Sample Category Title

Yen Strengthens Despite Unchanged BOJ Monetary Policy

USDJPY fell on Tuesday after BoJ kept ultra-low rates unchanged, as yen strengthened on growing hopes that the central bank will start tightening policy soon.

Fresh dip comes after a triple daily Doji candle, which signaled strong indecision and generating an initial signal that larger uptrend is stalling, and reversal may follow.

Fading bullish momentum on daily chart and stochastic emerging from overbought territory, add to negative signals, though verification of initial signal will require close below cracked pivotal supports at 147.54/45 (100DMA / broken Fibo 61.8% of 151.90/140.25).

In such scenario, fresh bears will face more tough supports at 146.78/73 (Fibo 23.6% of 140.25/148.80 / daily Ichimoku cloud top), violation of which will further weaken near-term structure and expose next pivotal supports at 145.53/32 (Fibo 38.2% / daily cloud base).

Caution on failure to sustain break below 100 DMA which would keep the price action in extended sideways mode, but biased lower as long as the price stays below 149.00 resistance zone.

Res: 146.97; 148.80; 149.15; 149.70

Sup: 147.45; 146.92; 146.78; 146.43

Currencies Consolidate Awaiting Bank of Canada and ECB Verdicts

The last full trading week of January is highly saturated with important fundamentals. This morning, the Bank of Japan held its meeting, tomorrow, the Bank of Canada will announce its verdict, and on Thursday, the ECB's press conference is scheduled. Major currency pairs, in anticipation of the mentioned events, continue to trade within narrow corridors formed earlier.

USD/CAD

The USD/CAD chart shows that the currency pair is trading near recent highs at 1.3520-1.3480. After an early-year rise, the pair retreated to support at the alligator lines on the daily timeframe. Yesterday, the price dropped to 1.3420 but interrupted the downward correction and rose to 1.3480 by evening. With a corresponding fundamental background, the pair may break the upper fractal at 1.3540 and continue to rise towards 1.3680-1.3570. The cancellation of the upward scenario may be considered with a confident fixation below 1.3400.

At 16:30 GMT+3 today, we await the publication of data on the new housing price index in Canada for December. Tomorrow at 18:00 GMT+3, the Bank of Canada will announce its decision on the base interest rate. Analysts predict that officials will leave the rate unchanged. For market participants, the Canadian regulator's comments on credit and monetary policy for the current year will be crucial.

GBP/USD

The GBP/USD chart shows the currency pair has held within a relatively narrow range for several days, between 1.2720 and 1.2600. Uncertainty in the credit and monetary policies of the Bank of England and the Federal Reserve keeps investors from both buying and selling the GBP/USD pair.

Tomorrow at 12:30 GMT+3, attention should be paid to the publication of data on the Purchasing Managers' Index (PMI) for the manufacturing sector in the UK for January. Also, tomorrow at 17:45 GMT+3, a block of important macroeconomic data will be released from the US, including the PMI for the services sector and the PMI for the manufacturing sector for the same period.

EUR/USD

The euro, after breaking the support at 1.0920, has been trading below the alligator lines on the daily timeframe for about a week. However, technical analysis of EUR/USD today suggests that there are no pronounced downward dynamics after the breakthrough of important levels: the price is trapped between 1.0900 and 1.0840.

Traders are likely awaiting the ECB's verdict; the European regulator's meeting is scheduled for Thursday. If officials' forecasts for the economic recovery of the Eurozone for the current year turn out to be pessimistic, the price may break support at 1.0840 and resume the downward movement towards 1.0700-1.0600. The breakdown of the downward scenario may be expected after a confident fixation above 1.1000.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

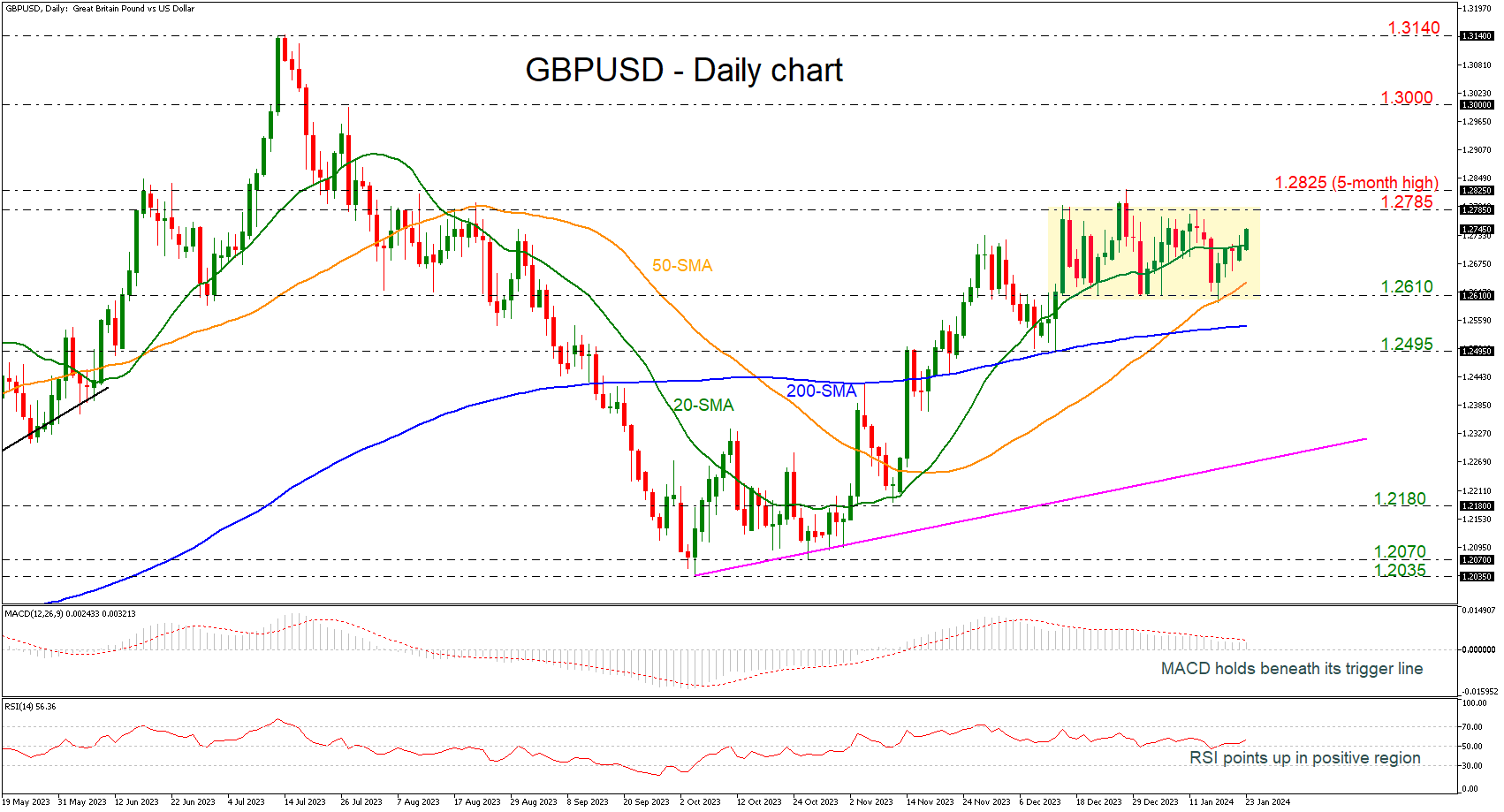

GBPUSD Ticks Up in Trading Range

- GBPUSD surpasses 20-day SMA

- RSI points up in bullish area

- Short-term bias positive, but there are more threats higher

GBPUSD has reversed back higher again after finding support at the lower boundary of the trading range of 1.2610-1.2785. Currently, the price is rising beyond the 20-day simple moving average (SMA) and is approaching its previous highs.

Momentum indicators are showing some mixed signs. The MACD is still losing momentum beneath its trigger line in the positive region, while the RSI is pointing north in the bullish area after a flattening period in the past.

Should the pair manage to strengthen its positive momentum, the next resistance could come around the 1.2785-1.2825 restrictive zone. A break above it would shift the bias to a more bullish one and open the way towards the 1.3000 psychological mark.

However, if prices are unable to break into the upper band of the range in the next few sessions, the risk would shift back to the downside, with the 50-day SMA at 1.2635 once again coming into focus, as well as the 1.2610 support. The next key level to watch lower down is the 200-day SMA at 1.2545 ahead of the 1.2495 barrier.

In the medium-term, the outlook remains bullish since prices hold above all the moving average lines and the ascending trend line, which has been drawn since October 4.

BoJ’s Ueda elaborates on inflation and wages, hinting at future policy shifts

During his post-meeting news conference, BoJ Governor Kazuo Ueda confirmed that the economy is aligning with the central bank's inflation projections, adding "our core-core inflation forecast is at 1.9%, very close to our 2% target". This closeness, he explained, significantly contributes to BoJ's growing confidence in sustainably achieving its price target.

However, Ueda acknowledged the challenges in quantifying the exact progress towards this goal. He pointed out that recent movements in service prices have been influenced by several one-off factors and that consumption weakness is impacting these prices. BoJ is analyzing these trends by separating such factors, and Ueda believes that, despite these complexities, "service inflation is gradually accelerating as a trend."

Ueda also addressed the timing of monetary policy adjustments in relation to wage negotiations. He suggested that waiting for the outcome of wage talks across all firms, including smaller ones, would be impractical due to the extended timeframe this would require. BoJ, therefore, intends to use various economic indicators and data from hearings to predict wage trends. Ueda emphasized the influence of larger firms' wage negotiations on smaller firms and the availability of data on smaller firms' profit outlooks as potential early indicators.

Bank of Japan Kept Its Monetary Policy Unchanged

Markets

The Bank of Japan kept its monetary policy unchanged this morning with a -0.1% policy rate and a 10-yr JGB target with a “soft” upper bound of 1%. In its new policy forecasts, the BoJ kept its inflation forecast for the current fiscal year unchanged at 2.8%, while lowering it from 2.8% to 2.4% for the fiscal year starting April 2024 (especially because of declining oil prices) and slightly increasing the one for fiscal year 2025 from 1.7% to 1.8%. Risks to the forecasts are “generally balanced” over the policy horizon whereas the BoJ previously suggested that the 2025 projection was skewed to the downside. The outcome of spring wage talks (shunto) seems to be the pivotal moment for the BoJ to whether or not proceed (more rapidly) with its policy normalization process. The BoJ’s wants more signs on the risks of a wage-price spiral before acting. The Japanese central bank pencils a growth path of 1.8%-1.2%-1% for fiscal year 2023-2025 compared with 2%-1%-1% in October. The outcome of the meeting was as broadly expected and doesn’t impact Japanese bond markets. The yen initially prevented more losses, but this was more thanks to the Friday-Monday comeback of core bonds rather than with the BoJ outcome. It even started appreciating a bit during BoJ governor Ueda’s press conference as he said to mull if negative rates should be kept if the price goal is in sight. The currency is nevertheless in desperate need of some firmer backing. USD/JPY rose towards the 148-area prompting a first FX intervention warning by Fin Min Suzuki on Friday. End 2022 and end 2023, the USD/JPY 150-zone has proven critical resulting in effective interventions (2022) and significant verbal warnings (2023).

Today’s eco calendar remains rather soft ahead of EMU January PMI’s (tomorrow), 4th quarter US GDP data and the ECB policy meeting (both on Thursday) later this week. Blackout periods hold central bankers back from commenting, though the ECB with its quarterly Bank Lending Survey still publishes a key piece of information today. Other things to watch are the January Richmond Fed Manufacturing index in the US and EMU consumer confidence. The US Treasury starts its end-of-month refinancing operation with a $60bn 2-yr Note auction while Q4 earnings season gets more and more traction with Netflix today’s highlight after US close. Investors since Friday turned to a more neutral approach going into key ECB and Fed (next week) meetings after scaling back end 2023 aggressive policy rate cut bets. We nevertheless think that too much policy easing is still discounted. In that same move, the dollar gives away some ground (EUR/USD 1.0910) while stock markets flourish. Both the US Dow Jones and S&P 500 yesterday closed at record levels for a second straight session.

News & Views

Chinese authorities are considering a package of measures to stabilize the slumping stock market, Bloomberg reported citing people familiar with the matter. Policymakers are said seeking to mobilize about 2 trillion yuan; mainly from offshore accounts of Chinese state-owned enterprises, as part of a stabilization fund to buy shares onshore through the Hong Kong exchange link. Officials also are said to have earmarked at least CNH 300bn of local funds to invest in onshore shares. Other additional measures might still be added to the plans and concrete steps might be announced as soon as this week. The ‘plans’ are aimed at restoring confidence as Chinese equity markets are under heavy selling pressure with the CSI 300 touching the lowest level in about 5-years. The CSI 300 reversed an earlier loss, but gains currently are still very modest at +0.5%.

According to a survey of National Australia Bank, business conditions softened further in December from 9 to 7. Business confidence still improved from -8 to -1. However, especially subseries on prices and costs have eased substantially compared to the previous month. Labour costs eased from 2.3% Q/Q to 1.8% Q/Q. purchase costs slowed from 2.5% to 1.6% while price growth for final products declined to 0.9% from 1.2%. Capacity utilization also eased from 83.6% to 82.7%. Indications on price growth should give the Reserve Bank of Australia some comfort as it currently maintains a wait-and-see approach after raising the policy rate to 4.35%.

AUD/USD Technical: Potential Short-term Bullish Reversal

- The higher beta risk-sensitive AUD has started to see a turnaround to the upside against the US dollar in the past two sessions.

- Reinforced by risk-on behaviour in global stock markets coupled with today’s China Premier Li Qiang’s verbal intervention that advocated more “forceful” measures to negate the rout in the China equities.

- AUD/USD’s minor bullish reversal unfolding with next intermediate resistances at 0.6640 and 0.6735.

Since last Thursday, 18 January the recent US dollar strength has started to dissipate which has come in line with a risk-on behaviour in global stock markets except for China and Hong Kong equities that are still mired in structural long-term bearish configurations.

The US S&P 500 rallied to a fresh all-time high last Friday, 19 January after similar bullish feats were seen earlier on the Dow Jones Industrial Average and Nasdaq 100. This positive reflexive animal spirits feedback loop in equities has spilled over to the foreign exchange market where the higher beta (risk-on/risk-off) sensitive currencies such as the Aussie (AUD) has managed to catch a bid and stalled its previous multi-week sell-off against the US dollar.

Recent AUD weakness has stalled supported by China’s plan to stabilize the stock market rout

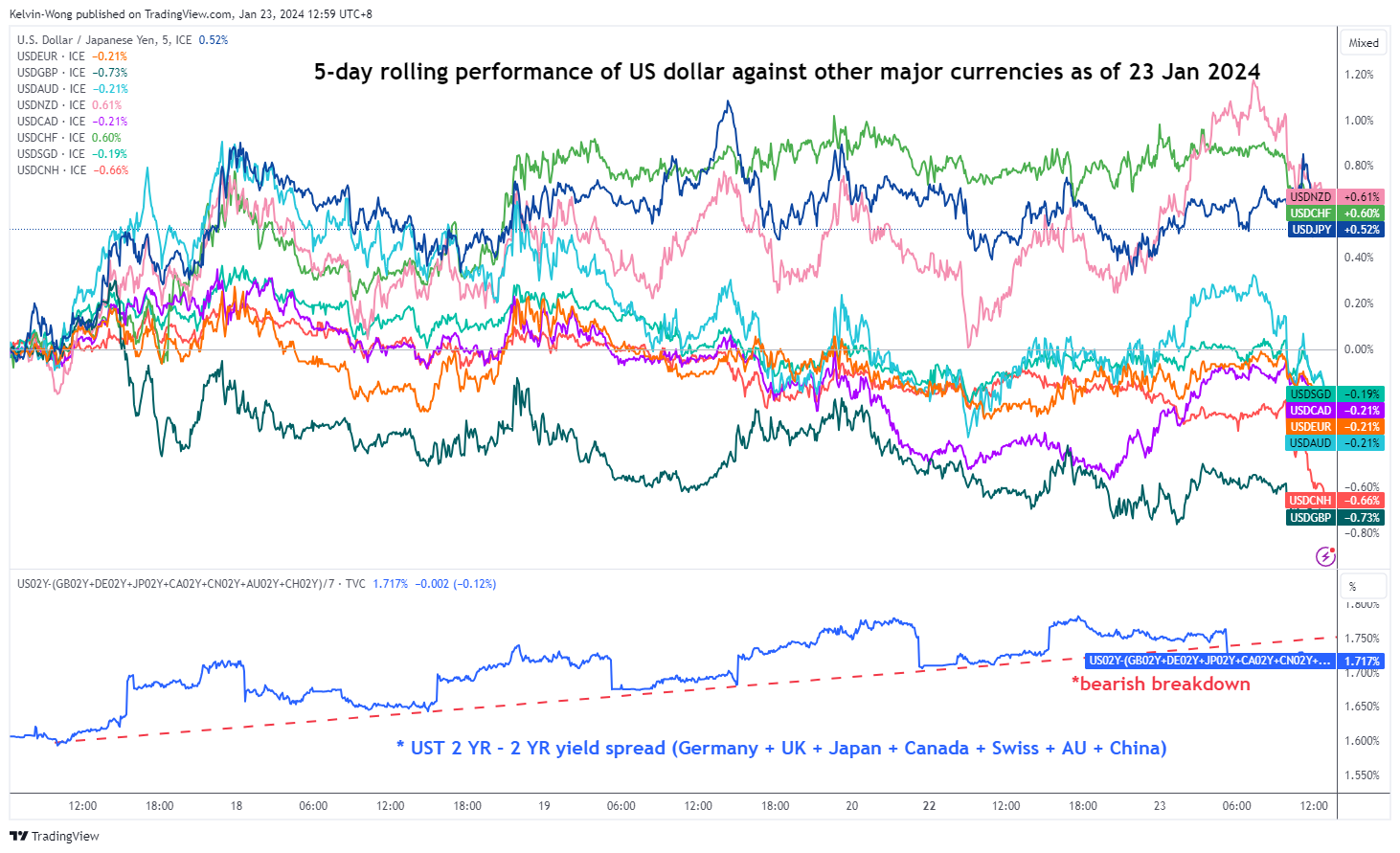

Fig 1: 5-day rolling performances of the US dollar against other currencies as of 23 Jan 2024 (Source: TradingView, click to enlarge chart)

Based on a 5-day rolling performance, the US dollar has now recorded a loss of -0.2% against the AUD, the third strongest performing currency after CNH (offshore yuan), and GBP against the US dollar at this time of the writing.

Today’s Asian session’s outperformance of the AUD is primarily driven by potential further indirect stimulus measures from Australia’s key trading partner, China.

After another horrendous start to the week in China and Hong Kong stock markets, the CSI 300, Hang Seng Index, and Hang Seng China Enterprises Index declined by -1.5% to -2.4% toward multi-year lows.

China’s Premier Li Qiang has issued a “verbal intervention” today to ask Chinese authorities to embark on more forceful measures to stabilize the major bearish trend phases of China’s benchmark stock indices. Thereafter, several media outlets reported that Chinese policymakers are attempting to mobilize about 2 trillion yuan from offshore accounts of Chinese state-owned companies, as part of a stabilization fund to buy onshore China equities via the Hong Kong exchange link.

AUD/USD traded back above the key 200-day moving average

Fig 2: AUD/USD medium-term trend as of 23 Jan 2024 (Source: TradingView, click to enlarge chart)

In the lens of technical analysis, the multi-week decline of the AUD/USD from its 28 December 2023 high of 0.6871 to the recent 18 January 2023 low of 0.6526 may have formed a minor inflection point at the 0.6520 medium-term support.

In addition, it has reintegrated back above the 200-day moving average with the daily RSI momentum indicator that flashed a bullish condition near its 30-level oversold region.

Watch the 0.6570 key short-term support

Fig 3: AUD/USD minor short-term trend as of 23 Jan 2024 (Source: TradingView, click to enlarge chart)

The minor pull-back from yesterday, 22 January Asia session high of 0.6614 managed to stall at 0.6570 which also confluences with the 50% Fibonacci retracement of the minor rally from last Wednesday, 17 January low to 22 January high.

The near-term resistance will be at 0.6640 (also the 50-day moving average & the minor descending trendline from the 28 December 2023 high), and clearance above it sees the next intermediate coming in at 0.6735.

On the flip side, failure to hold at 0.6570 negates the bullish tone to expose the 0.6520 medium-term support.

Say Something Hawkish, I’m Giving Up on You

The week started on a positive note on both sides of the Atlantic Ocean. Equities in both Europe and the US gained on Monday. The tech stocks continued to do the heavy lifting with Nvidia hitting another record. The positive chip vibes also marked the European trading session; the Dutch semiconductor manufacturer ASML regained its status as the third-largest listed company in Europe, surpassing Nestle, thanks to an analyst upgrade.

Moving forward, the earnings announcements will take the center stage, with Netflix due to announce its Q4 results today after the bell. The streaming giant expects to have added millions more of new paid subscribers to its platform after it scrapped password sharing last year.

Away from the sunny US stocks, the situation is much less exciting for China. Right now, the CSI 300 stocks trade near 5-year lows and Chinese stocks listed in Hong Kong are trading with the deepest discount to the mainland peers in 15 years, as the Chinese interventions are said to be less felt in Hong Kong than in the mainland. Today, though, the Chinese stocks are better bid because Chinese Premier Li Qiang called for more effective measures to stabilize the slumping Chinese stocks, but the truth is, investors left Chinese stocks because of the ferocious government crackdown on most loved Chinese companies. Nothing less than drastic financial support would be enough to bring investors back.

The Japanese stocks continue to be the bright spot among the Asian equity markets. The Bank of Japan’s (BoJ) negative interest rates, the cheap yen and the positive outcomes of the tech war between the US and China have been pushing the Japanese Nikkei index to multi-decade highs, and these factors are not ready to reverse just yet. Today, the BoJ didn’t only announce that it would keep the interest rates unchanged at -0.10% and the upper band for the 10-yer yield steady at 1%, but the bank lowered its inflation forecasts citing the decline in oil prices. We haven’t heard the BoJ presser at the time of writing but lowering inflation forecast highlights that there is no emergency to make any changes to the BoJ policy, even less so after a powerful earthquake hit the island at the very beginning of the year. On the contrary, if inflation – which is the bad side of low rates – is under control, the bank would do better to keep the rates low and its economy supported. As such, the USDJPY remains bid above the 148 level after the BoJ decision and before the post-decision presser. The long yen trade looks much less appetizing today than it did by the end of last year. Yet going short the yen is a risky option considering the rising risk of a verbal intervention when the USDJPY approaches the 150 level. Therefore, the USDJPY will likely waver between the 145/150 range, until there is more clarity about the timing of the BoJ normalization.

Elsewhere, the day is expected to unfold slowly. Investors will monitor the Richmond manufacturing index and await Netflix's earnings release. Additionally, attention is on Donald Trump, who has gained favoritism after Ron DeSantis withdrew his support and endorsed Mr. Trump for this year's presidential race. The potential impact of a Trump victory on financial markets is challenging to quantify; he may adopt a tougher stance on China, implement tax cuts, and increase spending, leading to mixed effects.

For those who missed out on the meme stock frenzy, it's however intriguing to observe Trump's special-purpose acquisition company, DWAC, which surged nearly 90% yesterday.

Bank of Japan Continues its Loose Monetary Policy

In focus today

Today, the primary election to become the Republican nominee for US presidential election 2024 heads to New Hampshire. Sunday, Ron DeSantis announced that he suspended his campaign and endorsed Donald Trump. The only other remaining candidate is Nikki Haley.

In the euro area, we will receive the quarterly ECB bank lending survey which will show how banks' credit standards changed in Q4 2023. Banks have tightened credit standards significantly since ECB started tightening monetary policy, while loan demand has been on a downward trajectory.

Early Wednesday we will get PMIs from Japan. PMIs will reveal whether the growth picture with modest declines in manufacturing activity and a strong service sector has continued.

Economic and market news

What happened overnight

The Bank of Japan (BoJ) kept its quantitative and qualitative easing with yield curve control policy unchanged this morning as expected. The policy rate stays at -0.1% and the 10-year yield target around 0, with the upper bound of 1.0 percent as a reference rate. BoJ has also published a new Economic Outlook. Inflation in the fiscal year (FY) 2024 has been revised 0.4pp lower to 2.4%, but the core inflation outlook remains unchanged at 1.9% for both FY2024 and FY2025. This was widely expected and thus the market reaction was muted. We expect the BoJ will be ready to start normalising policies at the April meeting when they are more certain that wage growth will pick up. A policy hike and releasing the grip on the yield curve are both at play but the normalisation pace will very much depend on the wage outlook and the pressure from softening among other major central banks.

In China, the authorities are considering a package of stimulus of USD 278 billion to stabilize the slumping equity market according to a Bloomberg article released overnight. The rumours are not confirmed by official sources. Hang Seng is up 2.7% this morning.

In the Red Sea, US and UK launched new joint air strikes against the Houthi rebels. It is the eighth time since 11 January that the US has hit Houthi targets responding to the Houthis' attacking container vessels passing through the Red Sea.

What happened yesterday

In Denmark, employment increased by 3200 in November compared to October. We still await signs that the expected economic slowdown is shown in employment data from Denmark.

Equities: Global equities ended higher yesterday after Europe and Japan caught up to the strong Friday performance in US. There was no one-sided rotation and no major macro release to push the market strongly in any direction. Hence, it looked more like investors were buying into the rally as they realized they had been missing out on the strong rally lately as growth and inflation outlooks have improved more than expected. Underscoring the "better-than-expected" economic outlook could also be seen from REITs doing fine together with small caps. Two industries/styles that still have more upside potential in the current falling inflation, falling yields and soft-landing narrative continues to unfold. In US yesterday, Dow +0.4%, S&P 500 +0.2%, Nasdaq +0.3% and Russell 2000 +2.0%. Asian markets are higher this morning with Chinese stocks leading the advances. Rumours were that China is working with a massive package to support domestic equity markets. That comes after the CSI 300 is hitting a five-year low. To put this into perspective, S&P500 and some other western indices reached new all-time highs again yesterday. Futures in Europe and US are flat this morning.

FI: Global bond yields declined across maturities with 10Y US Treasuries declining 2bp and 10Y German government bonds declining some 5bp. The ECB has been trying to push back on the market pricing of ECB policy, but there is still plenty discounted in rates, and thus supportive for bond yields. Furthermore, the 10Y Italian-German yield spread continues to tighten and is now trading at 150bp, which is a one-year low. However, spreads typically perform when the central banks are entering an easing cycle and with Italy back on stable outlook the risk of downgrade is low, and this is supportive for Italian government bonds relative to EU peers.

FX: As widely expected, the BoJ did not make any changes to monetary policy in the first meeting of 2024 in a unanimous decision. The market reaction was muted, with USD/JPY hovering around 148. EUR/USD stuck at 1.09. EUR/Scandies and EUR/CHF stable mostly sideways yesterday and overnight, while the GBP traded slightly on the weak side.

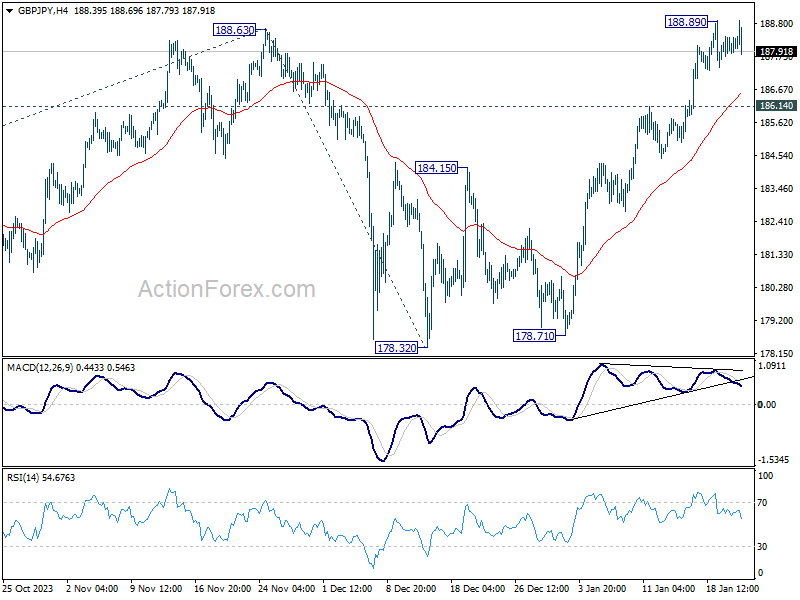

GBP/JPY Daily Outlook

Daily Pivots: (S1) 187.87; (P) 188.14; (R1) 188.51; More...

Intraday bias in GBP/JPY remains neutral as consolidation continues below 188.89. Further rally is expected as long as 186.14 resistance turned support holds. On the upside, break of 188.89, and sustained trading above 188.63 will confirm up trend resumption. Next target is 38.2% projection of 155.33 to 188.63 from 178.32 at 191.04.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

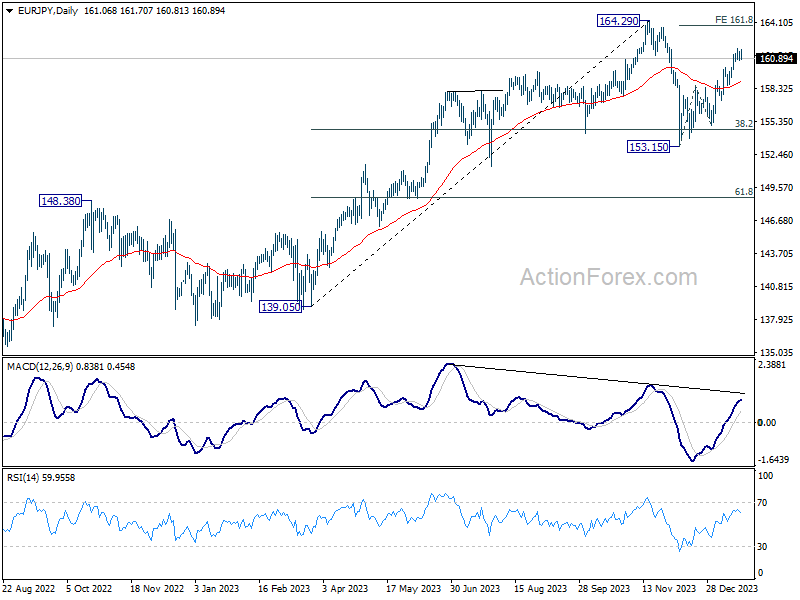

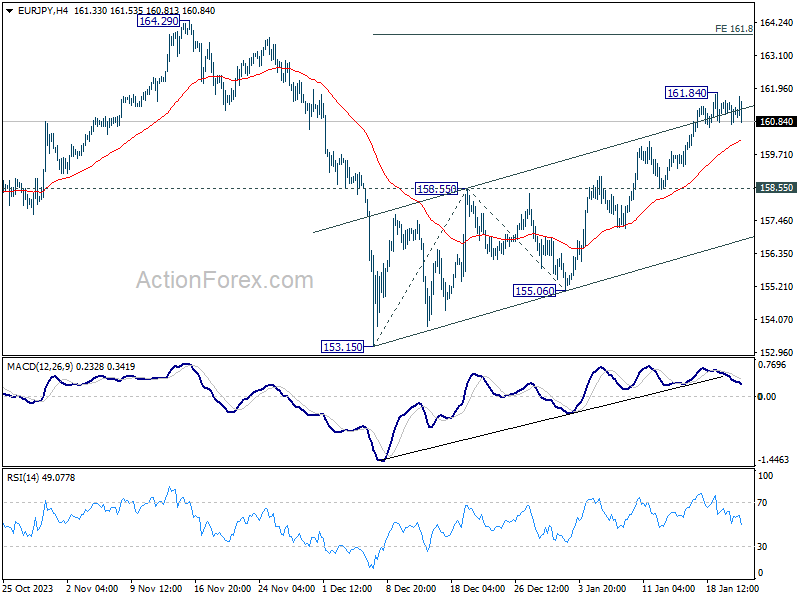

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.78; (P) 161.18; (R1) 161.60; More...

Intraday bias in EUR/JPY stays neutral for consolidations below 161.81. Even in case of deep retreat, further rally is expected as long as 158.55 resistance turned support holds. On the upside, break of 161.84 will resume whole rally from 153.15 to 161.8% projection of 153.15 to 158.55 from 155.06 at 163.79, which is close to 164.29 high.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage.