Sample Category Title

Is German Industry Ready for Revival?

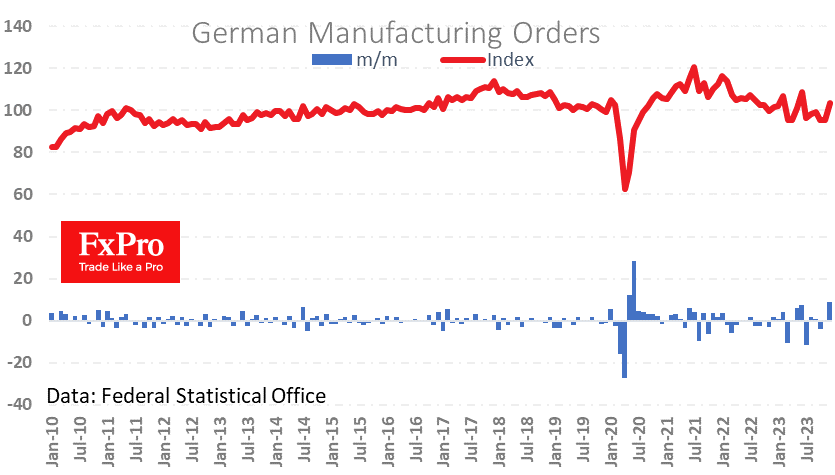

Industrial orders rose 8.9% in December against expectations for a 0.1% decline, a rare positive for Germany that the euro chose to ignore. This is the most robust monthly increase since mid-2020’s lockdowns.

In the same month last year, the increase was 2.7%. A positive year-over-year rate has been a rarity over the past two years, as a couple of spikes did not break the overall downtrend. Traders in European markets are likely looking for such an anomaly and ignoring today’s upbeat data. However, we may be seeing the result of a relatively long period of low gas prices, the effects of China’s stimulus and the economy’s adaptation after the inflationary shock.

So, suppose orders continue to rise next month. In that case, it promises to be a turnaround at a time when it seems that only the lazy have failed to talk about the deindustrialisation of the eurozone’s largest economy.

We will also be looking at German industrial production figures on Wednesday – will there be similarly strong growth? If so, markets may have rushed to bury the euro.

Japanese Yen Calm After Mixed Spending and Income Data

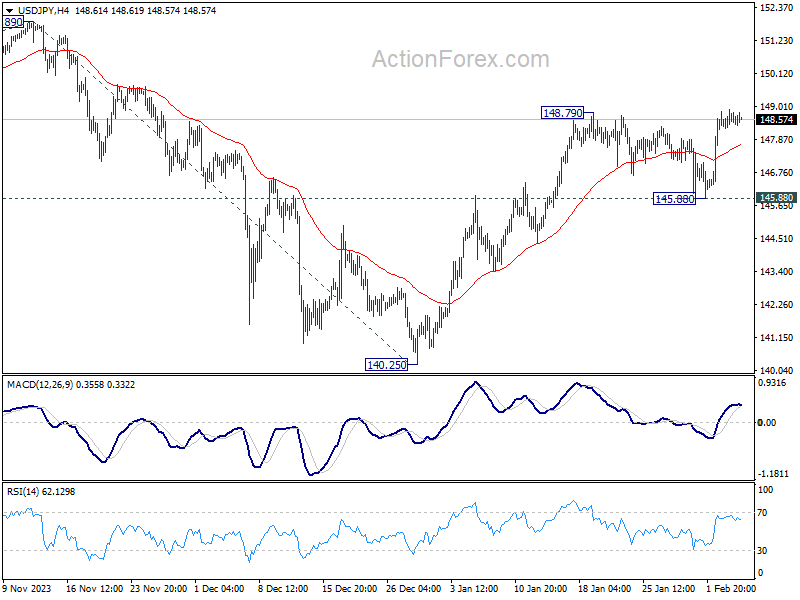

The Japanese yen is showing limited movement on Tuesday. In the North American session, USD/JPY is trading at 148.56, down 0.09%.

Japan released mixed data on Monday. Average Cash Earnings for December rebounded with a 1% gain, following a 0.2% gain in November. This was a strong reading but missed the market estimate of 1.3%. Household Spending can’t find its footing and posted a 10th straight decline, at -2.5% y/y. This followed the 2.9% drop in November and missed the market estimate of -2.1%.

Wage growth has become a key indicator as the Bank of Japan has stressed the need for higher wages before it will lift interest rates out of negative territory. The Bank hasn’t raised rates since 2007 and such a move would be a sea-change in monetary policy. The positive wage growth report is further evidence of stronger wage growth and there is speculation that the BoJ might could hit the rate trigger as soon as the April meeting. Japan’s annual wage negotiations started in January and there are reports that workers will win substantial wage hikes, which would raise expectations of a policy shift by the BoJ.

In the US, the Federal Reserve jumped on the rate-cut bandwagon in December but has continued to push back against market expectations. After the December meeting, the markets were licking their chops and priced in an initial rate cut in March but those expectations have steadily fallen as the US economy continues to perform well. Last week’s sizzling nonfarm payrolls was the latest example of the strength of the US economy. The Fed rate odds of a rate cut in March have fallen to 16%, while a June cut has been priced in at 95%, according to the CME FedWatch tool.

USD/JPY Technical

- USD/JPY is testing support at 148.62. Below, there is support at 148.33

- There is resistance at 148.96 and 149.25

Sunset Market Commentary

Markets

Core bonds, US Treasuries in particular, opened higher in an attempt to recoup some of the Powell-Payrolls-ISM triple whammy they suffered over the previous days. But US yields shedding between 0.1 and 3 bps across the curve is nothing compared to the 30bps+ they gained in just two trading days. Technically, the likes of the 2- and 10-year remain close to the (be it early) YtD (intraday) highs. A leap higher today was going to be difficult anyway given the lack of market moving events planned. We do note that some Fed speeches (Mester, Kashkari, Collins) are due after wrapping up the report as is the $54bn 3-year Note auction. Sticking to auctions, the Kingdom of Belgium announced a new syndicated benchmark bond (tomorrow), maturing June 2055. It’s the second out of three planned for this year with the remaining one having a medium-term maturity. The ECB’s December consumer inflation expectations survey is worth mentioning as well, despite leaving no traces whatsoever on markets. The series has been expanded with five countries and showed the one-year ahead gauge to have eased further from 3.5% (revised upwards for comparison reasons) to 3.2%. The three-year forward looking series ticked higher from 2.4% to 2.5% and remains above the 2% medium-term target, suggesting policymakers should rightly so not lower their guard just yet. Economic growth expectations for the next 12 months remained unchanged at -1.3% while expectations for the unemployment rate 12 months ahead decreased to 11.2%, from 11.4% in November. In terms credit access, the series hit a high, indicating increased tightness but consumers expect easier access in 12 months’ time than thought in November. German yields basically flatline with a minor underperformance at the long end within a 3 bps sideways trading range at the time of writing. Stocks inch about half a percent higher in Europe and open virtually unchanged on Wall Street.

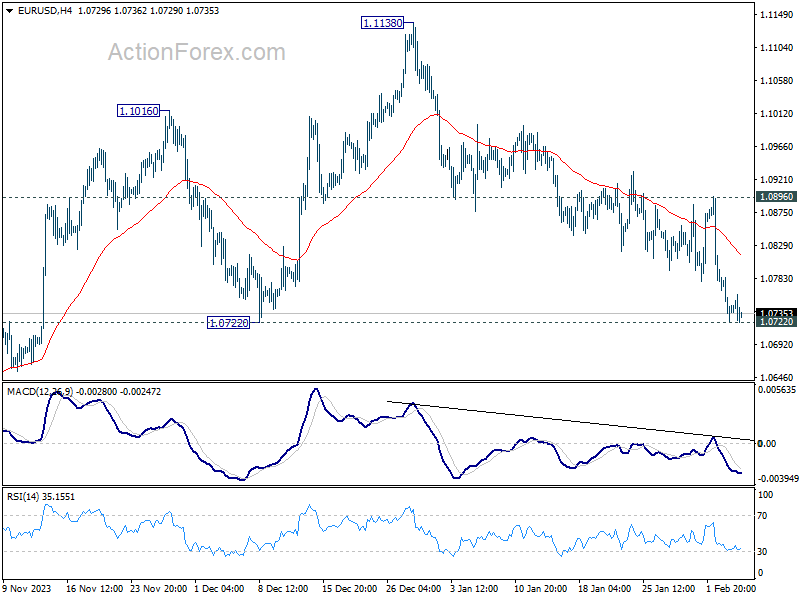

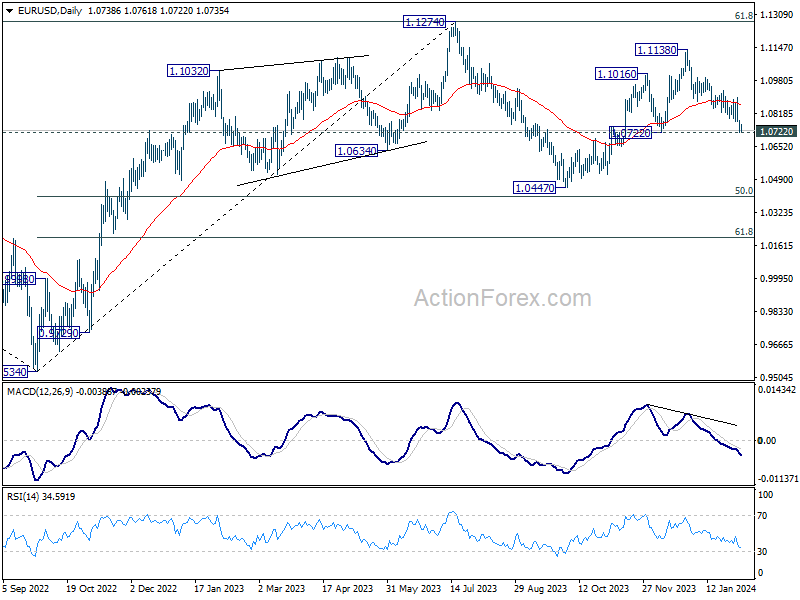

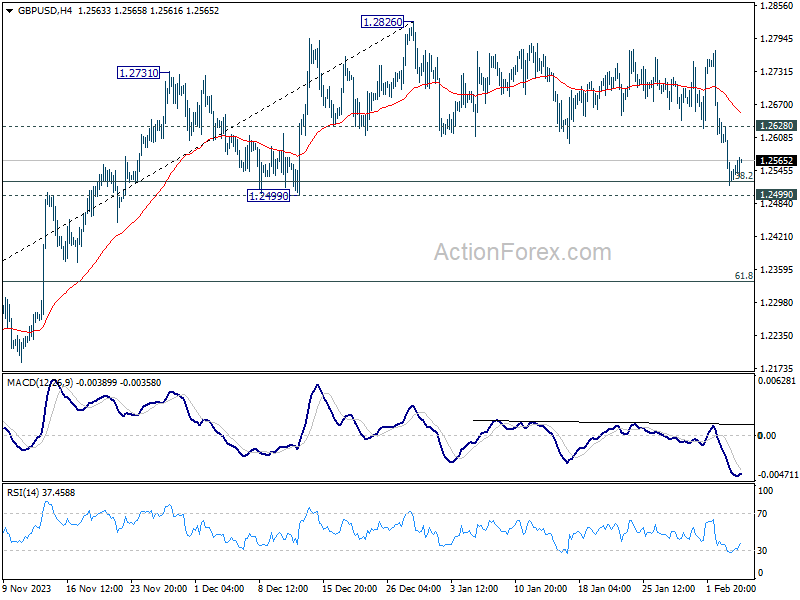

Currency markets show similar lack of guidance. Cable (GBP/USD) was perhaps the most interesting one to follow up after yesterday’s break below 1.26, which marked the lower bound of a sideways trading range in place since mid-December. Sterling prevented technical follow-through losses however. GBP/USD rises marginally to 1.256. The EUR/GBP mirror image shows the pair all but fully erasing yesterday’s uptick back to 0.854. The euro trades in the defensive against the dollar as well. EUR/USD eases further and prepares for the lowest close around 1.0735 since mid-November as the 1.0724/12 support area looms.

News & Views

Cocoa futures hit the highest level since 1977 ($5288 a metric ton) earlier this week, extending their astronomic surge since end 2022 ($2200 a metric ton). The latest 5% leap came after Ivory Coast government data suggested that farmers delivered less cocoa to local ports. Arrivals in the season that started October 1 totaled 1.04mn tons compared with an estimate of about 1.71mn a year ago. Production levels from neighboring country Ghana are way below last year’s levels as well with seasonal Harmattan winds – cool dry wind that blows from the northeast or east in the western Sahara and is strongest from late November to mid-March – drying out cocoa fields in both nations and further tightening global supply. Last year, Ivory Coast and Ghana were respectively responsible for 44% and 14% of global cocoa bean production.

Minutes of the previous policy meeting of the Brazilian central bank (BCB) confirmed the intention to cut policy rates at the following two meetings by 50 bps each, sticking with the pace in place since August of last year when the BCB started reducing its policy rate from a 13.75% peak level to currently 11.25%. The recap of the January meeting showed that the central bank will especially pay attention to developments in (sticky) services inflation and in a (temporary?) acceleration of real wage gains. Upside inflation risks related to weather events like El Nino have been downscaled. The Brazilian economy slowed last year, but high frequency indicators suggest a better start to this year. When it comes to future policy decisions, the BCB distances itself from future monetary policy and rate decisions by the Fed. There’s no mechanical link between the two. USD/BRL yesterday tested the psychologic 5 mark which is also this year’s YTD high on genuine USD strength. The attempt has been blocked for now.

NZD/USD Calm Ahead of NZ Job Data

- New Zealand’s job growth expected to rise to 0.2%

The New Zealand dollar is showing limited movement on Tuesday. Early in the North American session, NZD/USD is trading at 0.6052, down 0.03%.

New Zealand job growth expected to rebound

New Zealand releases the fourth-quarter employment report later today. Employment is expected to rebound with a 0.3% gain, after a decline of 0.2% in the third quarter, which was the first decline in over three years. The unemployment rate is expected to rise to 4.2%, up from 3.9% in the third quarter.

The Reserve Bank of New Zealand will be keeping a close eye on the job numbers as it charts its rate path. The RBNZ has kept the cash rate unchanged at 5.5% for five straight times, which likely means that its steep rate-tightening cycle has run its course. That has the markets hunting for clues of a rate cut, which is expected later in the year.

At the most recent meeting in late November, the RBNZ had a hawkish message for the markets, warning that inflation remained too high and if it rose unexpectedly, the central bank would “likely need to increase further”. I’m doubtful that the RBNZ is really planning to raise rates, barring a shock where inflation moves higher. The RBNZ’s aim may be to pour cold water on rate-cut expectations and allow high rates to continue to push inflation lower.

If key data such as the upcoming employment report are solid, it will provide the RBNZ with more room to continue to keep rates in restrictive territory. Conversely, weak job numbers would raise pressure on the RBNZ to lower rates in order to boost economic growth.

NZD/USD Technical

- NZD/USD is putting pressure on resistance at 0.6150. Above, there is resistance at 0.6211

- There is support at 0.6054 and 0.5993

ECB’s Vujcic: We need some patience now

In an interview with Reuters, ECB Governing Council member Boris Vujcic emphasized the need for "patience" in the current monetary policy environment. He acknowledged the positive disinflationary trends observed so far. However, "we still see also quite a lot of resilience in the services and what we call domestic inflation," he noted.

The ECB official also underscored the importance of cautious decision-making, referencing an IMF paper that cautioned against central banks declaring victory over inflation prematurely. Vujcic emphasized, "I don't think we should risk such a mistake."

On the topic of rate cuts, Vujcic downplayed the significance of timing, suggesting that a month or two's difference in the decision to reduce rates "doesn't really make that much difference", especially given that a serious recession now seems unlikely.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0714; (P) 1.0751; (R1) 1.0778; More...

No change in EUR/USD's outlook and intraday bias stays on the downside. Focus remains on 1.0722 structural support. Decisive break there will argue that whole rise from 1.0447 has completed. Deeper fall would then be seen to target this low. On the upside, break of 1.0896 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

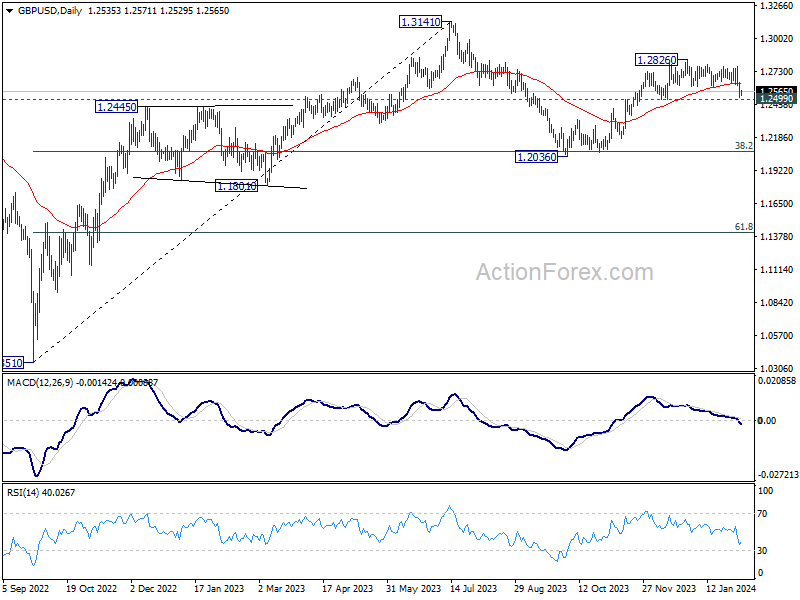

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2488; (P) 1.2566; (R1) 1.2614; More...

No change in GBP/USD's outlook and intraday bias remains on the downside. Strong support could be seen from 1.2499 structural support. Break of 1.2628 minor resistance will turn bias back to the upside for rebound. However, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's still in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

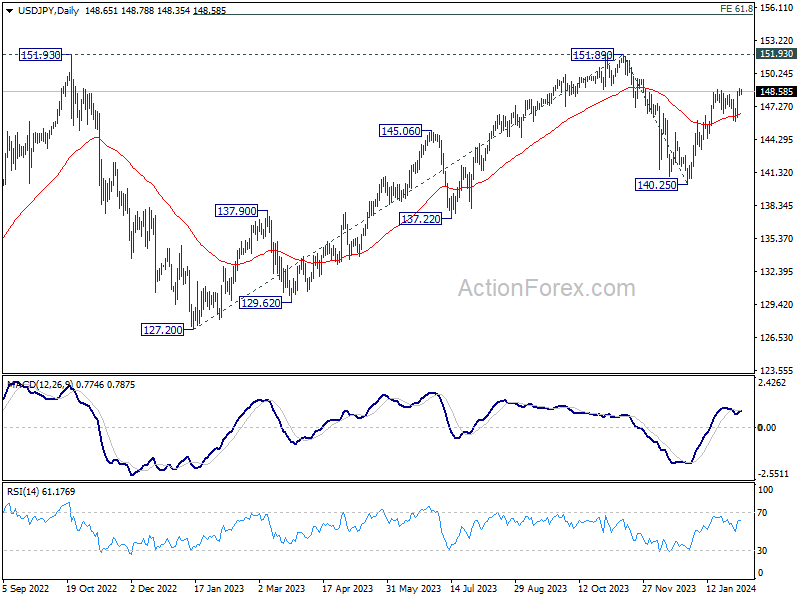

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.33; (P) 148.62; (R1) 148.96; More...

No change in USD/JPY's outlook as intraday bias stays neutral. Focus stays on 148.79 resistance. Firm break there will resume the rally from 140.25 to 151.89/93 key resistance zone. For now, further rise will remain in favor as long as 145.88 holds, in case of retreat.

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.

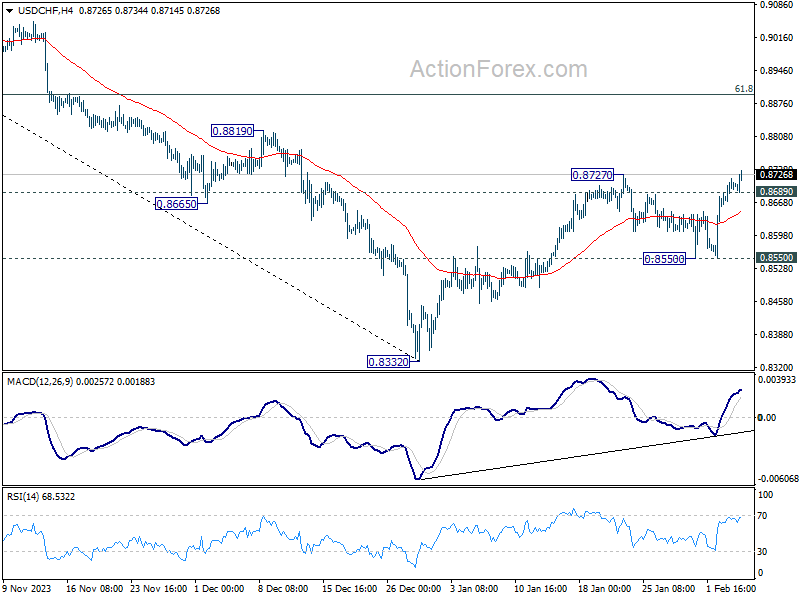

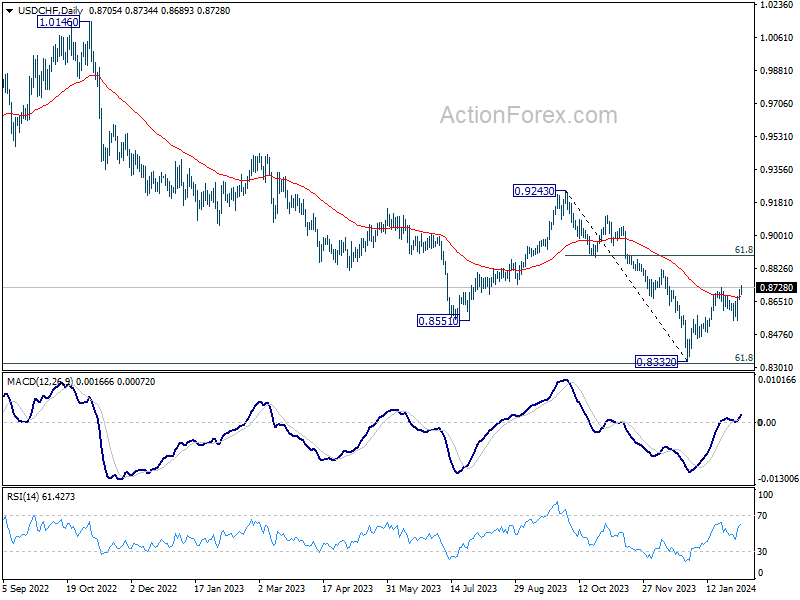

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8669; (P) 0.8694; (R1) 0.8731; More....

Break of 0.8272 resistance suggest that USD/CHF's rebound from 0.8332 is resuming. Intraday bias is back on the upside. Further rally should be seen to 61.8% retracement of 0.9243 to 0.8332 at 0.8995 next. On the downside, below 0.8689 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 0.8550 support holds, in case of retreat.

In the bigger picture, there is prospect of medium term bottoming at 0.8332 considering possible bullish convergence condition in W MACD, and the support from 0.8317 long term fibonacci support. Sustained trading above 55 D EMA (now at 0.8672) will affirm this case, and bring stronger rise back towards 0.9243 resistance, even as a corrective move.

Dollar in Consolidation Mode as Kiwi Eyes Upcoming NZ Job Data

Dollar is largely in a state of consolidation today, except with a minor uptick observed against Swiss Franc. In the absence of significant economic data from the US, market participants are poised to gauge the sentiment from forthcoming comments by Fed officials. However, the broader market dynamics, particularly the interplay with other financial markets, could play a more pivotal role in shaping the greenback's next. 10-year yield, nearing the upper echelon of its near-term range at 4.2%, might begin to taper off, while the stock markets are teetering on the edge of a mild pullback after struggling to sustain their record runs. These factors of countering forces could keep trading in Dollar sluggish for a while.

In the wider forex arena, Australian Dollar emerges as the day's strongest performer, albeit with a recovery that appears to lack conviction. Neither RBA's marginally hawkish posture nor the uplift from Chinese stock markets seems to provide Aussie with lasting momentum. British Pound, on the other hand, is solidifying its position as the second strongest, seemingly undeterred by dovish remarks from a known BoE dove. Meanwhile, Euro and the Swiss Franc are languishing alongside Dollar, whereas Yen displays mixed performance. Economists see that Japan's robust base pay growth could keep BoJ on a course towards rate hikes later in the year.

NZD/USD is worth some attention with New Zealand job data scheduled for the upcoming Asian session. The rejection by 55 D EMA is a near term bearish sign. Rebound from 0.5771 has possibly completed at 0.6368 already. Sustained break of 61.8% retracement of 0.5571 to 0.6368 at 0.5999 will strengthen that case that it's trying to resume whole down trend from 0.6537. For now, risk will stay on the downside as long as 0.6172 resistance holds, in case of recovery.

In Europe, at the time of writing, FTSE is up 0.71%. DAX is up 0.26%. CAC is up 0.50%. UK 10-year yield is down -0.0126 at 3.994. Germany 10-year yield is up 0.010 at 2.330. Earlier in Asia, Nikkei fell -0.53%. Hong Kong HSI rose 4.04%. China Shanghai SSE rose 3.23%. Singapore Strait Times fell -0.27%. Japan 10-year JGB yield rose 0.0022 to 0.723.

BoE Dhingra urges not to take risk on the economy

In a Financial Times interview, BoE MPC member Swati Dhingra articulated her concerns regarding the UK's economic outlook and inflationary trends. As the sole member to vote for a rate cut in the last meeting, she cautioned against underestimating the downside risks and and urged not to take a risk on them.

Dhingra expressed apprehension about the adverse impacts of past policy tightening on growth, emphasizing the paradox of experiencing "higher-than-historic rates" of wage growth against the backdrop of significantly weakened consumption, which has declined by 5.9% relative to pre-pandemic levels.

This stark drop in consumption, according to Dhingra, is expected to persist, highlighting the "lagged effects" of monetary policy tightening yet to materialize fully. She questioned the rationale behind risking further economic weakening by maintaining high-interest rates when inflation appears to be on a "sustainable path."

The conversation further delved into the challenges posed by the current consumption weakness, which Dhingra believes is unlikely to reverse swiftly enough to trigger a "resurgence in inflation".

Her comments reflect a deeper concern over underestimating the downside risks to the economy, especially as the financial cushion provided by pandemic-era savings begins to diminish. Additionally, the noticeable decline in job vacancies signals further strain on the real economy.

"I don't see why we should be risking that," Dhingra emphasized.

Eurozone retail sales falls -1.1%mom, EU down -1.0%

Eurozone retail sales fell -1.1% mom in December, worse than expectation of -1.0% mom. Volume of retail trade decreased by -1.6% mom for food, drinks and tobacco, by -1.0% mom for non-food products and by -0.5% mom for automotive fuels.

EU retail sales fell -1.0% mom. Among Member States for which data are available, the largest monthly decreases in the total retail trade volume were registered in Slovenia (-3.6%), Denmark (-3.2%) and Luxembourg (-3.1%). The highest increases were observed in Slovakia (+2.0%), Croatia and Hungary (both +1.4%) as well as in Portugal (+0.7%).

ECB consumer survey reveals declining inflation expectations

ECB's Consumer Expectations Survey for December highlighted a noteworthy trend in consumer sentiment regarding inflation and economic growth.

In a positive development, consumers' inflation expectations for the next 12 months have decreased for the third consecutive month, with median inflation expectation falling to 3.2%, a drop from November's 3.5% and October's 4.0%.

Conversely, the survey indicated a slight uptick in medium-term inflation expectations, with three-year ahead inflation expectations median rising marginally from 2.4% to 2.5%, although this figure remains below 2.6% observed in October.

On the economic growth front, the survey's findings were relatively stable, with mean growth expectation for the next 12 months remaining unchanged at -1.3%. Furthermore, the survey revealed a slight improvement in unemployment outlook, with expected mean unemployment rate declining from 11.4% to 11.2%, compared to 11.6% in October.

RBA stands pat, eases hawkish stance without shifting to neutral

RBA maintained cash rate target at 4.35%, aligning with broad market expectations. The hawkish stance has seen a slight moderation, with the acknowledgment that "a further increase in interest rates cannot be ruled out," hinting at a cautious approach rather than a definitive shift towards a neutral bias.

The updated economic forecasts paint a picture of gradual moderation in inflation pressures. Headline CPI is expected to decelerate from 4.1% at the end of 2023 to 3.2% by the close of 2024, reaching 2.8% at the end of 2025, and further softening to 2.6% by mid-2026.

Trimmed mean CPI mirrors this downward trend, projected to ease from 4.2% at the end of 2023 to 3.1% by the end of 2024, and gradually declining to 2.8% by December 2024, and then 2.6% by June 2026.

Additionally, RBA's outlook for cash rate assumes a decrease to 3.9% by the end of 2024, followed by a further reduction to 3.4% by the end of 2025, and eventually reaching 3.2% by mid-2026. This assumption aligns with the expectations derived from surveys of professional economists and financial market pricing.

On the growth front, RBA projects a modest GDP expansion of 1.8% in 2024, with an improvement to 2.3% in 2025.

Japan's labor cash earnings rises 1% yoy, with regular Pay at fastest pace since May

Japan saw a modest improvement in labor cash earnings in labor cash earnings, which increased by 1.0% yoy, accelerating from November's 0.7% gain. Despite this uptick, the growth fell short of anticipated 1.3% yoy.

A notable positive development was observed in regular pay, which rose by 1.6% yoy, marking the highest reading since May 2023. Additionally, special payments saw a marginal increase of 0.5% yoy, although overtime pay experienced a decline of -0.7% yoy.

With CPI standing at 3.0% yoy, real wages saw a decline of -1.9% yoy, albeit at a slower pace compared to -2.5% yoy observed in the previous month. This marks the slowest decline in real wages since June 2023, suggesting a slight easing in the pressure on household incomes.

However, this positive note is tempered by the latest household spending figures, which saw a -2.5% yoy drop, worse than the expected -2.1% yoy.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8669; (P) 0.8694; (R1) 0.8731; More....

Break of 0.8272 resistance suggest that USD/CHF's rebound from 0.8332 is resuming. Intraday bias is back on the upside. Further rally should be seen to 61.8% retracement of 0.9243 to 0.8332 at 0.8995 next. On the downside, below 0.8689 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 0.8550 support holds, in case of retreat.

In the bigger picture, there is prospect of medium term bottoming at 0.8332 considering possible bullish convergence condition in W MACD, and the support from 0.8317 long term fibonacci support. Sustained trading above 55 D EMA (now at 0.8672) will affirm this case, and bring stronger rise back towards 0.9243 resistance, even as a corrective move.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Dec | 1.00% | 1.30% | 0.70% | |

| 23:30 | JPY | Household Spending Y/Y Dec | -2.50% | -2.10% | -2.90% | |

| 03:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% | 4.35% | |

| 04:30 | AUD | RBA Press Conference | ||||

| 07:00 | EUR | Germany Factory Orders M/M Dec | 8.90% | 0.30% | 0.30% | 0.00% |

| 09:30 | GBP | Construction PMI Jan | 48.8 | 47.2 | 46.8 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Dec | -1.10% | -1.30% | -0.30% | 0.30% |

| 13:30 | CAD | Building Permits M/M Dec | -14.00% | 1.20% | -3.90% | -5.00% |

| 15:00 | CAD | Ivey PMI Jan | 55 | 56.3 |