Sample Category Title

USD/CAD Dips as Canadian Employment Shines

- Canadian employment jumps, wage growth falls

- USD/CAD edges lower

The Canadian dollar has climbed higher in the North American session after the release of Canada’s December employment report. In the North American session, USD/CAD is trading at 1.3432, down 0.20%.

Canada’s job growth beats forecast

Canada usually posts employment reports on the same Friday as the US, but had the stage all to itself today, as the US posted its job report last week. The news was good as employment jumped by 37,300 in January, smashing the market estimate of 15,000. The December reading was revised upwards to 12,300 from the initial estimate of just 0.1 thousand. The unemployment rate ticked lower to 5.7%, down from 5.8% in December and below the market estimate of 5.7%. As well, average hourly earnings eased to 5.3% y/y in January, compared to 5.7% a month earlier.

The Bank of Canada will be carefully monitoring the jobs data. Employment growth jumped, which points to a stronger labour market, but at the same time wage growth dropped. Wages are a key driver of inflation and today’s decline will support the BoC continuing to pause and not cut rates until the middle of the year or later. The BoC is content to continue its “higher for longer” stance and let high rates continue pushing inflation lower. The central bank’s top priority remains bringing down inflation to the 2% target, but businesses and consumers, especially homeowners, are groaning under the weight of elevated rates and are looking for some relief from the BoC.

The Federal Reserve continues to push back against rate cut expectations in March. This week, a host of Fed members delivered the message that inflation is heading lower but the Fed remains cautious and isn’t yet ready to lower rates, as the battle against inflation is not yet won. The markets have taken note of the Fed’s pushback and have pared expectations of a rate cut in March to 17%, down from over 70% in December, according to the CME’s Fed Watch tool.

USD/CAD Technical

- USD/CAD tested support at 1.3434 earlier. Below, there is support at 1.3392

- 1.3509 and 1.3551 are the next resistance lines

Canada’s Labour Market Strengthens in January, But Details Less Constructive

The Canadian labour market added 37.3k positions in January, with full-time employment down 11.6k and part-time employment up 48.9k.

The unemployment rate declined 0.1 percentage point to 5.7%, helped by a 0.1 percentage point to decline in the labour force participation rate to 65.3%. Despite a massive 126k increase in the population in January, only 18k net-new people entered the labour force, taking participation lower.

Employment by sector showed gains in wholesale/retail trade (+31k) and finance, insurance, real estate, rental and leasing (+28k). There was a notable decline in accommodation and food services (-30k).

Lastly, total hours worked rose 0.6% month-on-month and wages were down 5.3% year-on-year (from 5.7% on December).

Key Implications

The headlines for today's job report suggested surprising strength from the Canadian labour market. However, while falling unemployment is a good sign for the strength of the job market, the underlying details were weak. All the job gains were part-time, with the vast majority coming from cyclically insensitive public sector hiring. This along with the regular seasonality issue with January job reports (remember the head fake we got last January?), we'd argue that it is not the type of report the makes us think the Canadian labour market is in for a renewed upturn. Case in point, the lower unemployment rate was helped by weaker participation – not a typical sign of a strong labour market.

The Bank of Canada won't change course after today's report. The data are simply too volatile and don't paint a clear picture of the state of the Canadian economy. This leaves the BoC to continue fixating on the state of inflation. With headline and core inflation rates stuck around the mid-3% level, the Bank needs to see improvement before it can be convinced that it will reach its goal of price stability. This has markets pushing back on the timing of rate cuts, with June or July as the most likely start date.

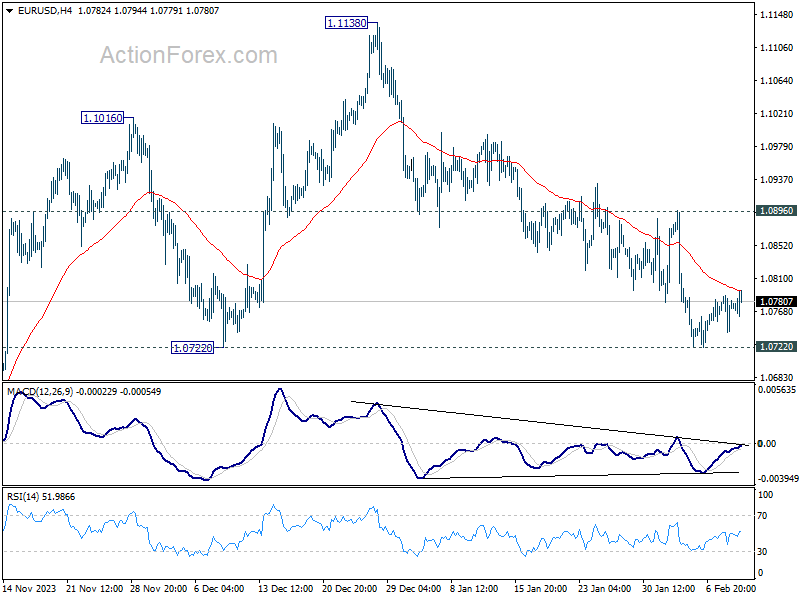

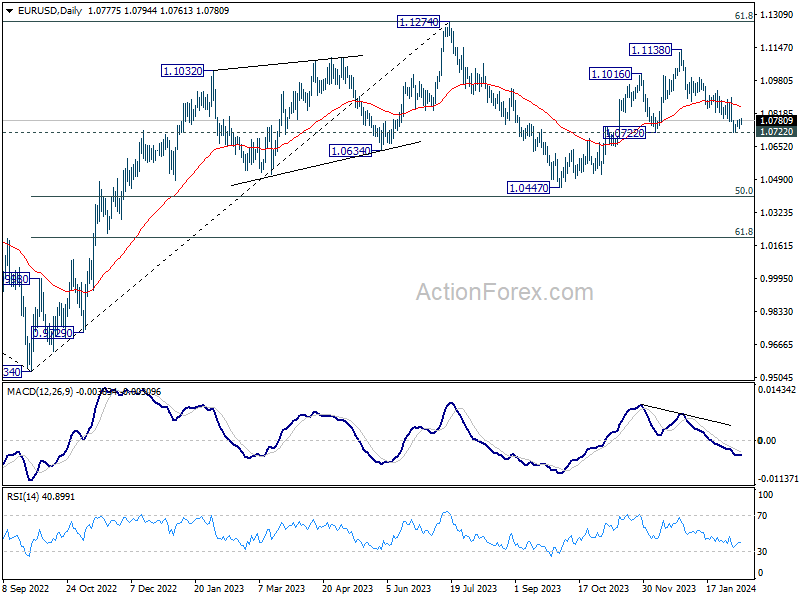

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0750; (P) 1.0770; (R1) 1.0797; More...

Intraday bias in EUR/USD remains neutral and outlook is unchanged. On the downside, decisive break of 1.0722 will argue that whole rise from 1.0447 has completed. Deeper fall would then be seen to target this low. On the upside, break of 1.0896 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

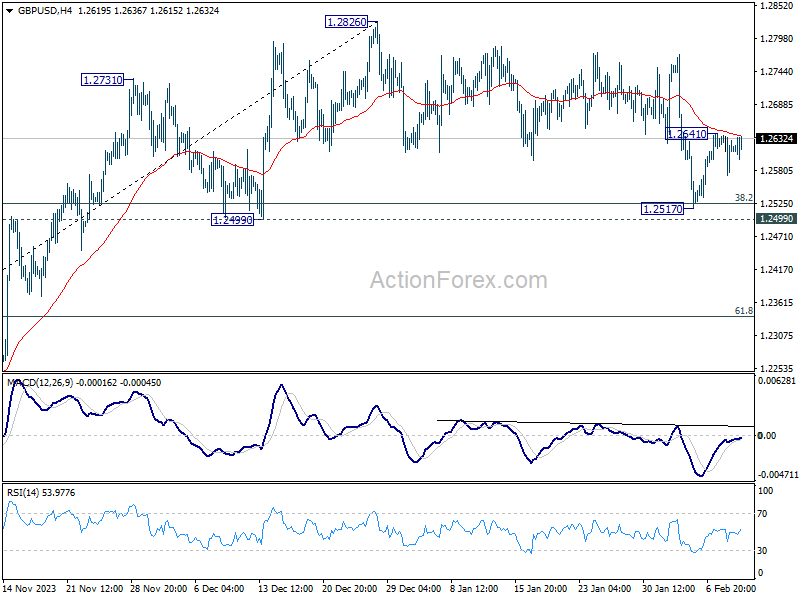

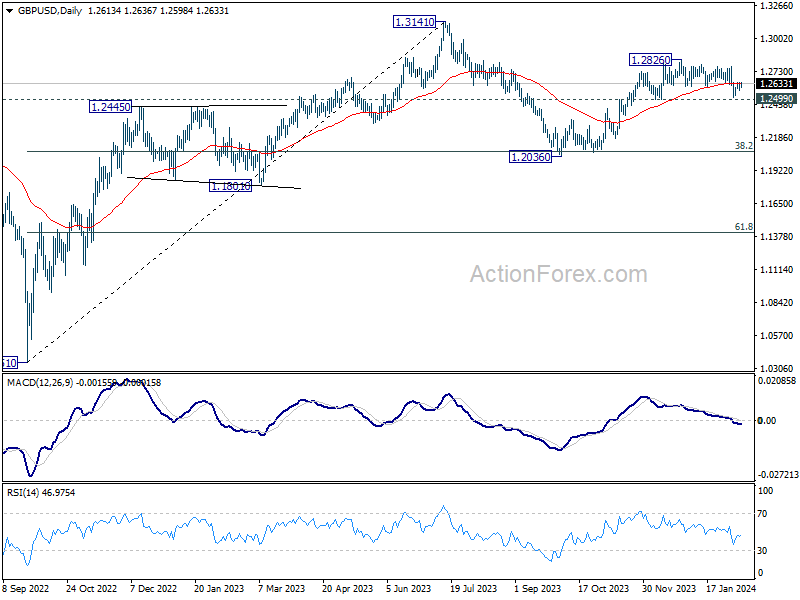

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2580; (P) 1.2609; (R1) 1.2647; More...

Intraday bias in GBP/USD stays neutral at this point. On the upside, above 1.2641 will resume the rebound from 1.2517 to retest 1.2826 high. On the downside, however, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's still in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

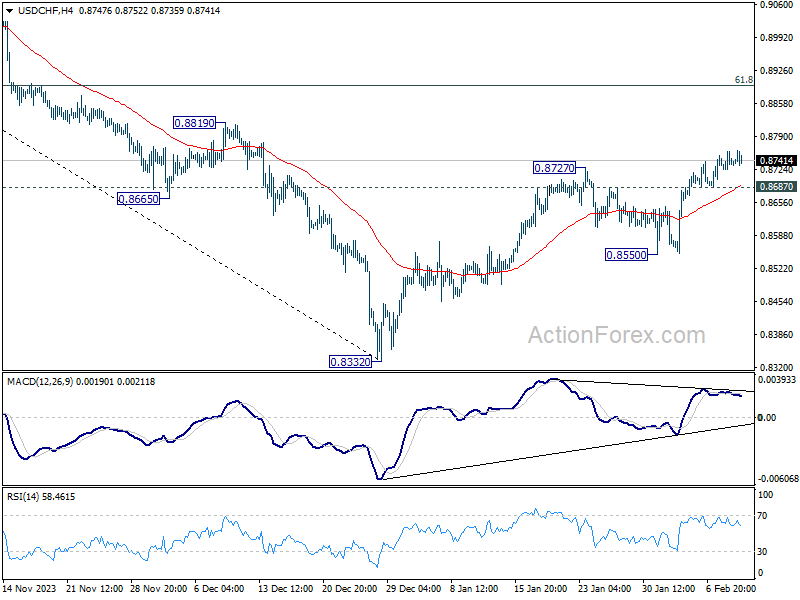

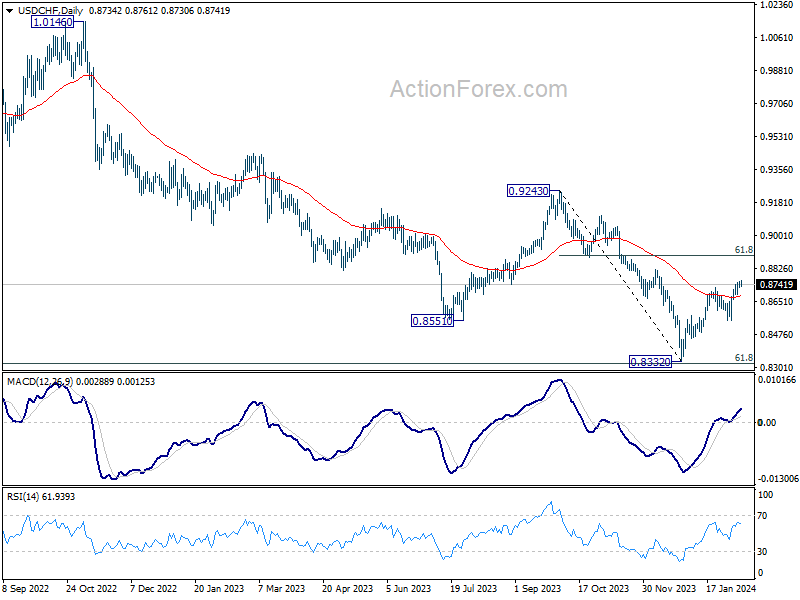

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8721; (P) 0.8741; (R1) 0.8757; More....

Intraday bias in USD/CHF remains on the upside at this point. Current rise from 0.8332 would target 61.8% retracement of 0.9243 to 0.8332 at 0.8995 next. On the downside, below 0.8687 minor support will turn intraday bias neutral first. But near term outlook will stay cautiously bullish as long as 0.8550 support holds.

In the bigger picture, there is prospect of medium term bottoming at 0.8332 considering possible bullish convergence condition in W MACD, and the support from 0.8317 long term fibonacci support. Sustained trading above 55 D EMA (now at 0.8677) will affirm this case, and bring stronger rise back towards 0.9243 resistance, even as a corrective move.

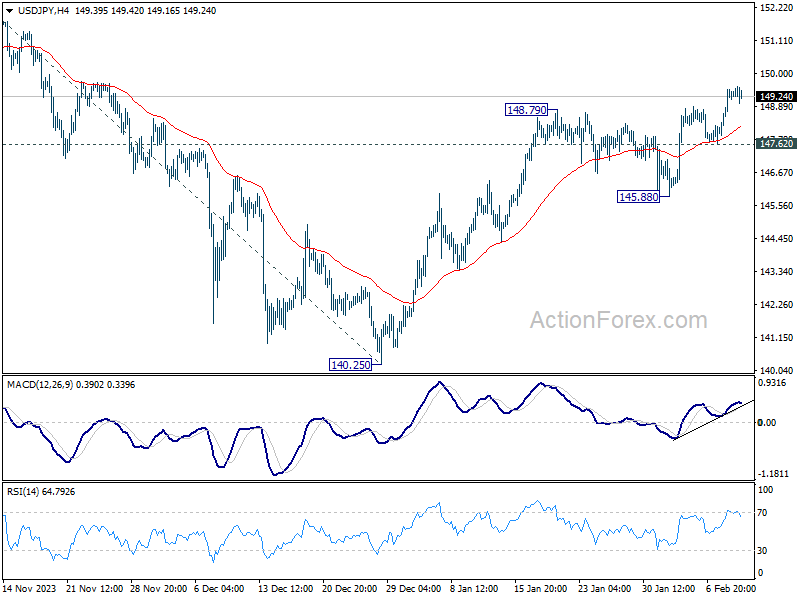

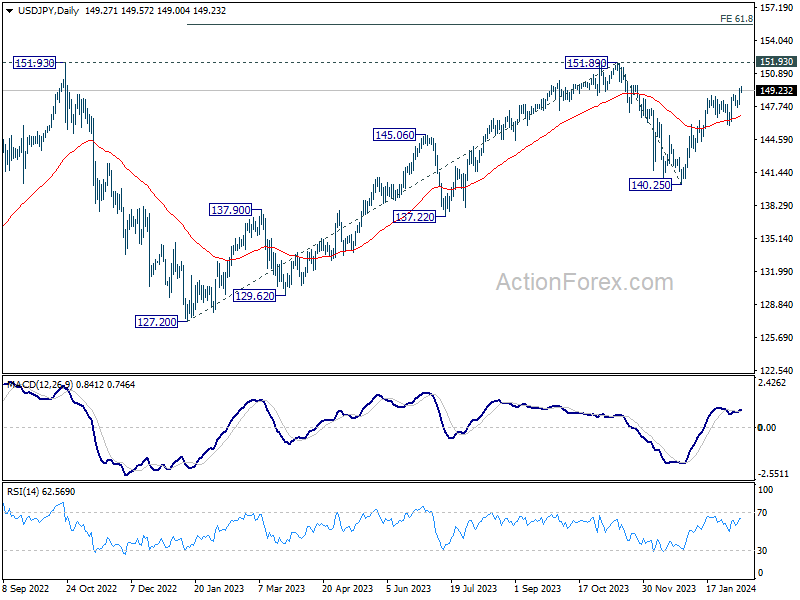

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.35; (P) 148.91; (R1) 149.89; More...

USD/JPY's rally from 140.25 is still in progress and intraday bias stays on the upside. Further rally would be seen to retest 151.89/93 key resistance zone. Decisive break there will confirm resumption of larger up trend. On the downside, below 147.62 minor support will turn intraday bias neutral first. But near term outlook will remain cautiously bullish as long as 145.88 support holds.

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption, and next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.

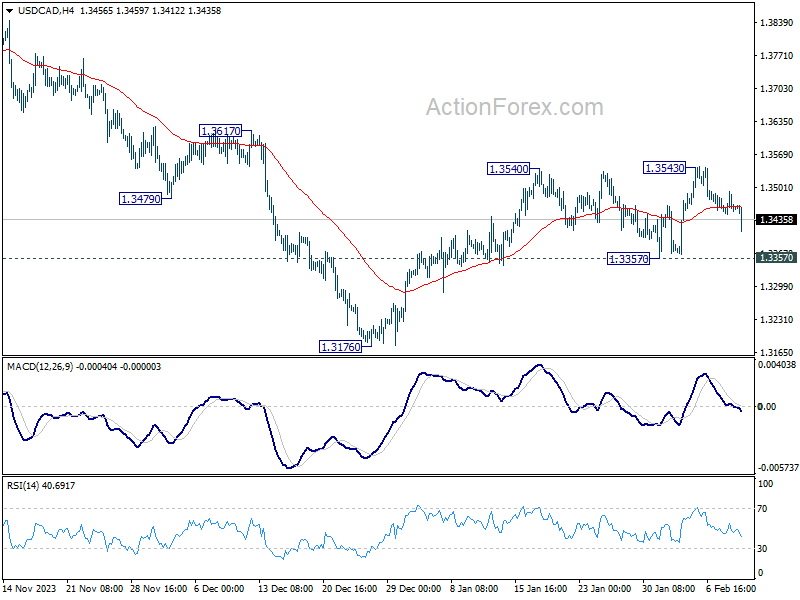

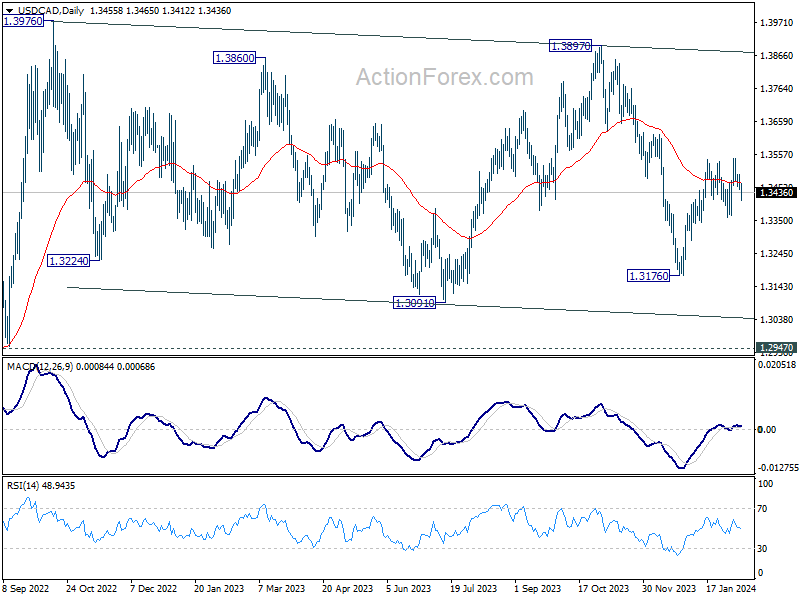

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3440; (P) 1.3467; (R1) 1.3485; More...

USD/CAD dips notably in early US session but stays well above 1.3357 support. Intraday bias remains neutral first and further rally is in favor. On the upside, decisive break of 1.3540/3 will resume the rise from 1.3176. That will also revive that case that whole fall from 1.3897 has completed, and target this resistance. Nevertheless, firm break of 1.3357 support will argue that rebound from 1.3176 has completed, and target this low for resuming whole fall from 1.3897.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

Canadian Dollar Rises on Strong Job Data, Yen and Franc Weakness Persists

Canadian Dollar bounces broadly in early US session, bolstered by unexpectedly robust Canadian employment data. This development comes amidst cautious remarks earlier in the week from BoC Governor Tiff Macklem, who tempered expectations by noting that achieving the 2% inflation target would be a gradual process, fraught with persistent risks. The January meeting minutes echoed this sentiment, highlighting concerns over the potential for enduring inflationary pressures and the dangers associated with prematurely easing monetary policy. Today's employment figures would likely provide BoC's more hawkish members with additional justification for maintaining a cautious stance on monetary adjustments.

The broader currency market is also reacting to a mild uptick in risk sentiment, which appears to be favoring commodity currencies at large. New Zealand Dollar is currently leading the pack, buoyed by ANZ's forecast that RBNZ will deliver rate hikes in both February and April. Australian Dollar is having a moderate increase as well, albeit at a slower pace compared to its counterparts.

The general trend towards strength in commodity currencies contrasts with the ongoing weakness observed in the Swiss Franc and Japanese Yen. Meanwhile, Dollar, Euro, and Sterling are continuing their range-bound trading patterns, reflecting a period of extended consolidation.

In Europe, at the time of writing, FTSE is up 0.15%. DAX is up 0.13%. CAC is up 0.02%. UK 10-year yield is down -0.0038 at 0.4048. Germany 10-year yield is down -0.0011 at 0.2356. Earlier in Asia, Nikkei rose 0.09%. Hong Kong HSI fell -0.83%. Singapore Strait Times fell -0.15%. Japan 10-year JGB yield rose 0.0253 to 0.724.

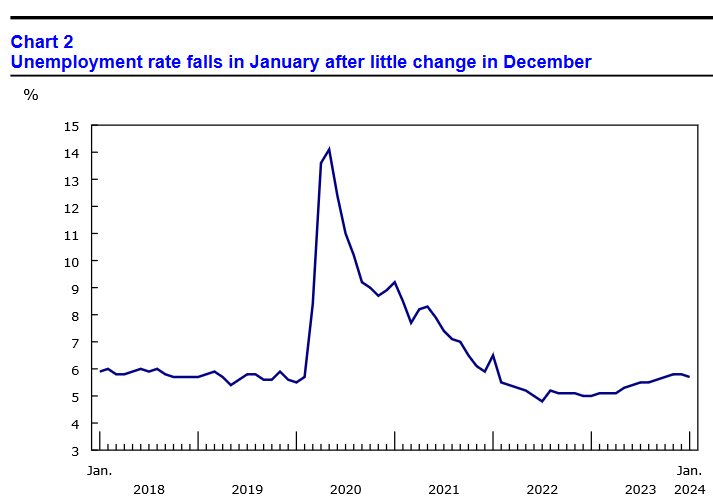

Canada's employment rises 37k in Jan, unemployment down to 4.7%

Canada's employment grew strongly by 37k in January, well above expectation of 35k.

Unemployment rate fell -0.1% to 5.7%, the first decline since December 2022, and below expectation of a rise to 5.9%. Participation rate fell -0.2% to 65.3%.

Employment rate fell -0.1% to 61.6%, as population growth (+0.4%) outpaced employment growth (+0.2%).

Average hourly wages rose 5.3% yoy, slowed from prior month's 5.4% yoy.

ECB's Kazaks: Summer the moment for rate cut, not Spring

ECB Governing Council member Martins Kazaks provided a tempered outlook on the prospects of interest rate reductions within Eurozone, cautioning against premature expectations for cuts as early as spring. In an interview with Latvijas Radio, Kazaks outlined his stance on the timing and conditions necessary for beginning to ease ECB's monetary policy stance.

"At the moment, there are expectations that the rates could be cut in the spring, in March or April — I wouldn't be optimistic," Kazaks stated. He advocates for a patient and data-driven approach, emphasizing the importance of ensuring that inflation trends are firmly under control before considering rate reductions.

"I would be cautious and I would wait until the inflation story is over. Then we can safely breathe and those rates can be lowered step by step," he elaborated.

Looking ahead, Kazaks indicated "Summer could be that moment". However, he cautioned that would depend on incoming data. "If nothing negative happens, that pushes up inflation and geopolitical risks, if nothing like that happens then this will be the year that rates start to be lowered," he added.

ECB's Villeroy confident in Eurozone's path to overcoming inflation sickness

ECB Governing Council member Francois Villeroy de Galhau, in an interview with LCI television, anticipates reducing interest rates within the year, marking a significant move away from the aggressive inflation-fighting measures.

"We will probably cut rates this year because we are making progress against inflation," Villeroy stated.

"We are exiting the emergency of fighting inflation and are on the right path to overcome the sickness," he elaborated.

Further bolstering this positive outlook, Villeroy projected gradual acceleration in economic growth in France in the coming months, fueled by decline in inflation rates that is expected to fall below pace of wage increases.

Bank of France's forecast, as mentioned by Villeroy, anticipates avoiding a recession, with an expected expansion rate of about 0.9% for the year.

BoE's Haskel defends focus on inflation persistence without regret

BoE MPC member Jonathan Haskel emphasized the importance of caution when interpreting UK's recent decline in headline inflation to 4% in December. While acknowledging this positive trend, he stressed the necessity of focusing on more enduring aspects of inflation.

"I'm not going to apologize for banging on about persistence because I think we're right to," he asserted. Particularly concerning to Haskel are the underlying measures of price growth, especially within the services sector. Despite the headline inflation drop, these measures have recently plateaued at an annual rate of approximately 6.5%, a level Haskel considers still too high.

"The signs that we've seen thus far are encouraging. I don't think we've seen quite enough signs yet," Haskel remarked. "But if we accumulate more evidence on persistence, then by the very logic I've just set out, I'd be happy to change my vote."

Haskel, who supported another rate hike in the last MPC meeting, described his decision as "finely balanced," highlighting his desire for more time to assess the inflationary trend's durability.

RBA's Bullock: Another hike neither ruled out nor ruled in

In an appearance before a parliamentary economics committee in Canberra today, RBA Governor Michele Bullock acknowledged the presence of "some encouraging signs" in Australia's economic landscape, yet cautioned that the nation's battle against inflation is "not over".

RBA's stance remains deliberately balanced, with Bullock stating, "At this stage, the Board hasn't ruled out a further increase in interest rates but neither has it ruled it in." Interest rate path will "depend upon the data and the evolving assessment of risks".

Bullock further elaborated on the dynamics of demand and supply within the Australian economy, indicating that demand levels continue to outstrip the economy's supply capacity. This imbalance, coupled with persistently tight labor market conditions, suggests that while the observed slowdown in demand is contributing to a moderation of inflationary pressures, the desired equilibrium has yet to be reached.

Goods price inflation has shown a softer trend than anticipated, mirroring patterns observed in international markets, Bullock noted. However, services price inflation remains elevated, driven by significant increases in both labor and non-labor input costs.

"Indeed, while inflation was lower than we were expecting in November, this is largely attributable to softer-than-expected goods inflation – services inflation was pretty much where we had forecast it to be."

ANZ forecasts RBNZ rate hikes, triggering Kiwi surge and AUD/NZD range breakout

New Zealand Dollar rises broadly today, buoyed by ANZ's forecast that RBNZ is set to increase the official cash rate in its upcoming meetings on February 22 and again in April, elevating interest rate to 6%.

ANZ's chief economist, Sharon Zollner, highlighted RBNZ's November warning that stronger-than-expected inflation pressures would necessitate further increases in the OCR.

"Data since then has been a series of small but pretty consistent surprises in that direction," Zollner noted. The economist further elaborated that the cumulative effect of these data surprises, though individually not game-changers, collectively strengthens the argument for the RBNZ to proceed with rate increases.

"Indeed, their OCR forecast peak of 5.69% implied that the burden of proof was now on finding reasons not to hike, strictly speaking," Zollner added.

In the currency markets, AUD/NZD's steep decline and strong break of 1.0658 support affirms the bearish case that consolidation from 1.0469 has completed at 1.0942 already. Outlook will stay bearish as long as 1.0691 support turned resistance holds. Next target is retest of 1.0469 (2022 low).

Decisive break of 1.0469 will resume whole down trend from 1.1489 (2022 high), and pave the way to 61.8% projection of 1.1489 to 1.0469 from 1.0942 at 1.0312 in the medium term.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3440; (P) 1.3467; (R1) 1.3485; More...

USD/CAD dips notably in early US session but stays well above 1.3357 support. Intraday bias remains neutral first and further rally is in favor. On the upside, decisive break of 1.3540/3 will resume the rise from 1.3176. That will also revive that case that whole fall from 1.3897 has completed, and target this resistance. Nevertheless, firm break of 1.3357 support will argue that rebound from 1.3176 has completed, and target this low for resuming whole fall from 1.3897.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Jan | 2.40% | 2.20% | 2.30% | |

| 07:00 | EUR | Germany CPI M/M Jan F | 0.20% | 0.20% | 0.20% | |

| 07:00 | EUR | Germany CPI Y/Y Jan F | 2.90% | 2.90% | 2.90% | |

| 09:00 | EUR | Italy Industrial Output M/M Dec | 1.10% | 0.50% | -1.50% | -1.30% |

| 13:30 | CAD | Net Change in Employment Jan | 37.3K | 15.0K | 0.1K | |

| 13:30 | CAD | Unemployment Rate Jan | 5.70% | 5.90% | 5.80% |

Canada’s employment rises 37k in Jan, unemployment down to 4.7%

Canada's employment grew strongly by 37k in January, well above expectation of 35k.

Unemployment rate fell -0.1% to 5.7%, the first decline since December 2022, and below expectation of a rise to 5.9%. Participation rate fell -0.2% to 65.3%.

Employment rate fell -0.1% to 61.6%, as population growth (+0.4%) outpaced employment growth (+0.2%).

Average hourly wages rose 5.3% yoy, slowed from prior month's 5.4% yoy.

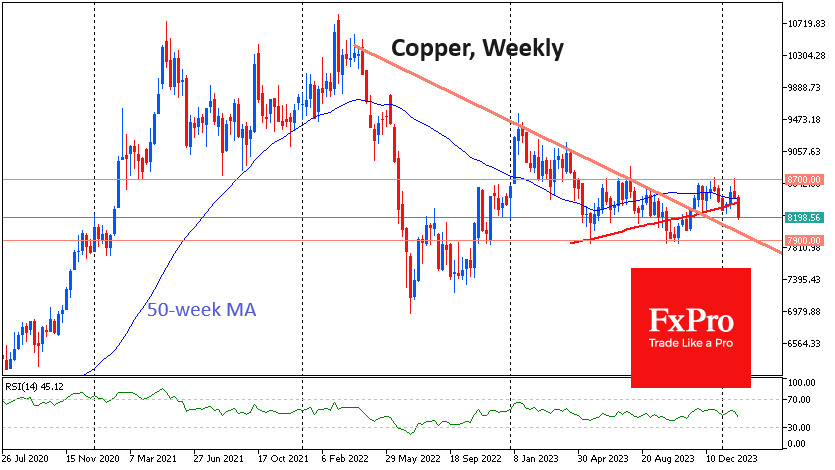

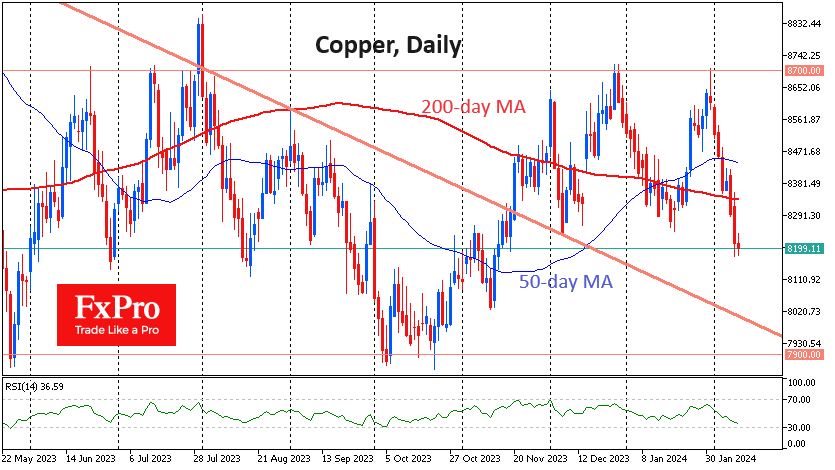

Copper’s Fall An Early Signal of Global Slowdown

Copper exchange prices on Thursday fell to their lowest since November, approaching $8200 a tonne and breaking out of the broad consolidation range of the past two months.

A move out of the $8250-8700 range technically leaves copper vulnerable to a quick fall into the $7900 region, where the lows of November 2022 and May and October 2023 are centred. The Relative Strength Index (RSI) is temporarily on the bears’ side as it has recorded three consecutive declining local peaks at relatively similar highs over the past two months.

Earlier in the week, the price dipped under its 200-day moving average, and the sell-off has only gained momentum since then.

Copper has sold off almost every trading session since the end of last month, losing around 6% in that time. The selloffs at the start of December and January were almost as persistent but had less amplitude.

Copper broke above a vital downtrend resistance level in November and is now set to test its strength as support. By the end of February, it will be just around $7900, which will further strengthen interest in testing this line.

Copper dynamics are essential not only for traders who hold it but also as a manifestation of global production dynamics. This is a signal of slowing global production despite the optimism of stock markets, where global, US, and European indices are storming new highs.

Further declines in the price of copper could attract more bears to global markets. Markets are receiving a similar bearish signal from the global economy in the form of falling natural gas prices. The price of US futures has fallen into the 2020 bottom area.