Sample Category Title

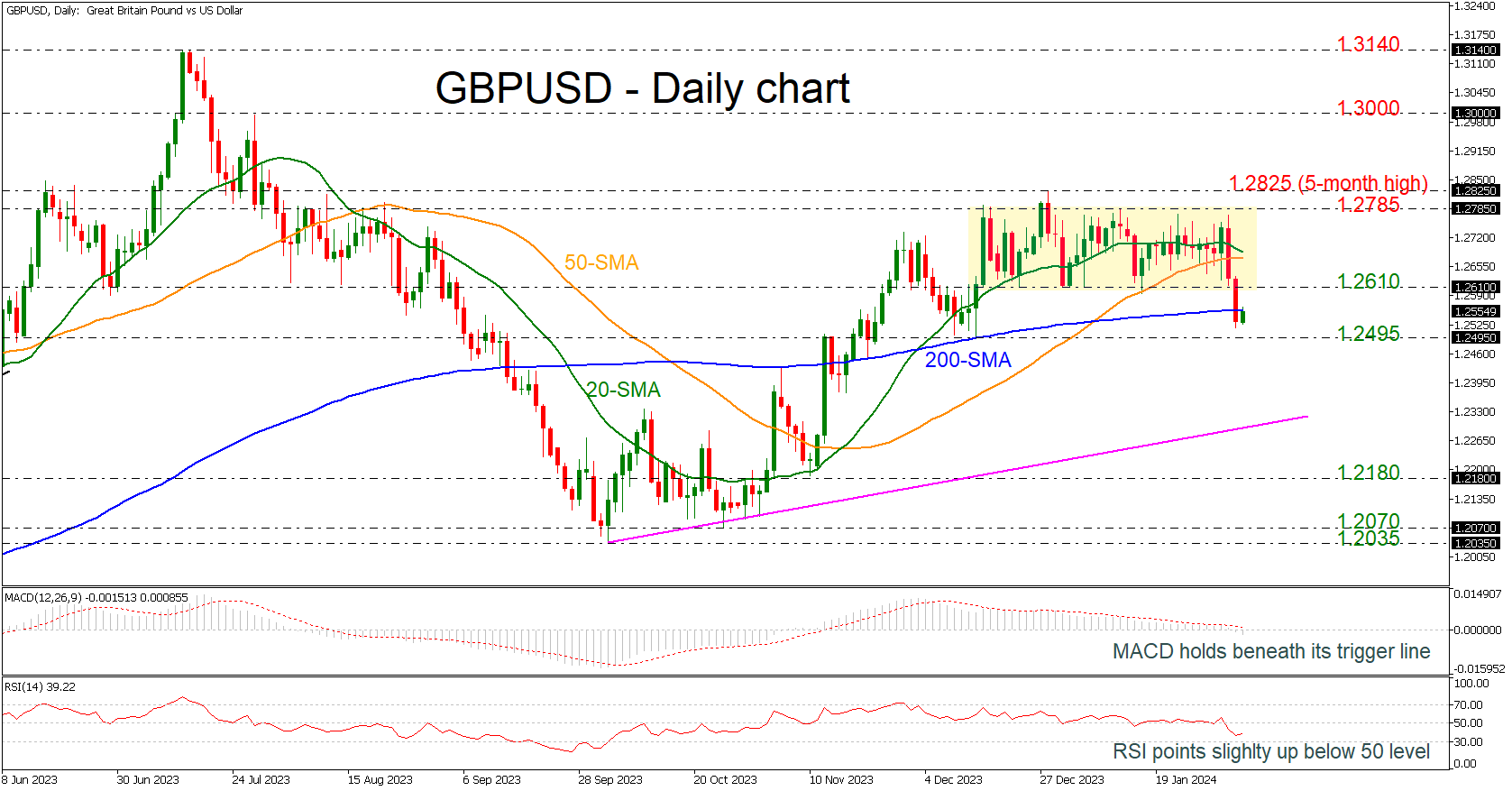

GBPUSD Plummets to 2-month Low

- GBPUSD tests 200-day SMA after strong sell-off

- Prices break trading range to the downside

- Outlook looks bearish in short-term

GBPUSD plunged to a new almost two-month low of 1.2517 on Monday’s session, falling beneath the short-term trading range and the 200-day simple moving average (SMA).

Currently, the market is recovering some losses with the RSI confirming the recent upside move as it is ticking slightly up below 50. On the other hand, the MACD oscillator is losing momentum beneath its trigger and zero lines, while the 20- and the 50-day SMAs are ready for a bearish crossover.

Should the bears press the price below 1.2495, the medium-term ascending trend line around 1.2300 may prevent an aggressive downfall towards the 1.2180 support level. If the latter gives way too, the decline could continue towards the 1.2035-1.2070 area, shifting the outlook to negative.

Alternatively, a climb back above the 200-day SMA and the 1.2610 resistance could meet the 20- and the 50-day SMAs at 1.2680 ahead of the 1.2780-1.2825 region. A climb above these levels could turn the outlook back to bullish.

All in all, GBPUSD is looking bearish in the very short-term timeframe after the tumble beneath the consolidation area; however, the market is still developing well above the medium-term uptrend line.

Several Interest Rates, Both in US and EMU Testing or Nearing Top of Sideways Range

Markets

Since last week’s Fed meeting, the combination of Fed speak and strong US data squeezed investors out of early easing bets and this move simply continued yesterday. The CBS 60 Minutes interview with Fed Chair Powell on Sunday (off script indication of first cut in June?) still resonated. Minneapolis Fed Kashkari reinforced Powell’s message that the Fed shouldn’t be in a hurry to cut rates. To validate this view, he indicated that the neutral policy rate may have increased post-pandemic. This makes current rates less restrictive and gives the Fed time to assess incoming data with less risk of derailing the economy due to overtightening. A few hours later, the incoming data pointed in the same direction. The unexpected setback of the US services ISM in December only proved to be an outlier. The headline index jumped decisively in expansion territory (53.4 from 50.5). New orders (55) are boding well for future activity. Employment also returns north of 50 (50.5). The prices paid index jumped sharply from 56.7 to 64.0. This doesn’t help the Fed to feel more confident that inflation is sustainably returning to 2%. US yields jumped between 13.8 bps (10-y) and 10.8 bps (2-y). Markets further reduced expectations for a May rate cut to <80%. German yields lagged the US but also added between 8.1 bps (30-y) and 4.4 bps 2-y. Several interest rates, both in the US and EMU are testing (ST yields) or nearing (longer maturities) the top of the sideways range that guided trading post the December FOMC meeting (US 2-y 4.50% area, 10-y 4.25% area; EMU 2-y swap 3.05/3.1% area, 10-y swap 2.75/2.77% area). US equities stalled after setting now top levels last week, but the damage was modest (S&P 500 -0.32%). The dollar outperformed. DXY closed above the 104/104.26 resistance. If confirmed, this improves the technical picture. Still, the picture isn’t unequivocal. EUR/USD briefly touched the 1.0724 (Dec low), but in the end, the 1.0712/24 area survived. USD/JPY tested he 148.8 resistance, but a clear break also didn’t occur yet.

This morning, Chinese equities (CSI 300 +3.0%) are rebounding as markets see more signs that authorities are stepping up efforts address the recent sell-off. Other Asian markets trade mixed to slightly lower on receding Fed rate cut expectations. US yields return a few bps on the recent rally. The dollar stabilizes. Later today, there are no important US data, but the Treasury will start its monthly refinancing with the sale of $ 54bln 3-year notes. In Europe, the ECB consumer expectations are worth keeping an eye on. Regarding markets, we look out whether interest rate markets can hold the recent rise or even take out the above-mentioned resistance levels without additional data evidence. Maybe some consolidation might kick in. Similarly, can the dollar take out nearby resistance as the rise in yields slows? For EUR/USD a less buoyant equity market or persistent euro weakness still might do the job.

News & Views

The Reserve Bank of Australia struck a slightly more hawkish tone than expected at its February policy meeting. It kept the rates steady at 4.35%, as expected, but highlighted lingering inflation risks, especially coming from the services sector. Prices in the latter eased more gradually than expected in November, contrasting developments in the goods area. This is in part due to a labour market tighter than what is consistent with sustained full employment and inflation at target, despite conditions having eased further. Both headline and core CPI in Q4 last year dropped more than the RBA foresaw but governor Bullock at the presser pushed back against those calling the November rate hike a mistake. Instead, both she and the RBA statement explicitly kept the option open for further tightening if needed. The twist comes even as GDP and CPI forecasts were revised down a little over the horizon. But inflation isn’t expected to reach the midpoint of the 2-3% target before 2026 though. Money markets stick to their pricing of a first cut by August. Australian swap yields spiked higher but forfeited gains shortly after. The Aussie dollar retains gains against an overall weaker USD this morning. AUD/USD rises towards 0.6508.

Total retail sales in January rose 1.2% y/y in January, the British Retail Consortium revealed this morning. A measure targeting same stores rose by 1.4%. Both represent a further easing from the festive period in November and December. As they are unadjusted for inflation, the slower pace along with tepid consumer demand also reflects easing price pressures. The BRC CEO noted that “Sales of big-ticket items such as furniture and household and electrical appliances remained poor” while food sales were a positive as British households stayed at home during two winter storms.

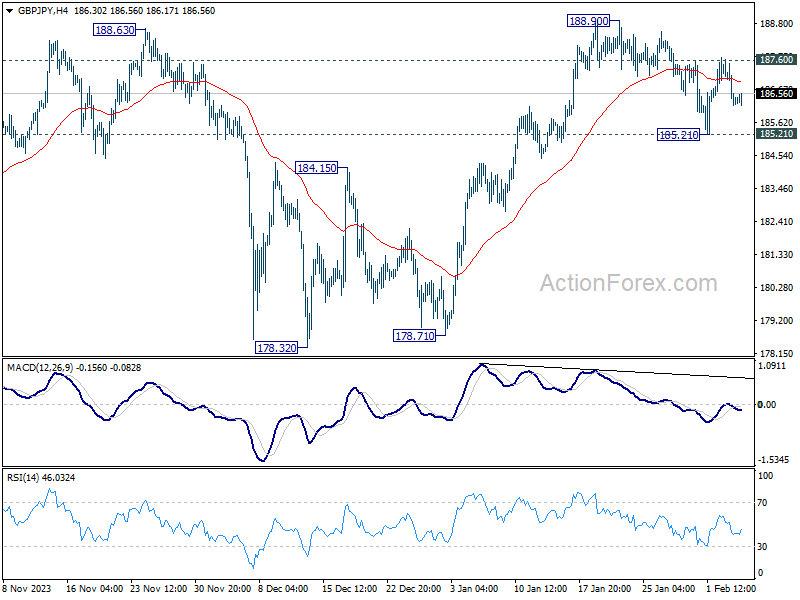

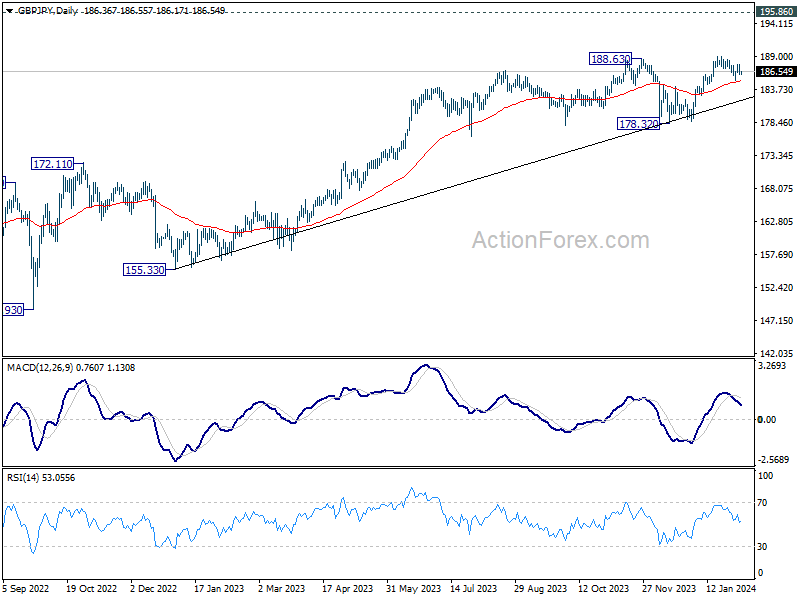

GBP/JPY Daily Outlook

Daily Pivots: (S1) 185.83; (P) 186.74; (R1) 187.31; More...

Range trading continues in GBP/JPY and intraday bias remains neutral for the moment. On the upside, firm break of 187.60 will turn bias to the upside for 188.90. Break there will confirm resumption of larger up trend. Meanwhile, below 185.21 will turn bias to the downside and extend the correction from 188.90.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

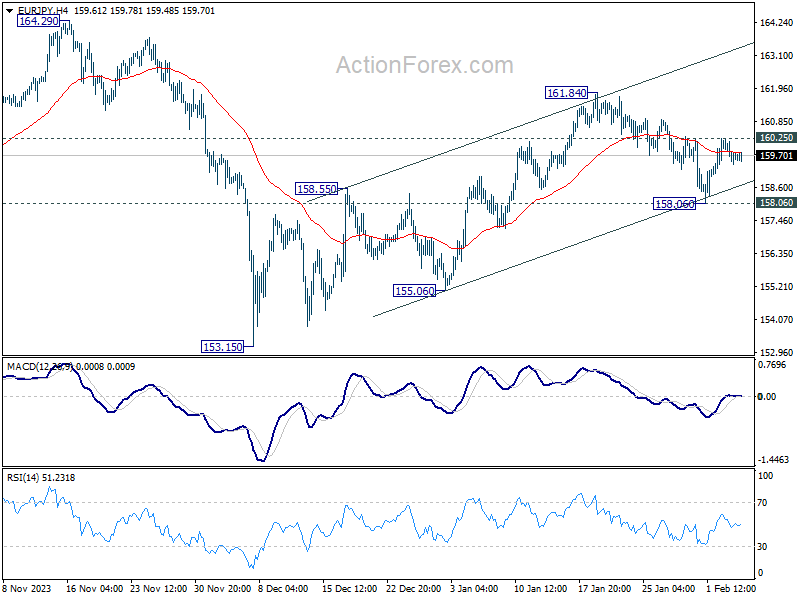

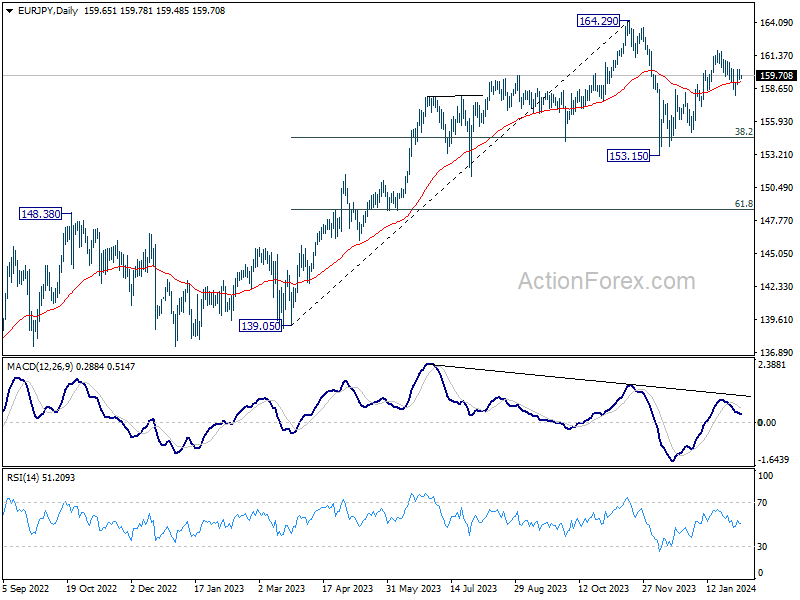

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.31; (P) 159.80; (R1) 160.20; More...

Intraday bias in EUR/JPY remains neutral with focus on 160.25 minor resistance. Decisive break there will indicate that rise from 153.15 is ready to resume, and turn bias back to the upside for 161.84 first. Nevertheless, break of 158.06 will now suggest that the rise from 153.15 has completed and turn bias back to the downside.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage.

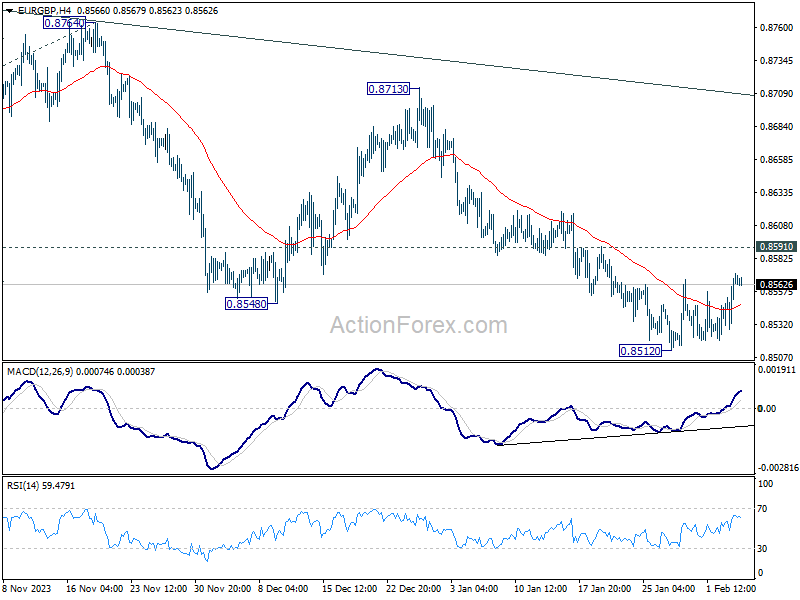

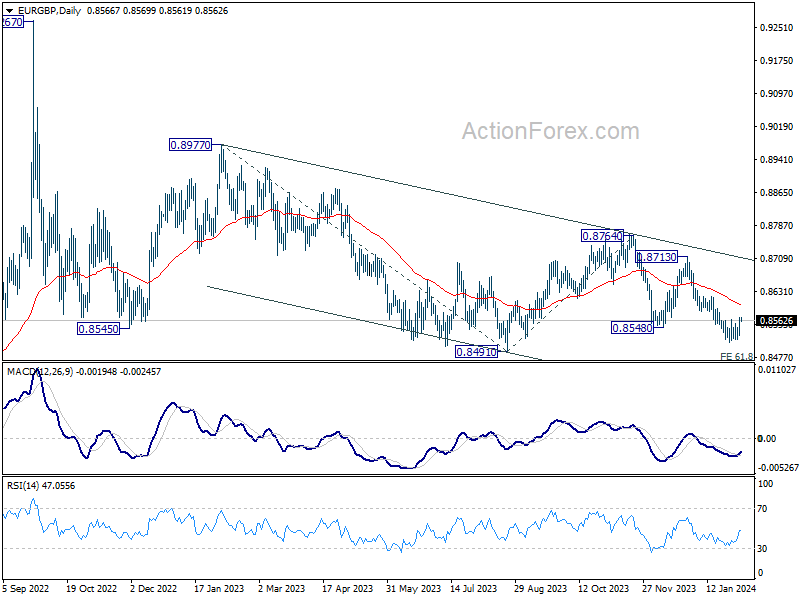

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8541; (P) 0.8557; (R1) 0.8584; More...

EUR/GBP is staying in range above 0.8512 and intraday bias remains neutral. Further decline is expected with 0.8591 resistance intact. On the downside, below 0.8512 will resume the fall from 0.8713 to 0.8491, and then 0.8464 projection level. However, firm break of 0.8591 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

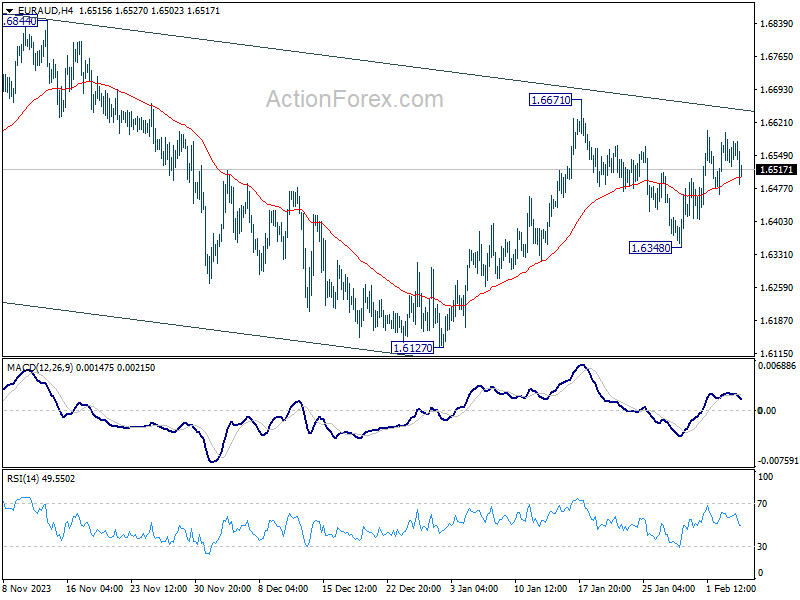

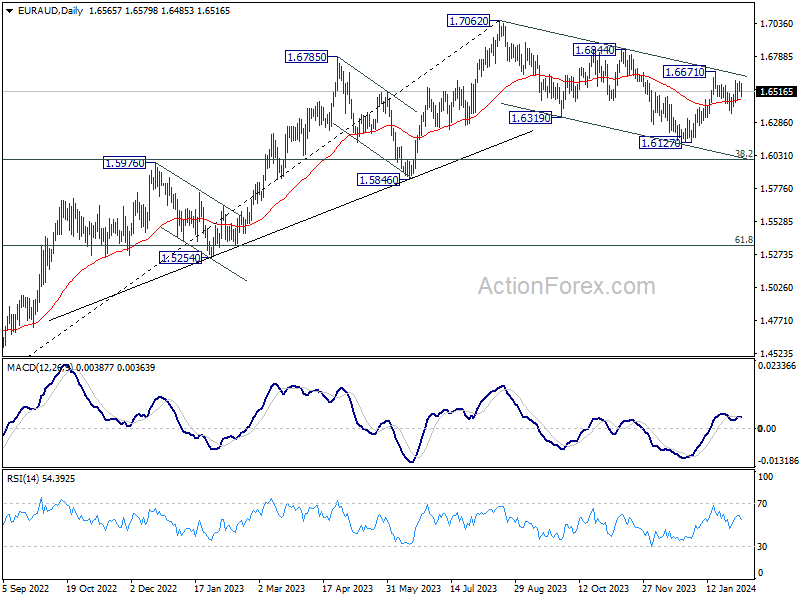

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6531; (P) 1.6566; (R1) 1.6607; More...

Range trading continues in EUR/AUD and intraday bias remains neutral. On the upside, decisive break of 1.6671 will revive the case that whole correction from 1.7062 has completed with three waves down to 1.6127. Further rally should then be seen to 1.6844 resistance for confirmation. Nevertheless, break of 1.6438 will bring deeper fall back to 1.6127 support instead.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

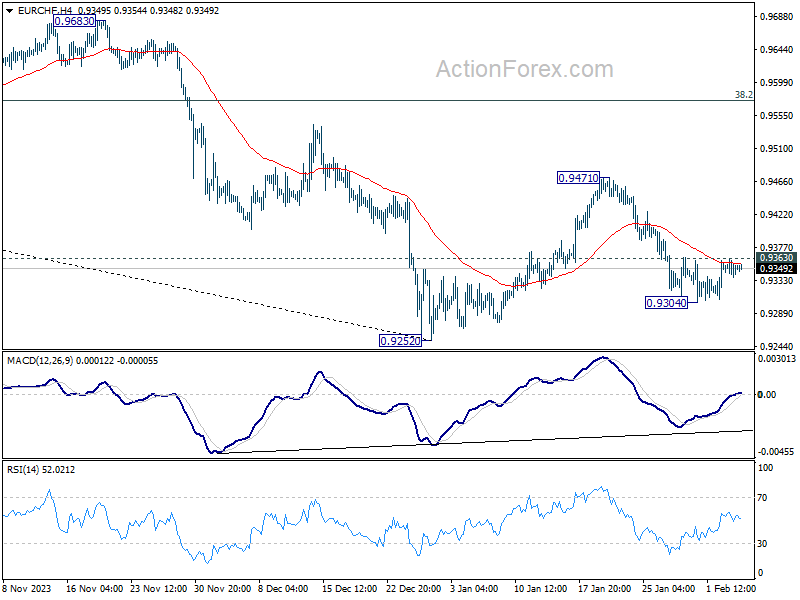

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9340; (P) 0.9352; (R1) 0.9365; More...

Intraday bias in EUR/CHF stays neutral at this point. Fall from 0.9471 might extend lower through 0.9304. But downside should be contained above 0.9252 low to bring rebound. On the upside, firm break of 0.9363 minor resistance will argue that the correction from 0.9471 has completed, and turn bias back to the upside for 0.9471 first.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). Further rise would be seen to 38.2% retracement of 1.0095 to 0.9252 at 0.9574. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.

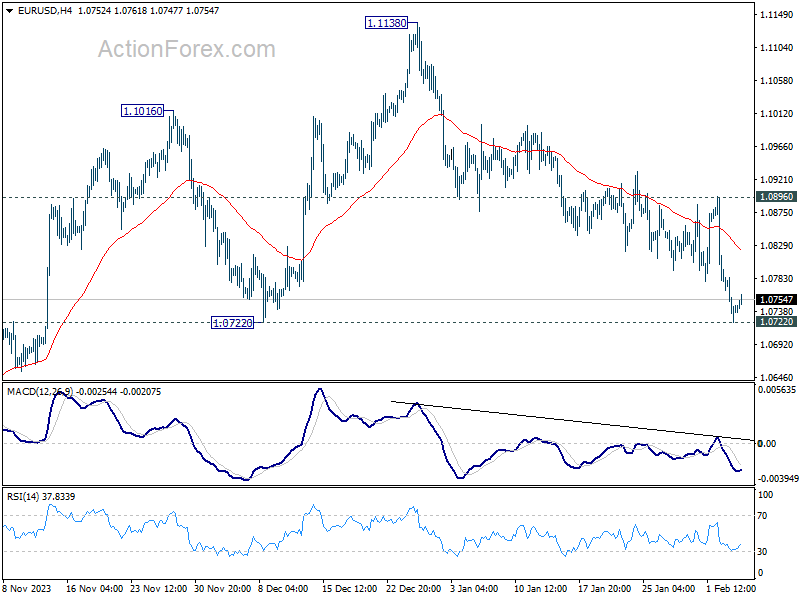

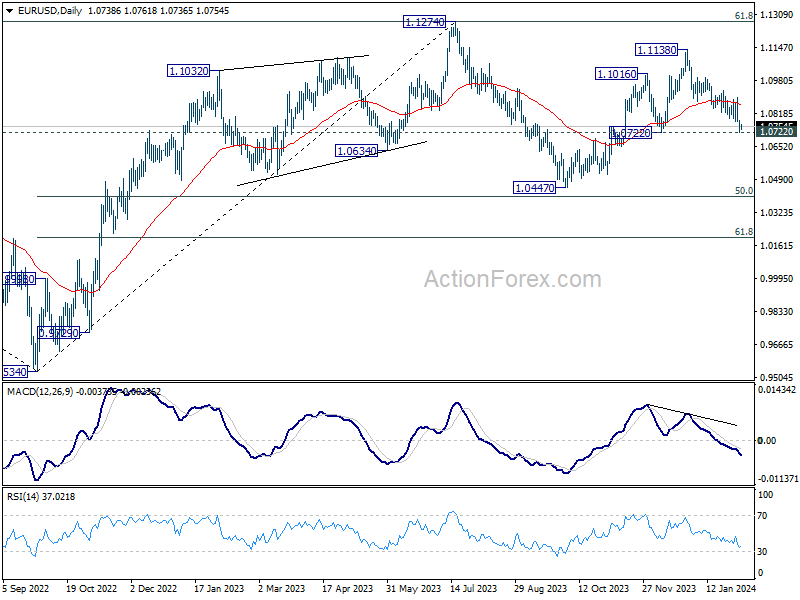

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0714; (P) 1.0751; (R1) 1.0778; More...

Intraday bias in EUR/USD remains on the downside, with focus on 1.0722 structural support. Decisive break there will argue that whole rise from 1.0447 has completed. Deeper fall would then be seen to target this low. On the upside, break of 1.0896 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

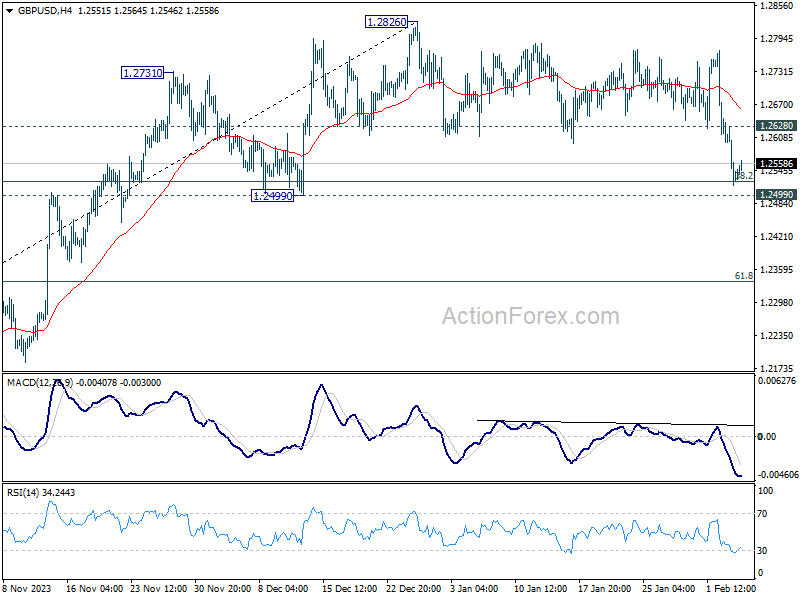

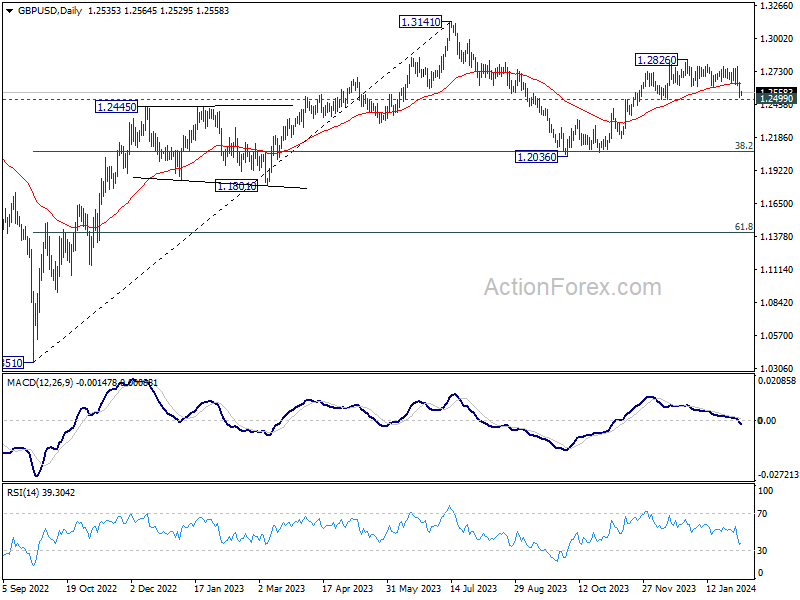

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2488; (P) 1.2566; (R1) 1.2614; More...

Intraday bias in GBP/USD remains on the downside at this point. Strong Support could be seen from 1.2499 structural support. Break of 1.2628 minor resistance will turn bias back to the upside for rebound. However, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's still in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

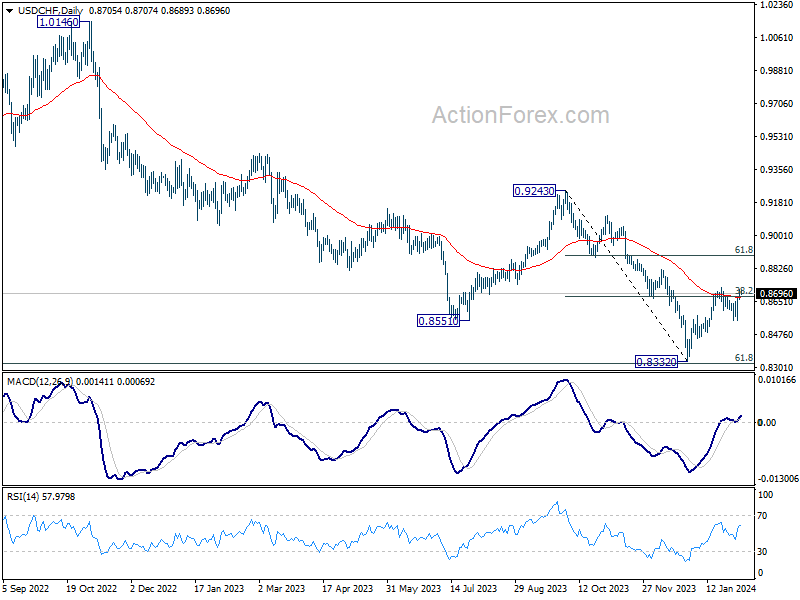

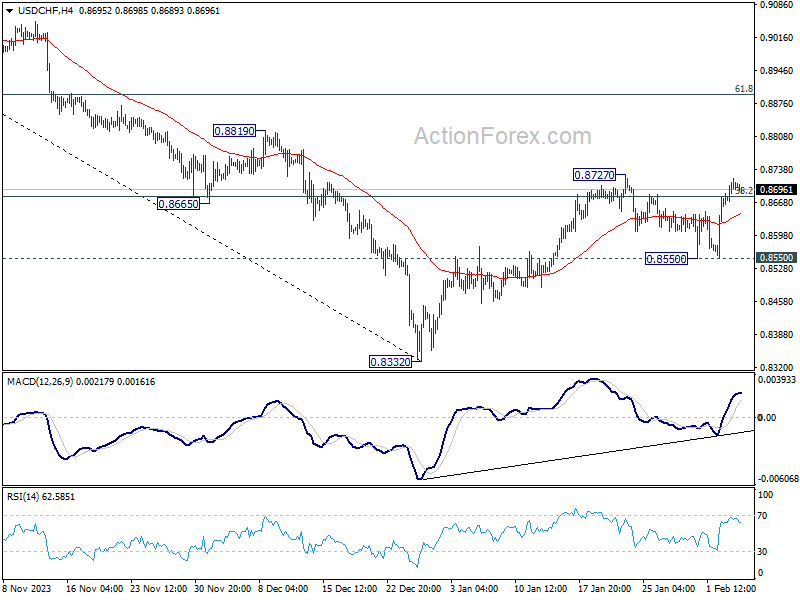

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8669; (P) 0.8694; (R1) 0.8731; More....

Intraday bias in USD/CHF remains neutral with focus on 0.8727 resistance. On the upside, decisive break of 0.8727 will resume the rebound from 0.8332, and target 61.8% retracement of 0.9243 to 0.8332 at 0.8995. On the downside, break of 0.8550 will turn bias back to the downside for retesting 0.8332 low instead.

In the bigger picture, there is prospect of medium term bottoming at 0.8332 considering possible bullish convergence condition in W MACD, and the support from 0.8317 long term fibonacci support. Sustained trading above 55 D EMA (now at 0.8672) will affirm this case, and bring stronger rise back towards 0.9243 resistance, even as a corrective move.