Sample Category Title

Will US GDP Surprise to the Upside?

- US will release GDP growth data at 13:30 GMT on Thursday

- An upside surprise seems more likely than a disappointment

- Dollar could benefit from a beat, as Fed cut bets are unwound

Dollar comes back to life

The US dollar started the new year on a strong note. A series of economic indicators have reaffirmed the resilience of the US economy lately, forcing traders to reconsider how quickly and how deep the Fed will cut interest rates this year.

Investors now see just a 45% probability that the Fed will cut rates in March, down from nearly 90% last month. This rethink follows the latest prints on inflation and retail sales, which came in stronger than anticipated, challenging the notion that the US economy is losing steam.

With the labor market also remaining in good shape, there doesn't seem to be any urgency to slash rates immediately. Several Fed officials have argued the same point lately, stressing that markets have gone overboard with pricing in such heavy rate cuts, and that the actual pace of rate reductions will likely be slower than what traders expect.

An upside GDP surprise?

With the prospect of a rate cut in March now priced almost like a coin toss, the upcoming GDP stats will be crucial in tipping the scales, driving the dollar accordingly. Economists expect the US economy to have grown at an annualized pace of 1.8% during the final quarter of 2023, driven by heavy government spending and solid consumption.

As for any surprises, a stronger-than-expected GDP print seems more likely than a disappointment. This is mostly because of the Atlanta Fed GDPNow model, which currently estimates growth at 2.4%, significantly higher than the official forecast.

This model has a solid track record in terms of predicting actual GDP numbers, and if it proves accurate this time as well, the dollar would likely benefit as investors continue to unwind bets of rapid Fed rate cuts.

Looking at the charts, euro/dollar has been in a steady decline so far this year. Another round of encouraging US data could add fuel to this selloff, pushing the pair down towards its recent low of 1.0840, a region that also encapsulates the 200-day simple moving average.

On the flipside, a disappointing GDP reading would likely propel euro/dollar higher, with the 1.1000 zone likely to act as the first major barrier to any advances.

Beyond the GDP data, another important release this week will be the latest core PCE price index on Friday.

Can the dollar keep rising?

All told, the outlook for the dollar still appears quite bright. The US economy is in much better shape than other major regions such as the Eurozone, which might already be in a minor technical recession.

With economic growth differentials favoring the United States, there's a clear risk that the Fed will cut interest rates at a slower pace than the ECB will during this cycle, keeping the dollar supported. Historically speaking, the dollar often thrives in late-cycle environments, especially if the US economy is healthier than the rest of the world.

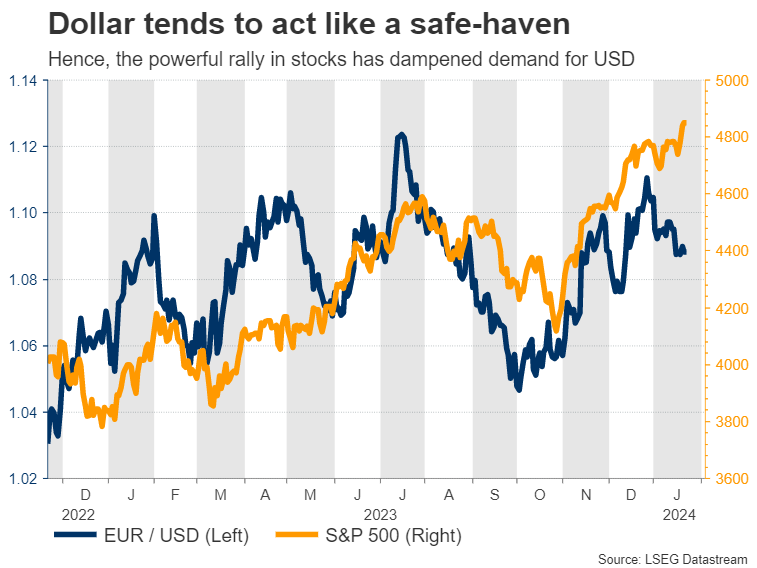

Finally, it's worth noting that the powerful rally in stock markets has dampened demand for safe haven instruments like the dollar in recent months. If this rally loses some steam and valuations compress now that investors have started to scale back rate cut bets, it could be another element that helps the dollar advance.

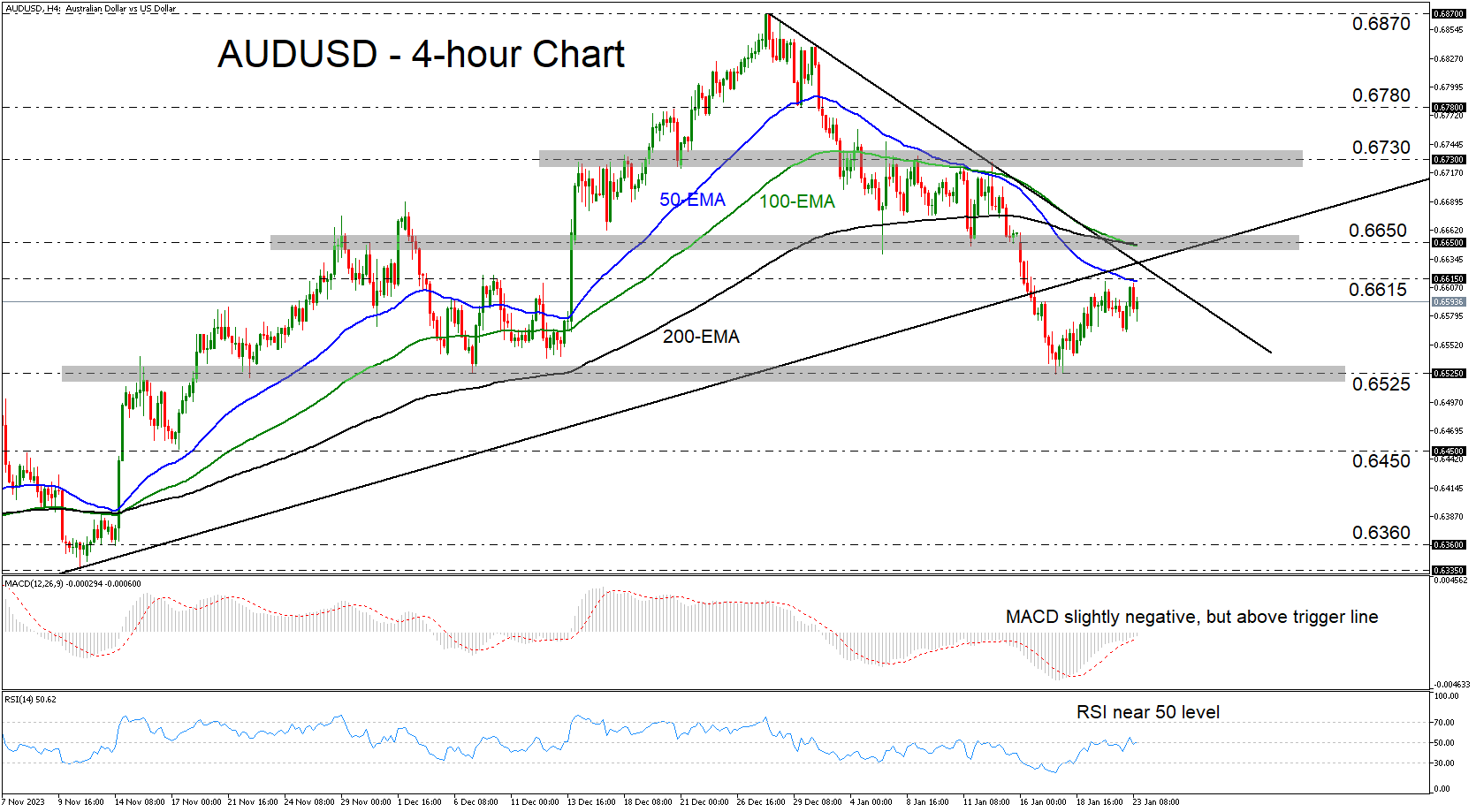

AUDUSD Recovers, But Remains Below Prior Uptrend Line

- AUDUSD recovers after hitting 0.6525

- But the bulls struggle below key resistance crossroads

- This increases the chances for another strike by the bears

AUDUSD entered a recovery mode after it hit support near the key zone of 0.6525. However, the bulls seem to be struggling to overcome the 0.6615 level and the 50-period EMA, with the pair staying below the prior uptrend line drawn from the low of October 26, and below a short-term term downside resistance line taken from the high of December 28. This means that the bears may still be hiding behind the bushes, waiting for the perfect time to attack.

The short-term oscillators corroborate the notion that the bulls have not gained full control yet. The RSI continues to oscillate around its equilibrium 50 line, while the MACD, although above its trigger line, remains slightly negative and is showing signs that it could turn south again soon.

If indeed the bears jump into the action again soon, they may initially dive towards the 0.6525 zone, the break of which would confirm a lower low and perhaps allow declines all the way down to the 0.6450 area, defined as support by the low of November 17.

For the short-term outlook to brighten, the pair may need to climb above the 0.6650 zone. This would confirm the upside violation of both the aforementioned diagonal lines and also take the pair above all three of the plotted EMAs. The bulls may then get encouraged to march towards the 0.6730 territory, which has been acting as a ceiling since the beginning of the year.

Recapping, AUDUSD recovered decently last week, but the advance remained limited below a prior uptrend line, suggesting that the bears could still attempt an attack anytime soon.

Euro Steady, Eyes PMIs

The euro is showing limited movement on Tuesday. In the North American session, EUR/USD is trading at 1.0866, down 0.15%.

Eurozone, German PMIs expected to remain in contraction

The eurozone economy is sputtering and the road to recovery is likely to be a long one. Manufacturing and services PMIs are useful gauges of economic activity and the news has been grim. Both the eurozone and Germany, the largest economy in the bloc, are grappling with prolonged contraction in the manufacturing and services sectors, with readings below 50. This is not expected to improve anytime soon, and the December PMIs, which will be released on Wednesday, are projected to remain in contraction territory.

ECB President Lagarde sounded hawkish at the December meeting, as she pushed back against expectations of rate cuts, saying that inflation could rebound and that there was no discussion of rate cuts at the December meeting. Lagarde was singing a different tune last week in Davos, as she acknowledged that a rate cut was likely in the summer. The markets have priced in 140 basis points of cuts this year, although ECB members have warned that the markets are getting ahead of themselves. The ECB meets on Thursday and investors will be keeping a close eye on the ECB rate statement and Lagarde’s follow-up press conference at Thursday’s meeting.

The markets were abuzz with excitement in December when Fed Chair Powell jumped on the rate-cut bandwagon. That optimism has dissipated somewhat as a March rate cut is looking less likely. A month ago, a quarter-point cut in March was priced at 75%; that has dropped to 42% currently, according to the CME’s FedWatch tool. Fed members continue to raise doubts about a March cut and are talking about two or three cuts this year, compared to the six cuts priced in by the markets. US economic data has been solid, which means that the Fed isn’t under pressure to lower rates right away.

EUR/USD Technical

- EUR/USD pushed below two support levels and has support at 1.0842

- There is resistance at 1.0891

NZD/USD Stems Slide, Inflation Next

- New Zealand Services PSI eases to 48.8

- New Zealand inflation expected to ease to 0.5%

The New Zealand dollar has edged higher on Tuesday. In the North American session, NZD/USD is trading at 0.6086, up 0.17%.

New Zealand’s economy has struggled in the fourth quarter and a soft services release won’t help things. The Performance of Services Index (PSI) slipped to 48.8 in December, a four-month low. This followed a November reading of 51.1. A reading below 50 indicates contraction. The low reading was driven by concerns over the cost of living and the economic slowdown.

New Zealand releases fourth-quarter inflation on Wednesday. The consensus estimate stands at 0.50% q/q, compared to 1.8% in the third quarter. On an annual basis, inflation fell in Q3 from 6.0% to 5.6% and the downtrend is expected to continue in the fourth quarter with a reading of 4.7%.

Another drop in inflation will put pressure on the Reserve Bank of New Zealand to lower interest rates from the current benchmark rate of 5.5%. The RBNZ hasn’t raised rates since April but has pushed against market expectations for a rate cut and warned that rate hikes are not off the table. The RBNZ doesn’t meet until February 28.

The markets were exuberant in December when Fed Chair Powell jumped on the rate-cut bandwagon. That excitement has dissipated somewhat as a March rate cut is looking less likely. A month ago, a quarter-point cut in March was priced at 75%; that has dropped to 42% currently, according to the CME’s FedWatch tool. Fed members continue to raise doubts about a March cut, saying that the markets are getting ahead of themselves. US economic data has been solid, which means that the Fed isn’t under pressure to lower rates right away.

NZD/USD Technical

- NZD/USD is tested resistance at 0.6096 earlier. Above, there is resistance at 0.6119

- There is support at 0.6052 and 0.6029

Sunset Market Commentary

Markets

The main ‘news’ for (global) trading was already available from the BoJ policy decision early this morning. However, the impact especially on global bond markets was close to non-existent. The Bank left the parameters of its policy (-0.1% policy rate, 0.0% target for the 10-y yield with an allowed deviation of 1.0%), unchanged. The Bank downwardly revised its projection for inflation in fiscal 2024 (2.8 to 2.4%) but grew slightly more confident that inflation might sustainably move to the target over the policy horizon (2025 forecast from 1.7% to 1.8%). The ongoing wage negotiations will be key to decide whether the BOJ can leave the era of negative interest rates behind. A assessment might come at the April meeting (or later in spring). Japanese bond yields reversed an initial decline. The 10-y yield closed marginally higher (+1.3 bps at 0.67%). However, the prospect on real BOJ normalization remains too diffuse to have any impact on global markets for now. Similar story for the yen. The Japanese currency tried to rally after Ueda’s press conference, but there is to little hard evidence on timing and the degree of potential BOJ normalization going forward. USD/JPY briefly dropped to the 147 area to again trade little changed near 148.

Very few data in the EMU and the US today, with the ECB January lending survey the exception to the rule. The report showed a moderate further tightening of credit standards for loans to firms. Banks also reported a further net tightening of their credit standards for loans to households. This was small for loans for house purchases and more pronounced for consumer credit and other lending to households. Demand for loans by firms and households also continued to decrease substantially, albeit less steeply than in the previous quarter. The data suggest that ECB policy is further filtering through into the economy. However, it looks that the sharpest tightening might be behind as the ECB as finalized its rate hike cycle. We don’t draw too firm conclusions, but if credit providing to the economy stabilizes due to markets anticipating some ECB easing further down the road this, ceteris paribus, leaves the ECB room to keep a wait-and-see approach with no need to rush to preemptively ease policy. Whatever, the impact on markets was limited. German yields are changing between 0.5 bps (2-y) and +5 bps (30-y), with the rise mainly starting after US traders joined. In technical trading, US yields show a similar steepening move (2-y +1.5 bps; 30-y +4.5 bps) counting down to tomorrow’s PMI’s and Thursday’s GDP release. The rally in equity markets is taking a breather, but there are no signs yet of change in trend (Eurostoxx 50 -0.35%, S&P little changed at the open). EUR/USD showed some intraday swings, with the dollar winning on points. The EUR/USD 1.085 support area is again coming on the radar (currently 1.086). EUR/GBP is extensively testing the 0.855 support area.

News & Views

Hungary’s Ministry of Economy suggested replacing the reference rate used in bank lending for the yield on Treasury Bills. Commercial banks currently add a margin to the Bubor interbank rate in determining the interest rate for loans. There is, however, a spread of more than 200 bps over yields on T-bills with the same tenor. Switching the reference would thus basically come down to significant easier financial conditions, typically the domain of the Hungarian central bank. The latter has been lowering policy rates steadily and is even eying bigger steps from next week on (100 bps) due to favourable inflation outcomes in recent months. But Economy Minister Nagy, amongst others, has lashed out several times already about real interest rates being too high and choking off the economy. The Hungarian forint extended losses after the report hit the wires, joining a regional move lower but underperforming peers. EUR/HUF is testing recent highs in the 385 zone.

In a draft document seen by the Financial Times, the European Commission estimated that the EU must invest about €1.5 trillion per year between 2031 and 2050 if it wants to cut greenhouse gas emissions by 90% by 2040 and reach net zero by the middle of the century. It’s an enormous amount that would nevertheless outweigh the cost of inaction as the effects of global warming become increasingly apparent through extreme weather events, the document explained. The numbers come in addition to the Commission’s estimation of an annual €360bn investments needed to reach the bloc’s 2030 goal, which include a legally-binding interim target of 55% reduction of greenhouse gases.

Forex Markets Lack Clear Theme; Yen Rebounds Briefly, EUR/GBP Resumes Downtrend

Identifying a singular driving theme proves challenging In today's forex market. Japanese Yen made an attempt to rebound following BoJ Governor Kazuo Ueda's post-meeting press conference, where he hinted at the potential of a future rate hike. However, this rebound was short-lived, and Yen soon reverted to its familiar tight trading range, indicating that the market is uncertain on when the anticipated rate move would happen. Dollar, despite being lower on the performance chart, is showing signs of gaining momentum against European majors as the market enters into the US session.

Australian Dollar is have broad gains, partly fueled by reports that China is considering a stock market rescue package. Though, Aussie remains confined within yesterday's range against most currencies, except Euro and Canadian Dollar.

A more significant movement is observed in EUR/GBP, which has broken through last week's low, extending its recent downtrend. This move could indicate that traders are positioning themselves ahead of tomorrow's PMI data from Eurozone and UK, anticipating potential shifts in contrasting economic outlooks.

Technical, Yen pairs are seen as staying in consolidations only, despite today's pull back. Near term outlook of Yen remains generally bearish. This view will continue to hold as long as 145.97 support in USD/JPY, 158.55 support in EUR/JPY, and 186.14 support in GBP/JPY hold.

In Europe, at the time of writing, FTSE is up 0.08%. DAX is up 0.08%. CAC is down -0.18%. UK 10-year yield is up 0.046 at 3.965. Germany 10-year yield is up 0.018 a 2.312. Earlier in Asia, Nikkei fell -0.08%. Hong Kong HSI rose 2.63%. China Shanghai SSE rose 0.53%. Singapore Strait Times fell -0.44%. Japan 10-year JGB yield fell -0.0168 at 0.637.

NZD/USD losing downside momentum as NZ CPI awaited

One of the spotlights will turn to New Zealand's inflation data in the upcoming Asian session. Market are expecting quarterly CPI to rise 0.5% qoq in Q4, slowed from Q3's 1.8% qoq. Annually, CPI is expected to fall from 5.6% yoy to 4.7% yoy.

Should these predictions materialize, the results would fall significantly below RBNZ's forecast from the November Monetary Policy Statement, which projected 0.8% qoq and 5.0% yoy, although the annual rate remains well above 1-3% target band.

There is a divergence of opinions regarding RBNZ's interest rate path this year. While some economists hold the view that OCR will remain at 5.50% through 2024, 2-year swap market is fully pricing in an OCR cut as early as May. Therefore, the inflation data set to be released tomorrow is poised to play a critical role in reshaping these rate cut expectations.

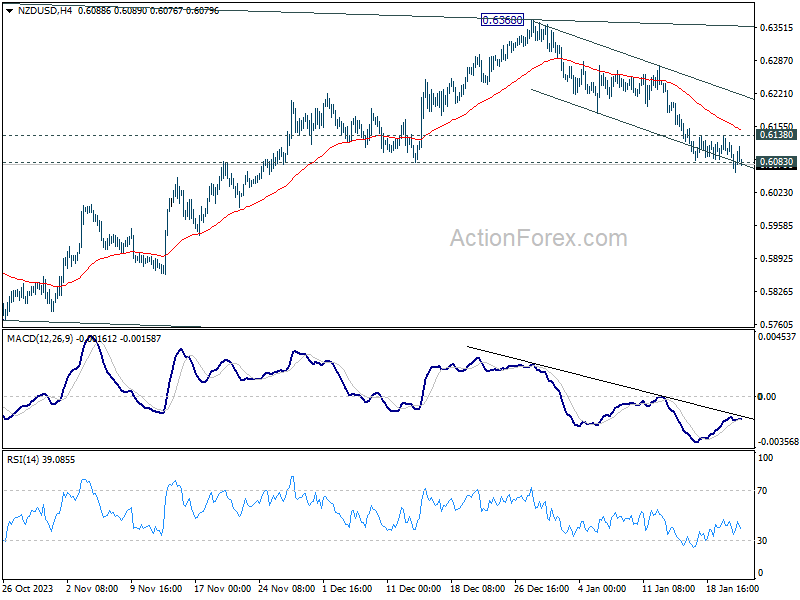

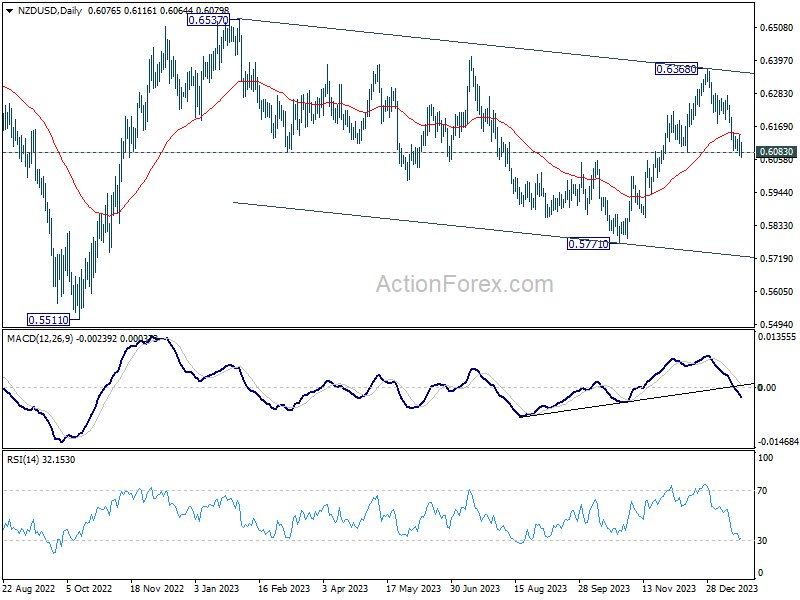

NZD/USD's fall from 0.6368 lost much momentum after breaching 0.6083 support, but there is no sign of a rebound yet. Sustained break of 0.6083 will strengthen the case that this decline is the third leg of the corrective pattern from 0.6537, and target 0.5771 support next. Nevertheless, break of 0.6138 minor resistance will neutralize immediate bearishness, and bring recovery first.

BoJ's Ueda elaborates on inflation and wages, hinting at future policy shifts

During his post-meeting news conference, BoJ Governor Kazuo Ueda confirmed that the economy is aligning with the central bank's inflation projections, adding "our core-core inflation forecast is at 1.9%, very close to our 2% target". This closeness, he explained, significantly contributes to BoJ's growing confidence in sustainably achieving its price target.

However, Ueda acknowledged the challenges in quantifying the exact progress towards this goal. He pointed out that recent movements in service prices have been influenced by several one-off factors and that consumption weakness is impacting these prices. BoJ is analyzing these trends by separating such factors, and Ueda believes that, despite these complexities, "service inflation is gradually accelerating as a trend."

Ueda also addressed the timing of monetary policy adjustments in relation to wage negotiations. He suggested that waiting for the outcome of wage talks across all firms, including smaller ones, would be impractical due to the extended timeframe this would require. BoJ, therefore, intends to use various economic indicators and data from hearings to predict wage trends. Ueda emphasized the influence of larger firms' wage negotiations on smaller firms and the availability of data on smaller firms' profit outlooks as potential early indicators.

BoJ holds steady, with CPI core-core projected at 1.9% in next two fiscal years

BoJ left monetary policy unchanged as widely expected. The forecast for fiscal 2024 CPI core was downgraded, whereas fiscal 2025 CPI core forecast saw a slight upgrade. Notably, CPI core-core forecasts for fiscal 2024 and 2025 were left unchanged at 1.9%, indicating a steady path towards achieving Japan's 2% inflation target sustainably.

Under Yield Curve Control, BoJ kept short-term policy interest rate unchanged at -0.1%. Additionally, target for 10-year JGB yield remains around 0%, with an allowance for fluctuation below 1.0% upper bound. These decisions were made by unanimous vote.

BoJ noted, "Consumer inflation is likely to increase gradually toward the BoJ's target as the output gap turns positive, and as medium- to long-term inflation expectations and wage growth heighten." The central bank also acknowledged the growing "likelihood" of realizing this outlook, albeit with an emphasis on the continued "high uncertainties" surrounding future developments.

In the median economic projections:

- Fiscal 2023 GDP growth at 1.8% (down from October's 2.0%).

- Fiscal 2024 GDP growth at 1.2% (up from 1.0%).

- Fiscal 2025 GDP growth at 1.0% (unchanged).

On the inflation front:

- Fiscal 2023 CPI core at 2.8% (unchanged).

- Fiscal 2024 CPI core at 2.4% (down from 2.8%).

- Fiscal 2025 CPI core at 1.8% (up from 1.7%).

- Fiscal 2023 CPI core-core at 3.8% (unchanged).

- Fiscal 2024 CPI core-core at 1.9% (unchanged).

- Fiscal 2025 CPI core-core at 1.9% (unchanged).

Australia's NAB business confidence rises to -1 amidst slowing price growth

Australia NAB Business Confidence fell rose from -8 to -1 in December. However, Business Conditions fell from 9 to 7. The decline was observed across several key areas: Trading conditions dropped from 13 to 10, while Employment conditions also decreased slightly from 8 to 7. Profitability conditions remained steady at 6.

NAB Chief Economist Alan Oster noted that "confidence and conditions are softest in manufacturing, retail and wholesale," attributing this to consumers cutting back on spending over time. Although there was a pickup in confidence within the retail sector in December, Oster expressed caution, stating that "it remains to be seen if this will be maintained."

Another significant development was the sharp decline in price and cost growth. Labor cost growth eased to 1.8% in quarterly equivalent terms, down from 2.3%. Purchase cost growth also declined from 2.5% to 1.6%. Overall price growth slowed from 1.2% to 0.9%, with notable decrease in retail price growth from 1.8% to 0.6%.

Oster highlighted the significance of this decline in retail price growth, attributing it in part to the sales periods around Black Friday and Christmas. He remarked, "The marked fall in retail price growth in December... is nonetheless an encouraging sign that inflation may have eased at the end of the quarter."

New Zealand BNZ services falls to 48.8, back in contraction

New Zealand BusinessNZ Performance of Services Index fell from 51.1 to 48.8 in December, back into contraction territory. This downturn also brings the index below long-term average of 53.4. The increase in negative sentiment is evident, with the proportion of negative comments rising from 54.0% to 58.7%. The primary concerns expressed by businesses revolve around seasonal factors, increasing costs of living, and an overall economic slowdown.

Breaking down the PSI, several key components showed declines. Activity and sales dropped from 48.7 to 47.1, employment fell from 50.6 to 47.5, and new orders/business dipped from 52.2 to 51.2. Additionally, stocks and inventories decreased from 55.0 to 51.5, while supplier deliveries also saw a reduction from 52.8 to 50.5.

Stephen Toplis, BNZ's Head of Research noted that the softening in PSI, combined with the previously reported weakness in Performance of Manufacturing Index, paints a concerning picture for New Zealand's near-term economic growth and employment. While tourism has been a critical driver for the services sector and is expected to continue supporting the economy, Toplis emphasized that it cannot solely bear the burden of economic revitalization.

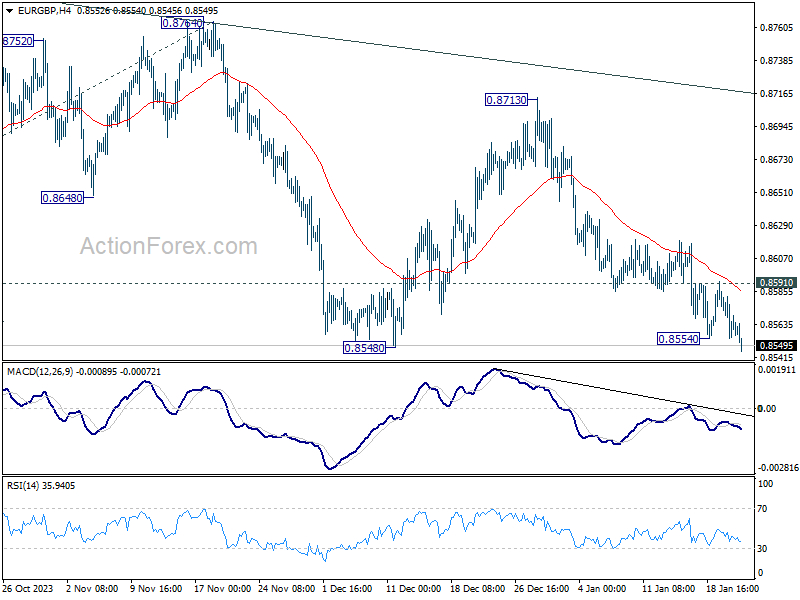

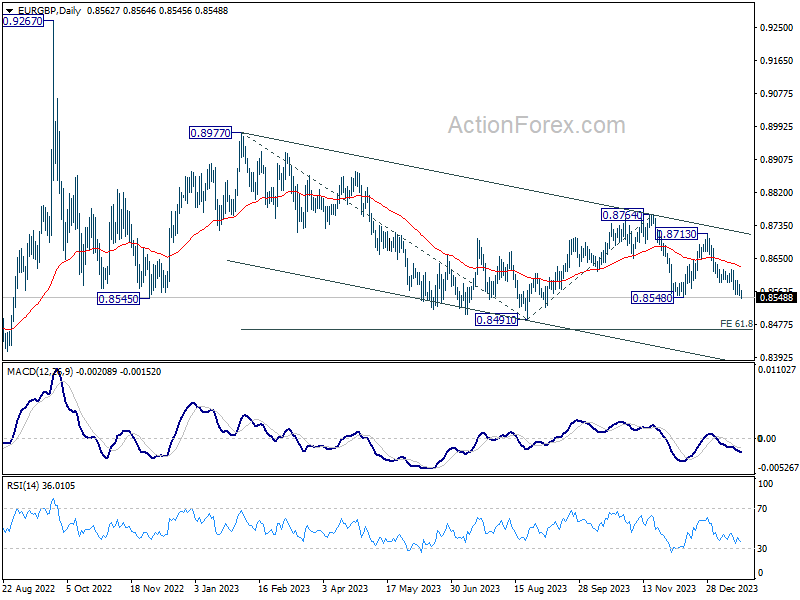

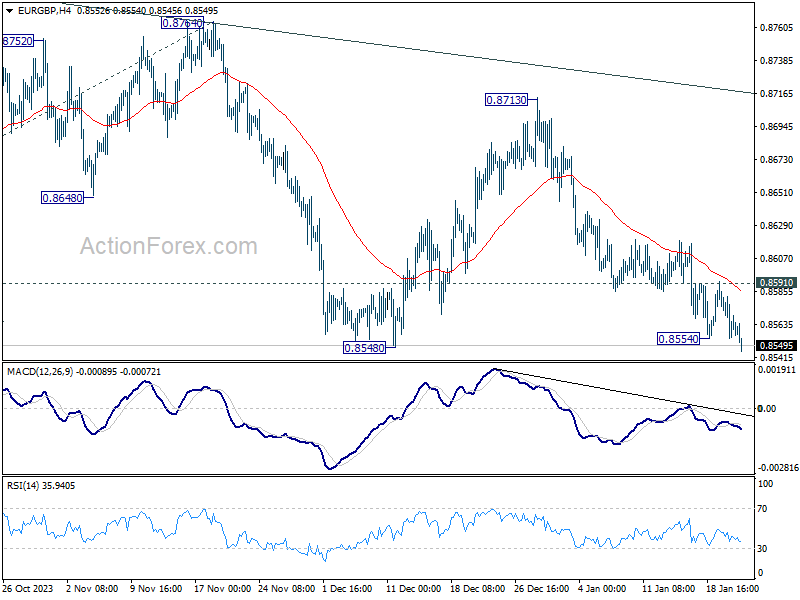

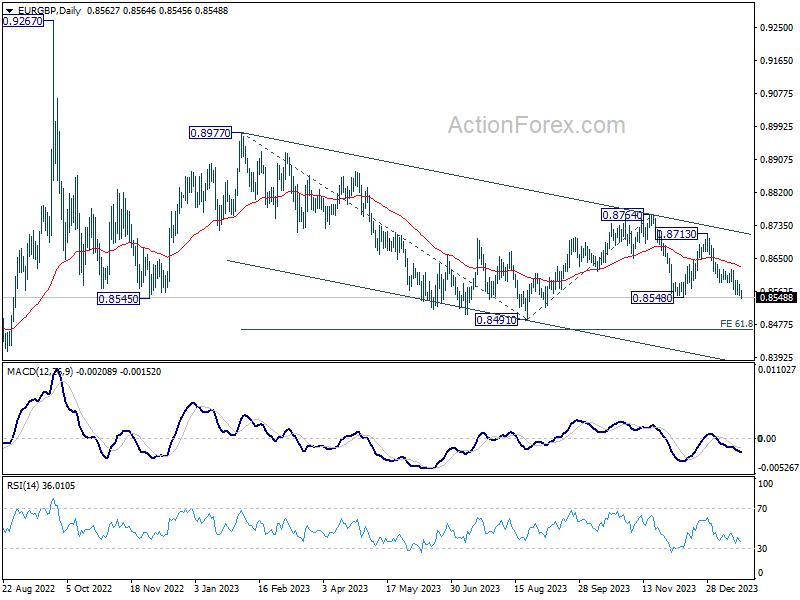

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8550; (P) 0.8568; (R1) 0.8580; More...

EUR/GBP's break of 0.8548/54 indicates down trend resumption. Intraday bias is back on the downside. Next target is 0.8491 low, and then 0.8464 projection level. On the upside, above 0.8591 minor resistance will turn intraday bias neutral and bring consolidations again.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Dec | 48.8 | 51.2 | 51.1 | |

| 00:30 | AUD | NAB Business Conditions Dec | 7 | 9 | ||

| 00:30 | AUD | NAB Business Confidence Dec | -1 | -9 | ||

| 03:09 | JPY | BoJ Rate Decision | -0.10% | -0.10% | -0.10% | |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Dec | 6.8B | 11.2B | 13.4B | 12.8B |

| 13:30 | CAD | New Housing Price Index M/M Dec | 0.00% | 0.00% | -0.20% | |

| 15:00 | EUR | Eurozone Consumer Confidence Jan P | -14 | -15 |

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8550; (P) 0.8568; (R1) 0.8580; More...

EUR/GBP's break of 0.8548/54 indicates down trend resumption. Intraday bias is back on the downside. Next target is 0.8491 low, and then 0.8464 projection level. On the upside, above 0.8591 minor resistance will turn intraday bias neutral and bring consolidations again.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

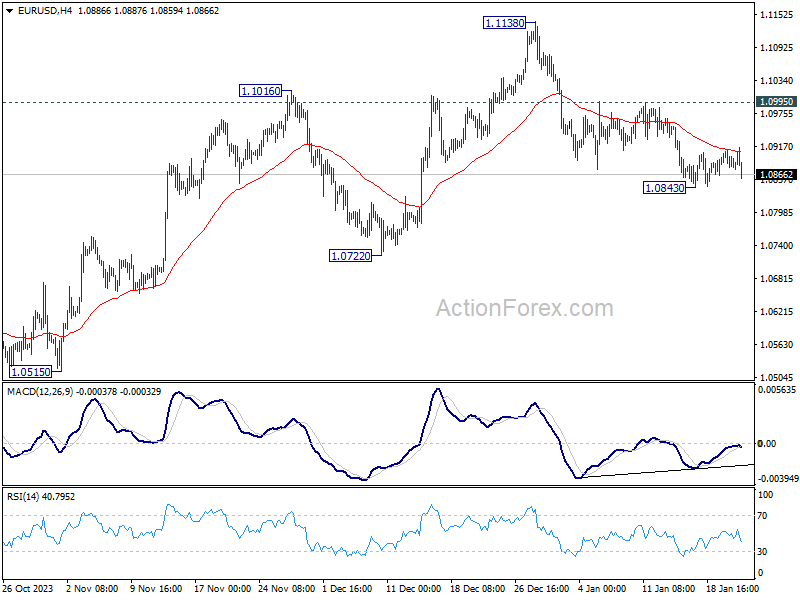

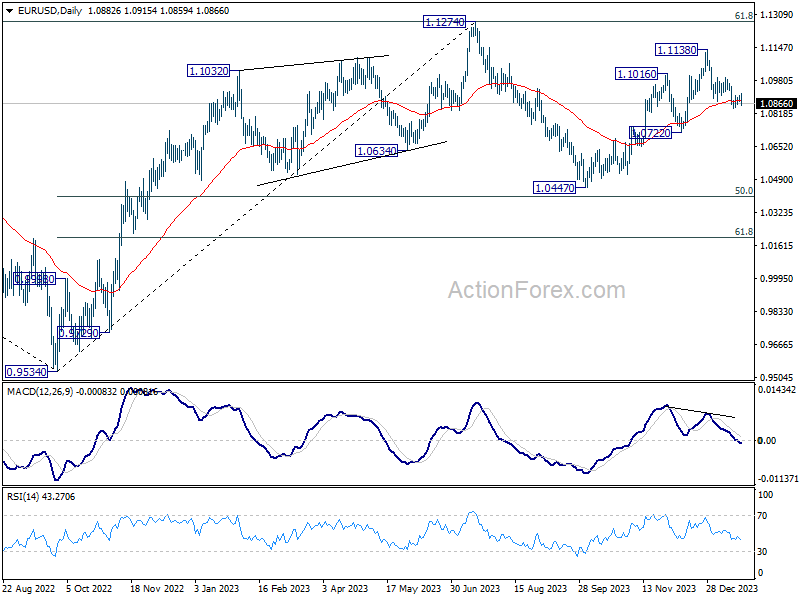

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0872; (P) 1.0891; (R1) 1.0902; More...

EUR/USD dips notably today but stays above 1.0843 support. Intraday bias remains neutral and more consolidations could be seen. Further decline is expected as long as 1.0995 resistance holds. Below 1.0843 will target 1.0722 support next. Decisive break there will argue that whole rise from 1.0447 has completed, and target this low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

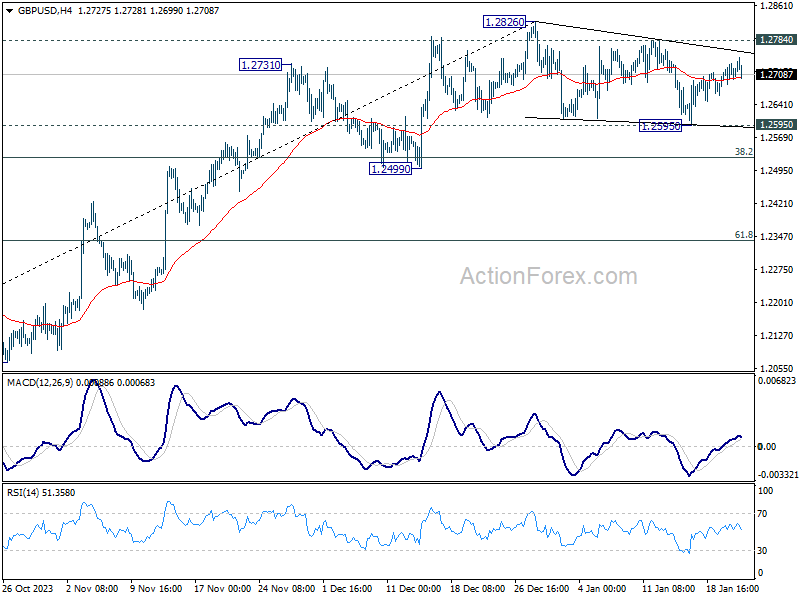

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2686; (P) 1.2710; (R1) 1.2732; More...

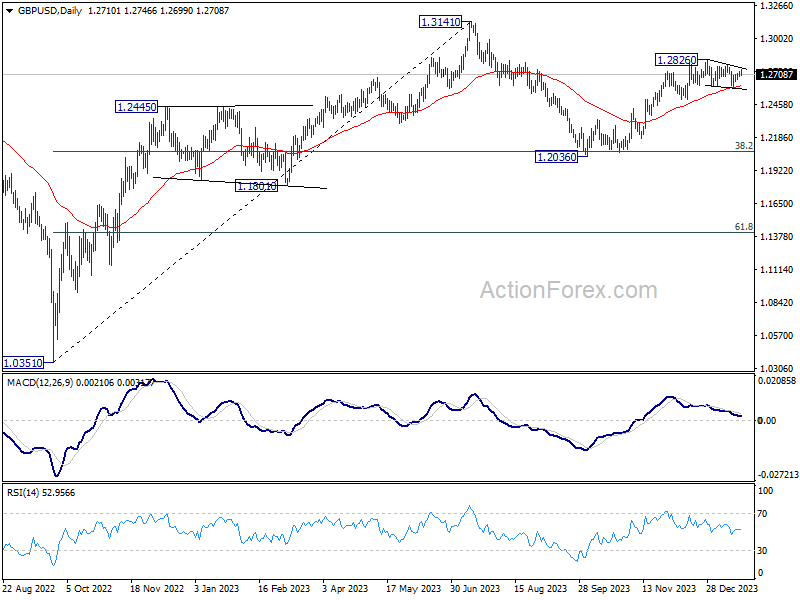

No change in GBP/USD's outlook as it's still bounded in consolidation from 1.2826. Intraday bias stays neutral at this point. On the downside, break of 1.2595 support will bring deeper correction to 1.2499 support. On the upside, however, firm break of 1.2784 resistance will suggest that the consolidation pattern has completed. Further rally should then resume through 1.2826 towards 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

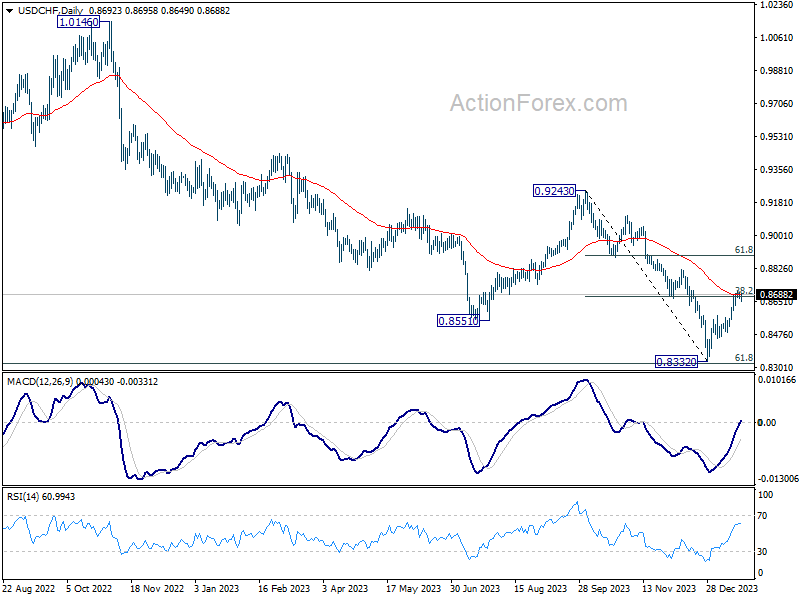

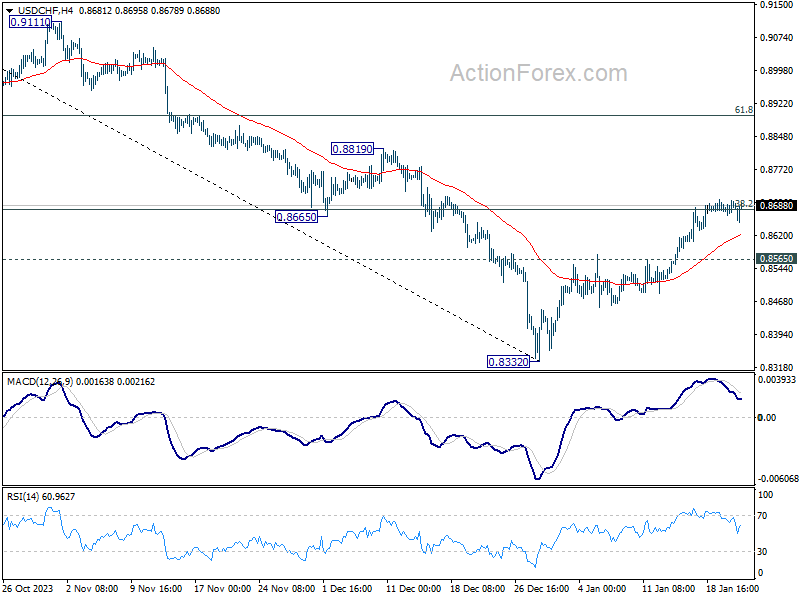

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8671; (P) 0.8686; (R1) 0.8706; More....

Intraday bias remains neutral in USD/CHF and outlook is unchanged. Focus stays on 38.2% retracement of 0.9243 to 0.8332 at 0.8680, which coincides 55 D EMA (now at 0.8686). Decisive break there will turn near term outlook bullish for 61.8% retracement 0.8995. Nevertheless, break of 0.8565 minor support will turn intraday bias back to the downside for retesting 0.8332 low.

In the bigger picture, while rebound from 0.8332 could be strong, there is no clear sign of medium term bottoming yet. This rebound is tentatively seen as a corrective move for now. Also, outlook will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.