Sample Category Title

Diving into the CPI Numbers

The strong demand for the US 30-year bond auction, that followed two other strong 3 and 10 year auctions this week triggered no appetite across the US bonds space yesterday, most probably because the 30-year paper is a long maturity paper and is mostly purchased by insurance and pension funds. But the week has been successful for the US Treasury department which saw a solid demand for its debt this week, and that’s thanks to the expectation that the rates will fall – sometime this year – and that the Treasury will also slow down the pace of purchases moving forward.

Appetite in risk assets remains robust. The S&P500 index shortly traded at the 5000 psychological mark before closing a few points below this level. The rally is not only fueled by rate cut expectations and AI speculation but is also backed – to some extent – by encouraging tech earnings from the stars of the league. Note that Apple, Microsoft, Alphabet, Amazon and Meta generated nearly $140bn cash from their operations last quarter. That was the highest on record.

CPI revisions

The Bureau of Statistics will release the CPI revisions today, which consists of the revised month-over-month CPI figures for the past five years, incorporating some adjustments. What’s important to know is that the non-seasonally adjusted data remains unchanged, hence the year-over-year figures for the entire year will remain the same.

Why do people care? Normally, they don’t, because these changes are small and don’t change the end result. But last year, the markets cared because the revisions were more significant than usual and resulted in lower adjusted m-o-m inflation numbers for the first half and higher revisions for the second half – a hint that the moderation in inflation was not as good as thought in the second half of 2022. The latter boosted the Federal Reserve (Fed) rate hike expectations and fueled the US 2-year yield. Today’s revisions could reveal if the downtrending US inflation numbers hide a more significant slowdown, or a late pick up. If the revisions hint at a slowing momentum in monthly inflation figures, the Fed doves should come back in charge and the dollar should eas. If the monthly revisions warn that inflation may not be slowing as fast as we think, the Fed doves will further retreat, and the dollar should gain. And if there are no major revisions, well all eyes will turn to next Tuesday, regular CPI update. And so goes life.

FX and energy

The US dollar struggles to gain further momentum above the 100-DMA. But the US economy’s positive divergence from the rest of the developed nations, its healthy jobs market, its decent fiscal spending are supporting the idea that the Fed is – maybe – not the best candidate to begin the pivot dance. The European Central Bank (ECB) for example is in a better position to start cutting its interest rates to prop up its depressed economies. That idea keeps the EURUSD offered near its own 100-DMA – which stands near 1.0780. Trend and momentum indicators remain comfortable negative and supportive of a deeper downside move in the EURUSD. Today, the German inflation data is expected to confirm a slowdown below the 3% in January – that should help the bears stay in charge.

Elsewhere, the yen bulls are feeling the heat of a totally unexpected return to nearly 150 level at the start of this year. The USDJPY is now trading above the 149 level, and the BoJ hawks are giving in to the expectation that the Japs won’t move soon or quick enough to make 2024 the year of the yen. The USDJPY’s positive trend becomes increasingly vulnerable to verbal intervention as we approach the 150 level.

In energy, we see a second positive attempt above the $76pb level, despite a 5.5-mio barrel build in the US inventories. The rising geopolitical tensions, strong US growth, and Chinese stimulus remain supportive for another attempt above the 200-DMA – near $77.50pb.

Fed’s Barkin Says Rate Cuts Will Have to Eait

In focus today

The last trading day of the week bids us mostly Tier-2 data points.

China celebrates the Lunar New Year on Saturday, and the transition into the Year of the Dragon. Hence, next week is a bank holiday in China, and it will thus be quiet on the Chinese news front. Besides festivities, the Chinese New Year marks a busy travel season, as hundreds of millions of people will be travelling to be with family. Not least the 250 million migrant workers in the cities.

In Norway, we get inflation numbers at 08.00 CET. We expect core CPI to land at -0.1% m/m and 5.2% y/y.

The U.S. Bureau of Labor Statistics publishes its annual revisions to CPI seasonal adjustment factors. While we do not expect material changes, last year the revisions did suggest that inflation had been stickier than previously thought.

In Sweden, we get a bunch of indicators from December in the form of household consumption and supply side factors. The indicators should eventually reflect an inevitable refill of inventories.

We look out for the final German inflation data to dissect the large monthly increase in core inflation registered in January. The increase was likely due to a VAT increase in restaurant services and administered price increases on education and healthcare. These one-off factors should not change the ECB's view on underlying inflation, but it is worth looking at whether the increase was more broad-based.

We wish you a great Friday and weekend!

Economic and market news

What happened overnight

In the US, Donald Trump won the Nevada state caucus as expected. Earlier Thursday he had also won the Virgin Island caucus. The wins put Trump even closer to the GOP nomination for the 5 November presidential election.

In commodities, oil prices rose more than three percent yesterday after Israeli premier Netanyahu refused a proposed ceasefire deal. The ICE Front Month Brent future trades flat this morning.

What happened yesterday

Fed's Barkin spoke at the Economic Club in New York City. He said it was wise for the FOMC to take its time before cutting rates, so as not to risk inflation reemerging. Barkin underlined that a very strong labour market, as well as strong demand gave the FOMC time to wait before beginning to cut rates. We believe the Fed will cut rates four times in 2024, whereas markets currently price in almost five cuts.

In the US, initial jobless claims fell to 218k from 227k last week, close to expectations.

In the Czech Republic, the central bank cut the repo rate by 50bp to 6.25% from 6.75%. A Reuters poll showed analysts expected a 25bp cut to 6.50%. The CZK sold off markedly following the announcement.

The Riksbank's deputy governor Per Jansson said a rate cut in Sweden was more likely in May or June than in March. He reiterated the message from the Riksbank's minutes released Tuesday, saying the bank would proceed with caution when it came to cutting rates. We expect the first rate cut in June.

Equities: Global equities were higher again yesterday and just like Wednesday without any major macro on monetary policy news to set the direction. We are for sure not big believers in technical analysis but admit it is a puzzle how S&P500 gets so extremely close to the 5000 level but not breaking it. To make it clear, we do not think it is a magic resistance level and it just a question of time until the index is higher. Yesterday we saw a bit more sector rotation with cyclical growth outperforming. That was not so surprising, but it is more interesting to see material and banks struggling when sentiment is improving like it is currently. Materials is very much a function of the challenging period for China (industrial metals down 3% last 5 trading days). Banks are lagging the faith from investors in being able to first avoid loan losses and secondly deliver earnings growth. We argue the fear of loan losses is overdone while we admit banks will struggle in delivering compatible earnings growth short term. In US yesterday, Dow +0.1%, S&P 500 +0.1%, Nasdaq +0.2% and Russell 2000 +1.5%. Asian markets are mixed this morning. Please note several markets are now closing for the Lunar New Year holiday. Futures in Europe and US are barely moving this morning.

FI: Bond yields traded higher in absence of new information through the European trading session. Because there was no significant driver, one may attribute the move higher in yields to be emanating from the front end with markets continuing to price out the aggressive policy easing. The 10y Bunds ended 4bp higher at 2.35%, which is a new year-to-date high. The US Treasury USD25bn 30y bond auction saw solid demand of 2.4 bid to cover ratio, which is in line with previous appetite. Rates moved 2bp lower on the back of the auction.

FX: The USD found some support yesterday after having struggled slightly over the previous three sessions. Meanwhile, BOJ Deputy Uchida's dovish statements pushed the JPY to the lowest level since late November, with USD/JPY eyeing 150 consequently. The Sterling weakened somewhat after jobs report showed easing wage growth. NOK defied rising oil prices and weakened, pulling NOK/SEK towards 1M low 0.9850.

ECB’s Kazaks: Summer the moment for rate cut, not Spring

ECB Governing Council member Martins Kazaks provided a tempered outlook on the prospects of interest rate reductions within Eurozone, cautioning against premature expectations for cuts as early as spring. In an interview with Latvijas Radio, Kazaks outlined his stance on the timing and conditions necessary for beginning to ease ECB's monetary policy stance.

"At the moment, there are expectations that the rates could be cut in the spring, in March or April — I wouldn't be optimistic," Kazaks stated. He advocates for a patient and data-driven approach, emphasizing the importance of ensuring that inflation trends are firmly under control before considering rate reductions.

"I would be cautious and I would wait until the inflation story is over. Then we can safely breathe and those rates can be lowered step by step," he elaborated.

Looking ahead, Kazaks indicated "Summer could be that moment". However, he cautioned that would depend on incoming data. "If nothing negative happens, that pushes up inflation and geopolitical risks, if nothing like that happens then this will be the year that rates start to be lowered," he added.

BoE’s Haskel defends focus on inflation persistence without regret

BoE MPC member Jonathan Haskel emphasized the importance of caution when interpreting UK's recent decline in headline inflation to 4% in December. While acknowledging this positive trend, he stressed the necessity of focusing on more enduring aspects of inflation.

"I'm not going to apologize for banging on about persistence because I think we're right to," he asserted. Particularly concerning to Haskel are the underlying measures of price growth, especially within the services sector. Despite the headline inflation drop, these measures have recently plateaued at an annual rate of approximately 6.5%, a level Haskel considers still too high.

"The signs that we've seen thus far are encouraging. I don't think we've seen quite enough signs yet," Haskel remarked. "But if we accumulate more evidence on persistence, then by the very logic I've just set out, I'd be happy to change my vote."

Haskel, who supported another rate hike in the last MPC meeting, described his decision as "finely balanced," highlighting his desire for more time to assess the inflationary trend's durability.

Nikkei Trading In An Impulse Sequence Favor Continuation Higher

The Short-Term Elliott Wave view in Nikkei (NKD_F) suggests that the rally from the 04 October 2023 low is unfolding in an impulse sequence favoring more upside to take place. In which the previous rally to 33780 high ended wave 1. Then a pullback to 32195 low ended wave 2. Up from there, the rally to 37010 high ended wave 3 & made a pullback in wave 4. The internals of that pullback unfolded in a double three structure. Whereas wave ((w)) ended at 35700 low. A bounce to 36290 high ended wave ((x)) and ended wave ((y)) at 35671 low. Thus completing wave 4 pullback.

Up from there, the index has made a new high already above 37010 high confirming the wave 5 higher. Also, the rally from the 35671 low is unfolding in an impulse sequence where lesser degree wave (i) ended at 36535 high as a diagonal. Down from there, a lesser degree pullback to 35835 low ended wave (ii) & started the next leg higher towards 37290 high to end wave (iii). Below from there, the index is doing a short-term pullback in wave (iv) towards 36789- 36567 area lower. From there, the index is expected to resume the upside or should produce a 3 wave reaction higher as long as the pivot from 35671 low stays intact.

Nikkei 1-Hour Elliott Wave Chart

Nikkei Elliott Wave Video

https://www.youtube.com/watch?v=traxZ013iZw

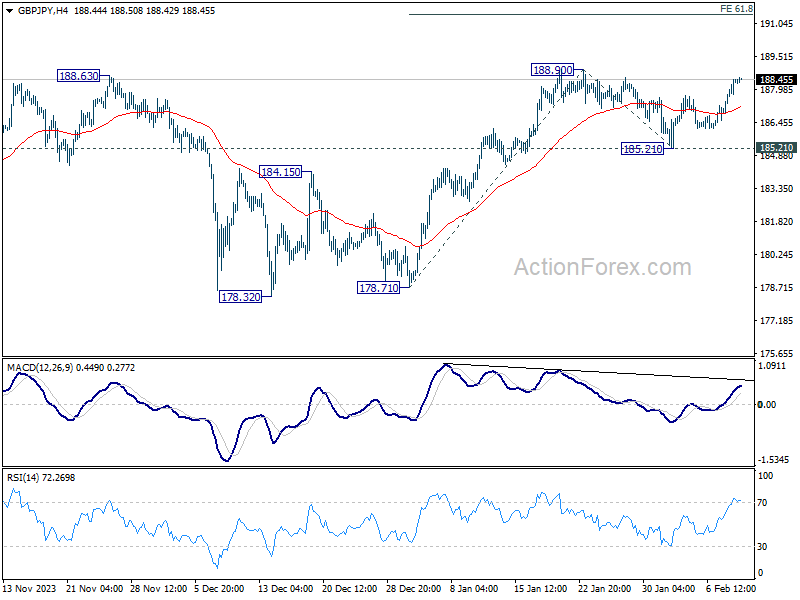

GBP/JPY Daily Outlook

Daily Pivots: (S1) 187.34; (P) 187.91; (R1) 188.96; More...

Intraday bias in GBP/JPY stays on the upside for 188.90 resistance. Firm break there will resume larger up trend. Next near term target will be 61.8% projection of 178.71 to 188.90 from 185.21 at 191.50. For now, near term outlook will stay bullish as long as 185.21 support holds, in case of retreat.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

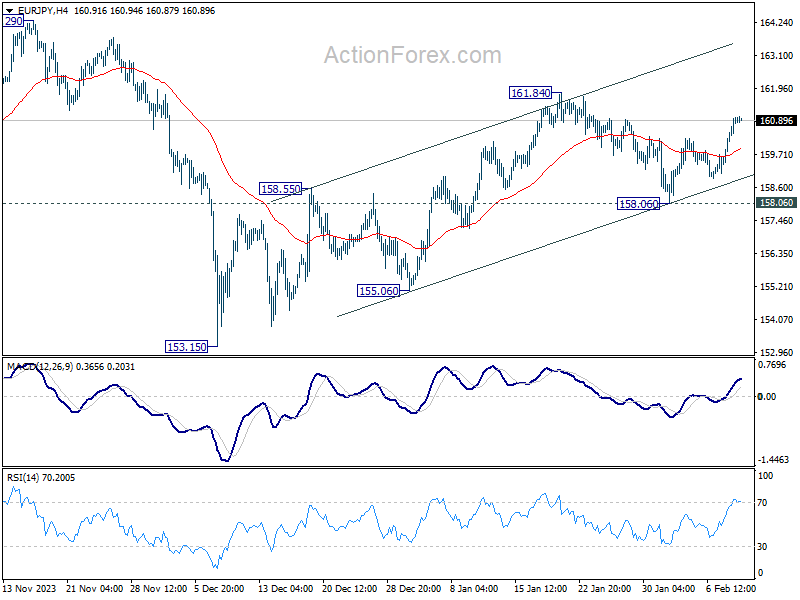

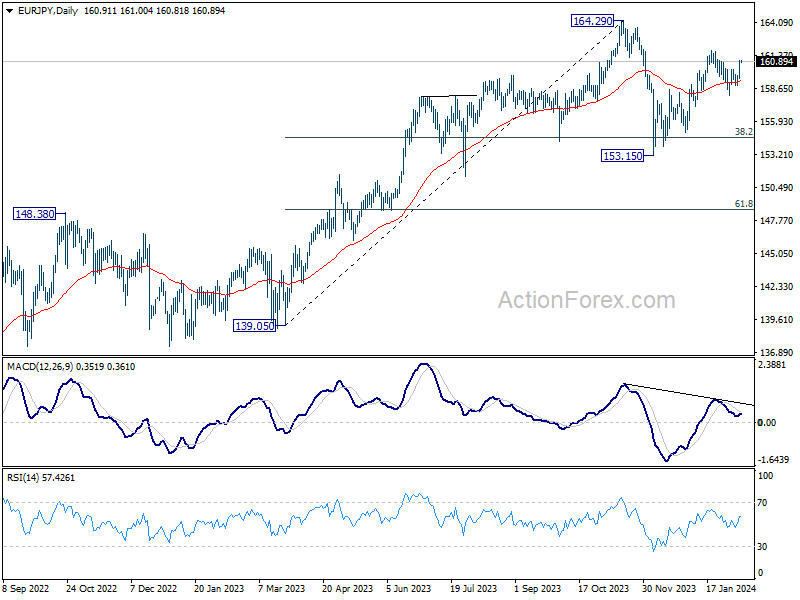

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.93; (P) 160.47; (R1) 161.47; More...

Intraday bias in EUR/JPY remains on the upside for the moment. Rise from 158.06 is in progress for retesting 161.84. Firm break there will resume whole rise from 153.15 and target 164.29 high. For now, further rally is expected as long as 158.06 support holds, in case of recovery.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage.

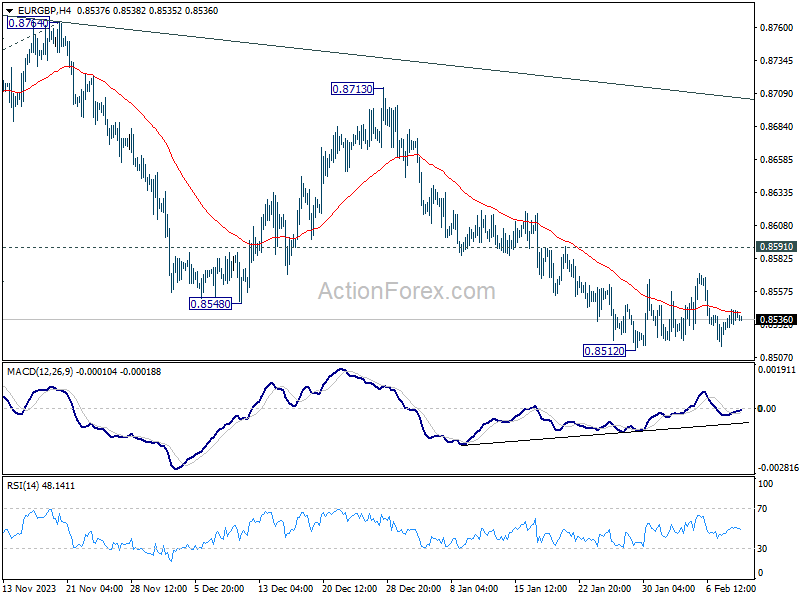

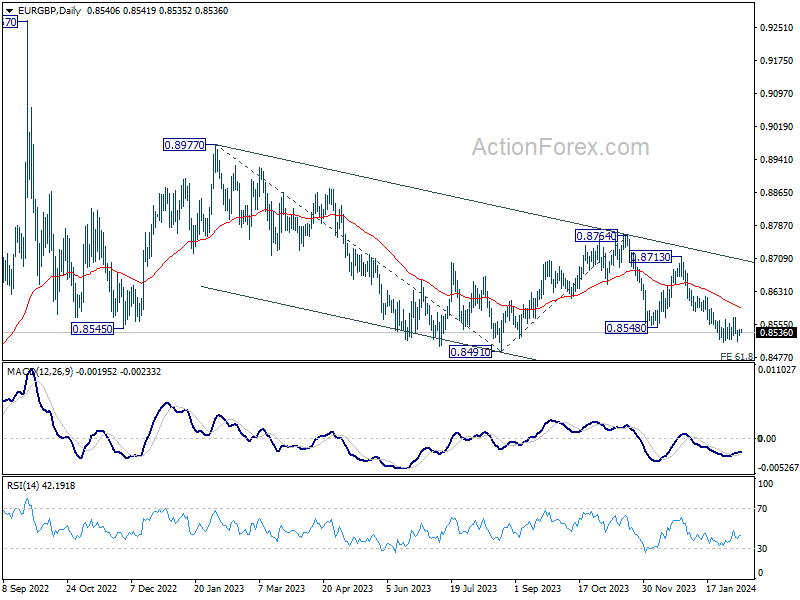

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8531; (P) 0.8538; (R1) 0.8550; More...

Intraday bias in EUR/GBP remains neutral as consolidation continues above 0.8512 support. Further decline is expected with 0.8591 resistance intact. On the downside, below 0.8512 will resume the fall from 0.8713 to 0.8491, and then 0.8464 projection level. However, firm break of 0.8591 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

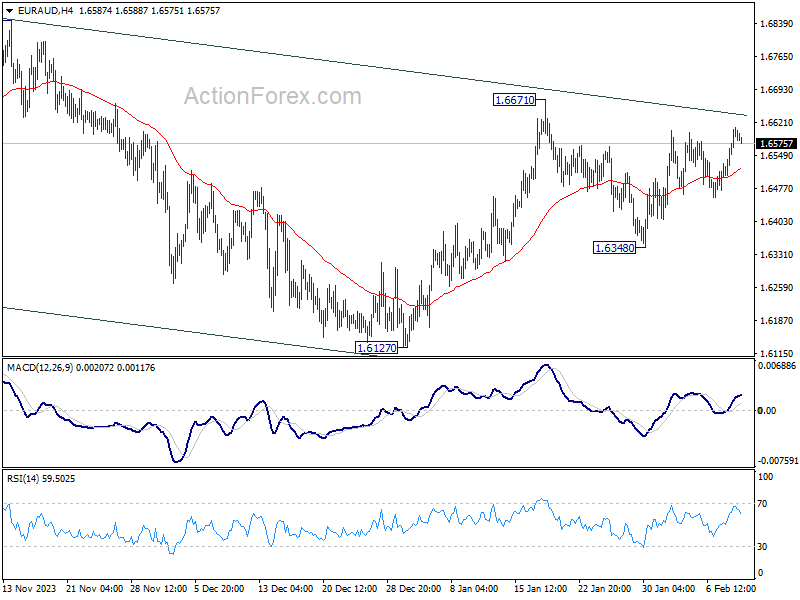

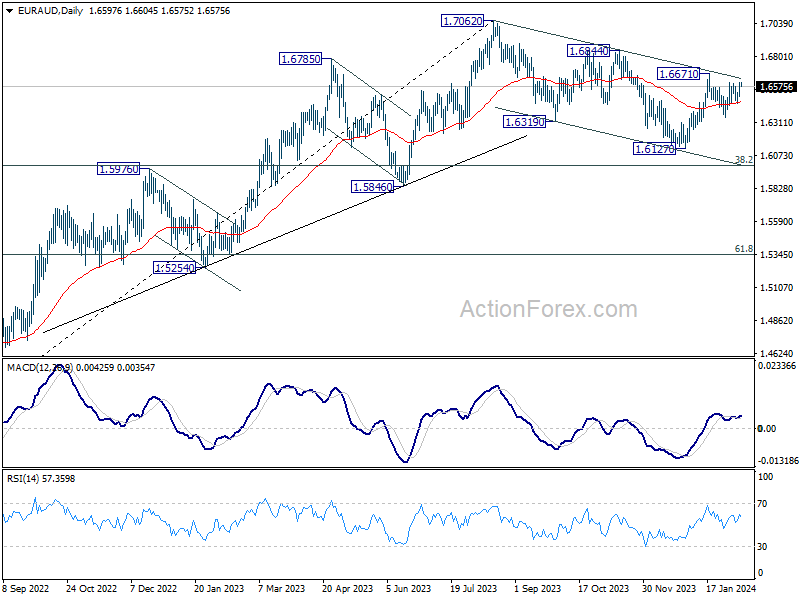

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6535; (P) 1.6573; (R1) 1.6640; More...

Intraday bias in EUR/AUD remains neutral as range trading continues. On the upside, decisive break of 1.6671 will revive the case that whole correction from 1.7062 has completed with three waves down to 1.6127. Further rally should then be seen to 1.6844 resistance for confirmation. Nevertheless, break of 1.6438 will bring deeper fall back to 1.6127 support instead.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

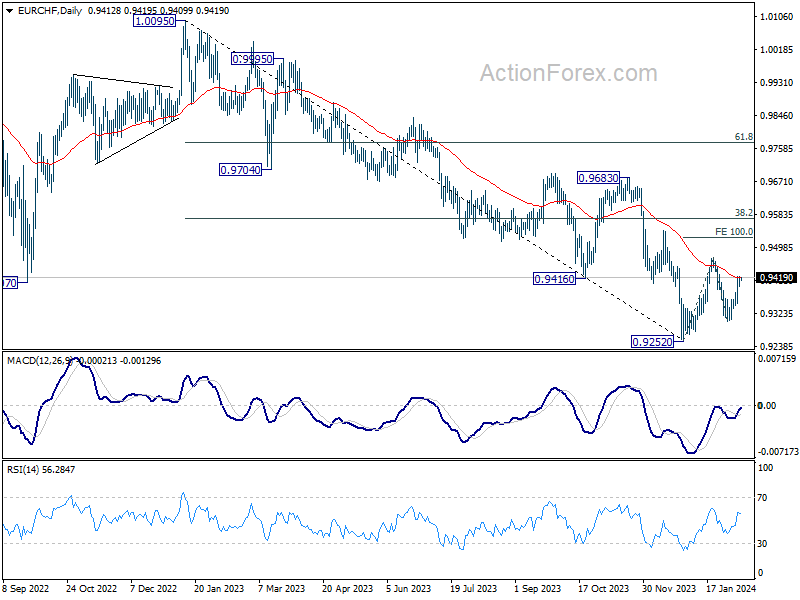

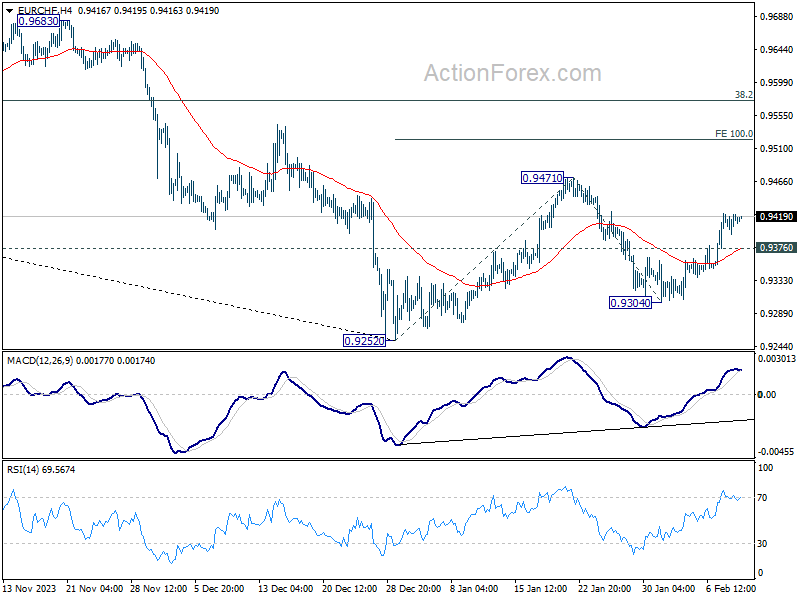

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9401; (P) 0.9413; (R1) 0.9428; More...

EUR/CHF's rise from 0.9304 is in progress and intraday bias remains on the upside for 0.9471 resistance. Firm break there will resume whole rebound from 0.9252. Next target is 100% projection of 0.9252 to 0.9471 from 0.9304 at 0.9523. On the downside, below 0.9376 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). Further rise would be seen to 38.2% retracement of 1.0095 to 0.9252 at 0.9574. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.