Sample Category Title

WTI Crude Oil Hugging $50 at Start of Week

West Texas crude has started the trading week quietly, as the pair trades just above the symbolic $50 in the North American session. On the release front, there is just one major release on the schedule. ISM Manufacturing PMI dropped to 57.2, matching the forecast.

It was a month to forget for crude, as prices sagged 6.0 percent. Weak oil prices is not the scenario that OPEC scripted, as its landmark deal to cut production was supposed to send crude above $60 a barrel and beyond. Instead, prices have fallen since the deal took effect on January 1. OPEC members have kept to the deal, as compliance levels have been exemplary. Still, the world remains awash in oil, as increasing US production has offset the OPEC cuts. US Crude Inventories continue to show surpluses, most of which have been higher than the forecast. Last week, US crude inventories have reached an all-time high of 534.0 million barrels, so oil prices may have trouble staying above the $50 level.

Donald Trump's young presidency has been rocky, with Trump's controversial statements and actions making headlines almost daily. The battles with the media continue, an economic policy remains a mystery, and Trump suffered a major setback as he couldn't even muster a vote over his healthcare bill. Despite these hiccups, the US economy hasn't missed a beat in 2017. The CB consumer confidence report soared to 125.6 in March, and strong consumer confidence levels should translate into increased consumer spending. GDP for the fourth quarter was revised to 2.1%, up from 1.9% in the previous GDP report. This points to strong growth for the economy,

The discussions around the monetary policy tables are not whether the Fed will raise rates, but rather how many times will the Fed press the rate trigger in 2017. The Fed has forecast two more hikes this year, but the markets are looking for three hikes, and the US dollar took a hit last week as the markets were disappointed with the Fed's dovish rate statement. The Fed will release the minutes of its March meeting on Wednesday, and the markets will be looking for clues as to the timing of a possible rate hike.

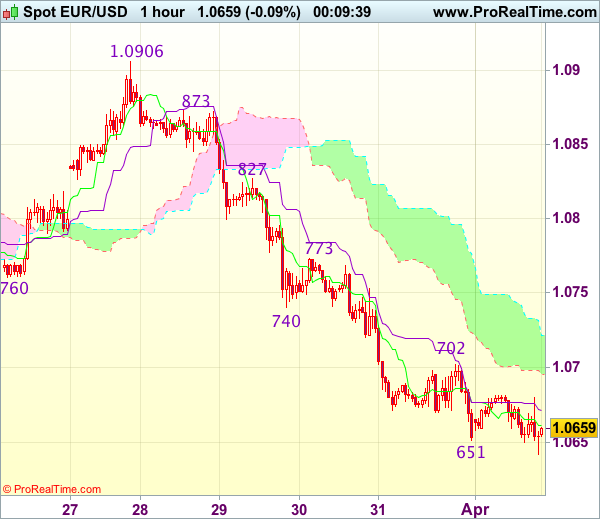

Trade Idea Wrap-up: EUR/USD – Sell at 1.0740

EUR/USD - 1.0658

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.0661

Kijun-Sen level : 1.0672

Ichimoku cloud top : 1.0722

Ichimoku cloud bottom : 1.0695

Original strategy :

Sell at 1.0740, Target: 1.0625, Stop: 1.0775

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0740, Target: 1.0625, Stop: 1.0775

Position : -

Target : -

Stop : -

As the single currency has remained under pressure after last week’s selloff, suggesting the decline from 1.0906 top is still in progress and bearishness remains for this fall to extend further weakness to 1.0620-25, then test of previous chart support at 1.0600, however, a sustained breach below the latter level is needed to retain downside bias for subsequent selloff to 1.0570-75 first, otherwise, risk from there is seen for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0735-40 should limit upside. Only a firm break above resistance at 1.0773 would suggest low is formed instead, bring a stronger rebound to 1.0800 but resistance at 1.0827 should remain intact.

BoC Survey Joins List of Indicators Pointing to Stronger Canadian Economy

Highlights:

- The future sales measure inched lower but remained above its long-run average the long-run average. The 'indicators of future sales' measure rose to a 5-year high.

- Hiring intentions rose for a third consecutive quarter and business machinery and equipment investment intentions jumped to their highest level since Q3 2010 (and matched the second-highest level on record)

- Capacity pressures tightened modestly although indicators of labour shortages eased.

- 94% of respondents expected inflation in the 1% to 3% Bank of Canada target range. That is up from 89% in Q4/16 and with the increase reflecting more respondents expecting growth in the top 2%-3% half of the range.

- Credit conditions eased modestly both from the borrower's perspective and the lender's perspective (from the concurrently released Senior Loan Officer Survey)

Our Take:

The data from the Q1 BOS remains consistent with earlier indicators (GDP growth, for example, is on track to outpace U.S. growth for a third consecutive quarter in Q1/17) pointing to a firming in the Canadian economic backdrop. Expectations for future sales growth moderated but held above long-run average levels and hiring intentions improved for a third consecutive quarter (consistent with strong labour market improvement to-date in 2017). Perhaps most encouragingly, business investment intentions surged to their highest level since Q3 2010, and matched the second-highest reading on record, despite reports of significant uncertainty around the outlook tied to potential trade disruptions and changes to U.S. taxation that could hurt Canadian competitiveness. The business investment intentions in the BOS survey are in sharp contrast to a pull-back in private business investment intentions in a closely-watched annual CAPEX intentions survey from Statistics Canada. The indicator of labour market shortages did tick lower but overall capacity pressures tightened slightly. Bank of Canada Governor Poloz remained adamant last week that, notwithstanding a run of good economic data, the economy continues to run well-below its long-run production capacity. Today's BOS report will not necessarily change the Bank's view ahead of next week's policy decision; however, the longer the run of stronger economic data persists, the harder that position will be to defend.

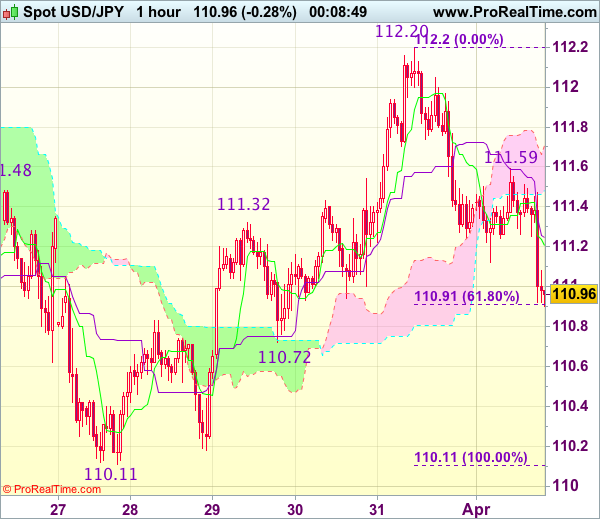

Trade Idea Wrap-up: USD/JPY – Stand aside

USD/JPY - 111.02

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 111.21

Kijun-Sen level : 111.25

Ichimoku cloud top : 111.71

Ichimoku cloud bottom : 111.48

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the greenback has fallen again on renewed cross-buying in yen, adding credence to our view that top has been formed at 112.20 last week and consolidation with mild downside bias remains for test of previous support at 110.72, however, near term oversold condition should limit downside to 110.50 and price should stay well above support at 110.11, bring rebound later.

In view of this, would not chase this fall here and would be prudent to stand aside in the meantime. Above the Kijun-Sen (now at 111.25) would bring recovery to 111.45-50 but break of intra-day resistance at 111.59 is needed to signal low is formed, bring a stronger rebound to 111.90-00 later.

Trade Idea: USD/CAD – Exit short entered at 1.3340

USD/CAD - 1.3359

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

Original strategy :

Sold at 1.3340, Target: 1.3200, Stop: 1.3400

Position: - Short at 1.3340

Target: - 1.3200

Stop: - 1.3400

New strategy :

Exit short entered at 1.3340, Target: 1.3200, Stop: 1.3400

Position: - Short at 1.3340

Target: -

Stop:-

As the greenback has rebounded again after holding above indicated previous support at 1.3264, suggesting further consolidation would be seen, however, reckon upside would be limited and as long as resistance at 1.3415 holds, mild downside bias remains for another decline, below said support at 1.3264 would add credence to our view that top has been made at 1.3535 earlier this month, bring further fall to 1.3235-40 (61.8% Fibonacci retracement of 1.3056-1.3535) and then 1.3200-10, however, oversold condition should limit downside and reckon 1.3170 would hold from here.

In view of this, would be prudent to exit short entered at 1.3340. Above said resistance at 1.3415 would signal low is formed and shift risk back to upside for a stronger rebound to 1.3450 and possibly test of resistance at 1.3479, however, only break of 1.3495 resistance would indicate the pullback from 1.3535 has ended and bring retest of this level later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Gold Steady as ISM Manufacturing PMI Meets Expectations

Gold has posted slight gains in the Monday session. In North American trade, gold is trading at $1252.81 per ounce. On the release front, there is just one major release on the schedule. ISM Manufacturing PMI dropped to 57.2, matching the forecast.

Donald Trump's young presidency has been turbulent, with Trump's controversial statements and actions making headlines almost daily. The battles with the media continue, an economic policy remains a mystery, and Trump suffered a major setback as he couldn't even muster a vote over his healthcare bill. Despite these hiccups, the US economy hasn't missed a beat in 2017. The CB consumer confidence report soared to 125.6 in March, and strong consumer confidence levels should translate into increased consumer spending. GDP for the fourth quarter was revised to 2.1%, up from 1.9% in the previous GDP report. This points to strong growth for the economy,

The discussions around the monetary policy tables are not whether the Fed will raise rates, but rather how many times will the Fed press the rate trigger in 2017. The Fed has forecast two more hikes this year, but the markets are looking for three hikes, and the US dollar took a hit last week as the markets were disappointed with the Fed's dovish rate statement. The Fed will release the minutes of its March meeting on Wednesday, and the markets will be looking for clues as to the timing of a possible rate hike. If the minutes are dovish in tone, gold could head lower.

ISM Manufacturing: Solid Factory Hiring, Rising Prices

The ISM manufacturing index dipped half a point to 57.2 in March, a level still consistent with solid activity in the factory sector. Hiring jumped over the month, while rising input costs pressures did not let up.

Dip in March, but Factory Activity Still Solid

Consistent with many of the regional purchasing managers indices released over the past few weeks, growth in the manufacturing sector looks to have cooled a touch last month. The ISM manufacturing index edged back half a point to 57.2 in March. At that level, however, the factory sector is still expanding at a solid clip.

The largest drag on the headline this month was a pullback in current activity. The production index edged back 5.3 points and is now slightly below its six-month average. The pipeline for activity, however, remains strong. New orders were little changed at 64.5 and remain near a three-year high.

Much of the strength in new orders stems from the improved global backdrop. The index on export orders rose 4.0 points in March. While not seasonally adjusted, the index indicates the fastest pace of export growth since late 2013, when the value of the broad trade-weighted dollar was more than 20 percent lower.

Inventories contracted slightly over the month, which also weighed on the composite index. After entering expansion territory for the first time since mid-2015 in February, the inventory index fell 2.5 points to 49.0. That said, the ISM finds that readings above 42.9 are consistent with growth in manufacturing inventories as measured by the Bureau of Economic Analysis, which is consistent with our call that inventories will not be a drag on growth this year like they were in 2016.

Another Month of Solid Hiring in Manufacturing

Partially offsetting the weaker - although not outright weak - readings in production, new orders and inventories that led to a lower headline in March was improvement in supplier deliveries and employment. Supplier delivery times lengthened in March, with the index rising 1.1 point to 55.9. The biggest improvement in sub-indices, however, came from the employment component. Factory hiring looks to have strengthened materially in March, with the employment index up nearly five points to the highest level since mid-2011. The jump suggests another solid gain in manufacturing payrolls in March, which have increased an average of 19,000 jobs over the past three months.

Inflation Pressures Mounting

Price pressures continue to mount in the factory sector. Lower oil prices in the second half of the month do not appear to have been passed on to manufacturers, who reported no commodities down in price in March. The prices paid index rose to 70.5, which is the fastest rise in input prices in nearly six years and supports our outlook for inflation to rise further over the course of the year.

ISM: U.S. Manufacturing Activity Expands for the Seventh Consecutive Month in March

The Institute for Supply Management (ISM) manufacturing index declined by half a point to 57.2 in March. Nevertheless, despite the slightly slower rate, the U.S. manufacturing sector expanded for the seventh consecutive month. Moreover, the reading was just above consensus forecast that expected a headline number of 57 - a slightly slower rate of expansion than what materialized.

Moves in the subcomponents of the index were mixed, with about half recording an expansion at a faster pace in March. Some of the biggest moves higher included employment (+4.7 to 58.9), new export orders (+4.0 to 59), and prices (+2.5 to 70.5). Of those subcomponents that recorded a decline in March, production fell the most (-5.3 to 57.6), followed by inventories (-2.5 to 49) and new orders (-0.6 to 64.5).

Given the greater decline in inventories that offset the much smaller decline in new orders, the spread between the two - useful as a leading indicator of activity - widened slightly in March to 15.5 from 13.6 in February. This suggests that manufacturing activity is likely to continue to expand in the months ahead.

No industry reported contractions, with seventeen of the eighteen reporting expansion in March. Electrical equipment appliances and components, printing and related support activities, and furniture and related products all registered the strongest expansion in the month.

Key Implications

Despite the pace of expansion in the headline index slowing slightly in March, the underlying details of this morning's ISM manufacturing report are broadly positive. The U.S. manufacturing sector expanded at a robust pace in the first quarter, although momentum appears to have slowed. All categories except inventories and customers' inventories are healthy, while both new orders and production remain resilient despite taking a breather in March. Comments by survey respondents were broadly positive, with an acknowledgement by some that rising input prices are being passed on to buyers via higher sales prices.

Despite its recent strong showing, the U.S. manufacturing sector is likely to continue to face a number of challenges this year. For one, although the trade weighted dollar has given up its gains from early in the year, it still remains about 3% above the level from a year ago and is expected to continue to dampen the export competitiveness of U.S. firms. Perhaps another more important concern is the elevated level of policy uncertainty both globally and domestically, particularly surrounding any changes to the U.S. trading relationship with the rest of the world. Given U.S. manufacturers strong integration in global value chains, any material changes to U.S. trade policies could destabilize and do more harm than good as far as domestic industries are concerned in the short to medium term.

March ISM data for the U.S. manufacturing sector mirrors the good news from other purchasing manager's surveys for Europe, Japan, India, and other large emerging markets released this morning. The momentum from the strong pickup in global growth from last year has likely carried through March, suggesting a strong handoff into the second quarter. Still, although there has only been a slow trickle of non-survey based economic data for 2017 thus far, we anticipate that the global economy is on pace to expand at an above 3.0% rate in the first half of 2017.

Bank of Canada Business Outlook & Senior Loan Officer Surveys: Firms Remained Optimistic in Early 2017

The Bank of Canada's quarterly Business Outlook Survey (BOS) pointed to continued optimism among Canadian businesses, supported by gains in indicators of future sales and further improved investment intentions.

On a backward-looking basis, sales growth has been stable, with the balance of opinion remaining effectively unchanged for a seventh straight quarter (balance of opinion: +2). On a forward-looking basis it was a more positive story. Sentiment for sales over the next 12 months fell slightly on balance, but remained near recent highs at +21. Moreover, the 'indicator of future sales' (based on order books, sales inquiries, etc.) climbed sharply, reaching +46 (Q4 survey: +32). Rebounds in energy-related activity and the level of the loonie were both cited as factors supporting the sales outlook.

Firms were also more optimistic regarding the outlook for investment. At +35, the balance of opinion on investment now sits near all-time highs as the share of firms planning to decrease spending dropped for a fourth straight quarter. Although sentiment improved, the Bank of Canada noted that many firms expect the anticipated increase in spending to be "modest" in scope.

Hiring intentions were effectively unchanged from the previous survey, as more than half of firms expect to increase their staffing levels.

There was not much reported in terms of burgeoning price pressures. The pace of output price growth is expected to remain around current levels on balance despite a modestly positive balance of sentiment around input prices. Consistent with this, 64% of respondents expect inflation over the next two years to be between 1% and 2%, with only 30% expecting price growth of 2% to 3%.

Senior Loan Officer Survey

The Bank of Canada also released its Senior Loan Officer Survey, which pointed to a third quarter of effectively unchanged business lending conditions. In aggregate, both price and non-price conditions were unchanged. Overall demand for credit was reported to have decreased in the first quarter owing to substitution to capital market fundraising among corporate borrowers.

Key Implications

Add another tick to the 'plus' column for the Canadian economy. Canadian firms remained optimistic on balance, and the details of the report were encouraging. Although there are caveats around what pace it may translate to, investment intentions are sitting at historic highs, and the outlook for hiring remains healthy. The BOS suggests that while the hot pace of first quarter activity is not likely to be repeated, it may be reasonable to expect solid economic momentum as we head into the remainder of 2017.

The Bank of Canada is undoubtedly pleased with today's report, but it is not likely to change the dovish tone of recent communications. Governor Poloz has remained focused on the downside risks, and the possibility that Canada may be in the midst of a 'false start'. To his point, the outlook for machinery and equipment investment showed steady improvement throughout 2016, outlook for machinery and equipment investment showed steady improvement throughout 2016, and yet actual investment fell over this time (although a box in today's report suggests that the BOS as a whole may provide a better indication of the path of investment). Until intentions begin translating into actual investment, Bank of Canada officials appear likely to downplay today's BOS and the recent improvement in the Canadian economic data more broadly.

Japanese Yen Shrugs Mixed Tankan Indices

The Japanese yen has edged higher in the Monday session. In North American trade, USD/JPY is trading at the 111 line. On the release front, the Japanese Tankan indices were a mixed bag. The Tankan Manufacturing Index improved to 12, short of the forecast of 14 points. The Tankan Non-Manufacturing Index climbed to 20, edging above the forecast of 19 points. In the US, ISM Manufacturing PMI dropped to 57.2, matching the forecast.

What can the markets expect from the Bank of Japan? According to the summary of the minutes, which were released last week, we're likely to see "more of the same" as far as monetary policy. There were no surprises from the summary, as policymakers said the BoJ's ultra-easy monetary stance would continue as long as inflation remains well below the target of 2 percent. Japan's economy has improved in recent months, boosted by a stronger manufacturing sector and an increase in exports. At the same time, domestic demand remains soft, which has resulted in weak inflation levels.

Donald Trump's young presidency has been turbulent, with Trump's controversial statements and actions making headlines almost daily. The battles with the media continue, an economic policy remains a mystery, and Trump suffered a major setback as he couldn't even muster a vote over his healthcare bill. Despite these hiccups, the US economy hasn't missed a beat in 2017. The CB consumer confidence report soared to 125.6 in March, and strong consumer confidence levels should translate into increased consumer spending. GDP for the fourth quarter was revised to 2.1%, up from 1.9% in the previous GDP report. This points to strong growth for the economy, as the discussions around the monetary policy tables are not whether the Fed will raise rates, but will it press the rate trigger twice or three times in 2017. The Fed will release the minutes of its March meeting on Wednesday, and the markets will be looking for clues as to the timing of a possible rate hike.