Sample Category Title

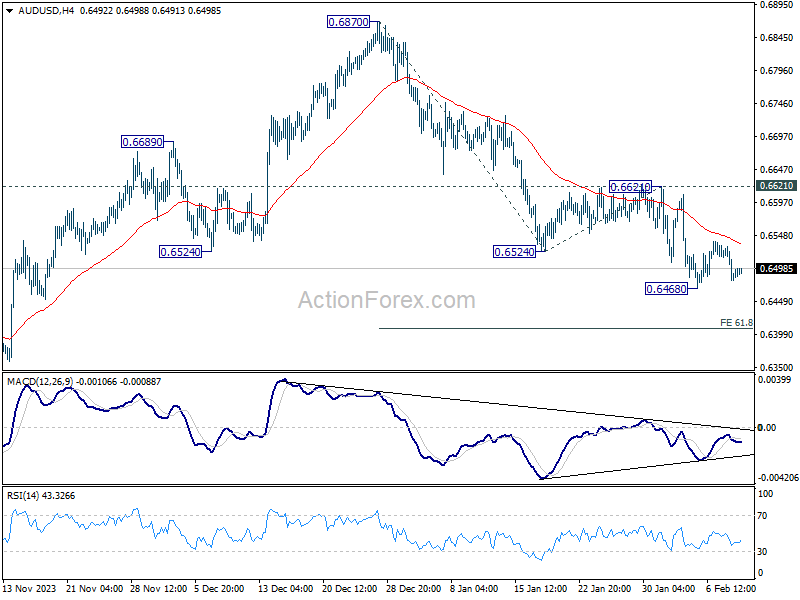

AUD/USD Daily Report

Daily Pivots: (S1) 0.6471; (P) 0.6502; (R1) 0.6522; More...

Intraday bias in AUD/USD stays neutral and outlook is unchanged. While another recovery cannot be ruled out, but outlook will stay bearish as long as 0.6621 resistance holds. On the downside, break of 0.6468 will resume the fall from 0.6870, as part of the down trend from 0.7156, to 61.8% projection of 0.6870 to 0.6524 from 0.6621 at 0.6407 next.

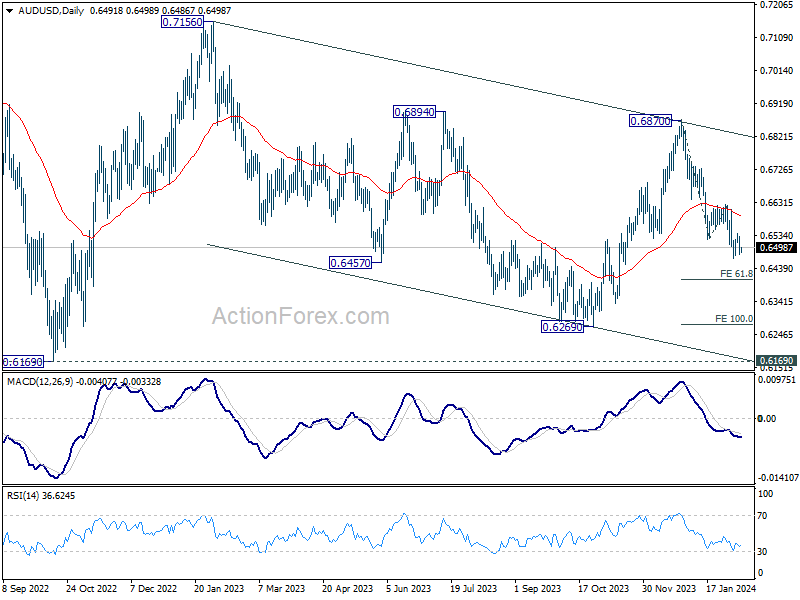

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

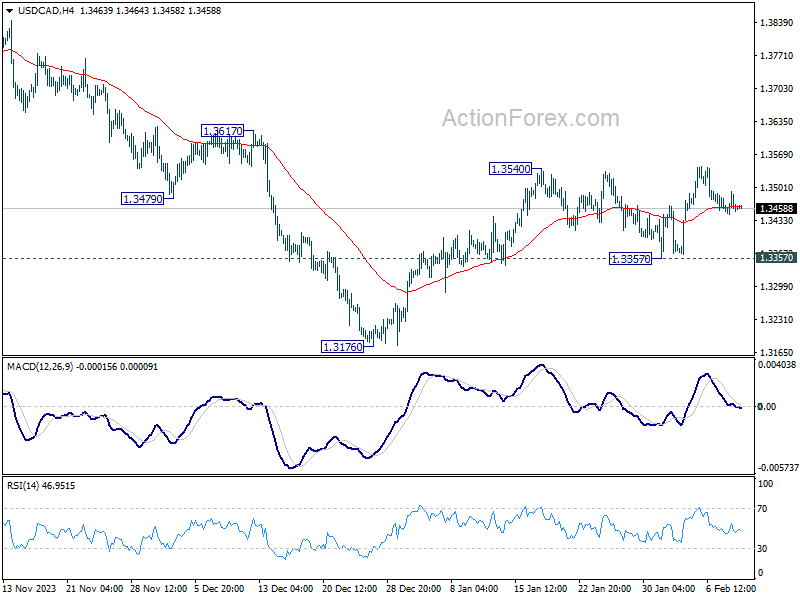

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3440; (P) 1.3467; (R1) 1.3485; More...

Range trading continues in USD/CAD and intraday bias stays neutral. On the upside, break of 1.3540 will resume the rise from 1.3176. That will also revive that case that whole fall from 1.3897 has completed, and target this resistance. Nevertheless, firm break of 1.3357 support will argue that rebound from 1.3176 has completed, and target this low for resuming whole fall from 1.3897.

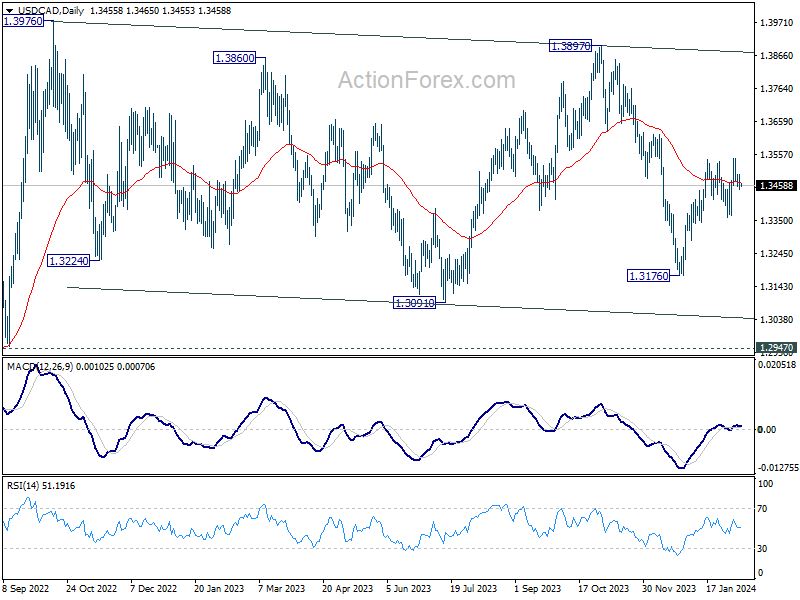

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

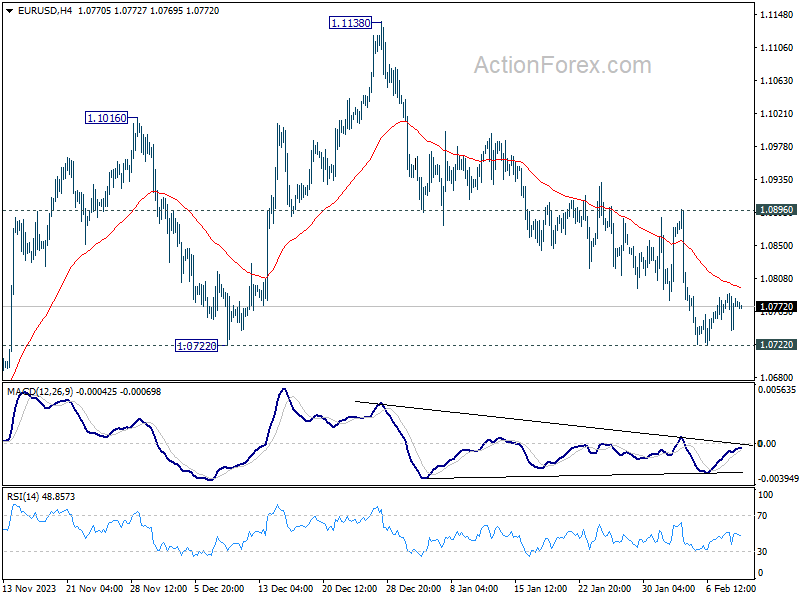

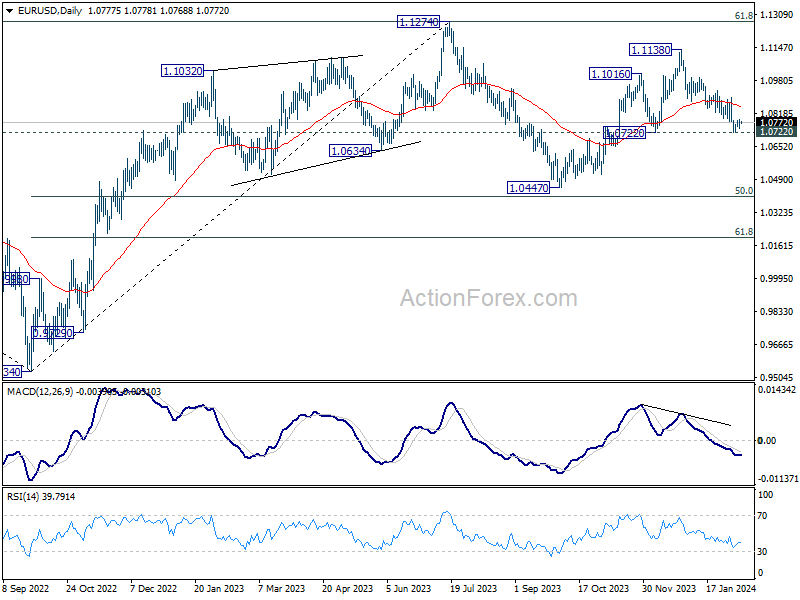

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0750; (P) 1.0770; (R1) 1.0797; More...

Intraday bias in EUR/USD remains neutral for the moment. On the downside, decisive break of 1.0722 will argue that whole rise from 1.0447 has completed. Deeper fall would then be seen to target this low. On the upside, break of 1.0896 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

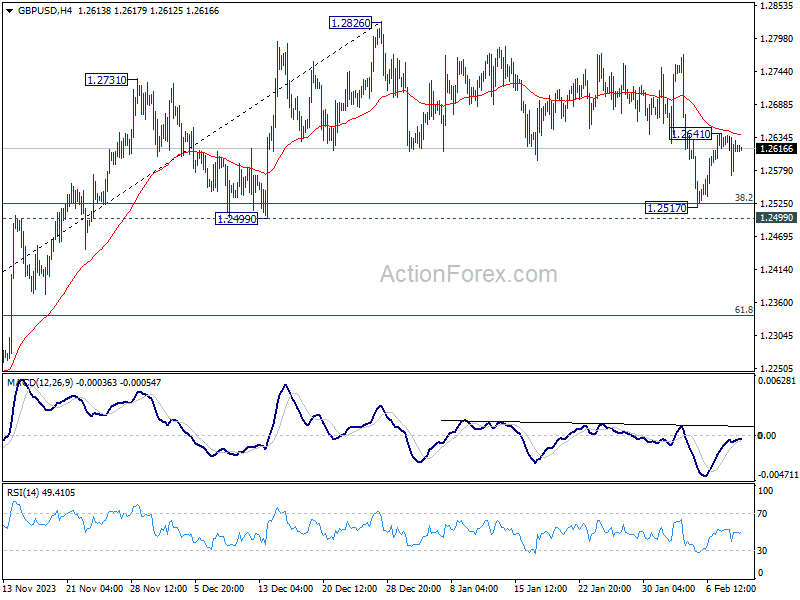

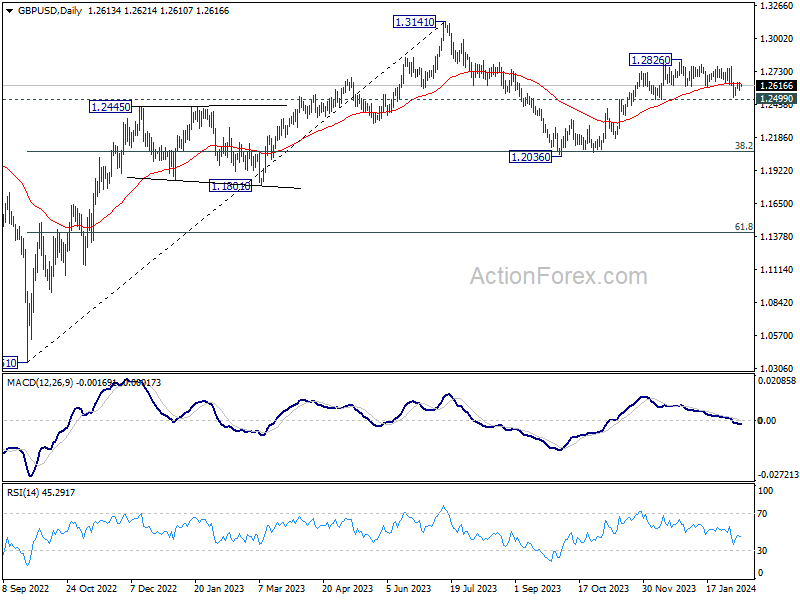

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2580; (P) 1.2609; (R1) 1.2647; More...

Intraday bias in GBP/USD remains neutral for the moment. On the upside, above 1.2641 will resume the rebound from 1.2517 to retest 1.2826 high. On the downside, however, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's still in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

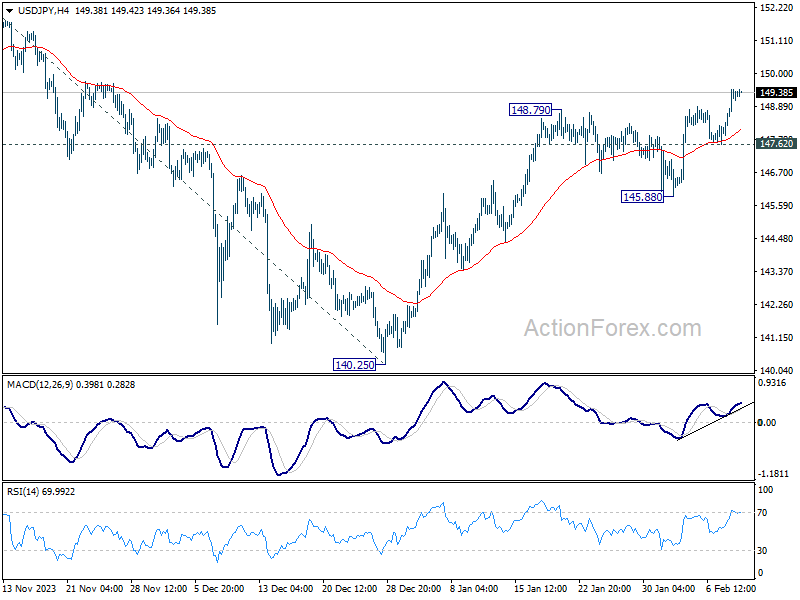

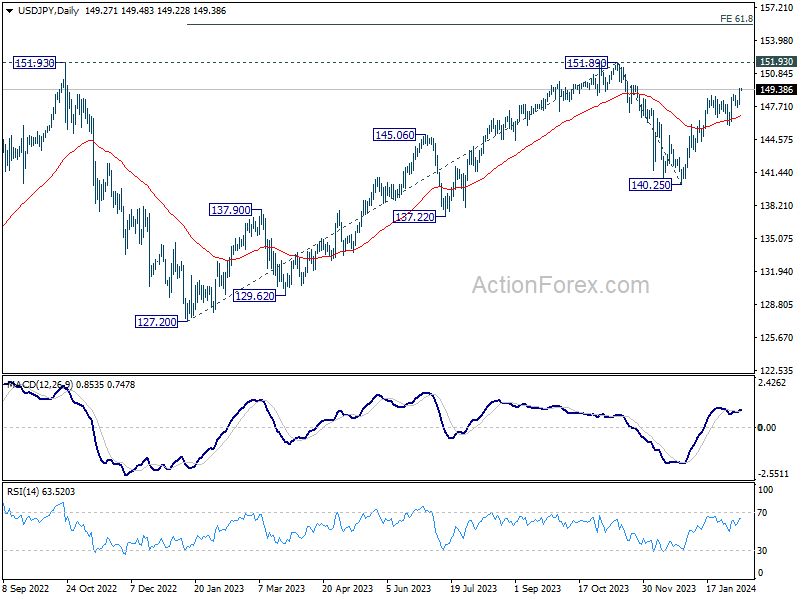

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.35; (P) 148.91; (R1) 149.89; More...

Intraday bias in USD/JPY remains on the upside for the moment. Current rise from 140.25 is in progress for retesting 151.89/93 key resistance zone. Decisive break there will confirm resumption of larger up trend. On the downside, below 147.62 minor support will turn intraday bias neutral first. But near term outlook will remain cautiously bullish as long as 145.88 support holds.

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption, and next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.

Cliff Notes: Confidence on Inflation a Matter of Time and Cconsideration

Key insights from the week that was.

At its first meeting of the year, the RBA Board decided to leave the cash rate unchanged at 4.35%. Since its last meeting in December, the key development was an encouraging quarterly update on inflation, the annual rate moderating from 5.4%yr in Q3 to 4.1%yr in Q4. Mirroring this progress, the tone of the Board’s decision statement shifted on the inflation outlook, “Whether further tightening of monetary policy is required…” was replaced with “… a further increase in interest rates cannot be ruled out.”

That said, the Board still characterised inflation as high and the level of demand too strong for supply, even though growth “remains subdued”. The simultaneous release of the Statement on Monetary Policy confirmed the RBA expects inflation to only move into the 2-3% target band in 2025 and be near the mid-point by June 2026.

As discussed by Chief Economist Luci Ellis in a video update mid-week, the RBA Board are not “ruling anything in or out” for now as they seek assurance on inflation’s sustainable return to target. Additional reads on the pace of disinflation and the health of the economy need to be received and evaluated before policy’s appropriateness is reassessed. Consistent with our revised inflation forecasts, we suspect that level of comfort will be achieved by September 2024. At that time, headline inflation is expected to be around the top of the target range on both a headline and trimmed mean basis.

The RBA Board are also wary of downside risks to domestic demand, something that was clearly on display in the September National Accounts and, more recently, Q4’s soft real retail sales result. The first half of this year will be challenging for the broader economy, but particularly households as the trifecta of high inflation, restrictive interest rates and a rising tax take weigh on real disposable incomes and discretionary spending.

Before moving offshore, a quick note on trade. Australia’s goods trade balance pared back slightly at year-end, from $11.8bn in November to a still-elevated $11.0bn in December. Taking the last few months together, the goods trade balance looks to have improved from $23.5bn in Q3 to $30.6bn in Q4. An increase in the terms of trade was the chief driver behind the improvement. Note, the services detail will only be available upon the release of the quarterly Balance of Payments, due March 5.

In the US, the ISM non-manufacturing survey saw a 2.9pt rise to 53.4pts supported by employment, prices and new orders. Relative to long-run averages, employment remains sub-par but prices are outperforming. These results encapsulate the risks present for the FOMC vis a vis activity and inflation.

FOMC members post-meeting return to market headlines reaffirmed Chair Powell’s key points from last week’s press conference – progress to date with inflation has been encouraging, but the strength of the economy provides time to make sure inflation risks do not linger. The flow of incoming data and the financial and credit conditions the economy face will also continue to be closely scrutinised, particularly given continued uncertainty over the health of commercial and multi-family property. On credit conditions, the latest Senior Loan Officer Opinion Survey confirms credit standards have tightened further in recent months while financial conditions were broadly unchanged.

Though, arguably of greatest significance in 2024 to the timing and pace of US policy easing will be momentum in the labour market. As detailed in our recent video, hours worked, household survey employment and the various business surveys all give cause to be wary about ongoing momentum. Indeed, the business surveys point to an outright decline in employment. We do not anticipate an abrupt decline, but rather a slowing of employment growth to a negligible pace. That would see slack build in the labour market and consumption slow to a sub-trend pace. These are conditions which warrant a timely moderate cutting cycle. We now expect the first cut by the FOMC in June, to be followed by July and September. From December, one cut per quarter is expected out to end-2025.

The pace and scale of FOMC rate cuts is largely expected to be mirrored by the ECB and Bank of England, and so we expect growth differentials and political uncertainty to act as the swing variables for FX markets over the forecast period. Both factors are likely to weigh on the US dollar, bringing it from well above long-run average levels to broadly in line by end-2025. Our just released February 2024 Westpac Market Outlook provides the full detail of our views on Australia, the world and financial markets.

Finally to China. In January, headline CPI inflation surprised, declining to –0.8%yr as food prices fell 5.9%yr. Excluding food, CPI inflation was up 0.4%yr and is seemingly finding its floor. Services inflation is supporting this process, rising 0.5%yr. Producer price inflation meanwhile remains very weak, -2.5%yr in Jan from -2.7%yr in December. These outcomes are a combination of soft demand and excess capacity which continues to be increased as Chinese firms build scale to compete against imports in their domestic market and expand their export footprint.

Large and targeted support for the property sector is needed to boost demand directly and via confidence. Further measures are also warranted to steady then strengthen equity markets. This week brought both action and rumours of further action on this front, but it won’t be until after the Lunar New Year holidays that we will find out its scale and effectiveness. Even when confidence and discretionary spending appetite returns, it is unlikely that consumer inflation will surge higher. China’s continued expansion of its capacity and focus on efficiency and productivity are laying the foundation for a lengthy period of disinflation for goods.

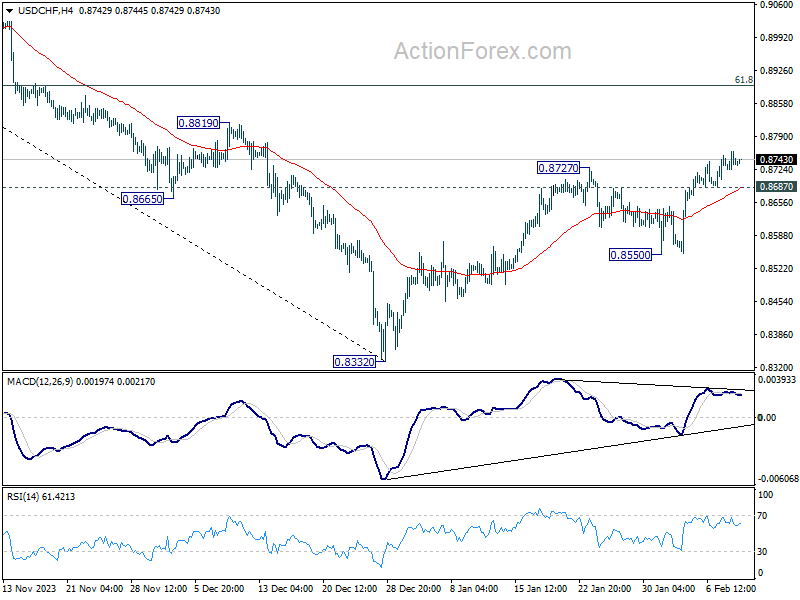

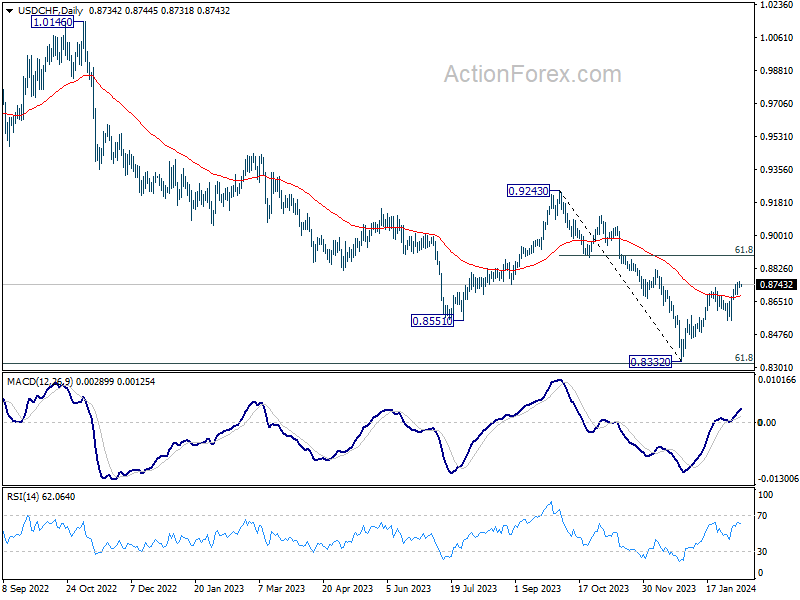

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8721; (P) 0.8741; (R1) 0.8757; More....

USD/CHF's rally is in progress despite some loss of upside momentum. Intraday bias stays on the upside. Current rise from 0.8332 would target 61.8% retracement of 0.9243 to 0.8332 at 0.8995 next. On the downside, below 0.8687 minor support will turn intraday bias neutral first. But near term outlook will stay cautiously bullish as long as 0.8550 support holds.

In the bigger picture, there is prospect of medium term bottoming at 0.8332 considering possible bullish convergence condition in W MACD, and the support from 0.8317 long term fibonacci support. Sustained trading above 55 D EMA (now at 0.8677) will affirm this case, and bring stronger rise back towards 0.9243 resistance, even as a corrective move.

Franc and Yen Underperform, Canadian Dollar Anticipates Jobs Report

Swiss Franc and Japanese Yen are currently the weakest performers for the week on a couple of interrelated factors. Firstly, global central bankers are tempering expectations for early rate cuts, suggesting rate difference between SNB/BoJ and other central banks would remain large for longer.

This stance has been further compounded by a significant rebound in benchmark treasury yields and a prevailing risk-on sentiment in US and Japan, impacting these traditionally safe-haven currencies.

S&P 500 reached new record high above 5000 handle overnight, driven by optimism regarding the resilience of US economy. Meanwhile, Nikkei achieved fresh 34-year highs in Asian session, following assurances from BoJ Governor Kazuo Ueda about continuation of easy monetary conditions, even in the after exit of negative interest rate policy.

Conversely, New Zealand Dollar stands out as the strongest currency this week, demonstrating resilience against the robust Dollar. It has been additionally buoyed by significant buying interest against Australian Dollar, which has found little support from hawkish comments by RBA Governor Michele Bullock.

Canadian Dollar follows closely as the second strongest, with the market's attention now turning to Canada's employment data. Meanwhile, Dollar maintains its position as the third strongest, as it continues to consolidate recent gains, with Euro and Sterling displaying mixed performance.

From a technical standpoint, CAD/JPY is currently in the spotlight, eyeing 111.14 key resistance level following yesterday's upside breakout. Decisive break there will confirm resumption of whole up trend from 94.04 and target 61.8% projection of 94.04 to 111.14 from 104.19 at 114.75 in short-to-medium term. For now, outlook will stay bullish as long as 108.80 support holds, in case of retreat. Today's Canadian employment data could potentially catalyze the anticipated break.

In Asia, Nikkei closed up 0.31%. Hong Kong HSI is down -0.83%. Singapore Strait Times is down -0.15%. China is on holiday. Japan 10-year JGB yield rose 0.0194 to 0.719. Overnight, DOW rose 0.13%. S&P 500 rose 0.06%. NASDAQ rose 0.24%. 10-year yield rose 0.060 to 4.170.

Fed's Collins anticipates 75bps in rate cuts this year as baseline

In an interview overnight, Boston Fed President Susan Collins described her "baseline" expectation for rate path as being "similar" to Fed's latest projection, which anticipates a total of 75 basis points cut in interest rates within the year.

She highlighted the importance of additional data to support the decision for the timing of the first rate cut. "I will need more, additional evidence" to confirm that inflation is consistently trending towards Fed's 2% goal, she stated.

Nevertheless, Collins noted that waiting for inflation to reach the target before acting "would be waiting too long," suggesting a proactive yet measured stance in adjusting policy.

ECB's Lane anticipates March projections for comprehensive update

ECB Chief Economist Philip Lane highlighted in a speech that recent data suggest the disinflation process "may run faster than previously expected" in the near term. However, he was quick to note that the implications for medium-term inflation remain "less clear".

The economic recovery's strength, fiscal policy paths, wage developments, firms' capacity to absorb higher input costs, and ongoing geopolitical tensions are all pivotal factors that Lane identified as having an "important bearing" on the inflation trajectory.

Lane also emphasized the significance of March 2024 ECB staff macroeconomic projections as a critical juncture for providing a "comprehensive update" of medium-term inflation outlook.

In terms of policy approach, Lane reaffirmed ECB's commitment to a "firmly data-dependent approach," stressing the importance of striking a delicate balance between the risks of overtightening and prematurely easing monetary policy.

"Monetary policy needs to carefully balance the risk of overtightening by keeping rates too high for too long against the risk of prematurely moving away from the hold-steady position," he stated.

Furthermore, Lane stressed the importance being "further along in the disinflation process" before gaining confidence that inflation will consistently meet ECB's target in a timely and sustainable manner.

BoE's Mann skeptical of continuing decline in UK inflation

BoE MPC member Catherine Mann expressed skepticism about the continuation of the recent deceleration in headline inflation, challenging the prevailing market sentiment anticipating imminent rate cuts by the central bank. "I am not convinced that the near-term deceleration in headline inflation will continue," Mann stated.

As financial markets are expecting rate reductions from the current 5.25%, her concern is that financial conditions have "eased too much already," complicating BoE's efforts to anchor inflation expectations and stabilize price growth.

Mann also highlighted "upside risks" to inflation stemming from geopolitical tensions in the Red Sea, noting that increased shipping and insurance costs could exacerbate the UK's inflation challenges. "

Against a backdrop of sluggish supply growth and possible upside shocks, I see risks of continued inflation momentum and embedded persistence," she remarked.

Comparing UK's inflation dynamics with its international peers, Mann expressed reservations about the optimistic view that the UK is merely trailing slightly behind in its efforts to return inflation to target. "A look at the data suggests to me that the 'bit later' might be quite a while later," she cautioned.

In the latest MPC meeting, Mann, alongside fellow external member Jonathan Haskel, stood out for advocating an additional interest rate hike. Mann described her decision as "finely balanced," attributing her stance to UK's slower progress in reducing inflation compared to US and Eurozone.

RBA's Bullock: Another hike neither ruled out nor ruled in

In an appearance before a parliamentary economics committee in Canberra today, RBA Governor Michele Bullock acknowledged the presence of "some encouraging signs" in Australia's economic landscape, yet cautioned that the nation's battle against inflation is "not over".

RBA's stance remains deliberately balanced, with Bullock stating, "At this stage, the Board hasn't ruled out a further increase in interest rates but neither has it ruled it in." Interest rate path will "depend upon the data and the evolving assessment of risks".

Bullock further elaborated on the dynamics of demand and supply within the Australian economy, indicating that demand levels continue to outstrip the economy's supply capacity. This imbalance, coupled with persistently tight labor market conditions, suggests that while the observed slowdown in demand is contributing to a moderation of inflationary pressures, the desired equilibrium has yet to be reached.

Goods price inflation has shown a softer trend than anticipated, mirroring patterns observed in international markets, Bullock noted. However, services price inflation remains elevated, driven by significant increases in both labor and non-labor input costs.

"Indeed, while inflation was lower than we were expecting in November, this is largely attributable to softer-than-expected goods inflation – services inflation was pretty much where we had forecast it to be."

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8721; (P) 0.8741; (R1) 0.8757; More....

USD/CHF's rally is in progress despite some loss of upside momentum. Intraday bias stays on the upside. Current rise from 0.8332 would target 61.8% retracement of 0.9243 to 0.8332 at 0.8995 next. On the downside, below 0.8687 minor support will turn intraday bias neutral first. But near term outlook will stay cautiously bullish as long as 0.8550 support holds.

In the bigger picture, there is prospect of medium term bottoming at 0.8332 considering possible bullish convergence condition in W MACD, and the support from 0.8317 long term fibonacci support. Sustained trading above 55 D EMA (now at 0.8677) will affirm this case, and bring stronger rise back towards 0.9243 resistance, even as a corrective move.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Jan | 2.40% | 2.20% | 2.30% | |

| 07:00 | EUR | Germany CPI M/M Jan F | 0.20% | 0.20% | ||

| 07:00 | EUR | Germany CPI Y/Y Jan F | 2.90% | 2.90% | ||

| 09:00 | EUR | Italy Industrial Output M/M Dec | 0.50% | -1.50% | ||

| 13:30 | CAD | Net Change in Employment Jan | 15.0K | 0.1K | ||

| 13:30 | CAD | Unemployment Rate Jan | 5.90% | 5.80% |

RBA’s Bullock: Another hike neither ruled out nor ruled in

In an appearance before a parliamentary economics committee in Canberra today, RBA Governor Michele Bullock acknowledged the presence of "some encouraging signs" in Australia's economic landscape, yet cautioned that the nation's battle against inflation is "not over".

RBA's stance remains deliberately balanced, with Bullock stating, "At this stage, the Board hasn't ruled out a further increase in interest rates but neither has it ruled it in." Interest rate path will "depend upon the data and the evolving assessment of risks".

Bullock further elaborated on the dynamics of demand and supply within the Australian economy, indicating that demand levels continue to outstrip the economy's supply capacity. This imbalance, coupled with persistently tight labor market conditions, suggests that while the observed slowdown in demand is contributing to a moderation of inflationary pressures, the desired equilibrium has yet to be reached.

Goods price inflation has shown a softer trend than anticipated, mirroring patterns observed in international markets, Bullock noted. However, services price inflation remains elevated, driven by significant increases in both labor and non-labor input costs.

"Indeed, while inflation was lower than we were expecting in November, this is largely attributable to softer-than-expected goods inflation – services inflation was pretty much where we had forecast it to be."

BoE’s Mann skeptical of continuing decline in UK inflation

BoE MPC member Catherine Mann expressed skepticism about the continuation of the recent deceleration in headline inflation, challenging the prevailing market sentiment anticipating imminent rate cuts by the central bank. "I am not convinced that the near-term deceleration in headline inflation will continue," Mann stated.

As financial markets are expecting rate reductions from the current 5.25%, her concern is that financial conditions have "eased too much already," complicating BoE's efforts to anchor inflation expectations and stabilize price growth.

Mann also highlighted "upside risks" to inflation stemming from geopolitical tensions in the Red Sea, noting that increased shipping and insurance costs could exacerbate the UK's inflation challenges. "

Against a backdrop of sluggish supply growth and possible upside shocks, I see risks of continued inflation momentum and embedded persistence," she remarked.

Comparing UK's inflation dynamics with its international peers, Mann expressed reservations about the optimistic view that the UK is merely trailing slightly behind in its efforts to return inflation to target. "A look at the data suggests to me that the 'bit later' might be quite a while later," she cautioned.

In the latest MPC meeting, Mann, alongside fellow external member Jonathan Haskel, stood out for advocating an additional interest rate hike. Mann described her decision as "finely balanced," attributing her stance to UK's slower progress in reducing inflation compared to US and Eurozone.