Sample Category Title

Summary 2/12 – 2/16

Monday, Feb 12, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 10:00 | EUR | EU Economic Forecasts | ||

| 23:30 | AUD | Westpac Consumer Confidence Feb | -1.30% | |

| 23:50 | JPY | PPI Y/Y Jan | 0.10% | 0.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 10:00 | EUR | EU Economic Forecasts | |

| Forecast: | Previous: | ||

| 23:30 | AUD | Westpac Consumer Confidence Feb | |

| Forecast: | Previous: -1.30% | ||

| 23:50 | JPY | PPI Y/Y Jan | |

| Forecast: 0.10% | Previous: 0.00% | ||

Tuesday, Feb 13, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Jan | -1 | |

| 00:30 | AUD | NAB Business Conditions Jan | 7 | |

| 02:00 | NZD | RBNZ Inflation Expectations Q1 | 2.76% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Jan | -9.90% | |

| 07:00 | GBP | Claimant Count Change Jan | 15.2K | 11.7K |

| 07:00 | GBP | Unemployment rate Dec | 4.00% | 4.20% |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Dec | 5.70% | 6.50% |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Dec | 6.00% | 6.60% |

| 07:30 | CHF | CPI M/M Jan | 0.60% | 0% |

| 07:30 | CHF | CPI Y/Y Jan | 1.60% | 1.70% |

| 10:00 | EUR | Germany ZEW Economic Sentiment Feb | 17.5 | 15.2 |

| 10:00 | EUR | Germany ZEW Current Situation Feb | -79 | -77.3 |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Feb | 20.1 | 22.7 |

| 11:00 | USD | NFIB Business Optimism Index Jan | 91.1 | 91.9 |

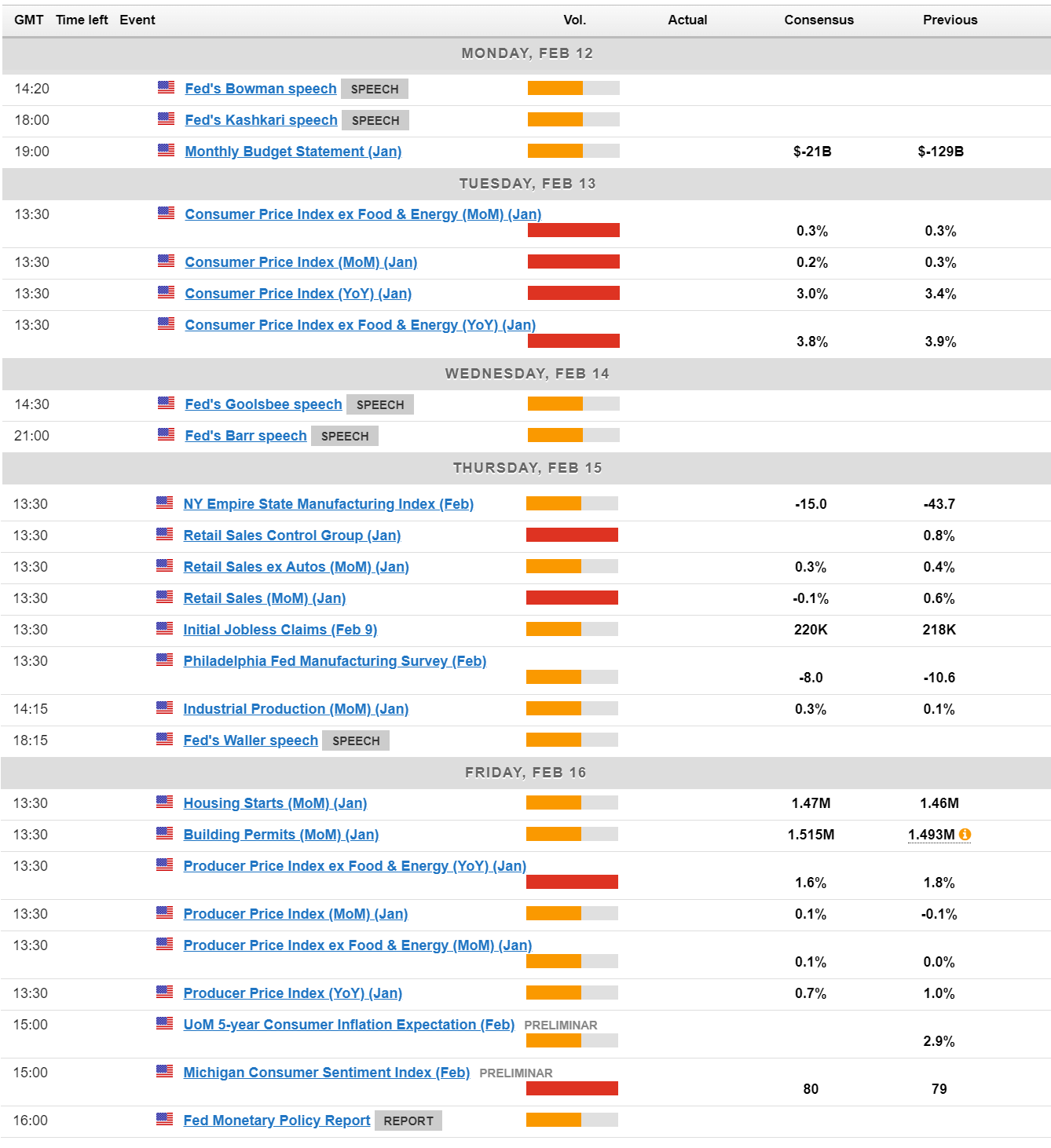

| 13:30 | USD | CPI M/M Jan | 0.20% | 0.30% |

| 13:30 | USD | CPI Y/Y Jan | 2.90% | 3.40% |

| 13:30 | USD | CPI Core M/M Jan | 0.30% | 0.30% |

| 13:30 | USD | CPI Core Y/Y Jan | 3.80% | 3.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Jan | |

| Forecast: | Previous: -1 | ||

| 00:30 | AUD | NAB Business Conditions Jan | |

| Forecast: | Previous: 7 | ||

| 02:00 | NZD | RBNZ Inflation Expectations Q1 | |

| Forecast: | Previous: 2.76% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Jan | |

| Forecast: | Previous: -9.90% | ||

| 07:00 | GBP | Claimant Count Change Jan | |

| Forecast: 15.2K | Previous: 11.7K | ||

| 07:00 | GBP | Unemployment rate Dec | |

| Forecast: 4.00% | Previous: 4.20% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Dec | |

| Forecast: 5.70% | Previous: 6.50% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Dec | |

| Forecast: 6.00% | Previous: 6.60% | ||

| 07:30 | CHF | CPI M/M Jan | |

| Forecast: 0.60% | Previous: 0% | ||

| 07:30 | CHF | CPI Y/Y Jan | |

| Forecast: 1.60% | Previous: 1.70% | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Feb | |

| Forecast: 17.5 | Previous: 15.2 | ||

| 10:00 | EUR | Germany ZEW Current Situation Feb | |

| Forecast: -79 | Previous: -77.3 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Feb | |

| Forecast: 20.1 | Previous: 22.7 | ||

| 11:00 | USD | NFIB Business Optimism Index Jan | |

| Forecast: 91.1 | Previous: 91.9 | ||

| 13:30 | USD | CPI M/M Jan | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 13:30 | USD | CPI Y/Y Jan | |

| Forecast: 2.90% | Previous: 3.40% | ||

| 13:30 | USD | CPI Core M/M Jan | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 13:30 | USD | CPI Core Y/Y Jan | |

| Forecast: 3.80% | Previous: 3.90% | ||

Wednesday, Feb 14, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | GBP | CPI M/M Jan | -0.30% | 0.40% |

| 07:00 | GBP | CPI Y/Y Jan | 4.10% | 4.00% |

| 07:00 | GBP | Core CPI Y/Y Jan | 5.20% | 5.10% |

| 07:00 | GBP | RPI M/M Jan | 0.50% | |

| 07:00 | GBP | RPI Y/Y Jan | 5.20% | 5.20% |

| 07:00 | GBP | PPI Input M/M Jan | 0.00% | -1.20% |

| 07:00 | GBP | PPI Input Y/Y Jan | -2.80% | |

| 07:00 | GBP | PPI Output M/M Jan | -0.20% | -0.60% |

| 07:00 | GBP | PPI Output Y/Y Jan | 0.10% | |

| 07:00 | GBP | PPI Core Output M/M Jan | 0.00% | |

| 07:00 | GBP | PPI Core Output Y/Y Jan | 0.10% | |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | 0.00% | 0.00% |

| 10:00 | EUR | Eurozone Employment Change Q/Q Q4 P | 0.20% | 0.20% |

| 10:00 | EUR | Eurozone Industrial Production M/M Dec | -0.30% | -0.30% |

| 15:30 | USD | Crude Oil Inventories | 5.5M | |

| 23:50 | JPY | GDP Q4 Q/Q P | 0.30% | -0.70% |

| 23:50 | JPY | GDP Deflator Y/Y Q4 P | 4.00% | 5.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | GBP | CPI M/M Jan | |

| Forecast: -0.30% | Previous: 0.40% | ||

| 07:00 | GBP | CPI Y/Y Jan | |

| Forecast: 4.10% | Previous: 4.00% | ||

| 07:00 | GBP | Core CPI Y/Y Jan | |

| Forecast: 5.20% | Previous: 5.10% | ||

| 07:00 | GBP | RPI M/M Jan | |

| Forecast: | Previous: 0.50% | ||

| 07:00 | GBP | RPI Y/Y Jan | |

| Forecast: 5.20% | Previous: 5.20% | ||

| 07:00 | GBP | PPI Input M/M Jan | |

| Forecast: 0.00% | Previous: -1.20% | ||

| 07:00 | GBP | PPI Input Y/Y Jan | |

| Forecast: | Previous: -2.80% | ||

| 07:00 | GBP | PPI Output M/M Jan | |

| Forecast: -0.20% | Previous: -0.60% | ||

| 07:00 | GBP | PPI Output Y/Y Jan | |

| Forecast: | Previous: 0.10% | ||

| 07:00 | GBP | PPI Core Output M/M Jan | |

| Forecast: | Previous: 0.00% | ||

| 07:00 | GBP | PPI Core Output Y/Y Jan | |

| Forecast: | Previous: 0.10% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | |

| Forecast: 0.00% | Previous: 0.00% | ||

| 10:00 | EUR | Eurozone Employment Change Q/Q Q4 P | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Dec | |

| Forecast: -0.30% | Previous: -0.30% | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 5.5M | ||

| 23:50 | JPY | GDP Q4 Q/Q P | |

| Forecast: 0.30% | Previous: -0.70% | ||

| 23:50 | JPY | GDP Deflator Y/Y Q4 P | |

| Forecast: 4.00% | Previous: 5.30% | ||

Thursday, Feb 15, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Feb | 4.50% | |

| 00:30 | AUD | Employment Change Jan | 20.7K | -65.1K |

| 00:30 | AUD | Unemployment Rate Jan | 4.00% | 3.90% |

| 04:30 | JPY | Industrial Production M/M Dec F | 1.80% | 1.80% |

| 07:00 | GBP | GDP M/M Dec | -0.20% | 0.30% |

| 07:00 | GBP | GDP Q/Q Q4 P | -0.10% | -0.10% |

| 07:00 | GBP | Industrial Production M/M Dec | -0.10% | 0.30% |

| 07:00 | GBP | Industrial Production Y/Y Dec | -0.10% | |

| 07:00 | GBP | Manufacturing Production M/M Dec | 0.00% | 0.40% |

| 07:00 | GBP | Manufacturing Production Y/Y Dec | 1.30% | |

| 07:00 | GBP | Goods Trade Balance (GBP) Dec | -14.1B | -14.2B |

| 07:30 | CHF | PPI M/M Jan | -0.20% | -0.60% |

| 07:30 | CHF | PPI Y/Y Jan | -1.10% | |

| 08:00 | CHF | SECO Consumer Climate Q1 | -34 | -40 |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Dec | 15.7B | 14.8B |

| 13:00 | GBP | NIESR GDP Estimate Jan | 0.00% | |

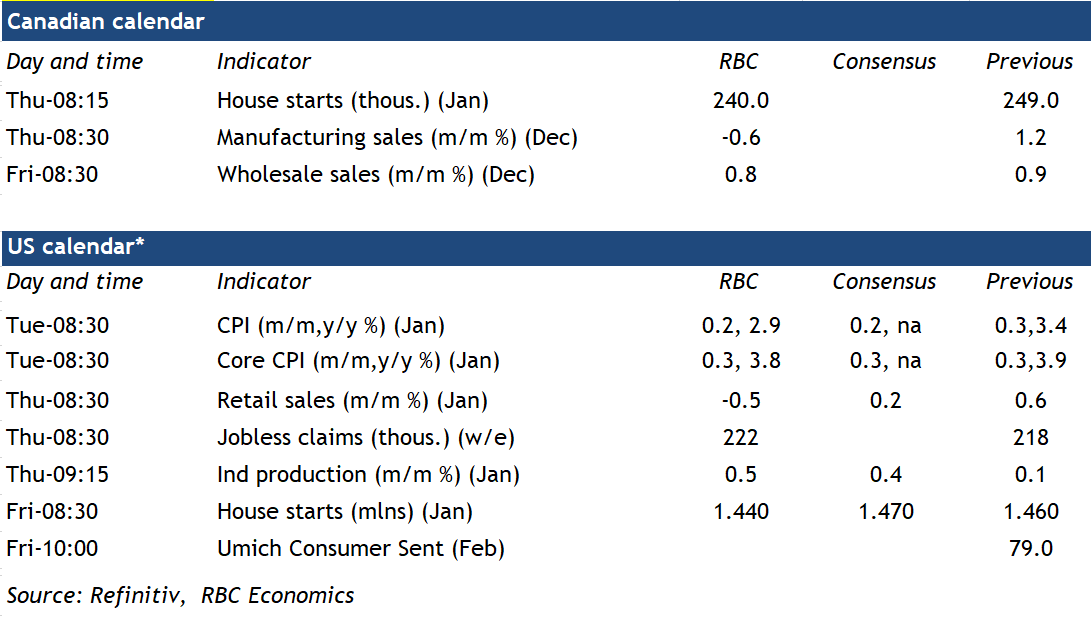

| 13:15 | CAD | Housing Starts Jan | 225K | 249K |

| 13:30 | CAD | Manufacturing Sales M/M Dec | -0.50% | 1.20% |

| 13:30 | USD | Initial Jobless Claims (Feb 9) | 217K | 218K |

| 13:30 | USD | Retail Sales M/M Jan | -0.20% | 0.60% |

| 13:30 | USD | Retail Sales ex Autos M/M Jan | 0.10% | 0.40% |

| 13:30 | USD | Import Price Index M/M Jan | -0.10% | 0.00% |

| 13:30 | USD | Empire State Manufacturing Index Feb | -12.5 | -43.7 |

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Feb | -8.9 | -10.6 |

| 14:15 | USD | Industrial Production M/M Jan | 0.30% | 0.10% |

| 14:15 | USD | Capacity Utilization Jan | 78.80% | 78.60% |

| 15:00 | USD | Business Inventories Dec | 0.30% | -0.10% |

| 15:00 | USD | NAHB Housing Market Index Feb | 46 | 44 |

| 15:30 | USD | Natural Gas Storage | -75B | |

| 21:30 | NZD | Business NZ PMI Jan | 43.1 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Feb | |

| Forecast: | Previous: 4.50% | ||

| 00:30 | AUD | Employment Change Jan | |

| Forecast: 20.7K | Previous: -65.1K | ||

| 00:30 | AUD | Unemployment Rate Jan | |

| Forecast: 4.00% | Previous: 3.90% | ||

| 04:30 | JPY | Industrial Production M/M Dec F | |

| Forecast: 1.80% | Previous: 1.80% | ||

| 07:00 | GBP | GDP M/M Dec | |

| Forecast: -0.20% | Previous: 0.30% | ||

| 07:00 | GBP | GDP Q/Q Q4 P | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 07:00 | GBP | Industrial Production M/M Dec | |

| Forecast: -0.10% | Previous: 0.30% | ||

| 07:00 | GBP | Industrial Production Y/Y Dec | |

| Forecast: | Previous: -0.10% | ||

| 07:00 | GBP | Manufacturing Production M/M Dec | |

| Forecast: 0.00% | Previous: 0.40% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Dec | |

| Forecast: | Previous: 1.30% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Dec | |

| Forecast: -14.1B | Previous: -14.2B | ||

| 07:30 | CHF | PPI M/M Jan | |

| Forecast: -0.20% | Previous: -0.60% | ||

| 07:30 | CHF | PPI Y/Y Jan | |

| Forecast: | Previous: -1.10% | ||

| 08:00 | CHF | SECO Consumer Climate Q1 | |

| Forecast: -34 | Previous: -40 | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Dec | |

| Forecast: 15.7B | Previous: 14.8B | ||

| 13:00 | GBP | NIESR GDP Estimate Jan | |

| Forecast: | Previous: 0.00% | ||

| 13:15 | CAD | Housing Starts Jan | |

| Forecast: 225K | Previous: 249K | ||

| 13:30 | CAD | Manufacturing Sales M/M Dec | |

| Forecast: -0.50% | Previous: 1.20% | ||

| 13:30 | USD | Initial Jobless Claims (Feb 9) | |

| Forecast: 217K | Previous: 218K | ||

| 13:30 | USD | Retail Sales M/M Jan | |

| Forecast: -0.20% | Previous: 0.60% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Jan | |

| Forecast: 0.10% | Previous: 0.40% | ||

| 13:30 | USD | Import Price Index M/M Jan | |

| Forecast: -0.10% | Previous: 0.00% | ||

| 13:30 | USD | Empire State Manufacturing Index Feb | |

| Forecast: -12.5 | Previous: -43.7 | ||

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Feb | |

| Forecast: -8.9 | Previous: -10.6 | ||

| 14:15 | USD | Industrial Production M/M Jan | |

| Forecast: 0.30% | Previous: 0.10% | ||

| 14:15 | USD | Capacity Utilization Jan | |

| Forecast: 78.80% | Previous: 78.60% | ||

| 15:00 | USD | Business Inventories Dec | |

| Forecast: 0.30% | Previous: -0.10% | ||

| 15:00 | USD | NAHB Housing Market Index Feb | |

| Forecast: 46 | Previous: 44 | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -75B | ||

| 21:30 | NZD | Business NZ PMI Jan | |

| Forecast: | Previous: 43.1 | ||

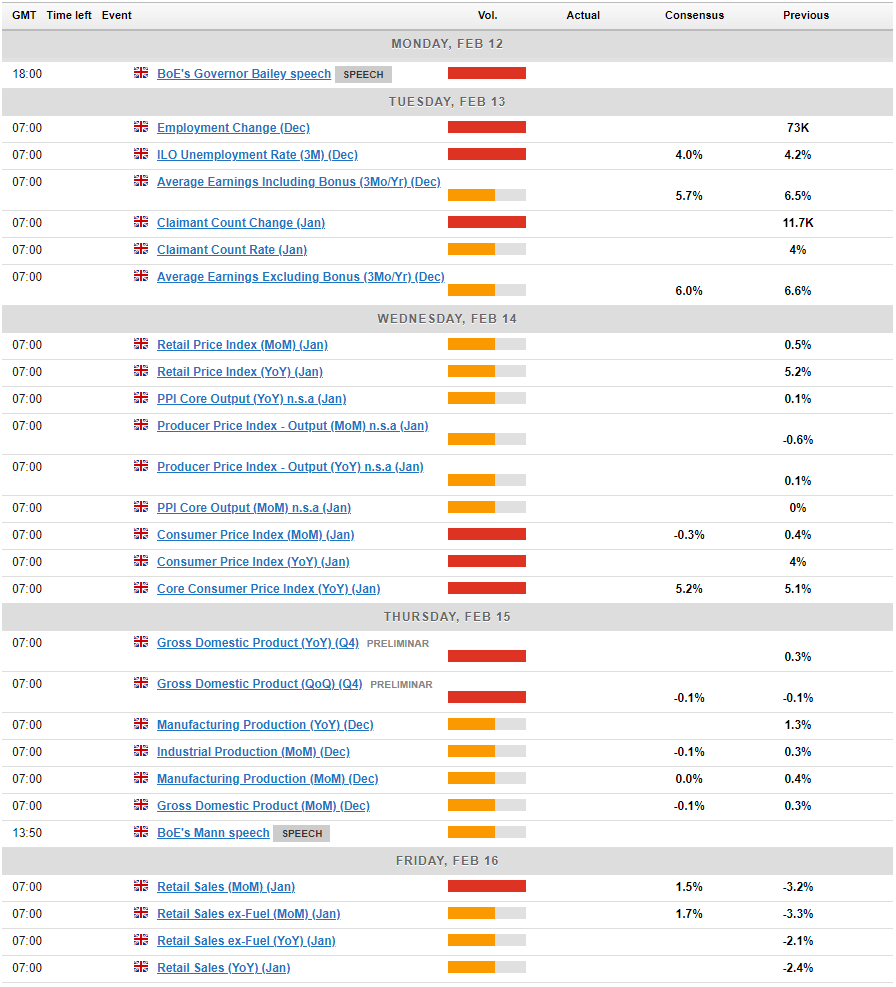

Friday, Feb 16, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Dec | 0.20% | -0.70% |

| 07:00 | GBP | Retail Sales M/M Jan | 1.50% | -3.20% |

| 13:30 | CAD | Wholesale Sales M/M Dec | 0.90% | |

| 13:30 | USD | Building Permits Jan | 1.52M | 1.49M |

| 13:30 | USD | Housing Starts Jan | 1.47M | 1.46M |

| 13:30 | USD | PPI M/M Jan | 0.10% | -0.10% |

| 13:30 | USD | PPI Y/Y Jan | 0.70% | 1.00% |

| 13:30 | USD | PPI Core Y/Y Jan | 1.70% | 1.80% |

| 13:30 | USD | PPI Core M/M Jan | 0.10% | 0.00% |

| 15:00 | USD | Michigan Consumer Sentiment Index Feb P | 80.0 | 79 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Dec | |

| Forecast: 0.20% | Previous: -0.70% | ||

| 07:00 | GBP | Retail Sales M/M Jan | |

| Forecast: 1.50% | Previous: -3.20% | ||

| 13:30 | CAD | Wholesale Sales M/M Dec | |

| Forecast: | Previous: 0.90% | ||

| 13:30 | USD | Building Permits Jan | |

| Forecast: 1.52M | Previous: 1.49M | ||

| 13:30 | USD | Housing Starts Jan | |

| Forecast: 1.47M | Previous: 1.46M | ||

| 13:30 | USD | PPI M/M Jan | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 13:30 | USD | PPI Y/Y Jan | |

| Forecast: 0.70% | Previous: 1.00% | ||

| 13:30 | USD | PPI Core Y/Y Jan | |

| Forecast: 1.70% | Previous: 1.80% | ||

| 13:30 | USD | PPI Core M/M Jan | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Feb P | |

| Forecast: 80.0 | Previous: 79 | ||

The Weekly Bottom Line: Fed Officials Continue to Signal Patience on Rate Cuts

U.S. Highlights

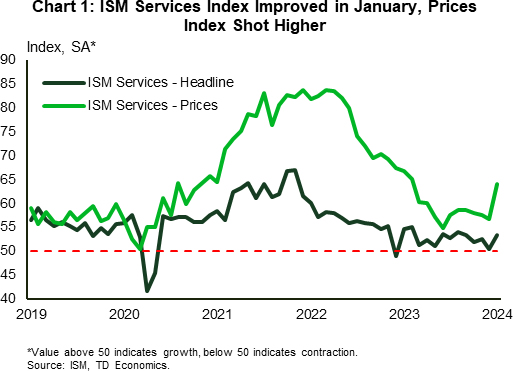

- The ISM Services index, which was on the cusp of falling into contractionary territory in December, improved notably in January, rising 2.9 points to 53.4. The one blemish to the report was a sharp move up in the prices index.

- With little on the data front, a series of Fed speeches took center stage this week. The key message was that with the economy remaining on decent footing, the Fed could afford to show patience on rate cuts. This didn’t interrupt the uptrend in equity markets, with the S&P 500 reaching a new milestone – the 500 mark.

Canadian Highlights

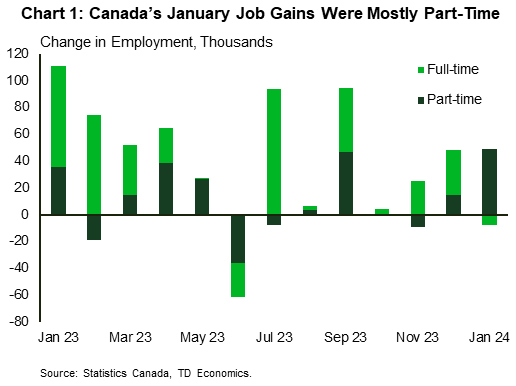

- January’s job gains came in stronger than expected, and the unemployment rate ticked down. However, the details under the hood painted a much more mixed picture of Canada’s labour market.

- December’s merchandise trade balance flipped to a modest deficit as imports rose, supported by strong domestic demand.

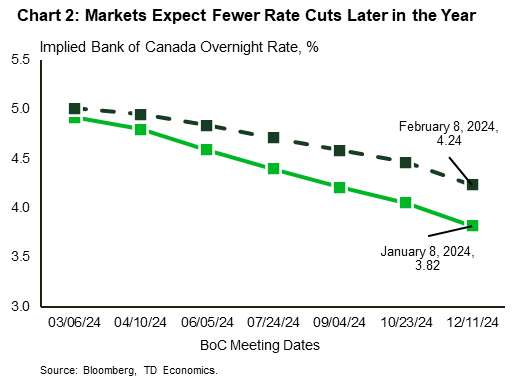

- This week’s messages from the Bank of Canada were hawkish, on balance. Without further progress in inflation, the BoC has little desire to start cutting rates. Given the current economic backdrop, markets price their expectations for the first rate cut to June or July of this year.

U.S. – Fed Officials Continue to Signal Patience on Rate Cuts

Recent economic reports focusing on GDP and employment growth have driven home the point that the U.S. economy remains on solid footing. This week’s limited data provided further support to this view. In this vein, several Fed officials this week reiterated their message that there’s no rush to cut interest rates, with bond yields trending moderately higher as a result. In what appeared to be a return of ‘good news being good news again’, stock markets shrugged off the prospect of interest rates remaining higher for longer and continued to trek higher, with the S&P 500 reaching another milestone by hitting the 5000 mark.

The ISM Services index, which was on the cusp of falling into contractionary territory in December, moved up notably in January, rising close to three points to 53.4. Looking under the hood, gains in three of the four main subcomponents helped lift the index higher. Of note, the employment sub-component flipped to signaling growth, as it jumped 6.7 points to 50.5. The one blemish to the report, was the fact that the prices index shot higher in January (Chart 1). A month of data does not make a trend, but the increase could signal additional inflationary pressure ahead.

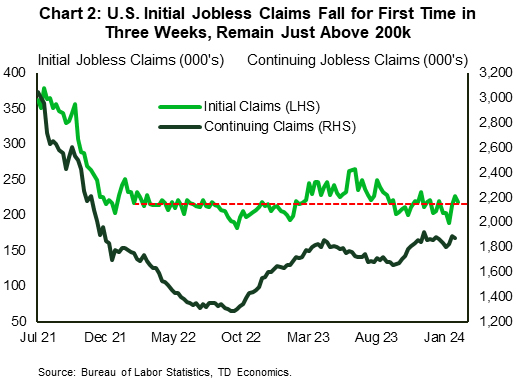

Weekly jobless claims data were consistent with a healthy labor market. Initial and continuing jobless claims continued to head lower (Chart 2). While several companies have announced plans to trim headcount this year, this is not yet being reflected in labor market data, suggesting that other businesses are growing.

With very little in the way of primary data releases, speeches from several Fed presidents and other Fed officials took center stage this week. Overall, the messaging was similar: the Fed needs to see further improvement on inflation, and with the economy on solid footing it can afford to be patient about the timing of rate cuts. Their remarks largely echoed those made by Fed Chair Powell on Sunday. Besides reiterating his message that the Fed is wary of cutting rates too soon, Powell covered a lot of ground in the ‘60 Minutes’ interview. Two comments a bit peripheral to monetary policy stood out. The first was on commercial real estate (CRE), where Powell characterized the risks as a ‘manageable’ problem for larger banks, and alluded to the low probability of a repeat of the events that unfolded during the Global Financial Crisis. However, he did note that some smaller banks that have large exposures to CRE may ‘close or be merged out’.

The other comment from Powell that stood out was his assertion that the U.S. is on an “unsustainable” fiscal path, with debt growing faster than the economy in the long run. To this end, the Congressional Budget Office (CBO) released new 10-year projections this week, which showed that the ratio of federal publicly held debt to GDP will rise from 97.3% last year to record high of 116% by 2034.

Looking ahead to next week, January’s inflation report will take center stage. The BLS released revisions to CPI data this morning, which were relatively minor and left the year-on-year path for inflation broadly unchanged. As for January, the market consensus expects a further moderation in the core measure.

Canada – The BoC to Remain Inflation-Focused

As the Lunar New Year approaches, the Canadian economy strides into the celebration with an upbeat tempo. Employment - the focal point of this week's economic calendar - came in stronger than anticipated at 37K new jobs in January, and the unemployment rate moved down a tick. This helped lift the equity market for the day, but not enough to push the benchmark index into the positive territory for the week (at least at time of writing). The Government of Canada 5-year bond yield, which got pulled up last week after strong U.S. employment report, gained another 10 basis points.

Delving into the particulars of January's labour force survey paints a far more complex picture. Signs of softening demand included job gains being largely in part-time positions, while full-time employment edged lower (Chart 1). Furthermore, private sector hiring, which is more sensitive to economic cycles, contributed only 7k positions – one fifth of today's gain. However, for now, the labour market remains fairly tight. The unemployment rate edged down, and remains low on a historic basis, and average hourly wage growth of 5.3% year-on-year is still too discomforting for the Bank of Canada.

In other economic news, December's merchandise trade balance flipped to a modest deficit after four consecutive months of surplus. The pull-back in exports was broad-based with the biggest drag coming from motor vehicles and parts exports. Total imports rose for a second month, primarily supported by the rise in consumer goods, indicative of strength in consumer spending, also evident in the latest spend data.

With economic data still showing some resilience, it's no surprise that this week's messaging from the Bank of Canada was more hawkish. Both Macklem's speech in Montreal and January's summary of deliberations emphasized a pivot in communication. The narrative has shifted from rate levels to the duration of restrictive policies required to tame inflation back to the 2% target. Central to this challenge is persistent shelter price inflation, which risks accelerating amidst relatively buoyant housing market activity. Higher home prices would result in direct implications on 'owned accommodation' inflation, but would also increase the cost of renting, amid higher borrowing cost and stretched affordability.

On this point, Macklem cautioned that the Bank has little power to influence house price dynamics, as housing remains chronically undersupplied. This underscores the complexity of addressing inflation as more than half of CPI components are growing at a rate higher than 3%, suggesting that it remains broad-based and stubbornly above the desired threshold. To get these components to decelerate faster requires a stronger pull-back in other parts of the economy. Without this progress, the Bank may be cautious about starting to cut rates. Market reactions have been telling, with the likelihood of a March-April rate cut receding below 30%, and expectations for 2024’s rate reductions adjusting downward (Chart 2).

Weekly Economic & Financial Commentary: Central Banks Still in the Spotlight

Summary

United States: Growth Still Solid, but Slowdown on the Horizon

- The ISM services index shot higher into expansion territory during January, which is the latest piece of evidence that economic growth is still firmly in positive territory. A sharp rise in the prices paid subindex, however, shows that inflation pressures have yet to be fully extinguished. Meanwhile, higher interest rates continue to weigh on consumer borrowing. Total consumer credit rose by $1.6 billion in December, a smaller-than-expected gain.

- Next week: CPI (Tuesday), Retail Sales (Thursday), Industrial Production (Thursday)

International: Central Banks Still in the Spotlight

- This week, the Reserve Bank of Australia held its policy rate steady at 4.35% and offered policy guidance that was more hawkish than expected. In Japan, the underlying details of the December wage data, as well as encouraging signs surrounding the ongoing spring wage negotiations, keep the central bank on course for an April rate hike, in our view. Mexico's central bank held rates steady, but less hawkish language in its statement suggests it could cut rates in March.

- Next week: U.K. CPI (Wednesday), Japan GDP (Thursday), Australia Employment (Thursday)

Credit Market Insights: Credit Conditions Are Coming into Balance

- The Senior Loan Officer Opinion Survey (SLOOS) for Q4-2023 saw a moderation in tight credit conditions. Most banks reported tightening lending standards for business commercial and investment (C&I), consumer and commercial real estate (CRE) loans, but the proportion tightening was significantly lower from the elevated levels seen throughout 2023.

Topic of the Week: Oh, Mexico It Sounds So Simple I Just Got to Go

- The U.S. international trade deficit has been volatile in the wake of the pandemic. After widening for three straight years, the trade deficit shrank by $178 billion last year, which more than reversed the 2022 widening. The headline that many glommed onto this week was that Mexico displaced China as the top import partner for the United States.

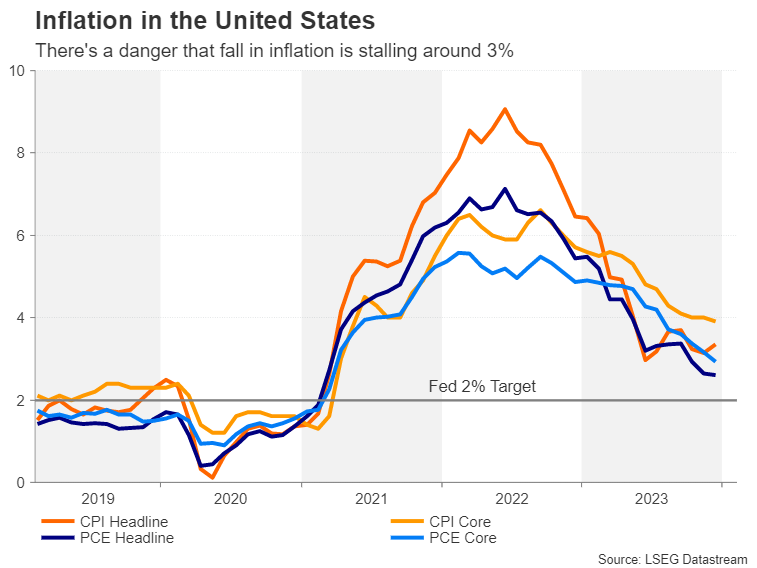

U.S. Inflation to Fall Below 3% for First Time in Nearly Three Years

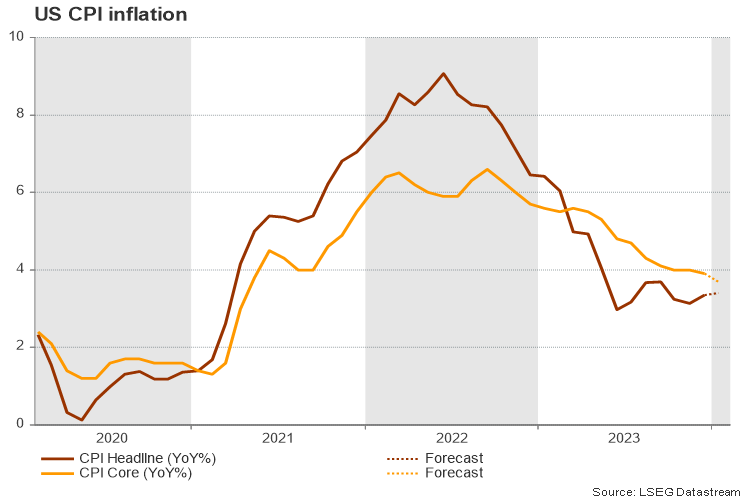

U.S. retail sales and consumer price index reports for January will be closely watched for whether strong consumer spending and slowing inflation continue to unexpectedly coexist. The U.S. Federal Reserve remains wary that strong demand could reignite price growth, but to date, inflation has continued to edge broadly lower. Strong consumer spending and resilient labour markets mean there is little pressure for the central bank to shift to interest rate cuts quickly. But, slower price growth is increasing confidence that the amount of economic pain feared when the Fed started aggressively hiking rates almost two years ago won’t necessarily materialize.

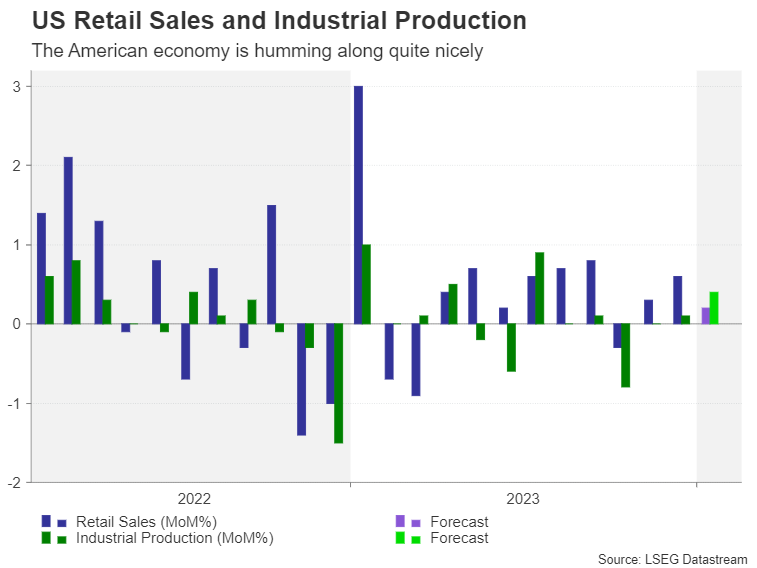

We expect January’s U.S. retail sales report to show a 0.5% decline from December led by a 7% drop in auto sales and a 2% fall in gasoline prices month-over-month. That marks the largest decline since March last year. Another surge in jobs in January (353,000) and acceleration in wage growth means household incomes are still strong but the household saving rate continues to run below pre-pandemic levels.

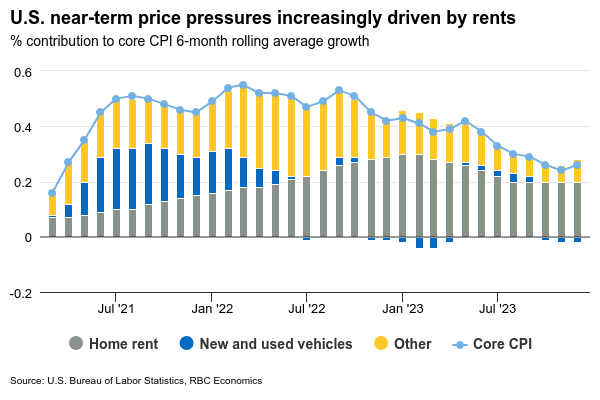

Consumer price growth is also expected to slow. We look for headline CPI growth (year-over-year) to fall below 3% for the first time in almost three years (since March 2021.) Most of that slowing is expected to come from a pullback in energy prices and another drop in food price growth. Core price growth, which excludes food and energy products, should ease less—we expect to 3.8% year-over-year in January from December’s 3.9%. But a disproportionate share of that increase still comes from higher home rents. The growth in shelter costs will continue to slow as lower market rents gradually feed through to leases. Price growth of goods has slowed back to around zero as the impact of acute global supply chain disruptions earlier ease.

Week ahead data watch

StatsCan's advance results indicated manufacturing sales declined 0.6% in December. And we expect the volumes to be little changed given a similar decline in the industrial product price index for the manufacturing sector in the month.

The early indicator for 'Core' wholesale sales (ex. Petroleum, Petrol Prod & Other Hydrocarbons) pointed to a 0.8% growth in December, mainly driven by higher sales in motor vehicle and parts subsector.

U.S. industrial production likely grew by 0.5% in January, hours worked for manufacturing sector were little changed, but a rise in electricity output is flagging an increase in the utility sector.

Week Ahead North America – US Inflation Data Eyed, Canada Quiet

- US inflation and retail sales among the highlights

- Tier three Canada data only after employment update

Could a March rate cut still be on the table?

US economic data since the turn of the year has been far from ideal considering traders had priced in up to 175 basis points of rate cuts at one stage.

Expectations have since been pared back with markets only pricing in 125 but some think that may even be too optimistic, particularly following the January jobs report.

The US inflation revisions on Friday helped to settle the nerves but now it’s over to the scattering of January data we get next week. CPI inflation is once again front and center as we look for further signs that near-term inflationary pressures have significantly abated which could improve the chances of a March cut.

But there are plenty of other releases too that traders will be watching closely for. Retail sales, jobless claims, and consumer sentiment to name a few. Inflation may be the most important but the combination helps to build a fuller picture for the central bank. And it is determined to only cut when its convinced inflation will fall sustainably back to target.

A quiet week for Canada after the unemployment release

January saw unemployment fall in Canada for the first time in more than a year which would be good news in normal times.

Unfortunately, at a time when the Bank of Canada is trying to create some slack in the labor market to achieve its inflation target, it’s far from ideal. A summer rate cut is still expected but we’ll need to see more improvements in the data between now and then.

Next week doesn’t offer much, with tier-three data the only releases on the calendar.

Source – OANDA

USDCAD tested the 50% Fibonacci retracement level once again earlier this week and just like on the previous occasions, the level offered significant resistance.

This now makes the recent low on 31 January all the more interesting as it would represent the neckline of a double-top formation.

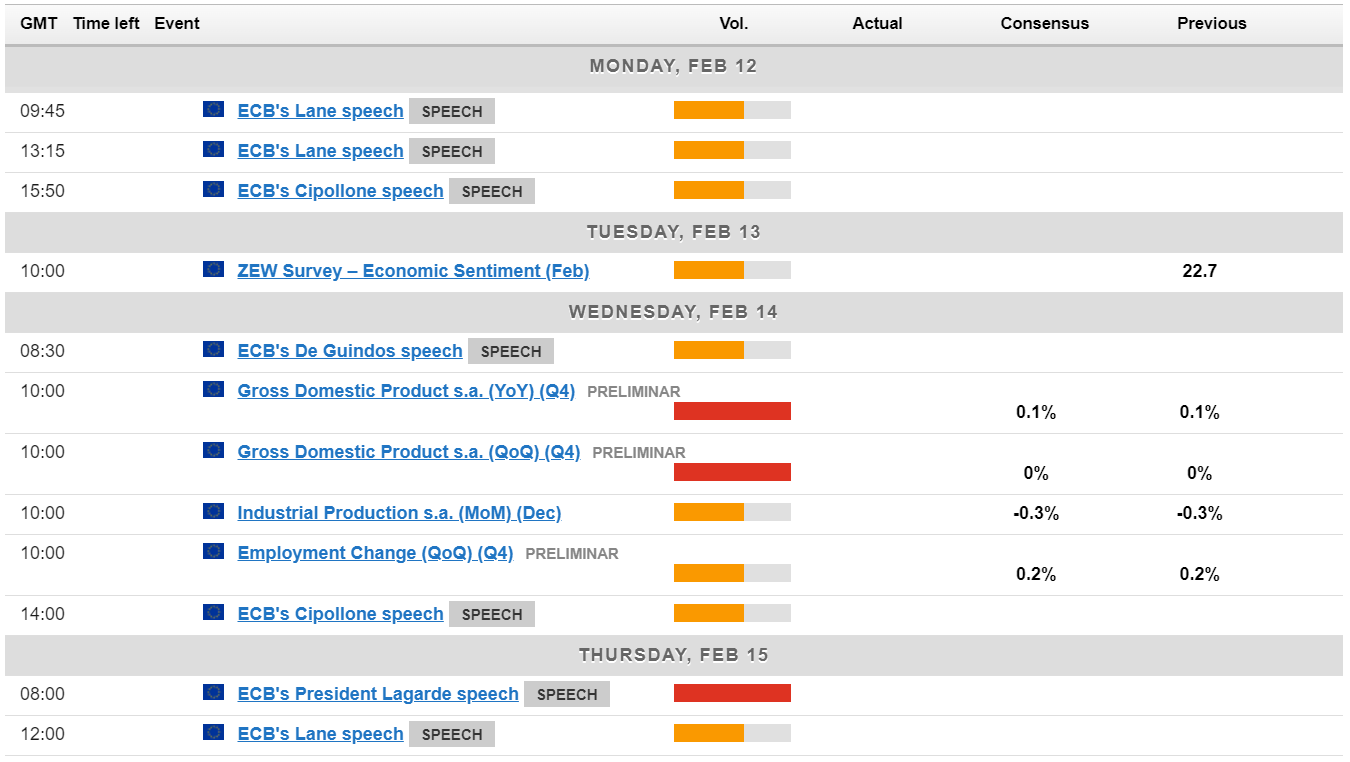

Week Ahead Europe – A Big UK Data Drop, ECB Speakers and Eurozone GDP

- Will ECB policymakers leave the door open to a March rate cut?

- UK data eyed amid division at the BoE

Eurozone GDP may leave bloc on the brink of recession

The eurozone appears to have avoided a recession at the end of last year but it may have simply been delayed.

GDP data for the fourth quarter will be released on Wednesday and is expected to show the bloc didn’t grow again in the final months of the year. It will only take a slight miss to leave the euro area at risk of being in recession in the current quarter.

That said, ECB policymakers probably won’t be particularly swayed by whether the eurozone is just in technical recession or not. That it’s happening while inflation is falling – and is expected to fall much further in the coming months – may do though. And we’ll hear from a number of them next week.

EURUSD Daily

Source – OANDA

EURUSD has trended higher for most of the week after a bad start to it and an end to last. It’s run into support around the 61.8% Fibonacci retracement level which should be an interesting test going forward.

Can the BoE be convinced to cut rates in May?

The standout release is naturally the CPI data on Wednesday as the BoE mandate is inflation at 2% – half the level it stood at in December. Inflation is expected to fall over the coming months but a greater decline in January could help the case of cutting rates sooner. Equally, a higher number could be a massive setback and suggest progress has stalled which could see rate expectations pared back again.

The jobs report on Monday is also key, most notably the average earnings component, as this is a major contributor to price pressures. Particularly in the services sector, an area central banks are most concerned about when it comes to getting inflation sustainably back to 2%. Average earnings growth both including and excluding bonuses were above 6% in the three months to December, a level far too high to be consistent with 2% inflation.

GBPUSD Daily

Source – OANDA

The pound has rebounded against the dollar this week but that’s occurred after it broke below the neckline of a topping formation between 1.26 and 1.28. It’s retraced back to the 50% Fibonacci retracement level but has failed to break above there so far.

Will January’s US CPI Inflation Be a Game Changer?

- Forecasts point to stable inflation, weaker core CPI

- Upside surprise is likely, as business indicators point to higher prices

US economy has a blockbuster performance

The US economy has left analysts speechless. Although the Fed has raised interest rates to the highest in four decades, the economy kept growing at a healthy pace in the last quarter of 2023 and six months after the central bank paused its tightening cycle.

The first data releases of the new year pointed to a soft landing or no landing at all. Nonfarm payrolls increased by 353k in January, and December’s reading was revised upwards by more than 100k. On the negative side, part-time jobs were mainly responsible for the increase in new job positions, but overall, the unemployment rate remained around record lows. On top of that, average hourly earnings continued to gain momentum for the third consecutive month and comfortably above the diminishing inflation rate, suggesting that consumers have enough purchasing power to fuel more demand for goods and services.

Retail sales for January could reflect the latest changes in spending habits on Thursday at 13:30 GMT. Analysts expect a monthly slowdown to 0.1% from 0.6% previously. The retail sales control group data, which excludes volatile items, could ease from 0.8% m/m to 0.5%.

Developments on the business front were encouraging, too. The ISM and S&P global business PMI readings expanded faster than analysts expected in January, reporting a notable increase in new orders and hiring. However, what caused a stir was a significant pickup in cost pressures in the services sector. The price index jumped by 7.3 points to 64.00 to the highest since March 2023, reminding investors that the fight against inflation is far from over.

How could CPI inflation data affect sentiment?

On Tuesday, investors will search for more clues on recent price tendencies when January’s CPI inflation data come into the public eye. Forecasts point to a stable headline CPI inflation of 3.4% y/y and a weaker core CPI of 3.7% y/y compared to 3.9% previously.

If forecasts materialize, investors may defend the May rate cut scenario. Note that the probability of a late spring rate cut declined to a toss-up following last week’s upbeat data. Hence, any surprise in the data could be a game changer for rate prospects, but perhaps a tweak in the total number of projected rate cuts could cause more volatility since investors remain confident that the Fed will deliver more than four 25 bps rate cuts despite the central bank projecting only three.

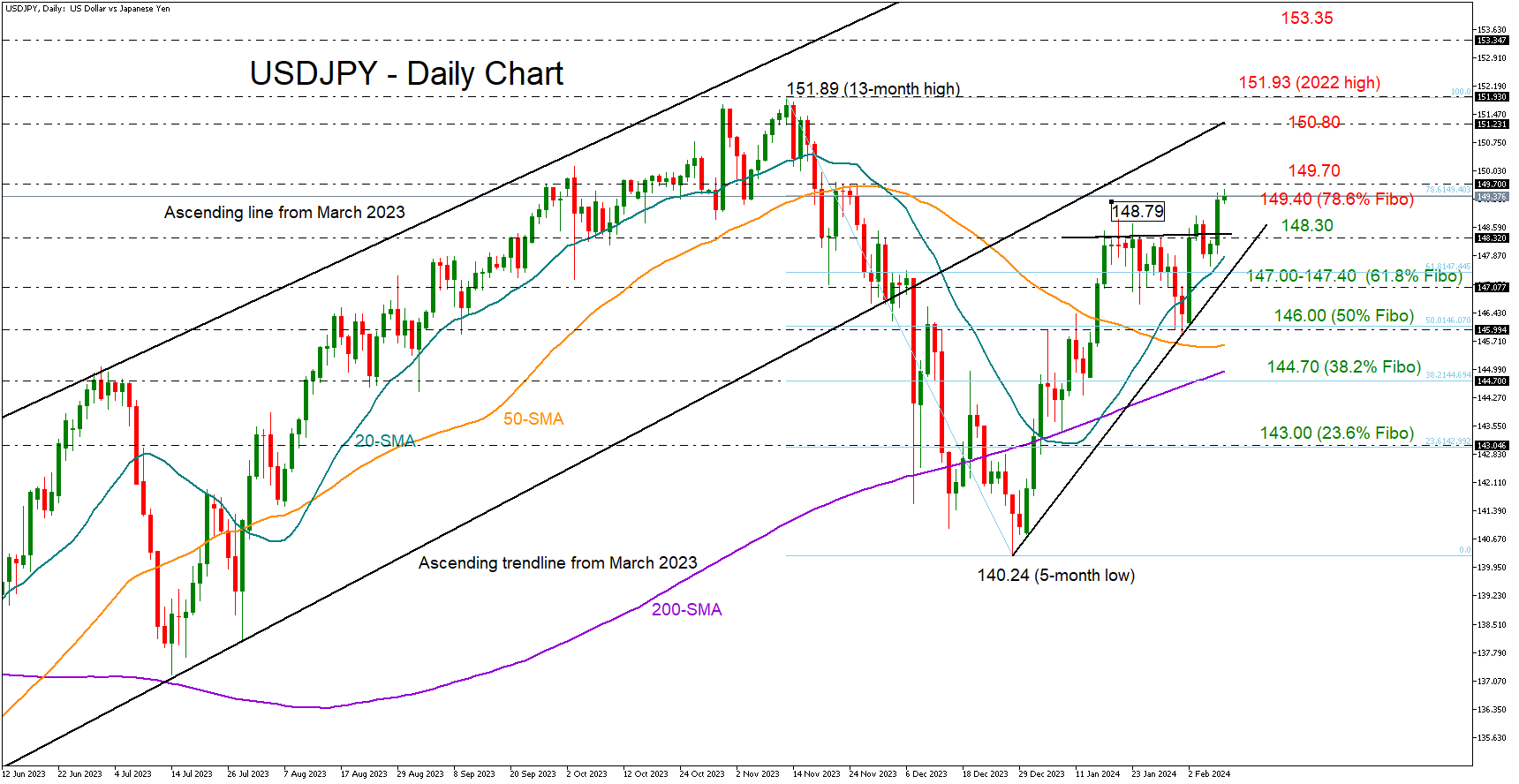

USD/JPY

In FX markets, weaker-than-expected CPI data could oppose the Fed’s wait-and-see stance over rate cuts, putting USDJPY under pressure. Still, from a technical perspective, only a clear close back below the 147.00-147.40 zone, where its 20-day simple moving average (SMA) is positioned, could raise new selling interest.

In the opposite scenario where inflation extends December’s upturn and, more importantly, the core CPI drifts higher too, investors might move the case of a rate cut from May to the summer. There are multiple risk events, from a potential wage-price spiral to rising geopolitical tensions affecting global trade routes, which could still lift business costs and therefore send positive price shockwaves to consumers throughout the year.

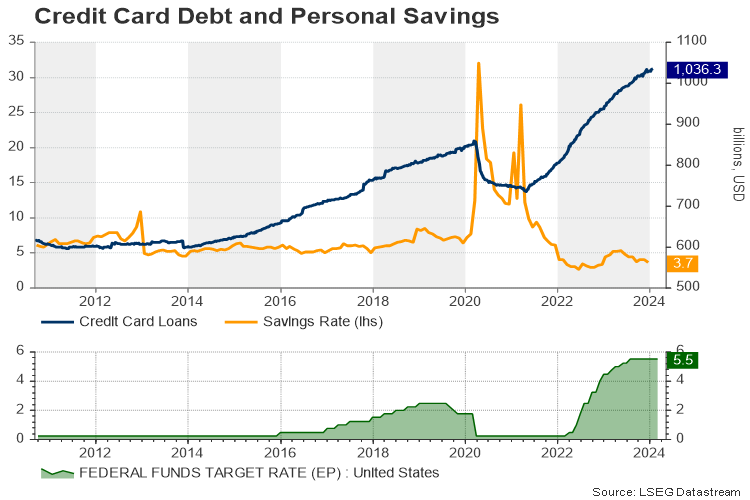

At the same time, the more persistent inflation is, the more fragile the economy can become to a potential downturn as households’ savings ratio is currently at the lowest since the 2007-2009 financial crisis. Moreover, the latest bank episode with the regional New York Community Bancorp revealed that the drop in commercial property values - partially on the back of remote jobs - could raise risks in the financial system. The Fed chief admitted that smaller banks could close or merge, but he added that the issue should be manageable, with the Treasury secretary Jannet Yellen backing that narrative too.

Nevertheless, talks of economic struggles could be a topic for another day. In the meantime, an upside surprise in CPI figures would justify the Fed’s guidance and bode well for the greenback, sending USDJPY above the 149.70 barrier and towards 151.00.

Week Ahead – US CPI in the Spotlight as Dovish Fed Bets Fade

- All eyes on US CPI on Tuesday after run of strong data

- Retail sales on the agenda too for the US dollar

- Pound on standby for UK data flurry, including CPI and GDP

- Japanese GDP and Australian employment coming up too

Will US CPI remain sticky?

Inflation in the United States has generally been trending lower but the progress to get it all the way down to 2% has stalled in recent months, at least according to the CPI metric. Whilst Fed officials are optimistic that price measures will continue to head lower over the next few months, the resilience of the US economy is proving to be a thorn in the side of the Fed, as strong domestic demand increases the odds of inflationary pressures brewing again, particularly if there’s a significant re-acceleration in wage growth.

The consumer price index rose to 3.4% y/y in December, having been hovering above 3.0% since last July. There was somewhat better news for core CPI, which eased below 4.0% y/y for the first time since May 2021.

The picture for PCE inflation – the Fed’s preferred measure – is a little more encouraging, especially on an annualized basis. Headline PCE stood at 2.0% and core PCE at 1.9% on a six-month annualized basis in the last two months of 2023. This may have contributed to the markets’ exuberance in anticipating an imminent dovish pivot by the Fed.

However, Fed officials have overwhelmingly signalled that a rate cut may be some time away, giving the US dollar a leg up as investors priced out a March move.

Tuesday’s CPI print could be crucial in determining whether easing expectations will be pushed back further, as investors still see a strong likelihood of a rate cut in May. Forecasts suggest CPI stayed unchanged at 3.4% y/y in January.

US economy might be running hot again

But the worry isn’t just inflation not coming down fast enough. The US economy appears to have enjoyed a pickup in activity in January so Thursday’s retail sales numbers will be vital too. The consensus estimate is for a 0.2% m/m increase, pointing to a cooldown from December.

In other data, the Philly Fed manufacturing index is also due on Thursday along with industrial production figures for January. Wrapping up the week on Friday are housing starts, building permits, producer prices and the University of Michigan’s preliminary consumer sentiment survey.

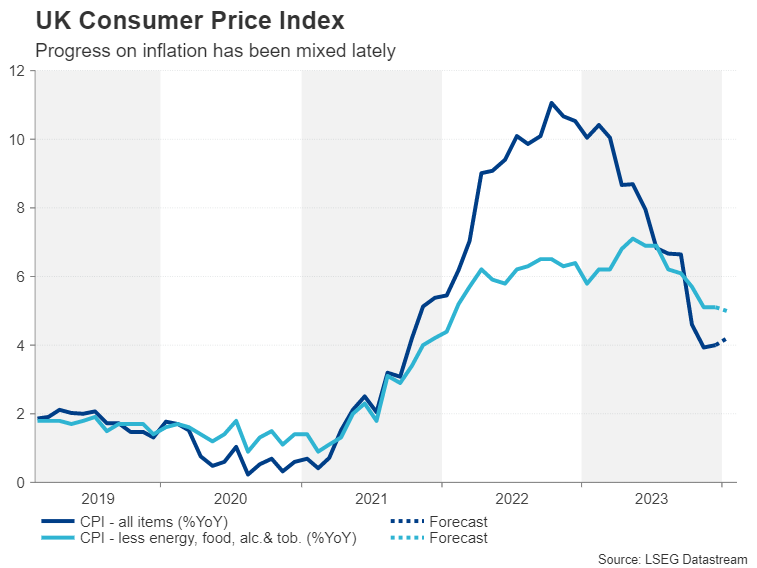

Pound to seek direction from UK CPI and GDP data

Inflation in the UK fell rapidly at the end of 2023 before edging up slightly. If both headline and core CPI resume their decline in January, this would come as a relief for the Bank of England but probably not for the pound. However, only the core measure is forecast to tick lower and headline CPI is expected to climb again to 4.2% y/y.

Although BoE policymakers have been pushing back on market expectations of an early rate cut, investors could ratchet up their bets if there’s a surprise drop in inflation.

But like in the US, it’s not just about the inflation picture as the economy has also been performing somewhat better than anticipated. UK GDP contracted by 0.1% in the three months to September, raising fears about a recession. But Q4 data due on Thursday is expected to show that the UK economy avoided a recession and recorded flat growth during the period.

Meanwhile, retail sales numbers will be watched on Friday for signs that consumer spending is recovering following an upbeat services PMI.

Not to forget about the labour market where wage growth has only just started to moderate. The employment report for December is out on Tuesday and any unexpected strength in the jobs market could dampen rate cut bets, lifting the pound.

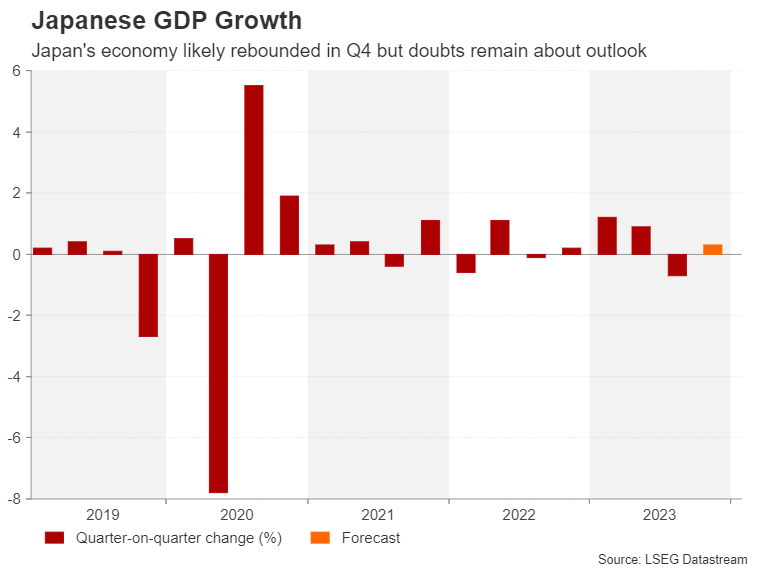

Japanese economy probably returned to growth in Q4

In Japan, the focus will be on the nation’s Q4 GDP readings on Thursday. After suffering a steeper-than-expected contraction in the third quarter of last year, economic growth is forecast to have rebounded by 0.3% q/q in the final three months of 2023.

If Thursday’s figures disappoint, doubts about the strength of the recovery are likely to persist as recent data has been rather mixed amid subdued consumption, although higher exports probably boosted GDP in Q4.

The Bank of Japan is hoping that this year’s ‘Shunto’ wage negotiations will spur pay growth and generate more sustainable inflation. But this could be a hard target to achieve even if the BoJ is confident enough to project it, so a sound economic backdrop is essential in adding credibility to its forecasts.

The yen could come under pressure on the back of a softer-than-expected bounce back, but an upside surprise cannot be ruled out either as most businesses have been positive in the BoJ’s most recent Tankan surveys.

Aussie and kiwi on a slippery slope

The Australian dollar hasn’t had a very good start to 2024 even though the Reserve Bank of Australia is expected to be one of the last to cut rates this year. China’s economic woes and the resurgent US dollar have offset the RBA’s relatively more hawkish stance.

An improvement in the labour market might lessen the aussie’s pain. Employment fell in December, taking markets by surprise. But Thursday’s jobs numbers are expected to provide some relief as the Australian economy likely added 30k jobs in January. This could pull the aussie away from multi-month lows versus the greenback as investors would pare back their bets of how many times the RBA would cut rates this year.

Chinese markets will be shut for the entire week for the Lunar New Year celebrations so the aussie could be more sensitive than usual to domestic data.

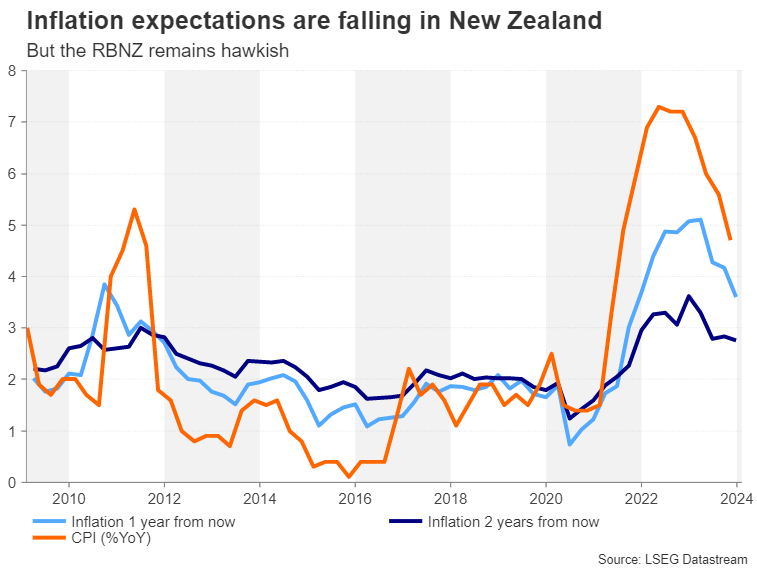

Across the Tasman Sea, the New Zealand dollar will be keeping an eye on the latest inflation expectations survey on Tuesday that the Reserve Bank of New Zealand publishes quarterly.

In the last report, one-year inflation expectations had fallen to 3.6% and two-year ones to 2.8%. Should expectations about future inflation maintain their downward path, this could undermine any fresh hawkish rhetoric from RBNZ Governor Adrian Orr when he speaks on Thursday.

Nevertheless, any downside reaction in the kiwi would likely be short lived as the RBNZ would need to see more evidence of abating inflation before turning dovish.

Weekly Focus – Higher Rates and Central Bank Pricing

Focus this week has been on the increase in interest rates and the decline in market expectations for central bank rate cuts that were initiated by the strong US job market report late Friday last week. While the headline numbers were very strong, we stress that the underlying details were softer. Average weekly hours worked declined to the lowest level since 2010 (when excluding March 2020) in a sign that the labour market is not as tight as one could fear. Also, average weekly earnings growth was negative month-on-month. Yet, markets have scaled back interest rate cut expectations for 2024 for the Fed and ECB from almost six 25bp cuts to four and a half cuts since Friday last week. These moves were also supported by speeches from Powell and ECB's Schnabel. Powell reiterated that the Fed would most likely not cut rates in March and backed the December dot plots of three cuts this year. Schnabel warned against the still present upside risks to euro area inflation that could cause inflation to flare up again.

The US ISM services index rose more than expected in January to 53.4 (cons: 52.0, prior: 50.6) and the prices paid subindex rose to the highest level since February 2023. The ISM services index has been very volatile and the rise in the price index contrasts the signal from PMI services. Hence, one should not put too much emphasis on a single print. However, in the big picture it is still nearly all recent US data releases that have surprised to the upside.

Chinese inflation fell more than expected in January with CPI at -0.8% y/y vs expectations of -0.5% y/y (previous was -0.3% y/y). Inflation was especially pulled lower by food prices. However, core CPI also declined to 0.4% y/y from 0.6% y/y in December. While deflation is still not widespread in core measures, the falling core inflation is clearly a symptom of a weak economy with too soft demand relative to supply.

In the euro area, retail sales fell 1.1% m/m in December in a sign that euro area consumers were still cautious about spending in December like the entire year. Given the low current consumption share, strong savings, high employment, and rising real wages there is room for private consumption to pick up in 2024. Yet, we likely still need to see a more pronounced increase in consumer confidence before private consumption picks up.

In Japan, the average wage growth for December came in at 1.0% y/y, which was stronger than in November, albeit lower than the 1.3% expected by consensus. Wage growth is key to the outlook for the Bank of Japan's (BoJ) monetary policy and possible tightening. We expect that we will probably have to wait until spring wage negotiations for wages to start moving much higher, and thereby for BoJ tightening to start tightening monetary policy. In the UK, wage growth eased in January in a comforting sign for the BoE although the wage pressure is still strong, and the labour market remains tight.

Focus next week is on US Inflation. The January US CPI print will be key in determining whether the recent upside surprises in US macro translates into higher price pressures. Also in the US, we look out for retail sales and the University of Michigan survey. From the UK we receive the job market report and January CPI. In the euro area, focus is on industrial production and German ZEW. Finally, in Japan we look out for 2023Q4 GDP.

Sunset Market Commentary

Markets

The US Bureau of Labor Statistics published its annual CPI revisions today. The same event last year showed some deviations from the initial outcomes large enough that they casted doubt on the speed of the disinflationary process. This time around, however, the hyped-up release lived up to its reputation as a non-event. Both the headline and core measure saw some adjustments but they were minor and two-sided. Having last year’s unpleasant surprise in mind, financial markets breathed a sigh of relief. US Treasury yields dropped from their intraday day highs in a kneejerk reaction before reversing course and resume today’s ride higher. They currently add between 2.4-3.7 bps across the curve. German Bunds underperform in an inversion move. Yields rise 6 bps at the front with the 2-y feeling ready for a test of the YtD high. Central bank speech was limited to ECB’s Kazaks nothing that inflation has fallen strongly, making 2024 the year of rate cuts. While the precise timing depends on the data, Kazaks said he isn’t as optimistic as markets on an inaugural cut in spring (euro area money markets price in about 35 bps of cuts by June). Speaking of data, market attention is gradually shifting towards Tuesday’s US CPI reading (January). Analysts expect the headline figure to ease from 3.4% to 2.9% and see a more gradual decline in core CPI from 3.9% to 3.7%. With all but every Fed member basically ruling out a March cut, all eyes are turned to the May policy meeting. A rate cut then (not our preferred scenario) is for about 80% discounted and could in theory gain further traction in case of a number in line or below consensus. Other important US data include January retail sales on Thursday and University of Michigan consumer confidence on Friday. The UK, however, is taking center stage with an extended economic update, spanning the labour market, retail sales and especially January CPI & Q4 GDP numbers. This may well be the trigger needed to unlock EUR/GBP from its current impasse. The pair is unable to escape from the laws of gravity, keeping it in an extremely tight trading range since mid-January. EUR/GBP looks especially vulnerable for a break to the downside with the key technical reference at 0.8492 the only thing standing in the way for a return to 0.834 (August 2022 correction low).

News & Views

Inflation in Hungary for the first time since March 2021 returned within the 3.0% +/- 1.0% target band of the MNB. Prices rose 0.7% M/M but this still reduced the Y/Y measure from 5.9% to 3.8% (consensus 4.3%), lower than the mean value in the December inflation report. According to the MNB, the positive surprise was primarily due to lower than expected fuel and processed food prices. In a separate assessment the National Bank of Hungary reckoned that measures of core inflation also declined. Core inflation ex indirect taxes eased from 7.6% to 6.1%. CPI ex processed food slow from 9.6% to 8.1%. Core inflation was also slightly below the MNB expectations while the rises in prices of demand-sensitive items was in line with the projection. On a more general level, the MNB sees a general slowdown in inflation, fuelled by the combined effect of tight monetary policy, the government’s measures to strengthen competition, subdued demand, base effects and a significantly lower external cost environment. The MNB sees the continued slowdown in underlying inflation illustrated by the fact that three-month annualised core inflation and inflation were both below 3 percent. The 2-y Hungarian swap yield dropped 11 bps after. The data again raise the case for the MNB to step up the pace of rate cuts from 75 bps to 100 bps. However, this argument is in balance with the forint weakening close to the EUR/HUF 390 barrier Admittedly, the forint didn’t decline any further today (EUR/HUF 388.5).

According to data published by the Swedish Riksbank today, the Bank reached the targeted amounts aimed at reducing the currency risk on its foreign exchange reserves. In September last year, it started the process of hedging the countervalue of USD 8 bln and euro EUR 2 bln of reserves. The procedure was expected to take between 4 and 6 months. The amounts of hedged funds were reached in the week of January 26, completing the program. The procedure officially wasn’t intended to serve as a currency intervention to support the krone. At the same time, it was seen as a tool to limit losses in reserves if the krone, which was seen as trading at a weak level, would appreciate. EUR/SEK currently trades at 11.28, compared to levels close to EUR/SEK 12 at the end of September.