Sample Category Title

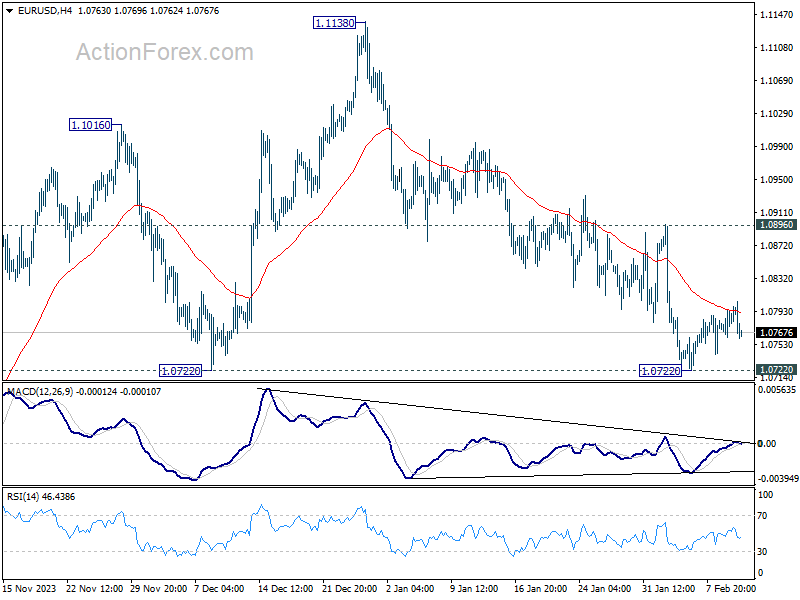

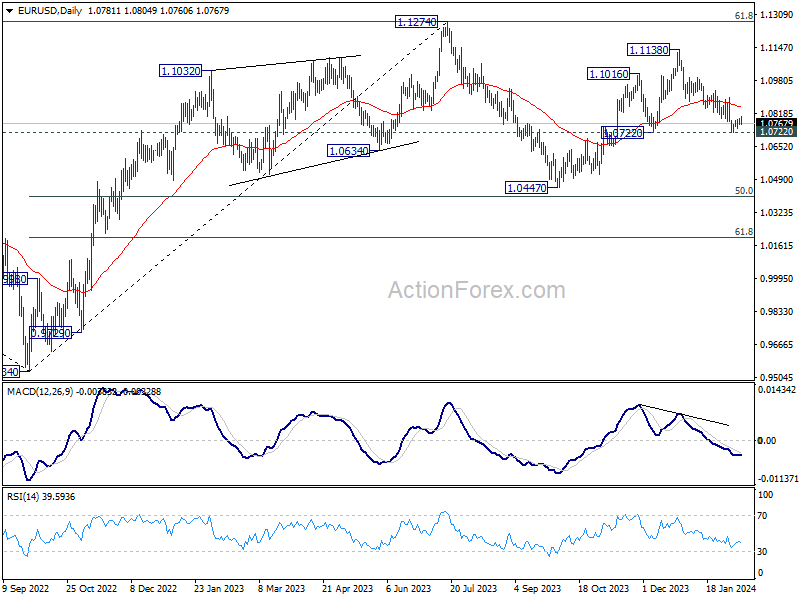

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0766; (P) 1.0781; (R1) 1.0799; More...

Intraday bias in EUR/USD remains neutral and outlook is unchanged. While stronger recovery cannot be ruled out, outlook will stay bearish as long as 1.0896 resistance holds. On the downside, sustained break of 1.0722 will argue that whole rise from 1.0447 has completed. Deeper fall would then be seen to target this low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

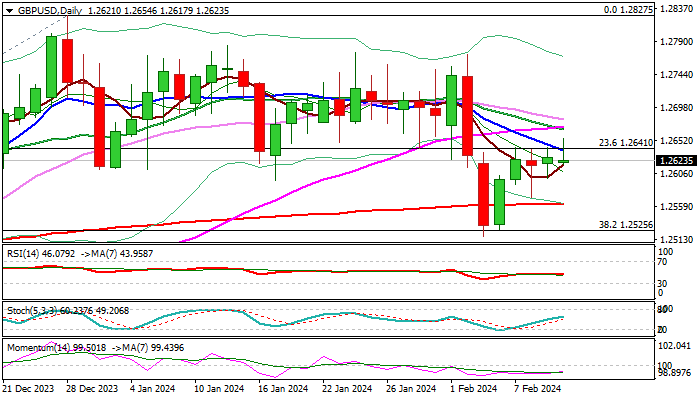

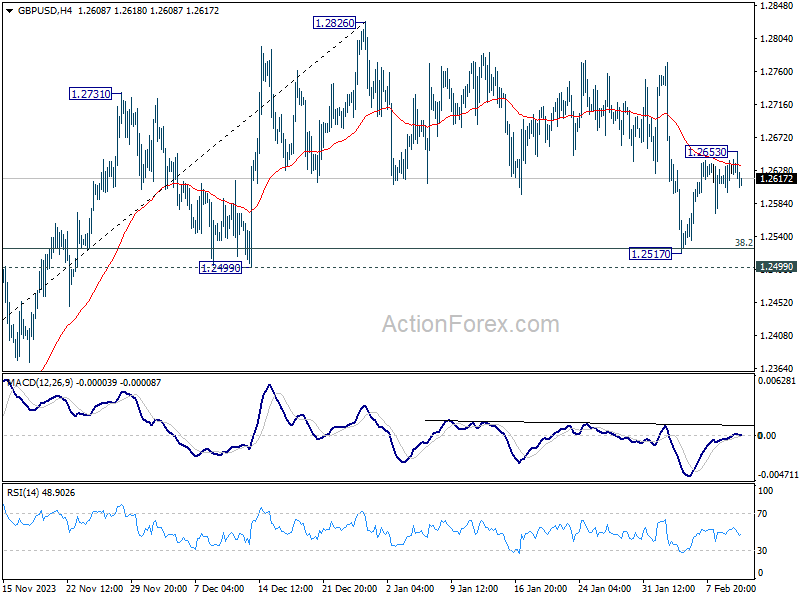

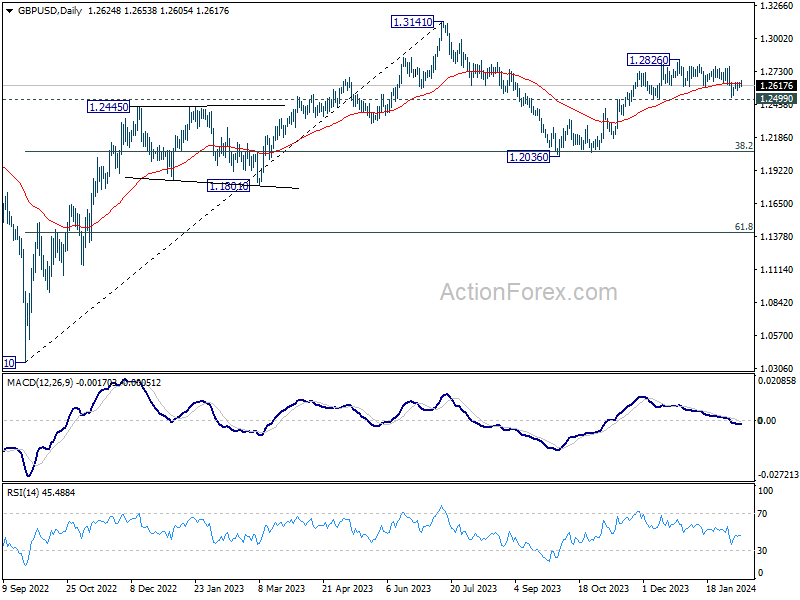

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2604; (P) 1.2624; (R1) 1.2648; More...

GBP/USD edged higher to 1.2653 today but failed to sustain above 55 4H EMA again. Intraday bias remains neutral for the moment. On the upside, firm break of 1.2653 resistance will affirm the case that correction from 1.2826 has completed at 1.2517, after drawing support from 1.2499. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, would could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

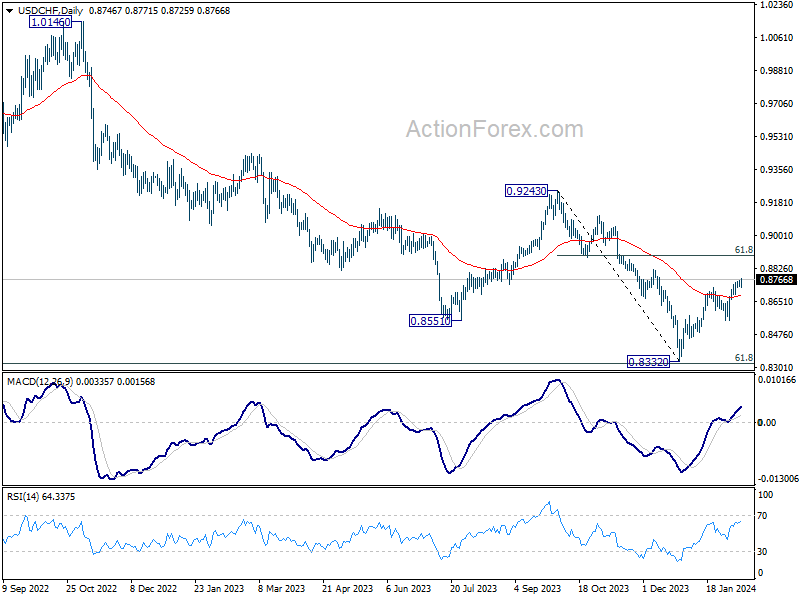

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8733; (P) 0.8747; (R1) 0.8763; More....

USD/CHF's rally continues today and intraday bias stays on the upside. Current rise from 0.8332 should target 61.8% retracement of 0.9243 to 0.8332 at 0.8995. On the downside, below 0.8725 minor support will turn intraday bias neutral first. But near term outlook will stay cautiously bullish as long as 0.8550 support holds.

In the bigger picture, there is prospect of medium term bottoming at 0.8332 considering possible bullish convergence condition in W MACD, and the support from 0.8317 long term fibonacci support. Sustained trading above 55 D EMA (now at 0.8681) will affirm this case, and bring stronger rise back towards 0.9243 resistance, even as a corrective move.

GBP/USD Eyes Bailey, Jobs Report

The British pound is showing limited movement at the start of the week. In Monday’s North American session, GBP/USD is trading at 1.2610, down 0.15%.

Bank of England Governor Andrew Bailey will speak at a public event later today and the markets will be listening carefully, looking for hints about the BoE’s future rate path. The BOE kept rates unchanged at 5.25% for a fifth straight time at the meeting on January 31, as expected. The MPC vote was a surprise, however, with a three-way split. This indicates a divergence of views among MPC members as to the future rate path.

Inflation is running at a 3.9% clip, well above the 2% target and maintaining rates in restrictive territory should push inflation lower. At the same time, elevated interest rates could tip the weak UK economy into a recession, and weary home owners are looking for relief from high mortgage payments.

After Bailey’s remarks, market attention will focus on Tuesday’s employment report. The labour market has been cooling but remains in good shape and strong wage growth continues to drive inflation, which is a major headache for the BoE.

The economy is projected to have added 73,000 jobs in the three months to December, compared to 108,000 in the three months to November. Unemployment is expected to creep up to 4.0%, up from 3.9%, while average earnings including bonuses is projected to ease to 5.6%, down from 6.5%.

The Federal Reserve may have signaled that rate cuts are coming, but it has remained hawkish and continues to push back against market expectations of a rate cut. In December, Fed rate odds for a March cut were above 70%, but the odds have been shaved down to just 15%, as the US economy remains surprisingly strong and Fed members have dampened hopes of a March cut. We’ll hear later today from Richmond Fed President Thomas Barkin. Last week, Barkin said that he wants to be sure that inflation is clearly headed to 2% before he supports lowering rates.

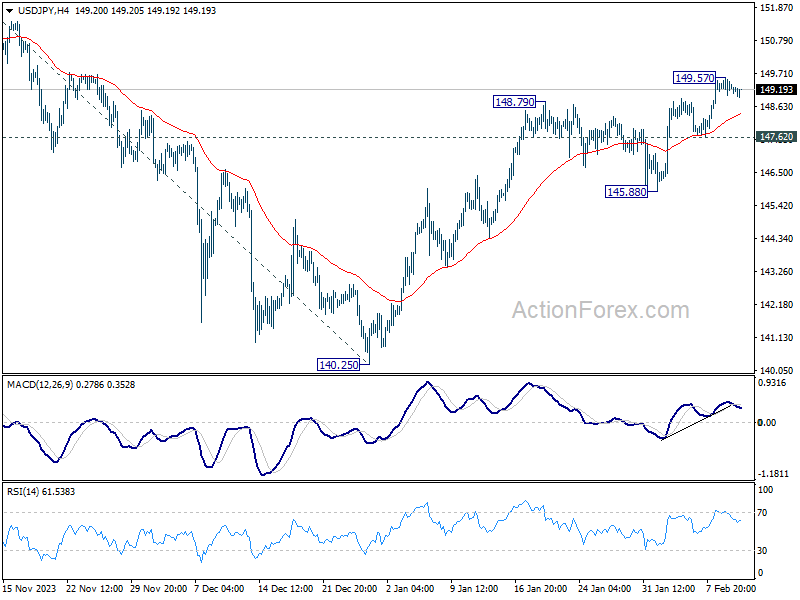

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.01; (P) 149.29; (R1) 149.56; More...

Intraday bias in USD/JPY is turned neutral as retreat from 149.57 is extending. Some consolidations could be seen but further rally is expected as long as 147.62 support holds. Above 149.57 will resume the rise from 140.25 to retest 151.89/93 key resistance zone. Decisive break there will confirm resumption of larger up trend.

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption, and next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.

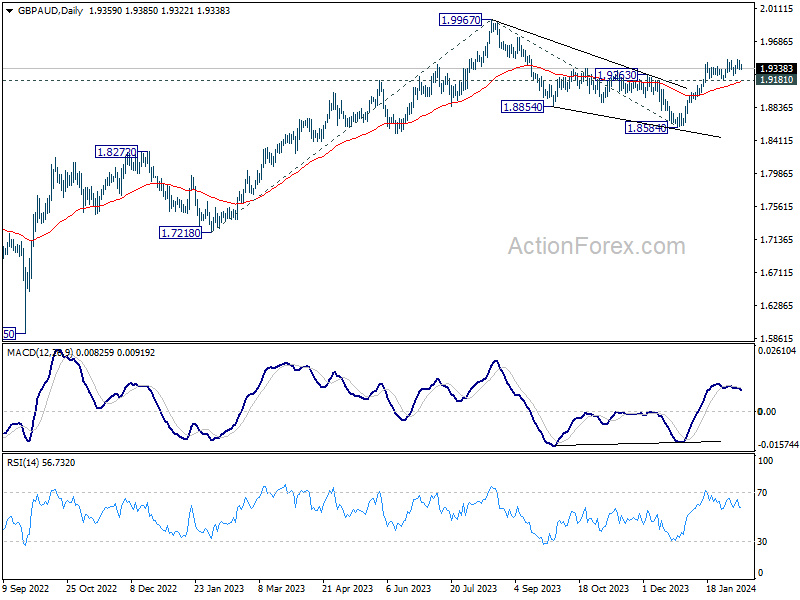

Yen Regaining Ground, GBP/AUD Staying Bullish Despite Loss of Momentum

Japanese Yen stages a broad recovery today, buoyed by notable retreat in European benchmark yields. Meanwhile, Dollar is softening against Yen, yet holding its ground across other major currencies. New Zealand Dollar emerges as the day's underperformer, yet its losses remain contained within Friday's range against all counterparts. Sterling and Euro follow closely as the next underperformers.

One currency pair to closely monitor this week is GBP/AUD, as the market braces for significant economic releases from both UK and Australia. UK's GDP and inflation data, coupled with Australian employment figures, are poised to potentially sway the direction of GBP/AUD.

Technically, rebound from 1.8584 has been losing momentum since mid January, as seen in D MACD. But near term outlook will stay bullish as long as 1.9181 support holds. Rise from 1.8584 is tentatively seen as resuming the long term up trend through 1.9967 high. However, firm break of 1.9181 will dampen this view and extend the correction from 1.9967 with another falling leg.

In Europe, at the time of writing, FTSE is down -0.08%. DAX is up 0.37%. CAC is up 0.42%. UK 10-year yield is down -0.032 at 4.055. Germany 10-year yield is down -0.034 at 2.351.

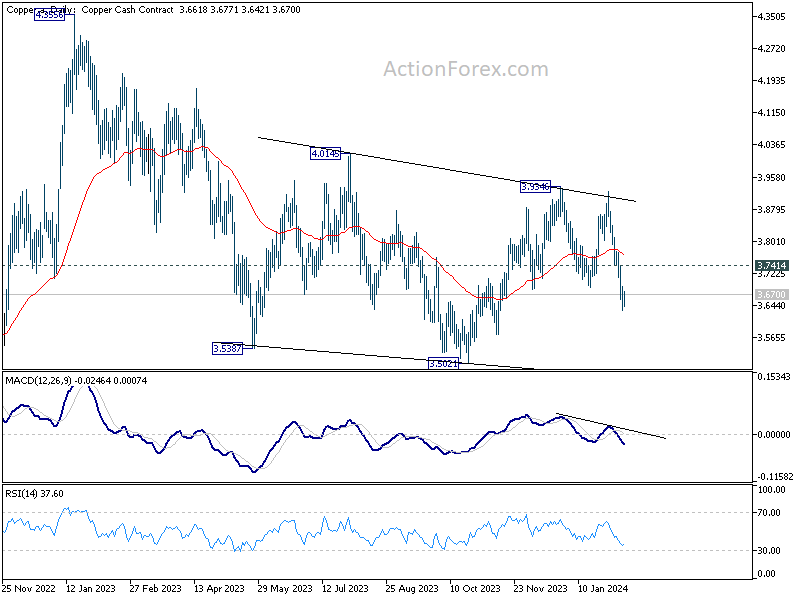

Copper stabilizes after selloff on supply concern, no clear bounce yet

Copper trades steadily in range today, showing no immediate signs of a rebound. Near term selloff intensified following last week's announcement by KoBold Metals, a venture with backing from notable figures including Bill Gates, about the discovery of a substantial copper deposit in Zambia. This revelation has the potential to significantly augment global copper supplies in the years ahead, casting a shadow over the commodity's near-term price outlook.

Technically, near term outlook will stay bearish as long as 3.7414 resistance holds. Deeper decline would be seen to 3.5021 support. Firm break there will pave the way to retest 2022 low at 3.1314. This bearish development, if realized could drag AUD/USD further towards 2022 low at 0.6169.

RBNZ's Orr stands firm on restrictive policy to combat persistent inflation

RBNZ Governor Adrian Orr, in a parliamentary committee appearance today, articulated a firm stance on maintaining restrictive monetary policy to tackle the country's higher-than-desired inflation rate.

Currently sitting at 4.7%, New Zealand's inflation remains "too high" and overshoots RBNZ's target band of 1% to 3%

"That's why we've retained a restrictive monetary policy stance with the official cash rate at 5.5%, and we'll be back at the end of this month again with our updated views on the wisdom of that stance."

Deputy Governor Christian Hawkesby provided additional insights, noting the resilience of New Zealand's financial system and the capacity of consumers to absorb higher interest rates.

"The vast majority of households have continued to manage the debt and service their mortgages, although some are struggling and falling behind," Hawkesby added.

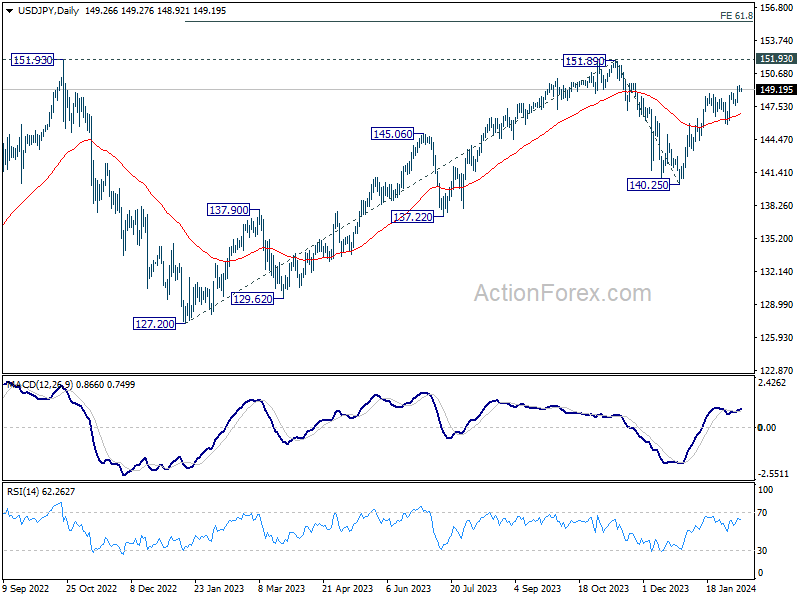

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.01; (P) 149.29; (R1) 149.56; More...

Intraday bias in USD/JPY is turned neutral as retreat from 149.57 is extending. Some consolidations could be seen but further rally is expected as long as 147.62 support holds. Above 149.57 will resume the rise from 140.25 to retest 151.89/93 key resistance zone. Decisive break there will confirm resumption of larger up trend.

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption, and next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 10:00 | EUR | EU Economic Forecasts |

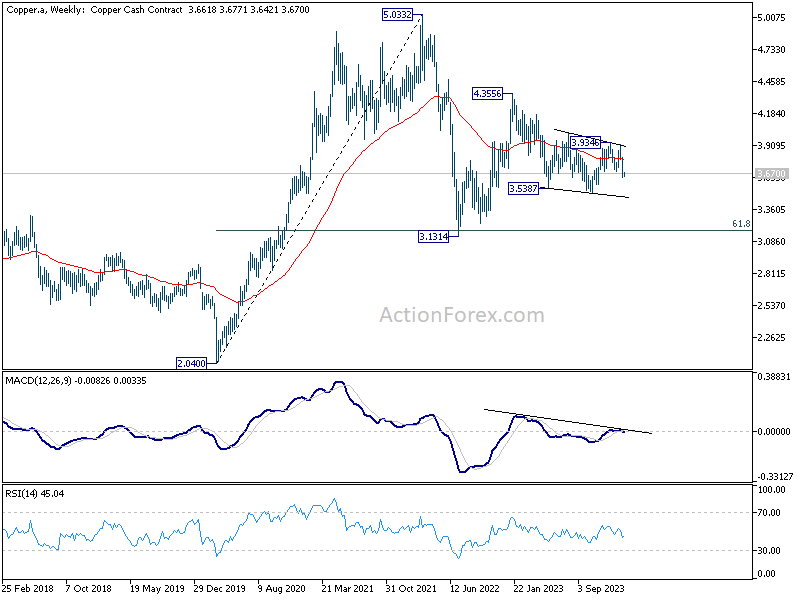

Copper stabilizes after selloff on supply concern, no clear bounce yet

Copper trades steadily in range today, showing no immediate signs of a rebound. Near term selloff intensified following last week's announcement by KoBold Metals, a venture with backing from notable figures including Bill Gates, about the discovery of a substantial copper deposit in Zambia. This revelation has the potential to significantly augment global copper supplies in the years ahead, casting a shadow over the commodity's near-term price outlook.

Technically, near term outlook will stay bearish as long as 3.7414 resistance holds. Deeper decline would be seen to 3.5021 support. Firm break there will pave the way to retest 2022 low at 3.1314. This bearish development, if realized could drag AUD/USD further towards 2022 low at 0.6169.

NZD/USD Dips Despite Hawkish RBNZ

- RBA’s Orr says high rates still needed

- New Zealand releases inflation Expectations on Tuesday

The New Zealand dollar is lower on Monday. In the European session, NZD/USD is trading at 0.6127, down 0.35%. The New Zealand dollar ended the week on a high note, gaining 0.86% against the US dollar on Friday.

RBNZ’s Orr says restrictive policy must continue

Reserve Bank of New Zealand Governor Orr told a parliamentary committee on Monday that inflation was still too high and the RBNZ would need to maintain its restrictive monetary stance.

Orr’s comments signaled a pushback against rate cut expectations, as the markets had priced in a cut as early as May. Orr said that the current inflation rate of 4.7% was still too high and the RBNZ was focused on lowering it to around 2%.

The RBNZ last raised rates in April 2023 and although the central bank hasn’t acknowledged that the rate-tightening cycle is over, the markets have assumed as much and have looked ahead to rate cuts. However, last week’s employment report was stronger than expected, with job growth rebounding 0.4% in the fourth quarter compared to -0.2% in the third quarter. This has dampened market expectations of a rate cut in May, as strong data reduces pressure on the central bank to lower rates.

The RBNZ’s steep rate-tightening cycle, which has raised the benchmark rate to 5.5%, has significantly lowered inflation but there is more work to be done. Orr & Co. wouldn’t mind maintaining rates in restrictive territory in order to continue pushing inflation lower.

We’ll get a look at New Zealand inflation expectations for the first quarter on Tuesday, which could move the New Zealand dollar. In the fourth quarter, inflation expectations eased to 2.76%, down from 2.83%, which was its lowest level in two years.

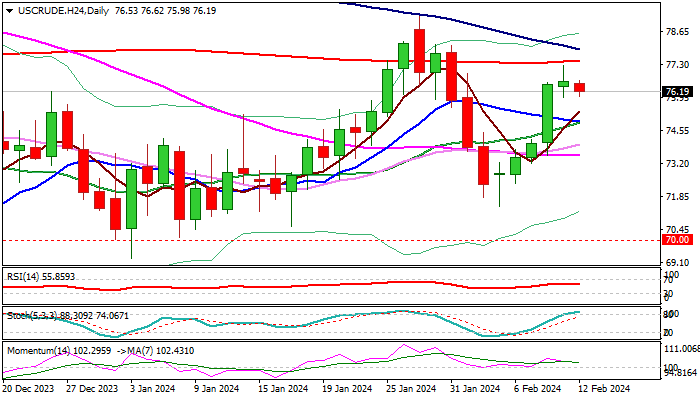

WTI Oil: Oil Price Dips on Easing Concerns About Middle East Supply

WTI oil edged lower in early Monday, following calmer tones regarding possible end of Israeli strikes on southern Gaza, which eased fears about supply disruptions from the Middle East.

Fresh easing started to develop a reversal pattern on daily chart after the recent four-day recovery rally was capped by 200DMA / daily cloud top ($77.45) and Friday’s Doji candle with longer upper shadow signaled indecision and rising downside pressure.

Overbought stochastic and south-heading 14-d momentum (although still in the positive territory) contribute to signals, but more work to the downside is required to verify signal.

Fresh bears pressure initial support at $75.88 (Fibo 23.6% of $71.40/$77.26 upleg / Friday’s low), with break here to weaken near-term structure for attack at lower pivot at $75.00 zone (Fibo 38.2% / converged 10/20DMA’s).

Falling 100DMA ($77.93) is approaching 200DMA and about to form a bear-cross, which would add to downside risk.

Alternative scenario requires lift through 200 and 100DMA’s to ease bearish pressure, while break above $79.27 (former high of Jan 29) and psychological $80 barrier to signal bullish continuation.

Res: 77.45; 77.93; 78.13; 79.27.

Sup: 75.88; 75.00; 74.33; 73.64.

GBP/USD: Limited Recovery Warns of Prolonged Sideways Mode

Cable ticked higher and hit new highest since Feb 2 in early Monday but was so far unable to sustain gains, keeping the price within congestion which extends into fourth straight day.

A double Doji (Fri/Thu) signal indecision as daily studies are mixed and keep near-term price action between 200DMA (1.2564) and falling 10DMA (1.2638).

Break of either side to generate initial direction signal, although more work at the upside will be required. Breach of sideways-moving and converged daily Tenkan-Kijun-sen (1.2645/51 respectively) to revive bulls, with lift and close above daily cloud top (1.2691) to confirm continuation of recovery leg from 1.2518 (Feb 5 low).

Conversely, break below 200DMA support to weaken near-term structure for renewed attack at 1.2525 pivot (Fibo 38.2% of 1.2037/1.2827 rally), violation of which to open way for deeper correction.

Res: 1.2651; 1.2670; 1.2691; 1.2755.

Sup: 1.2599; 1.2566; 1.2525; 1.2481.