Sample Category Title

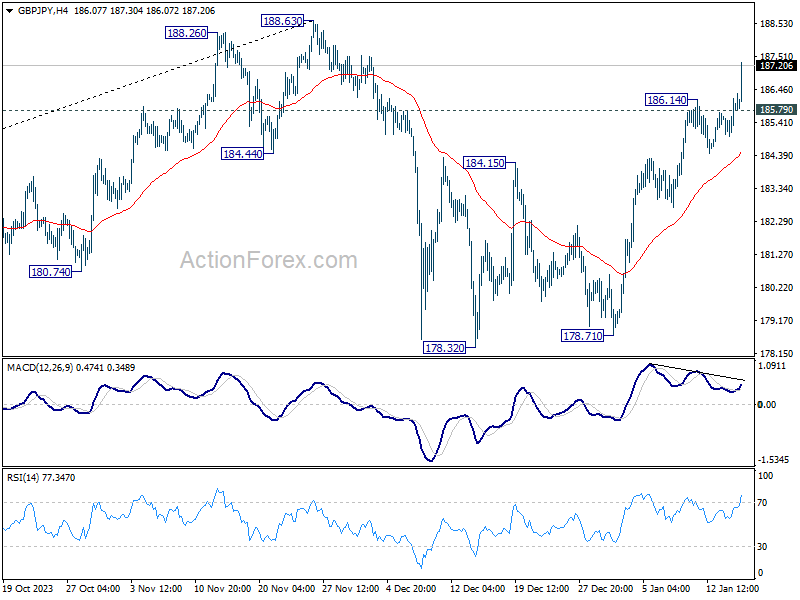

GBP/JPY Daily Outlook

Daily Pivots: (S1) 185.26; (P) 185.72; (R1) 186.45; More...

GBP/JPY's rally from 178.32 resumed by breaking through 186.14 temporary top. Intraday bias is back on the upside for retesting 188.63 high next. On the downside, below 185.79 minor support will turn intraday bias neutral and bring consolidations first. But further rally is expected as long as 184.15 resistance turned support holds.

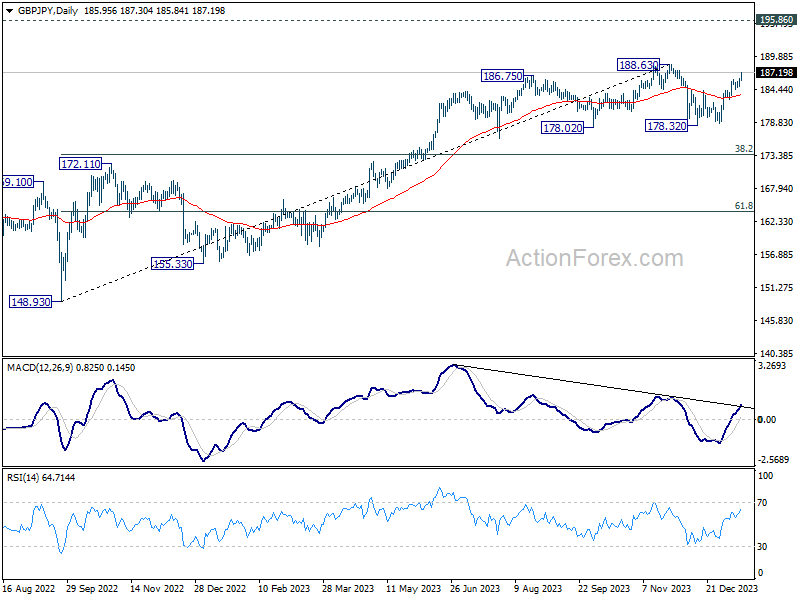

In the bigger picture, price actions from 188.63 medium term top are seen as a correction to the up trend from 148.93 (2022 low) only. As long as 172.11 resistance turned support holds, larger up trend from 123.94 (2020 low) is still in favor to resume through 188.63 at a later stage. Next target will be 195.86 long term resistance.

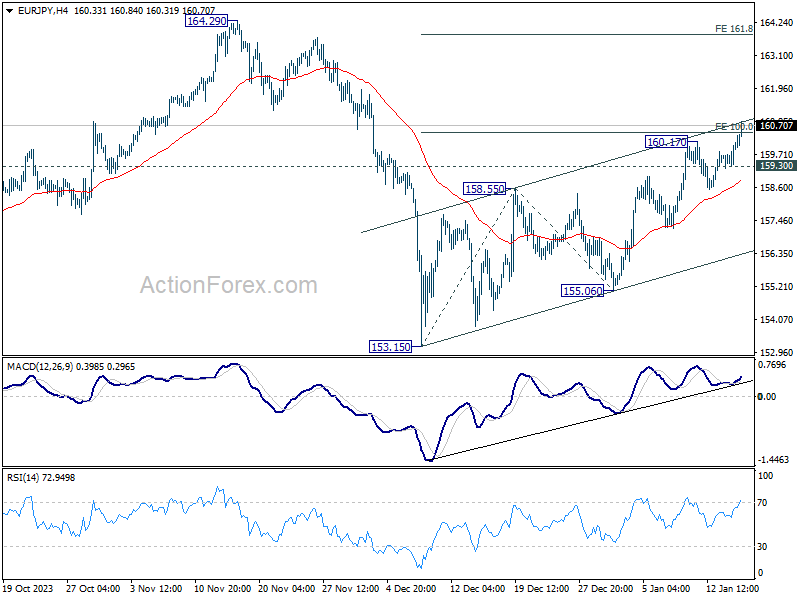

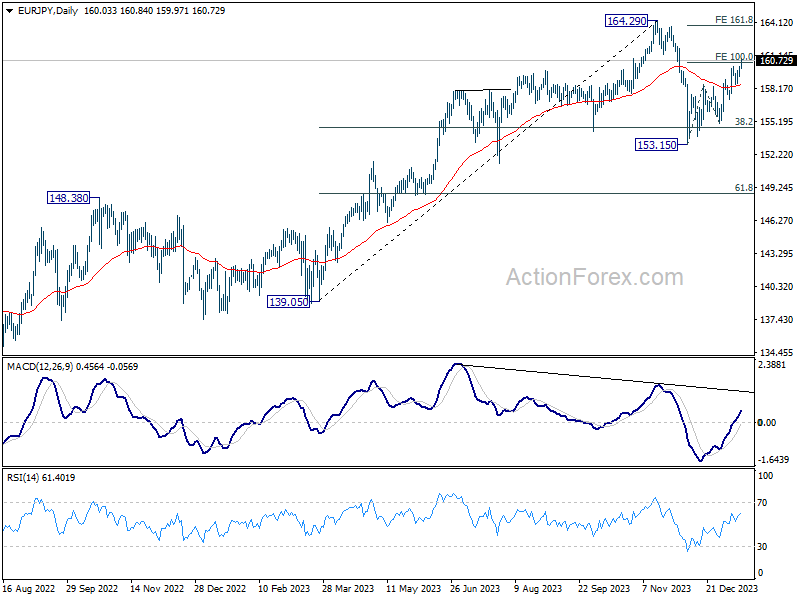

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.49; (P) 159.82; (R1) 160.40; More...

EUR/JPY's rally from 153.15 resumed by breaking through 160.17 temporary top. Intraday bias is back on the upside. Further rally should be seen to 161.8% projection of 153.15 to 158.55 from 155.06 at 163.79, which is close to 164.29high). ON the downside, below 159.30 minor support will turn intraday bias neutral first. But further rally is expected as long as 158.55 resistance turned support holds.

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.

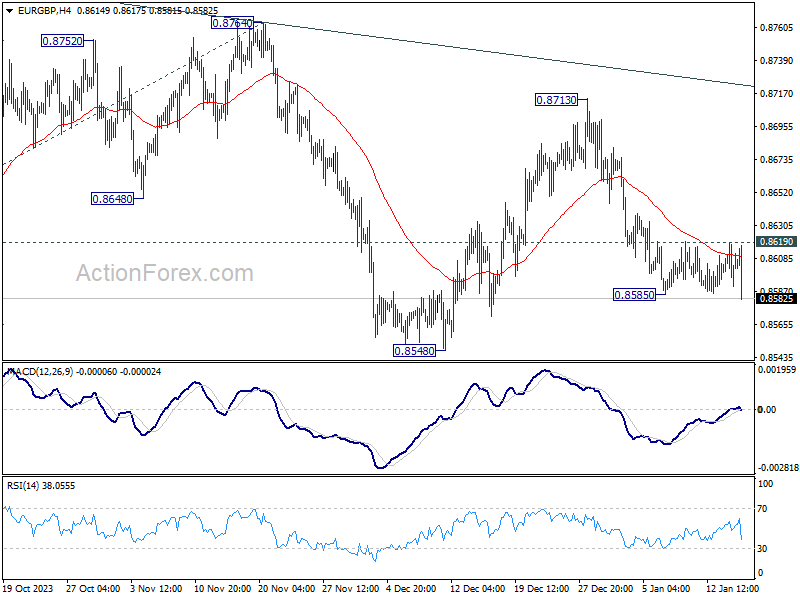

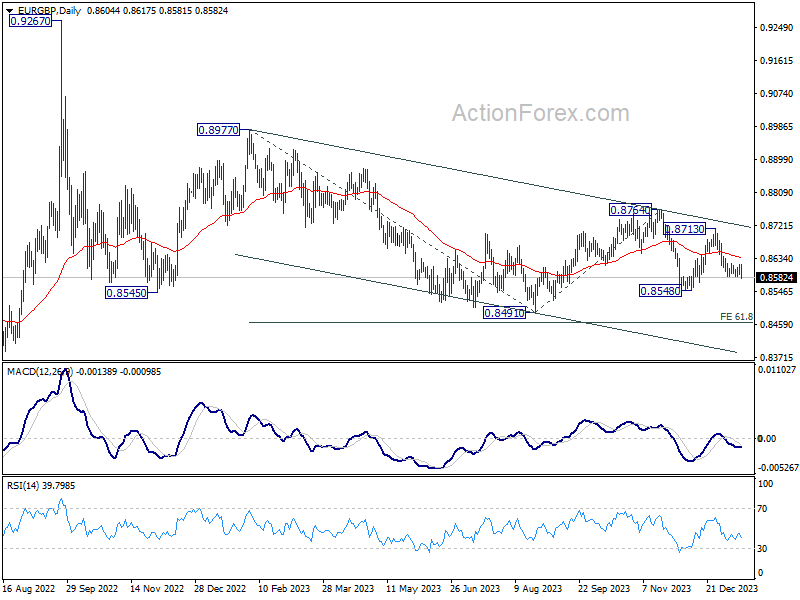

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8592; (P) 0.8606; (R1) 0.8621; More...

EUR/GBP's fall from 0.8713 resumed by breaking through 0.8585 today. Intraday bias is back on the downside for 0.8548 support first. Firm break there will argue that larger down trend is ready to resume through 0.8491 low. On the upside, break of 0.8619 resistance is needed to indicate short term bottoming. Otherwise, further fall is in favor in case of recovery.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8764 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

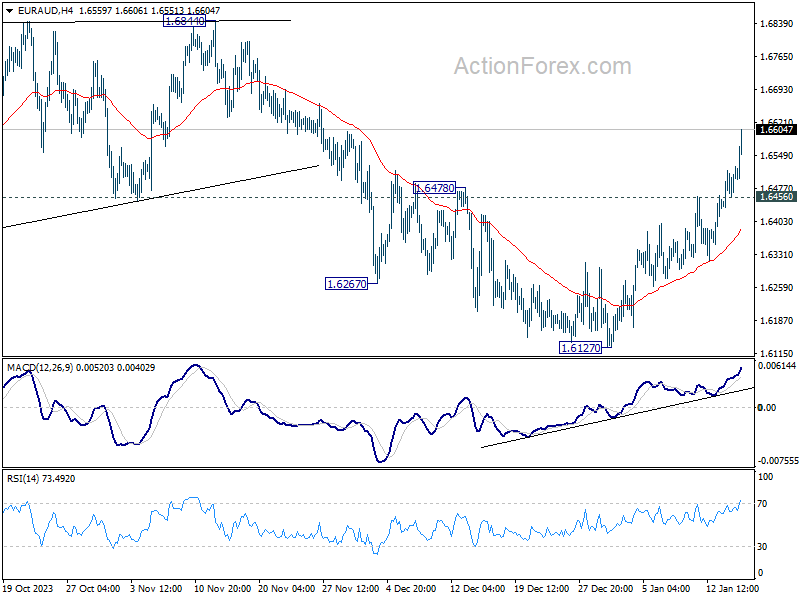

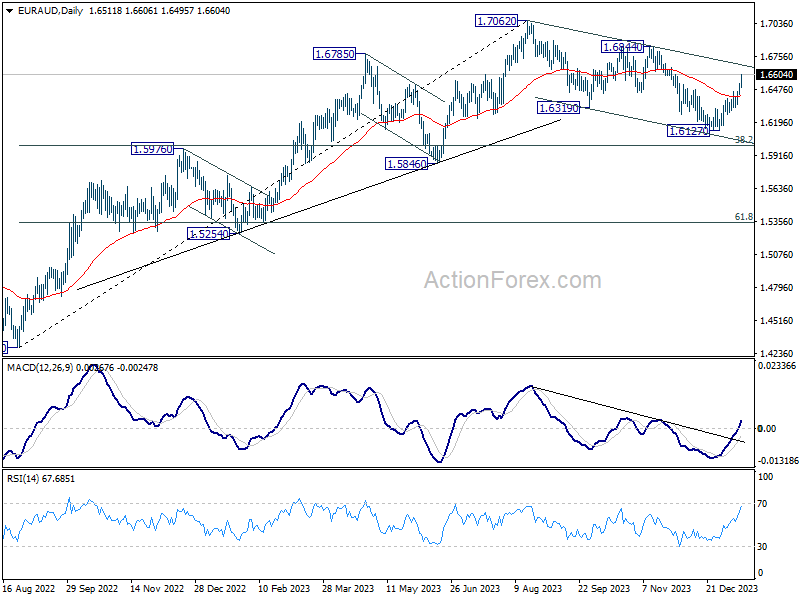

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6456; (P) 1.6492; (R1) 1.6554; More...

EUR/AUD's rebound from 1.6127 is in progress and intraday bias stays on the upside. Correction from 1.7062 should have completed with three waves down to 1.6127. Further rise should be seen to 1.6844 resistance for confirmation. On the downside, below 1.6456 minor support will turn intraday bias neutral and bring consolidations, before staging another rally.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 bring rebound.

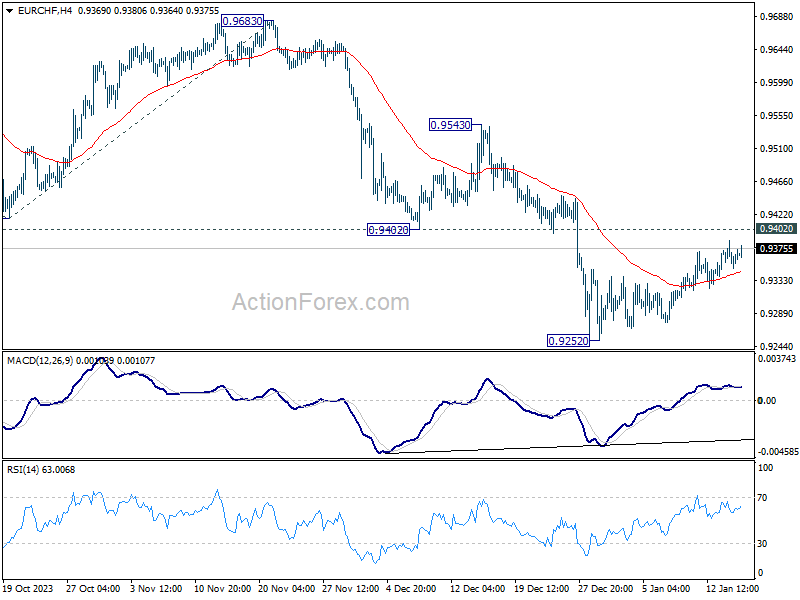

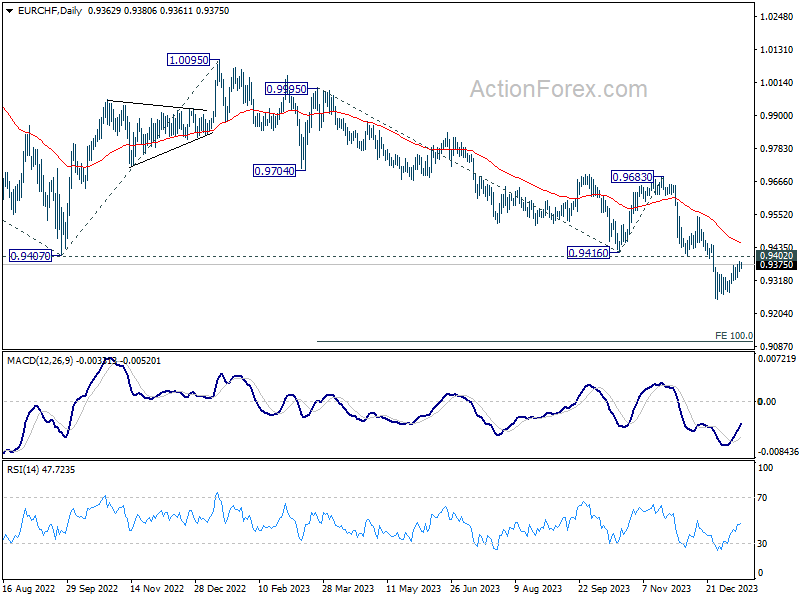

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9351; (P) 0.9370; (R1) 0.9389; More...

EUR/CHF is extending the corrective recovery from 0.9252 and intraday bias stays neutral. Outlook remains bearish with 0.9402 support turned resistance intact. On the downside, break of 0.9252 will resume larger down trend to 100% projection of 0.9995 to 0.9416 from 0.9683 at 0.9104 next. However, firm break of 0.9402 will dampen this view, and turn bias back to the upside for 0.9543 resistance instead.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Next target is 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

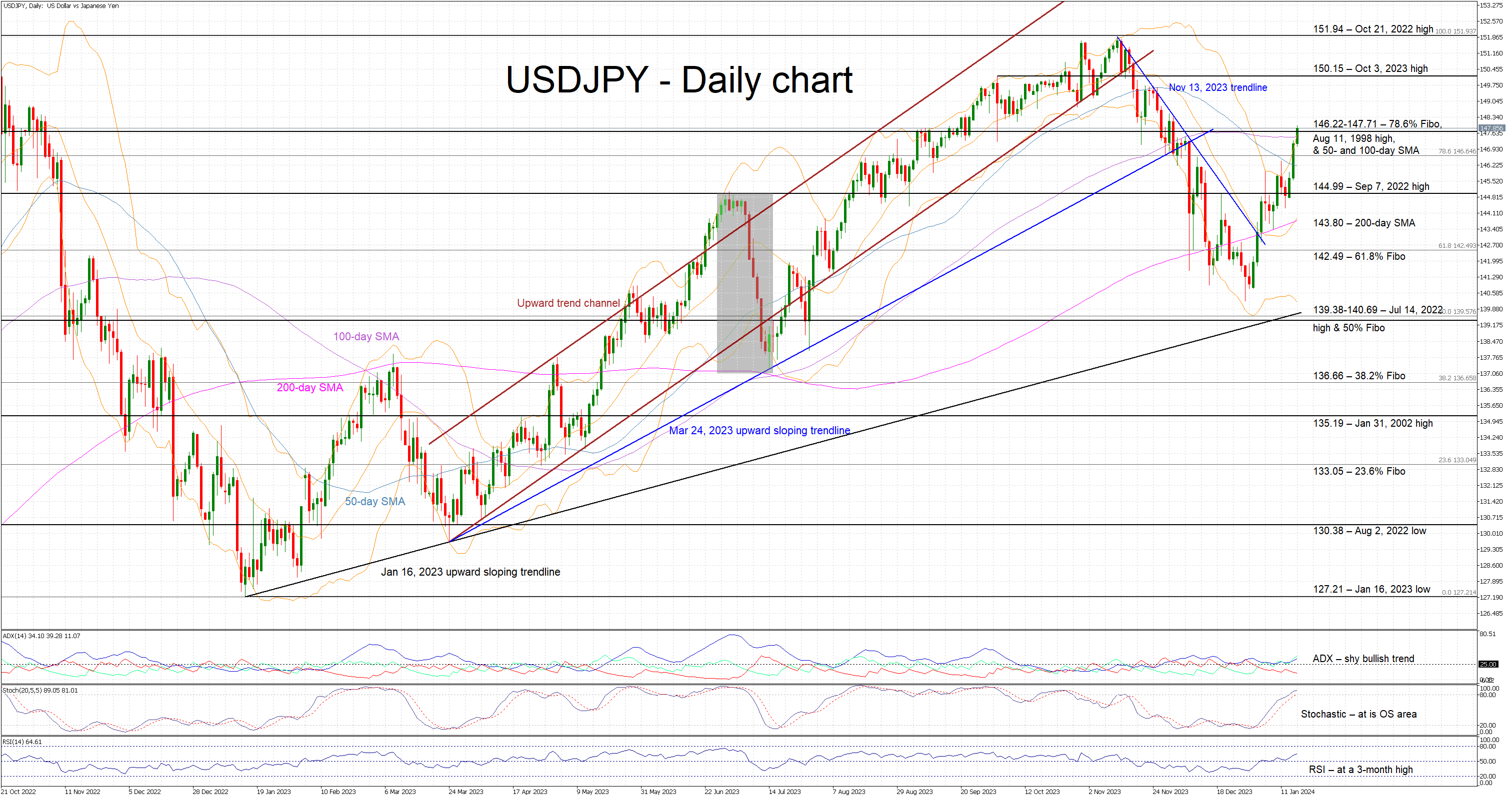

USDJPY Rallies Ahead of Key Market Events

- USDJPY continues its upward trend; third consecutive green session

- It now tries to overcome a very busy resistance area

- Most momentum indicators support the current upleg

USDJPY is recording its third consecutive green candle today and it is now trying to overcome the busy 146.22-147.71 area. It has been an aggressive rally from the December 28, 2023 low of 140.24, cancelling out a good part of the November-December 2023 downleg. The market is preparing for some key events over the next few trading days with most momentum indicators appearing supportive of the current upleg.

The Average Directional Movement Index (ADX) is edging higher, above its 25-threshold and signaling the presence of a modest bullish trend in the market. Similarly, the RSI has jumped above its 50-midpoint and is now hovering around a new 3-month high. More importantly, the stochastic oscillator has entered its overbought territory, a tad above its moving average. It can stay there for a while before signaling the end of the current bullish move.

Should the bulls remain hungry, they could try to decisively overcome the busy 146.22-147.71 range, which is populated by the 78.6% Fibonacci retracement of the October 21, 2022 - January 16, 2023 downtrend, the August 11, 1998 high and the 50- and 100-day simple moving averages (SMAs). Higher, the bulls could stage a move towards the October 3, 2023 high at 150.15 with the ultimate target possibly being the 151.94 level.

On the flip side, the bears could try to defend the 146.22-147.71 area and then gradually push USDJPY towards the September 7, 2022 high of 144.99. Even lower, the support set by the 200-day SMA at 143.80 could prove stronger than currently anticipated, but if successfully broken, the bears could then have a go at 61.8% Fibonacci retracement level at 142.49.

To sum up, the upward move in USDJPY continues, gaining the support of most momentum indicators but the bears are hoping that the busy 146.22-147.71 range could put a temporary stop on the current rally.

Any Speculation on Time of BoE Rate Cuts Very Premature

Markets

US yields yesterday started a catching up move after the rise in Germany on Monday. Contrary to last week, a poor NY Empire manufacturing survey this time was no pretext to push yields back lower. On the contrary, US yields were propelled higher by comments of Fed’s Waller as he provided a detailed analysis of the Fed’s rate strategy going forward. Waller acknowledged that the pieces are falling in place for the Fed to gradually start cutting rates this year. However, the process should be deployed ‘methodically and carefully’. In this respect, he tempered markets’ aggressive rate cut expectations. “With economic activity and labor markets in good shape and inflation coming down gradually to 2%, I see no reason to move as quickly or cut as rapidly as in the past”, he was quoted. He also indicated that it is reasonable to start thinking about slowing the pace of the balance sheet runoff. US yields extended their intra-day rise post Waller, closing between 7.5 bps (2-y) and 12 bps (30-y) higher. Spill-overs from the US also help German yields back into positive territory. In a steepening move, the 2-y yield closed little changed, but the 30-y added 3.0 bps. Equities stayed in the defensive (S&P -0.37%). The rise in US real yields also supported the dollar. DXY set a now 2024 top (close 103.35). EUR/USD extensively tested the 1.0877 support (close 1.0875).

This morning, the combination of higher US yields and poor Chinese data (cf infra) is causing an outright risk-off positioning on Asian market. The dollar profits. EUR/USD declines further to 1.086. USD/JPY extends its sharp rally (USD/JPY 147.75). US yields maintain yesterday’s rise. Later today, the US December retail sales are taking center stage. Monthly sales growth is expected at 0.4% M/M (0.2% for the control group). We look out whether markets keep Fed’s Waller’s assessment in mind that there is no reason to rush to aggressive rate cuts as US activity data continue to show resilience. Of course, the risk-off sentiment might hamper a further rise in (US) yields. Even so, the US 10-y yield sustainably returning above 4.10% indicates that the bottoming out process is finding more solid ground. The USD momentum is also improving further. EUR/USD 1.0724 (Dec low) is next target on the charts.

This morning, the UK inflation brought a material upward surprise, suggesting that there is still a lot of work to do for the BoE. Headline inflation rose 0.4% M/M and 4.0% Y/Y (from 3.9%). Core inflation was unchanged at 5.1% (VS 4.9% expected). Services inflation also remains stubbornly high at 6.4% (from 6.3%). The report clearly shows that any speculation on the time of BoE rate cuts is very premature. Sterling rebounds after the data. EUR/GBP drops from 0.8615 back to the 0.86 big figure.

News & Views

China’s economic growth hit the 5% target in 2023. Official numbers released this morning showed the economic number two in the world expanding 5.2% y/y while ending the year with 1% quarterly growth. Hitting the government target was made easier by 2022’s low comparison base. Separate December data indeed show the Chinese economy is still struggling to recover from a housing and consumer confidence slump. Residential property sales fell 6% for the whole year compared to 2022 and home prices declined at the fastest monthly rate (-0.45%) since 2015. Retail sales came in at a disappointing 7.2%. In addition, the jobless rate for the first time in five months picked up in December, from 5% to 5.1%. Industrial production extended a recovery that began early last year (4.6% YtD y/y) while fixed investments showed tentative signs of bottoming out after a year’s long decline. They are only faint spots that won’t ease calls for additional fiscal stimulus, especially as the government is rumoured to set a growth target between 4.5-5% for this year at the March National People convention. Monetary support is also seen as upcoming, even as the PBOC earlier this week defied expectations for a 10 bps cut to its one-year lending facility rate. China’s yuan is holding steady after the publication of the figures. USD/CNY is testing resistance at 7.20.

Early indicators from a Swedish private data company showed that housing construction started weakening again towards the end of 2023. Coming ahead of official data, the series showed new home construction fell by 4.7% m/m in December while readings of the previous months were revised lower. That brings the total decline from the peak in August 2021 to 68%. The numbers followed a couple of months which suggested the market was more or less stabilizing. Swedish housing faced a deep rout after the central bank sharply raised interest rates to fight inflation. Some 75% of homeowners have mortgages with variable rates, leading to a fast pass-through of monetary policy.

UK Inflation Unexpectedly Rebounds

Yesterday was just another day where another policymaker pushed back on the exaggerated rate cut expectations. Federal Reserve’s (Fed) Christopher Waller said that the Fed should go ‘methodically and carefully’ to hit the 2% inflation target, which according to him is ‘within striking distance’, but ‘with economic activity and labour markets in good shape’ he sees ‘no reason to move as quicky or cut as rapidly as in the past’, and as is suggested by the market pricing. So that was it. Another enlightening moment went down the market’s throat in the form of a selloff in both equities and bonds. The US 2-year yield – which captures the rate expectations rebounded 12bp, the 10-year yield jumped past the 4%, the US dollar index recovered to a month high and is testing the 200-DMA resistance to the upside this morning, while the S&P500 retreated 0.37%.

Waller spoke from the US yesterday, but many counterparts are wining, dining and speaking in the World Economic Forum in Davos this week, which doesn’t only offer snowy and a beautiful scenery this January, but it also serves as a platform to many policymakers to bring the market back to reason. Expect more comments of this hawkish kind during this week. It turns out that one of the most popular topics of this year’s WEF is rising inflationary risks due to the heating tensions in the Red Sea which disrupt the global trade roads and explode the shipping costs.

The EUR/USD slips into bearish consolidation zone

The European Central Bank (ECB) officials were the first ones to push back the rate cut expectations. They were the first ones to attract attention to the looming inflation risks and to the idea that the ECB doesn’t consider cutting the rates despite the slowing economic activity and looming recession that would – in theory – justify rate cuts in the euro area way more than rate cuts in the States, where growth and jobs numbers remain surprisingly and non-alarmingly resilient.

So many ask why the EURUSD doesn’t benefit from that hawkishness. Well, it did to some extent. The pair advanced past the 1.10 level at the end of last year. Yet, the reality is, even though the ECB starts cutting the rates after the Fed and cuts less than the Fed, the deterioration in the Eurozone’s economic fundamentals had already started counterweighing the hawkish ECB views. And now that the Fed members have started giving out a more hawkish voice to balance out the overly stretched Fed cut expectations, the downside correction in the EURUSD is all but surprising. From a technical perspective, there is an important development in the EURUSD. The pair slipped below 1.0875, the major 38.2% Fibonacci retracement on the October to now rebound and is now in the medium-term bearish consolidation zone. There is potential for a deeper fall. The next natural targets for the bears are the 200-DMA, near 1.0845, and the 50% retracement, near 1.0793.

Unexpected rise in UK inflation

Cable rebounded following an unexpected rebound in British inflation numbers this morning. Headline inflation unexpectedly rebounded to 4%, while core inflation remained steady at 5.1% versus the expectation of a decline below the 5% mark.

This morning’s inflation disappointment lead sterling bears to trim bets below the 1.26 mark.

To give Rishi Sunak his due, inflation in Britain more than halved last year and is expected to return to the Bank of England’s (BoE) 2% target by spring, but the possibility of a U-turn in the inflation trend due to the geopolitical developments is a mounting risk and call for a balanced approach from the BoE. But regardless of a hawkish position, UK’s anemic growth should limit any positive move in sterling against the US dollar.

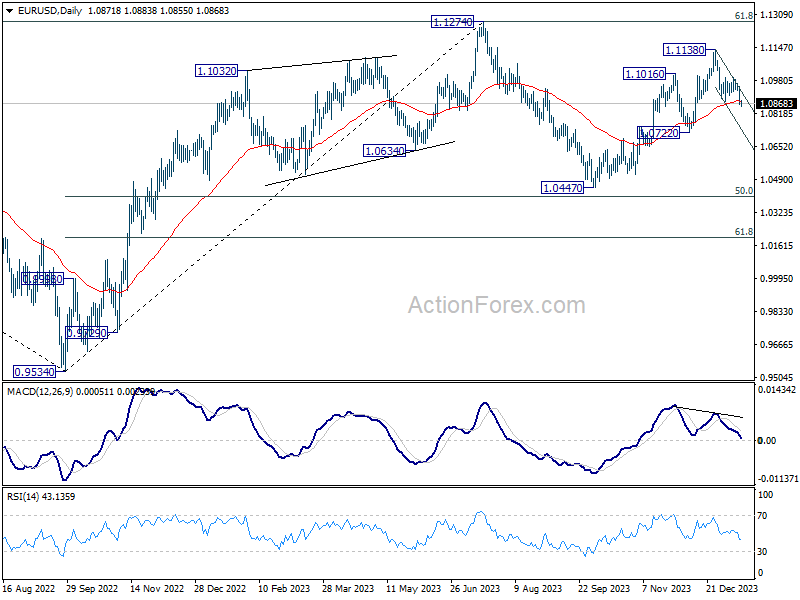

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0841; (P) 1.0897; (R1) 1.0933; More...

Intraday bias in EUR/USD remains on the downside. Fall from 1.1138 is in progress for 1.0722 support. Sustained break there will argue that whole rise from 1.0447 has completed, and target this low. For now, risk will stay on the downside as long as 1.0995 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

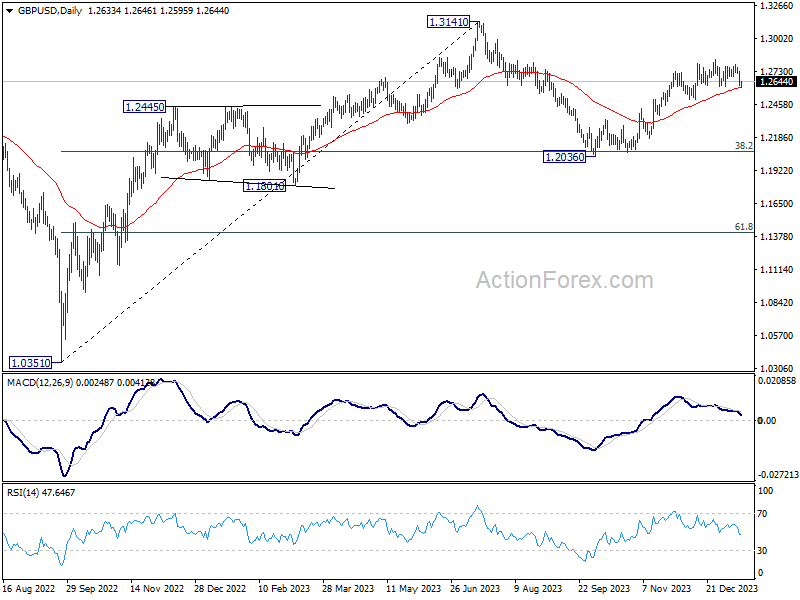

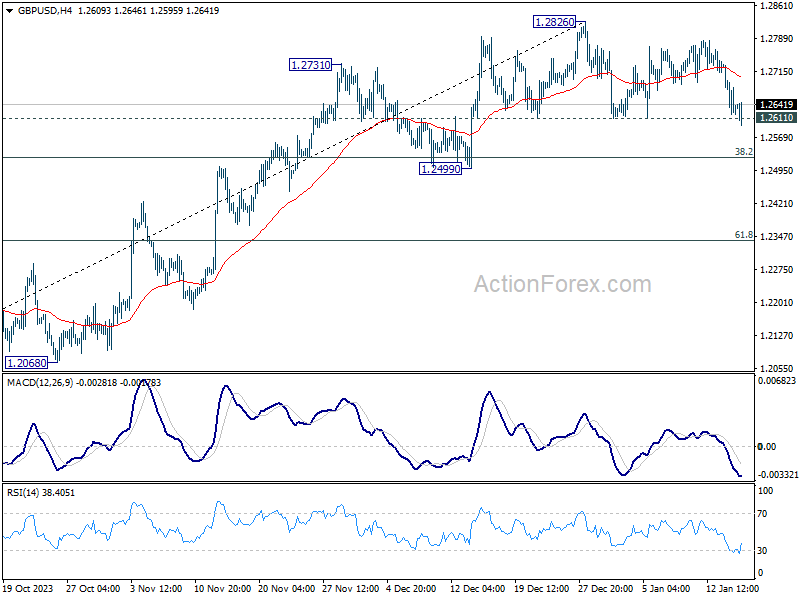

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2592; (P) 1.2664; (R1) 1.2709; More...

GBP/USD recovered quickly after brief breach of 1.2611 support and intraday bias remains neutral. On the downside, firm break of 1.2611 will resume the decline from 1.2826 to 1.2499 support. Nevertheless, strong rebound from current level will retain near term bullishness. Decisive break of 1.2826 will resume whole rally from 1.2036.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.