Sample Category Title

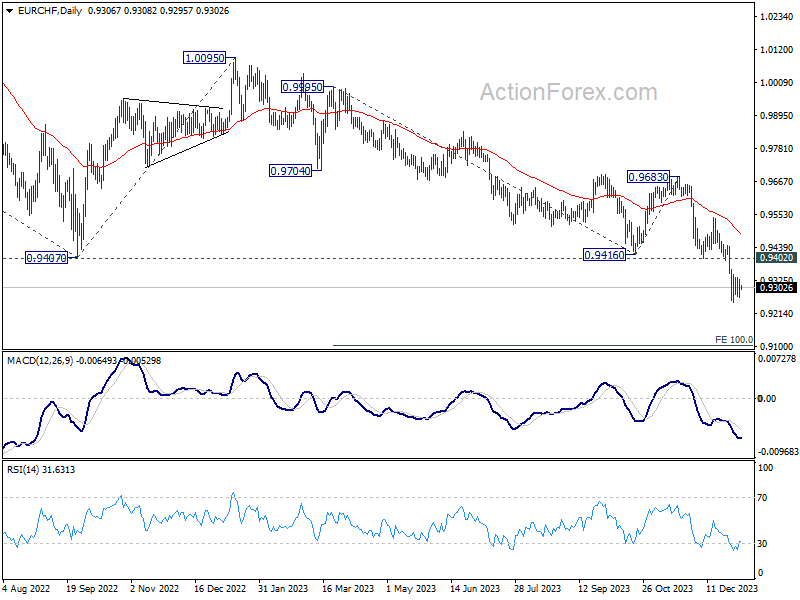

EUR/CHF on edge: Will Eurozone CPI trigger downside breakout?

Euro is currently trading weaker against its European peers and Dollar as market anticipates the release of Eurozone CPI flash data for December. Expectations are set for the headline CPI to increase from 2.4% yoy to 3.0% yoy, ending a six-month streak of consecutive declines. Meanwhile, core CPI is expected to slow down from 3.6% yoy to 3.4% yoy.

The jump in headline inflation shouldn't be a surprise to ECB officials. Executive Board member Isabel Schnabel had acknowledged last monththat a temporary uptick in inflation was possible. But she also expected it to "gradually" fall to ECB's 2% target by 2025. The anticipated continued decline in core inflation could reinforce the ECB's confidence that the trend of disinflation is still ongoing.

Currently, swap markets are factoring in approximately 1.6 percentage points of rate cuts by ECB this year, with 60% probability of these cuts commencing as early as March. The critical consideration now is the pace of disinflation: whether it is rapid enough to justify earlier rate cuts, or slow enough to warrant maintaining the current restrictive policy stance for a longer duration.

Today's Eurozone CPI data could be pivotal for the Euro's performance. Any results that fall short of expectations might trigger another wave of selling pressure. Specifically, break of 0.9252 support will resume EUR/CHF's down trend from 1.0095, and target 100% projection of 0.9995 to 0.9416 from 0.9683 at 0.9104 next.

10-year yield could break above 4% on strong NFP

As financial markets await December US non-farm payroll data, remains the strongest major currency for the week. 10-year treasury yield continues its attempt to breach break 4% psychological level, as its near-term recovery is still intact. Concurrently, NASDAQ leads pullback in the stock markets, reflecting cautious investor sentiment.

The current market mood suggests recalibration of expectations regarding Fed's policy loosening path. Traders are increasingly skeptical about Fed starting rate cuts as early as March, with the likelihood now estimated around 65% according to Fed funds futures. A robust set of NFP numbers could further solidify this sentiment shift, potentially boosting Dollar and treasury yields while exerting pressure on stocks.

Markets expect NFP to show 168k job growth in December. Unemployment rate is expected to tick up from 3.7% to 3.8%. Average hourly earnings are expected to grow 0.3% mom.

Recent released job market data suggest the possibility of an upside surprise in the NFP report. ADP private employment report showed 164k new jobs in the same month, exceeding expectations and showing an increase from the previous month's 101k. ISM Manufacturing PMI's employment component also improved, rising to 48.1 from 45.8, though it remains in contraction territory. Furthermore, 4-week moving average of initial unemployment claims decreased to 208k, down from previous month's 221k.

Market response to NFP data could particularly impact 10-year treasury yield. Technically, a short-term bottom appears to be in place at 3.785 with the current recovery, and D MACD crossed above signal line. Firm break above 4% level could provide momentum for TNX to target the 55 D EMA, currently at 4.212. While a break through 38.2% retracement of 4.997 to 3.785 at 4.247 seems unlikely at present, even a moderate rebound in TNX should lend near-term support to Dollar, especially against Yen.

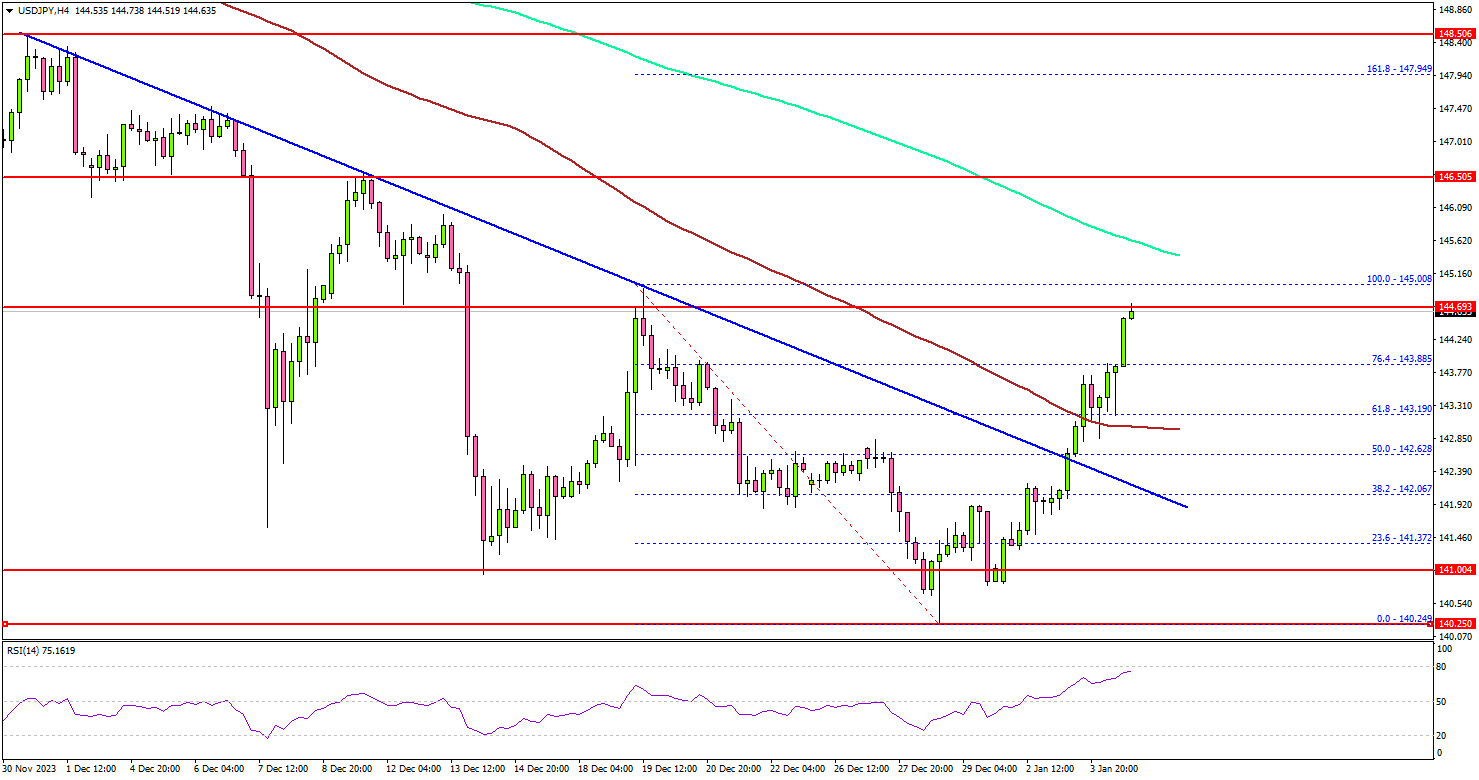

USD/JPY Regains Strength Ahead of US NFP Report

Key Highlights

- USD/JPY started a recovery wave above the 142.00 resistance.

- It broke a major bearish trend line with resistance at 142.60 on the 4-hour chart.

- Bitcoin price recovered losses, but it might struggle above $43,800.

- The US nonfarm payrolls could change by 170K in Dec 2023, down from 199K.

USD/JPY Technical Analysis

The US Dollar found support near the 140.25 zone against the Japanese Yen. USD/JPY started a recovery wave above the 141.50 and 142.00 levels.

Looking at the 4-hour chart, the pair broke many hurdles near 142.00. It even surpassed a major bearish trend line with resistance at 142.60. There was a move above the 50% Fib retracement level of the downward move from the 145.00 swing high to the 140.24 low.

The pair settled above 143.50 and the 100 simple moving average (red, 4 hours). On the upside, immediate resistance is near the 145.50 level and the 200 simple moving average (green, 4 hours).

The next key resistance is near the 146.20 level. A close above the 146.20 zone could open the doors for more upsides. The next stop for the bulls might be 148.00.

If there is a fresh decline, the pair might test the 143.80 support. The next major support sits at 142.85 or the 100 simple moving average (red, 4 hours).

A downside break below the 142.85 zone could spark a sustained decline. The next major support is 141.20, below which the pair might decline and test 140.00. Any more losses might send the pair toward the 138.00 zone.

Looking at Bitcoin, the price started a recovery wave after a sharp decline and is currently struggling to settle above $43,800.

Economic Releases

- US nonfarm payrolls for Dec 2023 – Forecast 170K, versus 199K previous.

- US Unemployment Rate for Dec 2023 - Forecast 3.8%, versus 3.7% previous.

- US ISM Services Index for Dec 2023 – Forecast 52.6, versus 52.7 previous.

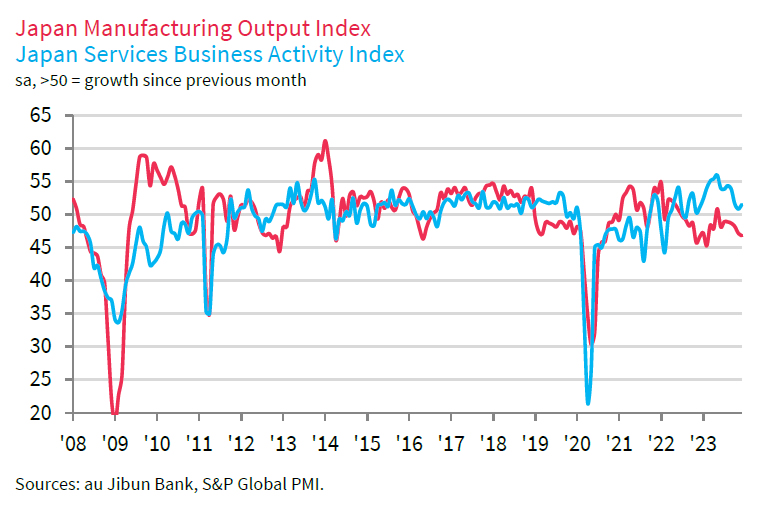

Japan’s PMI services finalized at 51.5, steeper increase in inflationary pressures

Japan's PMI Services was finalized at 51.5 in December, up slightly from November's 50.8, signaling a modest but positive growth in the sector. Composite PMI also improved, reaching the neutral mark at 50.0, up from 49.6 in the previous month.

Usamah Bhatti of S&P Global Market Intelligence attributed this growth to an increase in new orders and customer numbers. This uptick in business activity led firms to end the year with a more positive outlook. Service providers also expressed confidence about future activity, driven by expectations of economic recovery and plans for long-term business expansion.

However, Bhatti noted "steeper increase in inflationary pressures", mainly from escalated costs for raw materials, fuel, and labor. This resulted in the highest increase in service output charges since August.

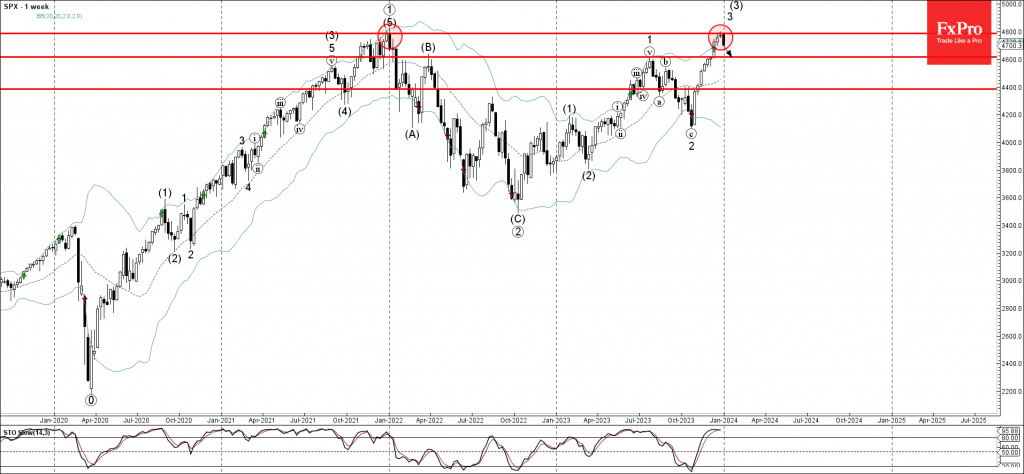

S&P 500 Index Wave Analysis

- S&P 500 index reversed from resistance level 4800

- Likely to fall to support level 4600.00

S&P 500 index recently reversed down from the major long-term resistance level 4800.00 (which stopped the sharp weekly uptrend at the end of 2021).

The resistance level 4800.00 was strengthened by the upper daily and weekly Bollinger Bands.

Given the strength of the resistance level 4800.00 and the strongly overbought weekly Stochastic, S&P 500 index can be expected to fall further to the next support level 4600.00.

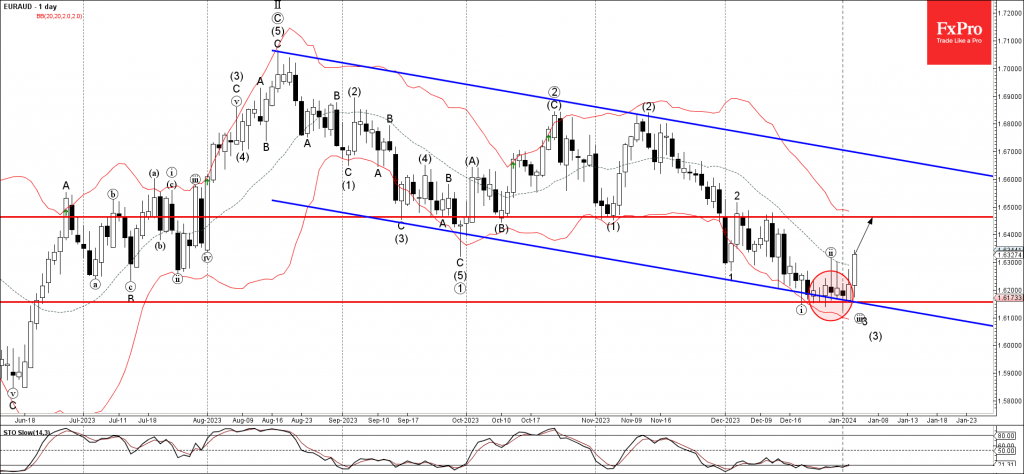

EURAUD Wave Analysis

- EURAUD reversed from support level 1.6155

- Likely to rise to resistance level 1.6465

EURAUD recently reversed up from the key support level 1.6155 (which reversed the price multiple times from the middle of December).

The support level 1.6155 was strengthened by the lower daily Bollinger Band and by the support trendline of the weekly down channel from August.

Given the strength of the support level 1.6155, EURAUD can be expected to rise further to the next resistance level 1.6465 (former double top from December).

Sunset Market Commentary

MarketsRegional inflation figures for North Rhine Westphalia wrongfooted investors at the very onset of today’s trading session. Prices fell by 0.1% M/M in Germany’s most populous state with the Y/Y-figure rising from 3% to 3.5%. That was less than what markets expected for the national German reading which was only published during afternoon. The Bund rallied from the start with the German 10-yr yield temporarily dipping below 2%, but the move rapidly lacked momentum. Other German regional figures showed that the NRW-release was the (soft) exemption while final figures showed upward revisions to December services (48.8 from 48.1) and composite (47.6 from 47) EMU PMI’s. French inflation rose by 0.1% M/M (vs 0.3% expected) and 4.1% Y/Y (from 3.9% Y/Y; mainly because of energy base effects) with services inflation accelerating (especially travel-related). German inflation eventually printed at 0.2% M/M (vs 0.3% expected) and 3.8% Y/Y (from 2.3%). A detailed breakdown isn’t available but energy base effects are definitely at play. Today’s (European) market reaction is more telling about positioning than about effective figures. Exactly the same data set would have started a huge Bund rally only a month ago, coming on the heels of the Fed-pivot and the ECB’s hold. It suggests that the bottom below yields is becoming firmer with markets already discounting too much policy rate cuts for 2024 (up to 150 bps both in Europe and the US). The proof of the pudding will be in tomorrow’s aggregate EMU number and US payrolls. German yields at the time of writing add 8 bps to 10 bps with the belly of the curve underperforming the wings. The German 10-yr yield is currently testing the recent high at 2.12%, trying to escape the steep downward trend channel in place since end November. US yields follow the move higher, erasing yesterday’s setback. They currently rise by 5.6 bps to 7.5 bps, the belly equally outperforming. The US 10-yr yield is trying to recapture the psychologic 4% mark. Today’s US eco data weigh on US Treasuries as well with ADP employment change showing 164k net job gains in December (vs 125k consensus) and weekly jobless claims dropping back to the historically low level of 202k (from 220k vs 216k forecast). The euro holds a slight edge over the dollar. EUR/USD moves up from 1.0922 to 1.0940. EUR/GBP erases part of yesterday losses, moving back in the direction of 0.8640. Stock markets hold steady despite the uptick in core bond yields with key European indices around 0.25% higher and US benchmarks opening mixed. News & Views

The Czech Ministry of Finance published its 2024 funding and debt management strategy today. Financing needs for this year amount to CZK 468.8 bn, or about 6.1% of GDP. That’s down CZK 191.2 bn from last year, mainly on a lower state budget deficit (CZK 252bn, minus CZK 36.5 bn) as well as lower redemptions (CZK 212.4 bn, minus CZK 159.1 bn). Gross issue of CZK-denominated medium term and long-term government bonds (at least two new ones) on the domestic primary market will be carried out in a total minimum nominal value of CZK 300 to 400 bn, down from CZK 520.0 bn in 2023, and with maturities along the whole yield curve. Issuance in the bucket up to 10 years is capped at CZK 300bn while the segment beyond that holds a maximum of CZK 150 bn. The Finance Ministry retains the possibility of a new issue of government EUR-bond under Czech law through an auction organised by the Czech National Bank or using a syndicated form of sale in cooperation with primary dealers and the Czech National Bank, possibly also in an ESG format. The Bank of England released its most recent Decision Maker Panel, surveying CFO’s of companies spanning all sizes. Firms reported that their output prices rose at an annual rate of 5.9% in the three months to December, down from 6.6% in the November report. The year-ahead gauge remained unchanged at 4.4%. CPI inflation expectations for the year ahead fell from a three-month moving average of 4.6% in November to 4.3% last month. The one looking three years into the future also fell, though by a marginal 0.1% to 3.1%. Annual employment trended lower to 2.8% but the forward-looking indicator strengthened 0.1% to 1.5%. Consequently, expected wage growth increased to 5.2% over the same horizon. The DMP noted slightly reduced uncertainty among British companies. 51% of them reported high or very high levels of uncertainty in December, compared to 53% the month before.

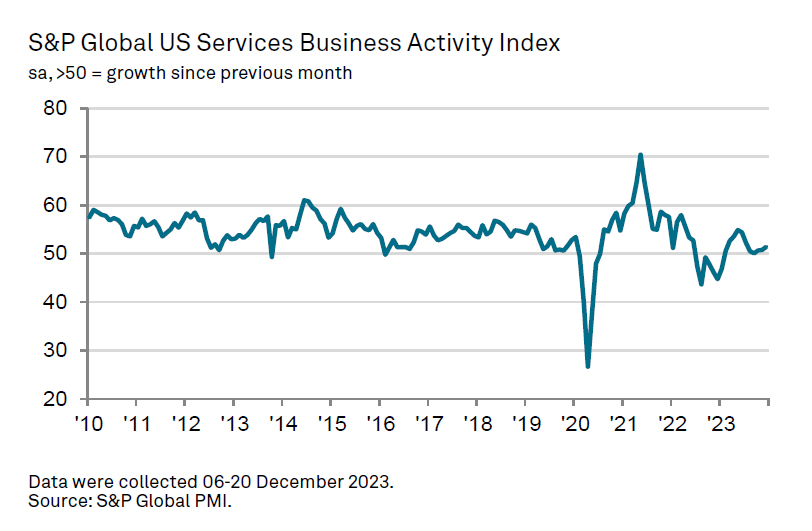

US PMI services finalized at 51.4, some New Year cheer

US PMI Services was finalized at 51.4 in December, up from November's 50.8. PMI Composite was finalized at 50.9, up from prior month's 50.7.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, said:

"Some New Year cheer is provided by the PMI signalling an acceleration of growth in the vast services economy, which reported its largest rise in output for five months in December. The improvement overshadows a downturn recorded in manufacturing to indicate that the overall pace of US economic growth likely accelerated slightly at the end of the year.

"Some support to financial services in particular is coming from the recent loosening of financial conditions amid growing hopes of interest rate cuts in 2024. Growth nevertheless remains subdued by standards seen over the spring and summer, with the struggling manufacturing sector dampening demand for business-to-business services and consumers remaining far less inclined to spend on luxuries such as travel and recreation than earlier in the year.

"The more challenging demand environment has dampened firms' pricing power, squeezing service sector selling price inflation to the lowest for over three years on average during the fourth quarter. With sticky service sector inflation being a key area of concern among Fed policymakers, the slower rate of price increase in December is welcome news."

ETHUSD Trades Sideways After Decline Pauses

- ETHUSD spikes aggressively to the downside

- Rebounds quickly and moves sideways in the last sessions

- Momentum indicators are heavily tilted to the downside

ETHUSD (Ethereum) experienced a sharp retreat following the formation of a double top pattern in the four-hour chart. Although the bulls managed to recoup some losses after the price tumbled to a fresh one-month bottom of 2,108, the digital coin is still hovering beneath both its 50- and 200-period moving averages (SMAs).

Should the sideways pattern break to the upside, immediate resistance could be encountered at the December support of 2,255. Breaking above that zone, the price may challenge the December resistance of 2,343 ahead of the 2,403 barrier. A violation of the latter might pave the way for the 2023 peak of 2,447.

On the flipside, bearish actions could send the price lower towards the recent support of 2,178. Failing to halt there, Ethereum could revisit its one-month bottom of 2,108. Even lower, the 1,985 hurdle registered in late November could provide downside protection.

Overall, ETHUSD managed to erase a part of its steep slide, but the price is still holding below both its 50- and 200-period SMAs. Hence, a break above the crucial hurdles is needed for the technical picture to improve.