Sample Category Title

Brent Crude Oil Prices Inch Upwards Amid Demand Speculations

Brent crude oil prices are witnessing a moderate rise as the week begins, with the cost per barrel currently near $78.40. This upward trend is primarily influenced by the evolving outlook on energy demand. Recent macroeconomic data have cast some doubts on future demand, somewhat offsetting factors previously buoying prices, such as tensions in the Middle East.

Currently, Brent crude seems poised for a phase of consolidation within a specific price range. Despite some existing downward pressures, the ongoing geopolitical tensions in the Red Sea and the Gulf of Aden are maintaining a significant risk premium in crude oil prices. Market dynamics are also reflected in the backwardation between the current Brent price and its six-month futures, suggesting an anticipation of potential future oil supply limitations.

Brent Crude Oil Technical Analysis

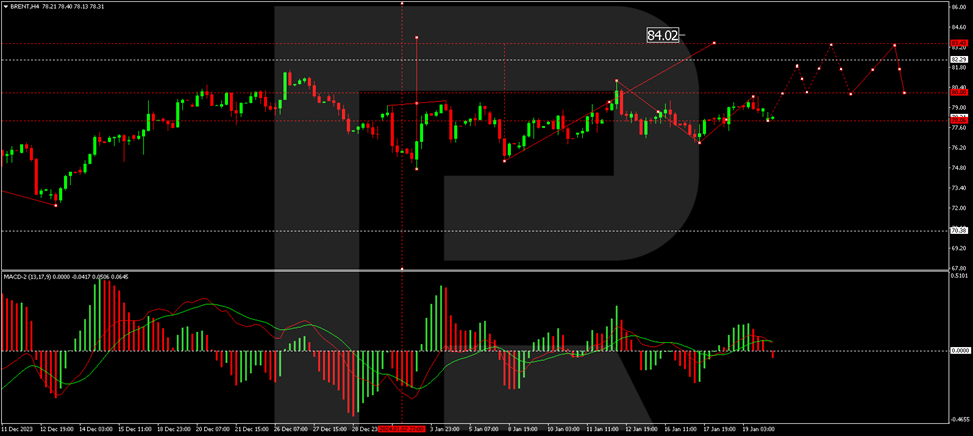

The H4 chart for Brent indicates a recent rise to $79.74, followed by a correction to $78.06. It's likely that a tight consolidation range will form above this level today. A break above this range could signal a growth trajectory towards $80.00, and potentially higher to $81.84 as a local target. The MACD indicator, with its signal line positioned above zero, supports the likelihood of continued growth.

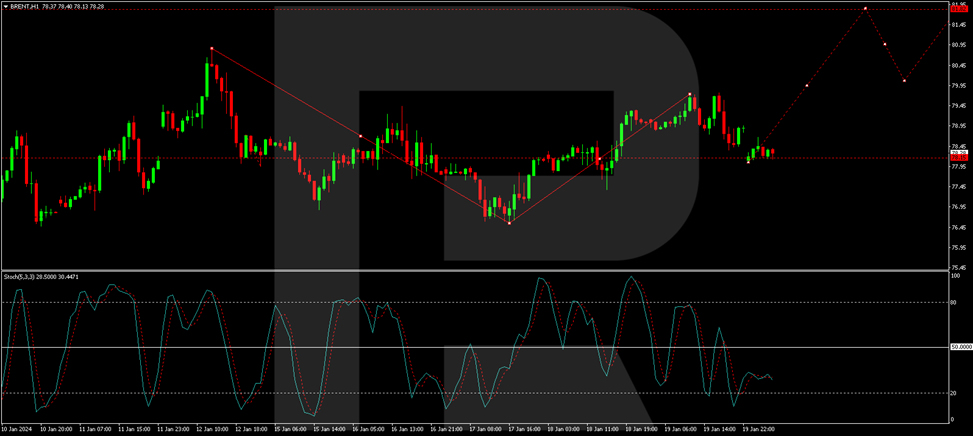

On the H1 chart, a correction phase appears to have concluded. The price may start ascending towards $79.79. Following this, a new consolidation phase around this level is anticipated. An upward breakout from this range could propel the price further to $81.84. This outlook is reinforced by the Stochastic oscillator, indicating a signal line trajectory from above 20, aiming towards 80.

Sunset Market Commentary

Markets

European stocks were off for a blazing start in the wake of new record highs on Wall Street (S&P 500, Down Jones) end last week. The EuroStoxx50 gapped >1% higher at the open before losing some momentum. US equities open higher as well, resulting in new highs for the major indices but the Nasdaq. Risk assets are still buoyed by market believe of economies slowing down enough to cool inflation while avoiding a painful recession. Such a scenario gives central banks all the reasons to kick off the monetary easing cycle. Core bond yields indeed slip several basis points today. German bonds outperform US Treasuries. Yields on the former had some minor catching up to do with a late-session swoon in US yields last Friday. Net daily changes currently vary between -4.2 bps (30-y) to -6.9 bps (-5y). The 10-year’s break above the 38.2% resistance level (2.32%) last week therefore doesn’t receive technical confirmation just yet. US yields are down 0.8 bps (2-y) to -3.8 bps (10-y). Using a magnifying glass, we spot some JPY outperformance on currency markets. Tomorrow morning’s BoJ meeting could upend that soon if governor Ueda keeps postponing (hints on) policy normalization. The main reason is that the central bank is not yet seeing enough signs of inflation getting anchored around the 2% target as long as there’s no virtuous cycle between wage and price growth. Prime minister Kishida today called upon companies for larger wage hikes, saying the country is at a critical point for escaping from deflation. USD/JPY eases to 147.47 after a blistering rally last week and, more broadly, all off 2024. EUR/JPY loses some ground to 160.88. Other cross rates including EUR/USD barely budge. EUR/GBP is back towards testing the 0.856 support area (December lows). A break would pave the way towards the August low of 0.849. This is not our preferred scenario

The European Union will tap the bond market tomorrow. It announced a dual tranche transaction comprising an increase of the EU 3.125% December 2030 and of the EU 3% March 2053 benchmark lines. The syndicated transaction is one of the six planned for the first half of 2024 along with seven bond auctions. The EU seeks to issue €75bn of long-term bonds during this period while setting the annual limit for all of 2024 at €160bn. The proceeds will be used to meet payments primarily related to NextGenerationEU (including possible payments under REPowerEU).

News & Views

Belgian consumer confidence fell from 0 to -2 in December, posting a first monthly decline since May. After last month’s rebound, household expectations for the general economic situation in Belgium deteriorated significantly (-14 from -9). On the other hand, consumers’ opinion on the trend in unemployment over the next twelve months remains unchanged (14). On a personal level, they expressed a bit more caution about their future financial situation (-1 from 1). Moreover, they revised their saving intentions very slightly upwards (21 from 20). Consumer confidence remains above its long term average of around -6. Belgian business confidence will be published on Thursday.

Polish retail sales (constant prices) rose by 11% M/M in December (vs 14.8% consensus). Compared with a year earlier, sales are down 2.3% (vs consensus +1.9% forecast). The decline was driven by an 11% decline in the sales of household goods, an 8.3% drop in newspapers, books and other sales in specialized stores, as well as a 6.4% fall in the sales of fuel. Average gross wages increased by 4.7% M/M & 9.6%Y/Y (vs 7.1% M/M & 12.1% Y/Y expected).

New Zealand Dollar Eyes Services PSI

- New Zealand releases Performance of Services Index on Tuesday

The New Zealand dollar is flat at the start of the week. In the European session, NZD/USD is trading at 0.6116, up 0.01%. It was a rough week for the New Zealand dollar, which declined 2% and fell to a five-week low.

New Zealand’s economy has struggled in the fourth quarter and the gauge of services activity, the Performance of Services Index (PSI) posted three contractions in the second half of 2023. The PSI improved to 51.2 in November, up from 49.2 in October, indicating weak growth. We’ll get a look at the December report on Tuesday.

China maintains benchmark lending rates

With global inflation on the decline, major central banks have likely ended their rate-tightening cycles and are looking to lower interest rates. In China, the central bank (PBOC) has been under pressure to lower rates due to the economic slowdown and deflationary pressures which have pushed up real borrowing costs. The PBOC has stood pat, not wanting to put further pressure on the yuan, which has fallen 1.4% in January against the dollar. The PBOC kept the one-year loan prime rate (LPR) at 3.45% and the five-year LPR at 4.20% on Monday, as expected. The decrease in economic activity is bad news for New Zealand, as China is its largest trading partner.

What a difference a week can make. In the case of Fed rate odds, the markets have become less confident that the Fed will press the rate-cut trigger in March. Just one week ago, the probability stood at 78% but that has fallen to 48% at present, according to the CME’s FedWatch tool. The Fed has pushed back against market expectations of six rate cuts this year, starting in March. Last week, Atlanta Fed President Bostic said he did not expect rate cuts until the third quarter and San Francisco Fed President Daly said the Fed would have to be “patient” about rate cuts.

NZD/USD Technical

- 0.6150 and 0.6211 and are the next resistance lines

- There is support at 0.6054 and 0.5993

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0877; (P) 1.0888; (R1) 1.0908; More...

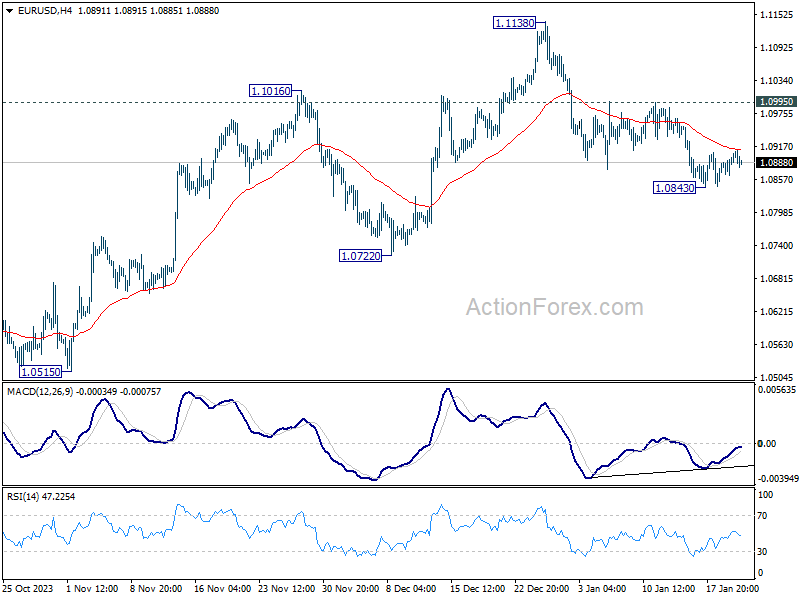

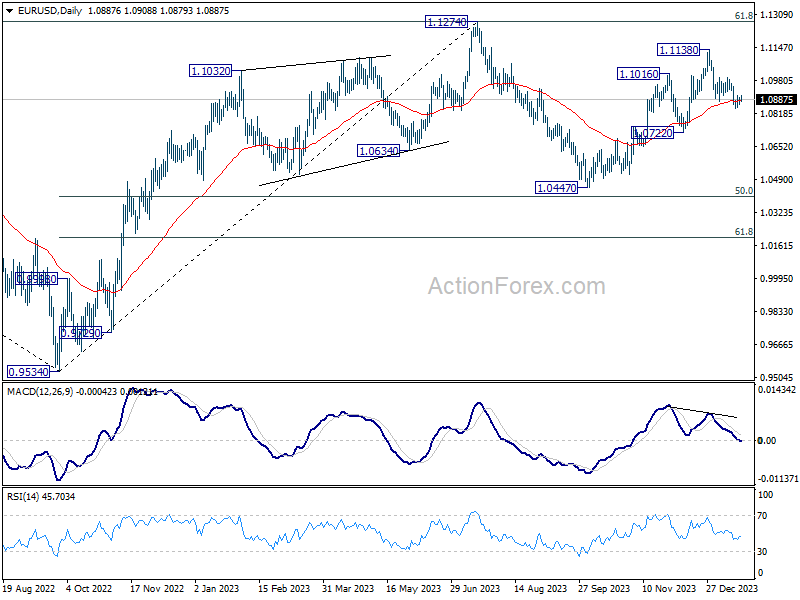

EUR/USD is extending the consolidation from 1.0843 temporary low, and intraday bias stays neutral. Further decline is expected as long as 1.0995 resistance holds. Below 1.0843 will target 1.0722 support next. Decisive break there will argue that whole rise from 1.0447 has completed, and target this low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

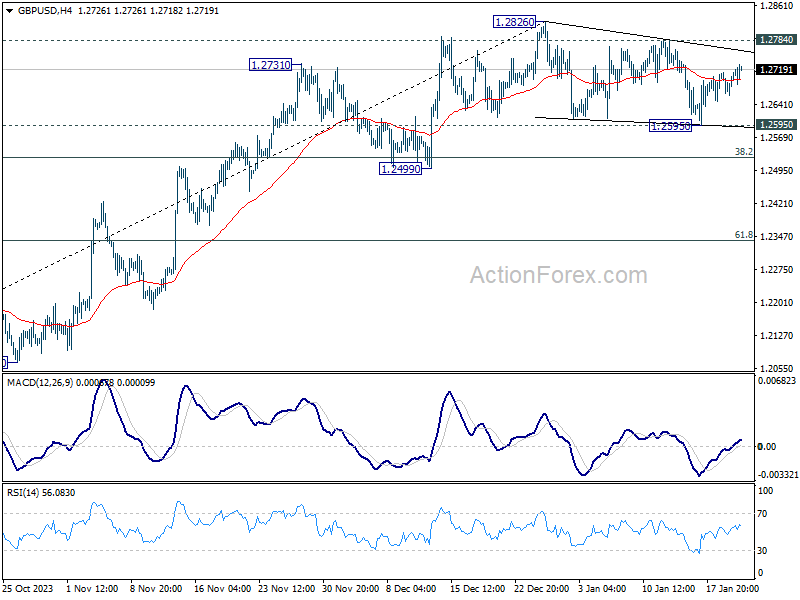

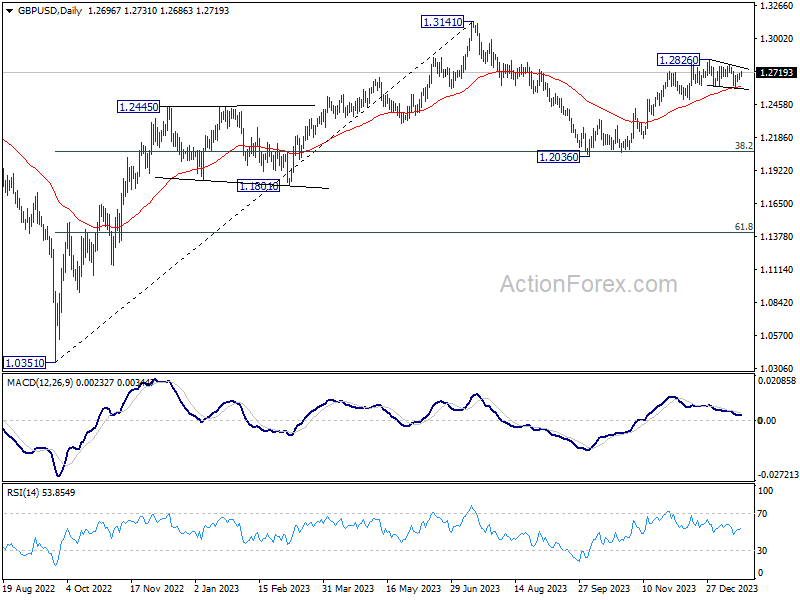

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2672; (P) 1.2694; (R1) 1.2725; More...

GBP/USD is still extending the consolidation pattern from 1.2826 and intraday bias stays neutral. Break of 1.2595 support will target 1.2499 support. On the upside, however, firm break of 1.2784 resistance will suggest that the consolidation pattern has completed. Further rally should then resume through 1.2826 towards 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

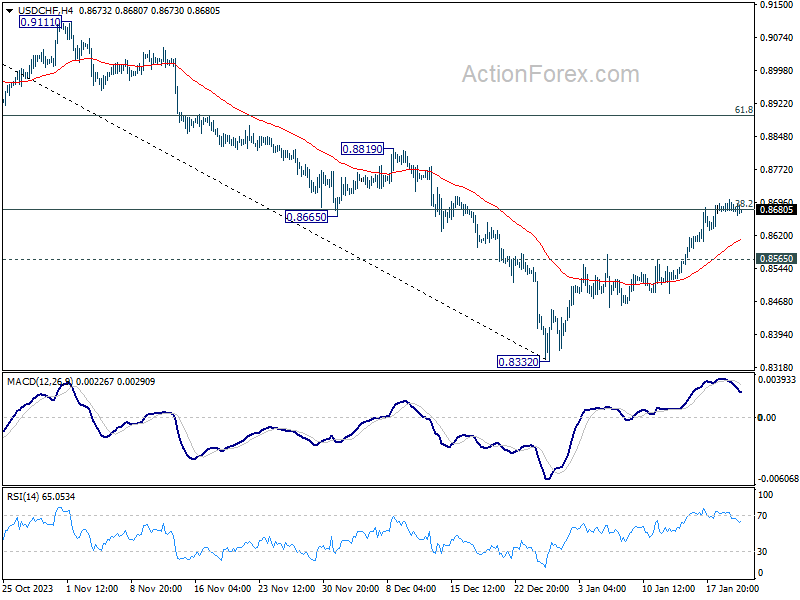

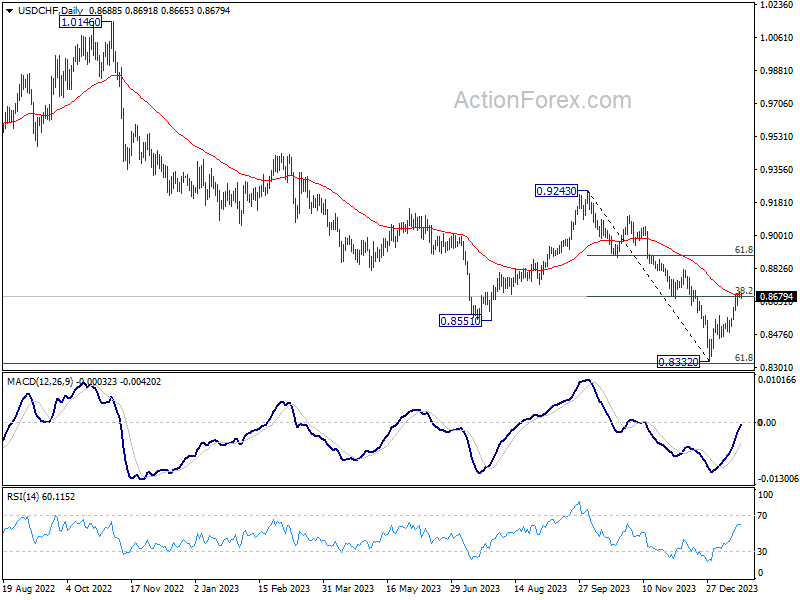

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8666; (P) 0.8685; (R1) 0.8700; More....

Intraday bias in USD/CHF stays neutral, with focus on 38.2% retracement of 0.9243 to 0.8332 at 0.8680, which coincides 55 D EMA (now at 0.8687). Decisive break there will turn near term outlook bullish for 61.8% retracement 0.8995. Nevertheless, break of 0.8565 minor support will turn intraday bias back to the downside for retesting 0.8332 low.

In the bigger picture, while rebound from 0.8332 could be strong, there is no clear sign of medium term bottoming yet. This rebound is tentatively seen as a corrective move for now. Also, outlook will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.

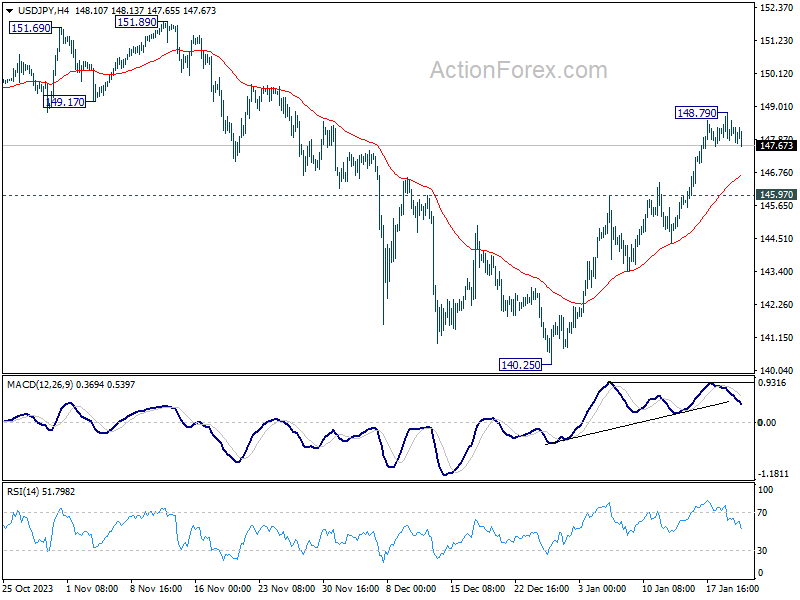

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.74; (P) 148.28; (R1) 148.71; More...

USD/JPY is extending the consolidation from 148.79 temporary top and intraday bias remains neutral. While deeper retreat cannot be ruled out, further rally is expected as long as 145.97 resistance turned support holds. Corrective fall from 151.89 should have completed at 140.25 already. Break of 148.79 will resume the rise from there for retesting 151.89/93 key resistance zone.

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 141.89) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.

Yen Strengthens Modestly Ahead of BoJ Decision; Forex Markets Quiet

Yen trades mildly firmer in tight range today, as markets are now keenly awaiting BoJ rate decision in the upcoming Asian session. No change in monetary policy is expected as BoJ should stick to negative interest rate for now. There is also no need to tweak the parameters of Yield Curve Control, with the yield curve being smooth without any distortion.

A critical aspect of the BoJ meeting will be the new quarterly economic projections. The market is particularly interested in whether the central bank projects core inflation to remain around 2% target throughout the forecast period. This projection is a key prerequisite to continue speculating on a rate hike in April.

In the broader forex markets, trading activity has been relatively subdued today, with most major currency pairs and crosses remaining within the range set on Friday. Yen has emerged as the stronger one, followed by Sterling and New Zealand Dollar. On the weaker side, Euro, Australian Dollar, and Swiss Franc are lagging, while Dollar and Canadian are showing mixed performance.

Technically, Nikkei's up trend resumed today and hit another 34-year high. Near term outlook will stay bullish as long as 35371.25 support holds. Next target is 161.8% projection of 30538.28 to 33853.46 from 32205.38 at 37651.22.

In Europe, at the time of writing, FTSE is up 0.07%. DAX is up 0.40%. CAC is up 0.39%. UK 10-year yield is down -0.0535 at 3.882. Germany 10-year yield is down -0.064 at 2.284. Earlier in Asia, Nikkei rose 1.62%. Hong Kong HSI fell -2.27%. China Shanghai SSE fell -2.68%. Singapore Strait Times fell -0.10%. Japan 10-year JGB yield is down -0.0152 at 0.654.

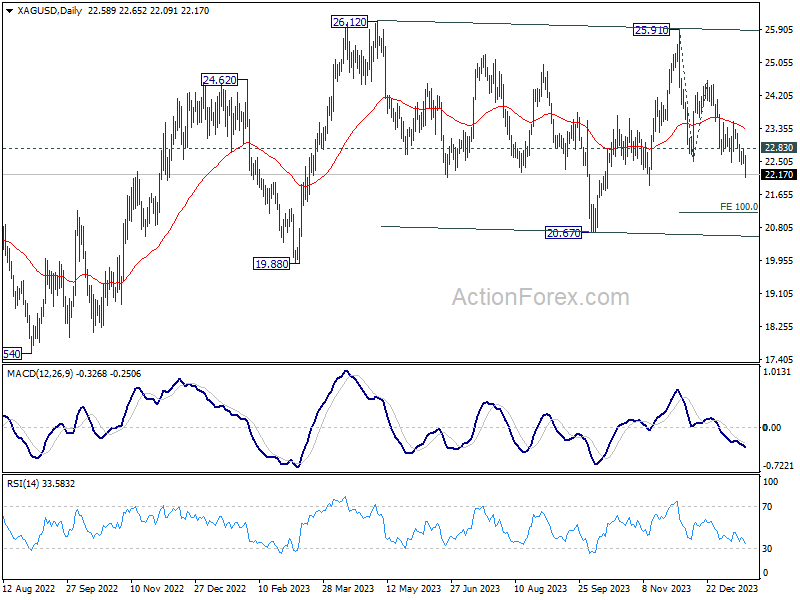

Silver tumbles amid rate cut expectation adjustments

Silver falls steeply today as the decline from 25.91 resumes. This steep selloff in the precious metal is interpreted, at least partly, as a reaction to the recent market adjustments in global central bank rate cut expectations. With the anticipation of prolonged high interest rates, the opportunity cost of holding precious metals like Gold and Silver remains elevated, putting additional pressure on their prices.

Technically, near term outlook in Silver will stay bearish as long as 22.83 resistance holds. Next target is 100% projection of 25.91 to 22.50 from 24.59 at 21.18.

Price actions from 26.12 are seen as a sideway consolidation pattern from with decline 25.91 as the third leg. While break of 20.67 cannot be ruled out, strong support should be seen 19.88 and 20.67 to conclude the fall from 25.91, as well as the sideway pattern.

PBoC holds 1-yr and 5-yr LPR steady

People's Bank of China announced today that it would maintain one-year loan prime rate at 3.45%, a level unchanged since August last year. Similarly, five-year rate, critical for mortgage financing, remains steady at 4.2%, consistent since its last reduction in June. This decision follows PBoC's unexpected move last week to keep its medium-term lending facility rate stable.

PBoC's decision to hold rates steady comes amid a sluggish economic environment in China, coupled with increasing deflationary pressures. Despite these challenges, the central bank appears reluctant to employ interest rate reductions as a tool to stimulate the economy, primarily due to concerns over the depreciating Yuan. PBoC might continue to avoid further rate cuts until Yuan regains some stability, to prevent exacerbating the currency's depreciation.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.74; (P) 148.28; (R1) 148.71; More...

USD/JPY is extending the consolidation from 148.79 temporary top and intraday bias remains neutral. While deeper retreat cannot be ruled out, further rally is expected as long as 145.97 resistance turned support holds. Corrective fall from 151.89 should have completed at 140.25 already. Break of 148.79 will resume the rise from there for retesting 151.89/93 key resistance zone.

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 141.89) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 15:00 | USD | Leading Index M/M Dec | -0.30% | -0.50% |

ECB Meeting: Summer Rate Cut in Focus Amid Pushback by the Hawks

- ECB faces a communication challenge in first meeting of the year

- Timing of rate cut likely to dominate discussion, but hawks to resist

- Mixed messages unhelpful to euro ahead of the decision on Thursday (13:15 GMT)

- Flash PMIs on Wednesday (11:00 GMT) on the agenda too

Progress on inflation may be slowing

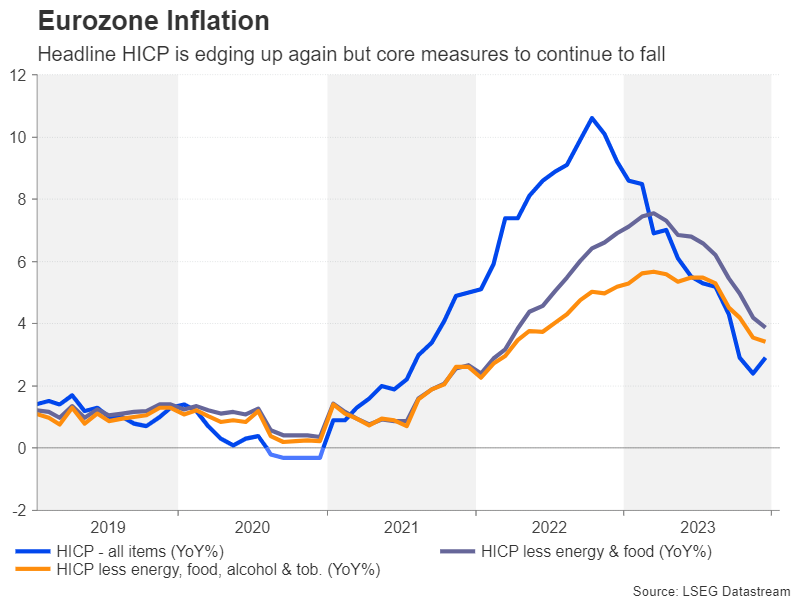

After inflation shot up to double digits in 2022, it’s fair to say that 2023 has been a more successful year for the European Central Bank. The annual rate of change in the Eurozone’s Harmonised Index of Consumer Prices (HICP) started the year at 8.6%. By December, it had fallen to 2.9%.

However, this was an uptick on November’s figure of 2.4%, marking the first increase since April. Policymakers expect this unwelcome reversal to continue in the first few months of 2024. With last year’s plunge in energy prices slowly dropping out of the calculations and energy subsidies across the bloc being phased out, HICP will likely soon pop back above 3.0%.

On the bright side, underlying inflation in the euro area has maintained its downward trajectory, so policymakers are reasonably confident that inflation is well on its way to hit their 2% target by 2025.

ECB wary of upside risks to inflation

There are risks, however. Wage growth in the Eurozone remains elevated despite sluggish economic growth. President Christine Lagarde has hinted that how the wage landscape evolves by late spring will be crucial to any decision on policy easing. But perhaps a bigger threat in the fight against inflation is the latest crisis in the Middle East.

The attacks by Houthi rebels on vessels passing through the Red Sea have intensified to the extent that many companies are suspending shipping through this route, instead rerouting ships around the Horn of Africa. This significantly increases the cost for European businesses importing goods from Asia. Without a de-escalation of tensions in the region, this temporary supply shock could turn into a major headache for the ECB.

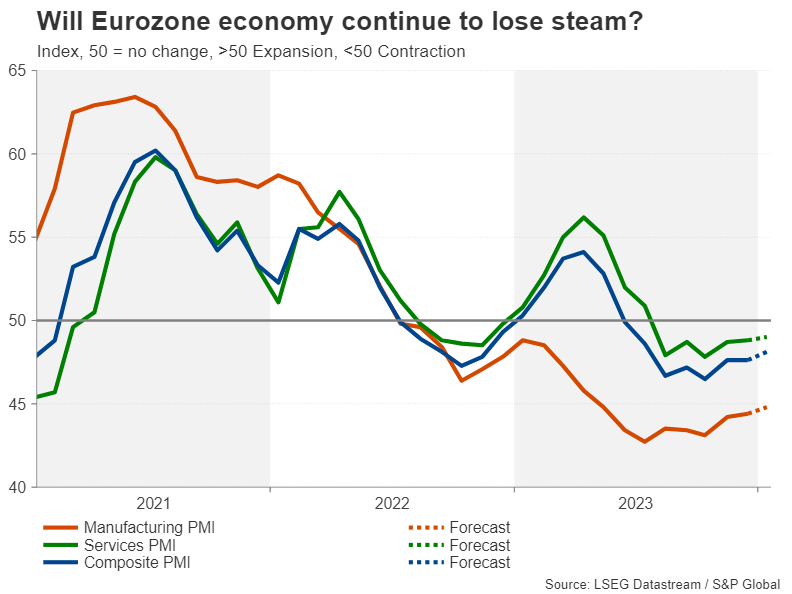

Flash PMIs eyed as Eurozone on verge of recession

It’s likely therefore that policymakers will maintain their data-dependent approach on Thursday, while repeating that “policy rates will be set at sufficiently restrictive levels for as long as necessary”. In the absence of fresh macroeconomic projections at the January meeting, investors will turn to Lagarde’s press briefing at 13:45 GMT for an updated view on the economy and the inflation outlook.

Recession risks have heightened again lately for the euro area, as business activity has failed to pick up substantially from the summer dip. The PMI surveys suggest Eurozone GDP is headed for a second consecutive quarter of contraction in the final three months of 2023. The flash readings for January are due a day before the ECB meeting and should they point to more misery for businesses at the start of the new year, the euro will probably go into the ECB decision on the backfoot.

Can euro’s uptrend stay intact?

Gloomy PMI numbers and a not-so-hawkish tone by Lagarde would potentially be the worst outcome for the single currency this week. The euro could breach its medium-term ascending trendline in such a scenario, which would set the stage for a test of the 50.0% and 61.8% Fibonacci retracement levels of this upleg at $1.0793 and $1.0711, respectively.

Alternatively, if Lagarde draws attention to June as the earliest time when policymakers will have enough data to consider whether rates should be cut, euro/dollar could stabilize around its 200-day moving average (MA) in the $1.0845 region. But for the pair to recover, Lagarde would need to additionally throw cold water on the prospect of the ECB slashing rates by anywhere near as much as what markets have priced in. Even after the latest pushbacks, cumulative bets for 2024 stand at 130 basis points. An improvement in the PMIs would also be essential for a euro rally.

Any rebound in euro/dollar could stretch towards the December peak of $1.1139, with obstacles likely to be found at the 50-day MA near $1.0920 and the 23.6% Fibonacci of $1.0976.

Davos deals a blow to dovish bets

ECB officials attending the World Economic Forum in Davos last week signalled they’re open to rate cuts in the summer if inflation stays on the right path, with Lagarde throwing her weight behind this timeline too. The more hawkish members of the Governing Council have been somewhat more reluctant to commit to a specific timeframe. But what is increasingly certain is that any hope of a March pivot has been dashed, and until the ECB is ready to flag its first rate cut, the euro could end up drifting sideways.