Sample Category Title

(RBA) Statement by Michele Bullock, Governor: Monetary Policy Decision

At its meeting today, the Board decided to leave the cash rate target unchanged at 4.35 per cent and the interest rate paid on Exchange Settlement balances unchanged at 4.25 per cent.

Inflation continues to moderate but remains high.

Inflation continued to ease in the December quarter. Despite this progress, inflation remains high at 4.1 per cent. Goods price inflation was lower than the RBA's November forecasts. It has continued to ease, reflecting the resolution of earlier global supply chain disruptions and a moderation in domestic demand for goods. Services price inflation, however, declined at a more gradual pace in line with the RBA's earlier forecasts and remains high. This is consistent with continuing excess demand in the economy and strong domestic cost pressures, both for labour and non-labour inputs.

Higher interest rates are working to establish a more sustainable balance between aggregate demand and supply in the economy. Accordingly, conditions in the labour market continue to ease gradually, although they remain tighter than is consistent with sustained full employment and inflation at target. Wages growth has picked up but is not expected to increase much further and remains consistent with the inflation target, on the assumption that productivity growth increases to around its long-run average. Inflation is still weighing on people's real incomes and household consumption growth is weak, as is dwelling investment.

The outlook is still highly uncertain.

While there are encouraging signs, the economic outlook is uncertain and the Board remains highly attentive to inflation risks. The central forecasts are for inflation to return to the target range of 2–3 per cent in 2025, and to the midpoint in 2026. Services price inflation is expected to decline gradually as demand moderates and growth in labour and non-labour costs eases. Employment is expected to continue to grow moderately and the unemployment rate and the broader underutilisation rate are expected to increase a bit further.

While there have been favourable signs on goods price inflation abroad, services price inflation has remained persistent and the same could occur in Australia. There also remains a high level of uncertainty around the outlook for the Chinese economy and the implications of the conflicts in Ukraine and the Middle East. Domestically, there are uncertainties regarding the lags in the effect of monetary policy and how firms' pricing decisions and wages will respond to the slower growth in the economy at a time of excess demand, and while the labour market remains tight. The outlook for household consumption also remains uncertain.

Returning inflation to target is the priority.

Returning inflation to target within a reasonable timeframe remains the Board's highest priority. This is consistent with the RBA's mandate for price stability and full employment. The Board needs to be confident that inflation is moving sustainably towards the target range. To date, medium-term inflation expectations have been consistent with the inflation target and it is important that this remains the case.

While recent data indicate that inflation is easing, it remains high. The Board expects that it will be some time yet before inflation is sustainably in the target range. The path of interest rates that will best ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks, and a further increase in interest rates cannot be ruled out. The Board will continue to pay close attention to developments in the global economy, trends in domestic demand, and the outlook for inflation and the labour market. The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome.

GBP/USD Tumbles Below Support, Upsides Capped

Key Highlights

- GBP/USD declined heavily below the 1.2650 support.

- It traded below a key contracting triangle with support at 1.2660 on the 4-hour chart.

- EUR/USD could attempt a recovery wave toward the 1.0820 resistance zone.

- The UK Construction PMI could increase from 46.8 to 47.3 in Jan 2023.

GBP/USD Technical Analysis

The British Pound started a fresh decline from the 1.2780 resistance zone against the US Dollar. GBP/USD traded below the 1.2720 support to enter a bearish zone.

Looking at the 4-hour chart, the pair settled below the 1.2700 zone, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

The bears even pushed the pair below the 1.2650 support. Besides, it traded below a key contracting triangle with support at 1.2660 on the same chart. Finally, the pair spiked below 1.2550. It is now consolidating losses near the 1.2540 level.

Immediate support is near the 1.2525 level. The first major support sits near the 1.2500 level. The next major support sits at 1.2440, below which the pair might gain bearish momentum.

In the stated case, the pair could even revisit the 1.2400 support level. On the upside, the bulls are facing hurdles near the 1.2580 level. The next key resistance is near the 1.2620 level. A close above the 1.2620 zone could open the doors for more upsides. The next stop for the bulls might be 1.2650. Any more gains might send GBP/USD toward the 1.2750 level.

Looking at EUR/USD, the pair tumbled toward the 1.0720 level and might soon attempt a recovery wave in the near term.

Economic Releases

- UK’s Construction PMI for Jan 2023 – Forecast 47.3, versus 46.8 previous.

Japan’s labor cash earnings rises 1% yoy, with regular Pay at fastest pace since May

Japan saw a modest improvement in labor cash earnings in labor cash earnings, which increased by 1.0% yoy, accelerating from November's 0.7% gain. Despite this uptick, the growth fell short of anticipated 1.3% yoy.

A notable positive development was observed in regular pay, which rose by 1.6% yoy, marking the highest reading since May 2023. Additionally, special payments saw a marginal increase of 0.5% yoy, although overtime pay experienced a decline of -0.7% yoy.

With CPI standing at 3.0% yoy, real wages saw a decline of -1.9% yoy, albeit at a slower pace compared to -2.5% yoy observed in the previous month. This marks the slowest decline in real wages since June 2023, suggesting a slight easing in the pressure on household incomes.

However, this positive note is tempered by the latest household spending figures, which saw a -2.5% yoy drop, worse than the expected -2.1% yoy.

BoE’s Pill: Rate reductions now a question of timing

BoE Chief Economist Huw Pill highlighted, in an online event overnight, a shift in BoE's monetary policy discussions, which has evolved to determining "when" rather than "if" it will be appropriate to commence reductions in the Bank Rate.

Pill pointed out that rate reductions is currently "premature." However, he suggested that the Bank does not require inflation to fully revert to its 2% target before easing monetary policy, given its current restrictive stance.

The Chief Economist also cautioned that due to developments in the Middle East, inflation is slightly more likely to "surprise on the upside than the downside" over the next year to 18 months. This perspective justifies to "to maintain restriction in the economy for some time". This scenario would warrant maintaining "for longer" or even increasing the restrictive nature of monetary policy to combat "second round effects".

Yet, Pill also left room for optimism, suggesting that if inflation dynamics dissipate more quickly than anticipated, there could be scope for more rapid interest rate reductions.

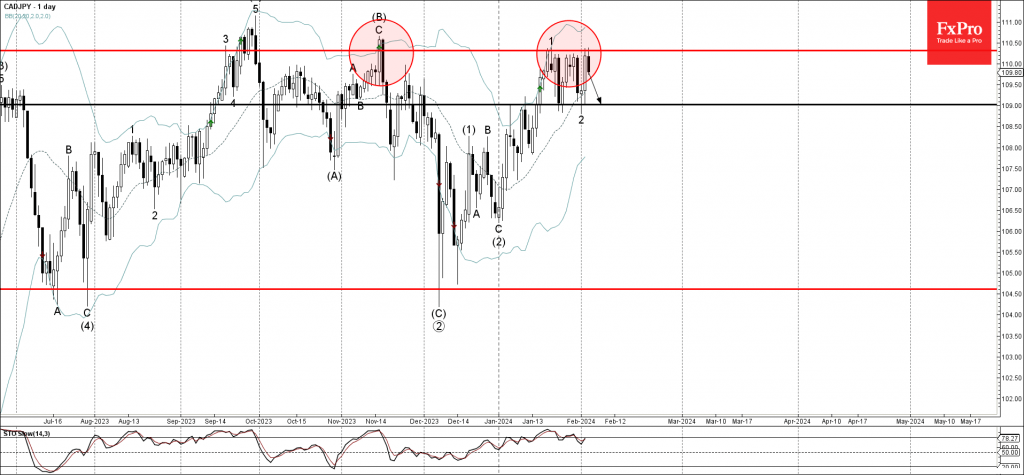

CADJPY Wave Analysis

- CADJPY reversed from resistance level 110.30

- Likely to fall to support level 109.00

CADJPY currency pair recently reversed down from the key resistance level 110.30, which has been reversing the pair from the middle of November.

The resistance level 110.30 reversed the pair multiple times from last month.

Given the strength of the resistance level 110.30 and the strengthening yen gains, CADJPY currency pair can be expected to fall further to the next support level 109.00.

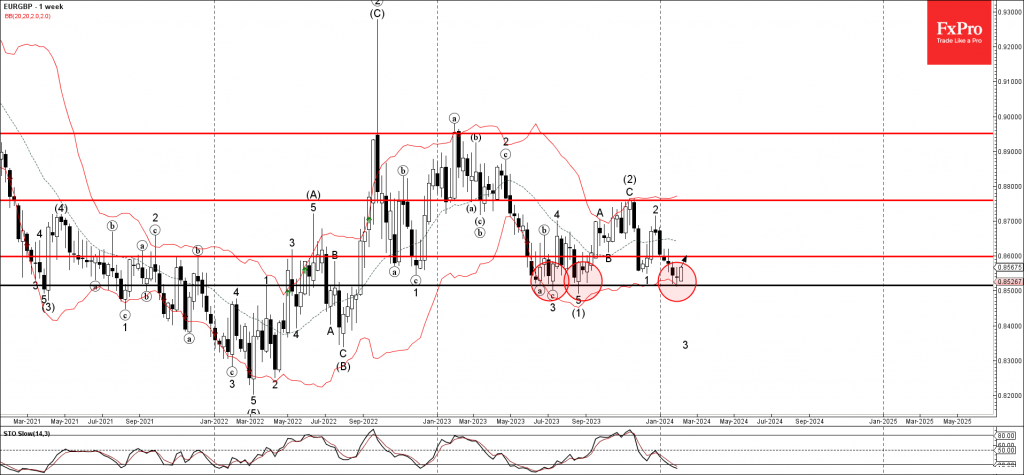

EURGBP Wave Analysis

- EURGBP reversed from support level 0.8515

- Likely to rise to resistance level 0.8600

EURGBP currency pair recently reversed up from the key support level 0.8515, which has been reversing the pair from the middle of last year.

The support level 0.8515 was strengthened by the lower weekly Bollinger Band.

Given the strength of the support level 0.8515 and the oversold weekly Stochastic, EURGBP currency pair can be expected to rise further to the next resistance level 0.8600.

ISM Shows Services Sector Expansion Accelerates in January

The ISM Services PMI jumped to 53.4 in January from 50.6 in December, comfortably beating the 52.0 consensus expectation. Ten industries out of 18 reported growth for the month – up from nine in December.

The business activity sub-index was unchanged at 55.8, while the new orders index rose to 55.0 from 52.8 in December.

The prices paid component jumped 7.3 percentage points (pp) to 64.0. The supplier deliveries sub-index rose to 52.4, the highest print since November 2022, and indicates longer delivery times compared to December.

The employment sub-component flipped to signaling growth, as it jumped 6.7 pp to 50.5.

Key Implications

Well, a healthy print from the services sector today. At 53.4, the index shows the sector continues to grow at a healthy clip, with new demand growth reaccelerating again in January. Moreover, the recovery in employment growth suggests December's contractionary reading was an outlier rather than a structural shift.

After Friday's gangbusters payrolls report showed 289k new jobs in the private services sector, today's ISM doesn't come as much of a surprise. If anything it only confirms what we already knew – the U.S. economy continues to chug along and show remarkable strength given the interest rate backdrop. Looking forward, eyes should be focused on whether the uptick in input price inflation is sustained and whether it feeds through to consumers.

Sunset Market Commentary

Markets:

The payrolls-Powell combo resonated through today’s European trading session in absence of other data/events. It put core bonds under further pressure from the start with US Treasuries underperforming German Bunds. Recall that Powell ruled out a March rate cut with the voiceover of the 60 Minutes interview on CBS suggesting that the Fed will only pull the trigger on rates by the middle of the year (June?!). Despite the significant two-day correction, US money markets are still discounting a 60% probability to a May move with cumulative 2024 rate cuts to the tune of almost 125 bps despite Powell confirming an unaltered FOMC view of 75 bps. Comments by Minneapolis Fed Kashkari strengthened the market pulse. He wrote in an essay that the neutral rates possibly rose during the post-pandemic recovery. It gives the FOMC time to assess upcoming economic data before starting to lower its policy rate with less risk that too-tight policy is going to derail the economic recovery. Policy may not be as tight as assumed given the low neutral rate environment that existed before the pandemic. In the December 2023 FOMC dot plot, 7 out of 18 governors indicated that the neutral rate could be above the 2.5% consensus view in place since mid-2019. The January US services ISM dealt a final blow to US Treasuries. The ISM rebounded more than expected (53.4 from 50.5 vs 52 expected). Details showed first employment growth since November (50.5), accelerating new orders (55) and a rapid increase in prices paid (64 from 56.7). US yields at the time of writing add 10 bps (2-yr) to 14 bps (10-yr). EUR/USD is testing 1.0724 support.

UK Gilts underperform German Bunds as well today. The UK Office for National Statistics announced that it will be reinstating from next week reweighted Labour Force Survey estimates. They incorporate latest views on the size and composition of the UK population and replace experimental estimates in place since October 2023. Under the new data, the UK unemployment rate was 3.9% in the three months through November compared to the previous estimate of 4.2%. From a dynamic point of view, the unemployment rate now shows a declining path since Summer compared with the previous more flattish shape. The outcome suggests that the UK labour market remains more tight than expected with the risk of more upward pressure on growth and (wage) inflation. It complicates the picture for the Bank of England and argues in favour of delaying a potential first rate cut. Sterling initially profited from the rate support against an ailing euro, but GBP/USD losing the bottom of its sideways trading channel (1.26) eventually helped the (EUR/GBP)-pair back towards 0.8550.

News & Views:

Turkish inflation accelerated more or less as expected by 6.7% M/M and 64.86% Y/Y in January, from 2.93% M/M and 64.77% Y/Y in December. Only “clothing and footwear” showed a monthly price decline (-1.61%). A core inflation gauge excluding unprocessed food, energy, alcoholic beverages, tobacco and gold rose by 6.85% M/M and 67.68%. Y/Y. A big increase in the minimum wage, price adjustments at the start of the year and the ongoing TRY-depreciation were important drivers of the inflation acceleration. Last month, the CBRT raised its policy rate by 2.5% to 45% while suggesting that the hiking cycle is over with the current rate being sufficient to bring inflation back under control. High domestic/services-related inflation poses an upside risk to outlook. Thursday’s quarterly inflation report of the central bank offers more guidance on the central bank’s intentions.

The OECD upwardly revised its global growth outlook to 2.9% from 2.7% in November. This still means a slowdown compared with expected growth of 3.1% for 2023. The picture diverges across countries with strong growth in the US and many emerging market economies offset by a slowdown in most European countries. Annual GDP growth in the US is projected to remain supported by household spending and strong labour market conditions, but moderate to 2.1% in 2024 and 1.7% in 2025. EMU GDP growth is projected to be 0.6% in 2024 and 1.3% in 2025, with activity held back by tight credit conditions short term before picking up as real incomes strengthen. Chinese growth is expected to ease to 4.7% in 2024 and 4.2% in 2025, despite additional policy stimulus, reflecting subdued consumer demand, high debt and the weak property market. Headline inflation in the G20 economies is projected to drop from 6.6% in 2024 to 3.8% in 2025, with core inflation seen easing to 2.5% in 2024 and 2.1% in 2025.

USD Strengthens Following Strong Employment Data

The US dollar has seen a significant increase in strength against the Euro, with the EUR/USD pair falling to 1.0770 by Monday morning. This movement is largely attributed to the recent release of robust employment sector reports in the US for January, which have shifted investor expectations regarding the Federal Reserve's interest rate decisions.

The Nonfarm Payrolls (NFP) report for January revealed an impressive increase of 353 thousand jobs, far exceeding the anticipated 187 thousand. Additionally, December's NFP figures were revised upwards to 333 thousand. Average hourly earnings also saw a notable rise of 0.6% month-over-month, doubling the forecast. These indicators suggest mounting inflationary pressures, potentially complicating the Federal Reserve's plans to normalize interest rates.

The latest employment data effectively solidified market projections, especially after Federal Reserve officials indicated that a rate cut in March was unlikely, with adjustments possibly being postponed until May.

EUR/USD Technical Analysis

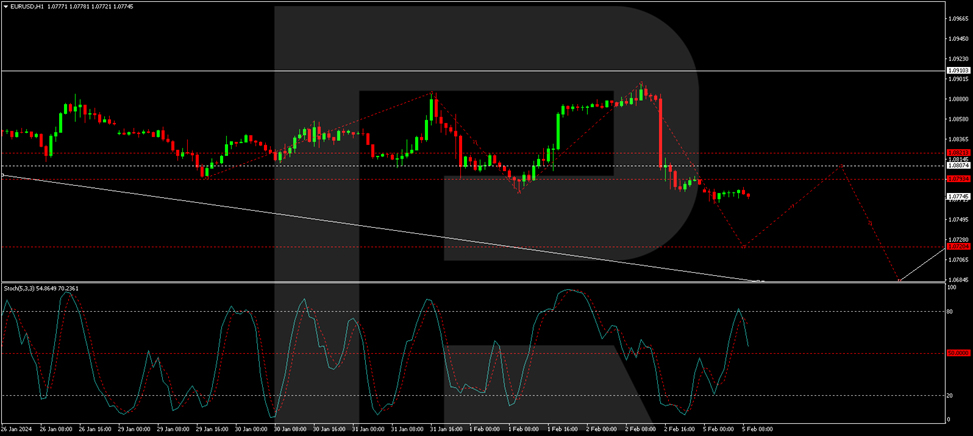

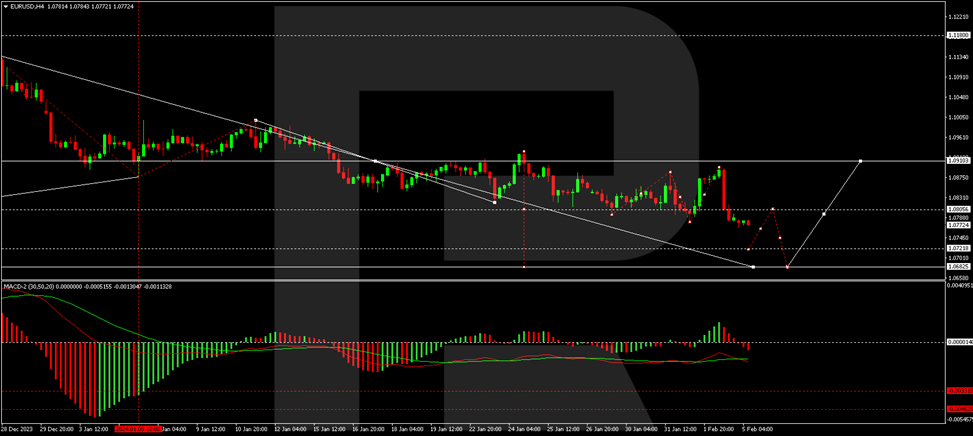

The H4 chart analysis of EUR/USD indicates that a corrective wave reaching 1.0896 has concluded. The market is now in the midst of a downward trend aiming for 1.0722. Upon achieving this target, a potential corrective movement to 1.0808 might occur, serving as a test from below, before the trend resumes its descent towards 1.0682. This outlook is supported by the MACD indicator, which is positioned below zero and indicates a continued downward trajectory.

On the H1 chart, the EUR/USD pair has established a consolidation range around 1.0808. Following a downward breakout, the declining wave is expected to proceed towards 1.0722. After reaching this milestone, a correction back to 1.0808 could be anticipated. The Stochastic oscillator, with its signal line currently above 50, suggests a potential climb to 80 before a decline to 20, reinforcing the bearish scenario outlined.