Sample Category Title

Copper Attempts to Break Its Mid-April $6.10 Spike – On the Way to New ATH? XCU/USD Outlook

- Copper and other metals are exploding higher from the elevated hopes of a conflict resolution

- Profiting from the tumble in the US Dollar, the Metal is retesting its early April highs and looks to break higher

- US Dollar Index (DXY) in-depth Technical Analysis

After a rough end of April, Copper and other metals are surging today, driven by growing optimism for a clear diplomatic solution to the conflict in the Middle East.

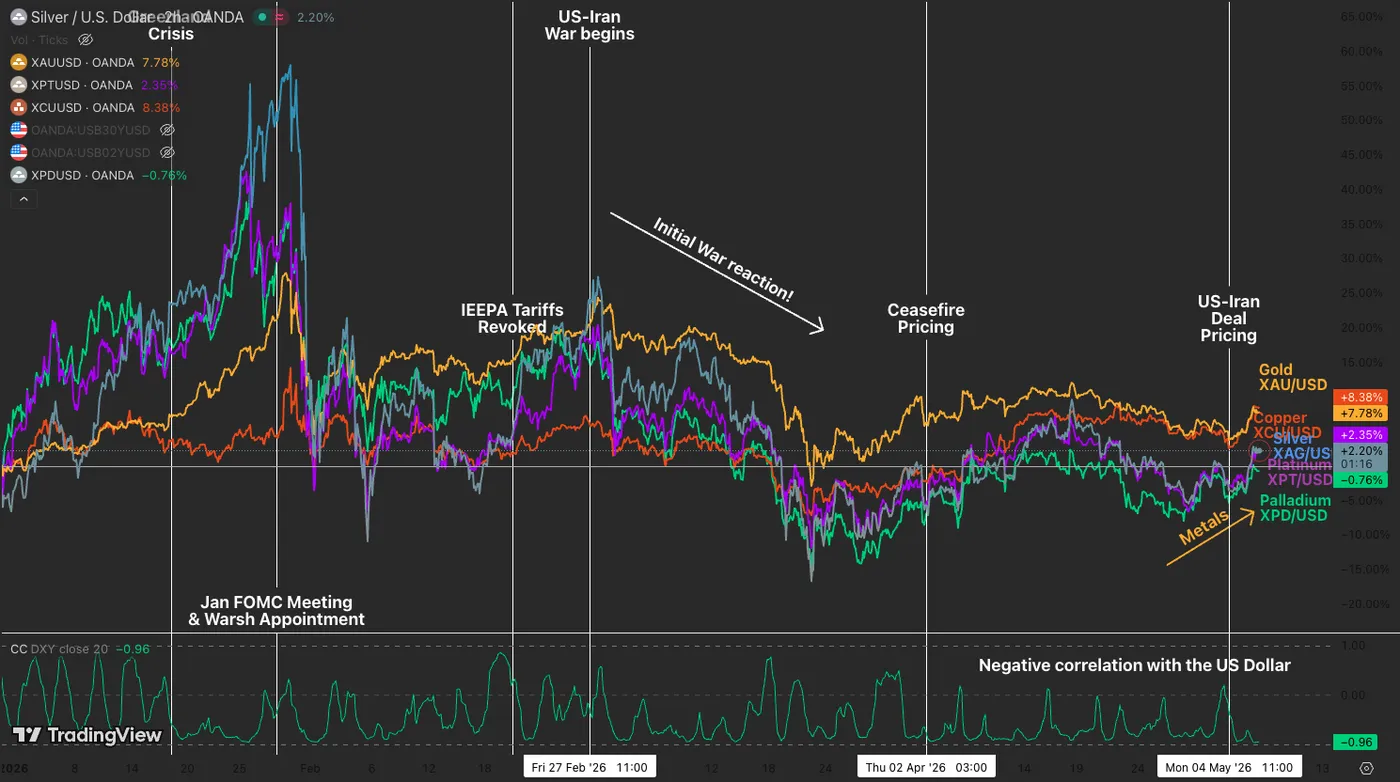

Since early 2025 and particularly since the start of the War, the metals market is showing an unusual pattern, moving in the opposite direction of the US Dollar. In the past, metals have often served as a defensive alternative when stocks are volatile.

But since this conflict began, metals and stocks have mostly moved together, reacting strongly to changes in geopolitical tension and relief.

Metals Performance in 2026 and Dollar Index Correlation – Source: TradingView

Copper has been making headlines, outperforming gold at the start of the year.

Copper is benefiting from today’s sharp drop in the US Dollar. It is now retesting its early April highs and appears ready to move even higher. But, in addition to short-term correlation factors, copper is getting strong support from major long-term trends.

The growth of AI infrastructure and heavy capital spending by large tech companies are driving demand for copper, which is needed for advanced data center circuits and cooling systems.

On top of that, large investments are planned to upgrade and modernize North America’s electrical grid. All of this is fueling strong interest in copper.

Metals Performance (15:03) – Source: TradingView. May 6, 2026

Overall, while copper is traditionally known as a highly cyclical industrial metal, standard cyclicality has simply not been dictating its recent price action.

On the contrary, these massive swings have been almost entirely explained by movements in the US Dollar. Luckily for copper bulls, the greenback is aggressively falling off the table in today's session, removing the primary overhead headwind.

Riding this perfect storm of fundamental demand and currency weakness, prices are now actively trying to push decisively beyond the massive $6.10 high established in April.

We’ll explore a few scenarios for upcoming action in an in-depth technical analysis of Copper (XCU/USD) as the metal attempts to break resistance.

Copper (XCU/USD) Multi-Timeframe Analysis

Daily Chart

Copper (XCU/USD) Daily Chart. May 6, 2026 – Source: TradingView

After its past month's 17% rise to $6.10, Copper could not resist the rough patch in the metals Market and pulled back close to 6% right back to its 50-Day moving average.

As seen throughout the 2025 bull trend, the asset class moves particularly strongly when reaching and breaching its Daily MAs, so this is a trend to keep your eyes on as traders.

The ongoing bounce is impressive as it erased more than two-weeks of progressive correction in two sessions, and the bull candles are now testing the key $6.10 resistance; above this, there isn't much that can stall the move back to the all-time highs ($6.50).

4H Chart and Technical Levels

Copper (XCU/USD) 4H Chart. May 6, 2026 – Source: TradingView

The intraday action is currently forming a tight bull channel to higher levels, and with the RSI reaching overbought levels, the ongoing rally could somewhat stall.

Still, higher timeframe momentum hasn't been so extreme yet, so this could see small consolidation which could then lead to continued upside, with the next stop at $6.20.

As mentioned in the introduction, Metals are moving on peace prospects, hence a clean deal will be awaited to confirm a continued path to all-time highs – Make sure to track the latest narratives around the peace process.

Higher Timeframe Levels to watch for Copper (XCU/USD):

Resistance Levels:

- $6.10 Early Jan 2026 and April Record (testing the upper bound)

- Psychological Resistance $6.20 to $6.25

- Current ATH Resistance $6.40 to $6.50

- $6.52 Current Record

- Potential Resistance $6.90 to $7.00

Support Levels:

- 4H 200-period MA / 50-day MA $5.76

- Momentum Pivot $5.70 to $5.90 Bullish above, Bearish Below recent bounce

- Minor Support at March 2025 Highs $5.40 to $5.50

- War lows $5.18

- 200-Day MA $5.24

- Major Monthly Support between $4.90 to $5.00

Safe Trades and keep track of the latest headlines!

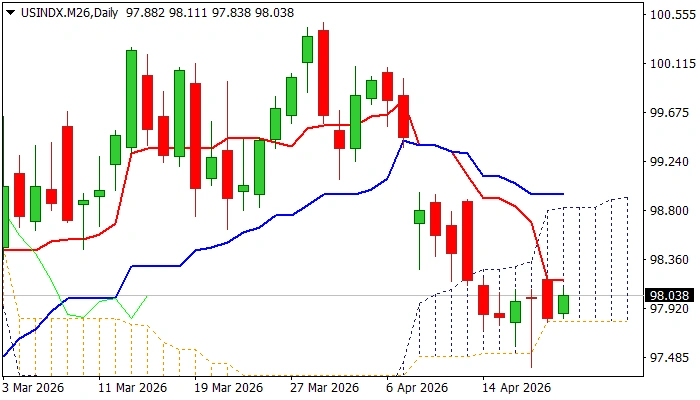

DXY: Dollar Probes Through Key supports Again as Fresh Optimism Fades Safe Haven Demand

The dollar came under increased pressure on Wednesday after fresh wave of optimism about a possible end of US-Iran war deflated safe-haven demand.

The dollar index, which tracks the performance of Greenback against its six major peers, hit three-week low, on renewed probe through the trendline support (currently at $97.85), after several recent attacks failed to register clear break of the trendline.

Support is reinforced by the base of thick daily cloud and 50% retracement of $95.35/$100.48 rally) that add to its significance.

Sustained break lower is needed to confirm bearish signal and open way for continuation of the downtrend from $100.48 (2026 high, posted on Mar 31) and expose next target at $97.31 (Fibo 61.8%).

Caution on potential repeated failure at trendline support, though near-term focus is expected to remain at the downside, as daily studies are in bearish configuration (reinforced by the latest 20/200DMA and 20/100 DMA bear-crosses and falling 14-d momentum entering negative territory).

Also keep focus on dynamics of peace talks in the Middle East, as geopolitics remain one of key dollar drivers nowadays.

Res: 97.90; 98.20; 98.43; 98.52

Sup: 97.50; 97.31; 97.00; 96.56

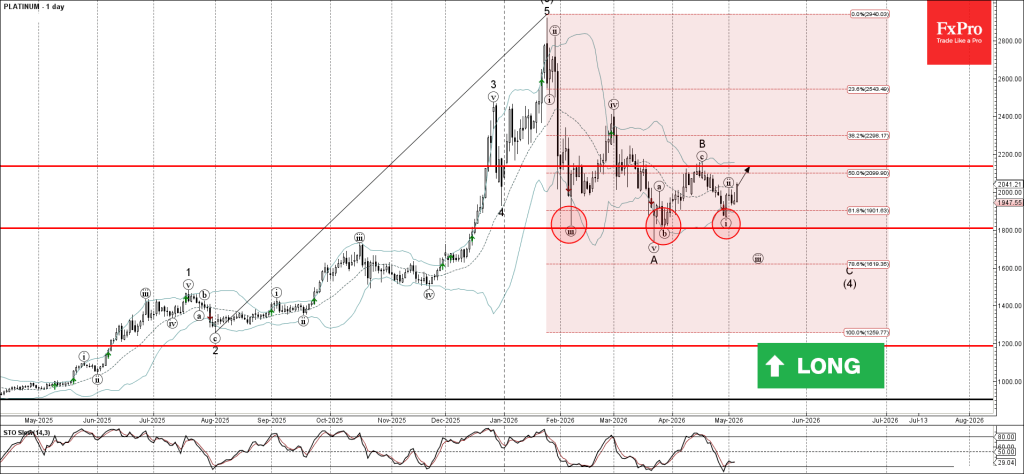

Platinum Wave Analysis

Platinum: ⬆️ Buy

- Platinum reversed from support zone

- Likely to rise to resistance level 2140.00

Platinum recently reversed up from the support zone between the pivotal support level 1800.00 (former multi-month low from February), lower daily Bollinger Band and the 61.8% Fibonacci correction of the upward impulse from July.

The upward reversal from this support level 1800.00 started the active minor correction ii.

Given the overriding daily uptrend, Platinum can be expected to rise to the next resistance level 2140.00. (top of the previous correction B).

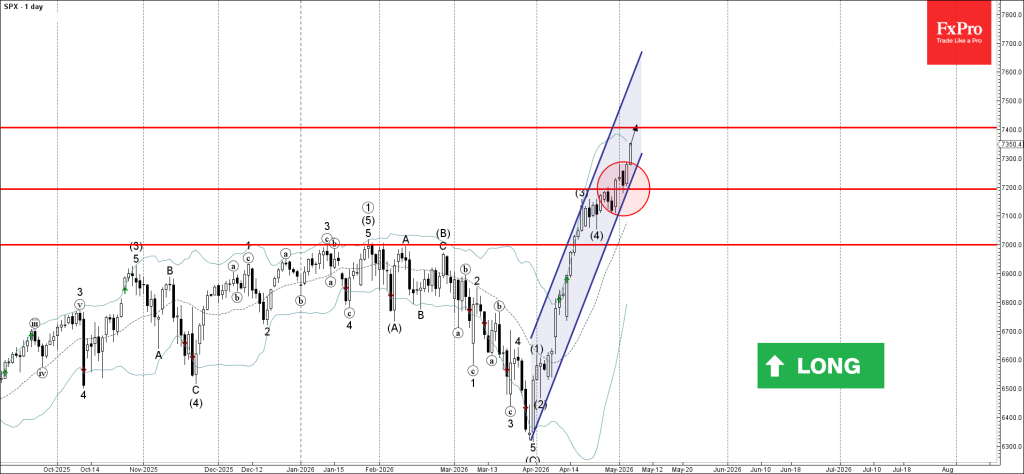

S&P 500 Wave Analysis

S&P 500: ⬆️ Buy

- S&P 500 reversed from support level 7200.00

- Likely to rise to resistance level 7400.00

S&P 500 index recently reversed up from the support level 7200.00 (former resistance from the end of April, acting as the support after it was broken earlier).

The support zone near the support level 7200.00 was strengthened by the 20-day moving average and by the support trendline of the daily up channel from March.

Given the strong daily uptrend, S&P 500 index can be expected to rise to the next resistance level 7400.00. (target price for the completion of the active impulse wave (5)).

Eco Data 5/7/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Apr | -11.30% | -10.50% | -11.60% | |

| 23:50 | JPY | BoJ Minutes | ||||

| 01:30 | AUD | Trade Balance (AUD) Mar | -1.84B | 4.45B | 5.69B | 5.03B |

| 06:00 | EUR | Germany Factory Orders M/M Mar | 5.00% | 1.10% | 0.90% | |

| 07:00 | CHF | Foreign Currency Reserves *CHF) Apr | 716B | 721B | ||

| 08:00 | CHF | Unemployment Rate M/M Apr | 3.00% | 3.00% | 3.00% | |

| 08:30 | GBP | Construction PMI Apr | 39.7 | 46.2 | 45.6 | |

| 09:00 | EUR | Eurozone Retail Sales M/M Mar | -0.10% | -0.40% | -0.20% | |

| 12:30 | USD | Initial Jobless Claims (May 1) | 200K | 199K | 189K | 190K |

| 12:30 | USD | Nonfarm Productivity Q1 P | 0.80% | 0.70% | 1.80% | |

| 12:30 | USD | Unit Labor Costs Q1 P | 2.30% | 2.60% | 4.40% | |

| 14:30 | USD | Natural Gas Storage (May 1) | 72B | 79B |

| 23:50 | JPY |

| Monetary Base Y/Y Apr | |

| Actual | -11.30% |

| Consensus | -10.50% |

| Previous | -11.60% |

| 23:50 | JPY |

| BoJ Minutes | |

| Actual | |

| Consensus | |

| Previous | |

| 01:30 | AUD |

| Trade Balance (AUD) Mar | |

| Actual | -1.84B |

| Consensus | 4.45B |

| Previous | 5.69B |

| Revised | 5.03B |

| 06:00 | EUR |

| Germany Factory Orders M/M Mar | |

| Actual | 5.00% |

| Consensus | 1.10% |

| Previous | 0.90% |

| 07:00 | CHF |

| Foreign Currency Reserves *CHF) Apr | |

| Actual | 716B |

| Consensus | |

| Previous | 721B |

| 08:00 | CHF |

| Unemployment Rate M/M Apr | |

| Actual | 3.00% |

| Consensus | 3.00% |

| Previous | 3.00% |

| 08:30 | GBP |

| Construction PMI Apr | |

| Actual | 39.7 |

| Consensus | 46.2 |

| Previous | 45.6 |

| 09:00 | EUR |

| Eurozone Retail Sales M/M Mar | |

| Actual | -0.10% |

| Consensus | -0.40% |

| Previous | -0.20% |

| 12:30 | USD |

| Initial Jobless Claims (May 1) | |

| Actual | 200K |

| Consensus | 199K |

| Previous | 189K |

| Revised | 190K |

| 12:30 | USD |

| Nonfarm Productivity Q1 P | |

| Actual | 0.80% |

| Consensus | 0.70% |

| Previous | 1.80% |

| 12:30 | USD |

| Unit Labor Costs Q1 P | |

| Actual | 2.30% |

| Consensus | 2.60% |

| Previous | 4.40% |

| 14:30 | USD |

| Natural Gas Storage (May 1) | |

| Actual | |

| Consensus | 72B |

| Previous | 79B |

Brent Heading Towards De-escalation

- The markets are betting on a swift resolution to the US-Iran conflict.

- The fall in Brent and WTI prices is likely to be sharp but short-lived.

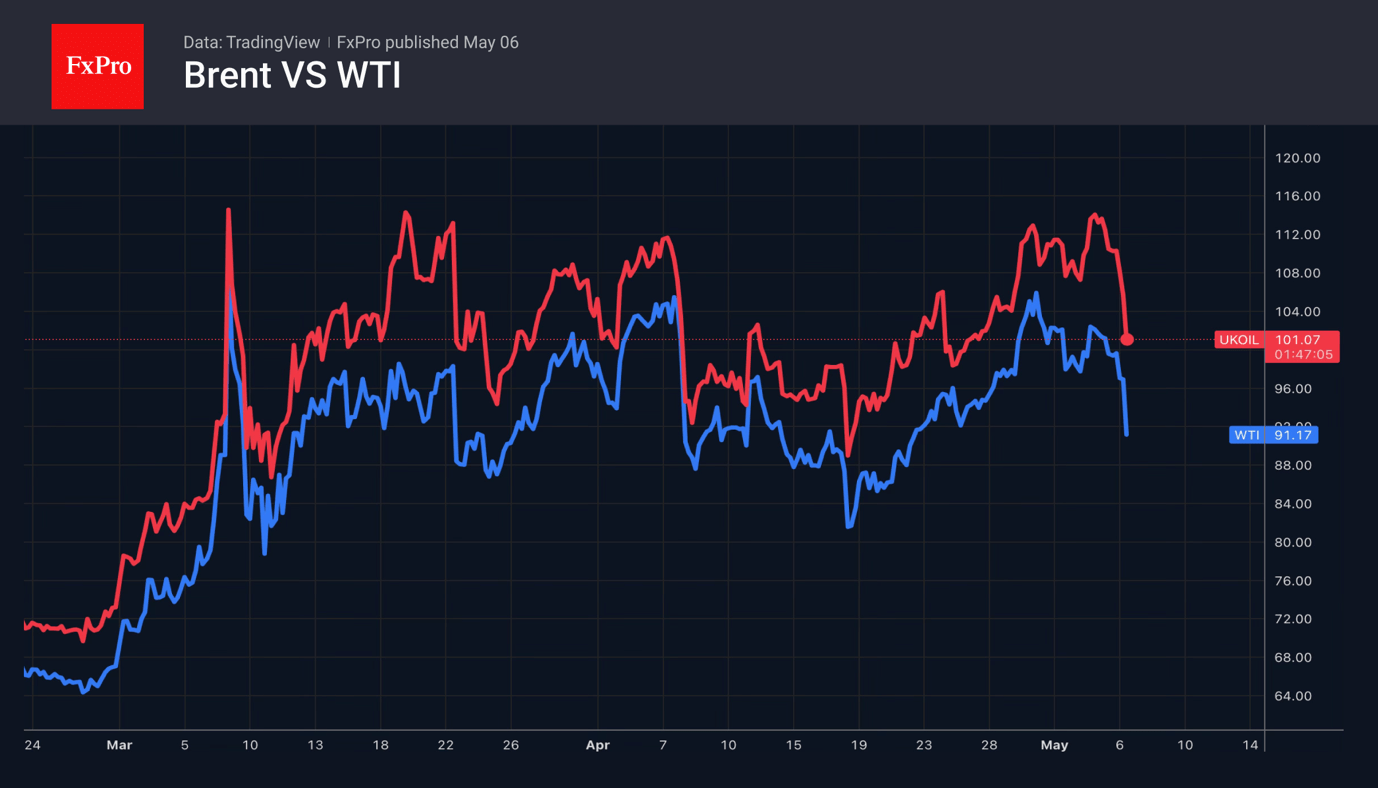

At the start of the week, the nearest Brent futures contract once again exceeded $113, hitting the ceiling formed since the start of the armed conflict in the Middle East following news that Iran had resumed attacks on the UAE’s energy infrastructure. However, on Wednesday, Brent crude fell by more than 10% intraday to $97, as the US announced the maintenance of the ceasefire and the conclusion of Operation Epic Fury. Donald Trump announced progress in negotiations with Tehran, and the latter noted that it was ready to strike a deal. This is a rather unusual turn of events, as we have almost become accustomed to a stream of contradictory statements.

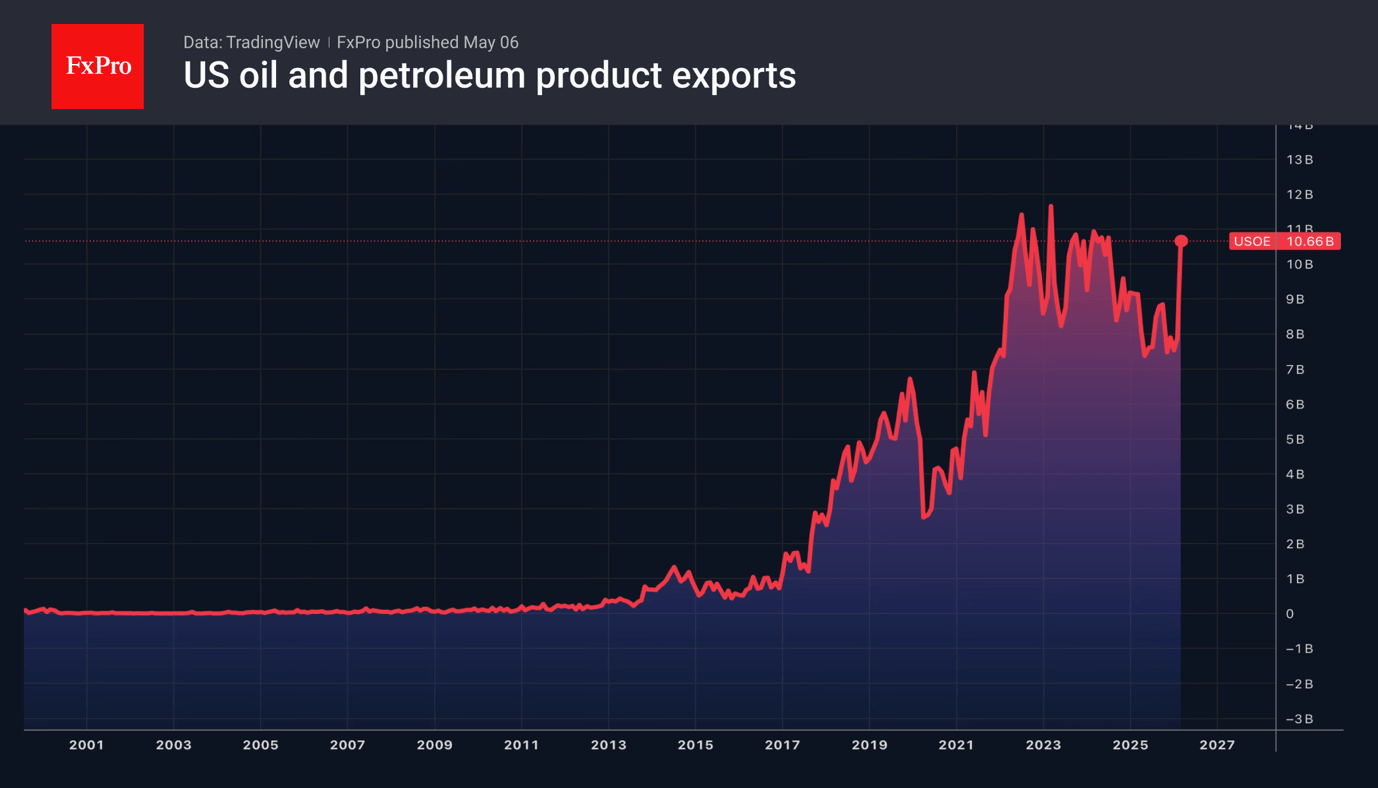

Looking to the future, markets are taking the words at face value, viewing the figures as a snapshot of the past. But in any case, Iran’s attacks on Fujairah have sparked fires and threaten to reduce global supply by a further 1.9 million bpd. Global oil reserves are rapidly dwindling. And the US has found itself in a better position to catch a tailwind, having become the world’s largest oil exporter, with around 6 million bpd, surpassing Saudi Arabia. In theory, the figure could reach 10 million bpd, but in practice, the ceiling is much lower, around 6–7 million bpd.

Russia has also benefited from the crisis in the Middle East. Its average crude oil flows over the past four weeks have jumped to their highest levels since December. Export revenue reached $2.42 billion for the week ending 3 May, the highest since February 2022.

Washington’s optimistic rhetoric and its reluctance to escalate tensions are allowing markets to view a peace agreement between the US and Iran as the base case scenario. A rapid resumption of shipping will lead to a short-term surge in supply from tankers stranded in the Strait of Hormuz, pushing down the price of Brent and WTI.

However, the depletion of global stocks and the time required to repair the damaged infrastructure in the Gulf states suggest that oil is unlikely to fall back to the levels seen at the end of February – below $72 for Brent and $67 for WTI – by the end of the year. Under this scenario, international trade risks losing more than 0.5 percentage points of growth. The World Trade Organisation’s March forecasts suggest a slowdown in growth from 4.6% in 2025 to 1.9% in 2026, with a partial recovery to 2.6% in 2027.

Sunset Market Commentary

Markets

Trading is extremely headline-driven today. This week’s build-up led markets to really pursue positive headlines for the first time since the cease-fire deadline was extended mid-April. US President Trump’s downplaying of Iranian missile and drone attacks against the UAE and his rapid pause to “Project Freedom” (helping navigate vessels through Hormuz) led markets into believing that something was cooking. An Axios report suggesting that the US and Iran were closing in on a one-page memo to end the war ignited a risk rally which pushed European equity indices initially more than 3% higher. The EuroStoxx50 approached the mid-April high in the process. Brent crude prices sank from $109/b to $97/b with core bond yield curves bull steepening. The difference between the intraday top and bottom for the EU 2y swap rate amounted to 13 bps. The US dollar faced a setback with EUR/USD moving from 1.1725 to an intraday top just shy of 1.18. It soon turned out that markets were again running ahead of themselves. It started with Iran downplaying the “US media campaign” with the US plan containing ambitious, unrealistic proposals. A threat by US President Trump to start bombing the country again, and at a much higher level than before, unless they agree to (US) terms came next. An Iranian spokesmen for the National Security and Foreign Policy Commission responded almost immediately by suggesting that violence will be met by violence. US President Trump later told the NY Post that it was too soon to prepare for an Iranian peace signing. Finally, some Pakistani sources sounded again more optimistic suggesting that a draft agreement is in place. It would set a timetable for upcoming negotiation rounds and setting a timetable for ending all hostile activities, including reopening Hormuz to international navigation. Unlike a few hours earlier, markets decided not to chase these latest headlines. At the time of writing, Brent crude trades back at $103/b and EUR/USD at 1.1750. The EMU swap rate curve still bear flattens but with daily changes varying between -9 bps (2-yr) and -3 bps (30-yr).

In other news, there was a strong though slightly below consensus US ADP employment report for the month of April. US firms added 109k jobs which was the first 100k+ outcome since January 2025. The report also showed that workers who changed jobs saw a 6.6% Y/Y pay increase with wage growth for those who kept their jobs was 4.4%. Today’s report validates last week’s hawkish hold by the Fed, putting the focus back (solely) on inflation for now. US Treasuries still rallied on the Axios reports, but underperform Bunds and Gilts. Daily changes on the US curve range between -7 bps (5-yr) and -5 bps (30-yr).

News & Views

Swedish inflation surprised to the downside in April. A monthly -0.6% drop fully offsets March’s same-sized increase. Details are not available yet but it’s assumed that a VAT decline (6% from 12%) for food has outweighed rising energy prices in the headline print. The annual reading halved to 0.8% from 1.6% to hit a five year low. Excluding energy, core inflation fell 0.6% m/m to stagnate on a yearly basis for the first time in three decades and missing the 0.4% bar. The central bank in its March meeting had outlined a scenario in which higher energy prices and the pass-through to other segments could warrant rate hikes, even if that comes at the cost of the economy. Today’s inflation numbers allow the Riksbank to bide some time given the rapidly changing geopolitical environment. Market optimism towards a US-Iran deal is overshadowing the data release. While money market pricing for Riksbank hikes dropped dramatically to just 60% in 2026H2 (vs 1.5 hike priced in just yesterday), the constructive risk sentiment tempers any losses for the Swedish krone. EUR/SEK stabilizes around 10.83.

Czech April CPI surprised to the upside (0.5% m/m, 2.5% y/y), driven mainly by energy and fuels (+2.3% m/m) amid faster-than-expected pass-through from utility pricing. Core dynamics were more mixed: services inflation remains elevated (+/-5%), and firmer non-energy goods prices may signal emerging second-round effects from higher oil, offset in part by ongoing food deflation. KBC Economics expects inflation to hover around 2.5% in coming months before edging toward 3% by year-end and higher in early 2027. Risks are skewed to the upside however, with the monetary policy outlook hinging on whether price pressures broaden further beyond energy. The central bank meets tomorrow and is bound to keep the policy rate steady for now, particularly in the light of the recent Gulf developments. EUR/CZK drops to 24.34 amid a benign risk backdrop.

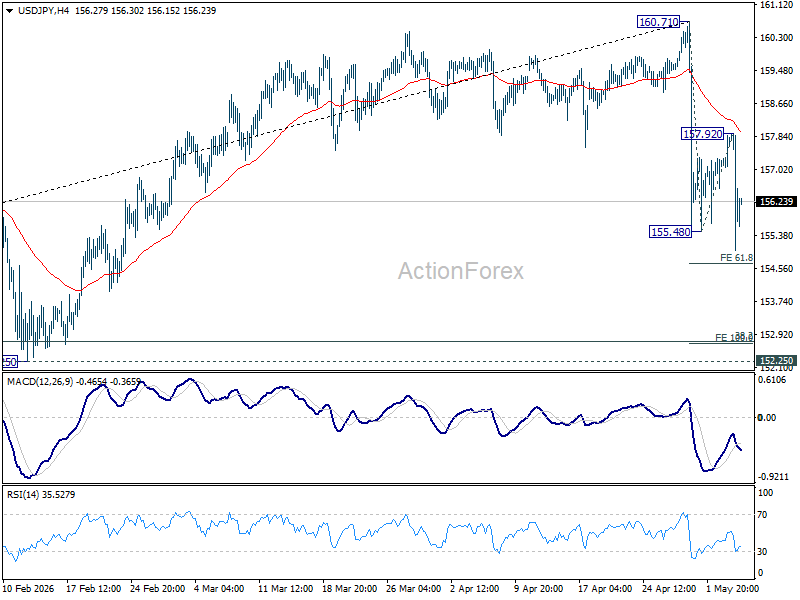

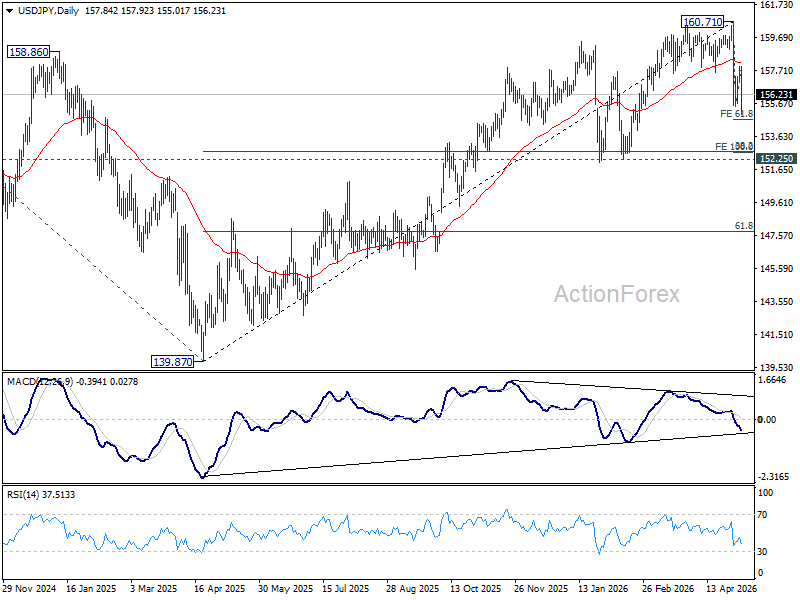

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.35; (P) 157.63; (R1) 158.18; More...

Intraday bias in USD/JPY remains on the downside. Fall from 160.71 would continue to 61.8% projection of 160.71 to 155.48 from 157.92 at 154.68. Firm break there will target 100% projection at 152.69. That would be close to key 152.25 cluster support (38.2% retracement of 139.87 to 160.71 at 152.74). For now, risk will stay on the downside as long as 157.92 resistance holds, in case of recovery.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.01) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

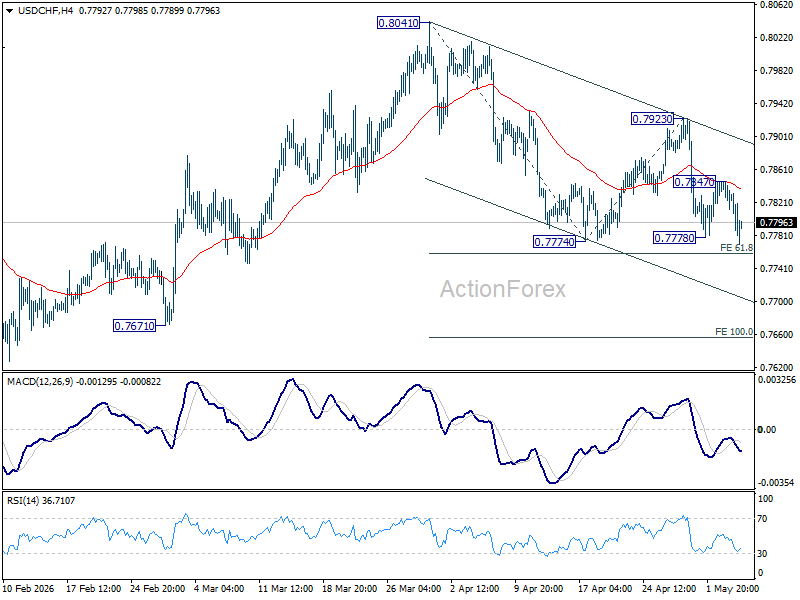

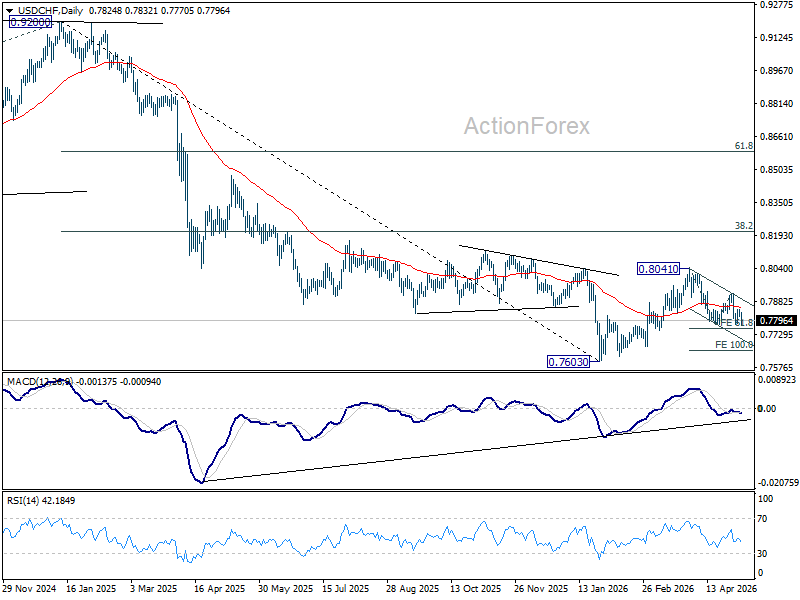

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7813; (P) 0.7832; (R1) 0.7851; More….

Intraday bias is back on the downside with breach of 0.7774 support, and fall from 0.8041 could be resumption. Firm break of 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758 will target 100% projection at 0.7656. On the upside, above 0.7847 minor resistance will turn bias neutral again.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8042) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

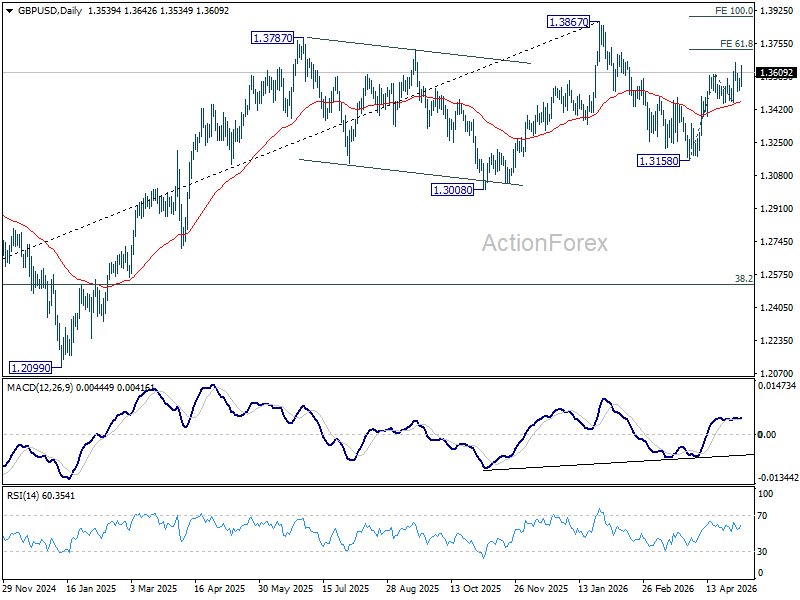

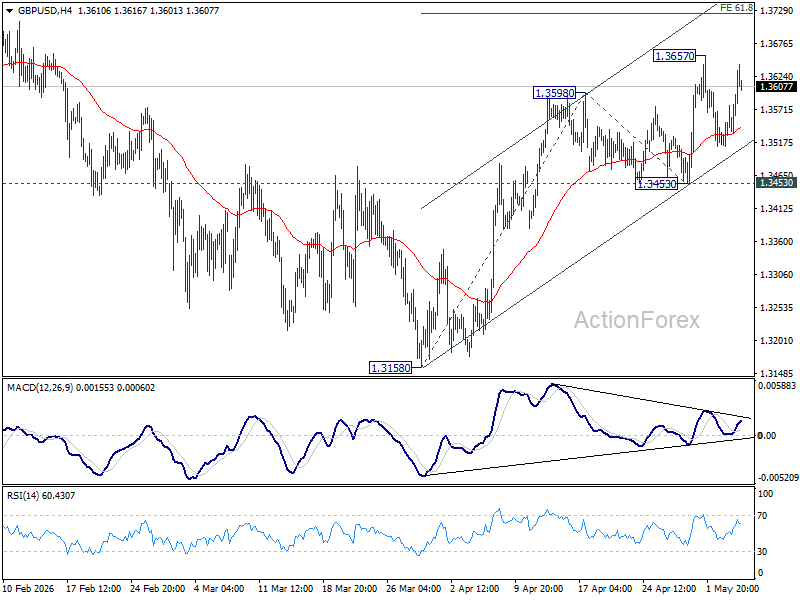

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3508; (P) 1.3544; (R1) 1.3574; More...

GBP/USD is still staying below 1.3657 despite today's rebound. Intraday bias is remains neutral for the moment. With 1.3453 support intact, further rise is expected. On the upside, above 1.3657 will target 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high. However, break of 1.3453 will turn bias back to the downside for 1.3158 support instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).