Sample Category Title

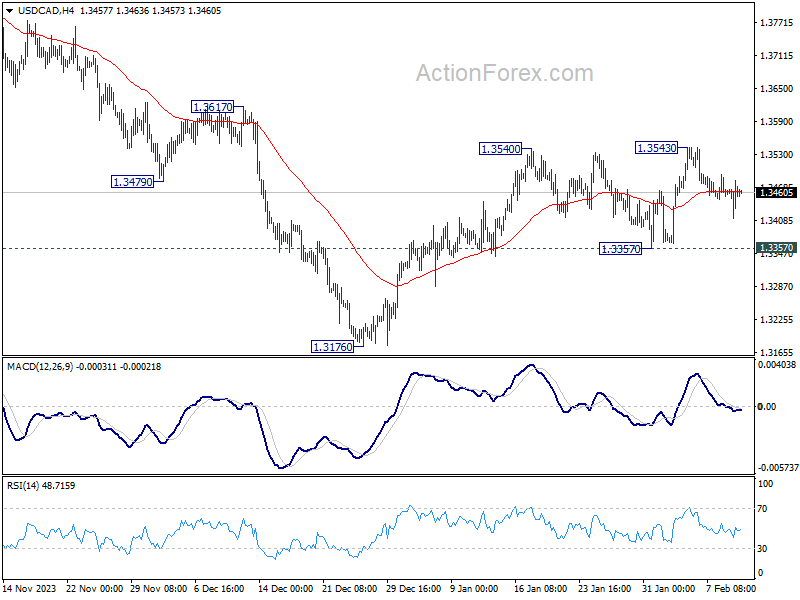

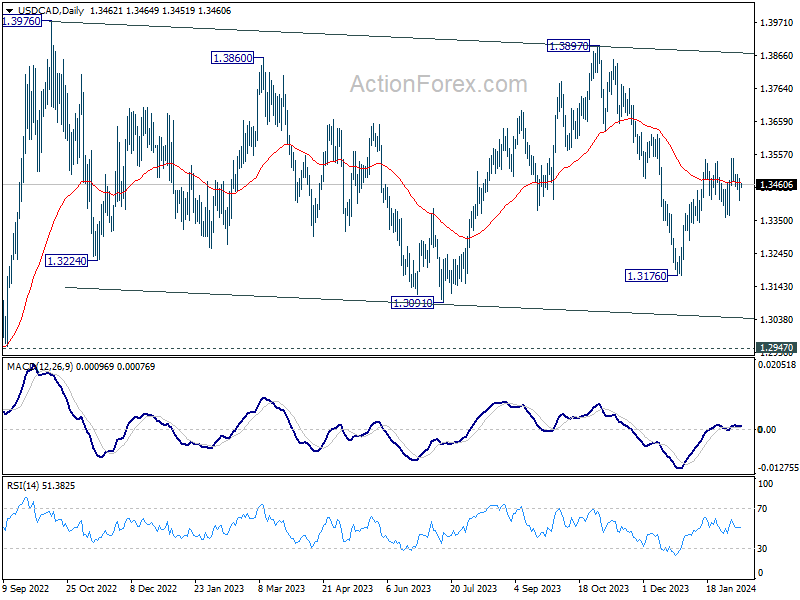

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3419; (P) 1.3451; (R1) 1.3488; More...

Intraday bias in USD/CAD remains neutral at this point and more consolidations could be seen. Further rise is mildly in favor as long as 1.3357 support holds. On the upside, decisive break of 1.3540/3 will resume the rise from 1.3176. That will also revive that case that whole fall from 1.3897 has completed, and target this resistance. Nevertheless, firm break of 1.3357 support will argue that rebound from 1.3176 has completed, and target this low for resuming the decline from 1.3897.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

Asia Calm in a Quiet Prelude, US CPI and UK Major Data to Highlight the Week

Today's Asian session sees an unusual quietness across the region, with major markets closed for holidays, leading to limited movement among major currency pairs and crosses. New Zealand Dollar is having a slight downtick following RBNZ Governor Adrian Orr's appearance before a parliamentary committee, where he left market participants parsing for clues on future rate adjustments. Despite Orr's non-committal stance, the minimal market response suggests that expectations for further rate hikes remain intact, albeit with an air of caution.

The day's economic calendar remains sparse, shifting the market's attention to forthcoming comments from notable central bank figures. Neverthless, speeches by ECB Chief Economist Philip Lane and Executive Board member Piero Cipollone, Fed Governor Michelle Bowman and Minneapolis Fed President Neel Kashkari, as well as BoE Governor Andrew Bailey could introduce some volatility into the markets.

However, the real anticipation builds towards Tuesday, setting the stage for a slew of pivotal data releases. US CPI report stands out as a particularly significant indicator, poised to shed light on the ongoing inflation narrative. Additionally, a barrage of important data from the UK, Eurozone, Japan, and Australia are keenly awaited too.

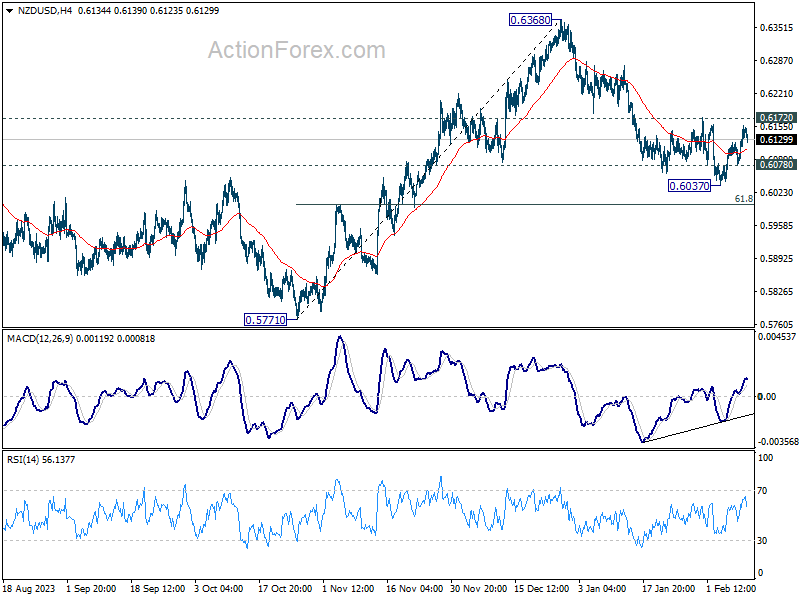

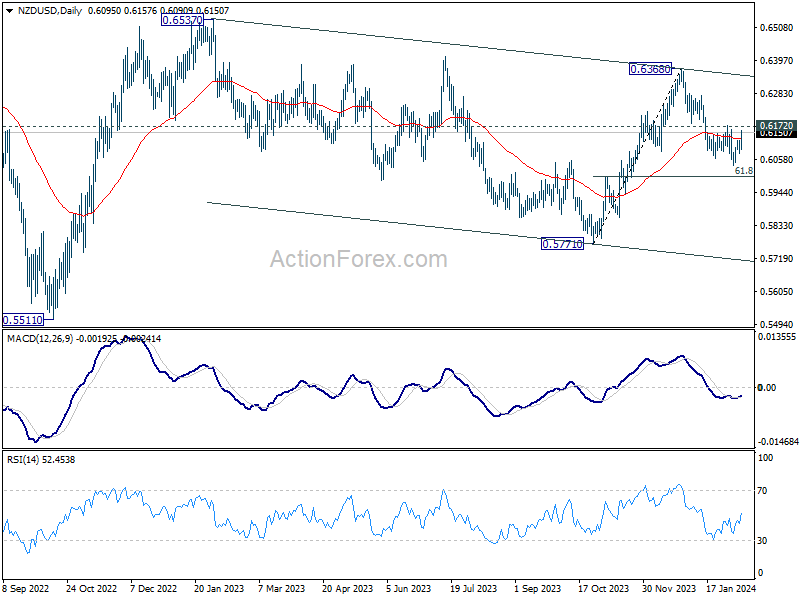

Technically, NZD/USD's recovery from 0.6037 is still seen as a correction to fall from 0.6368 only. Break of 0.6078 minor support will bring retest of 0.6037. Firm break there should resume the decline through 61.8% retracement of 0.5771 to 0.6368 at 0.5999. Nevertheless, strong break of 0.6172 will argue that the decline has completed and bring further rebound.

Happy Lunar New Year to those who're celebrating the year of Dragon!

ECB's Panetta argues for early and gradual rate cuts, dismisses core inflation fears

ECB Council member Fabio Panetta articulated a sense of urgency for ECB to loosen its approach, suggesting that "the time for a reversal of the monetary policy stance is fast approaching."

Panetta advocates for a nuanced evaluation of the timing and methodology of interest rate adjustments, contrasting the implications of initiating "quickly and gradually" against opting for "later and more aggressive" measures. He warns that the latter could "increase volatility in financial markets and economic activity".

The backdrop to Panetta's remarks is a macroeconomic conditions characterized by significant disinflationary progress at an "advanced stage", with progress toward 2% target "continues to be rapid.

He emphasizes the absence of any "upward de-anchoring of inflation expectations," pointing instead to emerging downside risks. This observation effectively counters concerns over enduring high core inflation, which Panetta now deems "groundless."

The crux of Panetta's argument lies in the potential consequences of delayed policy adaptation. "If monetary policy were to take too long to accompany the ongoing disinflation, downside risks to inflation could emerge that would conflict with the symmetrical nature of the objective set by the ECB's Governing Council," he said.

ECB's de Cos highlights March projections as key to rate cut decisions

In a newspaper interview published on Sunday, ECB Governing Council member Pablo Hernandez de Cos spotlighted the upcoming economic projections in March as a crucial factor in determining the timing for interest rate cuts.

De Cos outlined two primary considerations that the March projections will address: the confidence level in achieving ECB's 2% medium-term inflation target and the determination of an interest rate path that aligns with reaching this symmetric target.

Reflecting on past challenges, de Cos acknowledged the ECB's initial underestimation of the inflationary surge post-pandemic and following Russia's invasion of Ukraine. However, he noted a marked improvement in the accuracy of staff projections, highlighting recent instances where inflation figures came in slightly below expectations.

De Cos's remarks suggest a positive outlook on Eurozone's disinflation process, describing it as "well advanced" and likely "to continue in the coming quarters."

RBNZ's Orr stands firm on restrictive policy to combat persistent inflation

RBNZ Governor Adrian Orr, in a parliamentary committee appearance today, articulated a firm stance on maintaining restrictive monetary policy to tackle the country's higher-than-desired inflation rate.

Currently sitting at 4.7%, New Zealand's inflation remains "too high" and overshoots RBNZ's target band of 1% to 3%

"That's why we've retained a restrictive monetary policy stance with the official cash rate at 5.5%, and we'll be back at the end of this month again with our updated views on the wisdom of that stance."

Deputy Governor Christian Hawkesby provided additional insights, noting the resilience of New Zealand's financial system and the capacity of consumers to absorb higher interest rates.

"The vast majority of households have continued to manage the debt and service their mortgages, although some are struggling and falling behind," Hawkesby added.

US inflation slowdown and UK's major data release set the stage for market moves

The coming week spotlights a slew of crucial economic indicators poised to offer a clearer view of inflationary pressures, consumer health, and the broader economic trajectory across several major economies. With particular attention on US CPI and the batch of data from the UK.

In the US, forthcoming CPI data for January is the focal point, with expectations pointing towards moderation in headline inflation from 3.4% to 2.9%, and a slight dip in core CPI from 3.9% to 3.8%. Beyond inflation, retail sales, University of Michigan consumer sentiment index and inflation expectations, will be under scrutiny.

These figures come at a crucial juncture, as Fed evaluates the persistence of inflationary pressures against a backdrop of enduring consumer strength. With the fed fund futures currently indicating a 60% probability of a Fed rate cut in May, any upside surprises in inflation or consumer spending trends could prompt reassessments of the timing for policy easing, pushing expectations further into the year.

The UK also faces a week brimming with critical data, including December and Q4 GDP, complemented by January's CPI, retail sales, and employment figures. These releases arrive at a time of notable divergence within BoE's MPC. Hawks within the committee, like Catherine Mann and Jonathan Haskel, have voiced concerns over the stubbornness of inflation, suggesting that the UK's disinflationary path lags far behind its international counterparts. Conversely, dovish voices, represented by Swati Dhingra, warn of the economic fallout from overly restrictive monetary policy. This week's data will likely intensify the debate, offering ammunition to both sides of the policy divide.

The week also features pivotal releases beyond the US and UK, including Swiss CPI, German ZEW economic sentiment, Japan's GDP, and Australian employment figures. These indicators will shed light on the inflation scenario in Switzerland, economic sentiment in Germany, growth momentum in Japan, and the labor market situation in Australia.

Here are some highlights for the week:

- Tuesday: Australia Westpac consumer sentiment, NAB business confidence; Japan PPI, machine tool orders; UK employment; Swiss CPI; Germany ZEW economic sentiment; US CPI.

- Wednesday: UK CPI, PPI; Eurozone GDP revision, industrial production.

- Thursday: Japan GDP; Australia employment, UK GDP, industrial and manufacturing production, goods trade balance; Swiss PPI, SECO consumer climate; Eurozone trade balance; Canada housing starts, manufacturing sales; US retail slaes, Empire State manufacturing index, Philly Fed manufacturing index, jobless claims, import prices, industrial production, NABH housing index.

- Friday: New Zealand BusinessNZ manufacturing; Japan tertiary industry index; UK retail sales; Canada wholesale sales; US PPI, building permits and housing starts, U of Michigan consumer sentiment.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3419; (P) 1.3451; (R1) 1.3488; More...

Intraday bias in USD/CAD remains neutral at this point and more consolidations could be seen. Further rise is mildly in favor as long as 1.3357 support holds. On the upside, decisive break of 1.3540/3 will resume the rise from 1.3176. That will also revive that case that whole fall from 1.3897 has completed, and target this resistance. Nevertheless, firm break of 1.3357 support will argue that rebound from 1.3176 has completed, and target this low for resuming the decline from 1.3897.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 10:00 | EUR | EU Economic Forecasts |

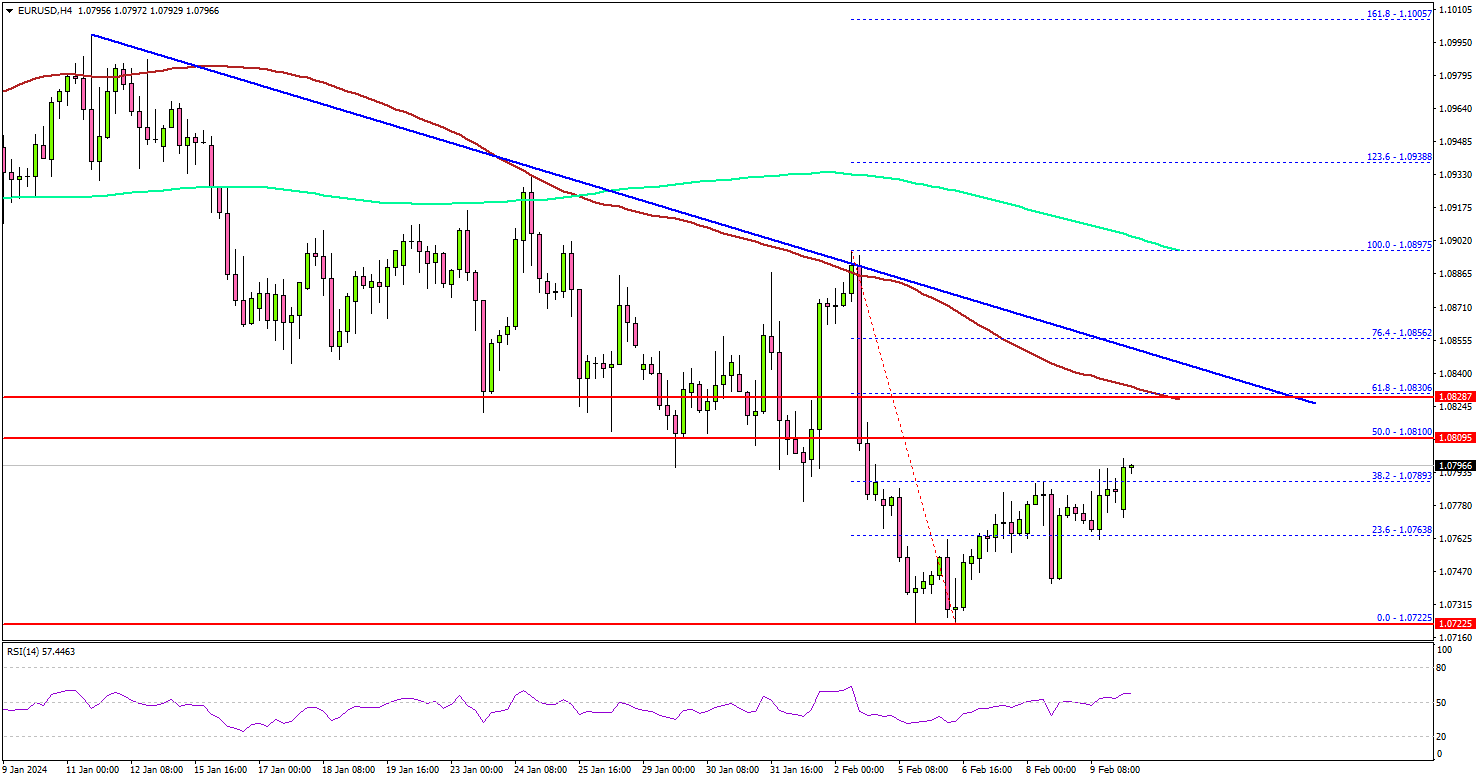

EUR/USD Attempts Recovery But Faces Key Hurdles

Key Highlights

- EUR/USD is attempting a recovery wave from the 1.0720 zone.

- A major bearish trend line is forming with resistance at 1.0830 on the 4-hour chart.

- GBP/USD is correcting losses and approaching the 1.2650 resistance.

- Bitcoin price accelerated higher above the $46,500 and $47,500 resistance levels.

EUR/USD Technical Analysis

The Euro extended its decline below the 1.0800 level against the US Dollar. EUR/USD tested the 1.0720 zone and is currently attempting a recovery wave.

Looking at the 4-hour chart, the pair climbed above the 1.0750 resistance zone. There was a move above the 23.6% Fib retracement level of the downward move from the 1.0897 swing high to the 1.0722 low.

On the upside, the bulls are facing hurdles near the 1.0810 level. It is close to the 50% Fib retracement level of the downward move from the 1.0897 swing high to the 1.0722 low.

The next key resistance is near the 1.0830 level or the 100 simple moving average (red, 4 hours). There is also a major bearish trend line forming with resistance at 1.0830 on the same chart. A close above the 1.0830 zone could open the doors for more upsides.

The next stop for the bulls might be 1.0880 or the 200 simple moving average (green, 4 hours). Any more gains might send EUR/USD toward the 1.0920 level.

Immediate support is near the 1.0765 level. The first major support sits near the 1.0720 level. The next major support sits at 1.0685, below which the pair might gain bearish momentum. In the stated case, the pair could even revisit the 1.0620 support level.

Looking at Bitcoin, there was a strong increase above the $46,500 resistance zone and the bulls even pumped the price above $48,000.

Economic Releases

- Fed's Kashkari speech.

RBNZ’s Orr stands firm on restrictive policy to combat persistent inflation

RBNZ Governor Adrian Orr, in a parliamentary committee appearance today, articulated a firm stance on maintaining restrictive monetary policy to tackle the country's higher-than-desired inflation rate.

Currently sitting at 4.7%, New Zealand's inflation remains "too high" and overshoots RBNZ's target band of 1% to 3%

"That's why we've retained a restrictive monetary policy stance with the official cash rate at 5.5%, and we'll be back at the end of this month again with our updated views on the wisdom of that stance."

Deputy Governor Christian Hawkesby provided additional insights, noting the resilience of New Zealand's financial system and the capacity of consumers to absorb higher interest rates.

"The vast majority of households have continued to manage the debt and service their mortgages, although some are struggling and falling behind," Hawkesby added.

ECB’s de Cos highlights March projections as key to rate cut decisions

In a newspaper interview published on Sunday, ECB Governing Council member Pablo Hernandez de Cos spotlighted the upcoming economic projections in March as a crucial factor in determining the timing for interest rate cuts.

De Cos outlined two primary considerations that the March projections will address: the confidence level in achieving ECB's 2% medium-term inflation target and the determination of an interest rate path that aligns with reaching this symmetric target.

Reflecting on past challenges, de Cos acknowledged the ECB's initial underestimation of the inflationary surge post-pandemic and following Russia's invasion of Ukraine.

However, he noted a marked improvement in the accuracy of staff projections, highlighting recent instances where inflation figures came in slightly below expectations.

De Cos's remarks suggest a positive outlook on Eurozone's disinflation process, describing it as "well advanced" and likely "to continue in the coming quarters."

ECB’s Panetta argues for early and gradual rate cuts, dismisses core inflation fears

ECB Council member Fabio Panetta articulated a sense of urgency for ECB to loosen its approach, suggesting that "the time for a reversal of the monetary policy stance is fast approaching."

Panetta advocates for a nuanced evaluation of the timing and methodology of interest rate adjustments, contrasting the implications of initiating "quickly and gradually" against opting for "later and more aggressive" measures. He warns that the latter could "increase volatility in financial markets and economic activity".

The backdrop to Panetta's remarks is a macroeconomic conditions characterized by significant disinflationary progress at an "advanced stage", with progress toward 2% target "continues to be rapid.

He emphasizes the absence of any "upward de-anchoring of inflation expectations," pointing instead to emerging downside risks. This observation effectively counters concerns over enduring high core inflation, which Panetta now deems "groundless."

The crux of Panetta's argument lies in the potential consequences of delayed policy adaptation. "If monetary policy were to take too long to accompany the ongoing disinflation, downside risks to inflation could emerge that would conflict with the symmetrical nature of the objective set by the ECB's Governing Council," he said.

Buckle Up for EU-China Trade Tensions

In this piece, we argue that there is a high probability that the EU will increase the tariff on Chinese electric cars, but there are also good arguments why that might not lead to a large-scale trade war.

The EU Commission has rung alarm bells over a doubling of the EU-China trade deficit over the past three years and in October 2023 launched an anti-subsidy probe into Chinese battery energy vehicles (BEVs).

We find it likely that EU will raise the tariff on imports of Chinese BEVs from 10% to around 20-25% when the investigation is concluded (by November this year). China will likely retaliate and potentially hurt specific smaller European sectors a lot. However, we think they will be careful not to scare of foreign companies more broadly and thus will choose a moderate overall response.

Trade tensions are likely to be a rising topic since China has become a leader in a long list of green products such as BEVs, batteries and solar panels - products that will see high European demand in coming years and where EU aims to de-risk from China.

Central Bankers Work to Recast Rate Expectations, Yet Market Optimism Remains Unwavering

Last week's financial markets were characterized by a mix of resilience, speculation, and divergent central bank signals.

In the US, the narrative remained steadfast with Fed officials emphasizing a patient approach towards monetary policy, firmly pushing back against the market's eager anticipations for imminent rate cuts. This cautious did little to dampen the spirits of investors, who propelled S&P 500 past the landmark 5000 level for the first time, a testament to the enduring optimism surrounding US economy's resilience.

The ascent of S&P 500 was coupled with slight uptick in 10-year yield. While Dollar Index made strides, reflecting some progress, the greenback's performance was notably middling when juxtaposed with its global counterparts.

In Europe, Swiss Franc bore the brunt of the market's recalibrations, finding itself at the bottom of the performance ladder. This position was influenced by similar cautionary messages from ECB and BoE regarding premature rate cut expectations. Nevertheless, Euro and Sterling ended the week on a slightly softer note against others.

Over to Asia, Japan presented a contrasting scenario, where a top BoJ official attempted to moderate expectations for aggressive policy tightening. This effort led to widespread sell-off in Yen, positioning it as the week's second weakest. But at the time same, Nikkei also soared to new 34-year highs, buoyed by anticipation of continued loose monetary policy.

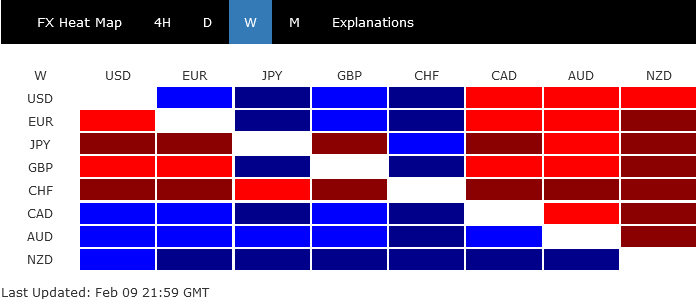

Commodity currencies emerged as the clear frontrunner amidst this global backdrop. New Zealand Dollar, in particular, stood out, riding high on the wave of speculation that RBNZ would implement further rate hikes. Australian Dollar, while also firming, trailed in the wake of RBA's noncommittal stance on future rate adjustments. Canadian Dollar, despite a fleeting post-employment data rally, settled into the third spot

Market Optimism Prevails as S&P 500 Breaks 5000 Mark

US stock market soared remarkably again last week, marking its fifth consecutive winning streak and the 14th positive week out of the last 15, reflecting investor confidence in the resilience of the US economy. Despite Federal Reserve officials tempering expectations for an early interest rate cut, indicating rates might hold steady at least until Q2, market participants remain unfazed. The question now arises: will the ongoing bullish runs in stocks trigger fear of missing out sentiment, fueling further risk-on rallies?

Minneapolis Fed President Neel Kashkari introduced an interesting perspective with his essay, arguing that current monetary policy might not be as restrictive as previously thought. He attributed the rapid decline in inflation primarily to supply-side improvements rather than deceleration in economic activity (as seen in the strong consumption and labor market data). This interpretation allows for more extended period to assess the economy's health before starting rate cut, without the risk of overly tight policy hindering growth.

Overall, Fed officials emphasized the need for further evidence of disinflation progress, particularly more broadening slowdown in price growth, before considering gradual easing of policy. At the same time, factors such as resilient consumer spending, robust job market, and global tensions present risks to inflation outlook.

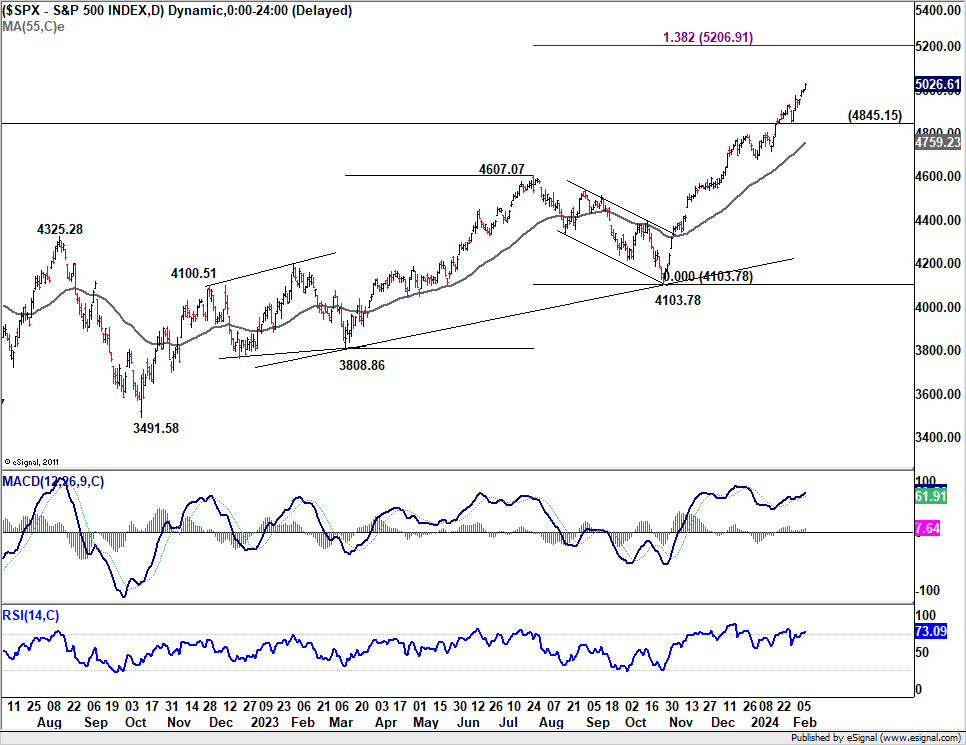

S&P 500 closed at record high at 5026.61 last week. There might be some brief struggles to sustain above 5000 psychological level initially. But near term outlook will stay bullish as long as 4845.15 support holds. Next target is 138.2% projection of 3808.86 to 4607.07 from 4103.78 at 5206.91.

10-year yield extended the near term rebound to close at 4.187 last week. At this point, strong resistance is still expected from 38.2% retracement of 4.997 to 3.785 at 4.247 to limit upside. Price actions from 3.785 are seen as a sideway consolidation pattern that would extend for a while before downside breakout happens.

However, sustained break of 4.247 would indicate some important change in the fundamental outlook, probably on expectations that Fed's interest rate would settle at a higher level during the upcoming rate cut cycle. In this case, 10-year yield could rally further to 61.8% retracement at 4.534.

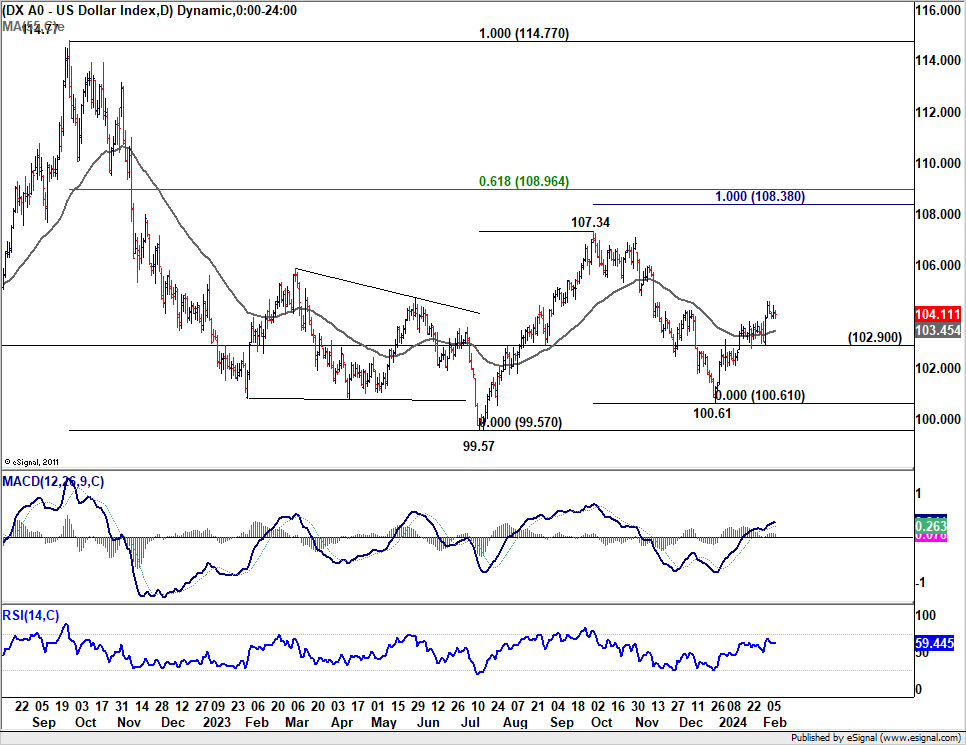

Dollar index's rally from 100.61 progressed as expected, even though just a small step. Further rise is expected as long as 102.90 support holds. Rise from 100.61 is seen as the third leg of the consolidation pattern from 99.57. Next target is 107.34 resistance.

BoJ's Dovish Stance Catapults Nikkei to New Heights, Yen Continues to Weaken

Japan's stock market also jumped last week, with Nikkei hitting a new 34-year high. The surge, fueled by strong corporate earnings and expectations of continued loose monetary The robust optimism was partly driven by impressive earnings from major companies like SoftBank, Nintendo, and Toyota. Meanwhile, anticipation of continuous loose monetary policy and the persistently weak Yen also played an import part.

A key factor contributing to Nikkei's surge was the speech by BoJ Deputy Governor Shinichi Uchida, who suggested that the central is unlikely to engage in aggressive interest rate hikes even after the cessation of its negative interest rate policy. Uchida's remarks underscore the distinct economic conditions in Japan compared to the US and Europe, arguing against drawing parallels in interest rate outlooks among these regions.

Uchida highlighted the divergence in inflation levels, noting that while Fed and ECB initiated interest rate increases in 2022 amidst inflation rates above 8%, Japan's inflation scenario is markedly different. Additionally, He emphasized the need for continued accommodative monetary policy to elevate medium- to long-term inflation expectations, which is still in the process of climbing to 2%.

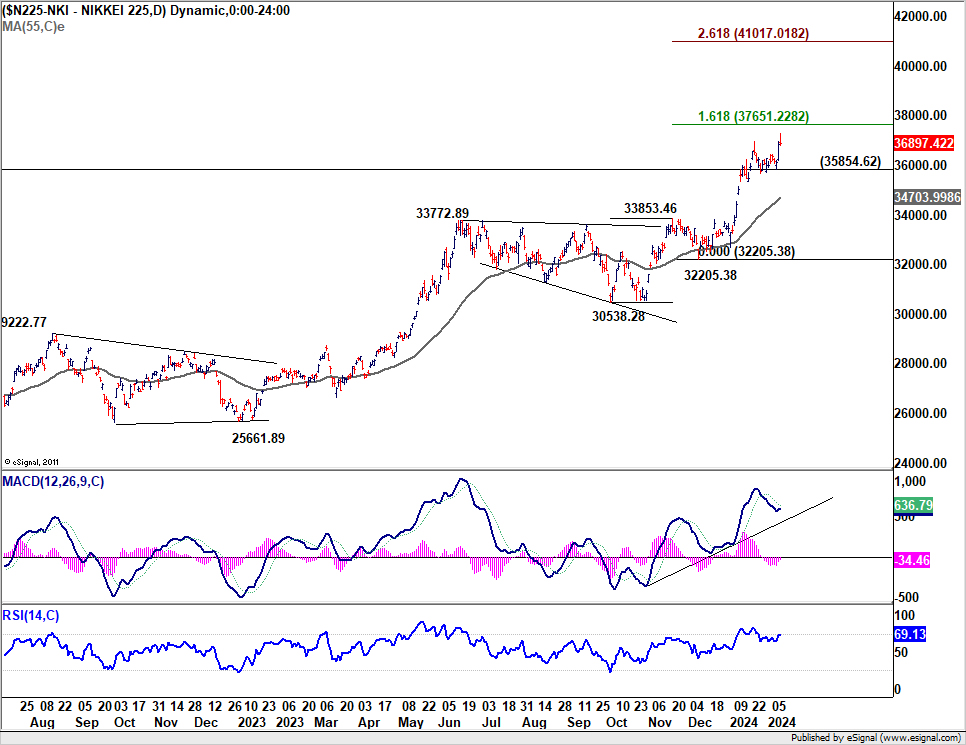

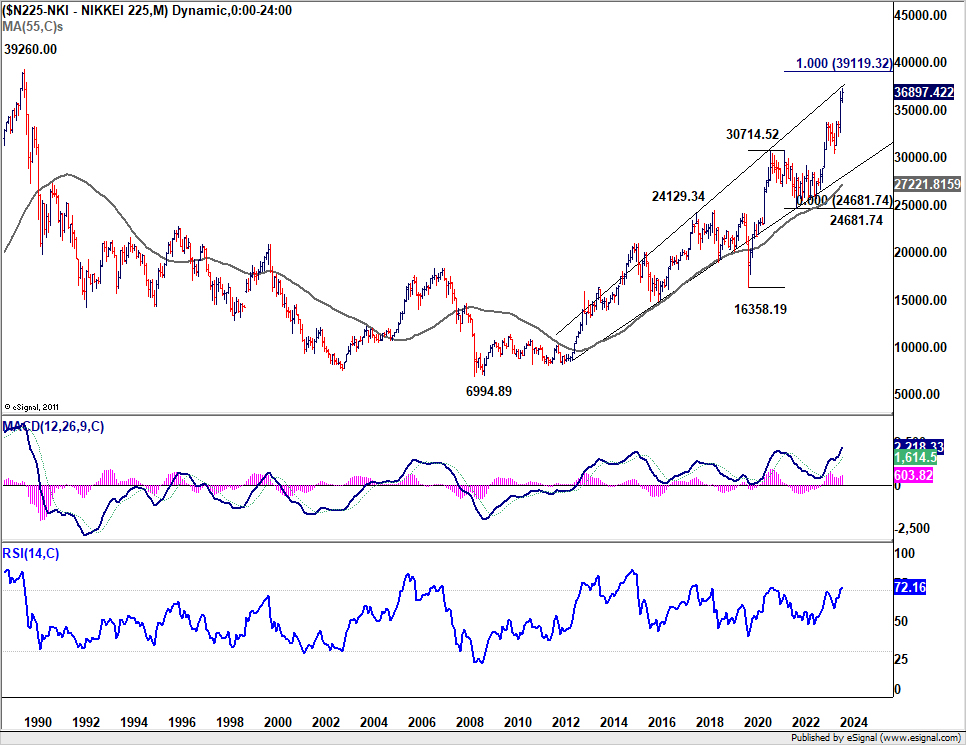

Technically, near term outlook in Nikkei will now stay bullish as long as 35854.62 support holds. Next near term target is 161.8% projection of 30538.28 to 33853.46 from 32205.38 at 37651.22. Next medium term target is 100% projection of 16358.19 to 30714.52 from 24681.74 at 39119.32, which is close to 39260 record high made in 1990.

Yen, meanwhile, emerged as the second-worst performer last week, influenced by delayed rate cut expectations among major central banks and the anticipation of gradual tightening by BoJ. Rising yields globally and the prevailing risk-on sentiment have further pressured Yen. Despite this, Japan's verbal interventions have been moderate so far. However, any intensification in the Yen's decline could prompt more assertive responses from Japanese authorities.

NZD/JPY was one of the biggest movers last week, losing -2%. The strong break of 91.50 resistance confirmed long term up trend resumption. Outlook will now stay bullish as long as 90.70 resistance turned support holds. Next target is 61.8% projection of 80.42 to 89.67 from 86.75 at 92.46.

Considering bearish divergence condition in D MACD. Strong resistance could be seen from 92.46 projection level to limit upside, at least on first attempt. However, decisive break through could prompt upside acceleration to 100% projection at 96.00.

NZD Rallies Amid Rate Hike Buzz, Orr's Upcoming Remarks to Set the Tone

Talking about New Zealand Dollar, it was surprisingly the standout currency last week, buoyed by anticipations of two more rate hikes by RBNZ in February and April, as suggested by ANZ's forecasts. Chief Economist Sharon Zollner highlighted a series of "small but pretty consistent" economic data surprises that, in her view, bolster the case for further monetary tightening.

Contrastingly, Westpac presented a more cautious perspective, pointing to softer-than-anticipated GDP and inflation figures since RBNZ's November Monetary Policy Statement. They argue for a pause by RBNZ throughout 2024, positing that the upcoming statement could set the stage for a possible rate increase within the next six months, contingent upon core inflation pressures subsiding sufficiently.

The stage is set for an intriguing development on Monday when RBNZ Governor Adrian Orr and Deputy Governor Christian Hawkesby are scheduled to speak before the parliament's Finance and Expenditure Committee. Though the session's official agenda focuses on the Financial Stability Report, it inadvertently provides a platform for Orr to directly address the evolving market expectations regarding monetary policy. The remarks made during this session have the potential to significantly sway market sentiment, either reinforcing the bullish momentum behind New Zealand Dollar or introducing a note of caution that tempers market enthusiasm.

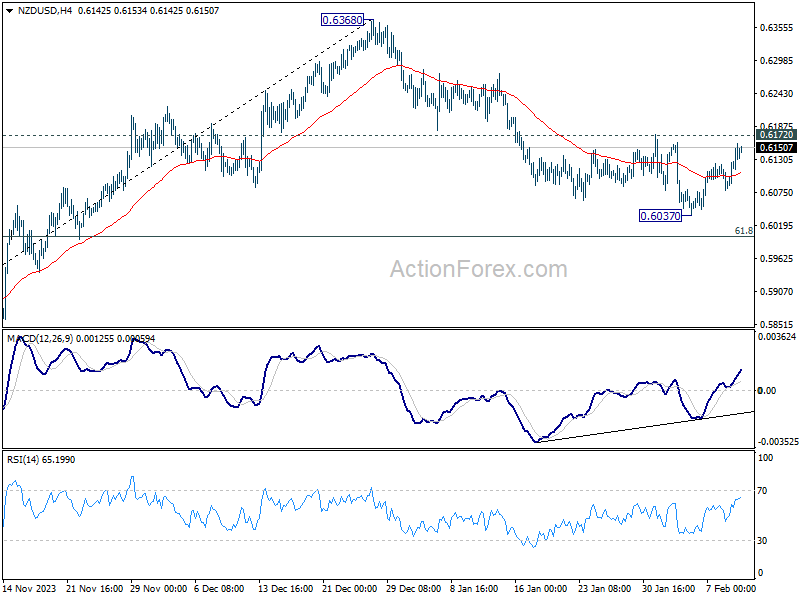

NZD/USD's decline from 0.6368 halted after hitting 0.6037, but recovery is capped below 0.6172 resistance so far. Another decline remains in favor, and break of 0.6037 would resume the fall towards 0.5771 low, as part of the whole down trend from 0.6537.

However, considering bullish convergence condition in 4H MACD, strong break of 0.6172 will dampen the above bearish view, and argue that the decline from 0.6368 has completed. Stronger rebound would then be seen back towards this resistance. We'd probably know which way it goes on Monday.

EUR/CHF Weekly Outlook

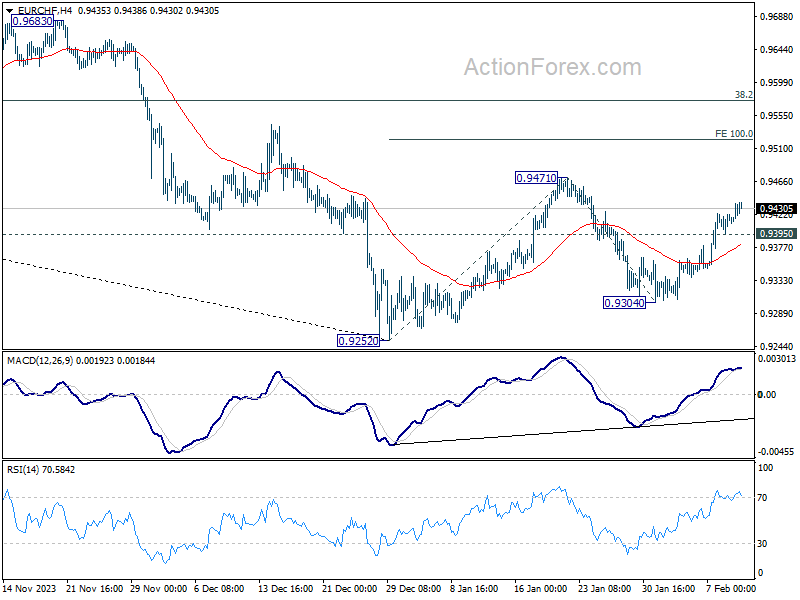

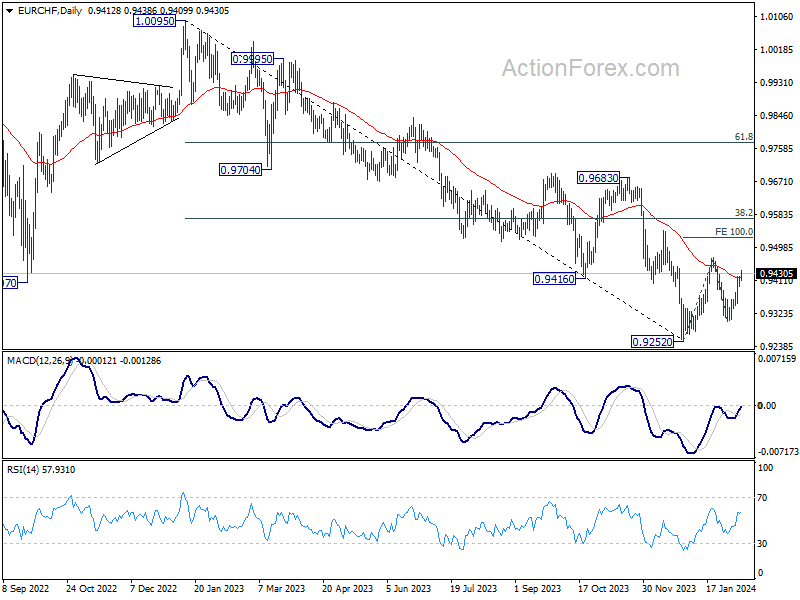

EUR/CHF's rebound last week suggests that pull back from 0.9471 has completed at 0.9304 already. Initial bias remains on the upside this week for 0.9471. Firm break there will resume whole rebound from 0.9252 to 100% projection of 0.9252 to 0.9471 from 0.9304 at 0.9523. On the downside, below 0.9395 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). Further rise would be seen to 38.2% retracement of 1.0095 to 0.9252 at 0.9574. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.

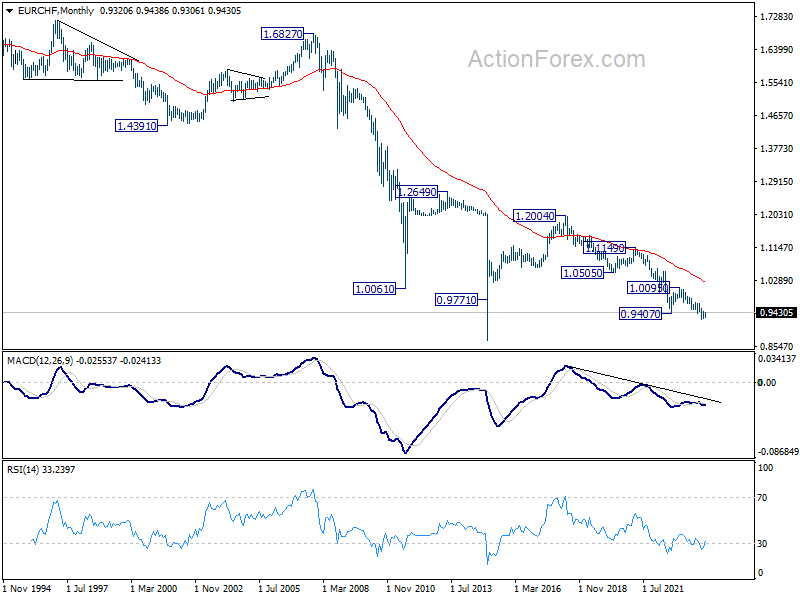

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 1.0095 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

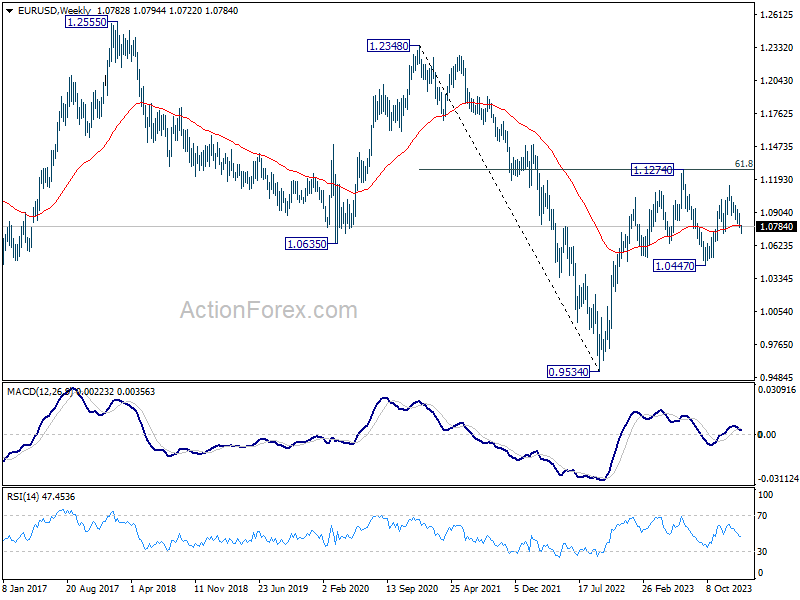

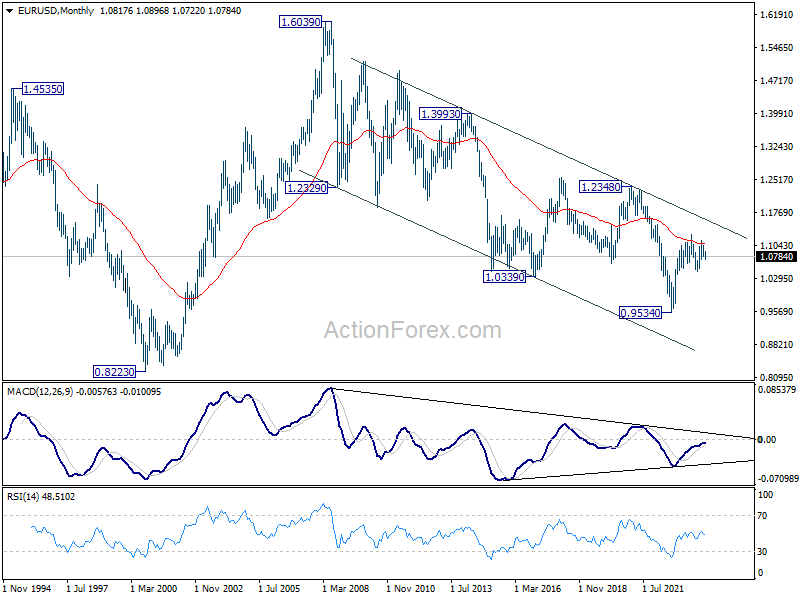

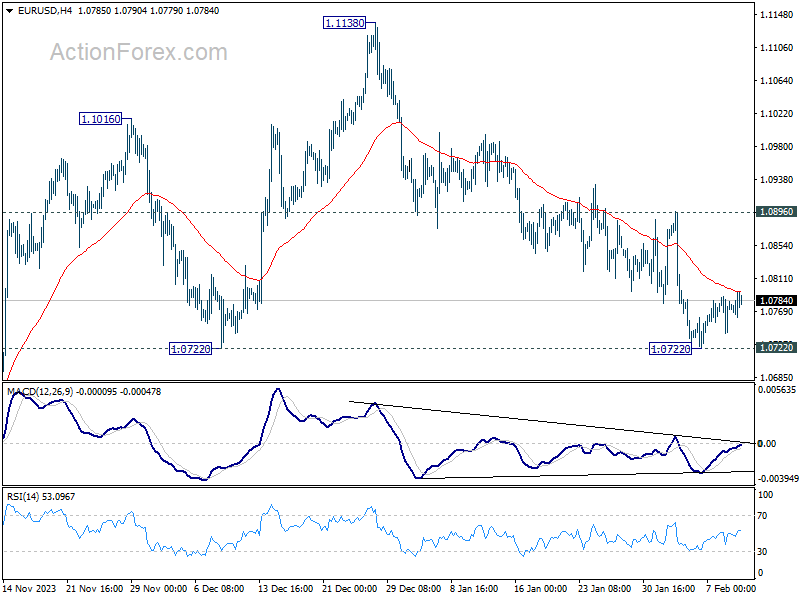

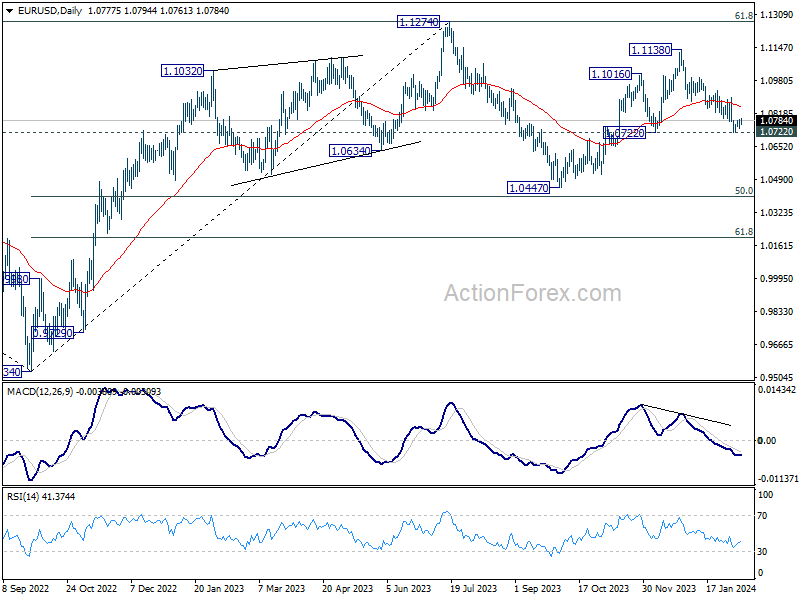

EUR/USD Weekly Outlook

EUR/USD fell further to 1.0722 last week but recovered since then. Initial bias remains neutral this week for more consolidations. While stronger recovery cannot be ruled out, outlook will stay bearish as long as 1.0896 resistance holds. On the downside, sustained break of 1.0722 will argue that whole rise from 1.0447 has completed. Deeper fall would then be seen to target this low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

In the long term picture, a long term bottom is in place at 0.9534 on bullish convergence condition in M MACD. It's still early to call for bullish trend reversal with the pair staying inside falling channel in the monthly chart. Nevertheless, sustained trading above 55 M EMA (now at 1.1059) and break of 1.1274 resistance will raise the chance of reversal and target 1.2348 resistance for confirmation.