Sample Category Title

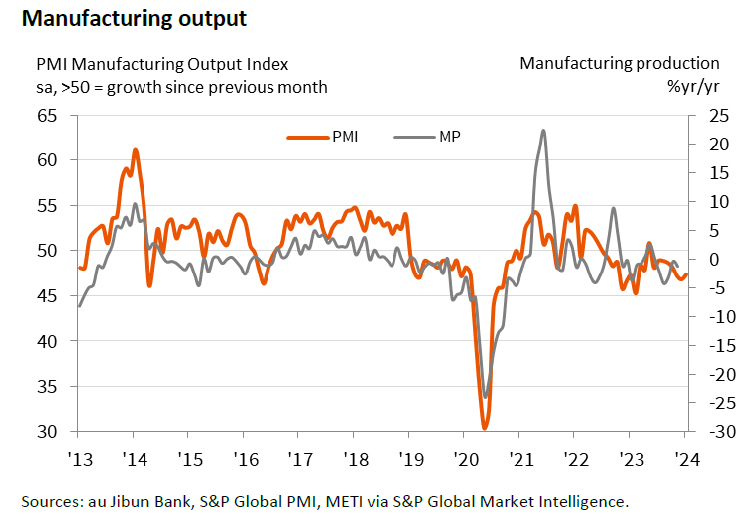

Japan’s PMI shows modest growth, manufacturing still in contraction

Japan's PMI Manufacturing rose fractionally from 47.9 to 48.0 in January, below expectation of 48.2. Manufacturing remained in contraction for the eighth consecutive months. PMI Services rose from 5.15 to 52.7. PMI Composite rose from 50.0 to 51.1.

Usamah Bhatti, Economist at S&P Global Market Intelligence, noted that while "modest" the private sector is having the strongest growth since September. However, there was disparity between the sectors, with services reaching a four-month high, while manufacturing marked its eighth consecutive month of contraction.

Regarding inflation, Bhatti said input price inflation "remains high historically". But output inflation eased to its "lowest since February 2022". This indicates that while input costs are still elevated, businesses are not passing these costs fully onto consumers.

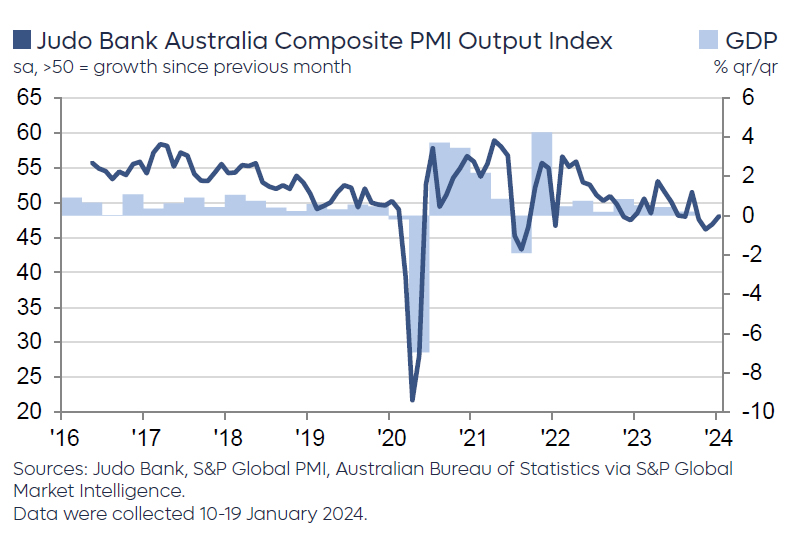

Australia’s PMI manufacturing Hits 11-month high, services Lagging

Australia PMI Manufacturing rose from 47.6 to 50.3 in January, back in expansion, and a 11-month high. PMI Services rose slightly from 47.1 to 47.9, a 3-month high. PMI Composite rose from 46.9 to 48.1, a 4-month high, but still in contraction.

Warren Hogan, Chief Economic Advisor at Judo Bank noted the PMI data indicates a that the economy remains on RBA's "narrow path" for soft landing. He highlights the manufacturing sector's rebound as a key factor in mitigating broader economic downturn risks.

Despite the general economic slowdown, Hogan observes that labor demand remains unexpectedly robust, differing from past economic cycles. However, he cautions that inflation pressures are still high, pointing out, "Input and output price indexes remain at levels suggesting CPI inflation is above the RBA's target range."

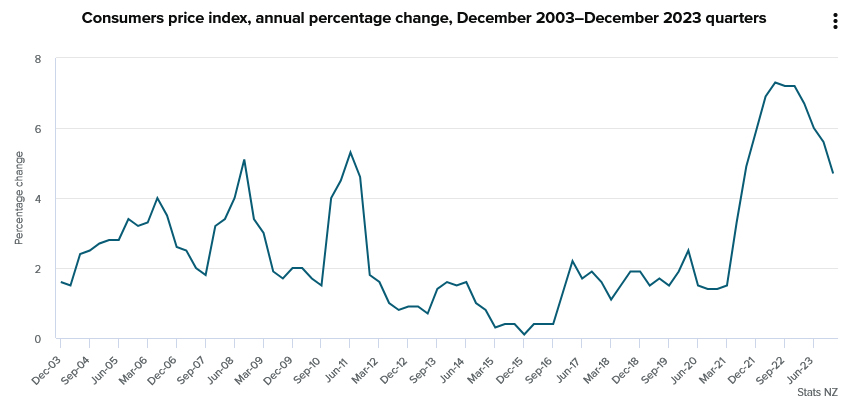

New Zealand CPI slows to 0.5% qoq, 4.7% yoy in Q4

New Zealand CPI rose 0.5% qoq in Q4, down from 1.8% qoq in Q3, matched expectations. Tradeable inflation turned negative to -0.2% qoq, from 1.8% qoq. Non-tradeable inflation slowed to 1.1% qoq, down from 1.7% qoq.

Annually, CPI slowed from 5.6% yoy to 4.7% yoy, matched expectations. Tradeable inflation slowed from 4.7% yoy to 3.0% yoy. non-tradeable inflation also slowed from 6.3% yoy to 5.9% yoy.

"While this is the smallest annual rise in the CPI in over two years, it remains above the Reserve Bank of New Zealand's target range of 1 to 3 percent," consumers prices senior manager Nicola Growden said.

NZ First Impressions: Consumers Price Index, December Quarter 2023

Consumer prices rose by 0.5% in the December quarter, leaving them up 4.7% over the past year. The December result was in line with our forecast, but below the RBNZ’s expectation.

Consumers Price Index, December quarter 2023

- Quarterly change: +0.5%

- Westpac forecast: +0.5%, RBNZ (Nov MPS): +0.8%

- Market median: +0.5%, range +0.3% to. +0.8%

- Annual change: +4.7%

- Westpac forecast: +4.7%, RBNZ (Nov MPS): +5.0%, Market: +4.7%

Key points

Consumer prices rose by 0.5% in the December quarter. That saw the annual inflation rate dropping to 4.7%, down from 5.6% in the year to September.

Today’s result was in line with our forecast, but it was lower than the RBNZ’s last published forecast which was finalised back in November.

Driving the fall in inflation (and the surprise to the RBNZ’s forecast) has been a fall in import prices. Much of that relates to volatile items like food and airfares. Movements in those sorts of volatile items are not the key focus for the RBNZ when setting monetary policy.

More importantly, domestic inflation pressures remain strong. Non-tradable prices were up 1.1% over the quarter - higher than our own or the RBNZ’s forecasts. On an annual basis, non-tradables inflation is running at a still-strong rate of 5.9%.

Core inflation measures have been dropping back, but remain elevated at rates of over 4%. Non-tradables excluding housing costs is tracking at an annual rate of 6.9%.

Implications

The divergence between the domestic and imported components of inflation helps to illustrate the big concerns that the RBNZ is trying to balance. Inflation is coming down, and faster than the RBNZ has been expecting. That will be important for stabilising inflation expectations and means that the RBNZ will feel more comfortable keeping the OCR on hold for now (recall that the RBNZ’s last policy statement in November signalled some chance a further rate rise).

However, this still leaves us with a picture of ‘lower’ inflation; not low inflation. That’s because domestic inflation is still running at rates that are much higher than the Monetary Policy Committee is comfortable with two years after the hiking cycle began. As a result, rate cuts won’t be on the table in the near term.

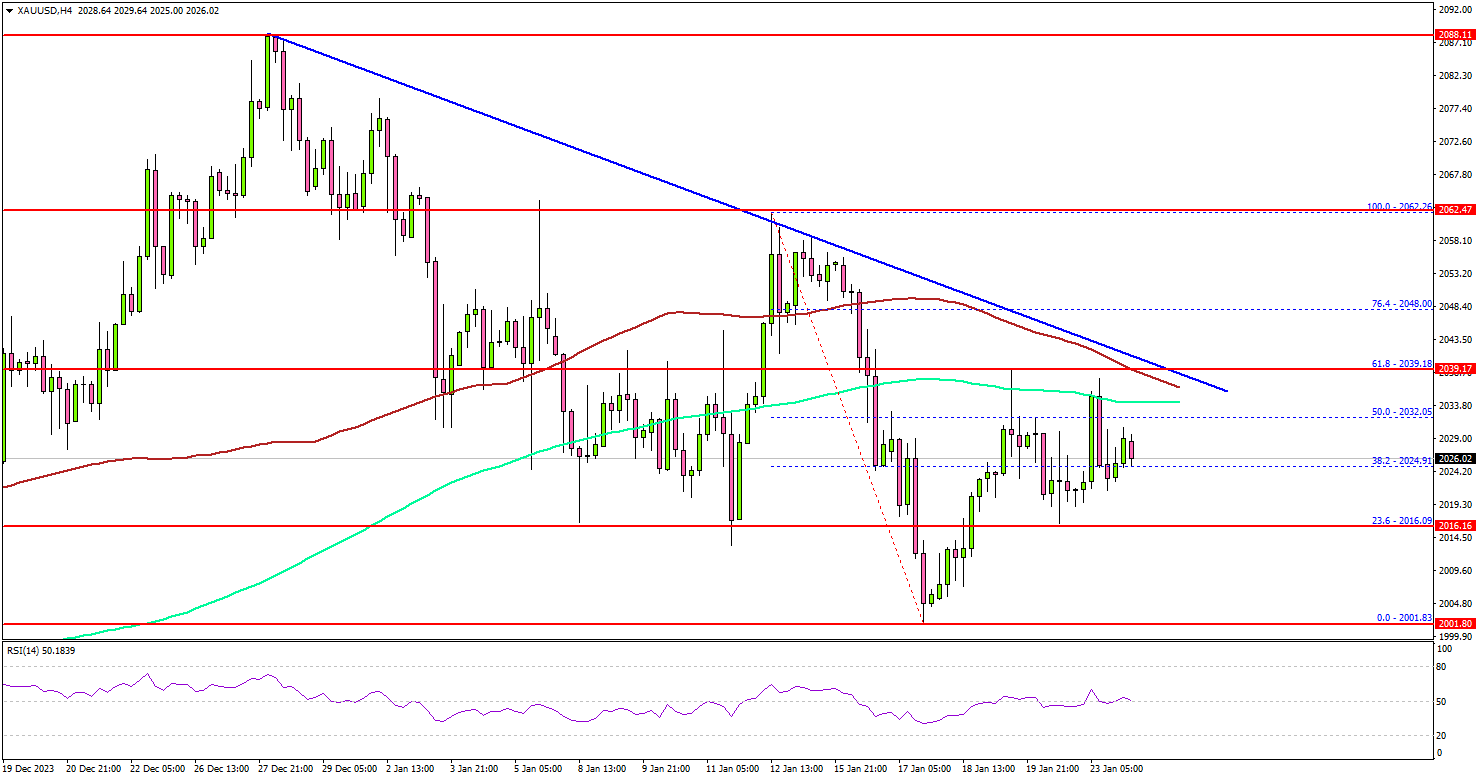

Gold Price Recovery Faces Hurdles, Bitcoin Dives

Key Highlights

- Gold prices are struggling to recover above the $2,040 resistance.

- A key bearish trend line is forming with resistance near $2,040 on the 4-hour chart.

- Bitcoin price declined heavily and traded below $40,000.

- The US Manufacturing PMI could remain at 47.9 in Jan 2023 (Preliminary).

Gold Price Technical Analysis

Gold found support near the $2,000 zone against the US Dollar. It started a recovery wave above the $2,020 zone but now faces a lot of hurdles.

The 4-hour chart of XAU/USD indicates that the price climbed above the 50% Fib retracement level of the downward move from the $2,062 swing high to the $2,001 low. However, the bears are still active near the $2,040 zone.

Gold is trading below the 100 Simple Moving Average (red, 4 hours) and the 200 Simple Moving Average (green, 4 hours). There is also a key bearish trend line forming with resistance near $2,040 on the same chart.

The trend line is near the 61.8% Fib retracement level of the downward move from the $2,062 swing high to the $2,001 low. An upside break above the $2,040 level could send the price soaring toward the $2,060 resistance. The next major resistance is near the $2,080 level, above which Gold could test $2,100.

Initial support is near the $2,015 level. The first major support sits at $2,000. Any more losses might call for a move toward the $1,975 level in the coming days.

Looking at Bitcoin, there was strong selling pressure and the bears managed to push the price below the $40,000 level.

Economic Releases to Watch Today

- Germany’s Manufacturing PMI for Jan 2023 (Preliminary) - Forecast 43.7, versus 43.3 previous.

- Germany’s Services PMI for Jan 2023 (Preliminary) - Forecast 49.5, versus 49.3 previous.

- Euro Zone Manufacturing PMI for Jan 2023 (Preliminary) – Forecast 44.8, versus 44.4 previous.

- Euro Zone Services PMI for Jan 2023 (Preliminary) – Forecast 49.0, versus 48.8 previous.

- UK Manufacturing PMI for Jan 2023 (Preliminary) – Forecast 46.7, versus 46.2 previous.

- UK Services PMI for Jan 2023 (Preliminary) – Forecast 53.2, versus 53.4 previous.

- US Manufacturing PMI for Jan 2023 (Preliminary) – Forecast 47.9, versus 47.9 previous.

- US Services PMI for Jan 2023 (Preliminary) – Forecast 51.0, versus 51.4 previous.

SNB’s Jordan: Real Franc appreciation hurts, yet no recession in sight

SNB Chairman Thomas Jordan, in his overnight address at an event, acknowledged the impact of the Franc's nominal appreciation on lowering inflation. However, he warned, the "Franc has also appreciated in real terms in 2023. And that hurts, companies feel that."

Despite the challenges posed by Franc's appreciation, Jordan expressed confidence in the Swiss economy's resilience. "Economists are confident that there won't be a recession — and we are also confident, otherwise we would forecast one," he commented, adding "So no recession, just weak growth."

Looking ahead, Jordan reiterated SNB's inflation expectations, stating that they anticipate Swiss inflation to approach but not exceed the 2% ceiling of their target range this year. The central bank does not foresee inflation breaching this mark until 2026.

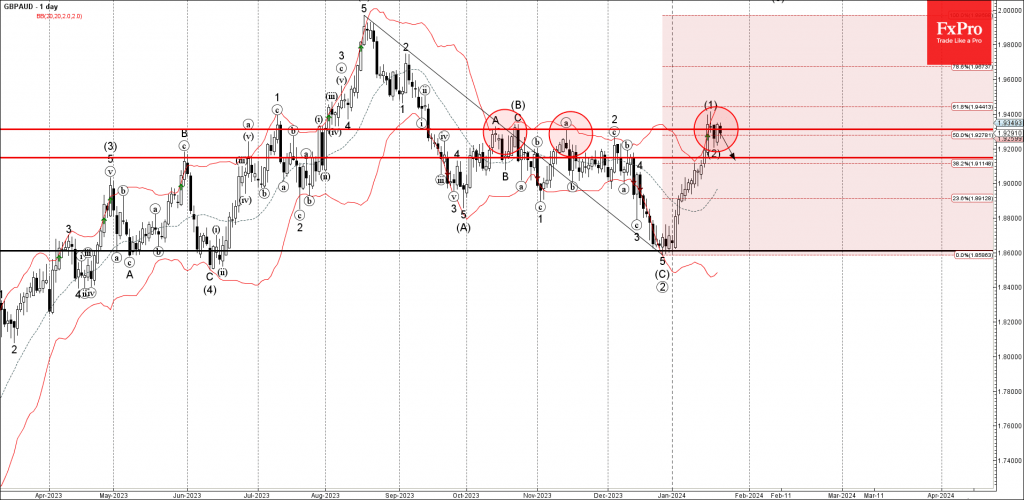

GBPUSD Wave Analysis

- GBPUSD reversed from resistance level 1.9310

- Likely to fall to support level 1.9150

GBPUSD currency pair under the bearish pressure after the earlier downward reversal from the resistance level 1.9310, which has been reversing the price from the middle of October.

The resistance level 1.9310 was further strengthened by the nearby 50% Fibonacci correction of the downward impulse from August.

Given the strength of the resistance level 1.9310, GBPUSD can be expected to fall further to the next support level 1.9150.

Bitcoin – Extends Losses to More Than 20% After Spot ETF Approvals

Bitcoin falls below $40,000

Is the bitcoin halving priced in?

50 Fib the next test

Bitcoin is trading around 2% lower on Tuesday, adding to losses at the start of the week and taking the price below $40,000.

The move takes the decline since peaking shortly after the SEC approved spot bitcoin ETFs to more than 20% in what appears to be another case of the rumor being heavily bought and the fact sold.

That’s not particularly important in the longer term and we’re used to this kind of volatility in the space. What matters now is what’s coming next that could generate excitement around cryptos and deliver further gains. The halving event in a few months could be that but it may take something more and skeptics could argue that’s already been priced in at this stage.

Big Fib levels eyed

The move below $40,000 could be a big technical loss as well as a psychological blow.

Source – OANDA on Trading View

The move over the last 24 hours also broke the 38.2% Fibonacci retracement level, drawing attention back to the 50% around $37,000. This is also the lower end of the 55/89-day simple moving average range which could offer additional support.

Below here, the 61.8% Fib could also be a level of interest, as could $35,000 having been so when it last traded here in October and November.

Will US GDP Surprise to the Upside?

- US will release GDP growth data at 13:30 GMT on Thursday

- An upside surprise seems more likely than a disappointment

- Dollar could benefit from a beat, as Fed cut bets are unwound

Dollar comes back to life

The US dollar started the new year on a strong note. A series of economic indicators have reaffirmed the resilience of the US economy lately, forcing traders to reconsider how quickly and how deep the Fed will cut interest rates this year.

Investors now see just a 45% probability that the Fed will cut rates in March, down from nearly 90% last month. This rethink follows the latest prints on inflation and retail sales, which came in stronger than anticipated, challenging the notion that the US economy is losing steam.

With the labor market also remaining in good shape, there doesn't seem to be any urgency to slash rates immediately. Several Fed officials have argued the same point lately, stressing that markets have gone overboard with pricing in such heavy rate cuts, and that the actual pace of rate reductions will likely be slower than what traders expect.

An upside GDP surprise?

With the prospect of a rate cut in March now priced almost like a coin toss, the upcoming GDP stats will be crucial in tipping the scales, driving the dollar accordingly. Economists expect the US economy to have grown at an annualized pace of 1.8% during the final quarter of 2023, driven by heavy government spending and solid consumption.

As for any surprises, a stronger-than-expected GDP print seems more likely than a disappointment. This is mostly because of the Atlanta Fed GDPNow model, which currently estimates growth at 2.4%, significantly higher than the official forecast.

This model has a solid track record in terms of predicting actual GDP numbers, and if it proves accurate this time as well, the dollar would likely benefit as investors continue to unwind bets of rapid Fed rate cuts.

Looking at the charts, euro/dollar has been in a steady decline so far this year. Another round of encouraging US data could add fuel to this selloff, pushing the pair down towards its recent low of 1.0840, a region that also encapsulates the 200-day simple moving average.

On the flipside, a disappointing GDP reading would likely propel euro/dollar higher, with the 1.1000 zone likely to act as the first major barrier to any advances.

Beyond the GDP data, another important release this week will be the latest core PCE price index on Friday.

Can the dollar keep rising?

All told, the outlook for the dollar still appears quite bright. The US economy is in much better shape than other major regions such as the Eurozone, which might already be in a minor technical recession.

With economic growth differentials favoring the United States, there's a clear risk that the Fed will cut interest rates at a slower pace than the ECB will during this cycle, keeping the dollar supported. Historically speaking, the dollar often thrives in late-cycle environments, especially if the US economy is healthier than the rest of the world.

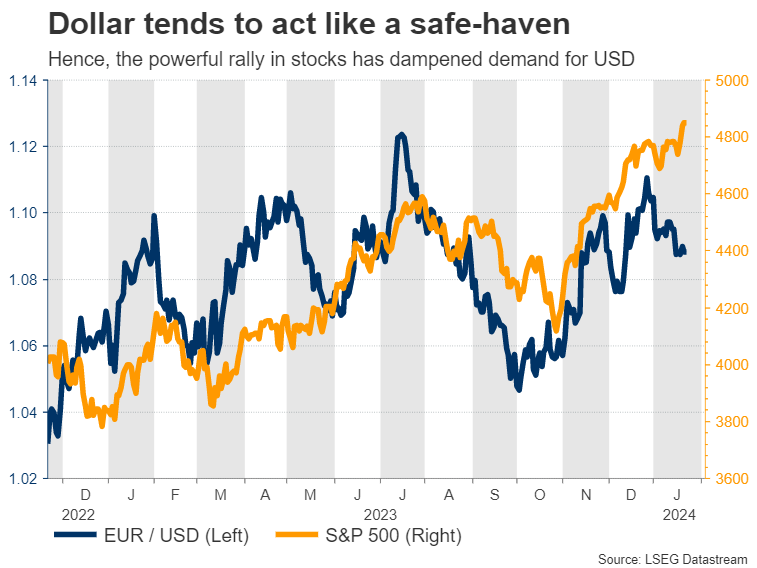

Finally, it's worth noting that the powerful rally in stock markets has dampened demand for safe haven instruments like the dollar in recent months. If this rally loses some steam and valuations compress now that investors have started to scale back rate cut bets, it could be another element that helps the dollar advance.