Sample Category Title

Sunset Market Commentary

Markets

With the policy meetings of major central banks having passed last week, markets today returned their focus to the conflict in the Middle East. The latest political development was labelled “Project Freedom”, with President Trump indicating that the U.S. would guide stranded ships in the Persian Gulf through the Strait of Hormuz.

Looking at oil prices, markets were not convinced this would help resolve the conflict. Brent crude at the European open moved back above $110/bbl. Skepticism proved justified as conflicting reports emerged regarding an incident involving a U.S. naval vessel entering the Strait of Hormuz. Later, U.S. Treasury Secretary Bessent reiterated that the U.S. is reopening Hormuz.

Whatever the underlying reality, oil prices do not yet signal any meaningful progress toward coordinated de-escalation. Central bankers, including the BoE and ECB, warned last week that a prolonged period of elevated oil prices and supply disruptions could force tighter policy.

U.S. and European yields reversed part of last Thursday’s decline, returning to a bear-flattening pattern alongside rising oil prices. U.S. yields gained between 3.5–4.5 bps, while German yields rose between 1.5–4 bps. A series of ECB speakers reiterated differing views along the hawkish-dovish spectrum.

Slovak ECB member Kazimir stood out, stating that “policy tightening in June was all but inevitable” as broad-based inflation risks increase. Others, including outgoing ECB member Villeroy, adopted a more balanced tone, though most acknowledged growing pass-through risks.

European equities struggled to follow tech-driven gains in parts of Asia and came under pressure as oil prices and yields moved higher (Eurostoxx 50 -0.85%). U.S. indices opened little changed.

On FX markets, the dollar is gaining on lingering geopolitical uncertainty and rising oil prices, though most moves remain technically limited. DXY trades near 98.40 (from 98.05), while EUR/USD holds near 1.17 despite some downside pressure.

The euro has so far shown limited damage from higher oil prices and renewed trade tensions, including President Trump’s threat to raise tariffs on EU autos to 25%.

Japanese markets remain closed for Golden Week, but markets are alert to potential yen-supportive intervention from the Ministry of Finance. Authorities reiterated their readiness to act against speculative moves. Despite a brief yen strengthening earlier, USD/JPY is little changed around 157.1.

News & Views

The Czech manufacturing PMI stabilized at 52.9 in April, beating expectations of 51.4. Output and new orders expanded despite significant supply chain disruptions. Firms increased input buying and stockpiling amid shortages linked to the Gulf conflict.

Supplier performance deteriorated sharply, marking the steepest decline in quality since mid-2022. Business confidence weakened, while cost pressures rose significantly.

Operating expenses surged at the fastest pace in nearly four years, with output prices accelerating to their strongest level since January 2023. Firms are increasingly absorbing costs through margin compression.

The ECB’s Survey of Professional Forecasters (Q2 2026) showed upward revisions to inflation expectations. Headline HICP is now seen at 2.7% for 2026 (from 1.8%) and 2.1% for 2027 (from 2%).

This aligns closely with the ECB’s March projections, which President Lagarde recently suggested are becoming outdated. Core inflation is now projected at 2.2% across the policy horizon, up from 2.0% previously.

Wage growth expectations also increased, averaging 3.3%, 3.1%, and 2.9% for 2026–2028. Long-term inflation expectations remain anchored at 2%.

Growth expectations were revised slightly lower, with GDP now seen at 1.0% for 2026 (from 1.2%), before stabilizing around 1.3% in 2027–2028.

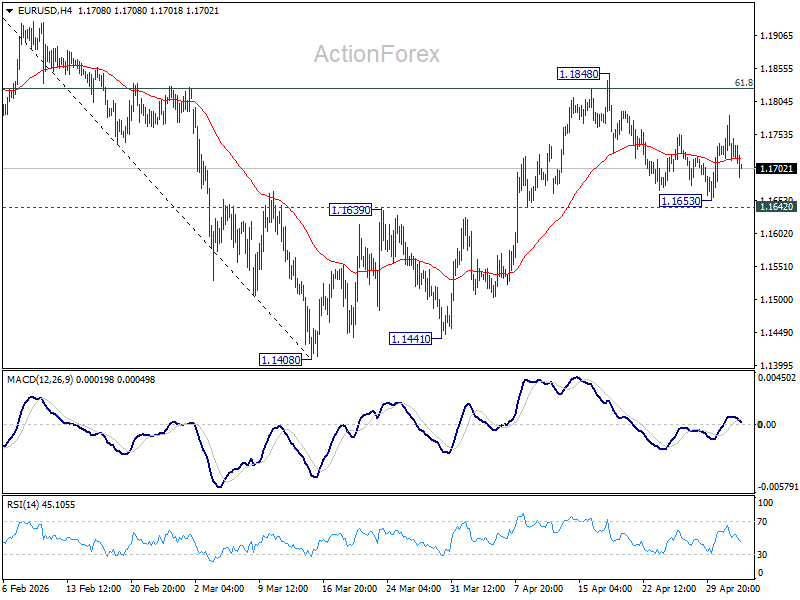

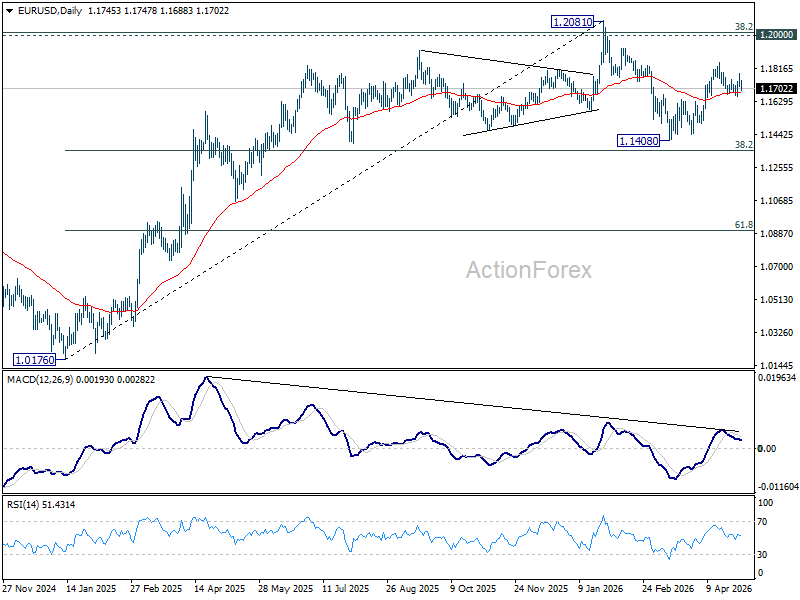

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1696; (P) 1.1741; (R1) 1.1767; More….

Sideway trading continues in EUR/USD and intraday bias remains neutral. Rise from 1.1408 is expected to continue as long as 1.1642 support holds. Firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1537). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

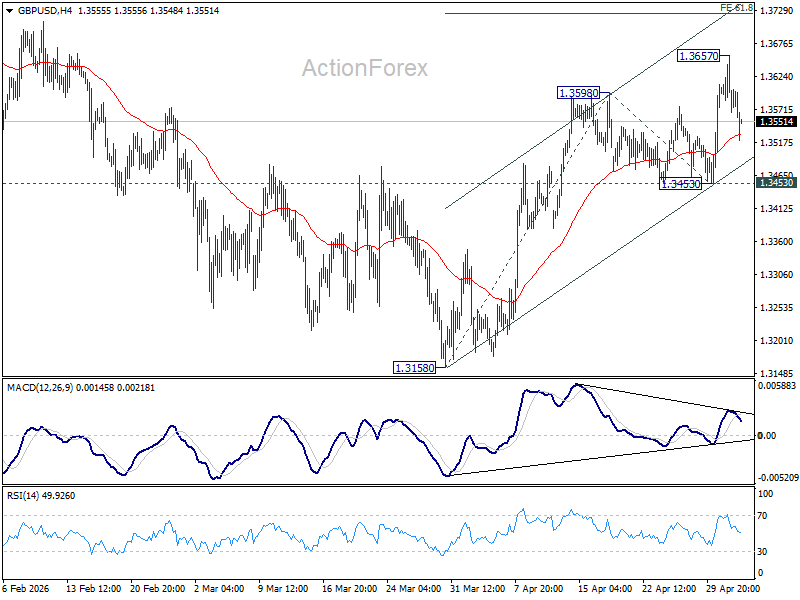

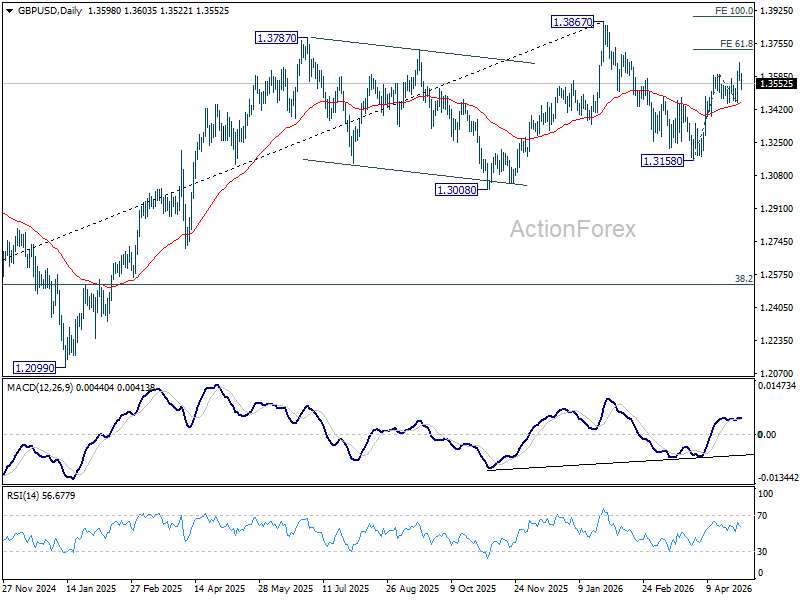

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3542; (P) 1.3601; (R1) 1.3634; More...

GBP/USD is staying in consolidations below 1.3657 temporary top and intraday bias remains neutral. Further rally is expected as long as 1.3453 holds. Above 1.3657 will target 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).

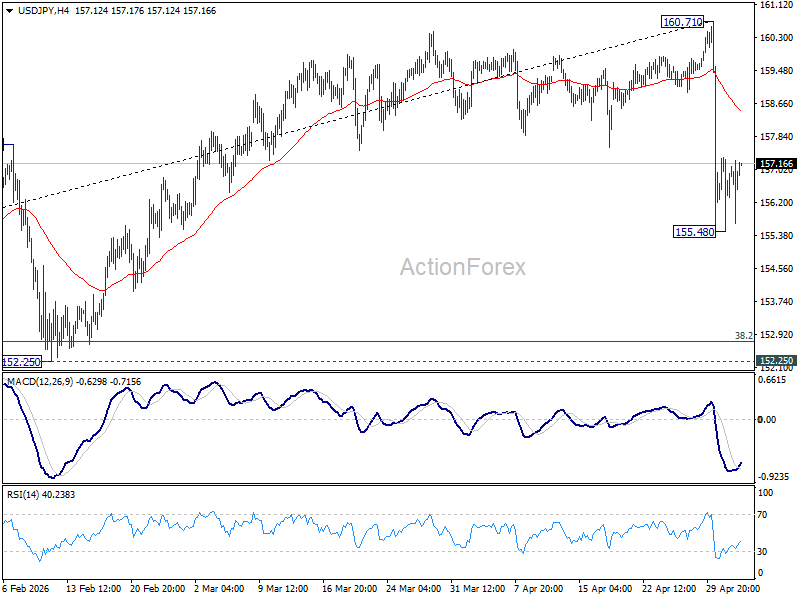

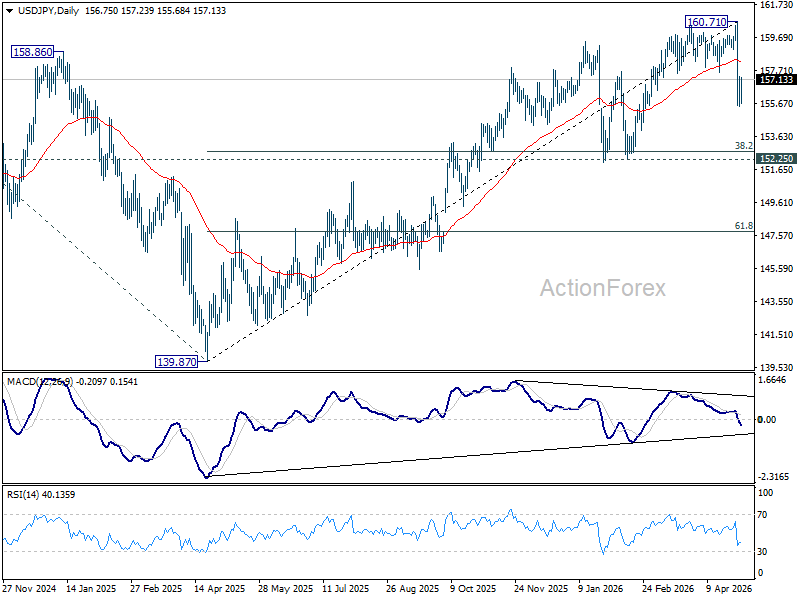

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.94; (P) 156.64; (R1) 157.75; More...

Intraday bias in USD/JPY remains neutral and more consolidations could be seen above 155.48 temporary low. Risk will stay on the downside as long as 55 4H EMA (now at 158.45) holds. Below 155.48 will extend the fall from 160.71 and target 152.25 cluster support (38.2% retracement of 139.87 to 160.71 at 152.74).

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.03) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

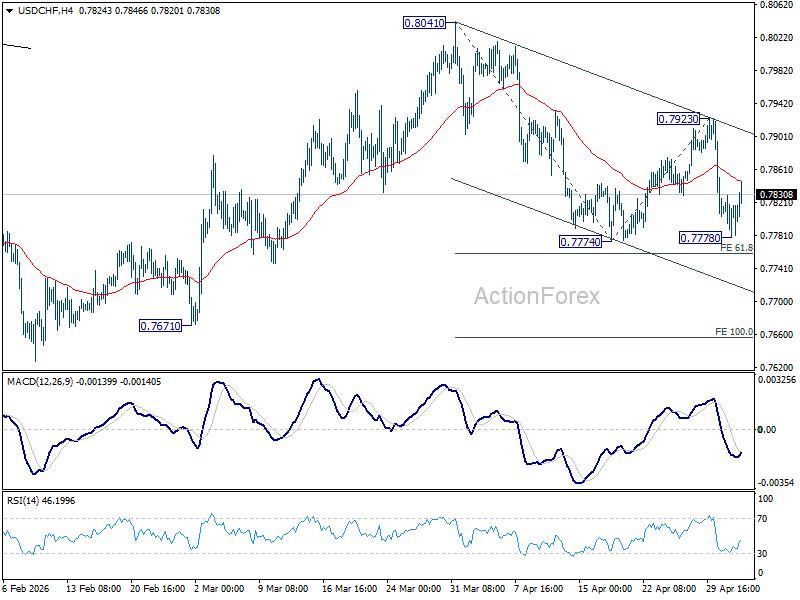

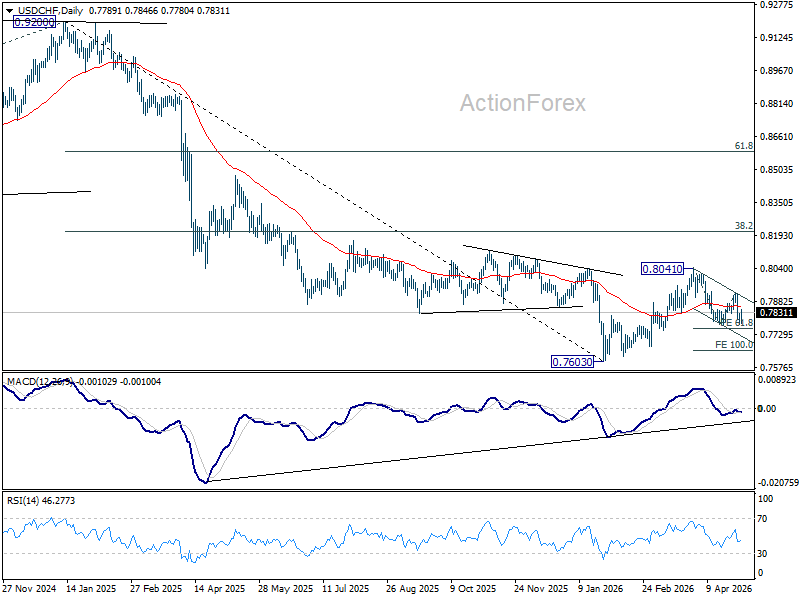

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7787; (P) 0.7810; (R1) 0.7841; More….

USD/CHF recovered ahead of 0.7774 support and intraday bias is turned neutral first. Risk will remain on the downside as long as 0.7923 resistance holds. Firm break of 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758 will extend the fall from 0.8041 to 100% projection at 0.7656.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8042) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

Debunked Strike, Real War Risk: Dollar Rallies on Panic Hedge as Hormuz Tensions Rise

Markets were whipsawed today by a dramatic but ultimately false headline—and the reaction says everything about current risk conditions. Reports that Iranian missiles had struck a US Navy vessel near the Strait of Hormuz sent oil surging and triggered an immediate rush into the Dollar as a panic hedge.

The logic was straightforward. A confirmed hit on a US warship would almost certainly have sparked a powerful military response and raised the risk of a full closure of the Strait. That scenario would have sent oil sharply higher and shaken global markets. Within minutes, traders moved to price that risk.

But the story unraveled just as quickly. US Central Command flatly denied the reports, stating that no ships had been hit and that any missiles launched “didn’t even come close” to US assets. As reality replaced speculation, Brent crude pulled back to around $110, unwinding much of the spike.

Yet the bigger picture has not changed. The United States has launched “Project Freedom,” actively escorting merchant ships and oil tankers out of the Persian Gulf. This is not a de-escalation—it is a sign that risks to shipping routes are rising.

Iran’s response was equally firm, warning that all vessels must coordinate with its military and pushing back against US involvement in the Strait. The standoff is becoming more structured, with both sides asserting control over one of the world’s most critical energy corridors.

And crucially, the risk is not hypothetical. The UAE confirmed that an ADNOC tanker was hit by two drones today. While the incident did not cause casualties, it confirms that the Strait remains a live conflict zone, where attacks on commercial shipping are already happening.

The market reaction, even after the denial, reinforces this reality. The Dollar continues to trade stronger as investors maintain defensive positioning. Yen is also firm, while commodity-linked currencies like the Aussie and Loonie lag. Swiss Franc is notably weaker, with Euro and Sterling largely neutral.

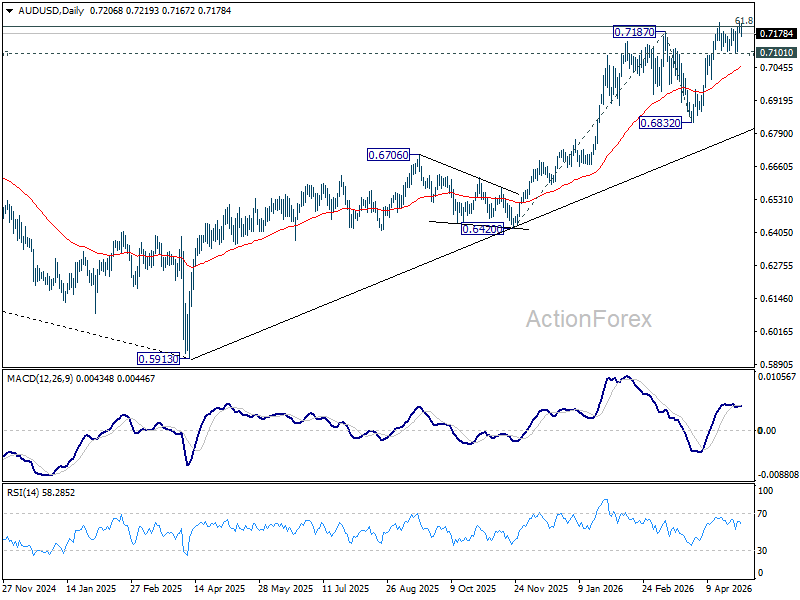

AUD/USD Awaits Hawkish RBA to Clear 0.72 Hurdle Decisively

AUD/USD is pressing a critical test at 0.72, with the RBA decision set to determine the next move. While a rate hike is largely priced in, markets are focused on whether policymakers signal more tightening ahead. A hawkish shift could drive a decisive breakout, but cautious guidance risks another rejection at key resistance. Read More.

ECB Survey Shows Higher Inflation, Weaker Growth as Energy Shock Bites

The Eurozone outlook is turning more difficult. ECB forecasters now see higher inflation and slower growth as energy prices rise, while wage pressures remain firm. With inflation staying elevated and activity weakening, policymakers face a growing stagflation dilemma. Read More.

Eurozone Sentix Improves to -16.4, But Germany Signals Deeper Trouble

Eurozone investor confidence is improving—but risks are far from over. While Sentix rebounded in May, recession concerns remain as inflation pressures persist and fiscal risks build. Germany’s continued decline adds another layer of concern, highlighting a fragile and uneven recovery across the bloc. Read More.

Eurozone PMI Manufacturing at Multi-Year High as War Triggers Record Cost Pressures

A strong Eurozone PMI reading is masking deeper risks. Manufacturing growth is being driven by stockpiling amid supply fears, while cost pressures are surging to record levels. With business optimism falling, the data point to a fragile outlook and rising challenges for policymakers. Read More.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7787; (P) 0.7810; (R1) 0.7841; More….

USD/CHF recovered ahead of 0.7774 support and intraday bias is turned neutral first. Risk will remain on the downside as long as 0.7923 resistance holds. Firm break of 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758 will extend the fall from 0.8041 to 100% projection at 0.7656.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8042) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

AUD/USD Awaits Hawkish RBA to Clear 0.72 Hurdle Decisively

The RBA is set to hike again in the upcoming Asian session—but that’s not the real story. Markets have largely priced in a 25 basis point move to 4.35%, and the focus has already shifted to what comes next. For the Australian Dollar, the outcome hinges not on the hike itself, but on whether the RBA signals that the tightening cycle is far from over.

Inflation is forcing the central bank’s hand. Headline CPI jumped from 3.6% to 4.6% in Q1. Trimmed mean measure eased slightly to 3.3% but remained elevated. Crucially, this strength is emerging even before the full impact of higher oil prices feeds through the economy, raising the risk that inflation could stay elevated for longer than previously expected, reinforcing the case for further tightening at this meeting

However, the path beyond May is unclear. According to a Reuters poll, while 18 of 31 economists expect the cash rate to remain at 4.35% through year-end, more than a third now see rates rising to at least 4.60% by the end of the third quarter, marking a notable shift in expectations compared to a month ago. This divergence underscores the importance of the RBA’s updated projections.

The Statement on Monetary Policy will be the real battleground. The key question is when inflation is expected to return to the 2–3% target. If that timeline is pushed back toward late 2026 or even 2027, it effectively signals that current policy is not restrictive enough—a clear green light for further tightening. Any hint from Governor Michelle Bullock that “more may be required” would reinforce that message.

This sets up a critical moment for AUD/USD, which is now pressing against the 0.72 resistance zone. This level, aligned with 61.8% retracement of 0.8006 to 0.5913 at 0.7206, has repeatedly capped rallies, turning it into a defining technical barrier.

Further rise is expected for now, with 0.7101 acting as near-term support. A clean break above 0.7206 would mark a decisive shift, opening the path toward the 0.80 handle in the medium term. But without a hawkish push from the RBA, the risk is that this rally stalls once again.

If the central bank leans cautious or avoids strong forward guidance, the market may interpret it as hesitation, triggering rejection at resistance. A break below 0.7101 would indicate rejection at resistance and could open the way for a deeper pullback toward 0.6832.

In this context, the RBA’s communication will be pivotal. A clearly hawkish signal, particularly via inflation projections or forward guidance, could provide the catalyst needed for AUD/USD to break through 0.72. Conversely, a more cautious or data-dependent tone may reinforce existing uncertainty and keep the pair within its current range.

XAU/USD: Gold Bears Dominate While the Price Holds Below Falling Thick Daily Cloud

Gold price fell at the start of the week, losing around 1.8% by mid-European trading on Monday, reflecting growing concerns about rising inflation that prompted major central banks to take more hawkish stance, despite that all of them kept rates unchanged in the policy meetings last week.

On the other hand, high geopolitical uncertainty surrounding the latest signals about possible escalation over the Strait of Hormuz, partially counters the action and provides headwinds for fresh bears.

Technical picture on daily chart remains bearishly aligned after recent recovery attempts were capped just under the base of thick descending daily Ichimoku cloud, with Friday’s Doji and today’s large bearish candle, about to complete reversal pattern.

Converging daily Tenkan/Kijun-sen are about to form a bear cross and along with strengthening negative momentum and DMAs in full bearish setup, contribute to negative near-term outlook.

Bears pressure pivotal $4500 support zone, consisting of last Wednesday’s one-month low and Fibo 50% retracement of $4099/$4899, violation of which to further weaken near-term structure and expose targets at $4401 (Fibo 61.8%) and $4285 (200DMA / Fibo 76.4%) in extension.

Initial resistance lays at $4587 (broken Fibo 38.2%), followed by $4631/41 (daily Kijun-sen / Tenkan-sen respectively) and key obstacle at $4665 (daily cloud base).

Res: 4587; 4641; 4700; 4740.

Sup: 4510; 4494; 4401; 4351.

ECB Survey Shows Higher Inflation, Weaker Growth as Energy Shock Bites

The ECB’s latest Survey of Professional Forecasters points to a worsening macro mix for the Eurozone, with higher inflation and weaker growth in the near term. Headline HICP inflation is now expected to rise from 1.8% to 2.7% for 2026 and from 2.0% to 2.1% for 2027, while remaining stable at 2.0% in 2028. Core inflation was also revised higher, from 2.0% to 2.2% for both 2026 and 2027.

At the same time, growth expectations have been downgraded. Real GDP is downgraded from 1.2% to 1.0% in 2026 and from 1.4% to 1.3% in 2027, reflecting the drag from higher energy prices linked to the Middle East conflict. While forecasts for 2028 and the longer term remain unchanged at 1.3%, the near-term downgrade highlights rising concerns about economic momentum.

The labor market outlook remains stable, with unemployment expectations unchanged at 6.3% for 2026, easing gradually to 6.1% by 2028. However, wage growth projections have been revised higher, from 3.0% to 3.3% for 2026 and from 2.9% to 3.1% for 2027, suggesting continued pressure on costs that could feed into broader inflation dynamics.

Overall, the survey reinforces a stagflationary tilt in the Eurozone outlook. While inflation is expected to return to target over the longer term, the near-term combination of rising prices and slowing growth presents a clear challenge for the ECB.

| Indicator | 2026 | 2027 | 2028 |

|---|---|---|---|

| HICP Inflation | 1.8% → 2.7% | 2.0% → 2.1% | 2.1% → 2.0% |

| Core HICP Inflation | 2.0% → 2.2% | 2.0% → 2.2% | 2.0% → 2.1% |

| Real GDP Growth | 1.2% → 1.0% | 1.4% → 1.3% | 1.3% → 1.3% |

| Unemployment Rate | 6.3% → 6.3% | 6.2% → 6.2% | 6.1% → 6.1% |

| Wage Growth | 3.0% → 3.3% | 2.9% → 3.1% | 2.8% → 2.9% |

The Yen is Recovering

- Japan has spent $34 billion on market interventions.

- The futures market has revised its outlook on Fed interest rates.

At the end of last week, the US dollar retreated to early March levels of 97.60, having rebounded to 98.10 at the time of writing. The catalyst for the USD index’s plunge at the end of last week was the markets’ reassessment of the Fed’s rate outlook and Donald Trump’s announcement that the US would begin withdrawing commercial vessels from the Strait of Hormuz. Nevertheless, investors’ doubts that the world’s main oil artery would be restored allowed the greenback to recover.

Before the April FOMC meeting, the futures market had priced in a low probability of a rate cut. The emergence of three dissenting voices on the committee increased the chances of monetary tightening and ruled out easing. However, the rhetoric of Fed members is once again shifting the situation.

Neel Kashkari of Minneapolis believes that the next move could be either a hike or a cut. Beth Hammack of Cleveland argues that rising uncertainty makes monetary policy itself more uncertain. Lori Logan of Dallas is concerned that it will take a long time for inflation to return to target. As a result, the futures market paints a balanced picture, with an 11.5% probability of both a cut and a hike in the federal funds rate in 2026, and a 77% chance of it remaining at the current level. This reassessment has deprived the dollar of significant support.

Investors are not yet giving much thought to the economic outlook. According to ECB Executive Board member Yannis Stournaras, concerns about a recession in the eurozone are real and justified. Conversely, the number of media mentions of a US economic downturn is declining.

The resumption of the trade war could add fuel to the fire of diverging economic growth. Donald Trump has announced a 25% tariff on European cars, citing the EU’s alleged failure to meet the terms of the agreement. A symmetrical response risks causing more harm to the eurozone than to the US.

Meanwhile, USDJPY bulls are trying to recover after Japanese authorities intervened in the forex market. Bloomberg estimated the cost of these interventions at 5.4 trillion yen ($34 billion). In 2024, Tokyo intervened in the market four times, with an average volume of around 3.8 trillion yen. On the intraday charts for Friday and Monday, resistance is clearly visible at 157.3 for USDJPY and 184.5 for EURJPY. This looks like a continuation of interventions aimed at establishing a trend of lower local highs and convincing the market of the sustainability of this reversal so that it becomes self-sustaining.