Sample Category Title

Sunset Market Commentary

Markets

With US investors returning from the Martin Luther King Holiday, question was whether US markets would join yesterday’s rebound in German yields. Or would they maintain their soft bias as was the case after last week’s CPI and even more US PPI data? Early in Asian and European dealings, US yields indeed copied the move from Germany yesterday. The 2-y tried to regain the 4.2% mark. The 10-y returned to the 4% barrier. German/EMU yields in the meantime eased slightly. Inflation expectations in the ECB consumer survey (November) for the 1-year ahead CPI expectation declined from 4.0% to 3.2%. 3-y expectations also eased more than expected, from 2.5% to 2.2%. On the hawkish side of the equation, ECB Nagel repeated that the ECB still has a way to go on inflation. French Council Member Villeroy, as usual was more balanced but also indicated the ECB is ‘bit more patient’ on rate cuts compared to what markets are pricing. Early in US dealings, the rise in US yields was briefly disrupted by an unexpectedly sharp fall in the NY Fed Empire manufacturing survey (-43.7 from -14.5 vs -5.0 expected). However, the market reaction function this time was different from end last week. US yields easily reversed the initial drop and currently add between 5 bps (2-y) and 9.0 bps (30-y). German yields can’t build on yesterday’s rebound, ceding between 4.0 bps (2-y) and 1.0 bp (30-y). Equities continue trading in red a s first earnings are kicking in. The rise in US yields combined with a fragile risk sentiment this time triggered outright USD strength. DXY jumped north of the 103 big figure (103.15). EUR/USD dropped below 1.09 and is testing last week’s low of 1.0877. A break would single more EUR/USD downside potential. Soft UK wage data published this morning (weekly earnings ex-bonus easing from 7.2% to 6.6%) failed to trigger a sustained rebound of EUR/GBP away from the 0.86 level, which is again under test currently. Tomorrow’s UK CPI data probably have more market moving potential.

News & Views

Polish monetary policy council member Kotecki today countered a proposal by his fellow rate setter last week. MPC Dabrowski suggested that the central bank might need to tighten monetary policy again if inflation rises back to 6%-8% in H2 2024 by either raising rates or selling Polish bonds during pandemic-related QE programmes (total amount of PLN 144bn). Kotecki called the QT proposal completely incomprehensible in a situation of single-digit and falling inflation and could be perceived as the MPC joining in on a political attack and blackmail against the new government. With the latter, he refers to rift between new PM Tusk and Polish president Duda, a nominee by the previous PiS-government. Since pivotal parliamentary elections in October of last year, Duda, who has quiet some vetoing powers, first delayed Tusk’s nomination. Next he vetoed the December budget bill and sheltered two fugitive (PiS) members of parliament in his palace, ignoring a court verdict for abuse of power. Tusk faces a tough balancing act as he doesn’t want to immediately overturn previous PiS-policies with local and European elections scheduled later this year. Presidential elections take place in 2025. The ongoing power struggle made the Polish zloty give back some of the impressive post-election gains with EUR/PLN moving from levels of around 4.33 at the start of the year to currently 4.39.

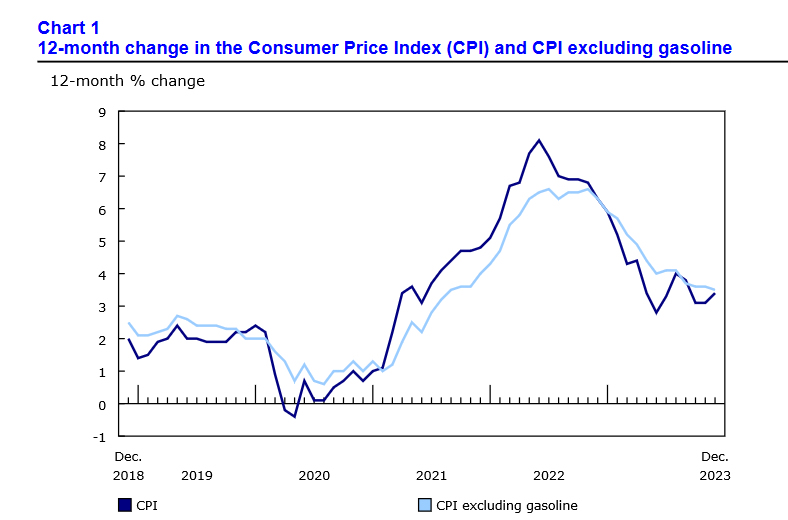

Canadian headline inflation printed in line with forecasts, dropping by 0.3% M/M with the Y-Y figure nevertheless up from 3.1% to 3.4% (base-year effect with gasoline prices falling more on a monthly basis in December 2022). The big (upward) surprise came from core inflation readings. The Bank of Canada’s preferred trimmed mean gauge accelerated from 3.5% Y/Y to 3.7% Y/Y instead of the hoped for slowdown to 3.4% Y/Y. Rent prices continued to climb, rising 7.7% Y/Y from 7.4% Y/Y. Passenger vehicle prices was the other main driver of core inflation. Another closely watched metric, a three-month moving average of underlying price pressure, rose back above 3% (annualized pace). Canadian swap yields rise by up to 5 bps at the front end of the curve with the loonie profiting (USD/CAD 1.3450 from 1.35 ahead of the release) despite USD strength. The Bank of Canada meets next week. Canadian money markets are less convinced that the BoC will start cutting policy rates as soon as April (preferred scenario ahead of data).

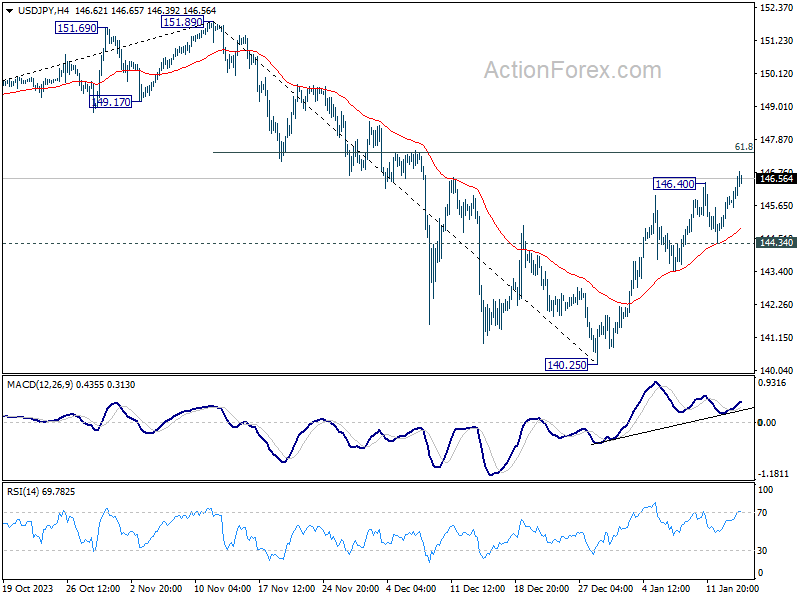

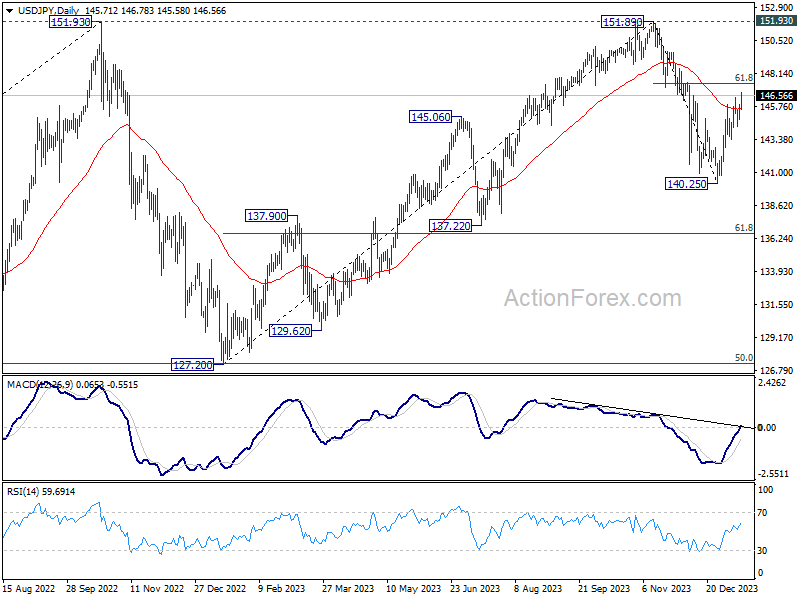

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.09; (P) 145.52; (R1) 146.19; More...

USD/JPY's rally from 140.25 resumed by breaking 146.40 and intraday bias is back on the upside. Strong resistance should be seen from 61.8% retracement of 151.89 to 140.25 at 147.4 to limit upside. On the downside, break of 144.34 will turn bias back to the downside for retesting 140.25 low. However, firm break of 147.44 will target 151.89 high instead.

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

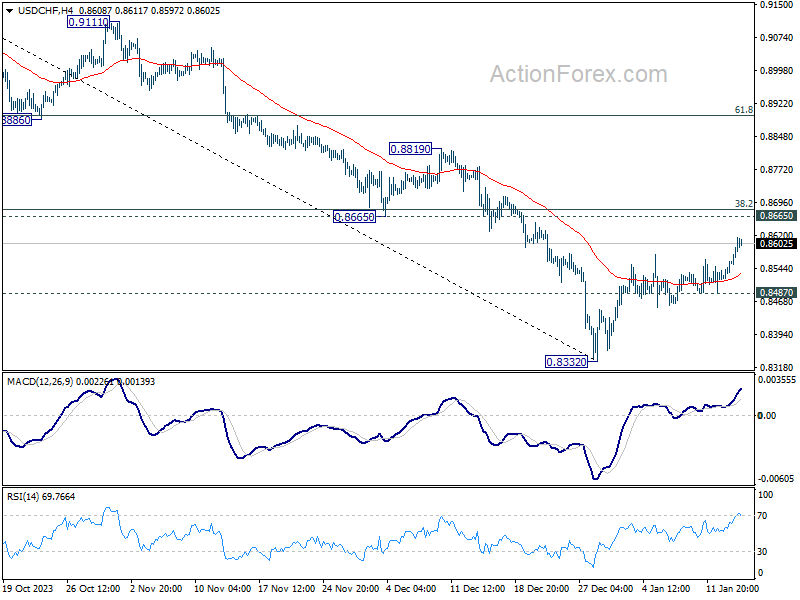

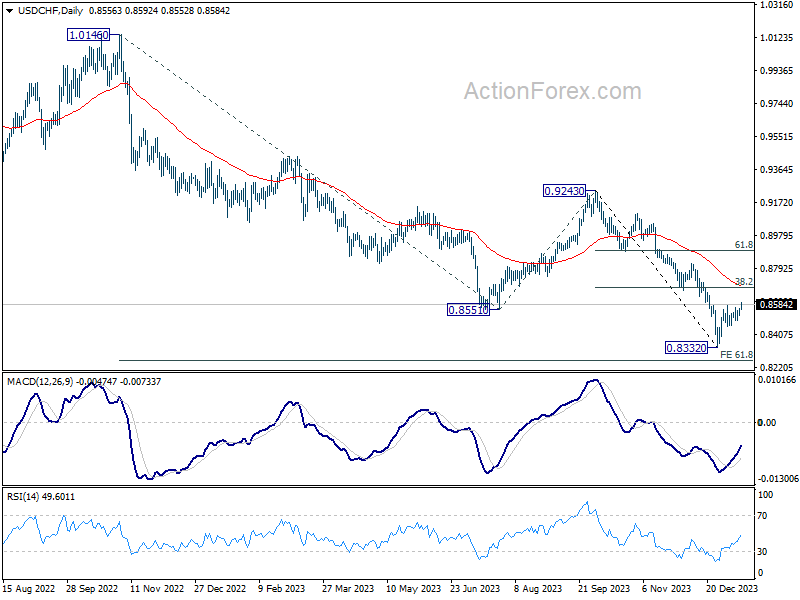

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8526; (P) 0.8547; (R1) 0.8579; More....

While USD/CHF's rebound could extend higher, near term outlook will stay bearish as long as 0.8665 support turned resistance holds. On the downside, break of 0.8487 minor support will bring retest of 0.8332 low first. However, decisive break of 0.8665 will rise the change of larger trend reversal and target 0.8819 resistance next.

In the bigger picture, outlook in USD?CHF will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should extend further to 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257.

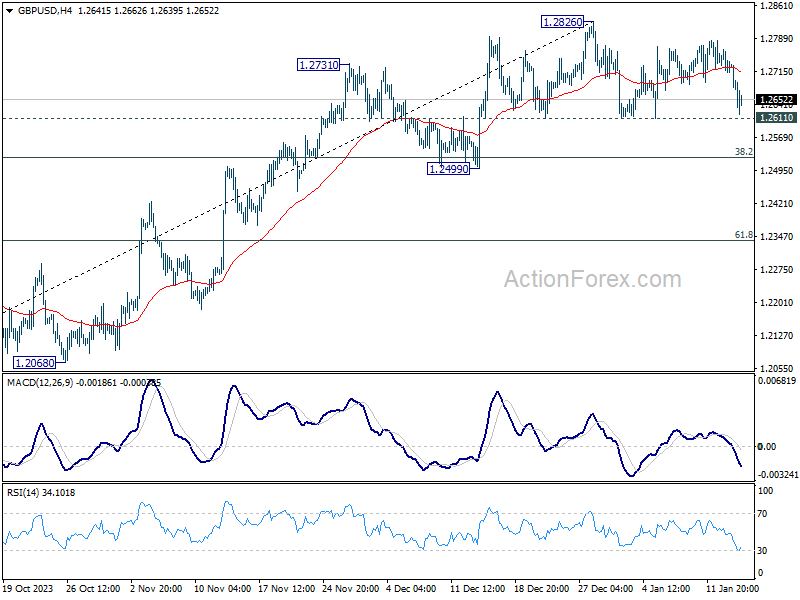

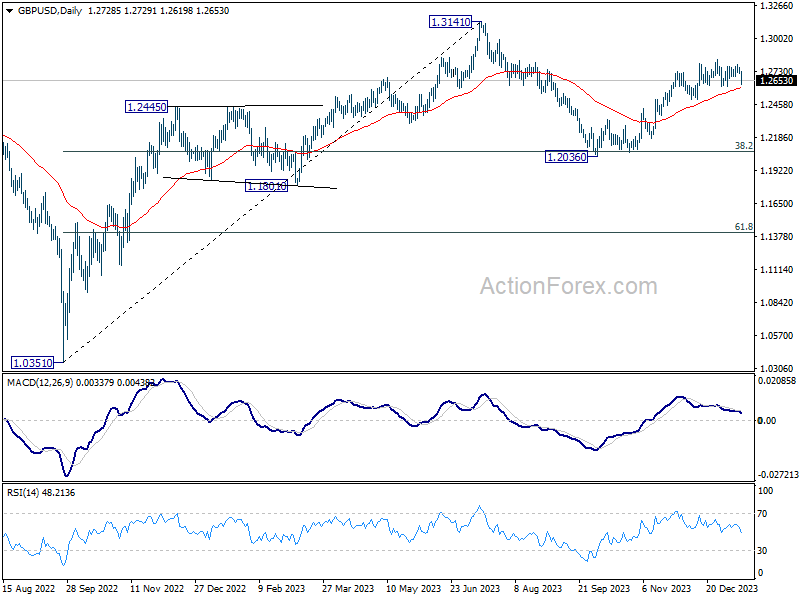

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2705; (P) 1.2735; (R1) 1.2758; More...

Immediate focus is now on 1.2611 support in GBP/USD with today's fall. Firm break there will resume the decline from 1.2826 to 1.2499 support. Nevertheless, strong rebound from current level will retain near term bullishness. Decisive break of 1.2826 will resume whole rally from 1.2036.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Canada: Little Progress on Inflation in December

As expected, headline CPI inflation moved in the wrong direction in December, rising three ticks to 3.4% year-on-year (y/y).

Energy prices, and more specifically gasoline prices, were a key culprit boosting headline CPI higher. Gasoline prices fell on a monthly basis, but are now 1.4% higher than a year ago, a big swing from being down 7.7% y/y in November. This is the result of a base-year effect, as prices fell 13% in December 2022.

Food inflation is proving stubborn, with prices up 5% y/y in December, matching November's pace, with prices rising 0.3% m/m.

Core goods prices were also a bit stubborn, up 2.2% y/y, with higher prices for new vehicles (+2.3% y/y) likely playing a role.

Services inflation thankfully cooled a bit in December, up 4.3% y/y versus 4.6% in November. This was despite continued strength in shelter inflation (+6% y/y), and particularly rent inflation, which was up 7.7% y/y from 7.4% in November.

The Bank of Canada's preferred "core" inflation measures also heated up in December. CPI trim was 3.7% y/y up from 3.5% in November, while CPI median held steady at 3.6% y/y.

Key Implications

If you are looking for data to signal a rate cut is imminent, this isn't it. December's inflation report underscores that the last mile of getting inflation all the way back to 2% is the hardest. It took about a year for inflation to drop from its peak of 8% to around 3%, but over the past six months further headway has been halting. This leaves the Bank of Canada cautious as it considers when it will be appropriate to cut interest rates.

Despite December's report, we expect inflation, and the economy, will have cooled sufficiently by the spring for the Bank of Canada (BoC) to make its first interest rate cut in April (see report). That said, inflation is unlikely to be quite at 2%. As Governor Macklem pointed out in December, the BoC doesn't need to see 2% to begin normalizing monetary policy, but rather be confident it is getting there.

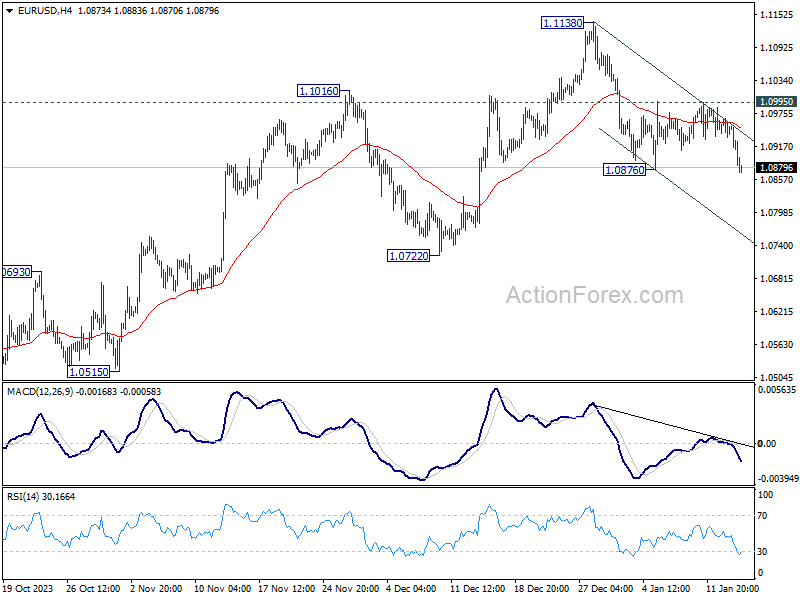

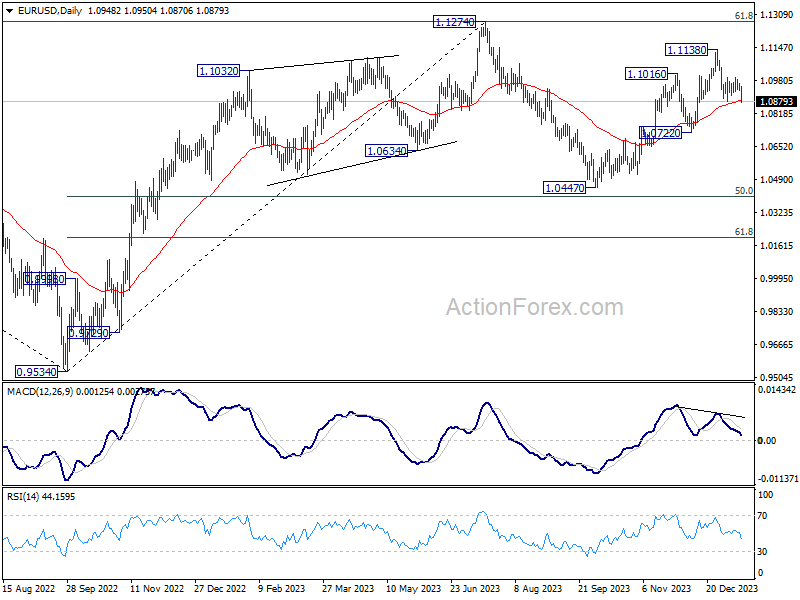

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0934; (P) 1.0951; (R1) 1.0968; More...

EUR/USD's fall from 1.1138 short term top is trying to resume be breaching 1.0876. Intraday bias is back on the downside for 1.0722 support. Sustained break there will argue that whole rise from 1.0447 has completed, and target this low. For now, risk will stay on the downside as long as 1.0995 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

Dollar’s Rally Unfazed by Weak Manufacturing Data, Bolstered by Risk Aversion

Dollar continues its strong rally in early U.S. session, making an attempt to surpass January high against Euro. The market appears to be ignoring surprisingly poor results of Empire State Manufacturing survey. Instead, mild risk-off sentiment is prevailing, offering some support to the greenback.

New Zealand and Australian Dollars are the weakest performers so far in the day's trading, with the Japanese Yen also underperforming. On the other hand, Canadian Dollar emerges as the second strongest currency, buoyed by higher-than-expected CPI data. Euro and Swiss Franc are also showing some strength, while British Pound is mixed. Sterling dipped against Euro earlier today after data showing slowdown in UK wages growth, but there was no follow through momentum.

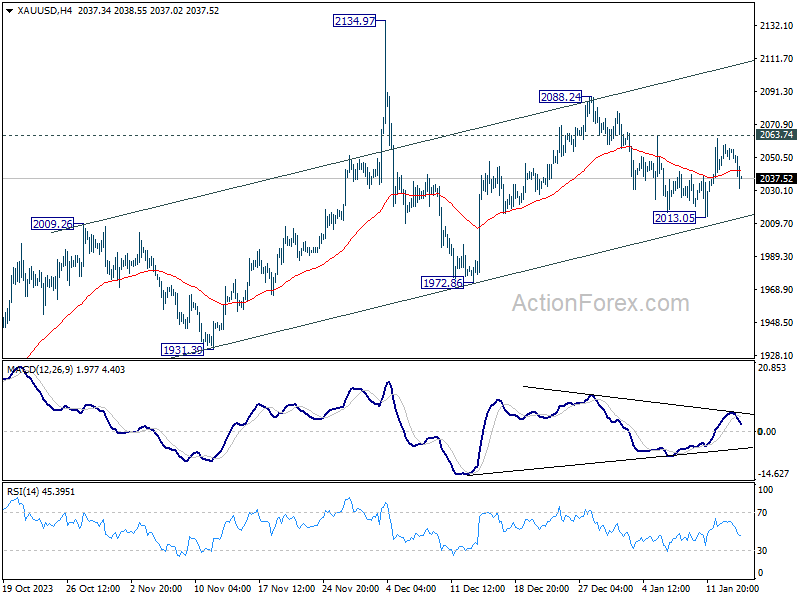

Technically, Gold fall sharply on Dollar strength today. The rejection by 2063.73 minor resistance argues that fall from 2088.24 might not be over yet. Break of 2013.05 will raise the chance of larger correction, and target 1972.86 support and below. Nevertheless, break of 2063.74 will retain near term bullishness for 2088.24 and above.

In Europe, at the time of writing, FTSE is down -0.47%. DAX is down -0.55%. CAC is down -0.43%. Germany 10-year yield is down -0.0103 at 2.228. UK 10-year yield is down -0.0070 at 3.796. Earlier in Asia, Nikkei fell -0.79%. Hong Kong HSI fell -2.16%. China Shanghai SSE rose 0.27%. Singapore Strait Times fell -0.45%. Japan 10-year JGB yield rose 0.0397 to 0.597.

Canada's CPI rises to 3.4% in Nov on gasoline base-year effect

Canada's CPI accelerated from 3.1% yoy to 3.4% yoy in November, above expectation of 3.3% yoy. The acceleration was largely due to base-year effect on gasoline prices. Excluding gasoline, CPI slowed slightly from 3.6% yoy to 3.5% yoy. On a monthly basis, CPI was down -0.3% mom, matched expected.

CPI median, which represents the middle point of price changes, remained steady at 3.6% yoy, exceeding the forecast of 3.4%. CPI trimmed, which excludes certain extreme price movements, rose from 3.5% yoy to 3.7%, also surpassing the expected 3.5%. Meanwhile, CPI Common, which is often viewed as the BoC's preferred measure of core inflation due to its stability, remained unchanged at 3.9% yoy, again higher than the anticipated 3.8%.

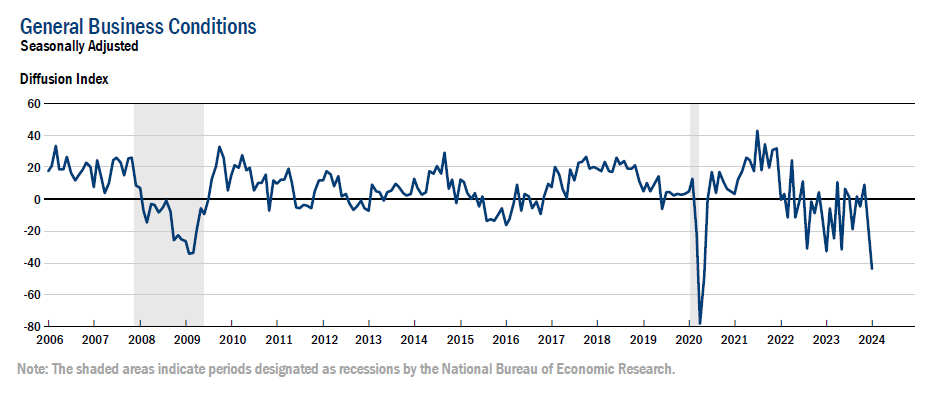

US Empire State manufacturing dives to -43.7, lowest since May 2020

US Empire State Manufacturing general business conditions index fell sharply from -14.5 to -43.7 in January, hitting the lowest level since May 2020. Looking at some details, new orders fell from -11.3 to -49.4. Shipments fell from -6.4 to -31.3. Prices paid rose from 16.7 to 23.2. Prices received fell from 11.5 to 9.5.

Richard Deitz, Economic Research Advisor at the New York Fed said, "this outsized drop suggests January was a difficult month for New York manufacturers, with employment and hours worked also contracting."

German's ZEW rises to 15.2 on rate cut expectations

Germany's ZEW Economic Sentiment rose from 12.8 to 15.2 in January, above expectation of 12.7. Current Situation index fell slightly from -77.1 to -77.3, below expectation of -77.0.

Eurozone ZEW Economic Sentiment fell from 23.0 to 22.7, above expectation of 21.9. Current Situation index rose 3.4 points to -59.3.

ZEW President Achim Wambach noted that "Economic expectations for Germany have improved again," attributing this positivity partly to expectations that ECB will cut interest rate in the first half of the year. This expectation is shared by "more than half of the respondents "

Furthermore, Wambach highlighted that there are even more pronounced shifts in US interest rate expectations. He stated, "More than two-thirds of the respondents predict interest rate cuts by the US Federal Reserve in the next six months."

Wambach also pointed out that the recent rise in inflation in Germany and Eurozone in December does not seem to have influenced the monetary policy expectations of the respondents.

ECB's Centeno: Inflation trajectory is very positive

At the World Economic Forum in Davos, ECB Governing Council member Mario Centeno highlighted the positive direction of medium-term inflation, noting that its "trajectory is very positive right now." He further told CNBC that "we don't need to do more than is needed"

On the topic of rate cuts, Centeno noted "once inflation starts going down sustainably, with an economy … that is not growing, where the challenges are huge, we need to be open to get all data on board and decide upon that."

Meanwhile, another ECB Governing Council member, Francois Villeroy de Galhau, speaking at a panel in Davos, cautioned against premature declarations of victory over inflation. However, he admitted that "our next move will be a cut, probably this year" even though he refrained from commenting on the timing.

ECB's Valimaki addresses market uncertainty rate and inflation outlook

In a Reuters interview, ECB Governing Council Member Tuomas Valimaki addressed the disparity between market pricing, which suggests a 150 basis points rate cut this year, and the views of economists.

He pointed out that the expectations reflected in money markets do not always align with economists' projections, indicating a significant level of uncertainty among market participants. The wide distribution around market prices, as mentioned by Valimaki, underscores the existing ambiguity and varied interpretations of future monetary policy directions.

Valimaki further elaborated on the implications of market expectations versus the ECB's baseline forecasts. He pointed out that if market rates were to fall more rapidly than projected, and the ECB's forecasts prove more accurate, it could lead to higher inflation. This scenario, he explained, "could delay monetary easing."

UK payrolled employment falls -24k in Dec, unemployment rate at 4.2% in Nov

UK payrolled employment fell -0.1% mom, or -24k, in December. Annual growth in employees fell from 1.3% yoy to 1.0% yoy. Median monthly pay increased by 6.6% yoy, up from prior month's 6.5% yoy. Claimant count rose 11.7k, below expectation of 18.1k.

In three months to November, unemployment rate rose to 4.2%, up 0.5% from the previous three month period. Employment rate fell to 75.5%, down -0.5%. Total weekly hours also fell -18.5 to 1040. Average earnings excluding bonus slowed from 7.3% 3moy to 6.6%, matched expectations. Average earnings including bonus fell from 7.2% 3moy to 6.5%, below expectation of 6.8%.

Japan's PPI slowed to 0.0% yoy in Dec, reflecting subsidy effects

Japan's PPI records a slowdown from 0.3% yoy to 0.0% yoy in December, above expectation of -0.3% yoy. Nevertheless, this figure represents the lowest PPI reading since -0.9% yoy decline in February 2021.

The deceleration in Japan's wholesale prices can be attributed partially to the government's intervention in the form of subsidies aimed at curbing petrol and utility bills. According to a BoJ official, these subsidies reduced wholesale inflation rate by approximately 0.9 percentage points.

In terms of trade-related price indices, there was a slight increase in export price index from 1.0% yoy to 1.1% yoy. Import price index improved from -10.1% yoy to -9.5% yoy.

On a month-over-month basis, the PPI rose by 0.3% mom, Meanwhile, export price index saw a marginal decline of -0.1% mom, and import price index was flat.

Australia's Westpac consumer sentiment plunges to 81, bleakest start since 90s

Australia's Westpac Consumer Sentiment index dropped by -1.3% mom to 81 in January. This figure is especially significant as it ranks in the bottom 7% of all observations since the inception of the survey in the mid-1970s. The only other instances of more pessimistic starts to the year were observed during the severe recession of the early 1990s.

Westpac attributed this "intense pressure" on consumers to surging cost of living, significantly higher interest rates, and increased tax burden, all of which are collectively impacting consumer incomes.

Despite the subdued consumer sentiment, Westpac highlighted that high inflation remains the primary concern for RBA. This focus on inflation suggests that the upcoming quarterly CPI release at the end of January will be a crucial determinant of RBA's policy decision in February.

"On balance, we expect the RBA to leave rates unchanged in February, and to be unlikely to raise rates further from here," Westpac noted. However, it also cautioned that an unexpected surge in inflation could complicate the decision, making it "a more finely balanced decision".

NZIER survey reveals improved business outlook and steady RBNZ policy anticipated

The latest quarterly survey of business opinion by New Zealand Institute of Economic Research revealed notable improvement in business sentiment. Only a net 2% of firms now expect general business conditions to deteriorate, compared to the 52% pessimism recorded in the previous quarter.

Christina Leung, principal economist at NZIER, expressed confidence that inflation in New Zealand is on track to return to RBNZ's target range of 1% to 3% by the second half of 2024, with a projection of reaching 2% in the first half of 2025.

"It's a pretty encouraging picture for the Reserve Bank and it reinforces our expectations that there won't be further increases," in interest rate, Leung stated.

However, Leung also mentioned that NZIER does not anticipate a reduction in the cash rate until the middle of the next year, advocating for a "wait and see approach." This cautious stance reflects a recognition of the need to monitor economic trends before making significant policy changes.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0934; (P) 1.0951; (R1) 1.0968; More...

EUR/USD's fall from 1.1138 short term top is trying to resume be breaching 1.0876. Intraday bias is back on the downside for 1.0722 support. Sustained break there will argue that whole rise from 1.0447 has completed, and target this low. For now, risk will stay on the downside as long as 1.0995 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | NZIER Business Confidence Q4 | -2 | -52 | ||

| 23:30 | AUD | Westpac Consumer Confidence Jan | -1.30% | 2.70% | ||

| 23:50 | JPY | PPI Y/Y Dec | 0.00% | -0.30% | 0.30% | |

| 07:00 | GBP | Claimant Count Change Dec | 11.7K | 18.1K | 16K | 0.6K |

| 07:00 | GBP | ILO Unemployment Rate (3M) Nov | 4.20% | 4.20% | 4.20% | |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Nov | 6.60% | 6.60% | 7.30% | 7.20% |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Nov | 6.50% | 6.80% | 7.20% | |

| 07:00 | EUR | Germany CPI M/M Dec F | 0.10% | 0.10% | 0.10% | |

| 07:00 | EUR | Germany CPI Y/Y Dec F | 3.70% | 3.70% | 3.70% | |

| 10:00 | EUR | Germany ZEW Economic Sentiment Jan | 15.2 | 12.7 | 12.8 | |

| 10:00 | EUR | Germany ZEW Current Situation Jan | -77.3 | -77 | -77.1 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Jan | 22.7 | 21.9 | 23 | |

| 13:15 | CAD | Housing Starts Dec | 249K | 244K | 213K | 211K |

| 13:30 | CAD | CPI M/M Dec | -0.30% | -0.30% | 0.10% | |

| 13:30 | CAD | CPI Y/Y Dec | 3.40% | 3.30% | 3.10% | |

| 13:30 | CAD | CPI Median Y/Y Dec | 3.60% | 3.40% | 3.40% | 3.60% |

| 13:30 | CAD | CPI Trimmed Y/Y Dec | 3.70% | 3.50% | 3.50% | |

| 13:30 | CAD | CPI Common Y/Y Dec | 3.90% | 3.80% | 3.90% | |

| 13:30 | USD | Empire State Manufacturing Index Jan | -43.7 | -5 | -14.5 |

US Empire State manufacturing dives to -43.7, lowest since May 2020

US Empire State Manufacturing general business conditions index fell sharply from -14.5 to -43.7 in January, hitting the lowest level since May 2020. Looking at some details, new orders fell from -11.3 to -49.4. Shipments fell from -6.4 to -31.3. Prices paid rose from 16.7 to 23.2. Prices received fell from 11.5 to 9.5.

Richard Deitz, Economic Research Advisor at the New York Fed said, "this outsized drop suggests January was a difficult month for New York manufacturers, with employment and hours worked also contracting."

Canada’s CPI rises to 3.4% in Nov on gasoline base-year effect

Canada's CPI accelerated from 3.1% yoy to 3.4% yoy in November, above expectation of 3.3% yoy. The acceleration was largely due to base-year effect on gasoline prices. Excluding gasoline, CPI slowed slightly from 3.6% yoy to 3.5% yoy. On a monthly basis, CPI was down -0.3% mom, matched expected.

CPI median, which represents the middle point of price changes, remained steady at 3.6% yoy, exceeding the forecast of 3.4%. CPI trimmed, which excludes certain extreme price movements, rose from 3.5% yoy to 3.7%, also surpassing the expected 3.5%. Meanwhile, CPI Common, which is often viewed as the BoC's preferred measure of core inflation due to its stability, remained unchanged at 3.9% yoy, again higher than the anticipated 3.8%.

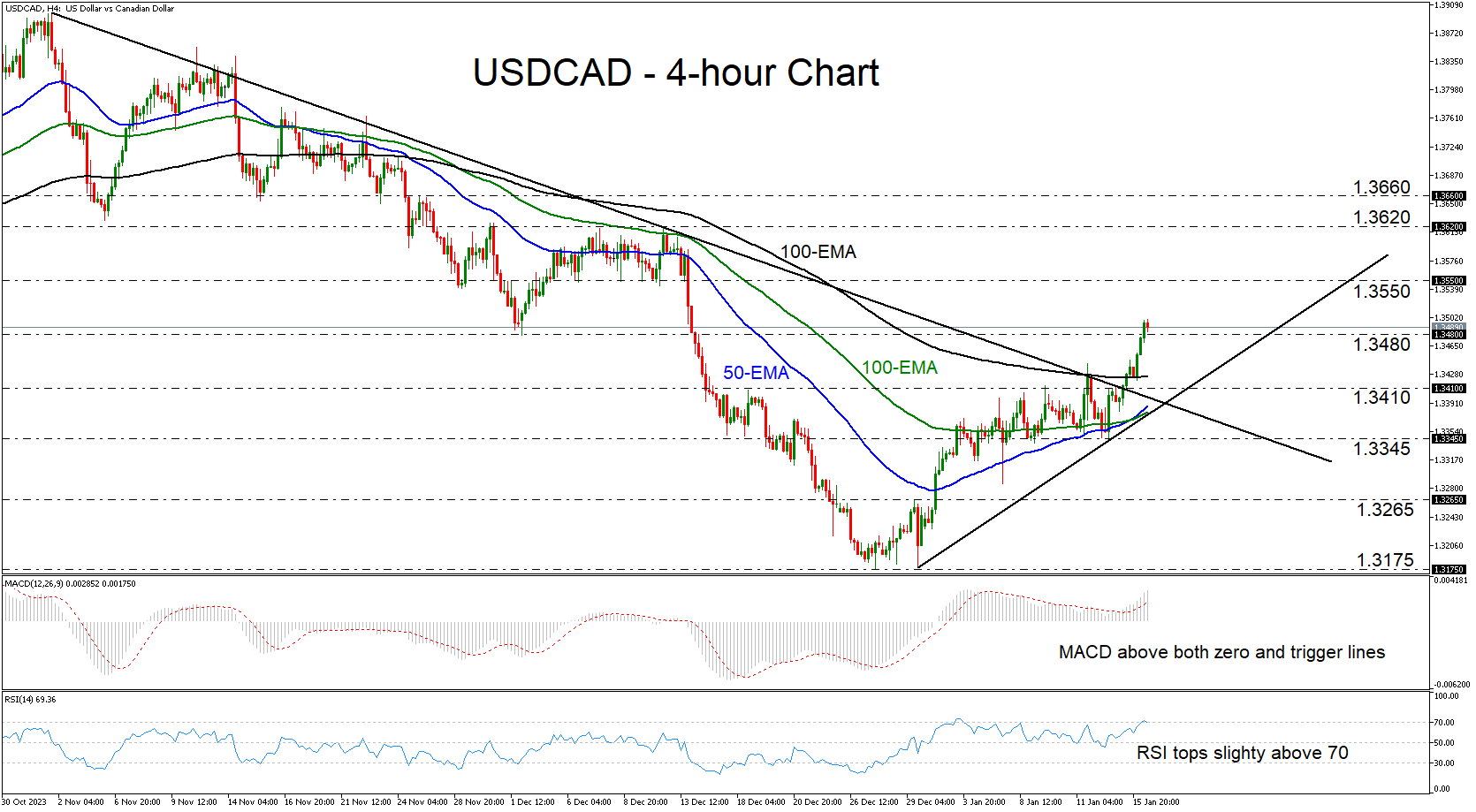

USDCAD Breaks Above Downtrend Line

- USDCAD surges after breaking a downtrend line

- MACD and RSI detect positive momentum

- A dip below 1.3345 is needed to turn the picture bearish again

USDCAD traded sharply higher today, after it broke above the downtrend line drawn from the high of November 1. The pair is currently respecting a new shorter-term upside support line taken from the low of December 29 and has just poked its nose above the 1.3480 zone, marked by the inside swing low of December 4.

The MACD lies above both its zero and trigger lines, while the RSI stands near 70. Both these short-term oscillators detect positive momentum, but the latter has ticked down, suggesting that there may be a corrective pullback in the works before the next leg north.

If the bulls are willing to jump back into the action soon, then the pair may travel towards the 1.3550 territory, which offered support between December 5 and 13. A break higher could carry more bullish implications, perhaps paving the way towards the highs of July 16 and December 12, at around 1.3620.

On the downside, a dip below 1.3345 may be needed to cancel the positive short-term picture. Such a move would take the pair below all three of the plotted moving averages and below both the aforementioned trendlines. The bears may then get encouraged to dive towards the 1.3265 zone, the break of which could see scope for additional declines towards the 1.3175 area, which offered support on December 27 and 29.

To sum up, the short-term picture of USDCAD looks positive as the pair is trading above a prior downtrend line. The move that could darken the outlook may be a dip below Friday’s low of 1.3345.