Sample Category Title

EUR/CHF Weekly Outlook

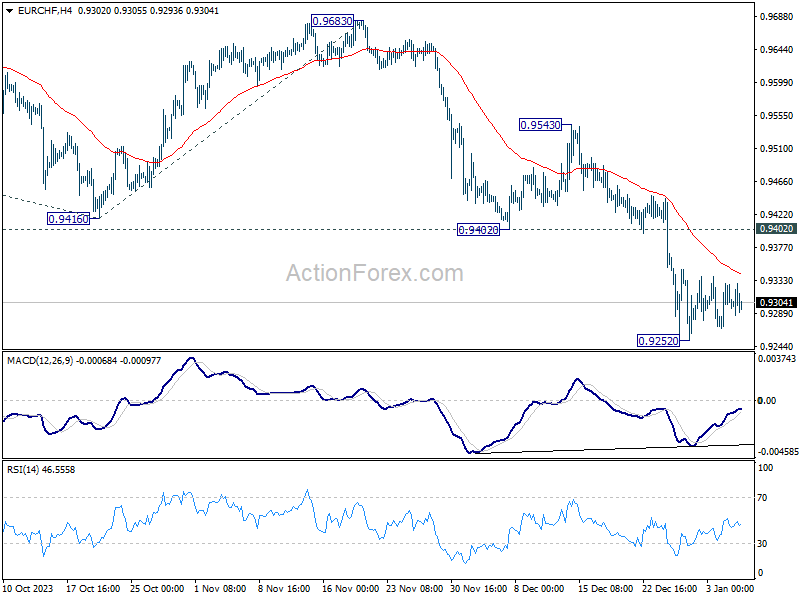

EUR/CHF stayed in consolidation above 0.9252 last week and outlook is unchanged. Initial bias stays neutral this week first. While another recovery cannot be ruled out, outlook will stay bearish as long as 0.9402 support turned resistance holds. On the downside, break of 0.9252 will resume larger down trend to 100% projection of 0.9995 to 0.9416 from 0.9683 at 0.9104 next.

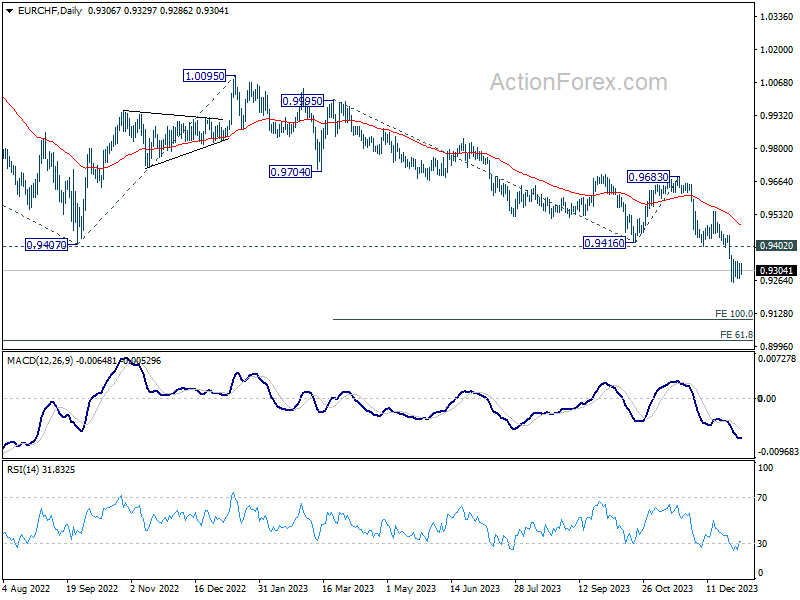

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Next target is 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

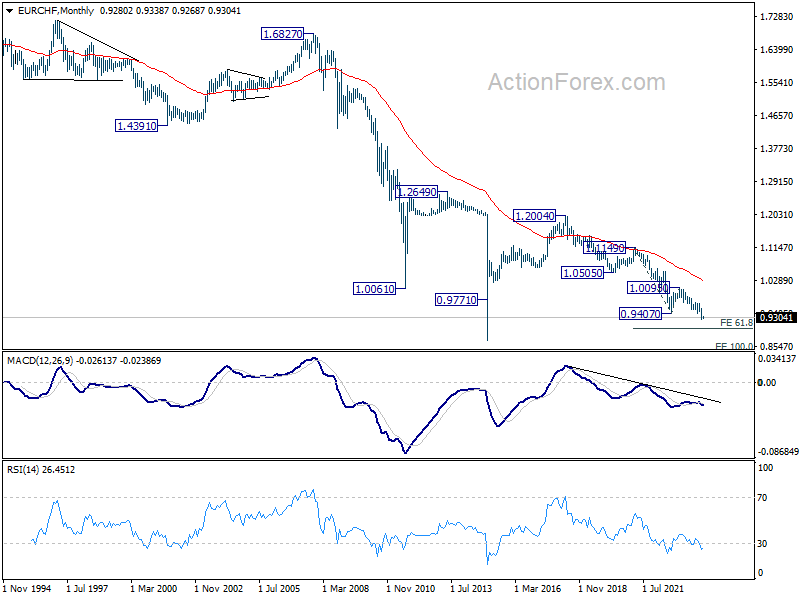

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.264). Larger down trend from 1.2004 (2018 high) is in progress.

USD/JPY: 2023 Review and 2024 Forecast

According to statistics, USD/JPY (US Dollar/Japanese Yen) is among the top three most traded currency pairs in the Forex market. This is facilitated by the pair's high liquidity, which ensures narrow spreads and favourable trading conditions. This means that traders can enter and exit positions with minimal costs. Additionally, the pair exhibits very high volatility, providing excellent profit opportunities, particularly in short-term and medium-term operations.

2023: The Yen of Unfulfilled Hopes

Throughout 2023, the Japanese currency steadily lost ground to the American dollar, and consequently, USD/JPY pair trended upwards. The yearly low was recorded on January 16th at 127.21, while the peak occurred on November 13th, with 1 dollar exchanging for 151.90 yen.

We have repeatedly mentioned that the weakening of the yen is due to the Bank of Japan's (BoJ) persistent ultra-dovish stance. Understandably, the negative interest rate of -0.1% cannot be attractive to market participants, especially against the backdrop of rising global yields and high rates set by the central banks of other leading countries. For investors, it was much more preferable to engage in carry trade: borrowing yen at low interest rates, then converting them to US dollars and Treasury bonds, which yielded a good profit due to the interest rate differential, all without any risk.

The monetary policy conducted by the Japanese Government and the Bank of Japan in recent years clearly indicates that their priority is not the yen's exchange rate, but economic indicators. Until mid-summer, to combat rising prices, regulators in the US, EU, and the UK tightened monetary policy and raised key interest rates. However, the BoJ ignored such methods, even though inflation in the country continued to rise. In June 2023, core inflation reached 4.2%, the highest in over four years. The only action the Bank of Japan took was to switch from strict to flexible targeting of the yield curve of Japanese government bonds, which did not aid the national currency.

Instead of tangible actions, Japan's Finance Minister Shunichi Suzuki, Bank of Japan Governor Kazuo Ueda, and Japan's top currency diplomat Masato Kanda actively engaged in verbal interventions. They and other senior financial officials consistently assured in their speeches that everything was under control. They claimed that the Government was "closely monitoring currency movements with a high sense of urgency and immediacy" and that it "would take appropriate measures against excessive currency movements, not ruling out any options." Here are a few quotes from Kazuo Ueda's speech: "Japan's economy is recovering at a moderate pace. […] Uncertainty regarding Japan's economy is very high. […] The rate of inflation growth is likely to decrease and then accelerate again. [But] overall, Japan's financial system maintains stability." In short, interpret it as you wish.

Winter-Spring 2023. At the beginning of the year, many market participants took the promises to "take immediate measures" quite seriously. They were hopeful for a rate hike, which had been stuck at a negative level since 2016. In January, economists at Danske Bank forecasted that following a rate increase, the USD/JPY pair would fall to 125.00 within three months. Analysts from the French Societe Generale pointed to the same target. Their colleagues from ANZ Bank did not rule out the possibility of the pair reaching around 124.00 by the end of 2023. According to BNP Paribas' projections, a tightening of monetary policy was expected to stimulate the repatriation of funds by Japanese investors, potentially leading the USD/JPY pair to fall to 121.00 by year's end. Economists from the international financial group Nordea anticipated it dropping below 120.00. Potential significant strengthening of the Japanese currency was also suggested by strategists from Japan's MUFG Bank and HSBC, the largest bank in the UK.

Summer 2023. As time passed, nothing significant occurred. Commerzbank, a German bank, stated that the yen is a complex currency to understand, possibly due to the BoJ's monetary policy. Kristalina Georgieva, the Managing Director of the International Monetary Fund (IMF), subtly hinted that it "would be appropriate to bring more flexibility to the monetary policy of the Bank of Japan."

In the first half of the summer, market participants began to adjust their forecasts. Economists at Danske Bank now predicted the USD/JPY rate to be below 130.00 over a 6-12 month horizon. A similar forecast was made by strategists at BNP Paribas, projecting a level of 130.00 by the end of 2023 and 123.00 by the end of 2024. Societe Generale's July forecast also became more cautious. Analysing the pair's prospects, the bank's experts expected that the yield on 5-year U.S. Treasury bonds would fall to 2.66% within a year, allowing the pair to break below 130.00. If the yield on Japanese government bonds (JGB) remains at the current level, the pair might even drop to 125.00.

Wells Fargo's prediction, one of the 'big four' banks in the US, was considerably more modest, with its specialists targeting a USD/JPY rate of 136.00 by the end of 2023 and 129.00 by the end of 2024. MUFG Bank declared that the Bank of Japan might only decide on its first rate hike in the first half of 2024. Only then would a shift towards strengthening the yen occur. Regarding the recent change in yield curve control policy, MUFG believed it was insufficient by itself to trigger a recovery of the Japanese currency. Danske Bank stated that expecting any steps from the BoJ before the second half of 2024 was not advisable.

Autumn-Winter 2023. No one held any hope that the Bank of Japan (BoJ) would change its monetary policy before the end of the year. However, market participants started fearing that the weak yen might eventually mobilize Japanese officials to move from verbal interventions to actual actions.

The USD/JPY pair was eagerly racing towards the critical mark of 150.00. Market participants vividly remembered that in the fall of 2022, when the pair reached a 32-year high at 152.00, Japanese authorities initiated financial interventions. Adding fuel to the fire was a report by Reuters, stating that Japan's chief currency diplomat Masato Kanda had announced the banking authorities were considering intervention to end "speculative" movements.

Then, on October 3, as the quotes slightly exceeded the "magical" height of 150.00, reaching a peak of 150.15, what everyone had been anticipating for so long finally happened. In just a few minutes, the USD/JPY pair plummeted nearly 300 points, halting the slide at 147.28. Japan's Finance Minister, Shunichi Suzuki, refrained from commenting on the event. He vaguely stated that "there are numerous factors determining whether movements in the currency market are excessive." However, many market participants believed this to be a real currency intervention. Although, of course, one cannot rule out the mass automatic triggering of stop-orders at the breakthrough of the key level of 150.00, as such "black swan" events have been observed before.

Whatever the case, the intervention did not significantly help the Japanese currency, and 40 days later, it was trading again above 150.00, at the level of 151.90. It was at this moment, on November 13, that the trend reversed, and the strengthening of the yen became consistent. This happened a couple of weeks after the peak in yields of the ten-year U.S. Treasury bonds when markets became convinced that their decline had become a trend. It's important to recall that there's traditionally an inverse correlation between these securities and the yen. If the yield on Treasuries rises, the yen falls against the dollar, and vice versa: if the yield on the securities falls, the yen strengthens.

The primary reason for the resurgence of the Japanese currency was growing expectations that the Bank of Japan (BoJ) would finally abandon its negative interest rate policy, possibly sooner than expected. Rumours suggested that regional banks in the country, lobbying for an abandonment of yield curve targeting policy, were exerting significant pressure on the regulator.

The yen also benefited from market confidence that the key interest rates of the Fed and the ECB had plateaued, with only a decrease expected thereafter. As a result of this divergence, it was anticipated that investors would unwind their carry trade strategy and reduce the yield spreads between Japanese government bonds and those of the U.S. and Eurozone. According to most analysts, all these factors were expected to bring capital back to the yen.

The fourth quarter's low was recorded on December 28 at 140.24, after which USD/JPY ended the year 2023 at a rate of 141.00.

2024 – 2028: Fresh Forecasts

After three years of sharp decline, the yen's value might finally be turning around. This is the view held by market participants surveyed by Bloomberg. Overall, respondents expect the Japanese currency to strengthen next year, with the average forecast for USD/JPY pointing to a level of 135.00 by the end of 2024.

Several banks anticipate the pair trading within the range of 125.00-135.00 (Goldman Sachs at 130.00, Barclays at 135.00, UBS at 132.00, MUFG at 125.00). Currency strategists at HSBC believe the US dollar is currently overvalued and will return to its fair value over the next five years due to declining yields in the US and rising stock markets. HSBC experts expect the exchange rate of the pair to reach 120.00 by mid-2024 and drop to 108.00 by 2028. According to ING Group's forecasts, the rate will fall to around 120.00 only in 2025.

However, there are also those who predict further decline for the Japanese currency and a continued 'flight to the moon' for the pair. For instance, analysts at the Economic Forecasting Agency (EFA) expect USD/JPY to reach 166.00 by the end of 2024, 185.00 by the end of 2025, and 188.00 by the end of 2026. Wallet Investor's forecast suggests that the pair will continue its upward rally, reaching a mark of 208.10 by 2028.

In conclusion, for those who favour graphical analysis, it's noteworthy to mention that the behaviour of USD/JPY throughout 2023 almost perfectly aligns with Elliott Wave Theory. If in 2024 the pair continues to follow the tenets of this theory, we can first expect a bullish corrective wave B. This will be followed by a bearish impulse wave C, which could lead the pair to the levels anticipated by proponents of a strengthening Japanese currency.

Weekly Economic & Financial Commentary: Wait a Minute

Summary

United States: The Great Divergence

- Incoming economic data continue to shed light on how tighter monetary policy is placing unequal pressure across economic sectors. Interest rate sensitive segments like manufacturing and commercial construction remain under disproportionate strain, while the labor market appears to be only slowly moderating.

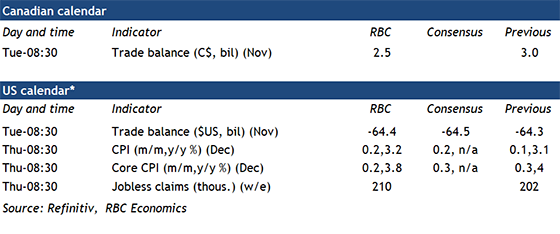

- Next week: NFIB Small Business Optimism (Tue.), CPI (Thu.), Monthly Treasury Statement (Thu.)

International: Ebbing Eurozone Inflation Suggests European Central Bank Edging Closer to Easing

- There was some mixed news from the Eurozone December CPI as headline inflation jumped to 2.9% year-over-year, but core inflation eased further to 3.4%. As long as Eurozone growth remains weak and the pace of price increases subdued, we believe the ECB will be comfortable delivering a rate cut at its April meeting.

- Next week: Mexico CPI (Tue.), Japan Labor Cash Earnings (Wed.), U.K. Monthly GDP (Fri.)

Interest Rate Watch: Wait a Minute

- The minutes from the FOMC's mid-December meeting suggest the committee aims to remain restrictive, though it acknowledges it may be cutting rates this year should recent progress on inflation continue. Despite market yearning for cuts, there was no large debate around when to start lowering rates.

Credit Market Insights: Index Points to Looser-Than-Average Financial Conditions

- The Adjusted National Financial Conditions Index (ANFCI), a tool used by the Chicago Federal Reserve to assess financial conditions conditional on growth in economic activity and inflation, dropped to -0.51 the last week of December, suggesting looser-than-average financial conditions.

Topic of the Week: Population Growth Returns to Pre-Pandemic Patterns in 2023

- New 2023 population estimates from the Census Bureau reveal the U.S. population grew by 0.5% between July 2022 and July 2023, translating to about 1.6 million new residents, the largest annual population gain since 2018. Overall, lower mortality and rebounding immigration point to population growth returning to pre-pandemic patterns.

The Weekly Bottom Line: Rate Cut Expectations Ease Slightly at the Start of 2024

U.S. Highlights

- Minutes from the December FOMC meeting confirmed that monetary policy was “likely at or near its peak” for this tightening cycle, but showed no meaningful discussion on rate cuts.

- The U.S. economy added a better-than-expected 216k jobs in December, but downward revisions to the prior two months kept a cooling trend intact. The unemployment rate held steady at 3.7%, while wage growth accelerated slightly.

- The ISM surveys overall signaled softness. Manufacturing remained in contractionary territory in December, albeit slightly less negative, while activity in the services sector slowed but remained in expansionary territory.

Canadian Highlights

- As the Canadian economy continues to gear down, the focus turns to when the Bank of Canada (BoC) will cut interest rates. Our view of a 25 basis-point cut at the BoC’s April rate setting date currently aligns with market expectations.

- Getting inflation back to the Bank of Canada’s 2% target remains the key consideration. We expect inflation to durably get below 3% in 2024 with a return to 2% in 2025.

- Canada’s job market is continuing to find its balance as job growth stalled in December. Meanwhile, preliminary housing market data showed surprising strength to end the year.

U.S. – Rate Cut Expectations Ease Slightly at the Start of 2024

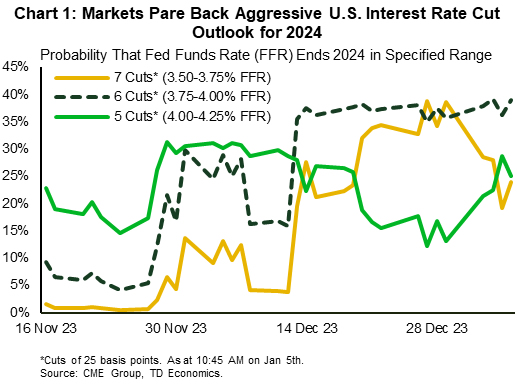

After a festive December where a sharp pullback in long-term yields sent risk assets higher, markets have gotten off to a much more sober start in 2024. Investors have seemingly adjusted their New Year’s resolutions, resulting in more moderate expectations for interest rate cuts this year. Cuts totaling 150 basis points by the end of 2024 remains the dominant scenario. The probability for more aggressive policy loosening (i.e., 7 cuts) has fallen sharply, while the probability of slightly less aggressive loosening (i.e., 5 cuts) has increased (Chart 1). In line with these developments, the 10-year Treasury yield has recouped some of the lost ground, rising from 3.8% at the end of December to near 4% recently, and equity markets have pared back year-end gains, with the S&P 500 down 1.6% from its recent peak.

The minutes from the December FOMC meeting contributed to the softening in expectations for interest rate cuts this week. After the Fed signaled that the policy rate would head lower in 2024, there was an anticipation that rate cut talk may have featured heavily at the last meeting. Committee participants confirmed that the policy rate was “likely at or near its peak for this tightening cycle”, given the reduction in inflation in 2023 and “growing signs of demand and supply coming into better balance in product and labor markets”. But, meaningful debate on rate cuts was missing. Instead, the discussion was somewhat more balanced, touching on both the risks of maintaining rates in a restrictive position for too long and the risks of prematurely easing policy. Participants noted that their outlooks were associated with an “unusually elevated” degree of uncertainty and stressed the importance of maintaining a data-dependent approach to setting monetary policy.

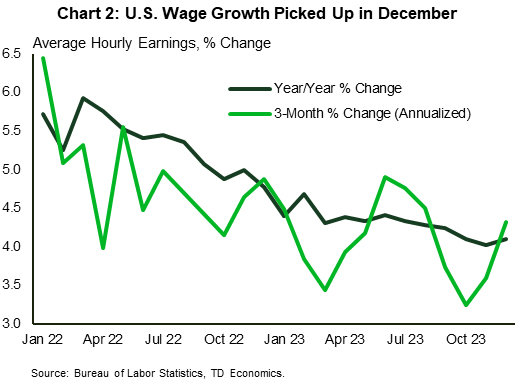

Chart 2 shows U.S. wage growth increased slightly in year-over-year terms in December, with a more meaningful acceleration recorded on a 3-month annualized basis (from 3.6% in November to 4.3% in December).

Speaking of data, this morning’s payrolls report showed that hiring unexpectedly accelerated in December, with the U.S. economy adding 216 thousand jobs. However, a downward revision of 71 thousand jobs to the prior two months limits some of the enthusiasm of this upward surprise. On a three-month moving average basis, hiring is still trending lower, which suggests that restrictive monetary policy continues to work as intended, cooling labor demand. Nonetheless, other aspects of the report still play in favor of showing some caution on easing monetary policy. The unemployment rate held steady at 3.7%. With the labor market still tight, wage growth gained some ground in December (Chart 2). A recent pullback in the job ‘quits’ rate – a leading indicator of labor costs – suggests that wage growth is nonetheless poised to cool ahead.

Other data reports were a mixed bag. Consumers increased vehicle purchases in December (up 3.2% to 15.8 million annualized), although this appears to be partially related to the return of year-end discounts. Meanwhile, the ISM indexes signaled softness. There was a slowdown in the expansion of the services side of the economy, and the manufacturing sector remained in contraction for the 14th month in row in December, albeit slightly less so on the month.

All factors considered, a loosening in monetary policy is coming, but we anticipate the Fed will show a bit more caution, with the first rate cut not likely to come until the second half of the year.

Canada – The Year of the Cut

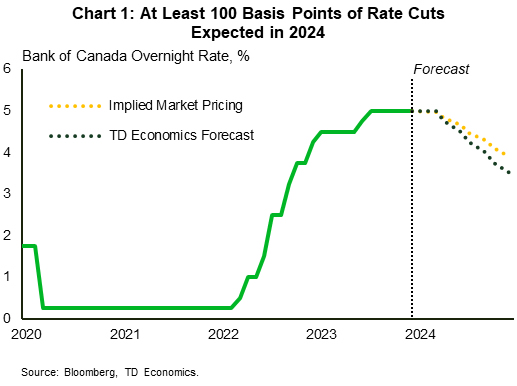

The new year is less than one week old, but the theme that will govern the next 12 months is firmly in place. After the most aggressive interest rate hiking campaign in over 40 years, the Bank of Canada's (BoC) focus is now shifting towards rate cuts. The burning questions are when the first cut will occur and how many cuts will be delivered. Markets had ended the year preparing for a loosening in conditions, with equities up over 10% from late-October and both Canadian and U.S. yields sliding almost 100 basis points (bps) from their fourth-quarter peaks.

The BoC will meet eight times in 2024 with their first policy decision on January 24th. For the last six months, the Bank has held the overnight policy rate at 5.00% as it continues to assess the incoming data. Markets are pricing the first rate cut to occur at the BoC's April meeting (Chart 1), in line with our forecast. We expect measured 25 bp cuts to occur over the remaining meetings, bringing the end-point to 3.50%, slightly lower than market expectations of 3.75%. Still, this rate is notably tighter than pre-pandemic levels.

Make no mistake, the effects of the cumulative 475 bps of interest rate hikes are taking hold. Consumers are reeling in their spending, and growth is evolving in a manner consistent with inflation inching closer to the BoC's 2% target. But the job is not done yet, as inflation remains elevated and wage growth is still running hot. Thus, we sit at a critical crossroads between prematurely cutting rates and potentially reigniting inflation, or keeping conditions too tight, causing more economic pain than necessary.

Recall that Canadian inflation printed on the hotter side in November, with headline and core measures above 3%. The next inflation release, due out on January 17th could see inflation accelerate on the back of base-effects that saw weak inflation a year-ago. However, inflation is trending in the right direction, and we forecast it will durably break below the 3% level in 2024.

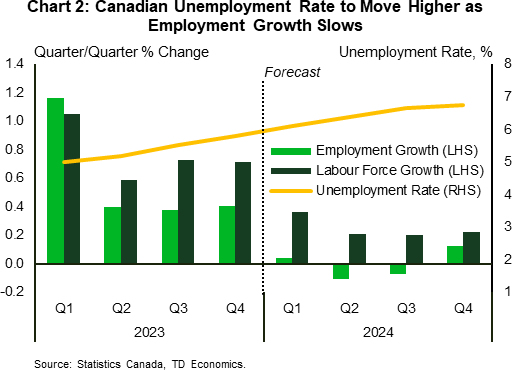

On the data front, Canadian employment was flat in December while the unemployment rate held steady at 5.8%. We are seeing signs that the job market is gradually losing momentum, but further cooling is needed to give the Bank of Canada comfort to pull the trigger on rate cuts. Over the year, we expect labour force growth to continue outpacing employment gains, pulling the unemployment rate higher from current levels (Chart 2). Meanwhile, job vacancies are declining across the country, although it is not occurring evenly across provinces, and wages remain elevated in the in 4-5% range.

Preliminary housing market data for the month of December pointed to strong sales activity and declining listings, tightening conditions in major markets. The greater-than-expected drop in yields, and subsequently mortgage rates, in the fourth quarter partially explains this uptick in activity. The BoC will be watching the housing market as seasonally strong spring homebuying will to fall directly in line with the expected timing of interest rate easing.

Summary 1/8 – 1/12

Monday, Jan 8, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | EUR | Germany Factory Orders M/M Nov | 1.10% | -3.70% |

| 07:00 | EUR | Germany Trade Balance (EUR) Nov | 17.9B | 17.8B |

| 07:30 | CHF | Real Retail Sales Y/Y Nov | 0.00% | -0.10% |

| 07:30 | CHF | CPI M/M Dec | -0.10% | -0.20% |

| 07:30 | CHF | CPI Y/Y Dec | 1.70% | 1.40% |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Jan | -15.4 | -16.8 |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Dec | 93.8 | |

| 10:00 | EUR | Eurozone Industrial Confidence Dec | -9.5 | |

| 10:00 | EUR | Eurozone Services Sentiment Dec | 4.9 | |

| 10:00 | EUR | Eurozone Consumer Confidence Dec F | -15.1 | -15.1 |

| 10:00 | EUR | Eurozone Retail Sales M/M Nov | -0.10% | 0.10% |

| 23:30 | JPY | Tokyo CPI Y/Y Dec | 2.60% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Dec | 2.10% | 2.30% |

| 23:30 | JPY | Tokyo CPI Core Y/Y Dec | 3.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | EUR | Germany Factory Orders M/M Nov | |

| Forecast: 1.10% | Previous: -3.70% | ||

| 07:00 | EUR | Germany Trade Balance (EUR) Nov | |

| Forecast: 17.9B | Previous: 17.8B | ||

| 07:30 | CHF | Real Retail Sales Y/Y Nov | |

| Forecast: 0.00% | Previous: -0.10% | ||

| 07:30 | CHF | CPI M/M Dec | |

| Forecast: -0.10% | Previous: -0.20% | ||

| 07:30 | CHF | CPI Y/Y Dec | |

| Forecast: 1.70% | Previous: 1.40% | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Jan | |

| Forecast: -15.4 | Previous: -16.8 | ||

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Dec | |

| Forecast: | Previous: 93.8 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Dec | |

| Forecast: | Previous: -9.5 | ||

| 10:00 | EUR | Eurozone Services Sentiment Dec | |

| Forecast: | Previous: 4.9 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Dec F | |

| Forecast: -15.1 | Previous: -15.1 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Nov | |

| Forecast: -0.10% | Previous: 0.10% | ||

| 23:30 | JPY | Tokyo CPI Y/Y Dec | |

| Forecast: | Previous: 2.60% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Dec | |

| Forecast: 2.10% | Previous: 2.30% | ||

| 23:30 | JPY | Tokyo CPI Core Y/Y Dec | |

| Forecast: | Previous: 3.60% | ||

Tuesday, Jan 9, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Nov | 1.20% | -0.20% |

| 00:30 | AUD | Building Permits M/M Nov | -2.00% | 7.50% |

| 06:45 | CHF | Unemployment Rate M/M Dec | 2.20% | 2.10% |

| 07:00 | EUR | Germany Industrial Production M/M Nov | 0.40% | -0.40% |

| 07:45 | EUR | France Trade Balance (EUR) Nov | -7.9B | -8.6B |

| 10:00 | EUR | Eurozone Unemployment Rate Nov | 6.50% | 6.50% |

| 11:00 | USD | NFIB Business Optimism Index Dec | 90.9 | 90.6 |

| 13:30 | USD | Trade Balance (USD) Nov | -64.8B | -64.3B |

| 13:30 | CAD | Trade Balance (CAD) Nov | 2.5B | 3.0B |

| 13:30 | CAD | Building Permits M/M Nov | 2.00% | 2.30% |

| 23:30 | JPY | Labor Cash Earnings Y/Y Nov | 1.50% | 1.50% |

| 23:30 | JPY | Overall Household Spending Y/Y Nov | -2.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Nov | |

| Forecast: 1.20% | Previous: -0.20% | ||

| 00:30 | AUD | Building Permits M/M Nov | |

| Forecast: -2.00% | Previous: 7.50% | ||

| 06:45 | CHF | Unemployment Rate M/M Dec | |

| Forecast: 2.20% | Previous: 2.10% | ||

| 07:00 | EUR | Germany Industrial Production M/M Nov | |

| Forecast: 0.40% | Previous: -0.40% | ||

| 07:45 | EUR | France Trade Balance (EUR) Nov | |

| Forecast: -7.9B | Previous: -8.6B | ||

| 10:00 | EUR | Eurozone Unemployment Rate Nov | |

| Forecast: 6.50% | Previous: 6.50% | ||

| 11:00 | USD | NFIB Business Optimism Index Dec | |

| Forecast: 90.9 | Previous: 90.6 | ||

| 13:30 | USD | Trade Balance (USD) Nov | |

| Forecast: -64.8B | Previous: -64.3B | ||

| 13:30 | CAD | Trade Balance (CAD) Nov | |

| Forecast: 2.5B | Previous: 3.0B | ||

| 13:30 | CAD | Building Permits M/M Nov | |

| Forecast: 2.00% | Previous: 2.30% | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Nov | |

| Forecast: 1.50% | Previous: 1.50% | ||

| 23:30 | JPY | Overall Household Spending Y/Y Nov | |

| Forecast: | Previous: -2.50% | ||

Wednesday, Jan 10, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Nov | 4.50% | 4.90% |

| 03:35 | JPY | 10-y Bond Auction | 0.70% | |

| 07:45 | EUR | France Industrial Output M/M Nov | 0.00% | -0.30% |

| 15:00 | USD | Wholesale Inventories Nov F | -0.20% | -0.20% |

| 15:30 | USD | Crude Oil Inventories | -5.5M | |

| 21:45 | NZD | Building Permits M/M Nov | 8.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Nov | |

| Forecast: 4.50% | Previous: 4.90% | ||

| 03:35 | JPY | 10-y Bond Auction | |

| Forecast: | Previous: 0.70% | ||

| 07:45 | EUR | France Industrial Output M/M Nov | |

| Forecast: 0.00% | Previous: -0.30% | ||

| 15:00 | USD | Wholesale Inventories Nov F | |

| Forecast: -0.20% | Previous: -0.20% | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -5.5M | ||

| 21:45 | NZD | Building Permits M/M Nov | |

| Forecast: | Previous: 8.70% | ||

Thursday, Jan 11, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Dec | 7.50B | 7.13B |

| 05:00 | JPY | Leading Economic Index Nov P | 107.9 | 108.9 |

| 09:00 | EUR | ECB Economic Bulletin | ||

| 13:30 | USD | Initial Jobless Claims (Jan 5) | 215K | 202K |

| 13:30 | USD | CPI M/M Dec | 0.20% | 0.10% |

| 13:30 | USD | CPI Y/Y Dec | 3.20% | 3.10% |

| 13:30 | USD | CPI Core M/M Dec | 0.20% | 0.30% |

| 13:30 | USD | CPI Core Y/Y Dec | 3.90% | 4.00% |

| 15:30 | USD | Natural Gas Storage | -14B | |

| 23:50 | JPY | Bank Lending Y/Y Dec | 2.70% | 2.80% |

| 23:50 | JPY | Current Account (JPY) Nov | 2.18T | 2.62T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Dec | |

| Forecast: 7.50B | Previous: 7.13B | ||

| 05:00 | JPY | Leading Economic Index Nov P | |

| Forecast: 107.9 | Previous: 108.9 | ||

| 09:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 13:30 | USD | Initial Jobless Claims (Jan 5) | |

| Forecast: 215K | Previous: 202K | ||

| 13:30 | USD | CPI M/M Dec | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 13:30 | USD | CPI Y/Y Dec | |

| Forecast: 3.20% | Previous: 3.10% | ||

| 13:30 | USD | CPI Core M/M Dec | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 13:30 | USD | CPI Core Y/Y Dec | |

| Forecast: 3.90% | Previous: 4.00% | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -14B | ||

| 23:50 | JPY | Bank Lending Y/Y Dec | |

| Forecast: 2.70% | Previous: 2.80% | ||

| 23:50 | JPY | Current Account (JPY) Nov | |

| Forecast: 2.18T | Previous: 2.62T | ||

Friday, Jan 12, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

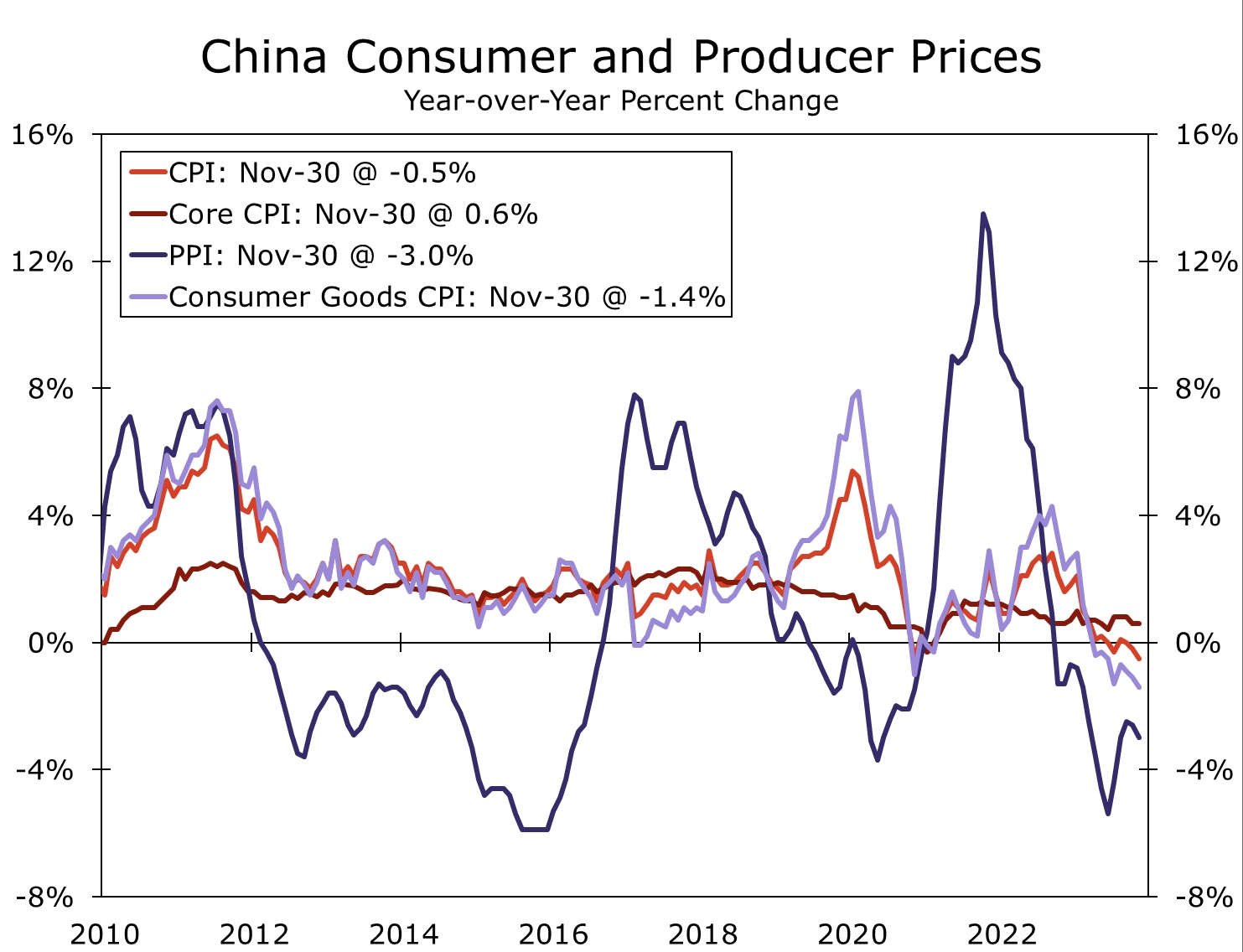

| 01:30 | CNY | CPI Y/Y Dec | -0.40% | -0.50% |

| 01:30 | CNY | PPI Y/Y Dec | -2.50% | -3.00% |

| 05:00 | JPY | Eco Watchers Survey: Current Dec | 49.9 | 49.5 |

| 07:00 | GBP | GDP M/M Nov | 0.20% | -0.30% |

| 07:00 | GBP | Industrial Production M/M Nov | 0.10% | -0.80% |

| 07:00 | GBP | Manufacturing Production Y/Y Nov | 0.80% | |

| 07:00 | GBP | Manufacturing Production M/M Nov | 0.30% | -1.10% |

| 07:00 | GBP | Industrial Production Y/Y Nov | 0.70% | 0.40% |

| 07:00 | GBP | Goods Trade Balance (GBP) Nov | -15.7B | -17.0B |

| 07:45 | EUR | France Consumer Spending M/M Nov | 0.00% | -0.90% |

| 13:00 | GBP | NIESR GDP Estimate (3M) Dec | -0.10% | |

| 13:30 | USD | PPI M/M Dec | 0.10% | 0.00% |

| 13:30 | USD | PPI Y/Y Dec | 1.30% | 0.90% |

| 13:30 | USD | PPI Core M/M Dec | 0.20% | 0.00% |

| 13:30 | USD | PPI Core Y/Y Dec | 2.00% | 2.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | CNY | CPI Y/Y Dec | |

| Forecast: -0.40% | Previous: -0.50% | ||

| 01:30 | CNY | PPI Y/Y Dec | |

| Forecast: -2.50% | Previous: -3.00% | ||

| 05:00 | JPY | Eco Watchers Survey: Current Dec | |

| Forecast: 49.9 | Previous: 49.5 | ||

| 07:00 | GBP | GDP M/M Nov | |

| Forecast: 0.20% | Previous: -0.30% | ||

| 07:00 | GBP | Industrial Production M/M Nov | |

| Forecast: 0.10% | Previous: -0.80% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Nov | |

| Forecast: | Previous: 0.80% | ||

| 07:00 | GBP | Manufacturing Production M/M Nov | |

| Forecast: 0.30% | Previous: -1.10% | ||

| 07:00 | GBP | Industrial Production Y/Y Nov | |

| Forecast: 0.70% | Previous: 0.40% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Nov | |

| Forecast: -15.7B | Previous: -17.0B | ||

| 07:45 | EUR | France Consumer Spending M/M Nov | |

| Forecast: 0.00% | Previous: -0.90% | ||

| 13:00 | GBP | NIESR GDP Estimate (3M) Dec | |

| Forecast: | Previous: -0.10% | ||

| 13:30 | USD | PPI M/M Dec | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 13:30 | USD | PPI Y/Y Dec | |

| Forecast: 1.30% | Previous: 0.90% | ||

| 13:30 | USD | PPI Core M/M Dec | |

| Forecast: 0.20% | Previous: 0.00% | ||

| 13:30 | USD | PPI Core Y/Y Dec | |

| Forecast: 2.00% | Previous: 2.00% | ||

China’s Rise To The World’s Largest Economy Is Delayed

Summary

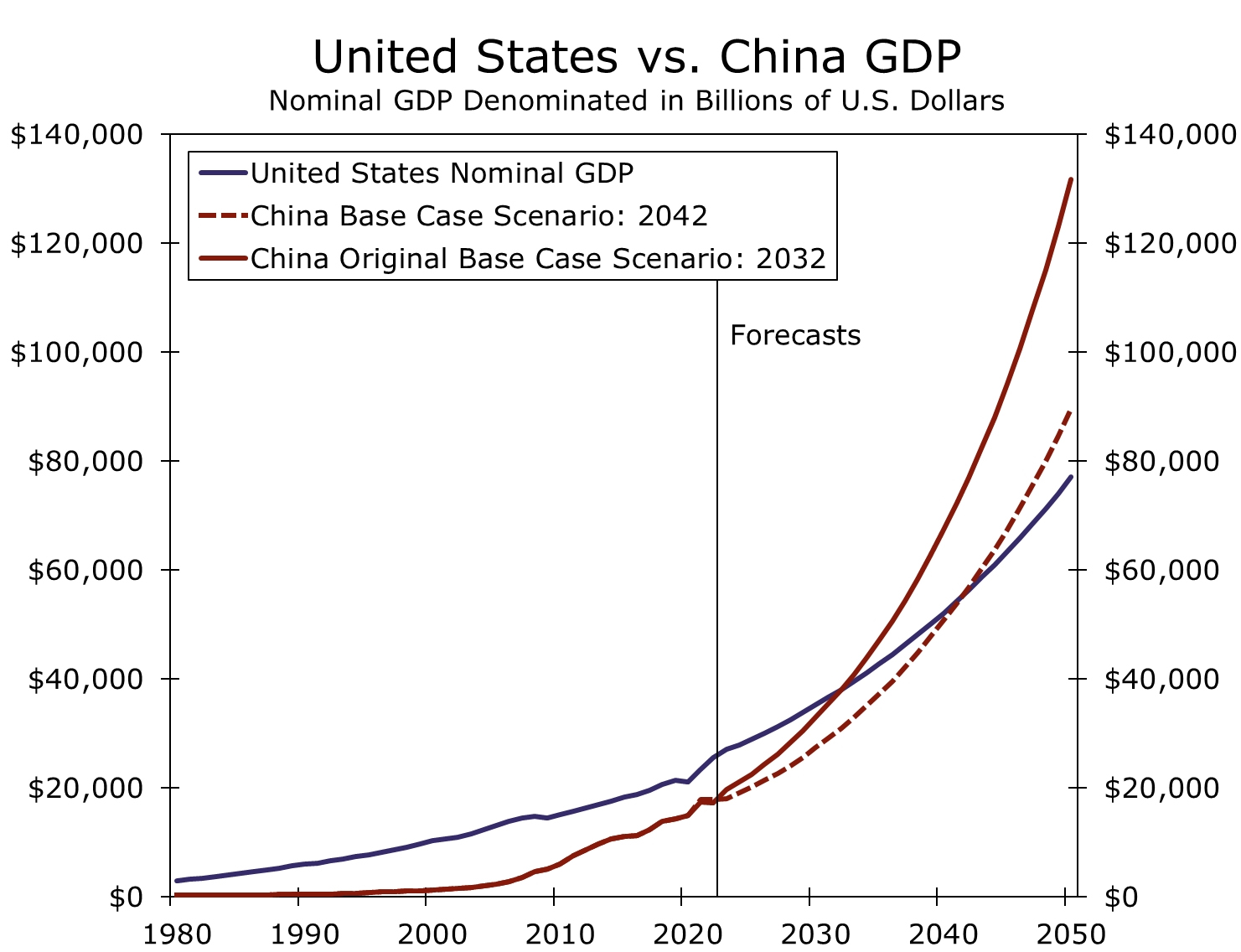

The U.S. economy remains the largest economy in the world. But, will the U.S. be able to maintain that status forever? In our view, the answer is no. We believe China is on a path to eventually overtake the U.S. and become the world's largest economy. However, China's structural challenges and vulnerabilities combined with tense geopolitical relations are taking a greater toll on the economy than we previously expected and earlier than originally anticipated. So, while China's rise to the world's largest economy is inevitable, reaching the top of the economic throne will likely take longer than we previously estimated.

China's Rise To The World's Largest Economy Is Delayed

Over the years, we have expressed a pessimistic outlook toward China's economy in multiple forums. Most recently, we highlighted the challenges that China faces in our 2024 International Economic Outlook publication. Our 2024 outlook mentions the fact that China has severe demographic problems, specifically a shrinking overall population as well as a dwindling labor force. In addition, we commented on how China's ongoing real estate crisis, deflation, elevated corporate sector debt and softening consumer demand are likely to contribute to a sharp slowdown in growth prospects. Tack on an unclear outlook for the overall direction of economic policy as well as geopolitical tensions that has China being removed from global supply chains and the country being questioned as an investment destination, and China's growth outlook is not particularly robust. In our view, the days of double-digit real GDP growth—even annual growth of 6%—are likely in the past. We do, however, believe China's economy will continue to grow at a faster pace than the United States, both in nominal and real terms, going forward. Which is why we continue to believe China will ultimately overtake the U.S. and at some point become the largest economy in the world. With that said, these structural issues are taking a bigger toll on China's economy than we previously expected, and that impact is materializing perhaps earlier than we initially thought. At the beginning of 2022, we published a report suggesting China could become the world's largest economy in 2032. Under a set of economic and FX views as well as longer-term assumptions, we believed China would ascend to the largest economy in the world in ten years as nominal GDP growth would outpace the U.S. well into the next decade. However, the way China's economy and financial markets have evolved, as well as the evolution of geopolitical trends, in our view mean that China's rise to the economic throne will likely be delayed. In fact, under our forecasts and assumptions for both China and the United States, we still believe China will overtake the U.S.; however, rather than the ascension taking place in 2032, our new estimate is 2042,10 years later than our original timeline.

Our revised estimate is rooted in a Chinese economy that has underperformed even relative to our already pessimistic outlook. Over the last few years, China has been plagued by a number of developments that has pushed out the timeline for challenging the U.S. in economic size. These developments include a short-lived post “Zero-COVID” rebound in activity, a weaker renminbi than we previously forecast, worsening geopolitical relations due to exogenous military conflicts in Europe and the Middle East, and structural imbalances that have intensified more than expected. In addition, and perhaps a consequence of those developments, inflation has fallen rapidly to the point that China is currently experiencing deflation (Figure 1). As of November, CPI is -0.5% year-over-year, well below China's long-run average inflation rate of around 2%. Deflation is arguably one of the primary drivers, in addition to a U.S. economy that has outperformed recently, why China will now take an additional decade to become the world's largest economy. Not only can deflation place additional pressure on already sluggish consumer spending and contribute to softer activity, but deflation will contribute to lower nominal GDP growth. Going forward, we believe China's economy will continue to decelerate and inflation will remain rather subdued. We expect many of China's structural issues and tail-risks to remain in place (i.e. a real estate induced financial crisis, invasion of Taiwan etc.); however, our base case scenario for China does not include a large-scale crisis unfolding. Rather, we believe Chinese authorities will pursue policies consistent with supporting the economy over the next few years, although more accommodative policy will, in our view, do little to change the direction of China's economy or alter underlying trends. As a result of shifting to more accommodative policy, we assume authorities will further pause its deleveraging campaign. Leverage has historically been a growth mechanism for China's economy; however, with the local real estate sector under pressure, we have our doubts deploying fiscal resources toward property development will yield more than only marginal benefits. We also assume the impact of an aging population and diminishing workforce will continue to weigh on growth prospects, while China slowly being removed from the global marketplace will disrupt China's current export driven economic model. Periods of deflation and subdued inflation, as well as high household saving rates, are also likely to keep consumer spending subdued and contribute to slower growth.

Under these assumptions, we forecast China's economy to grow 5.2% in 2023, 4.5% in 2024 and 4.3% in 2025. On the inflation side, we believe the CPI will rise 0.4% in 2023, 1.5% in 2024 and 1.8% in 2025. Combining our GDP and CPI forecasts, we expect China's economy to experience nominal GDP growth of ~5.5%-6% through the end of 2025. Relative to our initial estimate of when China could overtake the U.S. economy, our short-term nominal GDP forecasts have been revised lower to reflect a worsening of structural economic challenges and intensifying downside risks. Longer-term, we believe structural issues will remain intact and nominal GDP growth will slow. From 2026-2030 we assume average nominal GDP growth of 5.8% (4% real GDP growth & 1.8% rise in CPI). Over the course of the 2030s, we assume average nominal GDP growth of 5.3% (3.5% real GDP growth and 1.8% rise in CPI) and 4.8% nominal growth in the 2050s (3% real GDP growth and 1.8% rise in CPI). Our longer-term growth and inflation assumptions have also been revised lower as economic trends and vulnerabilities have worsened. As far as the United States, the U.S. economy was able to avoid recession in 2023 despite high inflation and elevated interest rates. The resiliency of the U.S. economy also contributes to China becoming the world's largest economy a decade later than our prior estimate. Going forward, our U.S. economists forecast the U.S. economy to expand at a nominal GDP growth rate of 6.2% in 2023, 3.1% in 2024 and 3.6% in 2025. Our colleagues also estimate that average nominal GDP growth for the U.S. economy is likely to be 4% over the long-term. Using these forecasts and long-run estimates for growth and inflation, China's nominal GDP could rise to a little over RMB296T by 2042. United States nominal GDP could rise to $56.5T by the same year.

But, in order to make a fair comparison of nominal GDP levels, China's nominal GDP must be converted into U.S. dollars. Exchange rate assumptions and the path of the renminbi can play a pivotal role in determining when, or if, China overtakes the United States. In our view, the Chinese renminbi is likely to strengthen over the next few decades. We believe authorities will gradually lift capital controls and play a reduced role in FX markets in an effort to have the renminbi gather momentum as a reserve currency and take a larger role in the global marketplace. In order for the renminbi to become more widely used, the currency will need to become market driven rather than influenced by the People's Bank of China and other local authorities. Most currency valuation methodologies indicate the renminbi is undervalued, likely due to capital controls and other regulations. Should controls and restrictions be lifted over time, the renminbi could strengthen toward “fair value” and facilitate China becoming the world's largest economy. Incorporating our long-term RMB view, as well as our GDP and inflation assumptions, China's nominal GDP, converted into U.S. dollars, could rise to a little over $57.5T by 2042, leaving China as the world's largest economy in a little less than 20 years—a more gradual ascent than the 10-year horizon we previously envisaged (Figure 2).

U.S. Inflation Data in Focus as Central Banks Consider Rate Cuts

U.S. inflation numbers will be front and center for the Fed as discussions among policymakers shift from how high to push interest rates to when the first cuts might be appropriate.

We look for U.S. CPI growth to show further signs of moderation in December, notwithstanding a likely tick higher in the year-over-year rate of headline price growth to 3.2% from 3.1% a month earlier. That small increase should be entirely explained by a smaller year-over-year decline in energy prices – gasoline prices were little changed in December from November (on a seasonally adjusted basis) but a large monthly decline a year ago will fall out of the year-over-year calculation.

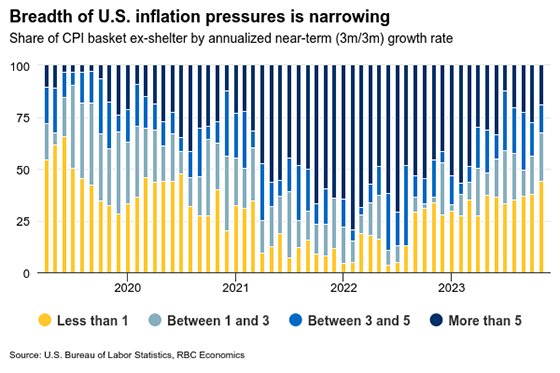

Food price growth likely continued to edge lower and we look for signs of a narrowing breadth of remaining inflation pressures in recent months to persist. We expect year-over-year price growth in core (excluding food and energy) products to slow to 3.8% from 4.0% on a more ‘normal’ looking 0.2% monthly (seasonally adjusted) increase from November. Home rent price growth is accounting for a disproportionate share of gains in core prices – roughly 70% of the year-over-year increase as of November by our count – and will continue to slow as moderation in growth in market rents passes through with a lag as leases are renewed. Excluding shelter costs, the share of goods and services in the U.S. CPI basket seeing inflation at above a 3% rate shrunk to 32% over the three months to November – a share broadly in line with pre-pandemic levels.

The Fed remains focused on getting inflation under control but sent a clear message in December that rate cuts are also coming into view. Indeed, with price growth trending in the right direction and signs that economic growth is slowing, the Fed is widely expected to pivot to interest rate cuts in the first half of this year. Our own forecast assuming the first decrease comes in Q2.

Week ahead data watch

We expect the Canadian trade surplus to shrink to $2.5 billion in November after ballooning to $3 billion in October. A 10% drop in oil prices in November will have lowered the value of exports more than imports.

Week Ahead – Market Spotlight Turns to US CPI Inflation

- US CPI inflation is the next big test for the US dollar

- Yen traders turn to Tokyo CPIs and wages for BoJ exit hints

- China’s inflation and trade numbers to impact broader sentiment

- UK monthly GDP on tap amid recession fears

Will the US CPIs corroborate the market’s implied Fed rate path?

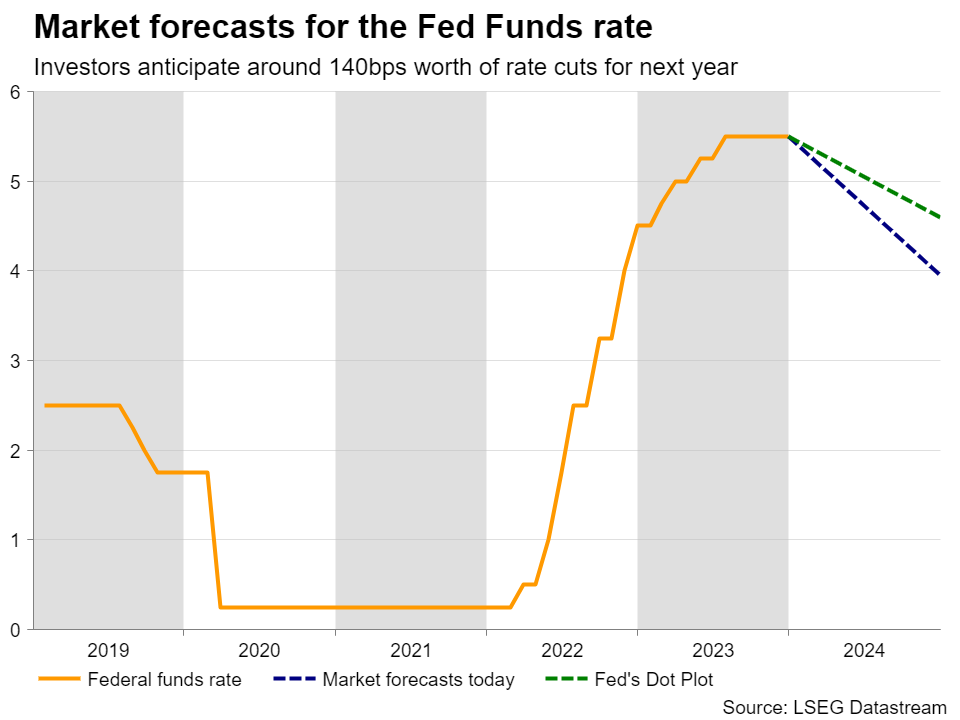

The US dollar staged a decent recovery during the first week of the year, with market participants scaling back some basis points worth of rate reductions expected by December, although the total number of rate cuts anticipated by investors is still way larger than the amount of rate cuts indicated by the Fed’s December dot plot.

At that gathering, the median dot for 2024 was revised down to 4.6% from 5.1% and Fed Chair Jerome Powell appeared more dovish than anticipated at the press conference following the decision. He said that rate increases are not the base case anymore and that the question now is “when will it become appropriate to begin dialing back?”

With that in mind, at some point last week, investors were nearly fully convinced that a 25bps cut will be delivered in March and that interest rates should be lowered by 160bps by December. Now that number stands at around 140 and the probability of a March cut is down to around 70%.

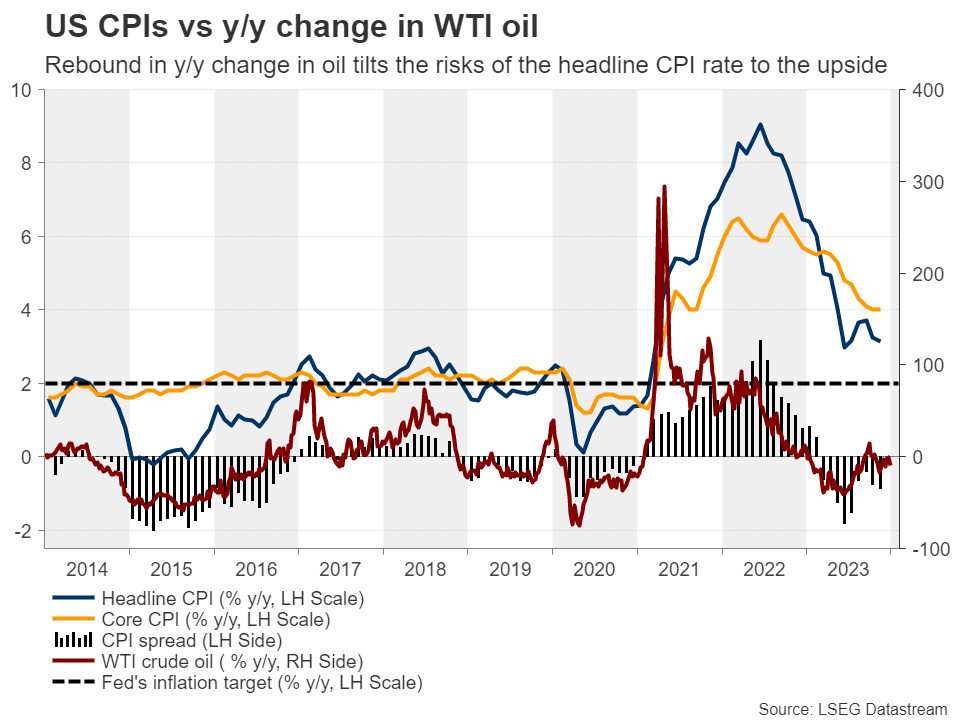

Next week, investors will stay locked in front of their screens in anticipation of the US CPI numbers for December, due out on Thursday. Inflation has come down quickly in recent months due to weaker goods prices and moderating costs of services, including travel, even as rent increases remained elevated. Headline inflation saw a faster slowdown than underlying price pressures as energy prices began drifting south in September, erasing nearly all the gains posted during the summer months.

However, with the 2022 downtrend now dropping out of the year-on-year calculation, oil prices are close to their opening levels for 2023, which means that the y/y change has moved from well into negative territory close to zero. And with the headline CPI rate resting well below the core one, even if the latter softens a bit more, this means that there are risks for a rebound in headline inflation.

Should this be the case, investors may further reconsider whether March is the appropriate time for a first rate reduction by the Fed, lowering the probability for that happening even further and scaling back more basis points worth of cuts for the whole year. Consequently, the US dollar could extend its recovery as Treasury yields edge higher.

When will the BoJ take rates out of negative territory?

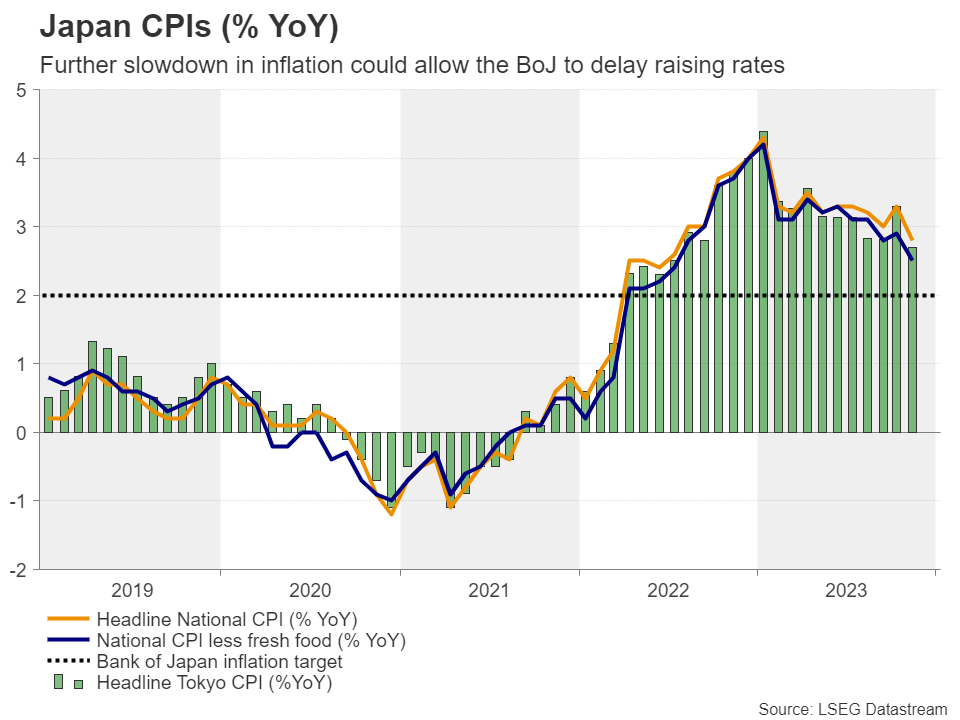

Japan’s Tokyo CPI and wage data, due out on Tuesday and Wednesday respectively, may also attract special attention next week. At its December gathering, this Bank decided unanimously to keep interest rates untouched at -0.1% and to stick to its yield curve control policy framework that places an upper bound of 1% for the 10-year Japanese government bond yield as reference.

With the Bank giving no signals that the era of ultra-loose policy conditions is nearing its end, next week’s releases can very well upset opinions on that front. The Tokyo CPI data for November revealed notable slowdowns in both headline and core consumer prices, with the latter rate hitting 2.3% y/y, slightly above the Bank’s objective of 2%. Therefore, further cooling could point to a similar reaction in the national CPI data for the month and may suggest that Japanese policymakers are not in a rush to take interest rates out of negative territory, thereby further hurting the recently wounded yen.

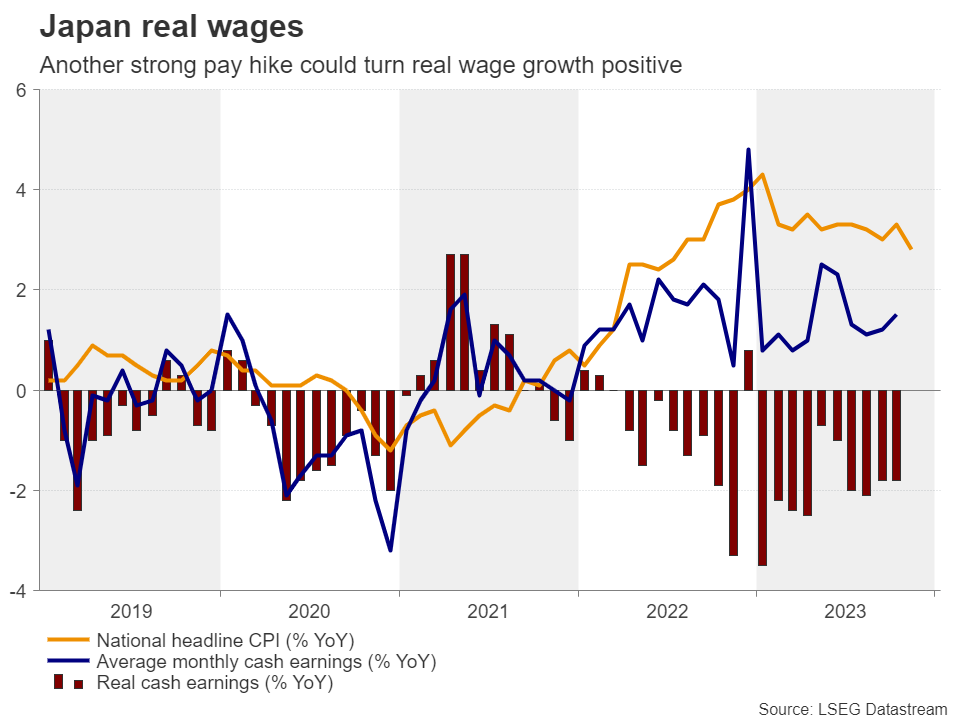

As for wages, they have accelerated to 1.5% y/y in October from 0.6%, but even if next week’s data reveals that the positive trend continued in November, the Bank may prefer to wait for the outcome of the spring wage negotiations before ending the negative-rate era. In October, Japan’s umbrella labor union, Rengo, said that they will demand hikes of at least 5%, which could take real wage growth into positive territory. Therefore, April seems a better choice for the BoJ to raise interest rates.

Considering that the market expects the Fed to cut interest rates by around 140bps next year, this may allow the yen to stay in an uptrend mode against its US counterpart, even if the latest slide continues for a while longer.

Will the outlook for the Chinese economy get gloomier?

With China’s official manufacturing PMI for December signaling contraction for the third straight month, investors who are concerned about the state of the world’s second largest economy may now turn their attention to China’s CPI and trade data for the last month of 2023. In November, China slipped further into deflation and although its exports improved, its imports slowed notably, suggesting weak demand.

Therefore, should this week’s data corroborate the gloomy outlook, risk aversion may intensify and pressure on Chinese authorities to adopt bolder stimulus measures may grow. With Australia and New Zealand being China’s main trading partners, aussie and kiwi may also correct lower. That said, a bearish reversal in those currencies may be premature as the market is currently anticipating fewer basis points worth of rate reductions by the RBA and the RBNZ than the Fed. Australia’s monthly CPI for November is also due to be released on Wednesday.

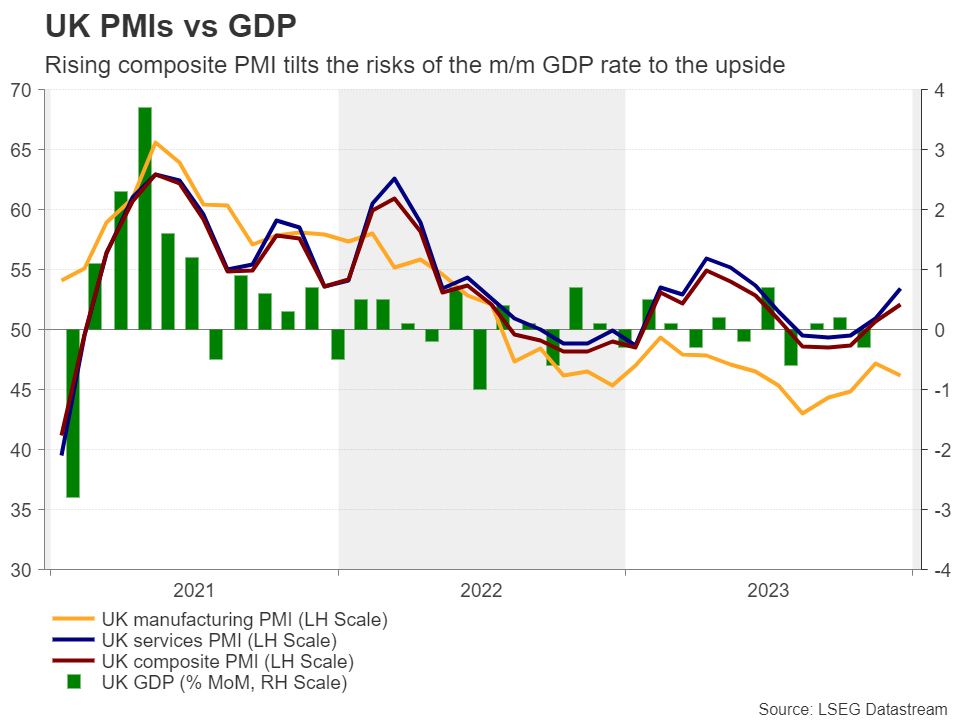

Is the UK heading for a recession?

The UK agenda was very light during the first week of the new year, but there are some items for pound traders to consider next week. The monthly GDP rate for November is due to be released on Friday alongside the industrial and manufacturing production prints for the same month.

In October, the UK economy contracted 0.3% m/m, while the quarterly rate for Q3 was revised to -0.1%, thereby ringing the recession alarm bells. Taking that into account, investors have added to their BoE rate cut bets, currently penciling in around 125bps worth of reductions by the end of the year, despite Governor Bailey and his colleagues sticking to their “higher for longer” mantra when they last met.

Thus, should the November data suggest that the economy continued performing poorly during the last quarter of the year, market participants could sell some pounds on speculation that the BoE may indeed start lowering borrowing costs sooner than it currently believes. Nonetheless, considering the rising composite PMI for that month, the risks surrounding the monthly GDP rate may be tilted to the upside.

Weekly Focus – Rates Will Be Cut – But How Much and How Soon?

The strong decline in US and European bond yields continued in the second half of December, as market expectations firmed for rapid and large interest rate cuts from central banks in 2024. This followed from dovish signals from the Fed earlier in December and signs that inflation is under control, and despite what seems to be attempts by some central bankers to moderate the expectations. In the first week of the new year, however, markets have moved a bit in the opposite direction, perhaps reflecting that the decline in bond yields and the accompanying increase in equity prices by themselves might stimulate economists so much that inflation rises. Our view continues to be that markets are pricing more rate cuts than are likely in 2024 in the US and the euro area, as we expect central banks to be cautious. Risks of inflation re-igniting are not gone, given tight labour markets and areas of high wage growth, for example. Our forecast is 100bp of rate cuts in the US this year beginning in March, and 75bp from the ECB beginning in June.

The US added 216,000 jobs in December and hourly earnings grew 0.4%, both above expectations. Job growth in November was revised down, but all in all, most data points towards a still-strong US labour market. Euro area inflation was 2.9% y/y in December as expected, up from 2.4% in November. The increase is mostly related to a lower comparison point for energy prices. The underlying momentum in core prices (measured as last three months compared to previous three months) is still declining and corresponds to 1.4% annual core inflation in the latest data, using ECB's seasonal adjustments. However, service price momentum is at 2.3%, which is likely still a worry for the ECB. PMI data from the US, Europe and Asia mostly suggest that the global manufacturing recession is coming to an end, and some leading indicators even suggest that we might be in for a modest manufacturing upswing.

One inflation risk factor continues to be conflict in the Middle East, where Houthi forces from Yemen have been attacking ships in the Red Sea. This has caused many shipping companies to send their ships around the Cape of Good Hope instead of through the Suez Canal, leading to significant increases in freight rates and shipping times. However, rates remain far below the heights seen in 2022, and we continue to see supply disruptions as much less of an inflation threat now than when excessive global demand strained supply chains to their outmost. Oil markets remain calm despite the risk that hostilities can escalate further, but of course, this could change.

The most important data release during the coming week will likely be the US CPI for December. Monthly core inflation was 0.3% in November and that is also our expectation for this release, still a bit to the high side for the Fed. Euro area unemployment is also interesting given the ECB's high degree of focus on the tight labour market, but indicators do not suggest that it increased in November from 6.5% level the month before. China will likely release another negative inflation print but with core inflation still positive, albeit low. We expect 2024 to be the year when Japan finally exits negative interest rates and that depends on price and wage growth, both of which we get data for this week. However, we will likely have to wait for the spring negotiations before seeing wages move much higher.

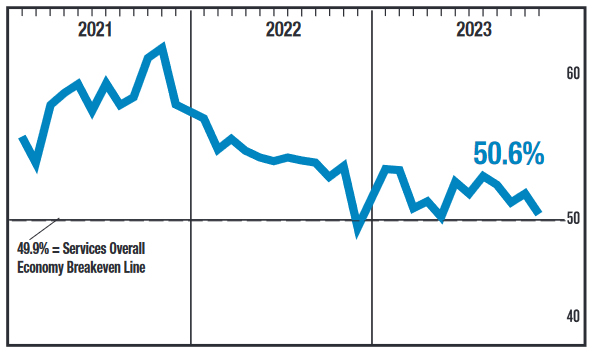

US ISM services falls sharply to 50.6, vs exp 52.7

US ISM Services PMI fell from 52.7 to 50.6 in December, below expectation of 52.7. Business activity/production rose from 55.1 to 56.6. New orders fell from 55.5 to 52.8. Employment fell sharply from 50.7 to 43.3. Prices ticked down from 58.3 to 57.3.

The past relationship between the Services PMI and the overall economy indicates that the Services PMI for December (50.6 percent) corresponds to a 0.3-percent increase in real gross domestic product (GDP) on an annualized basis.