Sample Category Title

ECB’s Wunsch sees some value to waiting

ECB Governing Council member Pierre Wunsch said today, "I'm on the side of those that believe there's some value to waiting" before cutting interest rates.

Nevertheless, Wunsch also acknowledged the inherent uncertainties in economic forecasting and the eventual need to make decisions based on the best available data. "But again, we won't get full comfort. So at some point, we'll have to look at all the information we have and take a bet," he said.

A critical factor in Wunsch's cautious stance is the current state of wage growth within Eurozone. He pointed out that wage increases are occurring at a pace that may undermine ECB's efforts to bring inflation down to 2% inflation target. Were it not for the uptick in salaries, ECB might already be in a position to initiate monetary easing.

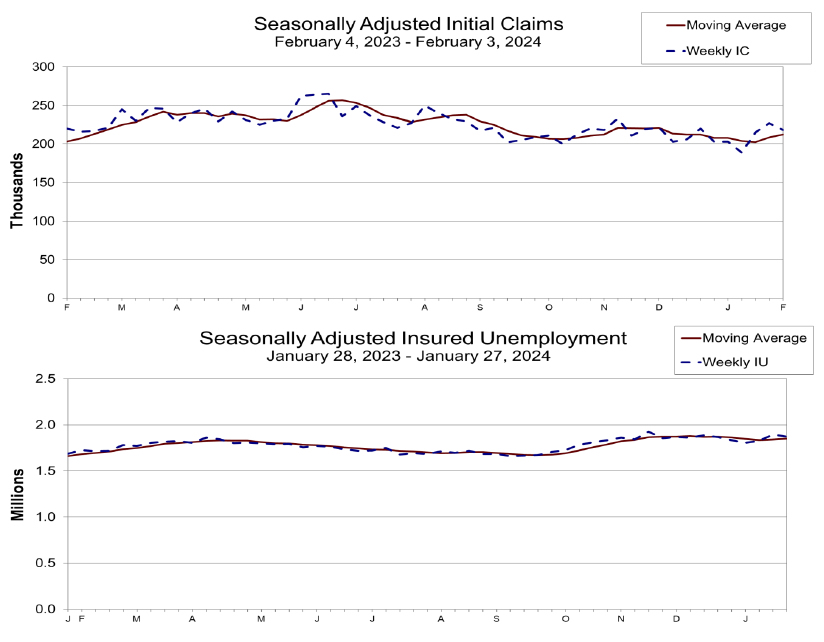

US initial jobless claims falls to 218k, vs exp 220k

US initial jobless claims fell -9k to 218k in the week ending February 3, slightly better than expectation of 220k. Four-week moving average of continuing claims rose 4k to 212k.

Continuing claims fell -23k to 1871k in the week ending January 27. Four-week moving average of continuing claims rose 9.5k to 1850k.

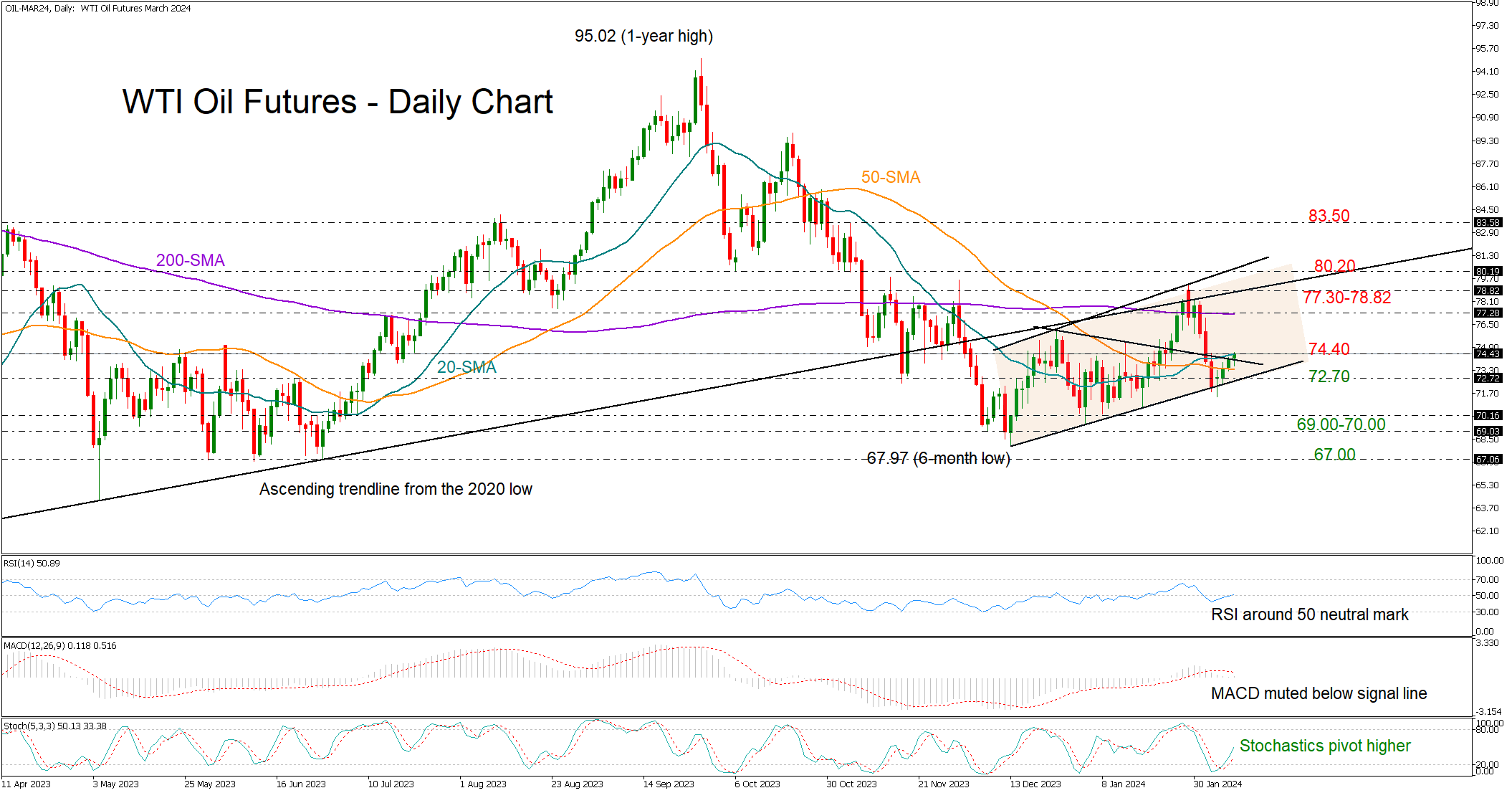

WTI Oil Futures Need One More Confirmation

- WTI oil aims for some recovery but lacks confidence

- Price fluctuates within a bullish channel

- Resistance at 74.40; support at 72.70

WTI oil futures have been tip-toeing higher after last week’s steep downfall paused at the lower boundary of a short-term bullish channel. The price posted a doji green candlestick on Monday with scope to change direction higher, but gains have been limited so far, and currently constrained below the 20-day simple moving average (SMA) at 74.40.

The technical indicators cannot embrace the latest upturn in the price either. Although the stochastic oscillator has resumed its positive slope, the RSI has yet to cross above its 50 neutral mark, while the MACD hasn't shown signs of improvement, remaining below its red signal line and close to zero.

Should the bulls pierce through the 74.40 area, the 200-day SMA and the long-term ascending trendline could cap upside movements within the 77.30-78.82 region, preventing a test at the upper band of the bullish channel at 80.20. If the price strengthens its uptrend above the channel, resistance could next develop near the 83.50 barrier.

Alternatively, a pullback below the 20-day SMA could re-examine the channel’s lower band around 72.70. A break beneath that threshold could initially stabilize somewhere between 70.00 and 69.00 and then extend towards the 67.00 constraining zone taken from May-June 2023.

Summing up, WTI oil futures cannot promise additional gains in the coming sessions, despite the latest increase in the price. A clear close above 74.00 could stimulate bullish forces, though only a new higher high above 80.00 would upgrade the bullish short-term outook.

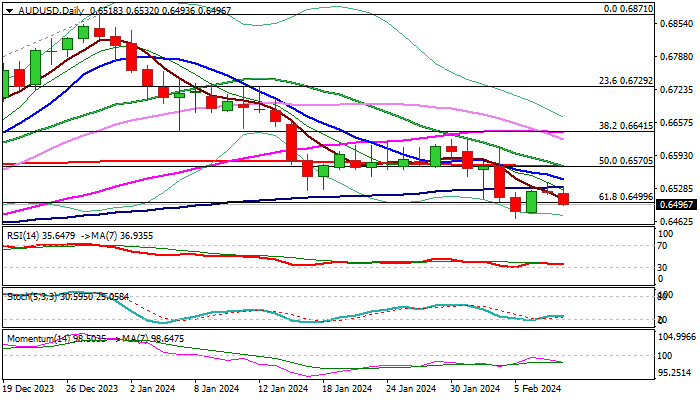

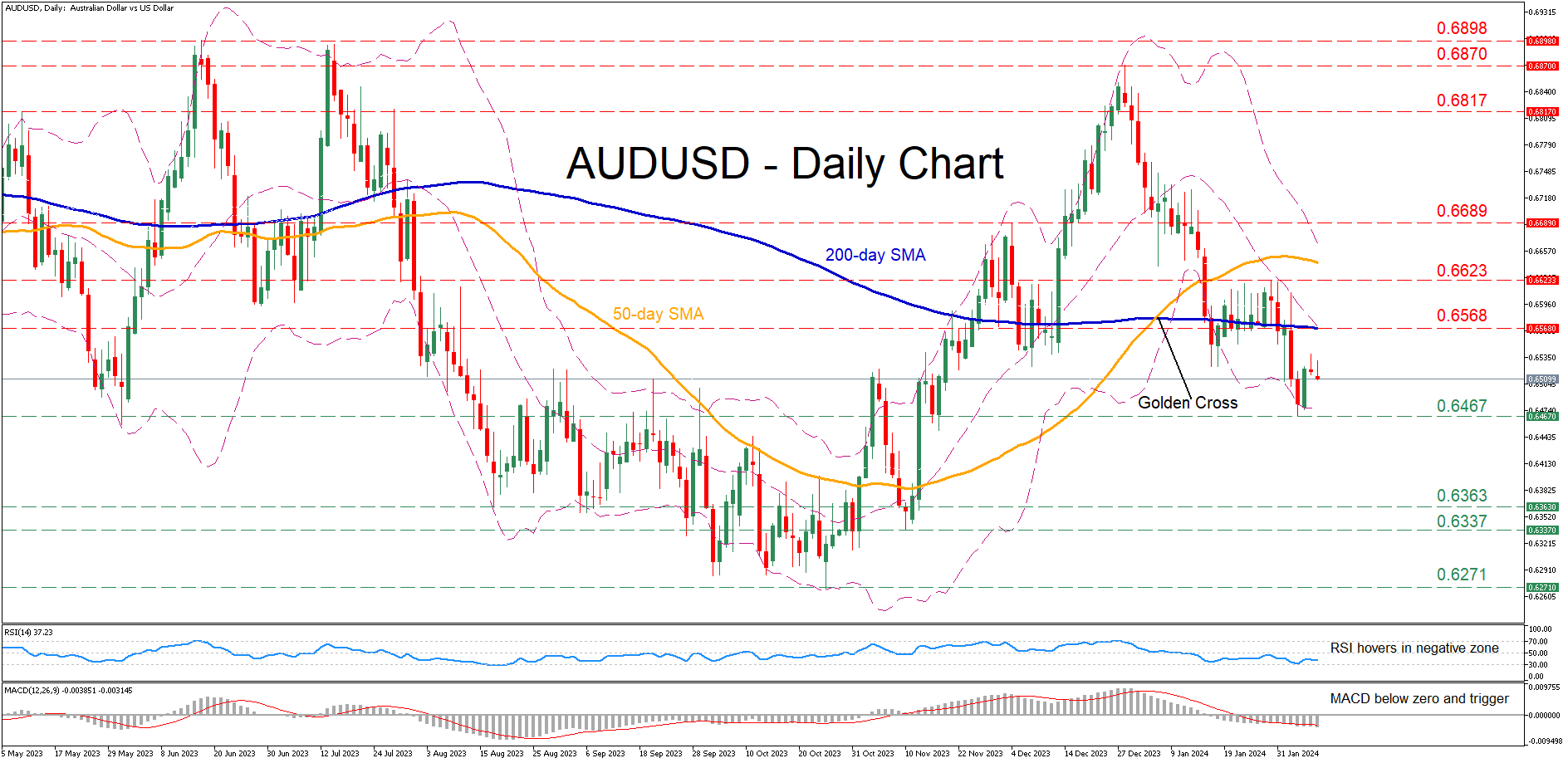

AUD/USD Outlook: Dips After Soft China CPI Data

AUDUSD eased below 0.6500 mark (cracked Fibo 61.8% of 0.6270/0.6871 rally) on Thursday, deflated by softer than expected China inflation data.

Fresh weakness emerged after recovery attempts from 0.6468 (new 2024 low, posted on Feb 5) were repeatedly capped by 100DMA (0.6530), keeping the larger bearish technical picture intact.

Daily moving averages remain in full bearish setup, with a double death-cross (10/200 and 20/200DMA’s) adding pressure, along with rising negative momentum.

Bears look for initial signal on daily close below 0.6500 to attack 0.6468 pivot, loss of which would open way for extension towards targets at 0.6411 (Fibo 76.4%) and 0.6338 (Nov 10 low).

Near-term bias to remain with bears as long as 100DMA caps, while break higher would ease bearish pressure and expose the upper pivot at 0.6571 (200DMA / base of thick daily Ichimoku cloud).

Res: 0.6530; 0.6571; 0.6600; 0.6624.

Sup: 0.6468; 0.6411; 0.6351; 0.6338.

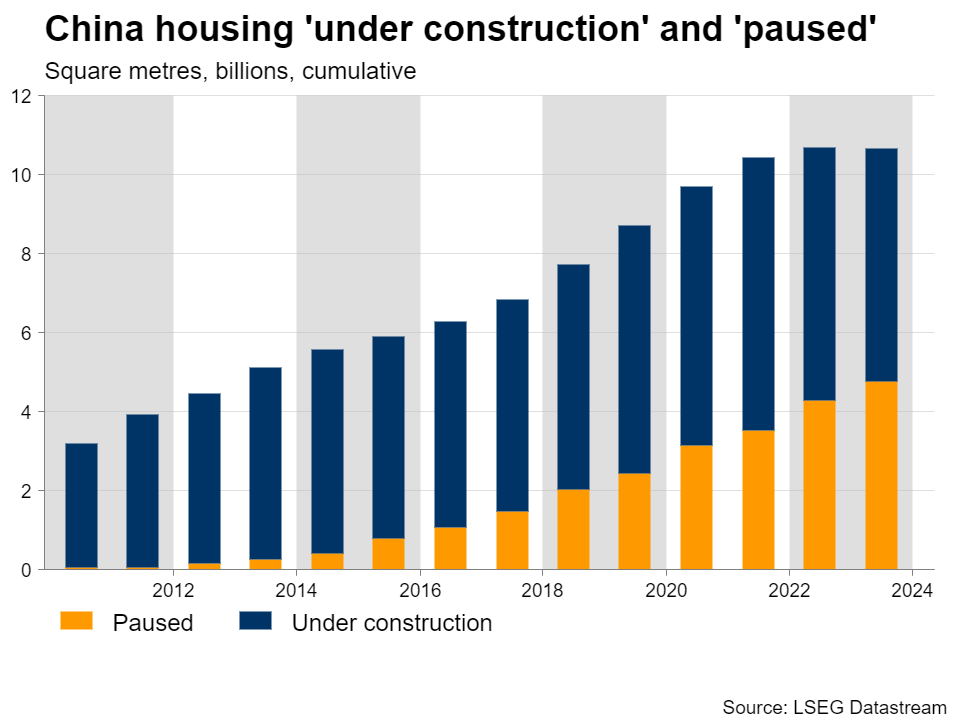

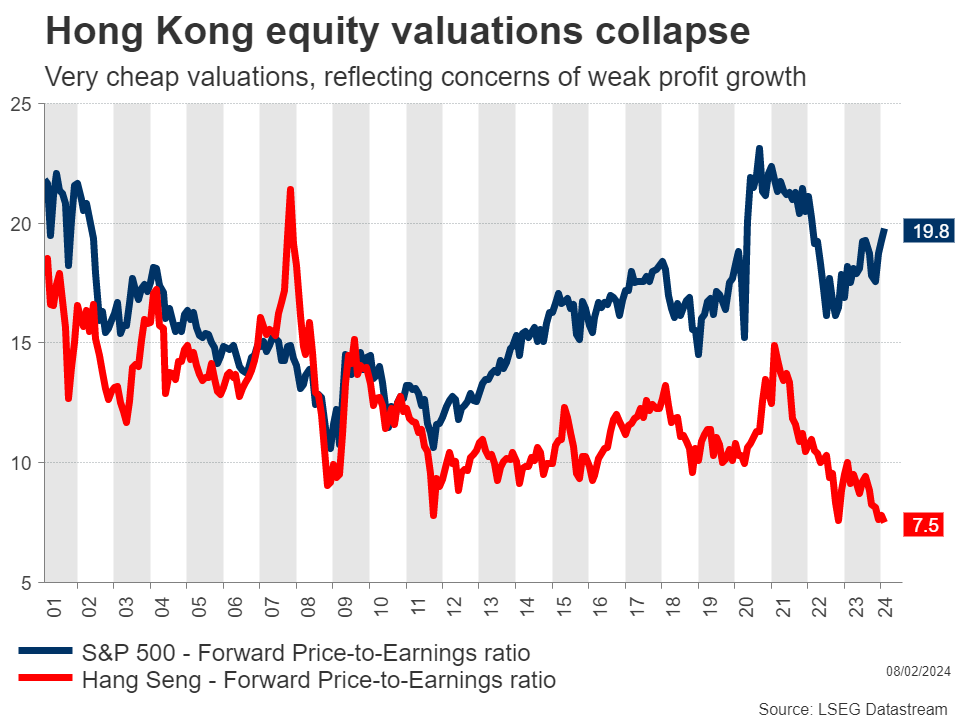

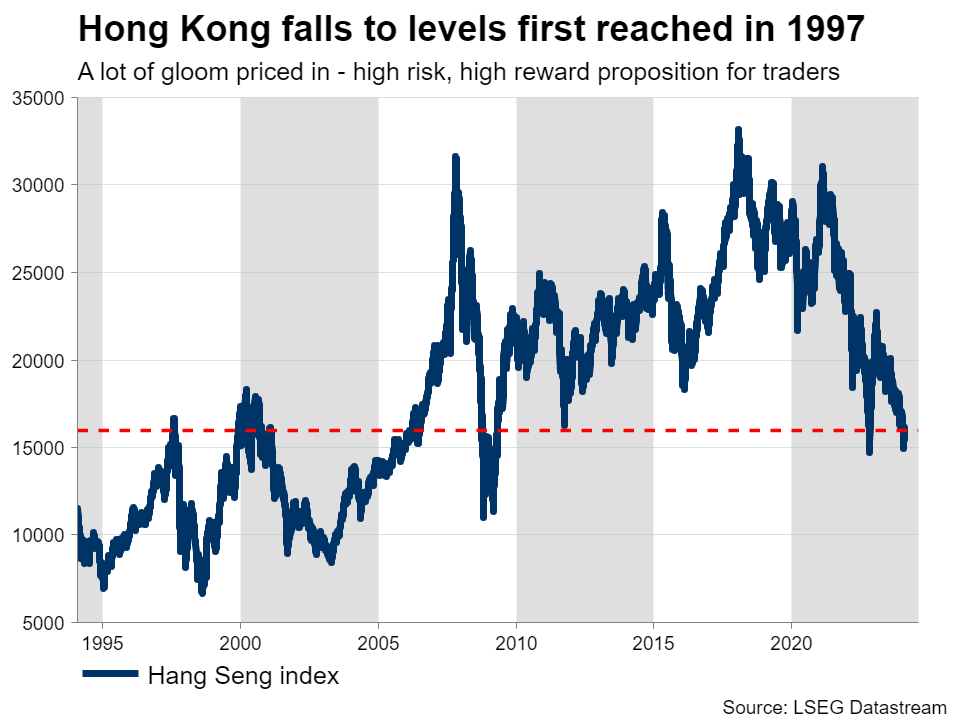

Why Are Chinese Stocks Melting Down?

- Chinese stock markets sink to lowest levels in five years

- Real estate crisis and other problems haunt investors

- Valuations are cheap, but more is needed for lasting recovery

Chinese equities implode

It’s been a tough few years for Chinese stock markets. Shares in mainland China have fallen to their lowest levels since 2019 as investors continue to liquidate their positions, despite a series of stimulus measures by Beijing that were meant to stop the bleeding.

An ongoing crisis in the property sector, a slowdown in global manufacturing, and high youth unemployment have joined forces to hamstring growth, pushing the Chinese economy into deflation. Deteriorating trade relations with the United States have made matters worse, fueling concerns that China is headed for a ‘lost decade’.

In the past, the solution to similar problems was to stimulate the economy, by encouraging local governments and businesses to take on debt and invest in infrastructure projects. Alas, the same trick won’t work this time, as the property sector is already dealing with the toxic aftermath of decades of malinvestment and overinvestment.

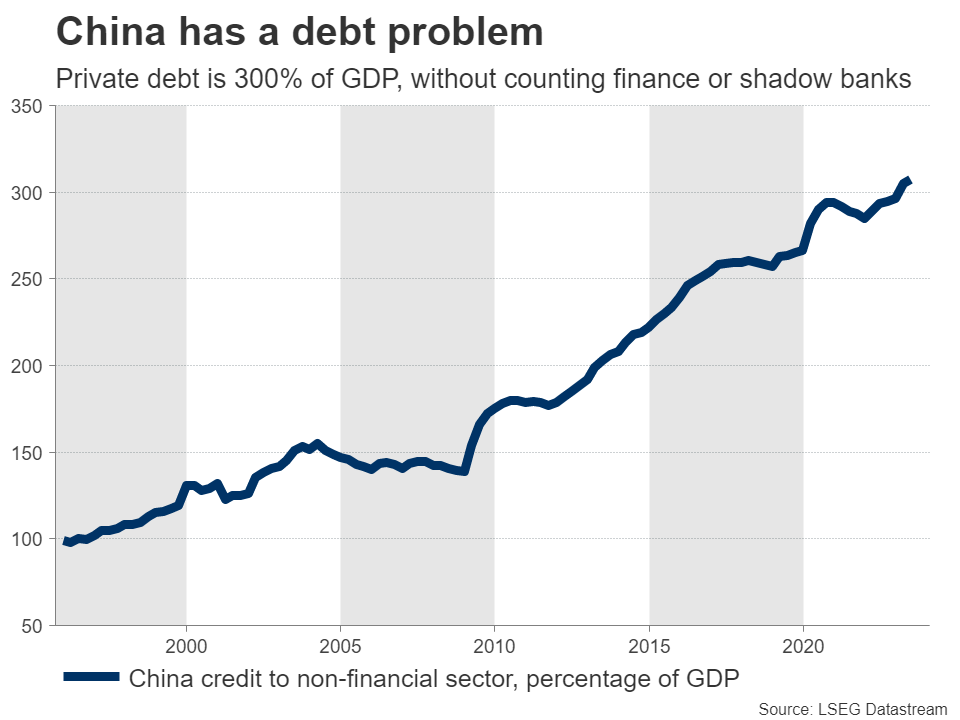

Another issue is that the scope for stimulus measures is limited. Debt in the private sector has skyrocketed to reach 300% of GDP, and that’s without even counting debts of financial institutions or shadow banks. Chinese authorities want to avoid a further increase in debt levels, as that could destabilize the financial system and lead to a deeper crisis.

For similar reasons, the central bank has not slashed interest rates in a meaningful way.

So far, measures have not been enough

Unable to flood the economy with debt-fueled stimulus, Beijing has taken a more cautious approach, announcing a series of piecemeal measures that appear insufficient to turn the tide.

The latest steps include a reduction in the cash that banks must hold in reserve. This is estimated to free up 1 trillion yuan that can be used for lending, which equals nearly 140 billion dollars. In tandem, the government said it will expand access to loans for struggling property developers, to restore confidence in a sector mired in bankruptcy.

But for the most part, authorities have focused on lifting the stock market. Strict restrictions on short selling have been introduced and recent reports suggest Beijing will deploy about 2 trillion yuan to purchase stocks directly.

Sadly, this rescue package probably lacks the firepower and scope to make a true impact on an economy haunted by plunging investment and depressed consumer sentiment. Throwing money at the stock market could temporarily calm investors, but a lasting recovery will require a turnaround in the real economy.

Valuations are cheap

With stock markets getting hammered, valuations have collapsed. For instance, shares listed in Hong Kong are currently trading for only 7.5 times what analysts expect earnings to be over the next year, which is their cheapest valuation in at least two decades. That’s almost three times as cheap as US equities.

These businesses are not heading for bankruptcy. The biggest among them include Alibaba and Tencent, both of which are highly profitable and regularly return cash to shareholders via dividends and buybacks.

Of course, there’s a reason why valuations are so cheap. Weak prospects for future profit growth, sudden regulatory crackdowns, and a general lack of investor protection have eroded confidence in Chinese assets. It’s going to take more than cheap valuations to solve that.

There are several other threats too. Another trade war could ensue if Trump is elected US president in November, as he has already promised new tariffs against China. Not to mention the risk that Beijing might let the yuan depreciate if the economy worsens.

The bottom line

Bearing all this in mind, the outlook for Chinese assets is not very bright. The housing sector will probably need several years to recover, judging by other countries that saw similar property collapses, such as Japan in the 1990s and the United States after 2008. That could restrict growth, especially in the absence of ‘bazooka-style’ stimulus.

That said, much of this pessimism is already reflected in depressed valuations. With so much gloom priced into Chinese equities, any piece of good news could have a disproportionately large impact. Therefore, Chinese markets offer a high-risk, high-reward proposition for traders.

The middle ground would be to focus on quality businesses. Companies such as Tencent are still growing earnings at a rapid pace, yet their share price has been slammed lower with the rest of the market and their valuations are as cheap as they have ever been.

In other words, shares of quality companies have suffered collateral damage, which might present an opportunity for brave investors. Ultimately though, the road to a sustained stock market recovery will be long and will almost certainly require more forceful steps from Chinese authorities.

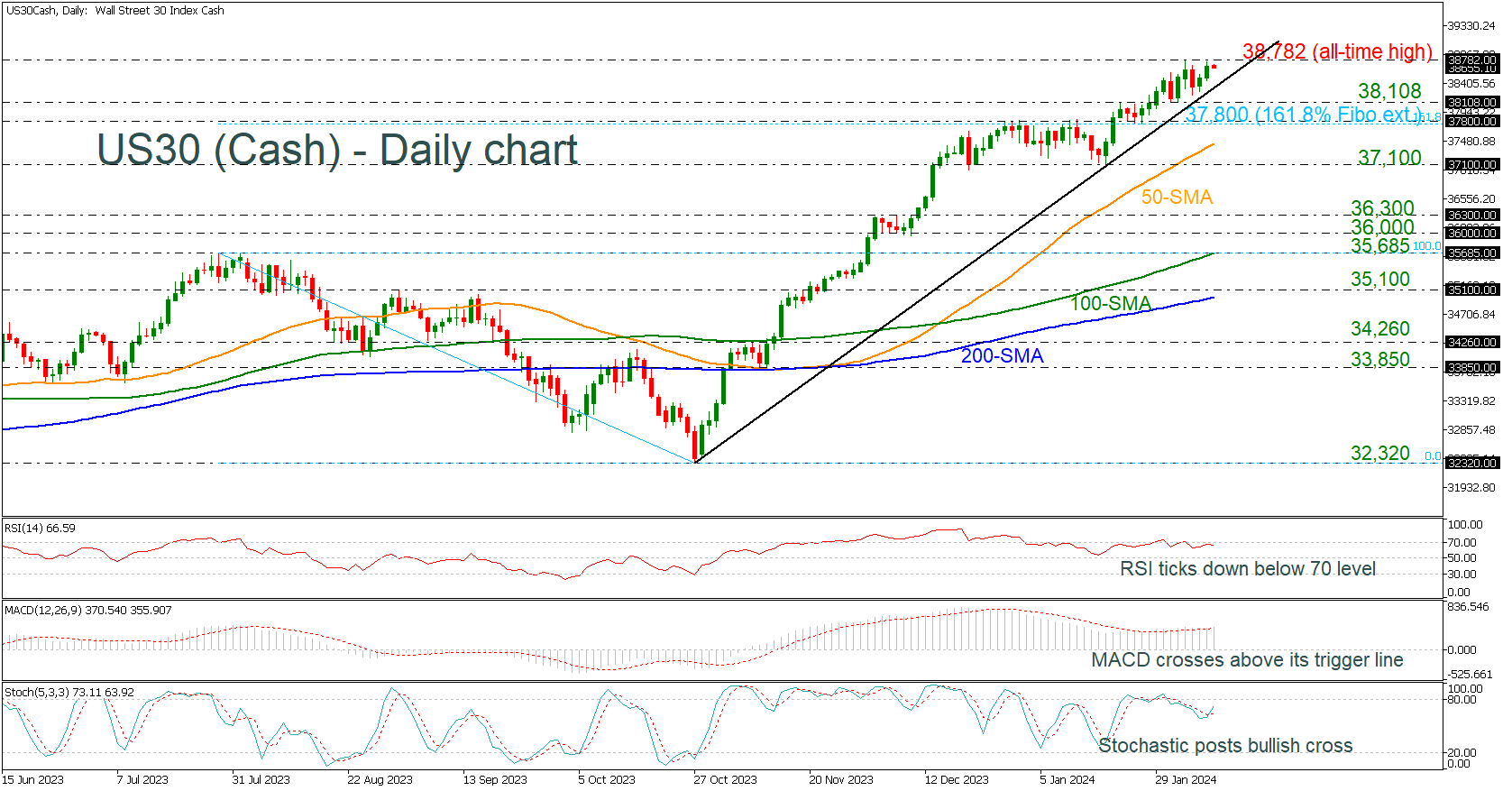

US 30 Index Flirts With All-Time High

- US 30 index retains bullish outlook above uptrend line

- Technical oscillators indicate more gains

The US 30 (cash) index is traveling slightly below the all-time high of 38,782 and above the medium-term rising trend line, suggesting a potential move to the upside again.

Given the current positive momentum, the question now is whether the index will stay resilient above the 38,108 key region. A clear step below it and beneath the uptrend line as well as the 161.8% Fibonacci extension level of the down leg from 35,685 to 32,230 at 37,800 would wipe out yesterday’s boost, pressing the price towards the 50-day simple moving average (SMA) at 37,447. Slightly lower, the 37,100 support could come next ahead of 36,300.

Technically, the short-term risk is leaning to the upside. The MACD crossed its trigger line to the upside in the bullish area, while the RSI is holding near the 70 level. Also, the stochastic oscillator posted a bullish crossover within its %K and %D lines, approaching the overbought zone.

On the other hand, traders will wait for a close above the previous high of 38,782 to upgrade the price’s outlook. Then, the next battle could take place somewhere near the 40,000 psychological number.

To sum up, the latest bullish move in the US 30 index has not excited traders yet. An extension above the record high of 38,782 is still required to make the upturn look more credible.

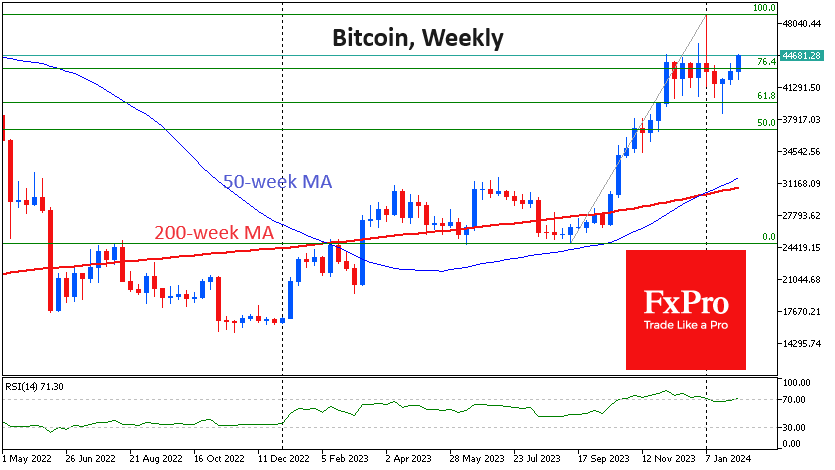

Bitcoin Completes Consolidation and Rushes to the High

Market Picture

The crypto market made an impressive move higher, rising 3.4% in 24 hours to $1.71 trillion. The rise to its highest level since 12 January came as the S&P500 and Nasdaq-100 indices hit all-time highs.

Bitcoin rose above its 50-day moving average, confirming the bullish medium-term trend and easing fears of a deeper correction. On a weekly basis, bitcoin is now above its December-January closing levels, although intra-week volatility briefly pushed the price higher earlier in the year. However, weekly closes are the more important benchmark for the markets.

Technically, bitcoin and the broader crypto market have gained strength after a long period of consolidation and are now poised to make new highs. The Fibonacci pattern is almost perfect: the rally from $25K to $49K ended with a 61.8% retracement of the initial move. Theoretically, a break of the highs at $49K would confirm the pattern and make $64K (161.8%) a target.

News Background

MicroStrategy bought an additional 850 BTC worth $37.2 million in January, bringing its reserves in the first cryptocurrency to 190,000 BTC (around $8.5 billion) at an average price of $31,224.

According to CoinLedger, the average realised gain for crypto investors in 2023 was $887.6, compared to a loss of $7,102 in the previous year.

The US SEC has delayed a decision on applications for spot Ethereum ETFs from Invesco and Galaxy. ‘The only date that matters for spot ETH ETFs at this point is 23 May. That’s the deadline for VanEck’s application’, notes Bloomberg.

Ethereum developers have successfully implemented the Dencun (Deneb-Cancun) update on the Holesky test network. It is expected to reduce commissions for L2 solutions based on roll-up technology by around ten times.

Thailand’s Ministry of Finance announced that crypto trading will be exempt from value-added tax. The agency aims to encourage the country’s transformation into a hub for digital assets and promote them as an alternative means of raising capital.

The CEO of South Korean cryptocurrency exchange Bitsonic, Jinwook Shin, was sentenced to seven years in prison for his involvement in a 10 billion won ($7.5 million) fraud scheme.

According to TheMinerMag, bitcoin mining by US miners fell to historic lows in January due to a 29-50% increase in electricity prices. High electricity costs are expected to continue until the end of the first quarter of 2024.

Australian Dollar Dips as China’s Inflation Declines

The Australian dollar has edged lower after China posted a soft inflation report. In the European session, AUD/USD is trading at 0.6509, down 0.18%.

The new year hasn’t brought much cheer to the Australian dollar, which hasn’t had a winning week in 2024. Earlier in the week, The Australian dollar dropped below the 0.65 line for the first time since mid-November. The slowdown in China, Australia’s largest export market, is weighing on the struggling Aussie.

China’s CPI falls to 14-year low

China’s consumer prices continued to slide and dropped in January by 0.8% y/y, the steepest decline since September 2009. This was lower than the market estimate of -0.5% and marked a fourth straight decline. The main driver of the downswing was lower food prices. Monthly, CPI rose 0.3%, up from 0.1% in December and below the market estimate of 0.4%. Producer prices fell by 2.5% y/y in January, the sharpest decline in four months.

The world’s second-largest economy is in a deflationary mode and there is the danger that deflation is becoming entrenched. Domestic consumption has weakened and confidence is falling, as evidenced by the massive drop in the Chinese stock market. Deflation was virtually unheard of prior to the Covid pandemic, but China’s shaky recovery has resulted in prolonged deflation.

The weak global economy has meant decreased demand for Chinese exports and this has hammered the manufacturing sector. Manufacturing activity contracted for a fourth straight month in January. The non-manufacturing PMI rose to 50.7 in January, up from 50.3, indicating stagnation.

China’s government has taken some steps to kick-start growth, such as slashing bank reserves and injecting those funds into the banking system, but more dramatic moves may be needed, such as lowering interest rates.

Reserve Bank of Australia Governor Bullock will testify before a House committee later today and traders will be looking for hints about the RBA’s future rate path. The RBA kept rates unchanged for a third time earlier this week and does not appear in any rush to lower rates.

AUD/USD Technical

- 0.6546 and 0.6590 are the next resistance lines

- 0.6468 and 0.6424 and providing support

AUDUSD Bounces Off 2024 Low

- AUDUSD hits its lowest level since mid-November

- Although decline halts, rebound looks unconvincing

- Momentum indicators remain tilted to the downside

AUDUSD has been in a constant decline after peaking at 0.6870 in December, breaking below both its 50- and 200-day simple moving averages (SMAs). This week, the price fell to a fresh two-month bottom of 0.6467 before recouping some losses, while the short-term oscillators still suggest that bearish forces are holding the upper hand.

Should bearish pressures persist, the price could revisit its 2024 bottom of 0.6467. A violation of that region could open the door for the August low of 0.6363. Sliding beneath that floor, the pair may descend towards the November low of 0.6337.

On the flipside, if the pair extends its near-term recovery, there is no prominent resistance until the 200-day SMA, currently at 0.6568. Further advances could then cease at the recent resistance of 0.6623 ahead of the 0.6689 hurdle. Conquering the latter, the bulls could attack the May peak of 0.6817.

Overall, AUDUSD dropped to its lowest level in two months as its short-term retreat shows no signs of easing. For the bearish sentiment to alter, the price needs to initially reclaim the 200-day SMA.

NZD/USD Rate Recovering from Its Low of the Year amid News from Labour Market

Yesterday's news showed that New Zealand's labour market is stronger and more resilient than expected.

In the fourth quarter of 2023, employment grew by 0.4% in the fourth quarter (forecast = +0.3%, quarter earlier = -0.1%). The unemployment rate is 4%, forecast = 4.3%.

A strong labour market indicates a margin of safety in the economy. And that may suggest that the Reserve Bank of New Zealand's tight monetary policy to quell inflation may continue longer.

The news helped the NZD strengthen against other currencies. Moreover, an interesting situation develops on the NZD/USD chart:

→ based on the results of yesterday, the price recovered and strengthened above the low C, which today is the minimum of 2024.

→ Moreover, level C is in the region of 50% of the rollback from the impulse movement A→B.

→ At the same time, the chart shows signs of a failed bearish breakout of the level of 0.6050, which previously served as resistance.

Considering the above arguments, there is reason to believe that the bulls may try to resume the uptrend (shown by the blue channel) after the price of NZD/USD has fallen below its border (for now - not for long). The trigger for a new surge in volatility could be news about the state of the labour market in the US, data is expected today at 16:30 GMT+3.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.