Sample Category Title

Chinese Investors Still Ponder Impact of Authorities to Arrest Equity Sell-off

Markets

Amid a very thin eco calendar, core bonds yesterday found some relief after the self-off that started with Powell’s push back against early rate cuts last Wednesday, reinforced by an exceptionally strong payrolls report and solid services ISM afterwards. Technical considerations also were in play with YTD top levels in yields at several maturities nearby (both in the US and in EMU). Fed Mester said she expects the Fed to get confidence to cut rates later this year, but at the same time indicated that policy currently is in a good place and that it would be a mistake to cut rates too soon. She still holds to the December to plot, expecting three rate cuts this year. She didn’t seem in a hurry to reduce the pace of the balance sheet roll-off. Minneapolis Fed Kashkari also took notice of the progress that has been made on inflation but also maintained the mantra that the Fed didn’t reach its goal yet. This kind of balanced comments understandably were not enough to push yields beyond key resistance levels. Bond gradually gained traction. The $54 bln 3-y US Treasury action also went smoothly on recent cheapening. US yields finally eased between 7.4 bps (5-y) and 3.7 bps (30-y). Moves in Bund yields were more modest, declining between 1.0 bp and 2.5 bps across the curve. US equity indices held near recent peak levels (S&P 500 +0.23%). The Eurostoxx50 even touched a new multi-year top (+0.76%). Easing global yields and a mild risk sentiment also capped the ascent of the dollar. The DXY index struggles to hold above the 104.00/25 previous resistance area (close 104.21). EUR/USD for a second consecutive day tested the 1.0724 December correction low, but in the end the 1.0712/24 support survived (close 1.0755). Cable tries to reverse Monday’s break below 1.26 range bottom (close 1.2598). EUR/GBP also reversed part of Monday’s rebound to close at 0.8637.

Asian equities mostly trade with modest gains this morning. Chinese investors still ponder the impact of the authorities to arrest the equity sell-off (CSI 300 +0.63%). Later today, there are again few data with market moving potential in US and EMU. We look out whether there are any further spill-overs of Moody’s cutting the rating of New York Community Bancorp to junk to broader (US) equity sentiment. Fed speakers include governors Kugler, Collins, and Barkin. In an interview with the FT, ECB Executive Board Member Isabel Schnabel warned that lower borrowing costs could cause inflation to flare up again, given a good reason against the ECB adjusting the policy stance hastily. Regarding trading today, it probably will remain difficult for yields to break above YTD peak levels without any high profile news. The dollar rally also slows but given underlying euro weakness, at test of the EUR/USD 1.0712/24 remains possible.

News & Views

New Zealand employment grew a faster-than-expected 0.4% q/q in Q4 2023. This followed a contraction by 0.1% in Q3. The unemployment rate ticked higher to 4%, matching the post-GFC and pre-pandemic high. The small uptick was nevertheless smaller than analysts (4.3%) foresaw, partially due to an unexpected decline in the participation rate to 71.9%. Both employment growth and the unemployment rate were also better than the Reserve Bank of New Zealand expected in its November forecasts. Combined with wages easing more slowly (to 3.9% y/y vs 3.8% expected) and stubborn (non-tradeable/services) CPI, it may prevent the central bank from dropping its hawkish bias and turn more neutral when it meets on February 28. The kiwi dollar reacted stoic to the labour data. USD/NZD is going nowhere just north of 0.61. New Zealand swap yields do add more than 5 bps at the front.

The Japanese government’s chief economist Hayashi said the Bank of Japan can retain its focus on beating deflation even if it were to phase out its ultra-easy monetary policy that still includes negative policy rates. The current BoJ framework is based on a 2013 pledge with the government to achieve the 2% inflation target “at the earliest date possible”. That has now come into question several times since inflation has been above 2% for more than a year now, prompting speculation of a near-term exit from the current policy stance. A positive wage-inflation cycle is critical for the BoJ to do so. According to Hayashi, this will be the case if this year’s wage growth, for which negotiations are ongoing, exceeds that of last year. The government as a result formally declaring an end to deflation could trigger further expectations for such a BoJ shift.

A Tug of War Between Hawks and Doves

The selloff in US sovereign bonds reversed yesterday after a solid demand for the US 3-year bond auction counterweighed a bulk of hawkish comments from Federal Reserve (Fed) members.

The Fed members are on the battlefield, fighting the doves. Loretta Mester said there is no rush to cut rates and Neel Kashkari said that the Fed hasn’t reached its inflation goal yet. The game is now being played for a May cut, with around two thirds probability attached to it.

And there is one thing that keeps the doves resisting: the resurfacing US regional bank worries and a potential commercial real estate crisis. The New York Community Bank Corp plunged another 22% on Tuesday after Moody’s downgraded its rating to ‘junk’. What’s encouraging is that the KBW index gave no reaction to the latest shake, as proof that the Fed has been extremely successful in isolating the banking sector woes with liquidity and stopgap measures. What’s worrying is that these measures will expire next month. But what’s soothing is that the Fed could use them whenever needed to calm down the market nerves. Investors also bear in mind that the next move from the Fed is most probably loosening of financial conditions – that should help the sector as a whole. And the sole expectation of easing Fed is enough to juice the market’s mouth. This is certainly why the New York Community Bancorp’s misfortune hasn’t triggered a domino effect across the banking sector, and the winds could turn around before a crisis pops in the problematic real estate sector. That’s happy news.

Happy enough to push the S&P500 index a little higher yesterday as one regional bank extended its weekly losses to 50%. In the bright spot was Palantir – a data analytics company, jumped 30% after announcing AI-related revenue earlier than thought. Their commercial revenue soared by 70% compared to the same time last year as the deal flow rose to a level that no one expected before 2025.

Elsewhere, Snap fell 32% in the afterhours trading after disappointing Q4 revenue, but it’s too small to care, and BP, in London, flirted with the 200-DMA after revealing higher than expected profits, and saying that it will buyback $1.75bn worth of shares each quarter in the H1, more than the $1.5bn buyback announced a quarter earlier. Worth noting: BP posted strong first results under its new CEO, giving the company a certain margin to stick to its strategy of shifting toward renewable energy sources rather than boosting investment in fossil fuel and gas (for which they are being forced by investors because there is more money in fossil fuel and gas). And if things go wrong, BP can scrap its promise to do good to the planet and go back to doing good to investors pockets.

Hope is life

The CSI 300 index is up for the 3rd straight session on broad-based stimulus measures and anticipation for more as Xi Jinping is being briefed on ‘the heck is going on’ in the financial markets. To be true, I would love to be a fly in that room to see how officials are going to tell Xi that his radical change of mindset is responsible for the mess, and not the lack of money, or love for Chinese companies.

Confidence is low and the economy is fragilized by a deepening property crisis, falling population and deflation. China is expected to post a deeper y-o-y deflation when it reveals its latest CPI figures tomorrow. The market's response may vary depending on investors' perceptions of the effectiveness of the stimulus measures. A deeper than expected deflation could boost the stimulus expectations and help stocks recover – in which case it could be an early sign of returning confidence. OR it would smash the latest stock market gains and leave the Chinese authorities desperate for support. Pick your side.

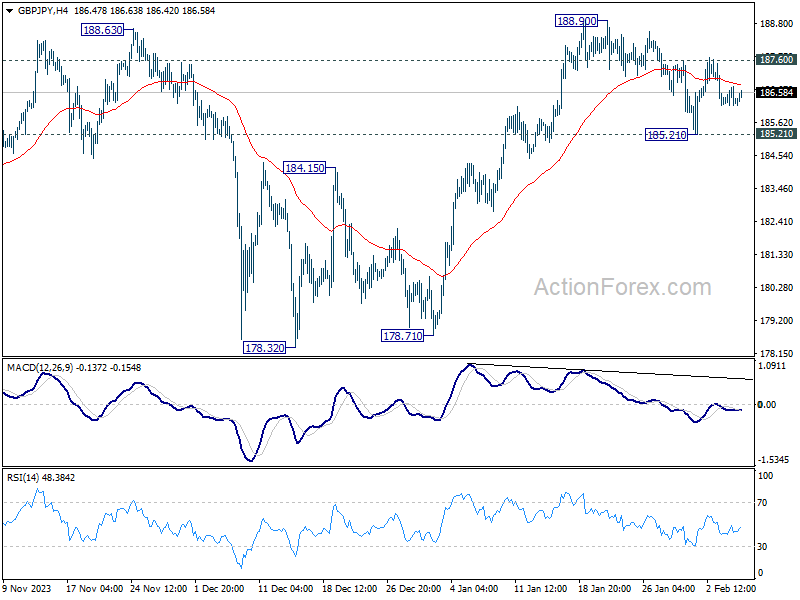

GBP/JPY Daily Outlook

Daily Pivots: (S1) 186.12; (P) 186.45; (R1) 186.71; More...

Intraday bias in GBP/JPY remains neutral and outlook is unchanged. On the upside, firm break of 187.60 will turn bias to the upside for 188.90. Break there will confirm resumption of larger up trend. Meanwhile, below 185.21 will turn bias to the downside and extend the correction from 188.90.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

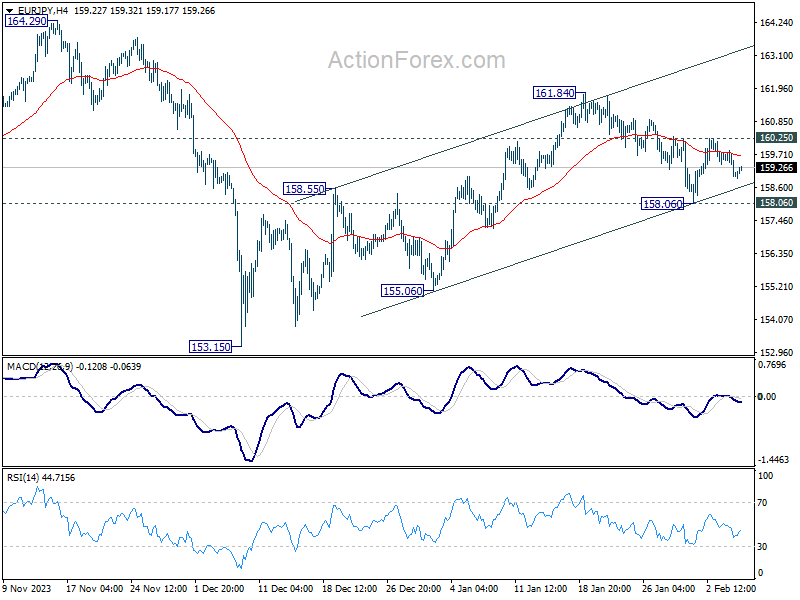

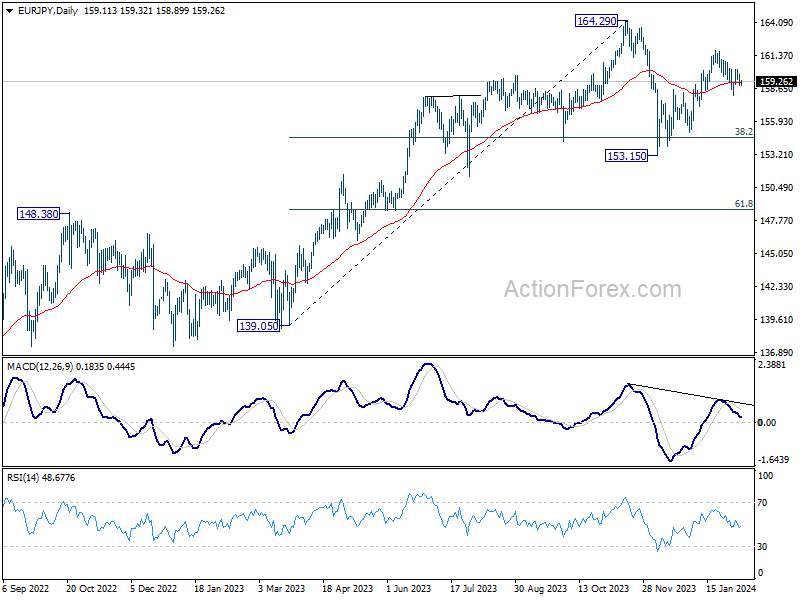

EUR/JPY Daily Outlook

Daily Pivots: (S1) 158.76; (P) 159.32; (R1) 159.66; More...

No change in EUR/JPY's outlook and intraday bias remains neutral. On the upside, decisive break of 160.25 resistance will indicate that rise from 153.15 is ready to resume, and turn bias back to the upside for 161.84 first. Nevertheless, break of 158.06 will now suggest that the rise from 153.15 has completed and turn bias back to the downside.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage.

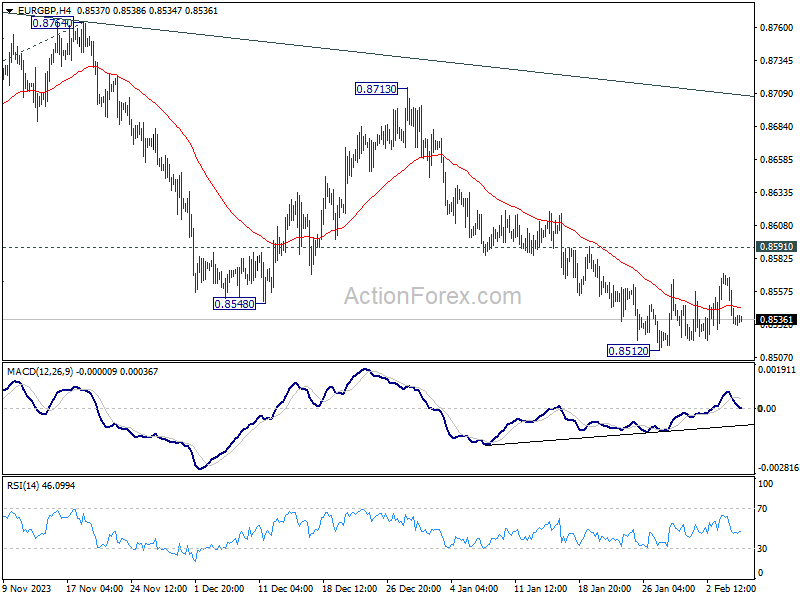

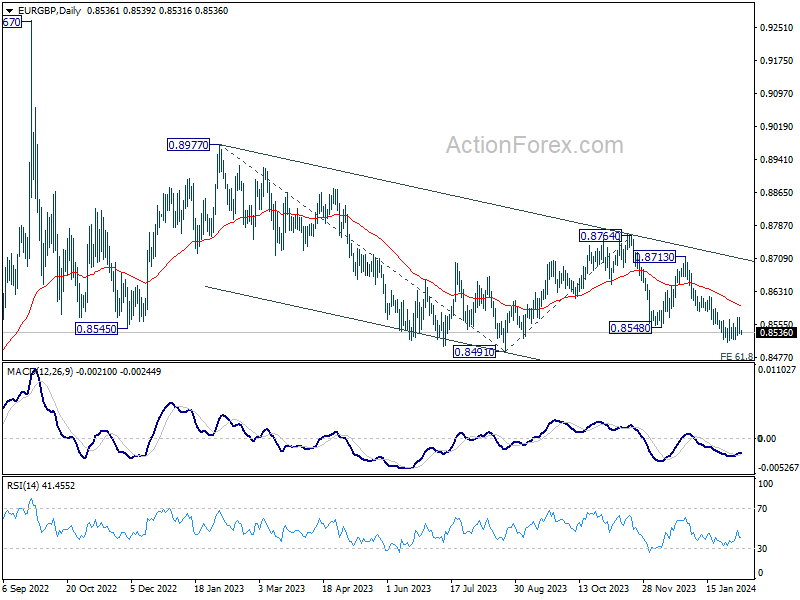

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8522; (P) 0.8548; (R1) 0.8563; More...

Intraday bias in EUR/GBP stays neutral as sideway trading continues. Further decline is expected with 0.8591 resistance intact. On the downside, below 0.8512 will resume the fall from 0.8713 to 0.8491, and then 0.8464 projection level. However, firm break of 0.8591 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

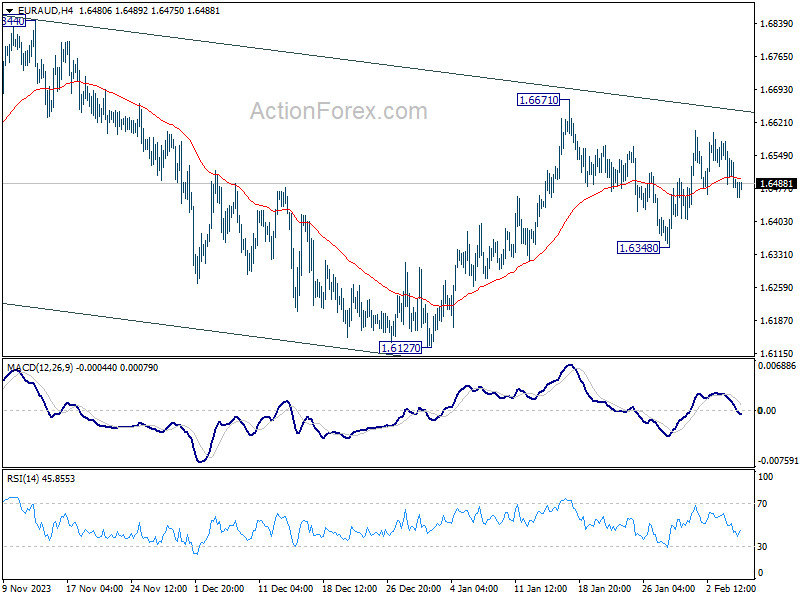

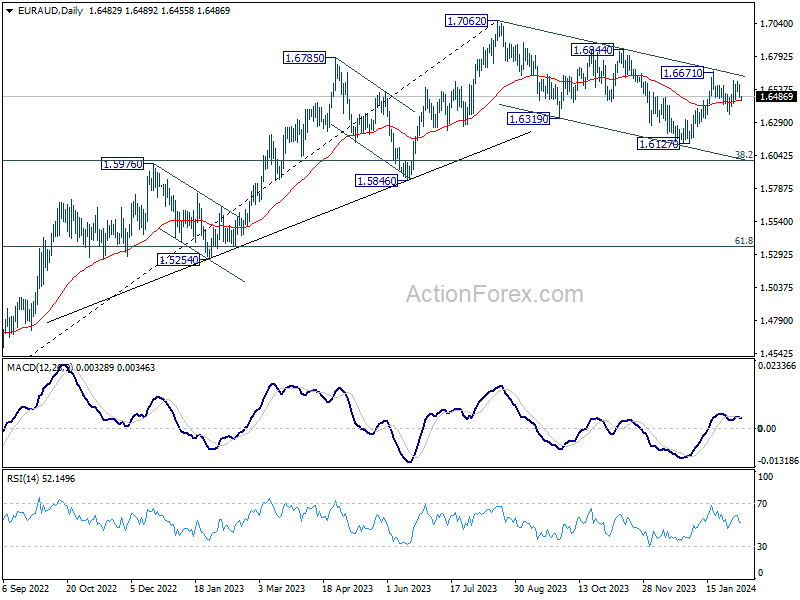

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6452; (P) 1.6516; (R1) 1.6552; More...

Intraday bias in EUR/AUD stays neutral as sideway trading continues. On the upside, decisive break of 1.6671 will revive the case that whole correction from 1.7062 has completed with three waves down to 1.6127. Further rally should then be seen to 1.6844 resistance for confirmation. Nevertheless, break of 1.6438 will bring deeper fall back to 1.6127 support instead.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

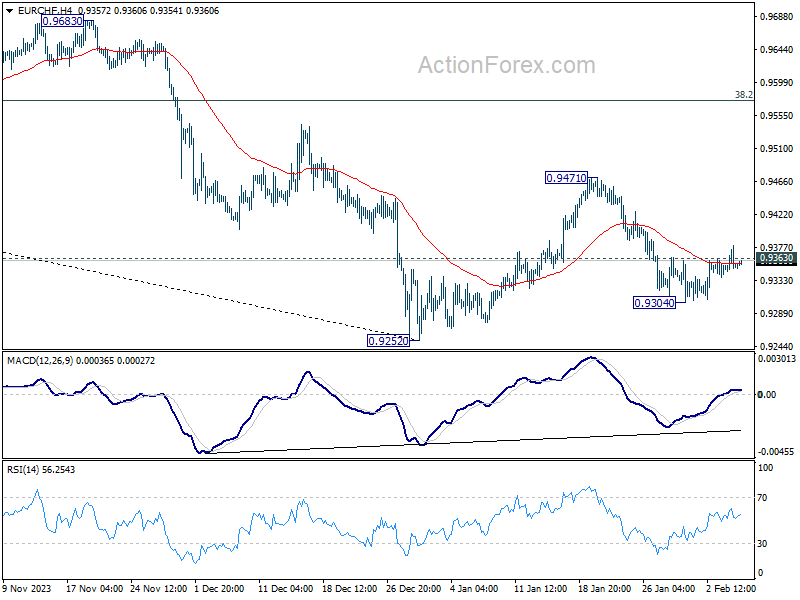

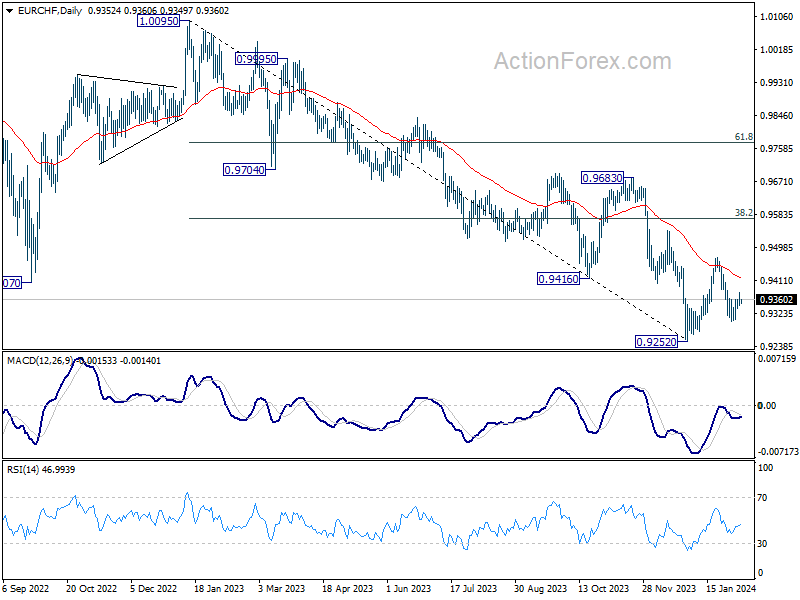

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9340; (P) 0.9361; (R1) 0.9375; More...

Intraday bias in EUR/CHF is mildly on the upside with breach of 0.9363 minor resistance. Pull back from 0.9471 could have completed at 0.9304 already. Rise from there would extend to 0.9471 resistance first. On the downside, break of 0.9304 will resume the fall from 0.9471 instead. But still, downside should be contained above 0.9252 low to bring rebound.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). Further rise would be seen to 38.2% retracement of 1.0095 to 0.9252 at 0.9574. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.

German Factories Orders Get Boost from Major Airplane Orders

In focus today

The Polish central bank announces its base rate at 14.30. We expect them to maintain their current rate level of 5.75%.

Early Thursday morning, Chinese CPI and PPI for January is released, and set to show another deflation print on the headline and thus continue the downbeat news flow out of China. Consensus looks for a -0.5% y/y print for headline CPI. It is partly driven by food prices, though, and we still do not see broad based declines in CPI ex food and energy, which is running at 0.6% y/y. But we might see a decline in core CPI inflation this time as the base from January 2023 may have seen a lift from the reopening after lockdowns.

Riksbank Minutes are released 09.30 CET. We expect a repetition from a majority of members that they are set to start cutting rates in June/July, moving in "cautious" steps from there (which we have interpreted as 25 bps cut at each "big" monetary policy meeting). Supposedly they will emphasize that inflation needs to be at 2% and on a stable trajectory. There could be some push-back on pricing given that 50bp cuts are priced in for H1. One hour later, 10.30 CET, Governor Thedeén speaks at Eesti Pank in Tallin.

Focus is on German industrial production data from December. The data will likely be weak as GDP declined 0.3% q/q in 2023Q4. Yet, it will be interesting to see how actual production fared in December as soft indicators have shown improvements.

US Secretary of State Anthony Blinken is visiting Israel where he will be discussing a proposed cease fire deal. Hamas had yesterday given a "positive response" to the deal.

Fed's Barkin and Bowman speak at 18.30 and 20.00 respectively.

Economic and market news

What happened overnight

It has been a rather quiet night with no major events.

What happened yesterday

In Germany, factory orders for the month of December rose unexpectedly by 8.9% m/m compared to consensus expectations of -0.2%. The big jump was however largely due to some major orders related to airplane manufacturing. Looking past these orders, factory orders fell 2.2% m/m, which also appears more in line with German GDP shrinking 0.3% q/q in 2023Q4.

In the euro area, retail sales for the month of December showed a drop of 1.1% m/m in line with consensus expectations. The drop was rather broad based hence the December print points to the euro area consumers still being cautionary with personal spending, as they have been throughout 2023.

In the US, an appeal court found that Donald Trump did not have immunity in the case of whether he tried to overturn the 2020 presidential election result. A Bloomberg poll of 31 January found that 53% of voters in key swing states would refuse to vote for him if found guilty of a criminal offense before the November presidential election. Trump vowed to appeal the decision.

Equities: Global equities rose yesterday without any particular news to set the direction for equities. As yields dropped, the focus on central bank reprising faded which was enough to bring back the positive sentiment in equities led by the small caps. Tech did underperform and the equal-weight S&P outperformed the official index. Interestingly, there haven't been the same focus on magnificent seven so far this year despite the tech sector has been outperforming year to data.

In US yesterday Dow +0.4%, S&P 500 +0.2%, Nasdaq +0.1% and Russell 2000 +0.9%. Asian markets are mixed this morning but with less intraday vol than we have been witnessing lately. US and European future also showing marginal change to yesterdays close.

FI: On a very uneventful day, market attention turned towards Moody's downgrade of NYCB (to junk) and the concerns surrounding the US commercial real estate market. Government bond yields in the US and Europe fell by a couple of basis points across the curve as markets added to rate cut expectations for 2024-25. German ASW-spreads continued tightening throughout the day.

FX: The USD pulled back from twelve-week highs as yields slipped amid further concerns regarding regional banks. Scandies thrived in said climate, with EUR/SEK and EUR/NOK both falling ten figures on the day, the exception being DKK with EUR/DKK rising above 7.4600 on the back of a deal announced by Novo.

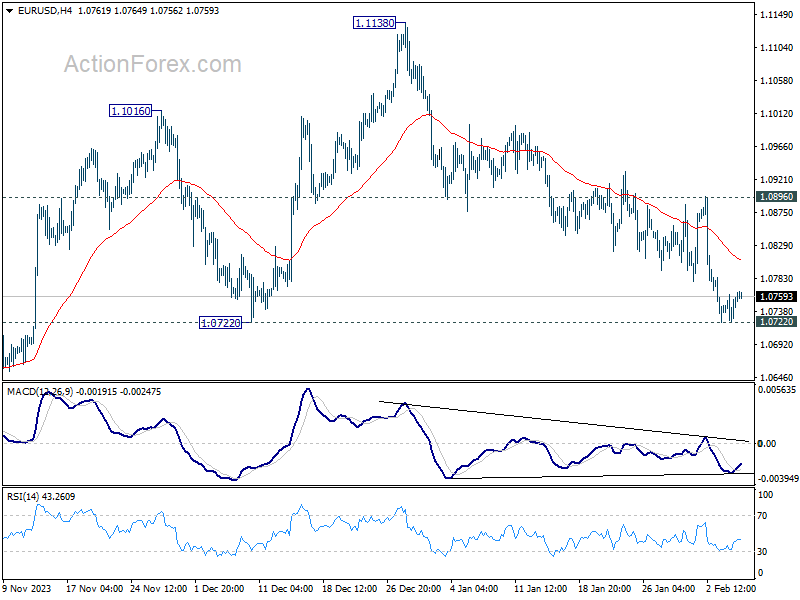

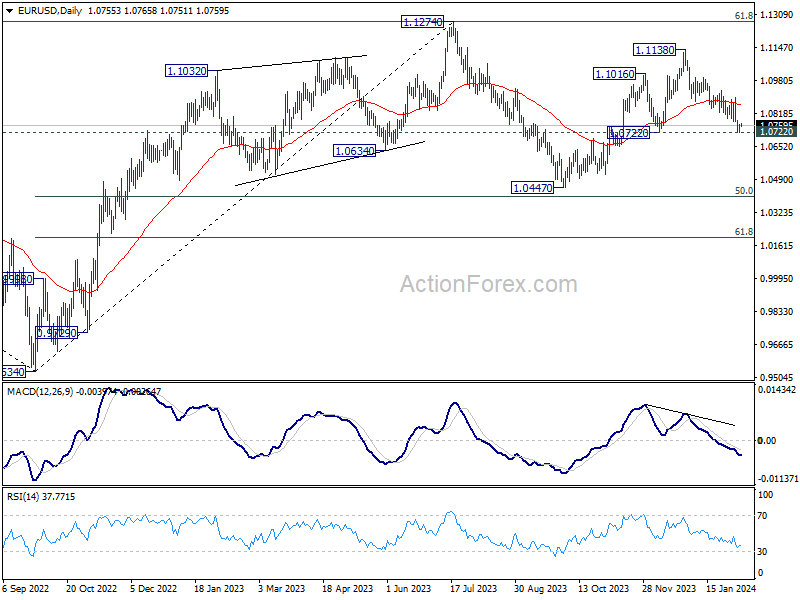

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0731; (P) 1.0746; (R1) 1.0770; More...

Intraday bias in EUR/USD is turned neutral first with current recovery. Focus remains on 1.0722 structural support. Decisive break there will argue that whole rise from 1.0447 has completed. Deeper fall would then be seen to target this low. On the upside, break of 1.0896 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

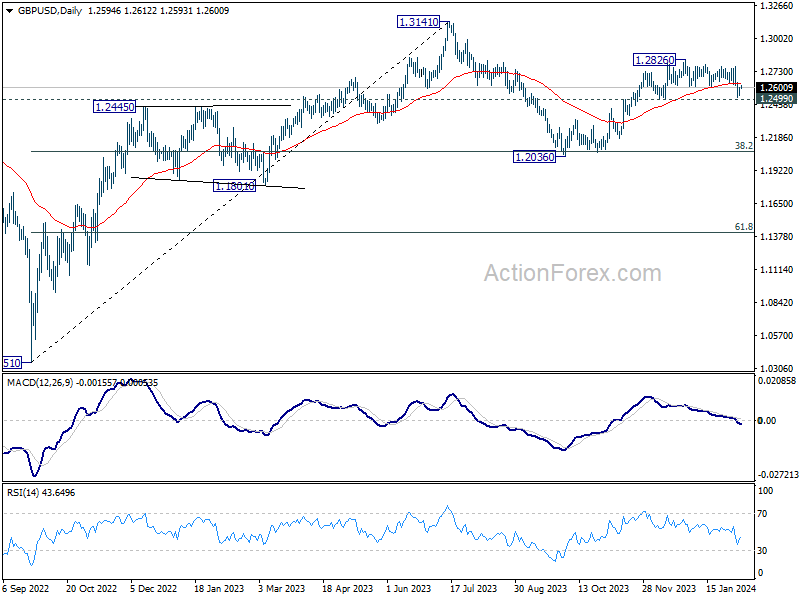

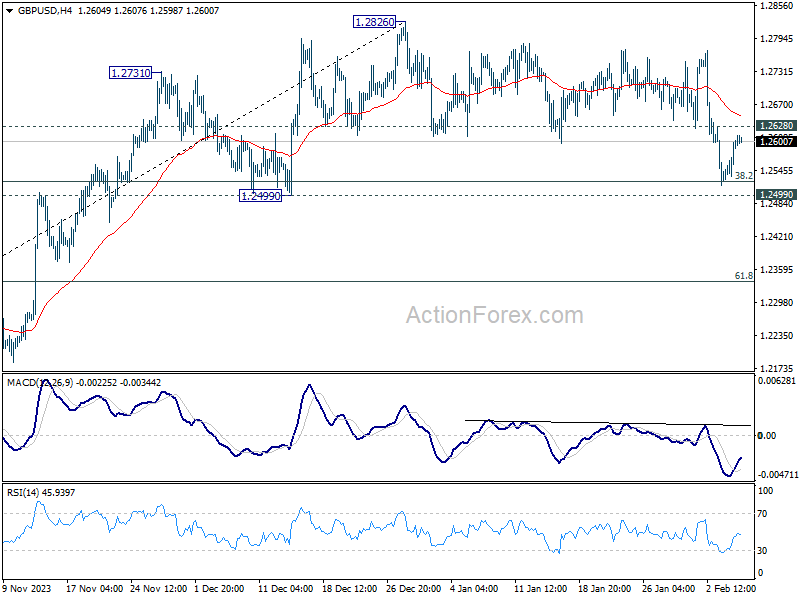

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2551; (P) 1.2577; (R1) 1.2624; More...

Intraday bias in GBP/USD is turned neutral first with current recovery. Strong support could be seen from 1.2499 structural support to complete the correction from 1.2826. Break of 1.2628 minor resistance will turn bias back to the upside for strong rebound. However, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's still in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.