of 60.900 new jobs in March, which was more than tripled from forecast at 20.000 and 2800 new jobs created in February. Australian unemployment remained unchanged in March and came along with forecast at 5.9%.

AUDUSD rallied strongly and took out important barrier at 0.7550 (200SMA), after broken previous pivot at 0.7516 (100SMA) kept the downside protected and underpinned Thursday's action.

Close above 200SMA will be seen as strong bullish signal, as current rally already retraced over 50% of 0.7675/0.7473 descend and may accelerate further if takes out next pivot at 0.7611 (daily Kijun-sen line).

However, daily studies are still weak and risk of recovery stall will exist if the pair fails to extend recovery above Kijun-sen pivot.

Return below 200SMA would re-activate negative scenario and shift near-term risk lower.

Support: 0.7550; 0.7516; 0.7500; 0.7473

Resistance: 0.7595; 0.7604; 0.7611; 0.7627

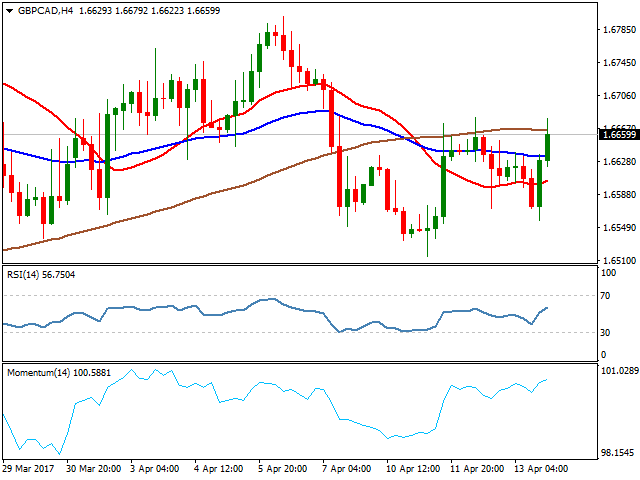

GBPCAD

The GBPCAD cross was higher on Thursday and ended trading positively after break above daily Tenkan-sen line (the upper boundary of near-term 1.6657/1.6589 congestion). With daily Tenkan-sen / Kijun-sen lines being in bullish setup and daily indicators holding in the positive territory, near –term bulls are looking for confirmation on break above next pivotal barrier at 1.6691 (200SMA), to open way for extension towards next target at 1.6800 (Apr 6 high).

The pair gained 0.35% on Thursday, as strong rally surged through hourly Ichimoku cloud and turned near-term studies to the bullish mode that would support further upside acceleration

Daily close above Tenkan-sen line will be initial bullish signal.

On the downside, daily Kijun-sen offers solid support at 1.6589, which should hold extended corrective dips.

Support: 1.6638; 1.6600; 1.6589; 1.6557

Resistance: 1.6679; 1.6691; 1.6736; 1.6800

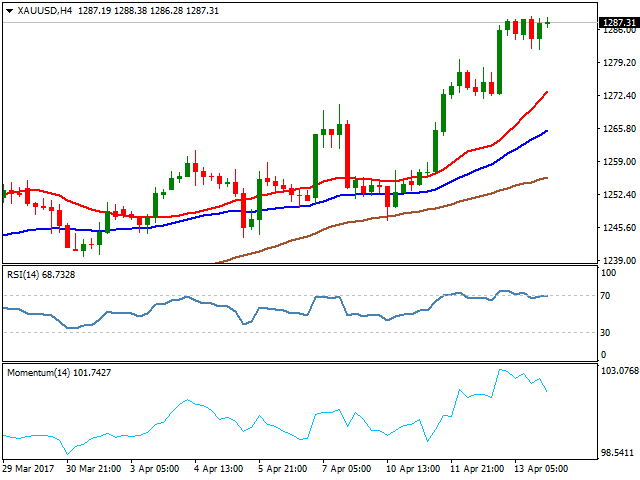

GOLD

Spot Gold continued to trend higher and hit fresh 5-month high at $1288 on Thursday, being supported by rising tensions over US relations with Russia and North Korea and recent dollar's fall after US President Trump said that the dollar is too strong. Gold is expected to remain supported as geopolitical tensions sparked risk-aversion in the markets and prompted investors to exit position in riskier assets and move into traditional safe haven gold.

The yellow metal could extend rally through next target at $1293 (weekly Ichimoku cloud top) and attack psychological $1300 barrier in extension.

However, daily studies are overextended and suggest that strong bulls may take a breather, but no firmer bearish signal have been generated for now.

Immediate support lies at $1281 (daily low) ahead of thick hourly Ichimoku cloud which is spanned between $1279 and $1268 and is expected to contain extended corrective dips.

Support: 1281;1279; 1270; 1268

Resistance; 1288; 1293; 1300; 1307

WTI CRUDE OIL

WTI oil ended Thursday's trading positively, signalling that previous day's pullback may be over, after dips from fresh five-week high at $53.74 found footstep at $52.70. However, risk of fresh easing remains in play and signalled by overbought daily slow stochastic that is reversing from overbought territory after forming bearish divergence. Loss of immediate support at $52.70 would initial signal of correction which could extend to $52.17 (Fibonacci 23.6% of $47.07/$53.74) and expose pivotal support at $51.66 (converged 55/100 SNMA's), loss of which would generate stronger correction signal.

Conversely, early downside rejection and return to $53.74 would signal bullish continuation and focus key barriers at $55.00 zone.

WTI contract will shut on Friday for Good Friday holiday.

Support: 52.52.83; 52.70; 52.17; 51.66

Resistance: 53.37; 53.74; 54.50; 55.00

DJIA

Major U.S. stock indexes fell on Thursday for a third straight day, as investors weighed earnings reports from big U.S. banks and geopolitical tensions, while the technical sector fell for a tenth consecutive session.

Dow Jones remained in red on Thursday and extended weakness for the second day, hitting target and key near-term support at 20385 (daily Ichimoku cloud base), break of which would generate fresh bearish signal, as index commenced fresh bear-leg after holding in directionless mode during previous two weeks and ended past week in red.

Risk remains shifted to the downside, as bearish technical studies weigh. Extension below daily cloud would open way for extension towards next support at 20266 (Fibonacci 61.8% of 19713/21160 rally).

Dow Jones will be closed on Good Friday.

Support: 20385; 20266; 20200; 20157

Resistance: 20548; 20607; 20692; 20827

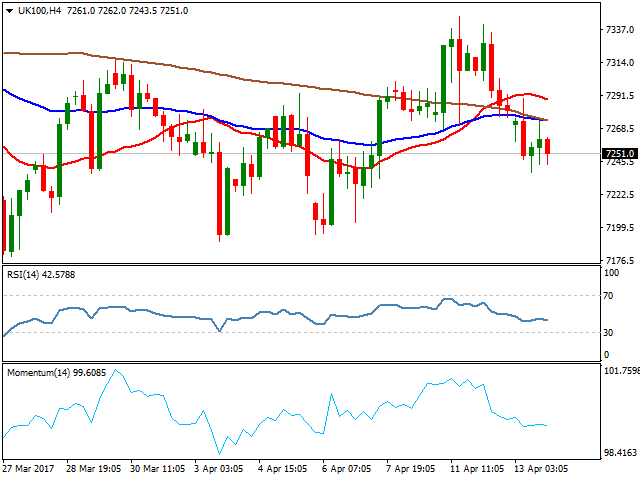

FTSE 100

FTSE index remained under pressure on Thursday and closed in red for the second consecutive day, extending below important support at 7268 (daily Tenkan-sen) and hitting key support at 7238 (top of daily Ichimoku cloud which underpins bulls since mid-Dec 2016). Fresh attack at daily cloud is the second one, after false break into cloud one week ago and may generate stronger bearish signal.

Daily Tenkan-sen / Kijun-sen lines are in bearish setup, along with daily indicators entering negative territory and weighing on near-term action, as index closed the week in red.

Focus will be on Monday's post-holiday opening, as index will be closed on Friday.

Support: 7238; 7203; 7184; 7140

Resistance: 7268; 7289; 7311; 7343

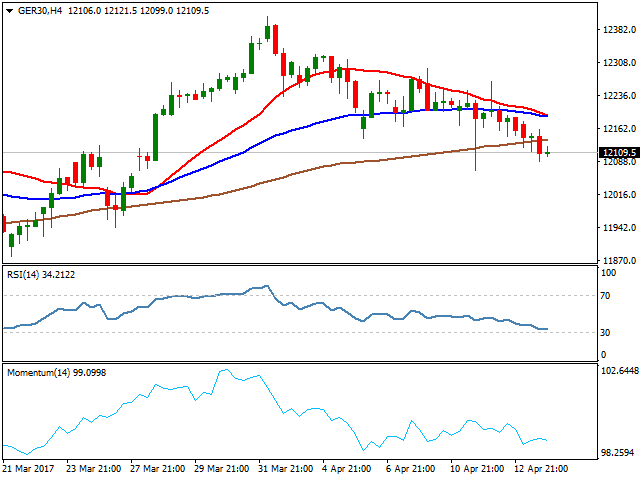

DAX

DAX closed in red for the fourth consecutive day and also ended the second week negatively, on extension from fresh record high at 12410, posted on Apr 03. Technical studies are losing traction as the price already cracked 61.8% retracement of 11878/12410 upleg at 12081 that could signal fresh bearish acceleration on break.

Negative sentiment is reinforced by surge through thick 4-hour Ichimoku cloud and sustained break below 12081 handle would expose psychological 12000 support.

Broken daily Kijun-sen line now acts as initial resistance at 12144, while upper breakpoint is marked by daily Tenkan-sen at 12240.

DAX will be closed on Friday.

Support: 12081; 12000; 11943; 11878

Resistance: 12144; 12178; 12207; 12240

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD Forecast:

The EURUSD failed to continue its bullish momentum yesterday after-unable to break above the H4 EMA 200 resistance as you can see on my H4-chart below. Price is now retesting the trend line support which remains-a good support and place to buy with a tight stop loss as a clear break-below the trend line support and 1.0575 area would expose 1.0500 region-as a part of the bearish continuation scenario after the false break-above 1.0873. The bias is bearish in nearest term. Immediate resistance-is seen around 1.0650. A clear break above that area could lead price to-neutral zone in nearest term retesting the H4 EMA 200 and 1.0700-region. Overall I remain neutral.

GBPUSD Forecast:

The GBPUSD failed to continue its bullish momentum yesterday bottomed at-1.2500. The bias is bearish in nearest term testing 1.2480 support area-which is a good place to buy with a tight stop loss as a clear break-below that area would end the bullish phase after bounced off 1.2375 key-support, testing 1.2450/00 region. Immediate resistance is seen around-1.2520/35. A clear break above that area could lead price to neutral-zone in nearest term but would keep the bullish phase remains alive and-kicking retesting 1.2615 region. Overall I remain neutral.

USDJPY Forecast:

The USDJPY was indecisive yesterday formed a Doji formation as you can-see on my daily chart below. The bias is neutral in nearest term but-overall I remain bearish. Immediate resistance is seen around 109.40. A-clear break above that area could trigger further bullish pullback-testing 109.85 – 110.10 region which is a good place to sell. On the-downside, a clear break and daily/weekly close below 108.72 would expose-107.50 area or lower next week.

USDCHF Forecast

The USDCHF failed to continue its bearish momentum yesterday after-unable to make a clear break below 1.0020 key support, topped at 1.0067.-The bias is bullish in nearest term testing 1.0115 – 1.0170 area. On-the downside, 1.0020 remains a key support. A clear break below that-area would end the bullish phase testing 0.9970 or lower. Overall I-remain neutral.

S&P 500, NOT the Start of a Major Decline…

S&P 500 (cash) near term outlook:

The market has continued to trade in that 2322/2401 range that has been in place since Mar 1st. Note that the sloppy, 3 wave moves (a-b-c's) in both directions continue to suggest a large correction, and with an eventual resumption of the longer term gains above that 2401 high after. May be forming a large triangle/pennant (3 waves moves in both directions a characteristic) suggesting at least another few weeks of this trading in a tighter and tighter range before resolving higher. Also, lots of support is just below the base of the range at 2322, so even in the case of a break below further downside may be limited. Further support is just below there at 2315/18 (50% from the Dec 30th low at 2234) and 2298/01 (broken Jan 26/Feb 7th highs). And finally, don't forget about that series of approx 5 month peaks in the VIX which again tops around this time and adds to the view of a nearing low/limited further downside in the s&p 500 (inverse relationship, see 2nd chart below). Nearby resistance is now at the earlier broken bull trendline from Dec (currently at 2341/44) and the bearish trendline from Mar 2nd (currently at 2372/75). Bottom line : sloppy ranging since the Mar 1st high at 2401 still seen as a large correction, but with scope for at least another few weeks of wide ranging (poss triangle) before resuming that larger upmove.

Strategy/position:

Took small profit Mar 27th buy at 2325 today below that bull trendline from Dec 30th (2342, closed at 2329 for 4 pts). For now with the action from Mar 1st seen as a large correction and the market nearing the base, looking to rebuy. However, not yet enough confidence to rebuy here as there is still no confirmation of even a short term low (and larger bottoms begin with smaller ones).

Long term outlook:

As discussed above, gains past that Mar 1st high at 2401 are still favored but lots of longer term negatives suggest that the bigger picture magnitude may be more limited. An interesting time for the longer term given a real contrast between the upside pattern which is quite far from "completion" (currently seen within wave 3 in the rally from that the July 2016 low) but at a time with lots of other longer term negatives. Those negatives include bearish technicals (sell mode on the weekly macd), overbought market after the huge surge from at least that Nov low at 2084) and lots of long term resistance just above that 2401 high at the rising trendline from Apr 2016 (currently at 2435/40) and that very long term ceiling of the bull channel from 2009 (currently at 2465/75). This in turn suggests at least another few months of potentially wide swings in both directions and marginal new highs as that longer term upside pattern unfolds (see "ideal" scenario in red on weekly chart/2nd chart below). Bottom line : gains above 2401 favored but the bigger picture magnitude may be limited and versus the start of a major, new surge.

Long term strategy/position:

With gains above 2401 favored looking to switch to bullish but in general would have that longer term strategy of fading the wide extremes. Note also switched the bullish bias that was put in place on Apr 7th at 2360 to neutral below that t-line from Mar (then 2342, closed 2329).

Current:

Nearer term : eventual resumption of gains above 2401, looking for signs of near term bottom to buy.

Last : long Mar 27at 2325,took profit Apr 13 below t-line from Dec (2342, closed 2329, 4pts).

Longer term: at least a few months of wide swings in both directions, looking to fade extremes.

Last : same as shorter term above.

Faith Fades, Bombs Fall

The confidence markets had in the new President and the Republican agenda is rattled. The Australian dollar was the top performer on the day while the Canadian dollar lagged. Japanese industrial production is next. Overnight's Aussie jobs figures exceeded expectations, forcing the Premium service to issue a hedging AUD trade. Our indices trade joins metals deeper in the green.

The quintuple flip-flop from Trump on Wednesday was followed by a fresh bomb in Thursday. This time, it was literally a bomb as US forced dropped a GBU-43/B Massive Ordnance Air Blast in Afghanistan near the Pakistani border. It's now the largest non-atomic bomb ever used in combat.

Markets wobbled a bit on the headlines but takeaways are tough. On the one hand, US officials wouldn't even say if Trump knew about it or authorized its use, so maybe it's nothing but a tactical attack on an enemy dug in deep.

A more sinister view would be that after last week's bombing in Syria, Trump is getting a taste for warfare. He wouldn't be the first leader who campaigned on less aggression and had his feelings change after getting power.

A less-sinister but more-troubling view for markets is that Trump doesn't stand for anything and that Congressional Republicans can't agree on anything. Markets have made a big bet on deregulation, infrastructure spending and tax cuts. Confidence is still high but it's waning and almost daily.

On Thursday, the S&P 500 fell 16 points to 2329 and is now just 7 points above the March low. In FX, the US dollar was strong and the general theme was an unwind of the moves on Wednesday.

We've highlighted bonds lately but 10s were flat on the day. Another spot we're watching closely is volatility. Several measures are disconnecting from markets in a way that could signal trouble ahead. The problem is that many such signals have been wrong in the past but volumes are increasingly large.

Markets are likely to quiet down in the day(s) ahead with Good Friday and Easter holidays. Asia-Pacific trading is mostly open on Friday and the US has decided to release retail sales and CPI into a thin market so that could be notable.

The next even to watch is Japanese industrial production at 0430 GMT. It's the final report and no revisions are expected from the +2.0% m/m prelim data.