Sample Category Title

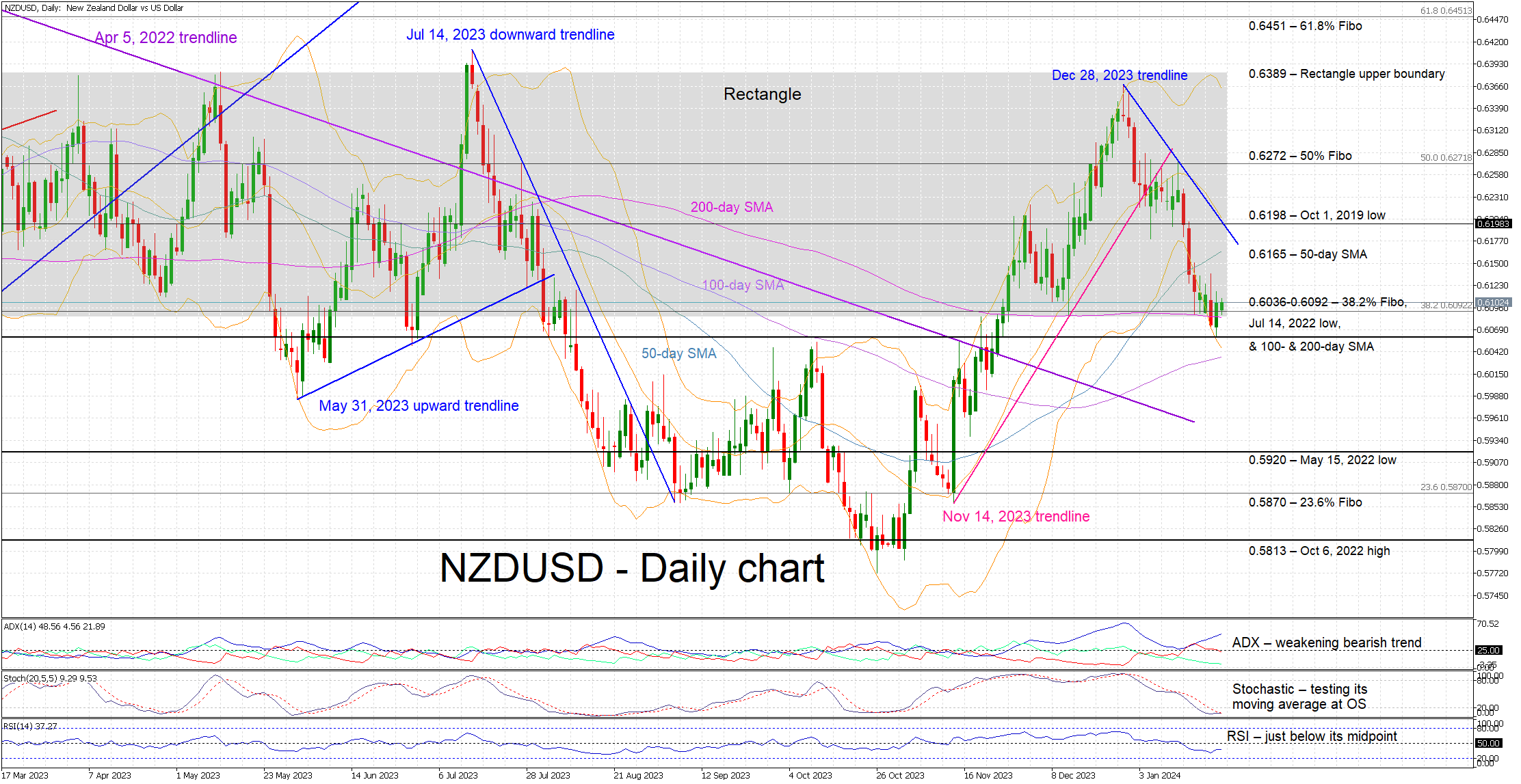

NZDUSD Continues to Trade Sideways

- NZUSD hovers above a key support area

- Aggressive downward move from late December 2023 peak

- Momentum indicators are mostly mixed at this juncture

NZDUSD is in the green today, but it continues to range trade. The 0.6036-0.6092 area appears to have put a temporary stop at the correction that has been in place since the December 28, 2023 high. Market participants could also be in waiting mode for some key market events coming up over the next 10 days, especially next week’s Fed decision.

The momentum indicators remain mostly mixed. More specifically, the RSI is trading a tad below its midpoint. Interestingly, the Average Directional Movement Index (ADX) is moving higher, but its D- subcomponent remains stuck below the 25 midpoint. More importantly, the stochastic oscillator is trying to break above both its moving average and oversold area. Should it succeed, it would send a strong signal for the direction of NZDUSD.

If the bulls decide to retake the market reins, they could try to lead NZDUSD towards the 50-day simple moving average (SMA) at 0.6165. Then, the October 1, 2019 low at 0.6198 looks a plausible target provided of course the bulls manage to overcome the resistance set by the December 28, 2023 descending trendline. Even higher, the bulls could have a go at the 50% Fibonacci retracement of the April 5, 2022 – October 13, 2022 downtrend at 0.6272.

On the flip side, the bears are keen to keep the current correction alive. They could try to break below the 0.6036-0.6092 area, which is populated by the 38.2% Fibonacci retracement, the July 14, 2022 low and the 100- and 200-day SMAs. The path then appears to be unhindered until the May 15, 2022 low at 0.5920.

To sum up, NZDUSD trades sideways with the bears hoping that the stochastic oscillator does not send a bullish signal soon.

EUR/USD Struggles, USD/JPY Could Extend Gains

EUR/USD started another decline from the 1.0915 resistance. USD/JPY surged and broke the 148.00 resistance zone.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- · The Euro started a fresh decline below the 1.0880 support zone.

- · There was a break below a key bullish trend line with support at 1.0880 on the hourly chart of EUR/USD at FXOpen.

- · USD/JPY climbed higher above the 148.00 and 148.30 levels.

- · There is a connecting bearish trend line forming with resistance at 148.00 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair struggled to clear the 1.0915 resistance zone. The Euro started a fresh decline and traded below the 1.0880 support zone against the US Dollar.

There was a break below a key bullish trend line with support at 1.0880. The pair even declined below 1.0840 and tested the 1.0820 zone. A low is formed near 1.0821 and the pair is now correcting losses.

On the upside, the pair is now facing resistance near the 50% Fib retracement level of the recent decline from the 1.0916 swing high to the 1.0821 low at 1.0865.

The next key resistance is near the 50-hour simple moving average at 1.0880. It is close to the 61.8% Fib retracement level of the recent decline from the 1.0916 swing high to the 1.0821 low. The main resistance is 1.0915.

A clear move above the 1.0915 level could send the pair toward the 1.0950 resistance. An upside break above 1.0950 could set the pace for another increase. In the stated case, the pair might rise toward 1.1020.

If not, the pair might resume its decline. The first major support on the EUR/USD chart is near 1.0840. The next key support is at 1.0820. If there is a downside break below 1.0820, the pair could drop toward 1.0785. The next support is near 1.0750, below which the pair could start a major decline.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a strong increase from the 146.50 zone. The US Dollar gained bullish momentum above 148.00 against the Japanese Yen.

It even cleared the 50-hour simple moving average and 148.30. However, the pair struggled to clear the 148.70 zone. It is now correcting gains from the 148.69 high. There was a move below the 148.30 level.

On the downside, the first major support is near the 50% Fib retracement level of the upward move from the 146.97 swing low to the 148.69 high at 147.80. The next major support is visible near the 147.60 pivot level.

The 61.8% Fib retracement level of the upward move from the 146.97 swing low to the 148.69 high is also at 147.60. If there is a close below 147.60, the pair could decline steadily.

In the stated case, the pair might drop toward the 147.00 support zone. The next stop for the bears may perhaps be near the 146.20 region.

Immediate resistance on the USD/JPY chart is near a connecting bearish trend at 148.00. The first major resistance is near 148.30. If there is a close above the 148.30 level and the RSI stays moves 50, the pair could rise toward 148.70. The next major resistance is near 149.25, above which the pair could test 150.00 in the coming days.

Trade global forex with the Innovative Broker of 2022*. Choose from 50+ forex markets 24/5. Open your FXOpen account now or learn more about trading forex with FXOpen.

* FXOpen International, Innovative Broker of 2022, according to the IAFT

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Our Bias Remains for a stronger USD

Markets

Core bonds drifted south yesterday in the run-up to this week’s big events, starting with January PMI surveys today. Daily changes on the US yield curve ranged between -2.1 bps (2-yr) and 4.3 bps (30-yr). German yields rose by 2.5 bps (2-yr) to 7.9 bps (30-yr). The ECB’s lending survey (sharpest tightening in credit standards behind us), disappointing US (Richmond Fed Manufacturing index) and EMU (consumer confidence) data and a rather soft $60bn 2-yr Note auction had no direct market impact. Q4 corporate earnings generally beat expectations, with a stellar Netflix result being the cherry on the cake after US close. The S&P 500 yesterday succeeded a third straight record high (+0.3%). Overnight, AP rapidly called a Trump win in North Hampshire Republican primaries, beating his sole remaining contestant, Haley, by a wide margin. If it weren’t for Trump’s legal issues and the upcoming primary in her home state, South Carolina (Feb 24), she would have likely considered leaving the race. We don’t see additional signs of USD strength after Trump’s win like it was the case after the landslide victory in the Iowa race. While it’s too early to contemplate the eventual outcome of this year’s US elections, we believe that Trump and USD momentum might go hand in hand. Not specifically because of USD-positive domestic policy, but rather for a foreign policy which could be negative for the likes of EUR, CNY,…

Turning to that dollar: the greenback had a good run yesterday. EUR/USD set a new YTD/correction low at 1.0820 before closing at 1.0854. Our bias remains for a stronger USD with support levels in the pair located at 1.0793 (50% retracement on Q4 rally, but especially at 1.0712/24 (61% retracement & December low). Today’s PMI surveys are expected to show a modest bottoming out in EMU and stabilization at a slow pace in the US. Ahead of tomorrow’s ECB gathering, we don’t expect EMU readings to have big market potential. ECB Lagarde set the stage for a potential first rate cut in summer with market expectations shifting to a June kick-off. US/Fed guidance is currently less specific with market consensus centering around a May start. PMI’s are unlikely to alter this thinking.

News & Views

New Zealand inflation slowed to 0.5% Q/Q and 4.7% Y/Y in Q4 2023, down from 1.8% Q/Q and 5.6% Y/Y in Q3. The outcome was in line with expectations, but below the forecasts of the Reserve Bank of New Zealand (5% Y/Y). There is a substantial divergence between tradable goods disinflation (-0.2% Q/Q & 3% Y/Y) and stubborn price rises for non-tradeable goods (1.1% Q/Q and 5.9% Y/Y). Prices for housing and households utilities rose 0.8% Q/Q. Food prices fell 1.2% Q/Q. Price for miscellaneous goods and services rose 1.5% Q/Q. The RBNZ at its end November meeting left its policy rate unchanged at 5.5%, but felt uncomfortable with the high level of core inflation. In this respect it warned that if inflation would turn out higher than expected, it still might raise the policy rate further. Today’s data probably allow the RBNZ to maintain a wait-and-see approach. Market speculation on a May rate cut is probably premature. NZD/USD rebounded to 0.61 after a protracted decline since the start of the year.

The Japanese composite PMI rose to 51.1 from 50 in December. The rise in activity still masks a contraction in the manufacturing sector (48 from 47.9) while services activity gained further traction (52.7 from 51.5). According to the report “Forward-looking indicators from the survey suggest the potential for demand and activity to rise over the coming months”. “The rate of input price inflation remained elevated by historical standards, with the latest rise in operating expenses little changed from the marked uptick seen in December. That said, Japanese private sector firms looked to absorb some of these costs, as the rate of output charge inflation eased to the softest since February 2022.” The Japanese 10-y yield this morning adds 5 bps, but this still is a mainly a reaction to yesterday’s BOJ press conference. The yen gains modestly (USD/JPY 147.95).

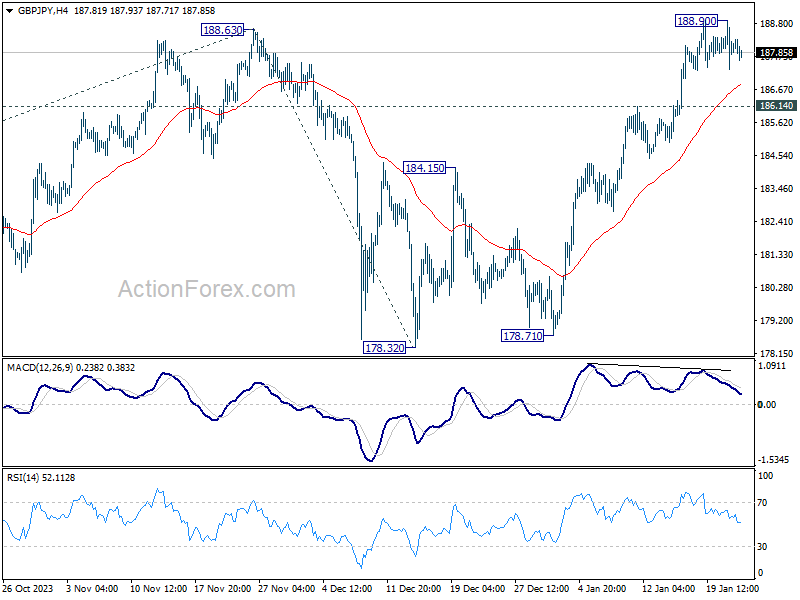

GBP/JPY Daily Outlook

Daily Pivots: (S1) 187.42; (P) 188.17; (R1) 188.99; More...

Intraday bias in GBP/JPY stays neutral as consolidation continues. Further rally is expected as long as 186.14 resistance turned support holds. On the upside, break of 188.90, and sustained trading above 188.63 will confirm up trend resumption. Next target is 38.2% projection of 155.33 to 188.63 from 178.32 at 191.04. However, break of 186.14 will turn bias to the downside for deeper pullback.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

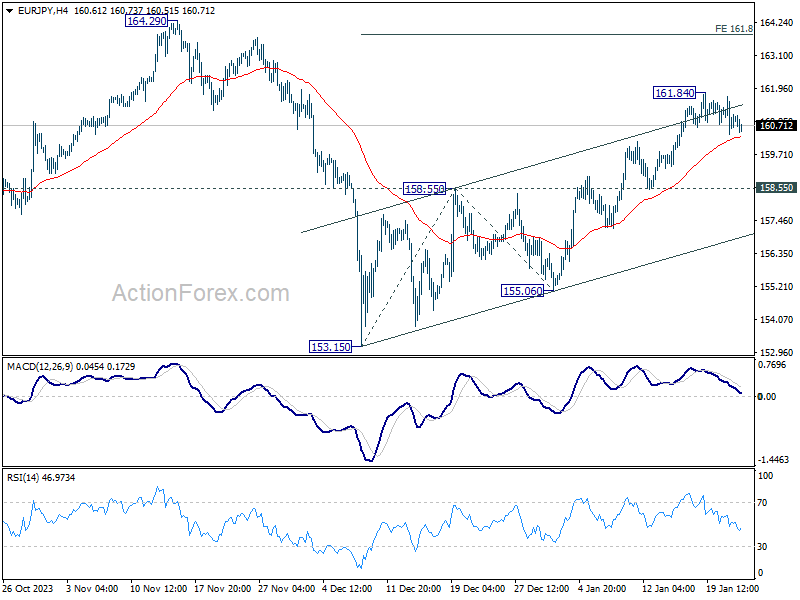

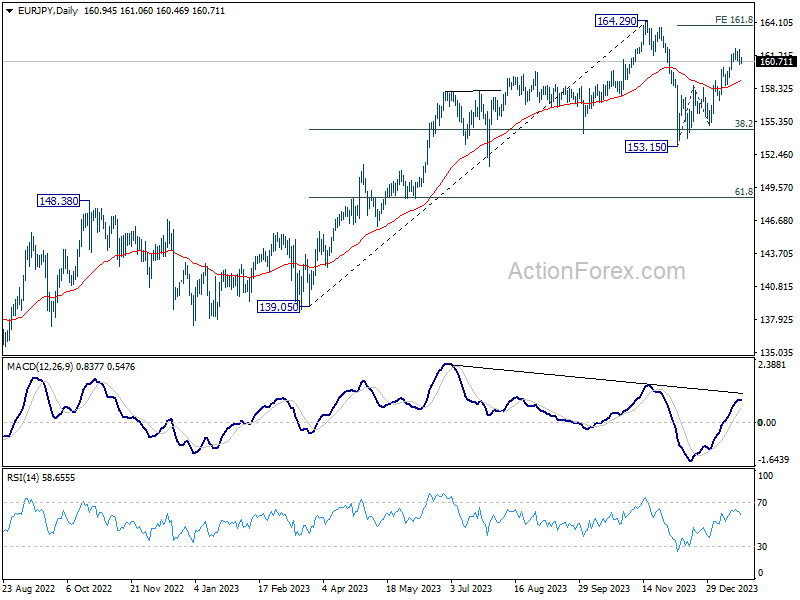

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.41; (P) 161.06; (R1) 161.70; More...

EUR/JPY's consolidation from 161.84 is still in progress and intraday bias remains neutral. Further rally is expected as long as 158.55 resistance turned support holds. On the upside, break of 161.84 will resume whole rally from 153.15 to 161.8% projection of 153.15 to 158.55 from 155.06 at 163.79, which is close to 164.29 high.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage.

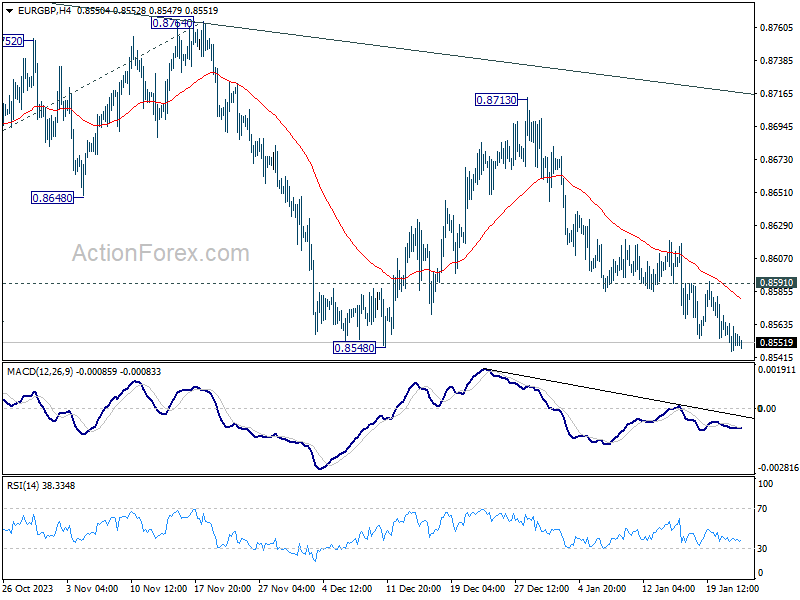

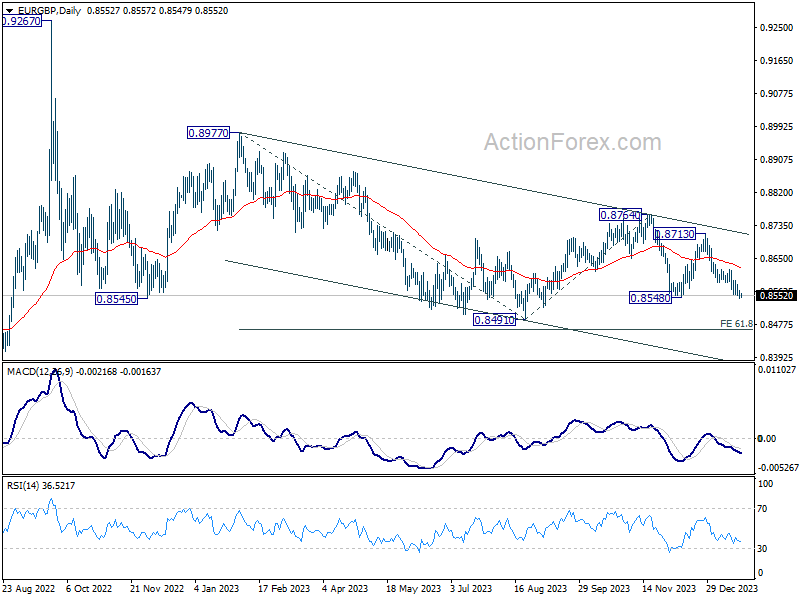

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8545; (P) 0.8557; (R1) 0.8566; More...

Intraday bias in EUR/GBP remains on the downside for the moment. Current fall from 0.8713 is part of the larger down trend. Deeper decline should be seen to 0.8491 low, and then 0.8464 projection level. On the upside, above 0.8591 minor resistance will turn intraday bias neutral and bring consolidations again.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

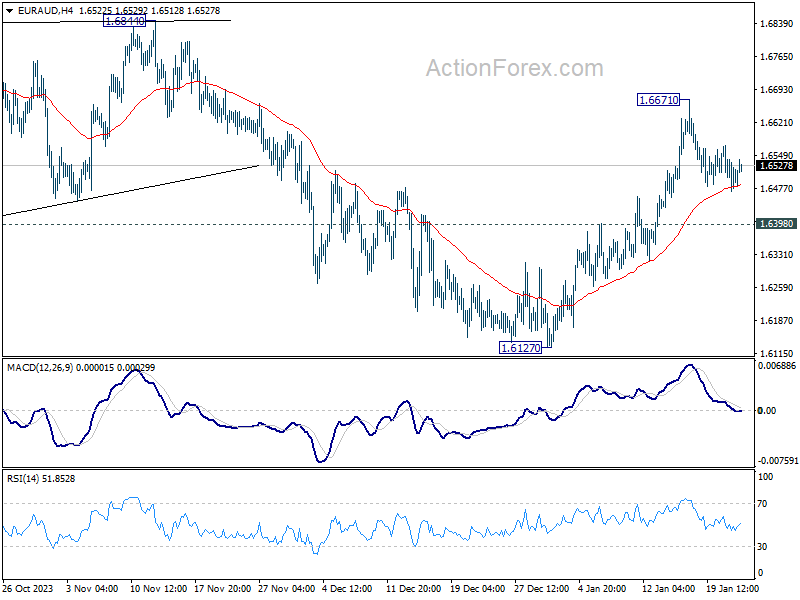

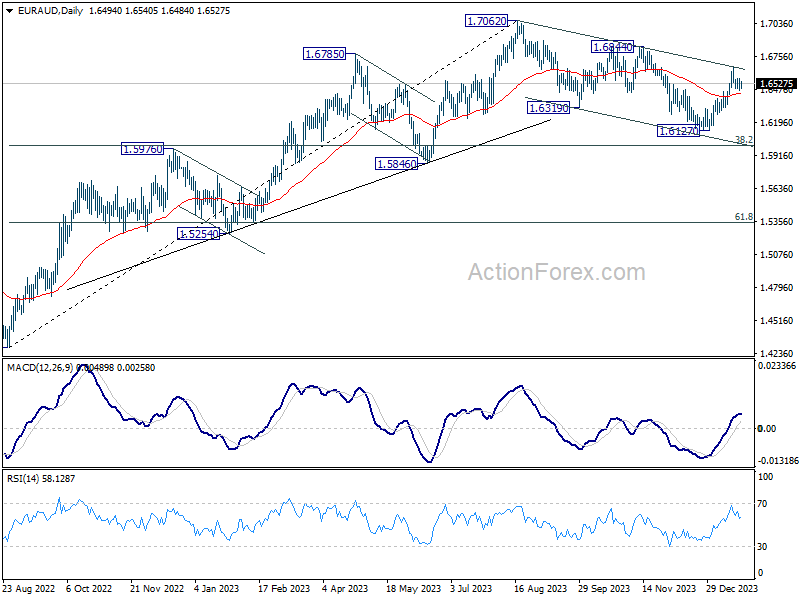

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6455; (P) 1.6514; (R1) 1.6555; More...

EUR/AUD's consolidation from 1.6671 is in progress and intraday bias stays neutral. Rise from 1.6127 is expected to continue as long as 1.6398 support holds. Corrective fall from 1.7062 should have completed with three waves down to 1.6127 already. Above 1.6671 will target 1.6844 resistance to confirm this bullish case.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

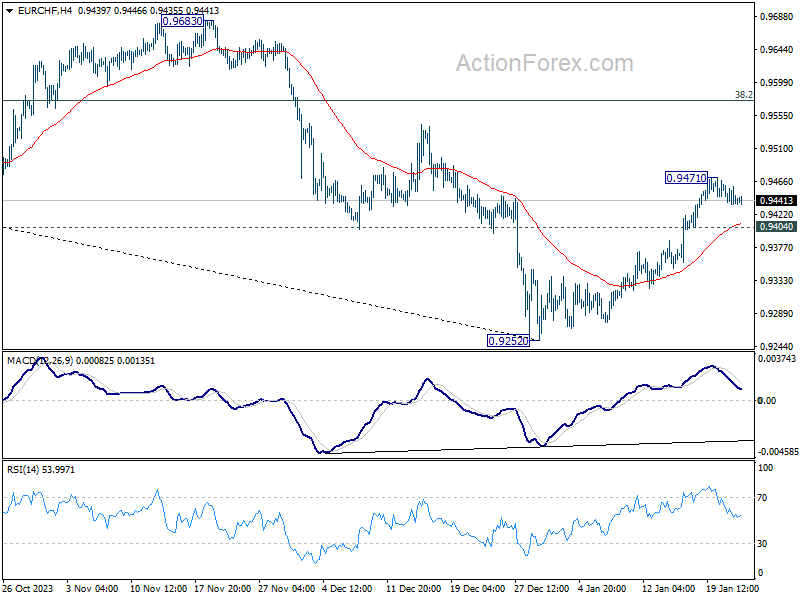

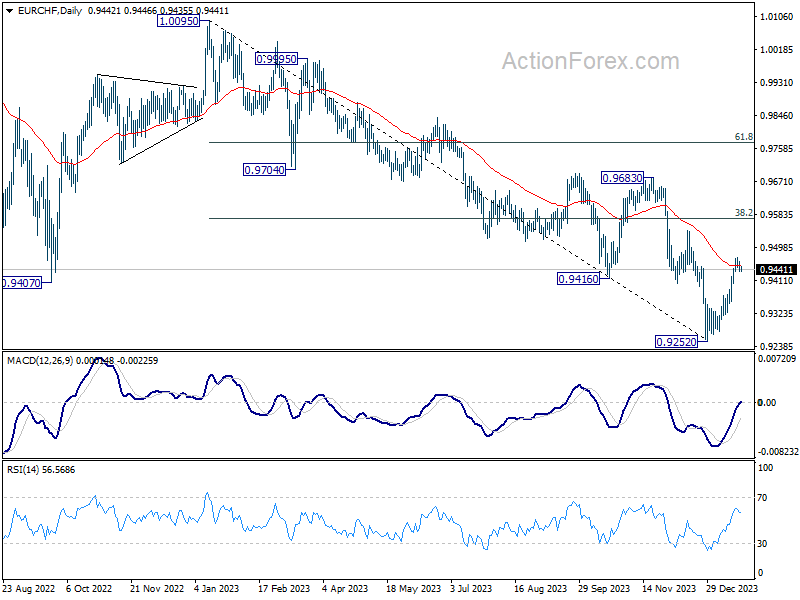

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9434; (P) 0.9449; (R1) 0.9460; More...

EUR/CHF's consolidation from 0.9471 is in progress and intraday bias stays neutral for the moment. Further rally is expected as long as 0.9404 minor support holds. Above 0.9471 will resume the rebound from 0.9252, as a correction to whole decline from 1.0095. Next target will be 38.2% retracement of 1.0095 to 0.9252 at 0.9574. However, break of 0.9404 will turn bias to the downside for deeper fall.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Another decline is in favor after rebound from 0.9252 completes. However, firm break of 0.9683, and sustained trading above 55 W EMA (now at 0.9659) will argue that EUR/CHF is already in a medium term rally, even as a corrective move.

Netflix Beats

Netflix jumped 8% in the afterhours trading as its revenue and new subscriptions topped estimates. More than 13 mio people decided that Netflix was worth paying for, and the number of total paid subscribers rose past 260 mio. The password sharing ban has been a boon for the company. The only thing they regret is not having thought about it before.

Strong Netflix results will likely give a positive spin to the major US indices which were slow to move yesterday after the Richmond manufacturing index came in much lower than expected.

In the sovereign space, a mixed 2-year bond auction in the US hinted at declining optimism from the Federal Reserve’s (Fed) dovish camp, but a jump from foreign buyers pulled the US 2-year yield lower. The 10-year yield remains steady above the 4.10% and will hopefully cross back above the 2-year yield after having stayed inverted for more than a year-and-a-half as the US soft-landing scenario is given more weight despite the slow manufacturing numbers as US consumer spending remains strong and helps keeping the US economy afloat. The US will release its latest GDP update tomorrow and is expected to print a decent 2% growth for the last quarter.

Robust US economic growth, strong earnings and prospects of lower Fed rates remain supportive of equity valuations, although the ATH levels and near-overbought market conditions in the S&P500 call for – at least – a minor correction in the short run. Today, Tesla will be reporting its latest Q4 results after the bell, and the results will unlikely be as enchanting as Netflix’. But overall, investors don’t want to miss the US stocks’ rally to fresh highs. And if the trend is your friend, well, the trend is clearly positive.

In China, though, sentiment is the exact opposite. Chinese stocks saw a little bump yesterday on the announcement of a $278bn rescue package to lift the Chinese stocks up. But skepticism reigned as 1. the rescue package was found to be a bit meagre compared with around $6 trillion of market value wiped off the value of Chinese and Hong Kong stocks in past 3 years. 2. The rescue package doesn’t solve the underlying fundamental problems, namely slowing economic growth, a serious property crisis and slowing population. And 3. No one can guarantee a consistent action plan from the Xi government in the medium to long run. The ruthless government crackdown and extreme Covid measures are responsible for a severe confidence loss. And the market reaction to Chinese measures prove that you can’t buy confidence.

In the FX, the US dollar index is testing the 200-DMA to the upside. Parallelly, the EURUSD is testing its 200-DMA support to the downside. Today’s PMI data and tomorrow’s European Central Bank (ECB) decision will likely help provide fresh direction to the pair. Fading inflation, sputtering European economies and ECB Chief Lagarde’s latest words in Davos hint that the ECB is preparing for a summer rate cut. More clarity on the ECB’s rate cut plans could provide a green light for a sustainable move below the 200-DMA. Elsewhere, the Bank of Canada (BoC) meets today and is expected to maintain rates unchanged. The Loonie remains under the pressure of limited appetite for oil.

Speaking of oil, US crude’s inability to clear the $75pb offers is intriguing despite news that would normally be positive for oil prices – like the geopolitical tensions in regions where oil is pumped and transported, and the US API data showing a 6.7-mio barrel slump in weekly oil inventories. The next decisive move in oil prices should be a positive breakout.

Trump Wins New Hampshire

In focus today

Today, we will get January PMIs for both the euro area and the US. They will be the first indicator on how the major economies performed at the beginning of 2024.

In the euro area, the manufacturing PMIs have risen since October in a signal of activity bottoming out in Q4 2023. We expect that the gradual rebound continued in January. The service PMIs have been relatively stable around the 48.5 level in the previous five months, and we expect this to be the case also in January.

From Sweden we will get the monthly inflation survey from Prospera for January. We see it as unlikely to deliver any big surprises, as inflation is gradually easing towards the target.

In the afternoon at 15:45 CET, Bank of Canada will announce their rate decision after their policy meeting. In line with market consensus, we expect them to hold policy rate unchanged at 5.00%. We will keep an eye on any signals on how long the bank expects to hold the rates at current level. Our base case is for a 25bp rat cut in March although recent developments has increased the risk that the first rate cut will not come until summer.

Economic and market news

What happened overnight

In the US, Donald Trump has now won two out of two states in the race to become Republican nominee in the presidential election. At the deadline for this publication Donald Trump won 11 out of 22 delegates corresponding to 54.6% of the votes, while Nikki Haley won 8 corresponding to 43.5%, with three delegates left to be decided. Haley indicated last night that she will continue in the race despite her significant defeat.

In the red sea, the US hit two anti-ship missiles from the Houthi rebels in Yemen, which were aimed at the Red Sea and prepared to launch.

In Japan, we got PMIs for January. The manufacturing PMI was more or less unchanged (48.0 in January against 47.9 in December). Service PMI increased from 51.5 in December to 52.7 in January. This means, that we continue to see modest decline in manufacturing and an even stronger service sector in Japan. Continued strong domestic demand in Japan keeps the upside risk to inflation present.

What happened yesterday

Turkey's parliament approves Swedish NATO membership bid. The Swedish NATO bid has now overcome a major hurdle and an about 20-month delay to become a NATO member. President Erdogan's AKP and its allies all voted in favour of Swedish membership. He is expected to sign the bill in the coming days. The only NATO member left to approve Sweden's bid is Hungary.

In the euro area, the results of ECB's Q4 bank lending survey was published. The survey was broadly in line with expectations, and hence we do not see it altering the monetary policy stance at the upcoming monetary policy meeting on Thursday. Most banks reported that credit standards are still tightened in 2023 Q4 and that loan demand declined. Yet, it was to a smaller extent than in the previous quarters, as more banks reported unchanged credit standards and loan demand while fewer reported tightening standards and decreased demand than in the previous survey.

Consumer confidence in the Euro area declined unexpectedly from -15.1 to -16.1. Market expected an increase to -14.3. Consumer confidence is thereby still stuck at low levels which is likely also the explanation to the sluggish consumption ratio. Hence, with consumer confidence still at low levels the upswing in private consumption that better confidence would support is still not in sight.

In Denmark, consumer confidence rose from -13 to -8.4. The consumer confidence is still at low levels but increasing again, after it fell in December. The increase was mainly driven by improved assessment of the economic and household financial situation over the last 12 months.

Equities: Global equities ended higher yesterday as most US indices rally into the cash close and hence secured another set of all-time highs. That said, Europe and Japan were still lower and in global indices 4 out of 10 sectors were lower. Earnings season is picking up speed and if history repeats itself, we will see some days with what we call odd sector correlations as big individual companies are disturbing the picture because of either super solid or super weak earnings. Yesterday in the US, Dow -0.3%, S&P 500 +0.3%, Nasdaq +0.4% and Russell 2000 -0.4%. Asian markets are mostly in red this morning with China sticking out on the positive side as people continue to speculate in very equity market focus stimulus coming. European and US futures are higher. In Europe some of this is catch-up to the US cash session while US futures are boosted by better-than-expected earnings after the bell yesterday.

FI: Global yields rose across the board throughout yesterday's session as markets digested the rumours of new Chinese stimulus and the still significant amount of issuance. 10Y Bund yields ended up by 6bp, while the front end was up by a couple of basis points. Implied volatility drifted slightly higher in EUR swaptions markets, while the Bund ASW-spread continued to widen.

FX: USD/JPY could not really decide what to do after the well-anticipated BOJ decision, first a knee-jerk spike, then a sharp sell-off, and after that back above pre-BOJ levels. CNH has held on to gains after the news about government support to the Chinese stock market. Meanwhile, the USD firmed vs EUR and Scandies where USD/SEK tried to make USD/NOK company above 10.50. USD/SEK has gained 6% in three weeks (!) - we continue to like the topside as a strategic position for 2024.