Sample Category Title

USDCAD Marks Bullish Wave in Short-Term

- USDCAD meets 20-day SMA

- Technical signals mixed; downtrend well intact

USDCAD has been rising since the end of 2023 after the bounce off the 1.3175 support level and is currently reaching the short-term 20-day simple moving average (SMA) near 1.3373, but is still developing beneath the descending trend line.

The MACD and the RSI are confirming the bullish move in the market as the first one is holding above its trigger line, and the latter is pointing marginally up near the neutral threshold of 50. However, the stochastic oscillator is suggesting an overstretched market and is ticking lower above the 80 level, indicating a potential downside correction.

To attract new buyers, the bulls will have to surpass the nearby resistance of the 20-day SMA at 1.3373 and move beyond the 1.3415 barrier. In this case, the price could pick up steam towards the important falling trend line and the 200-day SMA around 1.3480. Another successful battle there could see the price jumping into the 50-day SMA at 1.3570.

Hence, a downside correction could still be possible in the coming sessions. If the pair slumps below the five-month low of 1.3175 it could stabilize near the 1.3150 support. Otherwise, the sell-off could expand towards the 1.3090 territory.

To sum up, USDCAD has not eliminated downside risks yet, despite marking a positive wave. To boost buying confidence, the pair will need to crawl above 1.3480.

Gold Price Corrects Gains While Crude Oil Price Aims Higher

Gold price is correcting lower from the $2,088 resistance. Crude oil price is rising and it could climb further higher toward the $75.90 resistance.

Important Takeaways for Gold and Oil Prices Analysis Today

- Gold price failed to clear the $2,088 resistance and corrected lower against the US Dollar.

- A key contracting triangle is forming with support at $2,042 on the hourly chart of gold at FXOpen.

- Crude oil prices are moving higher above the $71.00 resistance zone.

- There is a key bullish trend line forming with support near $72.60 on the hourly chart of XTI/USD at FXOpen.

Gold Price Technical Analysis

On the hourly chart of Gold at FXOpen, the price was able to climb above the $2,050 resistance. The price even broke the $2,078 level before the bears appeared.

The price traded as high as $2,088 before there was a downside correction. There was a move below the $2,060 pivot zone. The price settled below the 50-hour simple moving average and RSI dipped below 50. Finally, it tested the $2,030 zone.

The price is now attempting a recovery wave above the $2,040 level. It climbed above the 23.6% Fib retracement level of the downward move from the $2,078 swing high to the $2,030 low.

If the bulls remain active, the price could start a fresh increase. Immediate resistance is near the 50-hour simple moving average at $2,046. The next major resistance is near the 50% Fib retracement level of the downward move from the $2,078 swing high to the $2,030 low at $2,055.

An upside break above the $2,055 resistance could send Gold price toward $2,078. Any more gains may perhaps set the pace for an increase toward the $2,088 level.

Initial support on the downside is near the $2,042 level. There is also a key contracting triangle forming with support at $2,042. The first major support is $2,030. If there is a downside break below $2,030, the price might decline further. In the stated case, the price might drop toward $2,010.

Oil Price Technical Analysis

On the hourly chart of WTI Crude Oil at FXOpen, the price started a decent increase against the US Dollar. The price gained bullish momentum after it broke the $71.00 resistance as mentioned in the previous analysis.

There was a sustained upward move above the $71.50 and $72.20 levels. The bulls pushed the price above the 50% Fib retracement level of the recent drop from the $74.02 swing high to the $71.14 low.

It is now trading above the 50-hour simple moving average and the RSI is rising toward 65. Immediate resistance is near the 76.4% Fib retracement level of the recent drop from the $74.02 swing high to the $71.14 low at $73.35.

If the price climbs further higher, it could face resistance near $74.00. The next major resistance is near the $75.90 level. Any more gains might send the price toward the $78.00 level.

Conversely, the price might correct gains and retest the 50-hour simple moving average and a connecting bullish trend line at $72.60. The next major support on the WTI crude oil chart is near $71.00.

If there is a downside break, the price might decline toward $69.40. Any more losses may perhaps open the doors for a move toward the $68.00 support zone.

USD/JPY Technical: Countertrend USD Rebound Remains Intact Ahead of US NFP

- The US dollar is the top performer against the JPY on a 5-day rolling basis (+3%).

- A monthly US NFP jobs gain of between +240K to +260K may ignite another bout of US dollar rally.

- Bullish momentum is supporting a potential extension of the ongoing countertrend rebound in USD/JPY.

- Watch the next intermediate resistance at 146.70/147.45

The USD/JPY has staged the expected countertrend corrective rebound from its 5-month low of 140.25 printed on 28 December 2023. It has rallied by +470 pips/+3.35% to hit a current intraday high of 145.37 today, 5 January Asian session at this time of the writing (see Fig 1).

Revival of short-term US dollar strength

So far, the US dollar has been on a bullish beat since the start of the new year and the USD/JPY is the top performer with a rolling 5-day return of +3% over the USD/AUD (+1.7%), USD/CHF (+1.2%), USD/EUR (+1%), and USD/GBP (+0.5%) ahead of today’s US non-farm payrolls (NFP) jobs data release where the consensus has pencilled in a lower number of +170K jobs added for December 2023 over the prior November’s print of +199K.

The persistent US dollar weakness seen throughout Q4 2023 has been driven by rising expectations on the US Federal Reserve’s dovish pivot to kick start its accommodating monetary policy in 2024 with six cuts on its Fed funds rate being priced in by the interest rate futures market according to the CME FedWatch tool.

+240K to +260K for December NFP may ignite further US dollar strength

Hence, if today’s NFP number shows a higher number of jobs added in December in a range of +240K to +260K that is above the prior 12 months’ average of around +240K monthly gain, the current dovish optimism on the Fed to enact the expected six interest rates cuts is likely to be tapered downwards as the US job market is not in the doldrums which in turn may see a continuation of the current bout of US dollar strength.

Bullish momentum remains intact

Fig 2: USD/JPY medium-term trend as of 5 Jan 2024 (Source: TradingView, click to enlarge chart)

Fig 3: USD/JPY short-term minor trend as of 5 Jan 2023 (Source: TradingView, click to enlarge chart

The prior three-day rally seen in the USD/JPY is not showing any clear signs of fatigue as its price actions have just surpassed the 20 and 200-day moving averages.

In addition, the hourly RSI momentum indicator has continued to trace out a series of “higher lows” above the 50 level which suggests short-term upside momentum remains intact.

If the 143.75 key short-term pivotal support manages to hold, the USD/JPY may continue its current countertrend corrective rebound leg to see the next intermediate resistances coming in at 146.70 and 147.45 (also the downward sloping 50-day moving average & 61.8% Fibonacci retracement of the medium-term downtrend from 13 November 2023 high to 28 December 2023 low).

However, failure to hold at 143.75 negates the bullish tone to expose the next intermediate support at 142.20 in the first step.

Main Dish Will Be December Payrolls and Services ISM

Markets

Yesterday’s market reaction to EMU and US eco data suggests that the bottom below core bond yields is becoming firmer after the significant November/December correction. Energy-related base effects and travel-related services costs caused a new uptick in national German/French inflation data, though in line with forecasts. Monthly price momentum was even softer than feared. Exactly the same figures would have evoked a bond rally last month around, but had the opposite effect yesterday. German yields added 7.2 bps (30-yr) to 11.9 bps (5-yr). The German 10-yr yield bounced off the 2% mark and is trying to escape the steep downward trend channel in place since December. Success in today’s close (>2.16%) would call off the correction and turn the technical picture more neutral short term with first real resistance situated around 2.32% (38% retracement on October to December yield decline). Aggregate EMU inflation figures are expected to clock at 0.2% M/M and 2.9% Y/Y (from 2.4%) for the headline reading while core inflation is set to slow from 3.6% Y/Y to 3.4% Y/Y. Deviations to consensus should be small after national outcomes. Anything bar a major downside surprise could keep Bunds on the backfoot. The main dish will be served at the start of US dealings with December payrolls and services ISM. Yesterday’s consensus-beating labour market data extended the bond sell-off which started in Europe. US yields closed 5.4 bps (2-yr) to 8.3 bps (10-yr) higher. The US 10-yr yield regained the psychologic 4% mark and similarly tries to escape the downward corrective channel in place since the November Fed meeting. 38% retracement on the autumn 2023 downleg is located at 4.25%. As for European inflation, we think that the natural drift higher in yields since year-end could stay in place unless we see big data misses. Such scenario could help the dollar’s recovery. Especially if risk sentiment suffers from the recovery in bond yields. Key US benchmarks yesterday lost up to 0.5% for Nasdaq following steeper losses earlies this week. First support stands at EUR/USD 1.0893 (YTD/low) to 1.0875 (38% retracement on October/December rally). Comments by central bankers are wildcards for trading. If any, we think they will push back on (too) aggressive market pricing of 150 bps cumulative rate cuts this year.

News & Views

Data published by the Czech Finance Ministry yesterday showed that the Czech Budget deficit for 2023 declined 20% to CZK 288.5bn. This was below the budget target of CZK 295bn. The reduction in the deficit occurred as income was up 17% while overall expenditure rose 11% Y/Y. The rise in spending was mainly driven by higher pension costs and support to mitigate the cost of higher energy prices. Debt servicing costs also rose. On the income side, the government last year implemented a windfall tax on energy companies and banks. According to Finance Minister Stanjura, the government will make on new assessment on the windfall tax in spring. The Finance Minister expects the 2023 fiscal deficit to be below 3.6%. The Government debt to GDP ratio is seen at 42.3%. For 2024, the government aims to reduce the budget deficit to 2.2%. In communication with the press during a visit in Nottinghamshire, UK PM Sunak indicated that his working assumption is for the UK Parliamentary elections to be held in the autumn of this year. The legal deadline is for the elections to be held in January 2025 at the latest. The opposition (Labour and the Liberal Democrats) called the government to hold election in May, but with the PM’s party lagging Labour by a huge margin of about 20% in the opinion polls, such a scenario looks unlikely. The government will propose a spring budget early March, which is expected to include measures to make progress in the five pledges the UK PM set out a year ago: halving inflation, growing the economy, stopping migrants entering in small boats, cutting NHS waiting lists and reducing national debt. Only the first of this five targets has been fulfilled as inflation dropped to 3.9% in November after reaching a peak of 11.1% in October 2022.

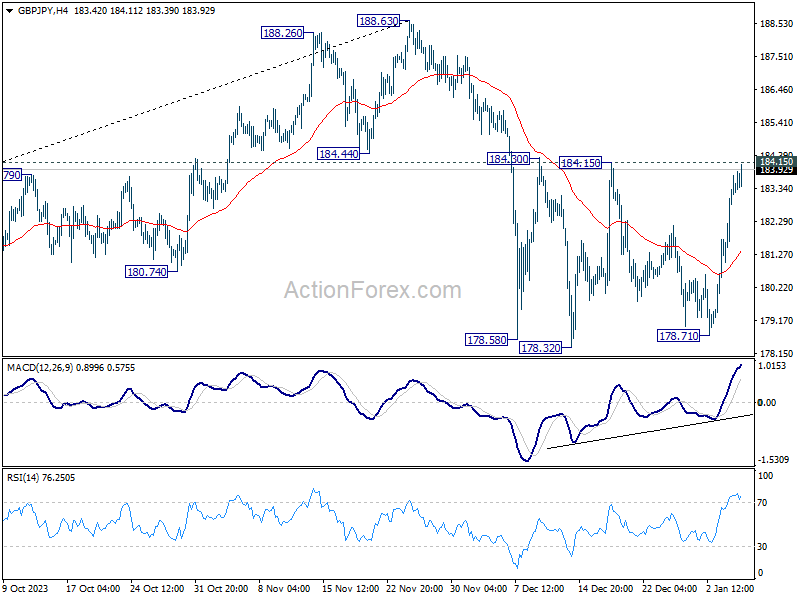

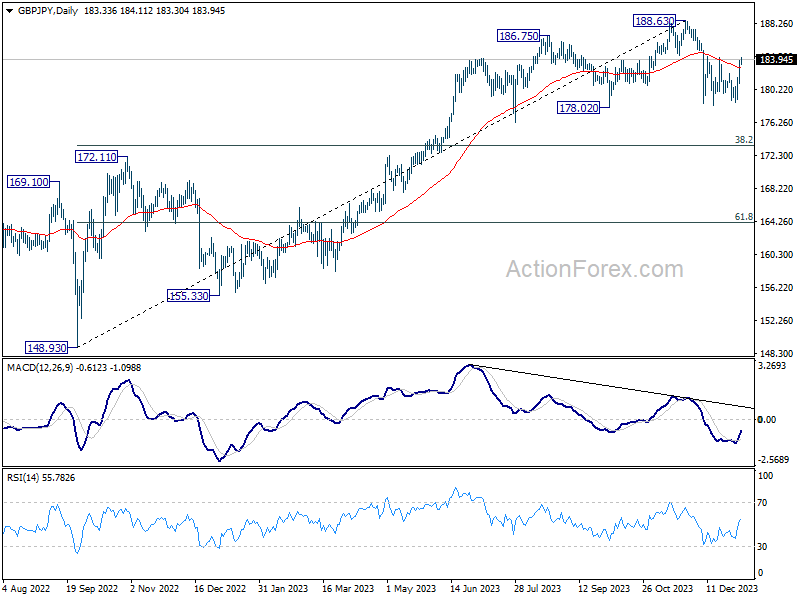

GBP/JPY Daily Outlook

Daily Pivots: (S1) 181.71; (P) 182.74; (R1) 184.47; More...

Intraday bias in GBP/JPY stays neutral at this point. On the upside, firm break of 184.15 resistance will argue that pull back from 188.63 has completed. Further rally would be seen to retest this high. On the downside, though, break of 178.71 will resume the decline from 188.63 and target 38.2% retracement of 148.93 to 188.63 at 173.46.

In the bigger picture, price actions from 188.63 medium term top are currently seen as a correction to the up trend from 148.93 (2022 low) only. As long as 172.11 resistance turned support holds, larger up trend from 123.94 (2020 low) is still in favor to resume through 188.63 at a later stage.

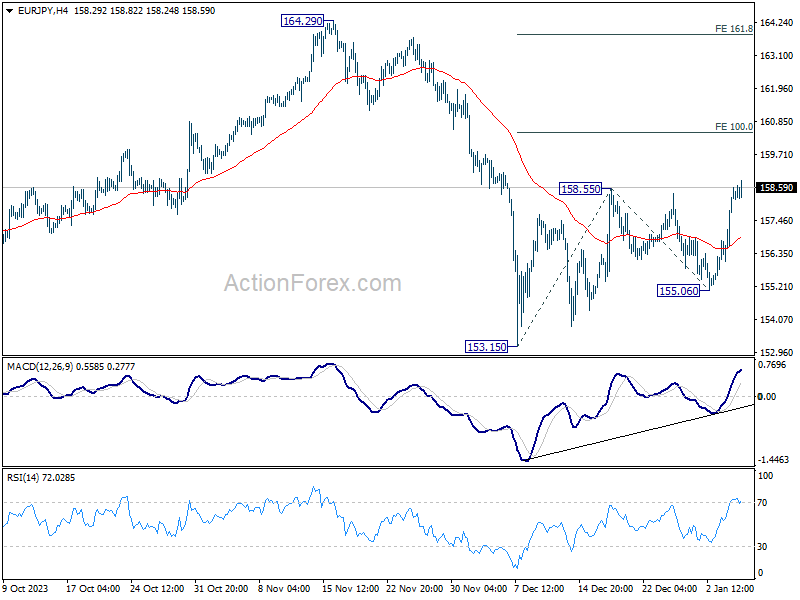

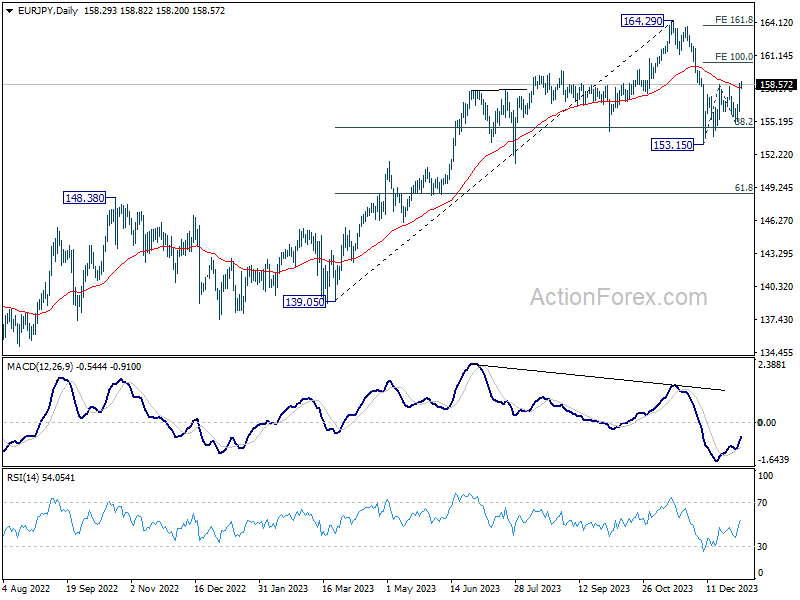

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.73; (P) 157.66; (R1) 159.25; More...

EUR/JPY's break of 158.55 resistance suggests that rebound from 153.15 is resuming. Intraday bias is back on the upside. Further rally should be seen to 100% projection of 153.15 to 158.55 from 155.06 at 160.46. For now, risk will stay mildly on the upside as long as 155.06 support holds, in case of retreat.

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.

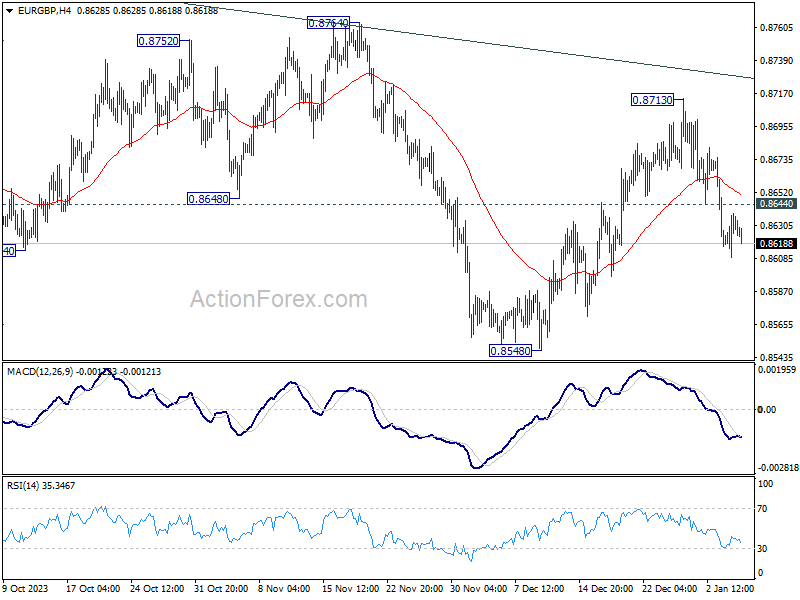

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8615; (P) 0.8627; (R1) 0.8644; More...

Intraday bias in EUR/GBP stays mildly on the downside for the moment. Rebound from 0.8548 should have completed, and deeper fall should be seen to retest this support first. Firm break there will target 0.8491 low. On the upside, however, above 0.8644 minor resistance will turn intraday bias neutral again.

In the bigger picture, current development suggests that down trend from 0.9267 (2022 high) is still in progress. This decline is seen as the third leg of the pattern from 0.9499 (2020 high). Break of 0.8201 will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969. In any case, outlook will stay bearish as long as 0.8764 resistance holds.

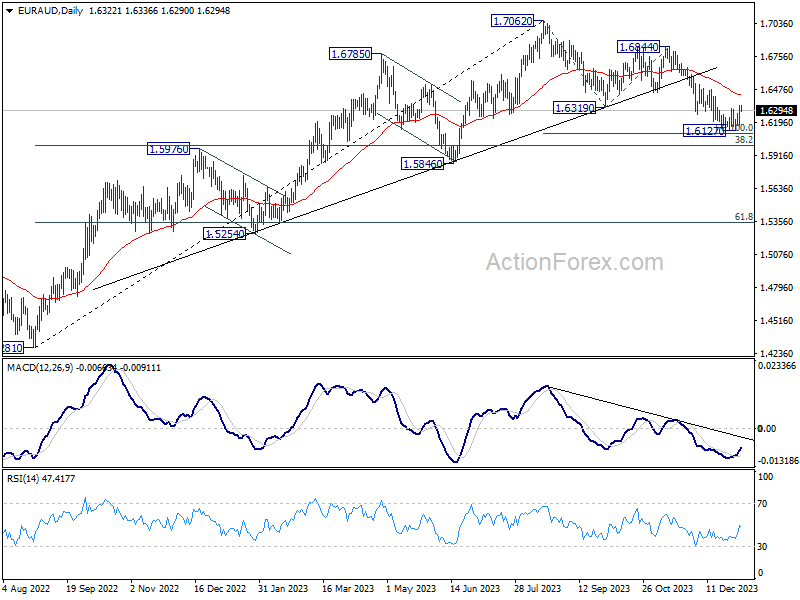

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6215; (P) 1.6280; (R1) 1.6385; More..

EUR/AUD's breach of 1.6313 resistance suggests short term bottoming at 1.6127, on bullish convergence condition in 4H MACD, just ahead of 100% projection of 1.7062 to 1.6319 from 1.6844 at 1.6106. Intraday bias is mildly on the upside for 1.6478 resistance next. For now, risk will stay on the upside as long as 1.6127 support holds, in case of retreat.

In the bigger picture, fall from 1.7062 medium term top is seen as correcting the whole up trend from 1.4281 (2022 low). Deeper decline could still be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support could be seen there to bring rebound. Sustained break of 55 D EMA (now at 1.6426) will argue that the correction has completed.

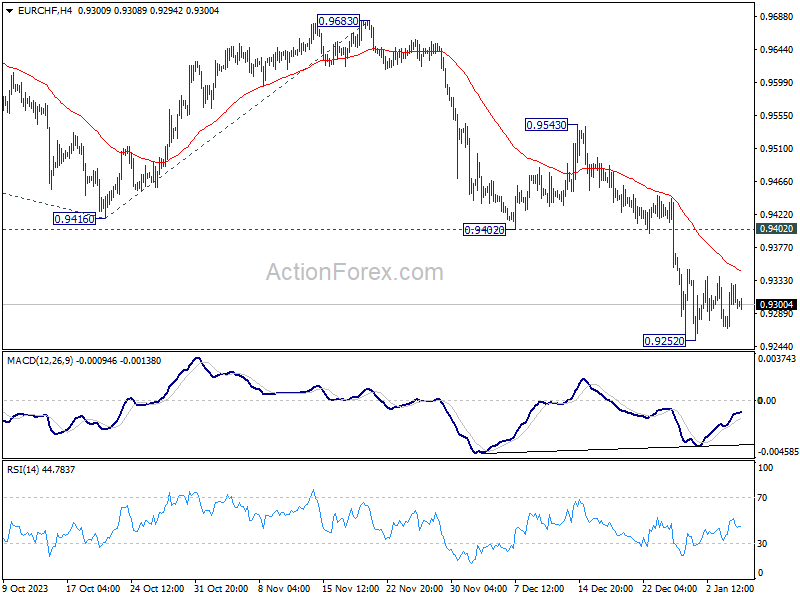

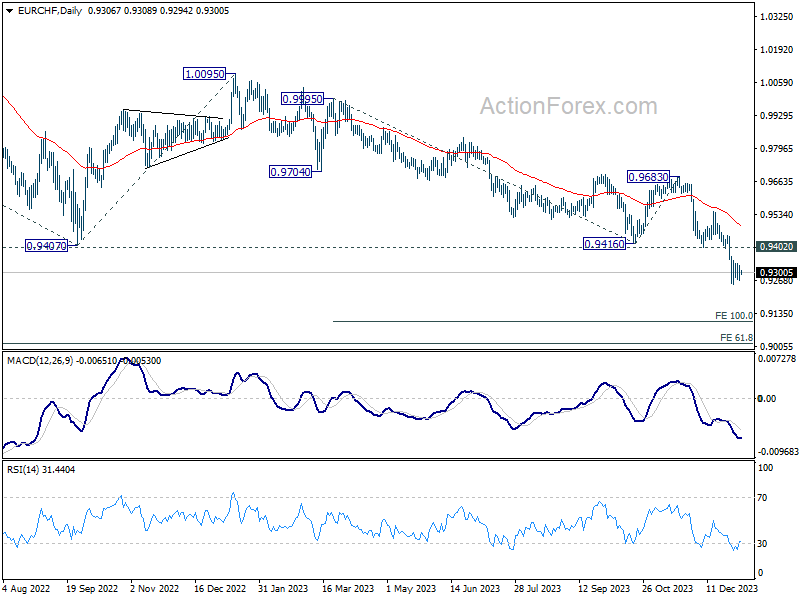

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9274; (P) 0.9303; (R1) 0.9334; More...

EUR/USD is staying in consolidation from 0.9252 and intraday bias remains neutral. While another recovery cannot be ruled out, outlook will stay bearish as long as 0.9402 support turned resistance holds. On the downside, break of 0.9252 will

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Next target is 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

It’s Payrolls Day

In focus today

The first week of January will be concluded with the December Jobs Report at 14:30 CET, and ISM services index at 16:00 CET. Recent data (Claims/ADP/JOLTs) has generally supported the narrative of robust US labour market conditions in December, and we forecast non-farm payrolls at +170k and average hourly earnings growth at 0.2% m/m seasonally adjusted. In light of ISM services, PMIs warrant a slight improvement in December, while consensus calls for a slight decline.

In the euro area, the star of the show will be the December HICP inflation. Amid fading base effects, we see headline inflation increasing to 2.9% y/y, whereas core inflation is expected to slide down to 3.3% y/y. We expect month-on-month increases in both measures consistent with annual inflation of around 2%. Inflation from Germany and France came in lower than expected yesterday, giving some downside risks to the consensus expectations for the euro area print of 3.0% y/y (0.2% m/m).

In Scandinavia, our focus today will be the Danish unemployment rate for November, which is released at 8:00 CET.

Economic and market news

What happened overnight: The news flow has been fairly light. Israel's defence minister put out the visions for the next stage of the conflict, and announced that there should be "no Israeli civilian presence" in Gaza when the war with Hamas is over. Additionally, Antony Blinken, U.S. Secretary of State, is set to visit Israel again over the coming days.

What happened yesterday: The second day with US labour market data affirmed the notion of resilience. The December ADP employment ticked higher than expected (164k vs. 115k), while initial jobless claims came in lower at 202k, indicating that firms are still reluctant to lay off workers. With data warranting a still robust US labour market, global equities climbed higher after its slump since the start of the new year. Similarly to stocks, yields ticked higher, with the 10Y UST reaching 4%. In commodity space, oil prices fell 1% (USD77.9/barrel) after the EIA report showed rising US fuel inventories and declining energy demand last week.

Equities: Equities were mixed on Thursday. European equities recovered amid solid macro data while US continued to drop somewhat. Stoxx 600 recovered 0.7% while S&P 500 closed down -0.3%. The defensive rotation continued, but in a slower pace than earlier this week. This translated into a preference for health care and banks while yield sensitive cyclicals that underperformed (tech, consumer discretionary, communication) as yields rose. In total, global defensives have outperformed cyclicals by 4p.p. this week, which is a lot. US futures unchanged in a wait-and-see mode ahead of the job report this afternoon.

FI: Soft headline inflation figures from Germany and France was not enough to counter a significant sell-off in bond markets yesterday. The Bund curve rose 9-10bp throughout the day as markets softened the bets on ECB rate cuts this year, declining from 162bp to 150bp. The repricing happened very smoothly during the session. 10Y UST yields followed European peers higher with ADP employment growth coming in above consensus estimates. Long-term inflation swap rates rose slightly across USD and EUR products.

FX: EUR/USD retraced some of previous sessions' gains yesterday, settling around 1.0950. JPY took a beating against both EUR and USD, which is a bit surprising given the sour risk sentiment, but possibly connected to speculation that the recent earthquake makes it harder for BoJ to abolish negative rates. Scandies strengthened modestly, defying risk sentiment. EUR/GBP had a quiet session, remaining above 0.86 despite stronger-than-expected UK PMIs.