Sample Category Title

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.06; (P) 188.40; (R1) 188.93; More...

GBP/JPY's strong break of 188.90 confirms up trend resumption. Intraday bias stays on the upside. Next near term target is 61.8% projection of 178.71 to 188.90 from 185.21 at 191.50. On the downside, below 187.83 minor support will turn intraday bias neutral and bring consolidations first. But outlook will stay bullish as long as 185.21 support holds, in case of retreat.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

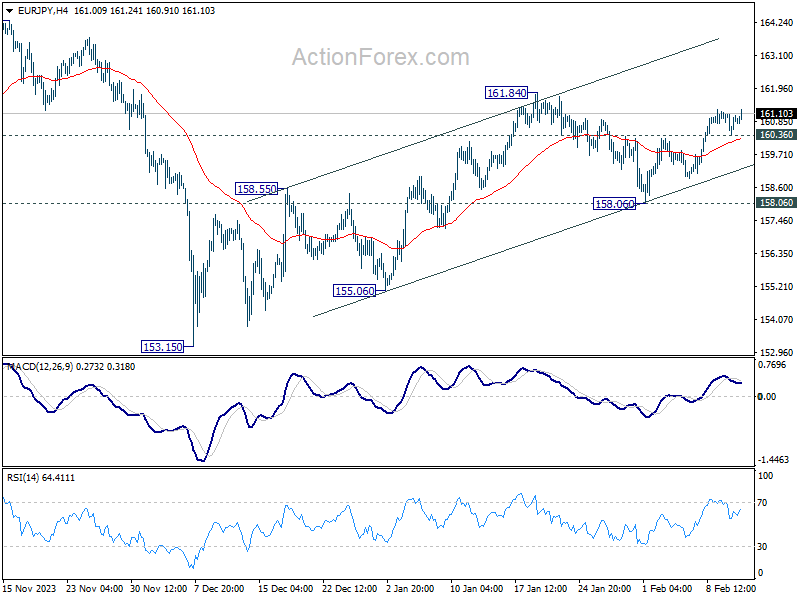

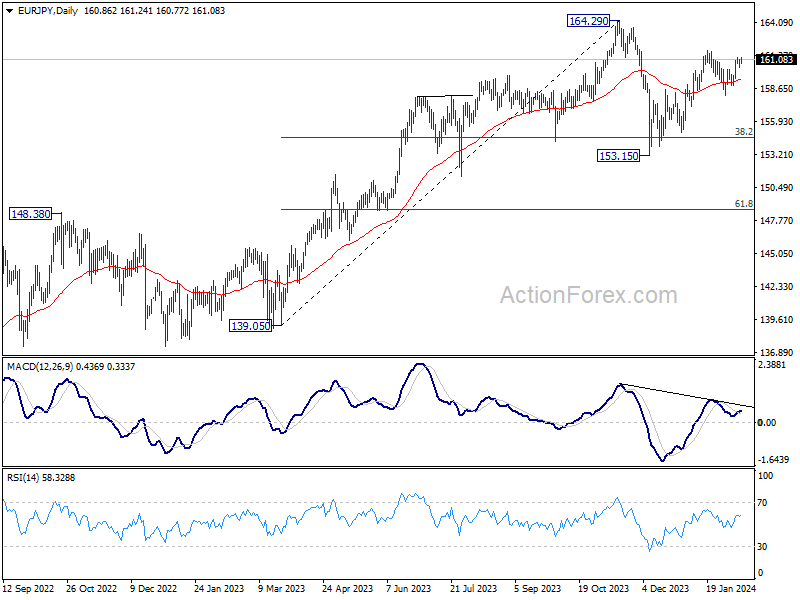

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.47; (P) 160.79; (R1) 161.19; More...

Intraday bias in EUR/JPY stays on the upside despite loss of momentum. Firm break of 161.84 will confirm resumption of whole rise from 153.15. Next target is a retest on 164.29 high. On the downside, below 160.36 minor support will turn intraday bias neutral first. But further rally is expected as long as 158.06 support holds, in case of retreat.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

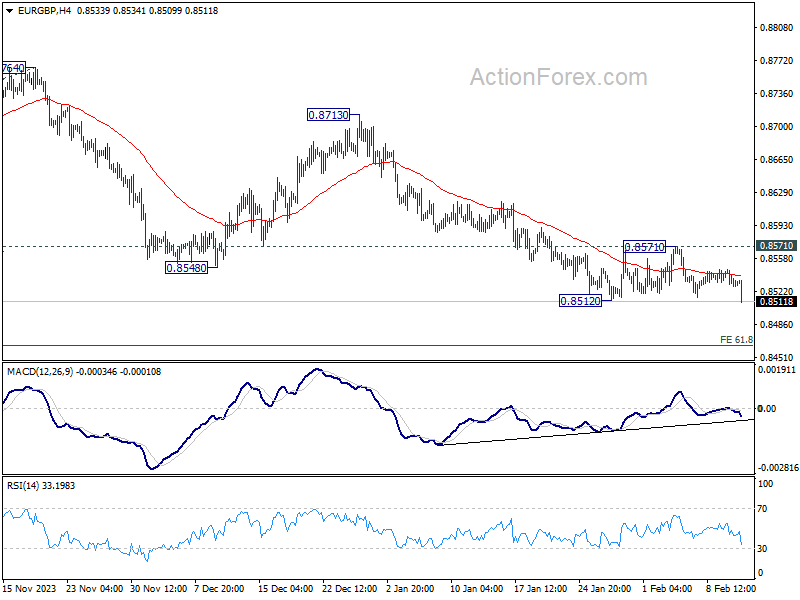

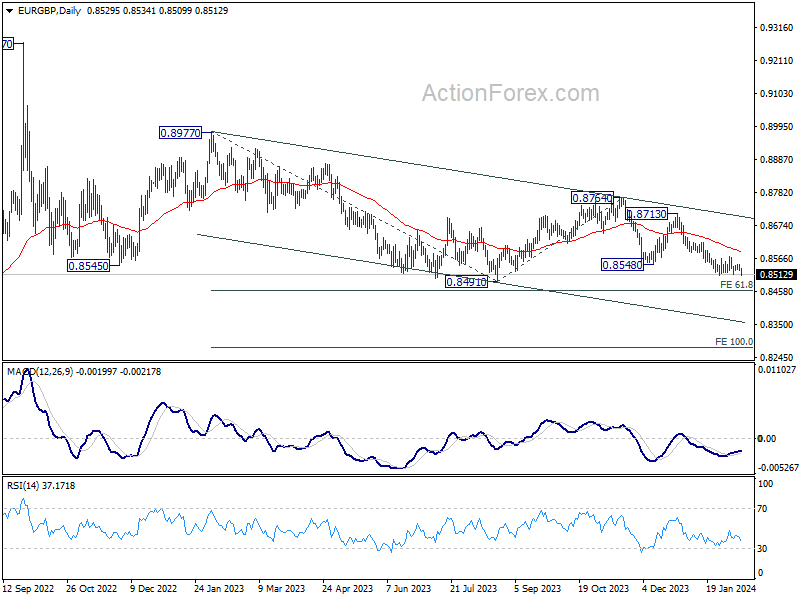

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8524; (P) 0.8535; (R1) 0.8542; More...

EUR/GBP's breach of 0.8512 support suggests that recent decline is resuming. Intraday bias is back on the downside for 0.8491. Break there will resume larger down trend to 0.8464 projection level. For now, break of 0.8571 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

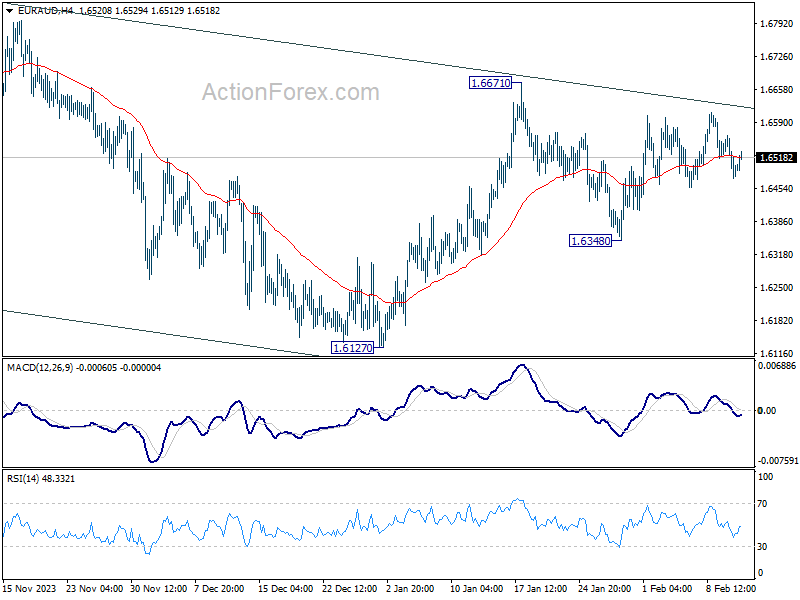

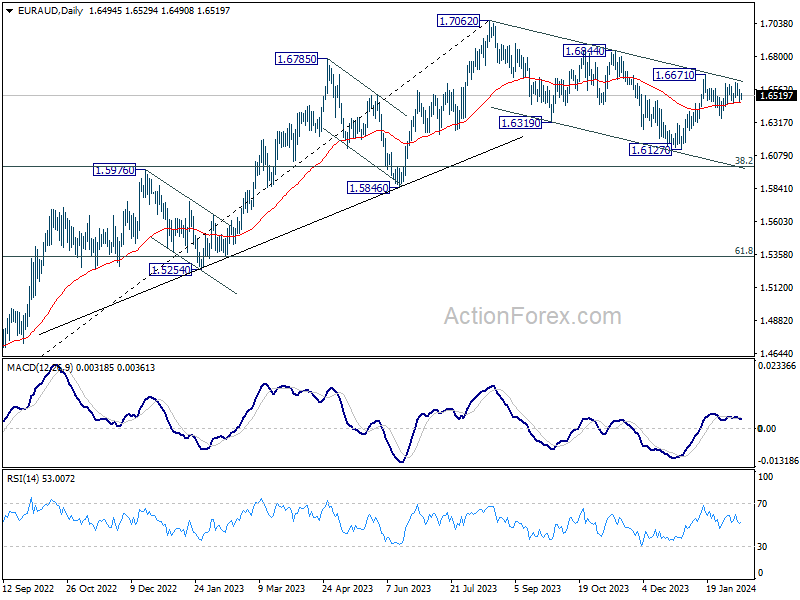

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6460; (P) 1.6512; (R1) 1.6547; More...

No change in EUR/AUD's outlook as sideway trading continues. Intraday bias stays neutral at this point. On the upside, decisive break of 1.6671 will revive the case that whole correction from 1.7062 has completed with three waves down to 1.6127. Further rally should then be seen to 1.6844 resistance for confirmation. Nevertheless, break of 1.6438 will bring deeper fall back to 1.6127 support instead.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

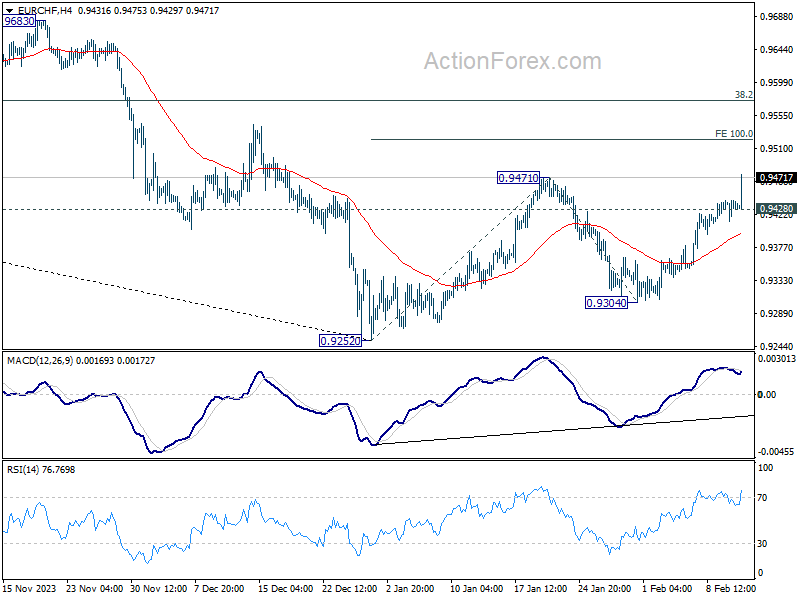

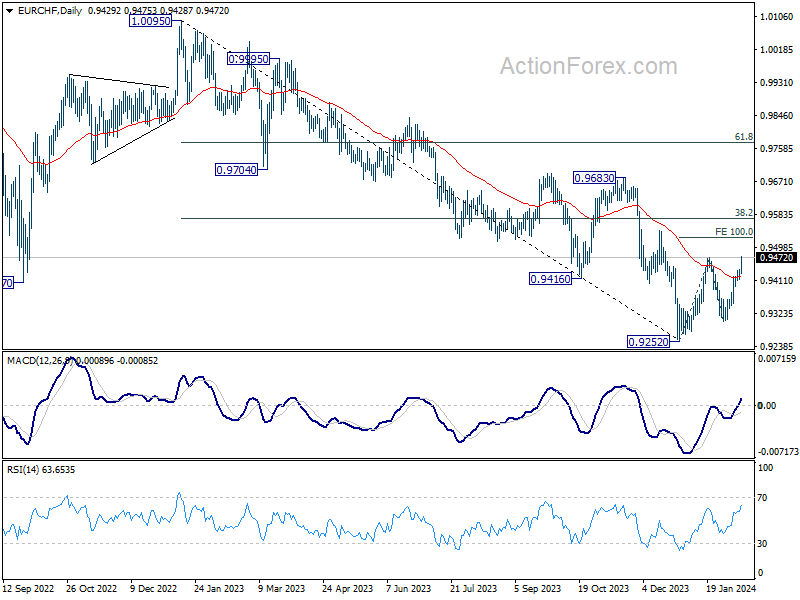

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9418; (P) 0.9430; (R1) 0.9446; More...

EUR/CHF's rally extends today, and it's now pressing 0.9471 resistance. Intraday bias stays on the upside. Firm break of 0.9471 will confirm resumption of whole rebound from 0.9252. Next target is 100% projection of 0.9252 to 0.9471 from 0.9304 at 0.9523. On the downside, below 0.9428 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). Further rise would be seen to 38.2% retracement of 1.0095 to 0.9252 at 0.9574. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.

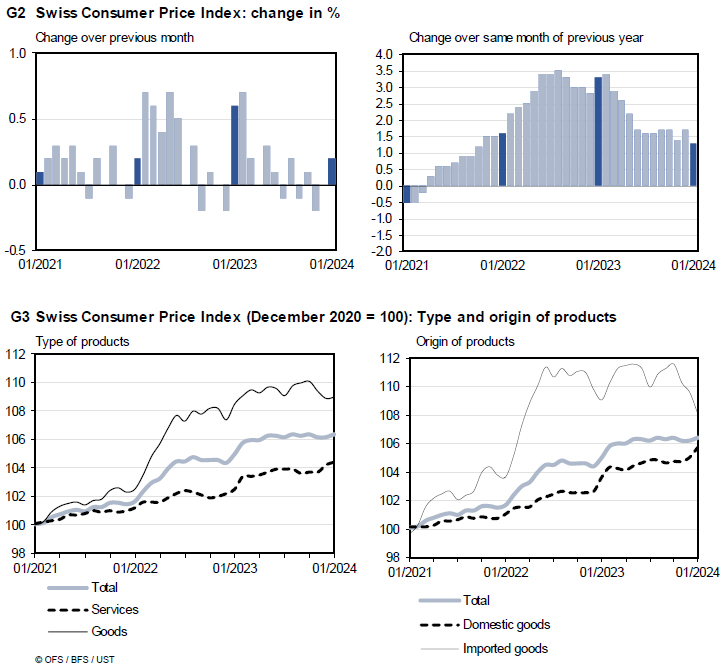

Swiss CPI down to 1.3% yoy in Jan, below expectation 1.6% yoy

Swiss CPI rose 0.2% mom in January, well below expectation of 0.6% mom. Core CPI (excluding fresh and seasonal products, energy and fuel), fell -0.3% mom. Domestic products prices rose 0.6% mom. Imported products prices fell -1.3% mom.

Annually, CPI slowed sharply from 1.7% yoy to 1.3% yoy, below expectation of 1.6% yoy. Core CPI slowed from 1.5% yoy to 1.2% yoy. Domestic products prices growth slowed from 2.3% yoy to 2.0% yoy. Imported products prices fell deeper, down from -0.2% yoy to -0.9% yoy.

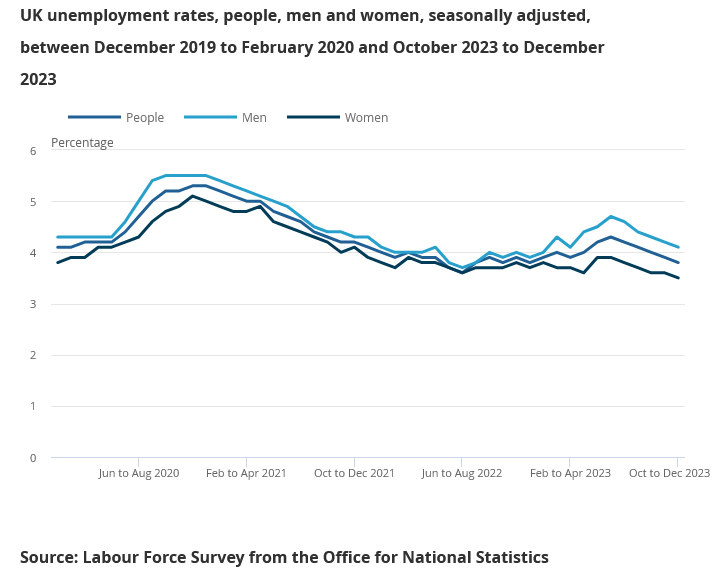

UK unemployment rate falls to 3.8%, wages growth slows but beat expectations

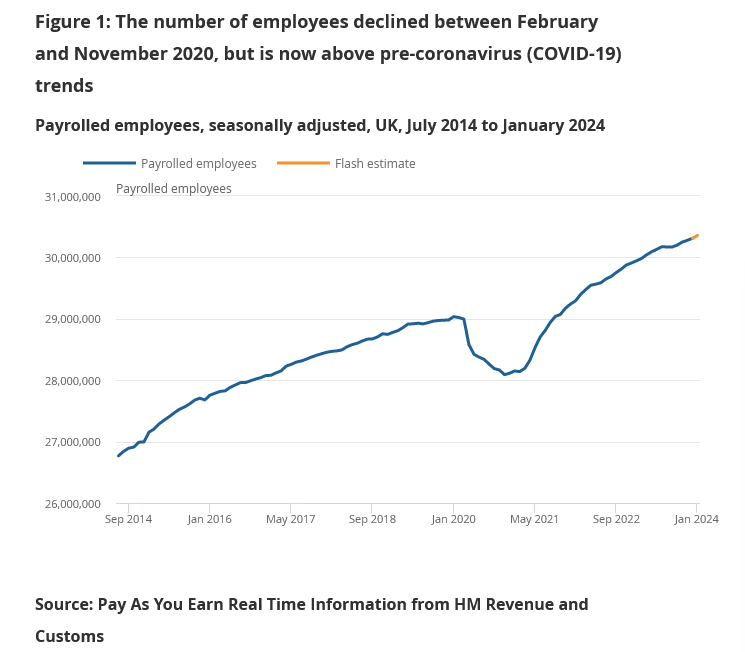

UK payrolled employment rose 48k or 0.2% mom in January. Over the 12-month period, payrolled employment grew 413k or 1.4% yoy. Median month pay rose 6.4% yoy, ticked up from December's 6.3% yoy. Claimant count rose 14.1k, below expectation of 15.2k.

In the three months to December, employment rate rose 0.2% (quarterly change) to 75.0%. Unemployment rate fell -0.2% to 3.8%. Inactivity rate was unchanged at 21.9%. Average earnings including bonus rose 5.8% yoy, down from prior month's 6.7% yoy, but above expectation of 5.7% yoy. Average earnings excluding bonus rose 6.2% yoy, down from prior 6.7% yoy, above expectation of 6.0% yoy.

All Eyes on US Inflation

The week started on a positive note on this side of the Atlantic Ocean, and on a mixed note on the American side. Equities in Europe were better bid on Monday, fueled by luxury stocks like LVMH for example which added 14 points to the index after Hermes hit a record high last week on string quarterly results. The Dutch Adyen extended last week’s post-earnings gains, adding around 34 points to the Stoxx, while Arm holdings jumped another 30% on Monday, after jumping more than 50% in the immediate aftermath of releasing its own quarterly results. All this to tell you that the rally in the European and US stock markets are somehow shouldered by a robust market reaction to encouraging corporate results. But a part of it is supported by the rate outlook. And the rate outlook is coming on slippery ground with every Federal Reserve (Fed) official adding his or her pinch of hawkishness into the mix. Yesterday, Fed’s Michelle Bowman said that the rates are in a good place to keep pressure on inflation and that there is no need to ease rates soon. Likewise, Richmond Fed’s Thomas Barkin said that they are ‘closing in on inflation’ but that they ‘are not there just yet’.

This being said, the New York Fed’s latest inflation survey came with a good surprise. The one and five-year expectations remained unchanged from the month before, but the 3-year inflation expectations fell to the lowest level on record, to 2.35%. That’s what the Fed is working so hard to achieve. And inflation expectations are very important to keep the actual inflation numbers in control. Therefore, the encouraging inflation expectations give hope that the Fed would start cutting rates despite strong growth and spending. However, the expectation of five rate cuts from the Fed is no longer the base case scenario; investors now see four rate cuts being more likely, with the first rate cut priced in at nearly 50-50 for May, and almost fully for June.

These probabilities could change today, in one way or the other, with the latest inflation update. Headline inflation in the US is expected to fall below 3% in January, and core inflation is seen easing to 3.7%. A softer-than-expected set of data will likely boost the May rate cut expectation, keep the dollar index below the 100-DMA and support equities. An unwanted upward surprise, however, should further hammer the May cut expectations and shift focus to June. In this case, we could see the US dollar index finally drill through the thick 100-DMA offers, and some profit-taking in the S&P500.

Crude eyes 200-DMA

American crude consolidates gains above $77pb and is preparing to test the 200-DMA to the upside. Trend and momentum indicators are supportive of a move above this level. Aramco says it sees robust global oil demand this year, OPEC and IEA will release their own predictions today and Thursday respectively. Of course, the predictions from OPEC should be expected to be rosier than the reality – because they have all the interest in the world to fuel oil prices – but the strong US growth and decent Chinese stimulus are indeed positive for the supply-demand dynamics.

However, note that rising oil prices are a double-edged sword. Good growth is positive for oil prices, but higher oil prices are not good for easing inflation. Hence, any U-turn in inflation would get the major central banks to further tighten their purses’ strings, hit growth prospects and hammer a potential oil rally. In conclusion, a rally above the $80pb could be hard to sustain – if the Chinese stimulus story fails to gain traction.

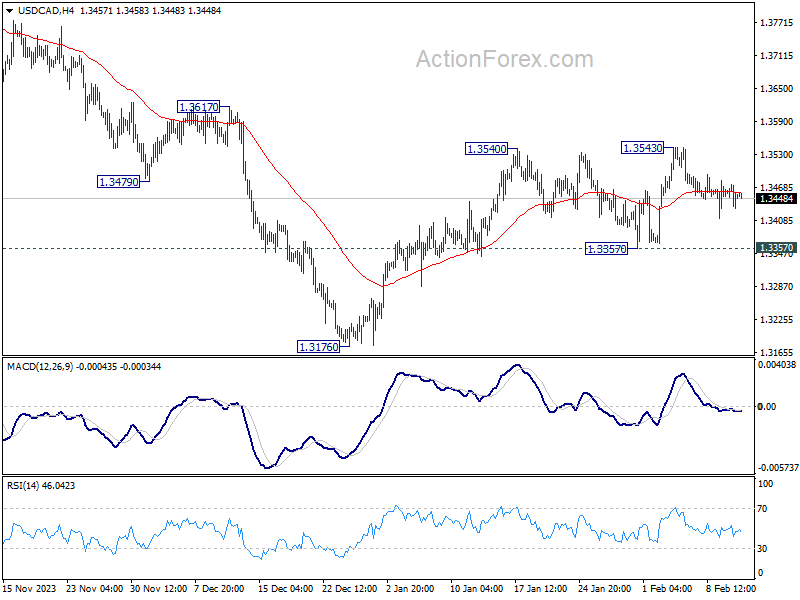

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3429; (P) 1.3452; (R1) 1.3474; More...

Intraday bias in USD/CAD remains neutral as sideway trading continues. Further rise is mildly in favor as long as 1.3357 support holds. On the upside, decisive break of 1.3540/3 will resume the rise from 1.3176. That will also revive that case that whole fall from 1.3897 has completed, and target this resistance. Nevertheless, firm break of 1.3357 support will argue that rebound from 1.3176 has completed, and target this low for resuming the decline from 1.3897.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

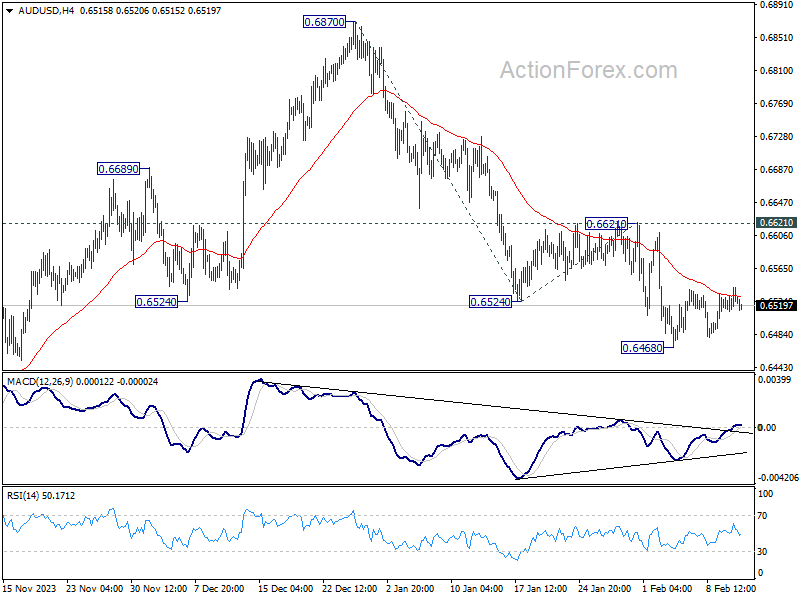

AUD/USD Daily Report

Daily Pivots: (S1) 0.6515; (P) 0.6529; (R1) 0.6545; More...

AUD/USD's consolidation from 0.6468 is still in progress and intraday bias remains neutral at this point. While stronger recovery cannot be ruled out, outlook will remain bearish as long as 0.6621 resistance holds. Break of 0.6468 will resume the decline from 0.6870 to 61.8% projection of 0.6870 to 0.6524 from 0.6621 at 0.6407.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.