Sample Category Title

XAU/USD: Gold Remains in Prolonged Consolidation Before Larger Bulls Resume

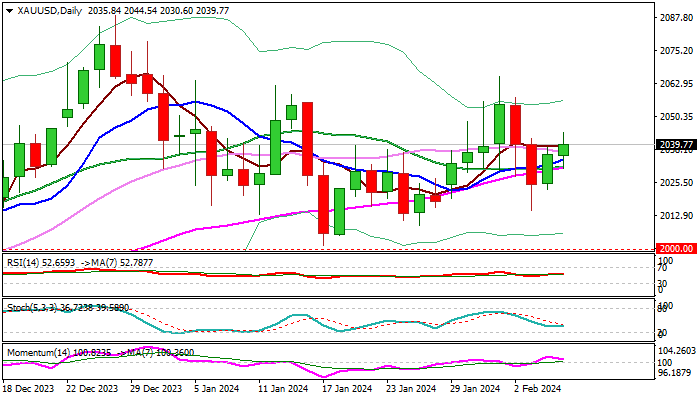

Short-term action remains in a sideways mode after the metal’s price spiked to new record high ($2141) in early December, holding within $1973/$2088 range, but mainly above psychological $2000 level, which adds to positive bias.

Gold is consolidating after Oct-Dec 2023 18% advance, a part of larger uptrend from $1616 (Nov 2022 higher low) with strong prospects for further gains, as growing global geopolitical tensions, economic uncertainty and signals that the Fed considers interest rates cuts later this year, continue to keep demand for safe-haven bullion steady.

The price is likely to continue to fluctuate within current range, awaiting fresh signals from fundamental side as technical studies on all larger timeframes remain bullishly aligned and contribute to positive outlook.

Gold can rise towards Fibonacci projections at $2206/26, on firm break of $2141 peak, with extension towards $2300 zone expected on stronger acceleration.

Res: 2056; 2065; 2088; 2100

Sup: 2014; 2009; 2000; 1985

Australia & New Zealand: What’s Up For The Down Under Economies?

Summary

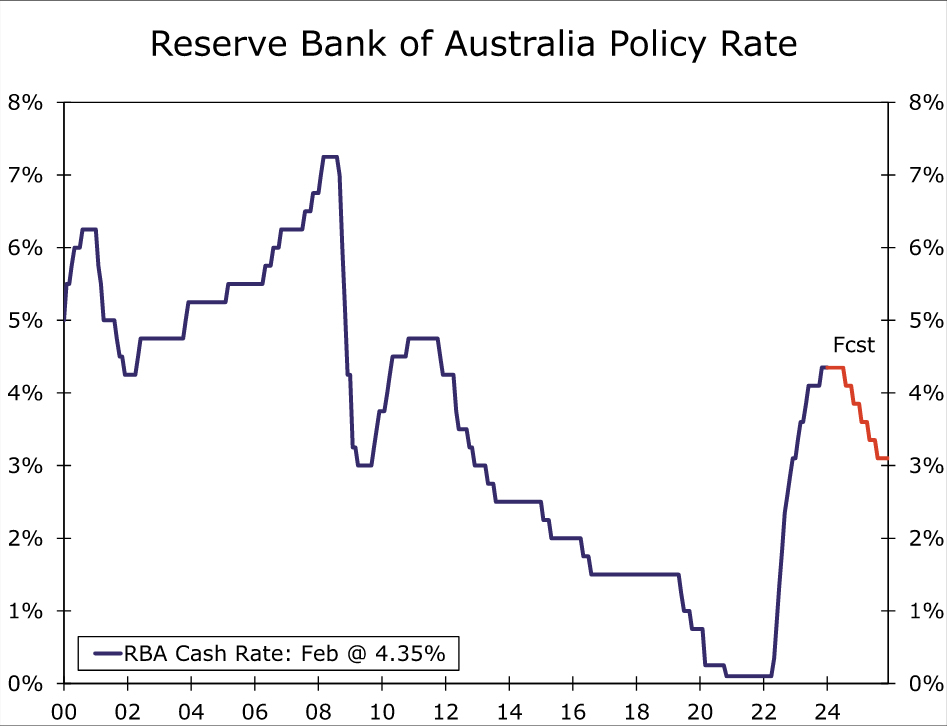

- The Reserve Bank of Australia (RBA) held its policy rate steady at 4.35% this week as expected, and its accompanying announcement was more hawkish than expected. The RBA did not rule out a further increase in interest rates, saying inflation—especially services inflation—is still high.

- We do not expect a further RBA rate increase, but with the central bank forecasting above-target inflation for an extended period, we believe rate cuts are some way off. We anticipate an initial 25 bps rate cut at the August meeting, while also acknowledging the balance of risks as tilted toward a later move.

- In New Zealand, improving sentiment surveys suggest the economy is moving toward recovery after a challenging 2023, while domestically oriented inflation pressures remain elevated. That backdrop is contributing to a continued hawkish stance from the Reserve Bank of New Zealand, which has not ruled out further rate hikes and said there is a way to go before inflation returns to target. We now see RBNZ rate cuts occurring later than previously envisaged, and forecast an initial 25 bps reduction at the August announcement.

- Against a backdrop of a U.S economic slowdown and Fed easing, a more gradual pace of rate cuts from the RBA and RBNZ could offer some support to the Australian and NZ dollars against the greenback over time.

Hawkish Hold From the Reserve Bank of Australia

The Reserve Bank of Australia (RBA) held its policy interest rate at 4.35% at this week's meeting, as widely expected. While acknowledging slower growth and improving inflation trends, the RBA is nonetheless clearly wary of reducing interest rates prematurely. This is reflected in several elements of its announcement:

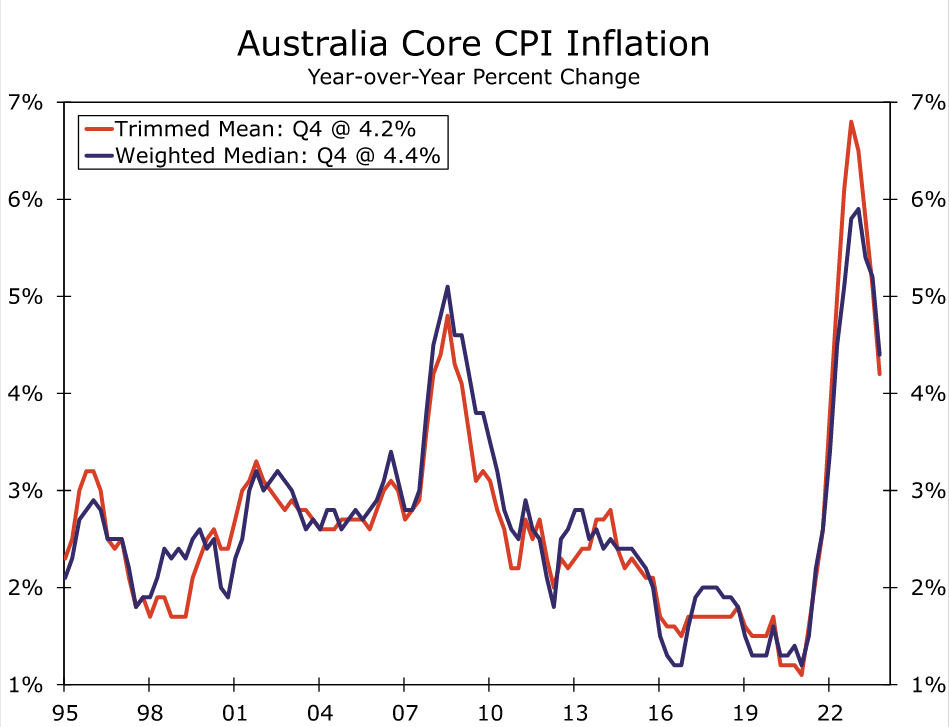

- Inflation remains high at 4.1 per cent. Goods inflation has slowed, but services inflation has declined at a more gradual pace, consistent with continuing excess demand and strong domestic cost pressures.

- The RBA remains highly attentive to inflation risks.

- While conditions in the labor market continue to ease gradually, they remain tighter than is consistent with sustained full employment and inflation at target.

- The RBA expects it will be some time yet before inflation is sustainably in the target range of 2%-3%. The path of interest rates that will best ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks, and a further increase in interest rates cannot be ruled out.

Importantly, therefore, the RBA kept the possibility of a rate increase on the table, even as it lowered both its GDP growth and CPI inflation forecasts. With respect to economic activity, the RBA now forecasts annual average GDP growth of 1.5% for 2024, down from the 1.8% it forecast in November. It also projects a slightly faster rise in the unemployment rate to 4.3% by the end of this year, compared to 4.2% previously. Meanwhile, despite a downside surprise for Australia's CPI in Q4-2023, inflation is expected to remain above the 2%-3% inflation target range for an extended period. Both headline inflation and trimmed mean inflation are not forecast to return to that target range until the end of 2025, and are not forecast to be at the midpoint of that range until mid-2026.

Keep in mind these forecasts are all predicated on the technical assumption of a policy rate path that is broadly consistent with market implied pricing, which sees the policy rate at 4.3% in mid-2024 and 3.9% by end-2024. Even with that technical assumption, however, the RBA projects inflation remaining above the target range for an extended period. In our view, given that RBA continues to highlight that "returning inflation to target within a reasonable timeframe remains the Board’s highest priority", at the very least that suggests rate cuts are unlikely to come before the second half of this year. That is, we view the RBA's announcement and forecasts as consistent with interest rate cuts starting in the second half of this year or later.

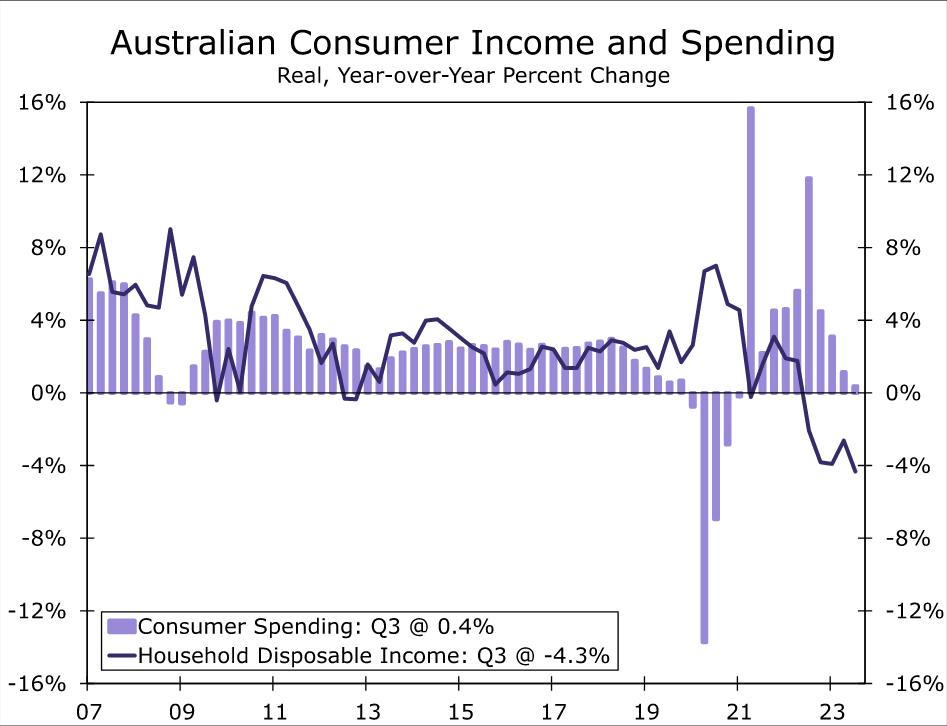

Against this backdrop, we doubt that sluggish economic growth will elicit early easing from Australia's central bank. The RBA has repeatedly highlighted an uncertain outlook for the consumer, uncertainty that is reflected in recent data. Q4 real retail sales rose a modest 0.3% quarter-over-quarter and, while that was better than expected, it was offset by a downward revision to Q3 sales. In fact, the increase in quarterly sales was the first since Q3-2022, and thus, in our view, represents more stabilization than strength in retail activity. In terms of consumer fundamentals, real household disposable incomes fell 4.3% year-over-year in Q3-2023 and the household saving rate dropped to just 1.1% of disposable income, arguing against a quick rebound in consumer spending. Perhaps on a more encouraging note however, tax cuts scheduled for 1 July have been adjusted to provide greater support to lower income earners, which should at least offer some support for consumer spending, and help to limit the extent of any slowdown in the overall economy.

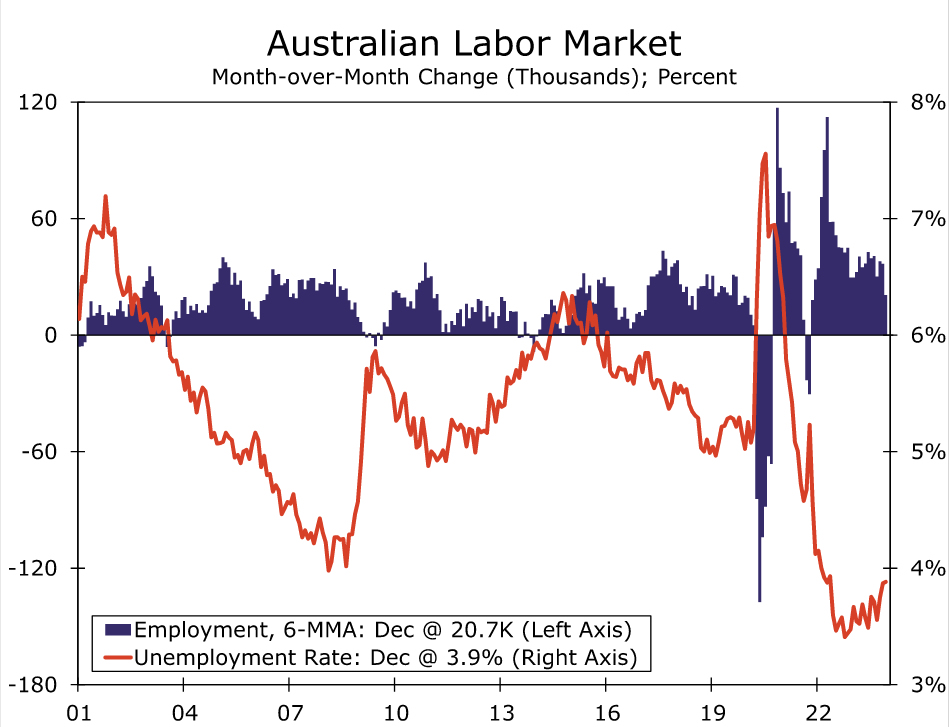

Even amid slow growth, the labor market has remained reasonably resilient so far. Employment has been particularly volatile in recent months, with a large December decline in jobs broadly offsetting a big November increase. Looking through that volatility, the average monthly employment increase slowed during the second half of last year to a still-respectable 20,700 per month. The unemployment rate has also increased to 3.9%, from as low as 3.4% in late 2022. While the labor market has loosened to some extent, we note that a further moderate increase in unemployment and slowing in wage growth (from the current 4.1% year-over-year for the Wage Price Index) would be in line with the RBA's forecast, and could make the central bank more comfortable that inflation is returning sustainably to the target range.

Accordingly, we think an initial RBA rate cut remains some way off. At this time, we remain comfortable with our outlook for an initial 25 bps rate reduction to 4.10% at the August monetary policy announcement, by which time the labor market will likely have softened further, and wage and price pressures will likely have moderated somewhat. We also expect the pace of rate cuts to be quite gradual even after that initial easing, at just 25 bps per quarter, which means the RBA's policy rate would not reach a low of 3.10% until the second half of 2025. While we see risks around this policy rate outlook in both directions, those risks are perhaps tilted toward a later rate cut than an earlier rate cut. Persistence in services or wage inflation could easily see an initial rate cut pushed back to Q4 of this year while, although it is not our base case, an especially sharp slowdown in consumer spending or inflation pressures could still prompt the RBA to move earlier than August.

The pace of monetary easing we forecast for the RBA, at least through the end of 2024, is broadly in line with that implied by market pricing. As mentioned, however, the risks are more heavily tilted toward a later move. Moreover, even our base case for an initial RBA rate cut in August sees Australia's central bank moving noticeably later than the Federal Reserve, where we expect an initial rate cut to occur in May. Overall, a gradual moderation of Australian economic growth and inflation that leads to only a gradual pace of monetary easing from the Reserve Bank of Australia should be supportive of the Australian dollar versus the greenback over time.

High Inflation and Recovering Economy Keeping New Zealand Central Bank Hawkish

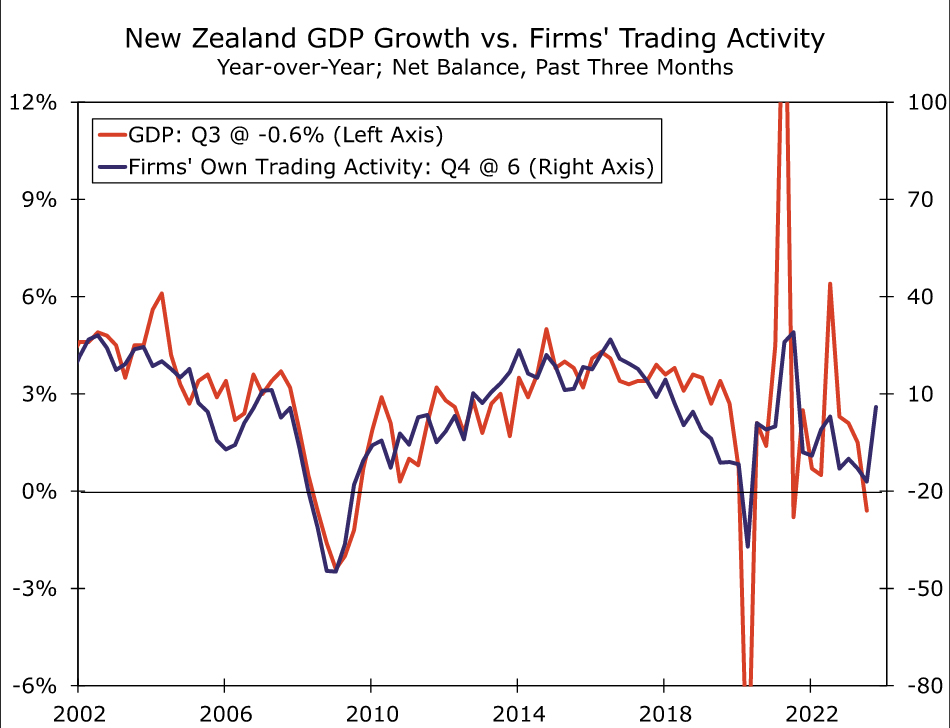

In New Zealand, the economy appears to be moving toward recovery after what was a challenging year through much of 2023. The impact of elevated inflation and the Reserve Bank of New Zealand's (RBNZ) aggressive monetary tightening contributed to GDP reporting sequential declines in three out of four quarters through Q3-2023, according to the latest available figures. Election-related uncertainty may have also provided a temporary restraint to growth late last year. Q3-2023 saw New Zealand's GDP fall 0.3% quarter-over-quarter and 0.6% year-over-year: economic underperformance that occurred even as immigration, and population growth, surged.

Some key economic headwinds facing New Zealand are now starting to abate; inflation has peaked, and we also believe the RBNZ has come to the end of its rate hike cycle. We think that should gradually allow for the economy to transition to a recovery phase, even if these key fundamentals have not turned to significant tailwinds just yet. That appears to be reflected in some available economic indicators for Q4 of last year. Most importantly, the Quarterly Survey of Business Opinion saw businesses become much less downbeat, as just a net 2% of businesses were pessimistic in Q4, compared to the net 52% of businesses who were pessimistic in Q3. Moreover, a net 6% of respondents reported an increase in their own trading activity in Q4, compared to net 17% who reported a decrease in Q3. This latter point is significant as, historically, it is firms' assessment of their own trading activity that has tended to be more closely correlated with overall GDP growth.

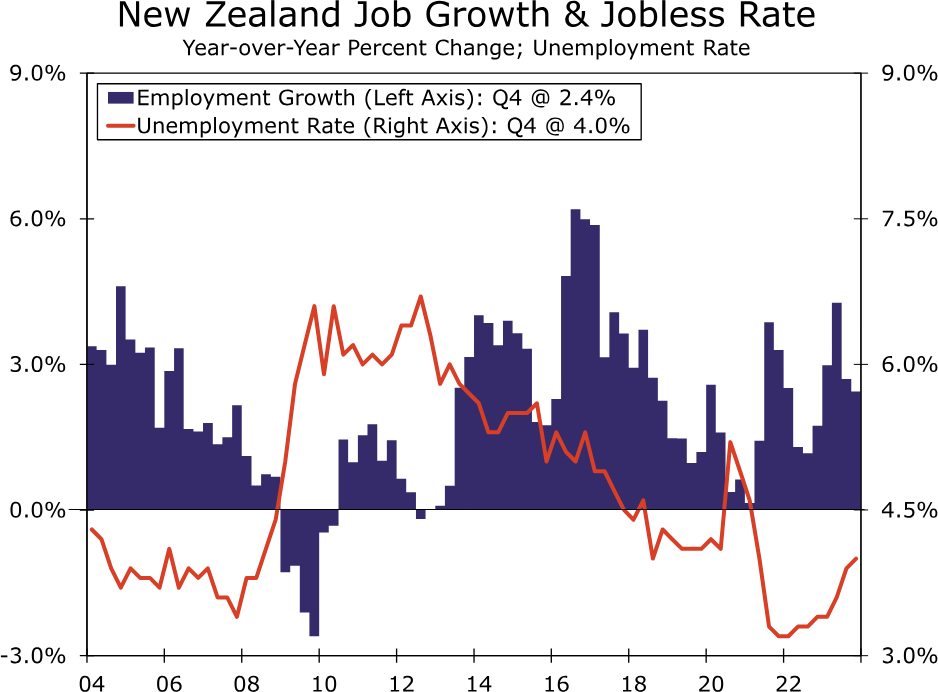

The improvement in sentiment in Q4 suggests that a gradual economic recovery may be upon us, a message that is also reflected in labor market data for the fourth quarter. Q4 employment rose 0.4% quarter-over-quarter, rebounding following a small decline in Q3, while employment was also up 2.4% year-over-year. The unemployment rate did edge higher to 4.0%, though in part, that stems from surging population growth. In fact, if anything, rising unemployment may help to place some restraint on wage pressures. The fourth quarter also saw the Labor Cost Index for the private sector rise to 1.0% quarter-over-quarter and ease to 3.9% year-over-year. Overall, we believe the New Zealand economy can enjoy a moderate recovery this year. We forecast GDP growth of 1.2% for 2024, which would be up from an estimated 0.8% growth in 2023.

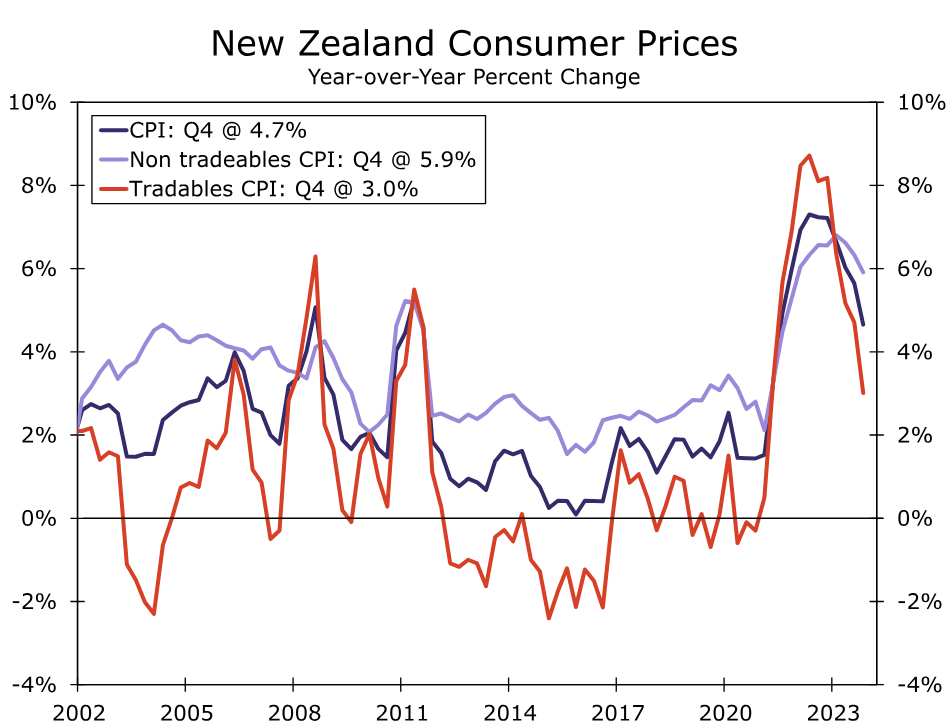

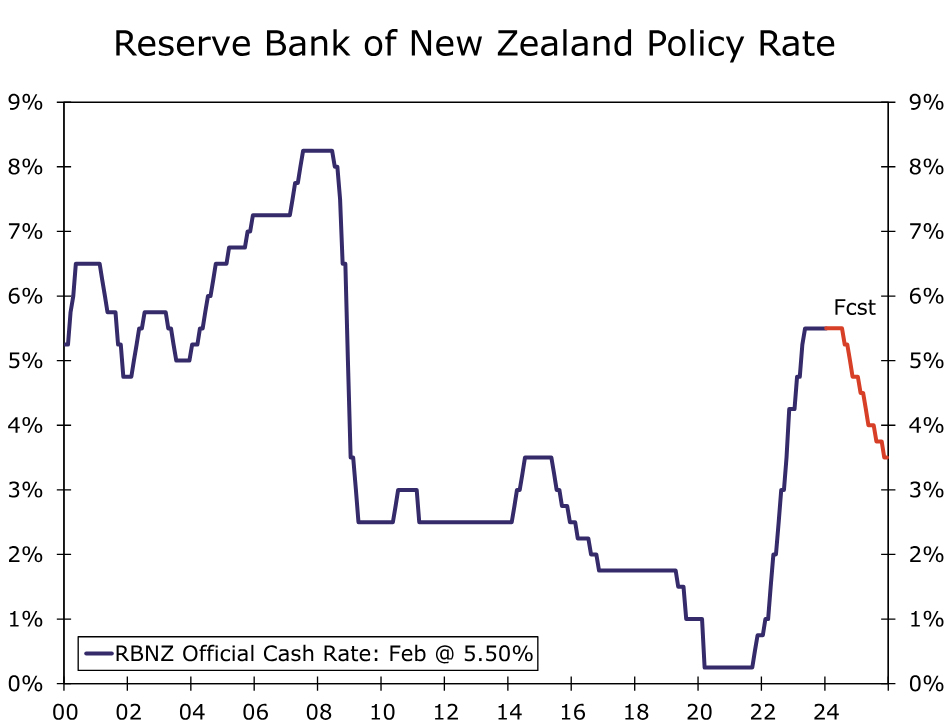

On the inflation front, consumer prices have started to recede, although domestically oriented inflation pressures remain persistent. Q4 CPI inflation slowed to 4.7% year-over-year, matching the consensus forecast. However, although tradeables inflation surprised to the downside and slowed to 3.0%, non-tradeables inflation surprised to the upside, with only a moderate slowing to 5.9%. Both headline inflation and, more particularly, domestically-oriented inflation, remain well above the central bank's 2% inflation target. As a result, the RBNZ has maintained a relatively hawkish monetary policy stance. At its most recent announcement in November, the RBNZ said that despite some decline, inflation remains too high, and policymakers maintain a wariness of inflationary pressures. In fact, the central bank said if inflationary pressures were stronger than expected, the policy rate would likely need to increase further. In more recent comments, RBNZ Chief Economist Conway offered additional hawkish comments. Conway said non-tradeables inflation was higher than expected and a long way from 2%, and that the central bank still has a way to go to get inflation back to target. Given the backdrop of improving sentiment, domestic inflationary pressures and a hawkish central bank, we now see RBNZ policy rate cuts occurring later than previously envisaged. We expect an initial 25 bps rate cut to 5.25% at the August announcement. Beyond that, we see a relatively steady pace of easing, with our forecast for a cumulative 75 bps of rate cuts in 2024, and a further cumulative 125 bps of rate cuts in 2025, which would see the RBNZ's policy rate reach 3.50% by the end of next year. Against a backdrop of a U.S economic slowdown and Fed easing, we believe a moderate rebound in NZ economic growth and gradual RBNZ monetary easing should see the New Zealand dollar enjoy moderate gains against the U.S. dollar over time.

What Impact Will Canada’s Employment Figures Have on Loonie?

- Canada’s economy likely added more jobs in January

- Ivey PMIs rises to its highest level in 9 months

- BoC summary of deliberations gets releasedon Wednesday

- Loonie rises ahead of Friday’s data due at 13:30 GMT

In Canada, a number of data releases are scheduled for this week. On Tuesday, the Ivey Purchasing Managers' Index (PMIs) came out, which will be followed by the summary of deliberations from the most recent Bank of Canada meeting on Wednesday. The report is analogous to the meeting minutes and will provide investors with a comprehensive record of the discussions that took place on January 24. On Friday, the employment data for January will determine if the upward trajectory of the jobless rate persists.

BoC’s Macklem speaks ahead of BoC summary of deliberations

Tiff Macklem, the Governor of the Bank of Canada, is defining the boundaries of monetary policy by cautioning that the central bank cannot address issues like housing affordability through adjustments in interest rates.

In his prepared remarks delivered in Montreal on Tuesday, Macklem asserts that historical evidence demonstrates the considerable efficacy of monetary policy in managing inflation over the medium term. However, the governor acknowledges that the system also has constraints, such as its incapacity to tackle immediate price changes.

As most people expected, the Bank of Canada kept the goal for its overnight rate at 5% for the fourth time in a row in January. This meant that the cost of borrowing money was at its highest level in 22 years. The Governing Council said that it is still worried about the risks to the outlook of inflation, especially the risks to underlying price growth after preferred core inflation gauges unexpectedly rose in December.

This means that tight monetary policy will stay in place. Headline inflation is expected to stay around 3% for the first half of the year, according to the central bank. It will then start to drop to the 2% goal in 2025. Even though tight policy has caused the economy to slow down, interest rates have stayed high. The Bank said that consumers have cut back on spending, business investment has decreased, and job market conditions have become more balanced.

Ivey PMIs hit highest level since April

According to Tuesday's Ivey Purchasing Managers Index (PMI) statistics, economic activity in Canada accelerated in January to its fastest pace in nine months.

The seasonally adjusted index rose from 56.3 in December to 56.5 in January, reaching its highest point since April. The Ivey PMI is a monthly indicator that tracks economic activity as reported by a group of Canadian purchasing managers. An increase in activity is indicated by a value above 50.

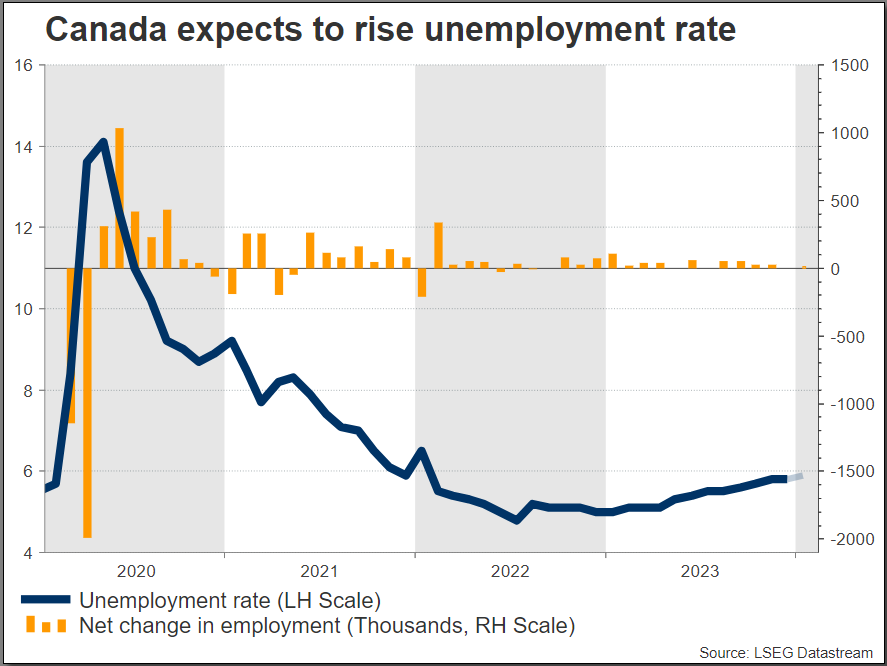

Canada’s unemployment rate expected to tick up

In December 2023, Canada's jobless rate stayed at 5.8%, the same as the 22-month high recorded the previous month. It was a little lower than the forecast of 5.9%, but it's expected to rise to 5.9% in January.

Notably, the indicator has exhibited a gradual upward trend since April, and a continuation in this direction could bolster demands for earlier reductions in borrowing costs.

Canada's employment level went up by 0.1k in December, after going up by 24.9k in November. This was less than the 13.5k growth that was expected. Based on this month's report, it is expected to add 15.0K jobs in January.

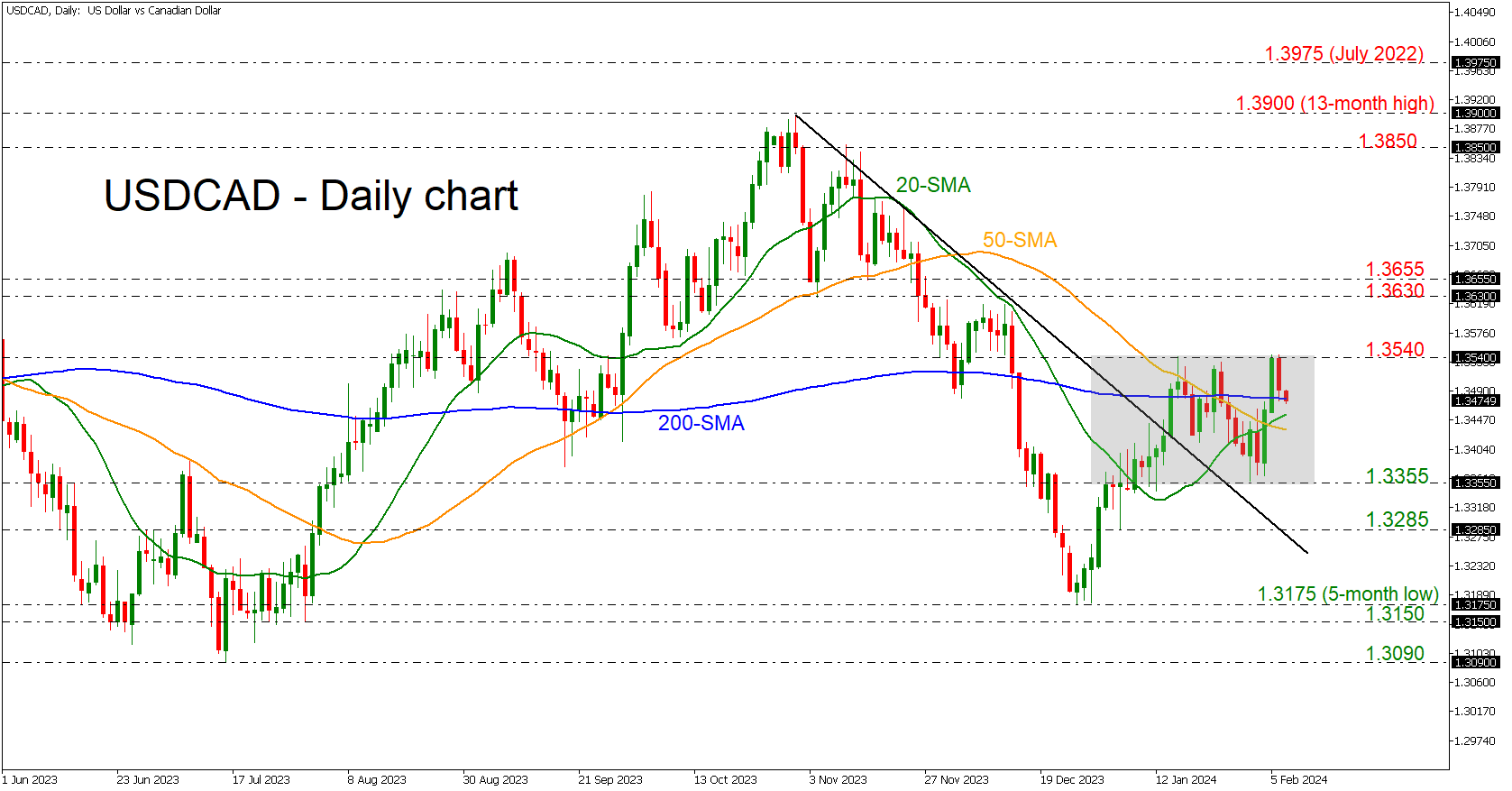

USDCAD loses ground in sideways channel

USDCAD loses ground in sideways channel

If the data indicates a slowdown in the economy, it is possible that USDCAD will stay above its simple moving averages (SMAs), which have been limiting upward movements around the 1.3400 level. More precisely, if the price surpasses the current resistance level of 1.3540, which is currently operating as the upper boundary of a short-term consolidation range between 1.3355 and 1.3540, it might potentially reach the restrictive zone of 1.3630-1.3655.

If the bears manage to push the price below the 1.3355 support level, selling pressure might increase below the 1.3285 area, approaching the five-month low of 1.3175.

EURJPY Rotates Lower as Rebound Falters

- EURJPY bounces back after 50-day SMA prevents decline

- But reverses lower again, finding support at descending trendline

- Momentum indicators are neutral-to-negative

EURJPY has been sliding lower in the short term, following its rejection at 161.85 in late January. Despite its temporary rebound at the 50-day simple moving average (SMA), the pair has been on the retreat again, holding marginally above the downward sloping trendline taken from its 15-year peak of 164.28.

Should selling pressures persist, the price could initially test the February support of 158.06. Further declines could then come to a halt at the January low of 155.05 ahead of the October support of 154.34. Even lower, the December bottom of 153.13 could provide downside protection.

Alternatively, if buyers re-emerge and propel the price higher, immediate resistance could be found at 160.80, which overlaps with the lower boundary of the pair’s ascending channel. Jumping above that territory, the price may revisit the January high of 161.85. A break above that area could pave the way for the 15-year peak of 164.28.

In brief, despite attempting to pause its short-term selloff, EURJPY remains under significant downside pressure. Hence, a break below the descending trendline currently in place could accelerate the decline.

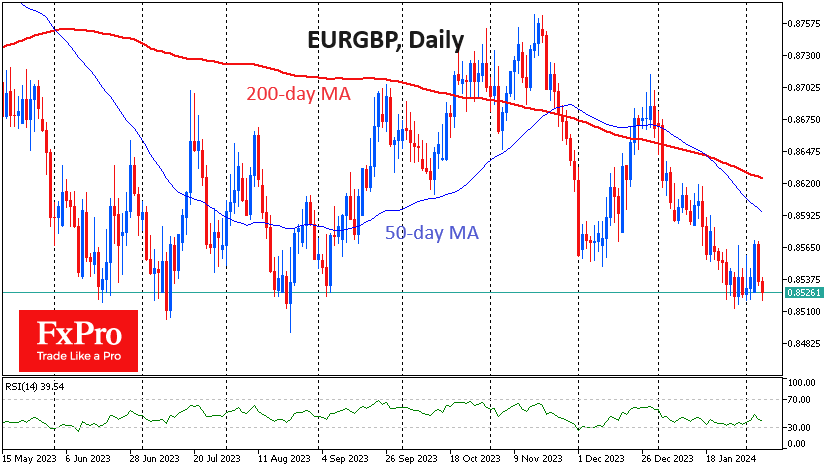

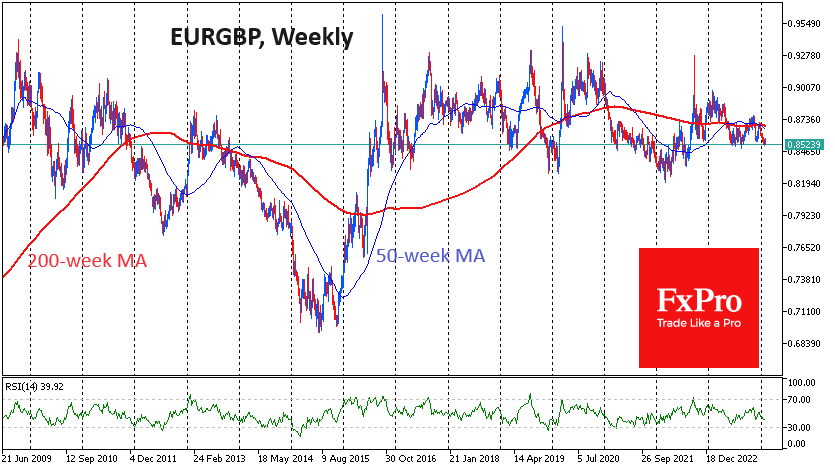

EUR/GBP One Step Away from a Descending Stair

The euro is back at 0.8520 against the pound. The pair bounced off this level in June and August last year. Reaching the same level in late January triggered a shake-out, but active declines resumed on Tuesday and Wednesday, and the pair is testing multi-month lows with renewed vigour.

Technically, a break of support at 0.8500 would allow a move towards 0.8250-0.8300 to be considered as a working scenario. A decline of 2.0-2.5% looks like a significant move. However, we may be seeing the beginning of a new global trend.

EURGBP has tried to break above 0.9200 several times since 2016, mainly triggered by the weakness of the pound. We may now be entering a period of euro weakness, like what we saw in 2013-2015. Back then, a wave of pressure on the euro pushed EURGBP towards 0.7000.

The reason for this global reshuffle in a rather dull pair could be the increasing divergence in economic dynamics. With interest rate changes on the agenda, interest is being drawn to the more buoyant economies where the UK has an advantage due to domestic demand.

The level of interest rates and interest rate expectations will also be critical in the coming quarters. The Bank of England’s base rate is now 5.25%, compared with 4.5% for the ECB. However, markets expect the Bank of England to cut four times to 4.25% by 2024. The ECB is expected to start its rate-cutting cycle a little earlier and bigger.

While one should be prepared for the EURGBP to return to a lower floor, confirmation in the form of a break of 0.8500 is still needed and is not yet a done deal. There is still a relatively high chance of renewed gains from current levels, as the current multi-month lows may attract buyers into the EUR.

AUDUSD: Initiating Macro Bearish Reversal

Bearish Scenario: Selling below 0.6516 with TP1: 0.65, TP2: 0.6487, and upon its breakout TP3: 0.6469. It is recommended to place a stop loss above 0.6541, at least 1% of the account capital. Trailing stop can be used.

Bullish Scenario: Buying above 0.6540 with TP1: 0.6572, TP2: 0.6594, and TP3: 0.66. It is recommended to set a stop loss (S.L.) below 0.6520 or at least 1% of the account capital.

Analysis from Daily Chart. Volume Profile and Structure.

AUDUSD may be facing a reversal of the bullish trend from the last quarter of 2023, with the breakdown of the December and January support at 0.6525, leaving resistance at 0.6624. The current correction may still extend towards the high volume node around 0.6565, to resume sales towards one of the high volume nodes of November at 0.6430 and the round level 0.64. This scenario will be active as long as the retracement does not break above 0.66 and the resistance at 0.6624. The RSI positioned in negative territory confirms a bearish momentum for the pair.

Scenario from H2 Chart.

The current correction leaves a local resistance at 0.6540, whose decisive breakout will extend purchases towards the daily bullish average range at 0.6572, opening the door to reach Friday's uncovered POC at 0.6594, thus covering the volume inefficiency or volume gap left by Friday's decline. This is a selling zone that will encourage bearish entry to resume pair sales.

On the other hand, an anticipated bearish scenario will be activated with quotes below the broken support at 0.6525 towards Tuesday's uncovered POC at 0.6493, whose breakout in a second touch will break the correction support at 0.6487, indicating a continued decline towards the next support and buying zone around 0.6466.

*Uncovered POC: POC = Point of Control: It is the level or zone where the highest volume concentration occurred. If there was previously a downward movement from it, it is considered a selling zone and forms a resistance zone. Conversely, if there was previously an upward impulse, it is considered a buying zone, usually located at lows, forming support zones.

Risk Management Consideration:

**It is very important that risk management be based on capital and traded volume. For this, a maximum risk of 1% of the capital is recommended. It is suggested to use risk management indicators like Easy Order.

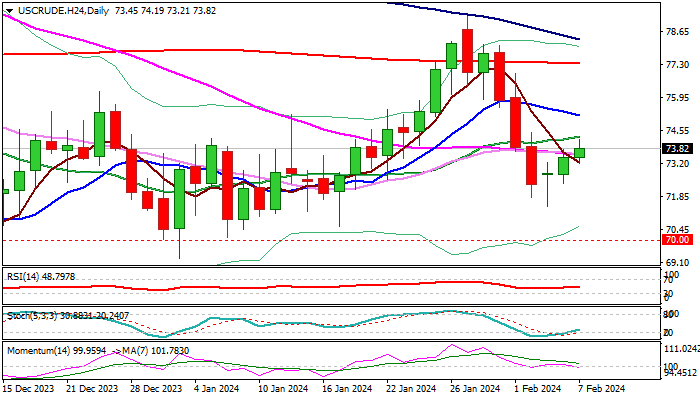

WTI Oil: Recovery Extends into Third Day But Risk of Stall Exists

WTI oil price extends recovery from new multi-week low ($71.40) into third consecutive day.

Profit-taking after last week’s 8.1% drop was contained by 200WMA, lifted the price along with lower than expected increase in US crude inventories (API report) and cut in forecast for US oil production growth which cooled concerns about potential oversupply.

Recovery penetrated thick daily cloud, (base of the cloud lays at $73.37) but faced increased headwinds at pivotal barriers at $74.27 (daily Kijun-sen) and generating initial signal of potential recovery stall.

The notion is supported by weakening bullish momentum and daily MA’s in predominantly bearish configuration, which keeps in play risk of very limited correction before larger bears regain full control for renewed probe through cracked $72.12 Fibo support, loss of which to open way for further retracement of $67.70/$79.27 uptrend.

Conversely, firm break of $74.27 pivot to firm near-term structure for attack at upper pivot at $75.34 (50% retracement of $79.27/$71.40 / daily Tenkan-sen).

Res: 74.27; 75.34; 76.92; 78.07.

Sup: 73.37; 72.37; 71.40; 70.61.

Sunset Market Commentary

Markets

In the absence of key eco data, both in the US and Europe, central bankers’ talk today was again earmarked as the main guide for bond markets. ECB board member Isabel Schnabel in the FT gave an in extenso assessment on the importance of the ECB walking the last mile to defeat inflation. She warns on a slowdown in the disinflationary process, especially in the services sector. Nominal wages are rising strongly as employees are trying to catch up on their lost income. At the same time Schnabel sees a worrying decline in productivity. This combination leads to higher unit labour costs. Question is how this will translate into firm’s pricing. Here monetary policy should continue to do its job. A restrictive policy dampening aggregate demand in this respect will make it more difficult for firms to pass through higher costs. The combination of sticky (services) inflation, a resilient labour market and at the same time a loosening of financial conditions makes Schnabel conclude that the ECB should be patient and cautious, even more as recent activity data (PMI’s) suggest that the peak of policy transmission might have passed. Schnabel’s well-founded analysis maybe helped to put a floor to yesterday’s retracement in yields. However, moves in interest rate markets still are limited on both side of the Atlantic. Both US and EMU yields add 1-2 bps across the curve before paring gains again amid intensifying worries in the US regional bank saga. Later today, Fed governors Kugler, Collins, Barkin and Bowman still are scheduled to speak. Fed Kashkari in an interview with CNBC suggested that he currently considers 2-3 rate cut as appropriate. However, more than additional CB guidance, markets further out probably will be driven by confronting incoming inflation, and equally important, activity data against the well-flagged CB guidance. A record $42 bln sale of US Treasuries might give some insight on the supply-demand balance in the US bond market after recent cheapening later today. The absence of bond market volatility is helping equities to hold near recent peak levels or even touching new records The Eurostoxx 50 is trading marginally lower after touching a minor new multi-year top at the open this morning. The S&P 500 even opened at new all-time highs. For now, there are no spill-over effects from the tensions amongst some US regional banks toward the broader equity market. In FX, some softening after recent rally for now is the path of least resistance for the dollar. DXY is revisiting the 104 big figure. EUR/USD is drifting higher in the upper half of the 1.07 big figure (1.0775) after a twice rejected test of the 1.0724 December low. Still the picture for the EUR/USD pair remains fragile/unconvincing. Sterling remains in good shape outperforming (admittedly slightly) the dollar (cable again north of 1.26) and the euro (EUR/GBP 0.853).

News & Views

EUR/HUF rises towards 388 in a move that shows the Hungarian forint clearly underperforming regional peers today. HUF came under pressure in early European dealings before extending losses after the European Union launched a new legal procedure against Hungary. The Commission today sent a letter of formal notice as a first step that could potentially lead to a lawsuit. Hungary has two months to reply. At the heart of the issue is the country’s Defence of National Sovereignty legislation, granting a newly created agency the power to probe organizations (including political parties, non-governmental organizations and the media) for possible violations of national sovereignty. The EC on its website underpinned the move by saying that “the Hungarian legislation at stake violates several provisions of primary and secondary EU law, among others the democratic values of the Union; the principle of democracy and the electoral rights of EU citizens; several fundamental rights enshrined in the EU Charter of Fundamental Rights […]; the requirements of EU law relating to data protection and several rules applicable to the internal market.” The new infringement procedure adds another layer of doubt to the disbursement of some €21bn in funds that are currently withheld. It’s also likely to anger president Orban, who only recently backed down on its opposition for additional Ukraine aid.

The Belgian Debt Agency successfully launched the new 30-y June 2055 OLO 101 bond. The syndicated sale printed €5bn at OLO+4 compared to initial guidance of OLO+7 area. Books were reported in excess of €62bn. Combined with the 10-y syndication in January (raising €7bn), the Debt Agency has completed about 30% of this year’s total OLO funding need (€41bn). Based on the 2024 funding plan, the BDA has one more syndicated sale in store for this year. The final one will have a medium term maturity of five or six years.

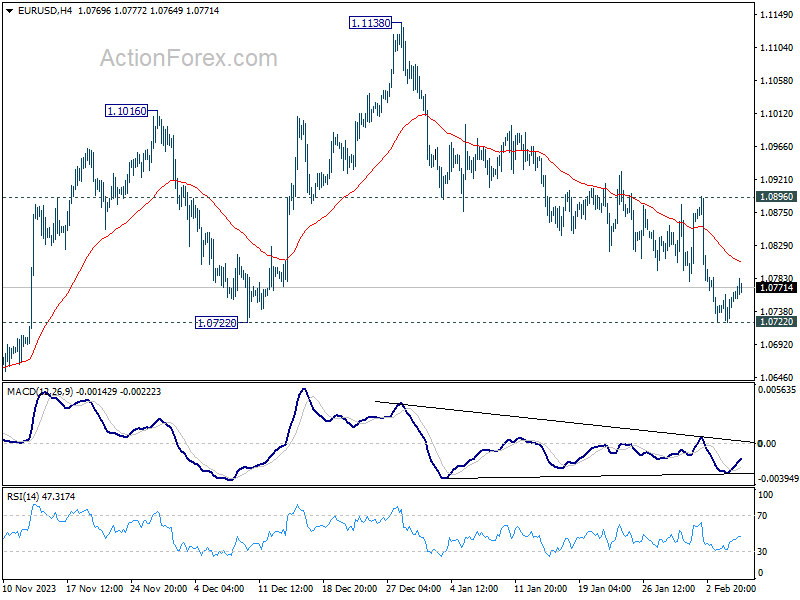

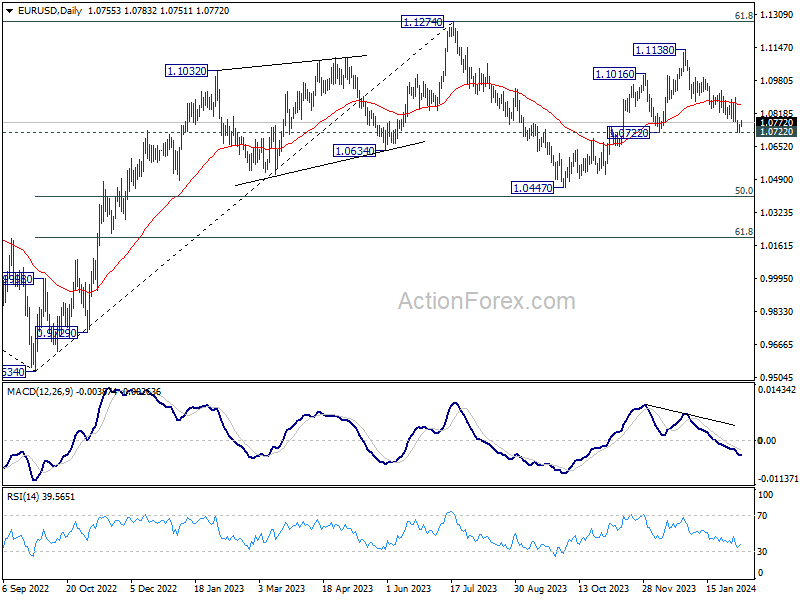

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0731; (P) 1.0746; (R1) 1.0770; More...

No change in EUR/USD's outlook and intraday bias stays neutral. Focus remains on 1.0722 structural support. Decisive break there will argue that whole rise from 1.0447 has completed. Deeper fall would then be seen to target this low. On the upside, break of 1.0896 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

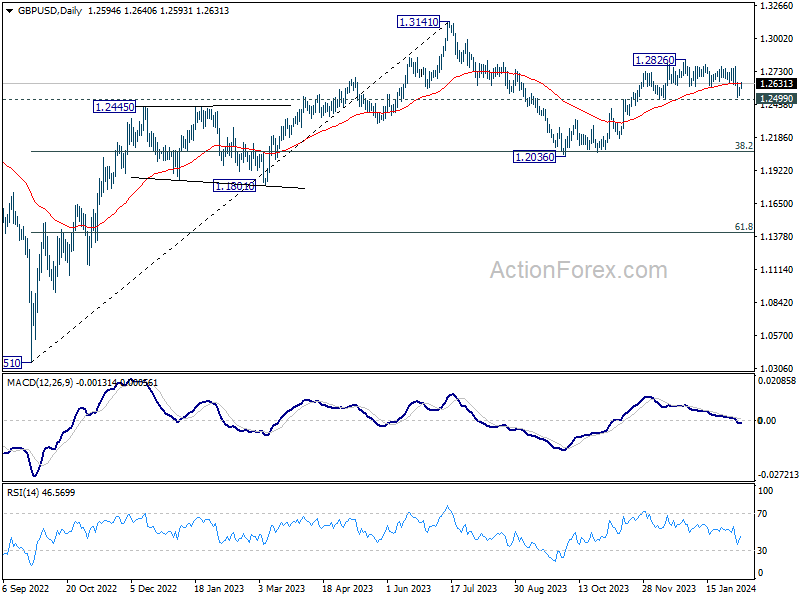

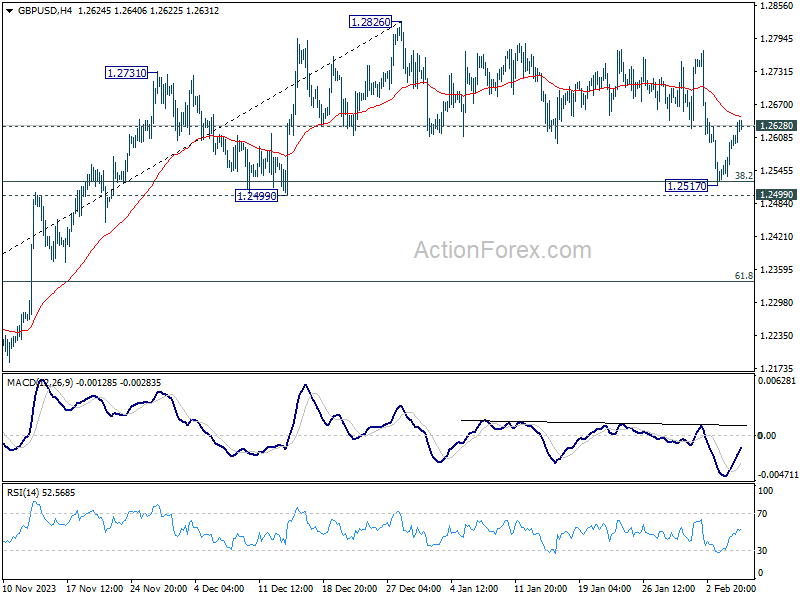

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2551; (P) 1.2577; (R1) 1.2624; More...

GBP/USD's break of 1.2628 minor resistance argues that correction from 1.2826 might have completed with three waves down to 1.2517. That came just ahead of 1.2499 structural support. Intraday bias is back on the upside for stronger rebound back towards 1.2826. On the downside, however, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's still in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.