Sample Category Title

Australian Dollar Stabilizes on Solid Chinese PMI

The Australian dollar has steadied on Thursday and is trading at 0.6732 in the European session, up 0.02%. This follows a four-day slide in which the Aussie fell 1.6%. Later in the day, the US releases unemployment claims and the ADP employment report, which comes just one day ahead of US nonfarm payrolls.

China’s Caixin Services PMI improved to 52.9 in December, above 51.5 in November and beating the market consensus of 51.6. The solid reading has helped the Australian dollar stabilize today. China is Australia’s biggest export market and the Australian dollar is sensitive to key releases out of China.

Fed uncertain about rate cuts timing

The December rate meeting was a barn-burner as Fed Chair Powell surprised the markets by jumping on the rate-cut bandwagon. The Fed is, however, showing more caution than the markets, which have priced in six rate cuts in 2024 compared to three from the Fed.

The minutes of the December meeting were on the dull side, as Fed members did not provide any details as to the timing of rate cuts. The minutes stated that the Fed viewed the current benchmark rate at or close to the peak, but added that there was an “unusually elevated degree of uncertainty” about the rate path, which would depend on economic conditions.

On the inflation front, members said “clear progress” had been made, but noted that core services continued to move higher. The message from the Fed was of caution – inflation is moving in the right direction but the battle is not yet over. The US dollar had a muted reaction to the minutes, while the equity markets declined as investors were disappointed that the timing of rate cuts remains up in the air.

AUD/USD Technical

- AUD/USD is testing resistance at 0.6735. Above, there is resistance at 0.6767

- 0.6698 and 0.6666 are providing support

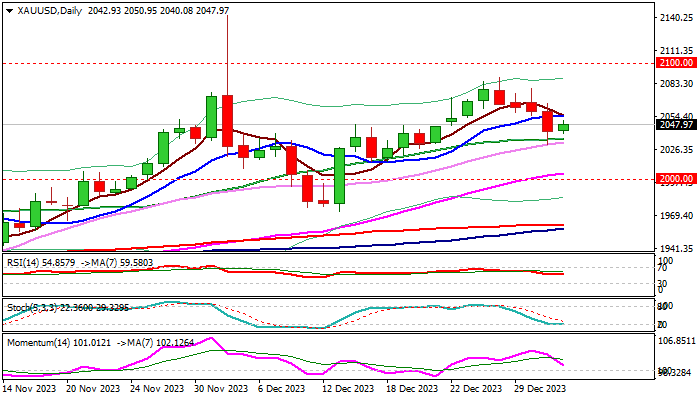

XAU/USD: Gold Regains Traction But More Evidence Needed to Signal Reversal

Gold price edged higher on Thursday morning, after a four-day pullback from $2088 (Dec 28 high) found a footstep at $2030 (50% retracement of $1973/$2088 upleg).

This points to initial signal of a healthy correction of larger uptrend, as technical studies on daily chart remain in predominantly bullish configuration and the metal continues to benefit from wide expectations that the Fed will start cutting interest rates in 2024, as well as signals that the US economy is likely to slow this year.

However, fading expectations of an early start of rate cuts in March on significant uncertainty in Fed’s rate cut outlook, continue to produce headwinds and keep the downside vulnerable.

Break of pivotal barriers at $2052/55 (Fibo 38.2% retracement of $2088/$2030 bear-leg / 10DMA) is needed to keep fresh bulls in play for stronger recovery.

Fibo 61.8% and 76.4% levels at $2066 and $2074 respectively, mark next targets, guarding key barrier at $2088, break of which would further strengthen bullish structure for renewed attempt through $2100.

Caution on failure to clear $2050, which would keep in play risk of retesting $2030 support and possible deeper drop on break.

Res: 2052; 2055; 2066; 2074.

Sup: 2040; 2030; 2017; 2009.

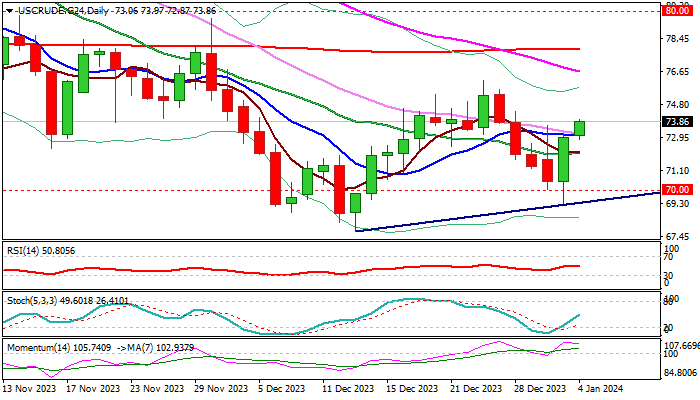

WTI Oil: Crude Oil Price Rises Further on Growing Supply Concerns

WTI Oil price rose further in early Thursday’s trading, in extension of 3.5% rally on Wednesday, the biggest daily gain since Nov 17.

Worsening fundamentals on closure of one of the largest oil fields in Libya and increased tensions around Israel-Palestine war, inflated oil price.

Stronger than expected fall in US crude inventories (API report, released late Wednesday) additionally supported oil prices.

Technical picture on daily chart has improved, following a bear trap under $70 level and subsequent bounce that left a bullish engulfing pattern and rose above daily MA’s (10,20,30), retracing so far over 61.8% of $76.16/$69.27 bear-leg).

Strong bullish momentum and north-heading RSI add to positive near-term outlook.

Bulls eye Fibo barrier at $74.53 (76.4% of $76.16/$69.27), ahead of key near-term resistance at $76.16 (Dec 26 high), violation of which would generate initial reversal signal.

Daily close above broken 10DMA ($73.10) is needed to keep fresh bulls in play.

Res: 74.00; 74.53; 75.36; 76.16.

Sup: 73.53; 73.10; 72.72; 72.10.

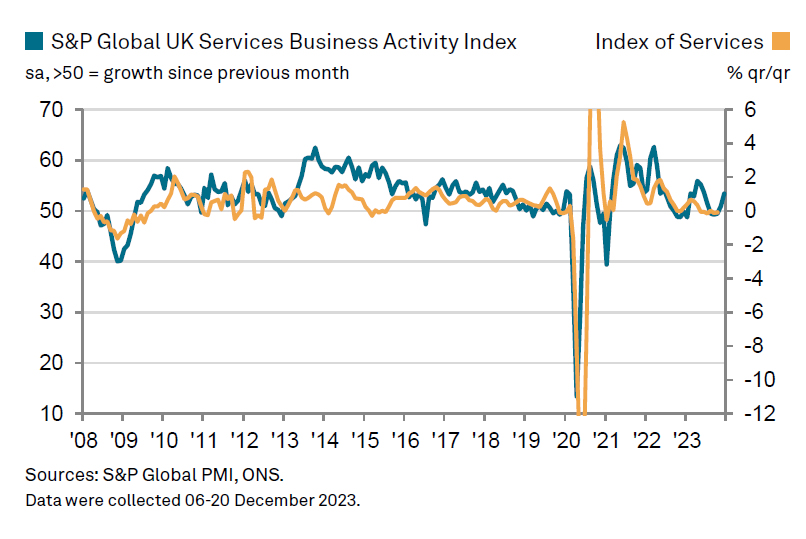

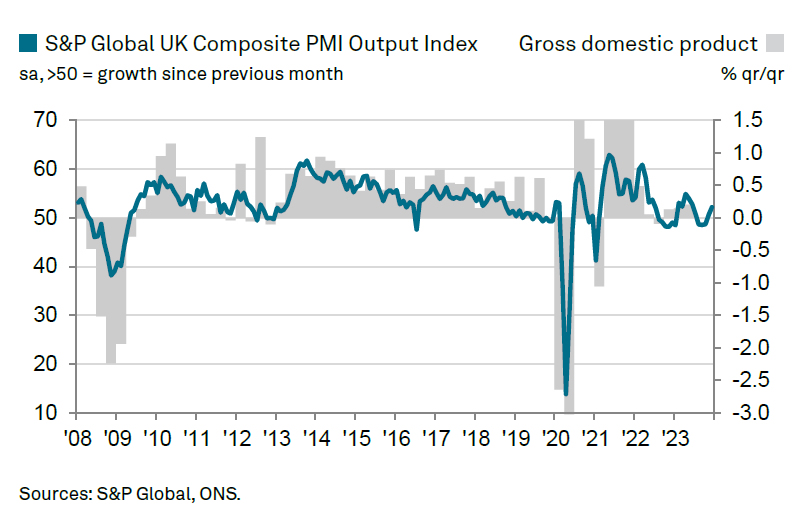

UK PMI services finalized at 53.4, rising output and price pressures

UK PMI Services was finalized at 53.4 in December, up from November's 50.9, and the highest reading since last June. S&P Global noted continuous rise in output and new work for the second consecutive month. However, the sector also saw a slight decline in employment numbers, and there was acceleration in price charged inflation. Price charged inflation accelerated again. PMI Composite was finalized at 52.1, up from prior month's 50.7.

Tim Moore, Economics Director at S&P Global Market Intelligence, stated, "December data indicated that the UK service sector ended last year on a high," attributing the recovery in client demand to expectations of lower borrowing costs and an improving global economic outlook for 2024.

Moore also highlighted that business activity expectations for the upcoming year are now at their most optimistic since May of the previous year, although he pointed out that staff hiring remained a weak spot in December, with many companies yet to lift their hiring freezes.

Moore further commented on the inflationary pressures within the service sector, noting substantial input cost increases driven by strong wage pressures. This trend has led to a robust rise in prices charged across the service sector as businesses strive to protect their margins. The rate of inflation in this regard was the fastest since July of the previous year, indicating the challenges faced by service providers in managing costs while maintaining competitive pricing.

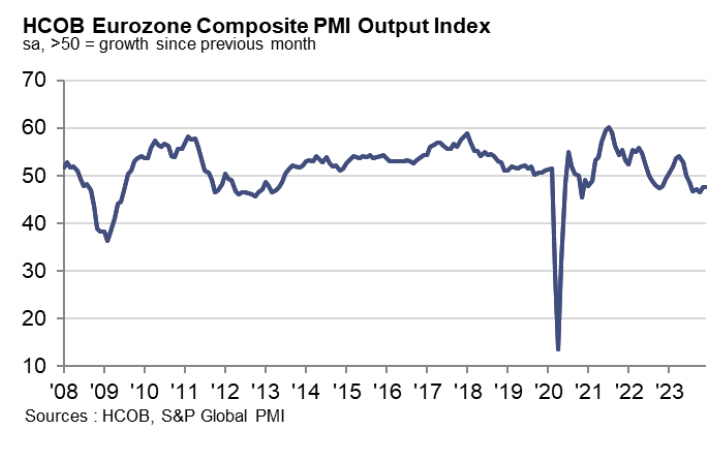

Eurozone PMI services finalized at 48.8, not quite recession yet, but hardly growth oriented

Eurozone PMI Services was finalized at 48.8 in December, up slightly from November's 48.7, a 5-month high. PMI Composite was finalized at 47.6, unchanged from prior month's reading, indicating continued contraction in the broader economy.

A country-by-country analysis of Composite PMI reveals varying performances. Ireland, with PMI of 51.5, experienced a two-month low, while Spain, at 50.4, reached a five-month high. Italy's PMI climbed to a three-month high of 48.6, and Germany's index, at 47.4, hit a two-month low. France, at 44.8, saw a four-month high, yet its service sector remains the weakest among the top Eurozone economies.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, observed that Eurozone's service sector is undergoing a slight contraction, with job numbers marginally increasing. He stated, "It's not quite recession territory yet for services, but the vibe is far from growth-oriented."

Furthermore, he expressed concerns about the broader economic outlook, noting that the Composite PMI is signaling a recession in Eurozone. The bank's GDP Nowcast model projects a consecutive contraction in the region's output for the fourth quarter, adding credence to this recessionary warning.

In examining the service sectors of the top Eurozone countries, de la Rubia identified significant variations. Spain's service sector is performing well, showing growth for four consecutive months. In contrast, Germany and Italy are experiencing stagnation, while France's service sector is consistently declining, making it the worst performer in this group.

AUDUSD Shows Some Upside Recovery Again

- AUDUSD remains in bullish territory

- 50- and 200-day SMAs ready for bullish cross

- Stochastic looks oversold

AUDUSD is recouping some losses of the preceding four red days after it found strong support at the 20-day simple moving average (SMA).

Given the current positive momentum, the question now is whether the pair will stay resilient above the 0.6690 key region. A clear step below it would wipe out today’s boost, pressing the price back to the 50- and the 200-day SMAs at 0.6580, which are ready to post a bullish crossover. Slightly lower, the ascending trend line near 0.6550 and the 0.6520 barrier could come next, within the Ichimoku cloud.

Technically, the short-term risk is leaning to the upside. The stochastic oscillator is heading upwards, indicating a bullish crossover between its %K and %D lines in the oversold area, while the RSI indicator is pointing upwards above the 50 level.

In the positive scenario, traders may wait for a close above the 0.6870 barrier and more importantly, beyond the 0.6895 barricade, taken from the peak on July 13.

To sum up, the latest upside move in AUDUSD has not excited traders yet. An extension towards the previous high is still required to make the upturn look more credible.

New Vigor on Bond Market Curtailed Dollar’s Momentum

Markets

The US eco calendar provided first meaningful input for 2024 trading yesterday. Data strengthened the goldilocks scenario of growth stabilizing at a low, but no recessionary, level in combination with a labour market turning less tight and an ongoing disinflationary process. The manufacturing ISM recovered marginally more than expected (47.4 from 46.7), but remains mired in recessionary territory (<50) for the 14th consecutive month. Details showed a mixed picture with production and export orders stabilizing and the pace of job cutting slowing. (Domestic) new orders fell at a more rapid pace though. Cheaper commodities (mainly oil prices) pulled the prices paid gauge in the ISM-report to a six-month low of 45.2. JOLTS job openings fell from 8.85mn to 8.79mn (from a 12.03mn peak in March 2022), the lowest level since early 2021 though still significantly above the pre-pandemic peak (7.59mn). The quits rate ticked down to 2.2% from 2.3%, the lowest since September 2020, suggesting less confidence to switch jobs. After some hesitation, the early (US) date releases provided new momentum for US Treasuries. The release of FOMC Minutes of the December policy meeting provided a final boost. There was no meaningful debate whatsoever on the timing of a first policy rate cut – high “for some time” – but they unexpectedly featured a paragraph on the balance sheet run-off. Several participants suggested it would be appropriate to begin discussing the technical factors that would determine when the US central bank slows its quantitative tightening process. The Fed started QT in June 2022 and currently allows $60bn of Treasuries and $35bn of mortgage-backed securities to mature each month without reinvesting the proceeds. Slowing and stopping QT should happen when bank reserves (currently $3.48tn) are “somewhat above the level judged consistent with ample reserves”. Minutes didn’t give any indication on what the equilibrium reserve level should be. During the previous QT campaign (2017-2019), reserves fell from around $2.4tn to $1.5tn.

Daily changes on the US yield curve yesterday ranged between -1.3 bps and +0.9 bps with the belly of the curve outperforming the wings. German yields dropped by 3.4 bps (30-yr) to 4.9 bps (5-yr). New vigor on the bond market curtailed the dollar’s momentum with the trade-weighted greenback halting its ascent near first resistance around 102.50. EUR/USD closed at 1.0922 from a start at 1.0942. Stock markets failed to profit from the change of tide with key European indices losing up to 1.5% and US benchmarks sliding up to 1.2% (Nasdaq). EUR/GBP slid from 0.8671 to 0.8617 on an underperformance of UK gilts (yields rising by up to 5 bps at the front end of the curve). Today’s eco calendar contains US ADP employment change and weekly jobless claims. National EMU inflation data for December offer a first glimpse on what to expect from the aggregate figure tomorrow. The main question is how large the (upward) impact from statistical base effects will be and whether they’ll be able to install a topping out pattern on the November/December bond rally.

News & Views

The South Korean government turned slightly less positive in its economic policy plan published this morning. 2024 growth is seen at 2.2%, down from 2.4% in the previous (July) estimate. 2023 growth is expected at 1.3%. Despite a more modest rebound in activity, the government expects inflation to stay somewhat higher at 2.6%, upwardly revised from 2.3% in July. "The economic recovery will be stronger (than last year) amid improvements in global trade and demand for semiconductors, but there will be difficulties in domestic demand and people's livelihoods due to persistently high inflation and interest rates," the government assessed. It intends to contribute to bring inflation back to 2% in the first half of this year, by tax and tariff cuts and a cap on utility prices. It also intends to advance/prolong tax incentives to support investment.

Will European Inflation Prints Support Rate Cut Narrative?

In focus today

Today, focus will be on inflation data coming out of Germany and France, which should indicate the direction of the euro area inflation released tomorrow.

In the US, we will get a new round of labour market data, as the ADP employment report for December and initial jobless claims are scheduled for release.

Geopolitics will remain in focus as tensions between Hezbollah and Israel are rising, sparking fears that the war in Gaza could be spreading to the wider region.

Economic and market news

What happened overnight: The Caixin services PMI from China increased to 52.9, expanding at the fastest pace in five months. Together with the better-than-expected Caixin manufacturing PMI, the composite PMI measure rose from 51.6 to 52.6, indicating that growth is finally picking up after a very challenging 2023. However, risk sentiment in Asian markets has remained negative with broad-based declines in equity indices overnight.

What happened yesterday: The risk-off market sentiment continued yesterday as uncertainty on the outlook for monetary policy continues to induce volatility across asset classes. Yields climbed higher for most of the session, though soft US data and the FOMC minutes managed to reverse most of the move in the evening. Equities continued down across sectors and regions throughout the session.

The December FOMC minutes were overall quite balanced with both hawkish and dovish signals. Almost all members were convinced at the December meeting that inflation was coming under control, while also noting that "upside risks" to inflation have diminished. Moreover, it appeared that members were increasingly concerned about the damage that "overly restrictive" monetary policy could do to the economy. Despite the relatively dovish hints, many officials expressed some concern that the easing of financial conditions could complicate returning inflation to the target. This could warrant keeping policy unchanged longer than currently anticipated.

In respect of the ISM and JOLTs, the signals were relatively mixed. The ISM December manufacturing index was in line with consensus, increasing slightly to 47.4, yet still remaining in contractionary territory. In terms of JOLTs, the print came out roughly in line with expectations as job openings rose less than projected, while the October figure was revised higher. The labour market is gradually cooling with both hiring and the number of quits declining in November. However, it still remains fairly robust - for instance the ratio of job openings to unemployed remains above pre-pandemic averages (1.4 vs. 1.25).

Equities: Investors took home profit across the US, Europe and Nordics yesterday. Equities sold off sharply, but Fed minutes and macro data not to blame, in our view. In fact, these were still as close to goldilocks as it can get. However, it is difficult to surprise investors positively when goldilocks are already the base scenario into 2024. Hence, excess optimism and stretched short-term positioning in equities will exaggerate small disappointments to the downside. That is probably what happened yesterday. We think fundamentals are still in place for an equity overweight, but with a VIX at record lows it is inevitable that the road will be bumpier than the last two months.

Stoxx 600 and S&P 500 fell -0.9%, Nordics -1% and small cap Russell 2000 a full -2.7%. Underperformers included the December winners: Cyclicals. This brought a mixed bag of real estate, consumer discretionary, industrials and materials to the losers club. Note that not only rate sensitive sectors sold off: Yields sensitive sectors like utilities, health care and communication outperformed. Hence, this was more about a defensive rotation than Fed disappointing. Same defensive rotation in the Nordics with industrials selling off -3% to the benefit of health care (Novo Nordisk +2%), telecom and banks. US futures are unchanged this morning, so the sell-off might be levelling off today.

FI: Global yields were higher for most of yesterday's session, though gaining some tailwinds from US data and the FOMC minutes in the last part. 10Y government bond yields in Germany and the US are down a couple of basis points, while the pricing of rate cuts from the ECB and Fed in 2024 is almost unchanged at 162bp and 148bp, respectively. The Bund ASW spread tightened further on Wednesday, now standing at 46.6 - the lowest level since early 2022.

FX: We saw continued USD-strength in yesterday's trading, although the FOMC minutes brought on a minor retracement at the end of the session. Meanwhile, DKK and SEK suffered through poor risk sentiment, whereas otherwise risk-sensitive NOK found (relative) support in rising oil prices. Yesterday's worst performer (vs USD) within G10 was JPY, with USD/JPY rising above 143 once again and at the other end of the spectrum we find GBP, posting a gain of 0.4% vs the USD on the day.

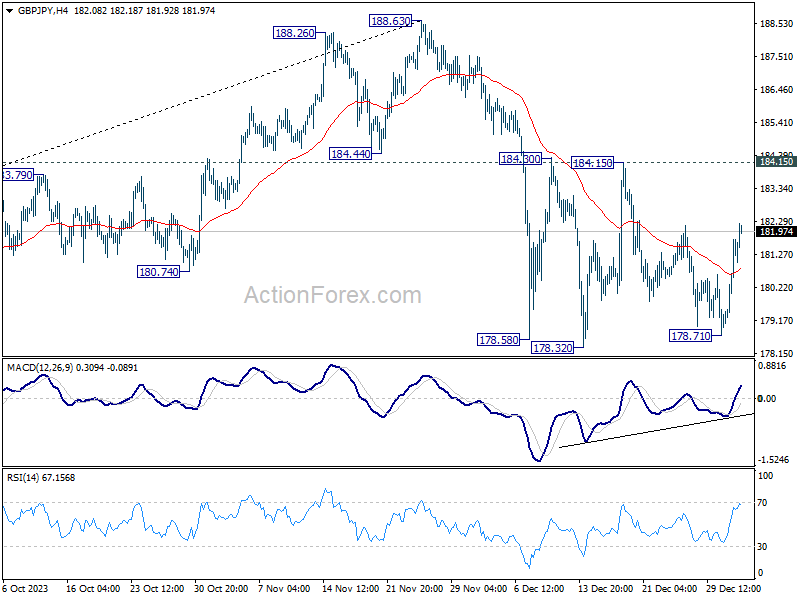

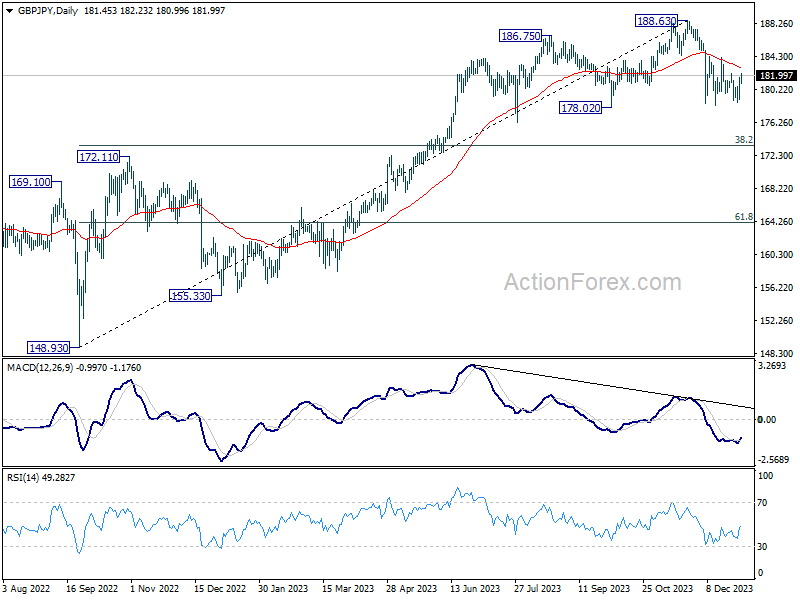

GBP/JPY Daily Outlook

Daily Pivots: (S1) 179.73; (P) 180.74; (R1) 182.48; More...

Intraday bias in GBP/JPY stays neutral for the moment, and range trading could continue above 178.32. Further decline is expected as long as 184.15 resistance holds. On the downside, break of will resume the decline from 188.63 and target 38.2% retracement of 148.93 to 188.63 at 173.46. However, decisive break of 184.15 will argue that pull back from 188.63 has completed and bring retest of this high.

In the bigger picture, price actions from 188.63 medium term top are currently seen as a correction to the up trend from 148.93 (2022 low) only. As long as 172.11 resistance turned support holds, larger up trend from 123.94 (2020 low) is still in favor to resume through 188.63 at a later stage.

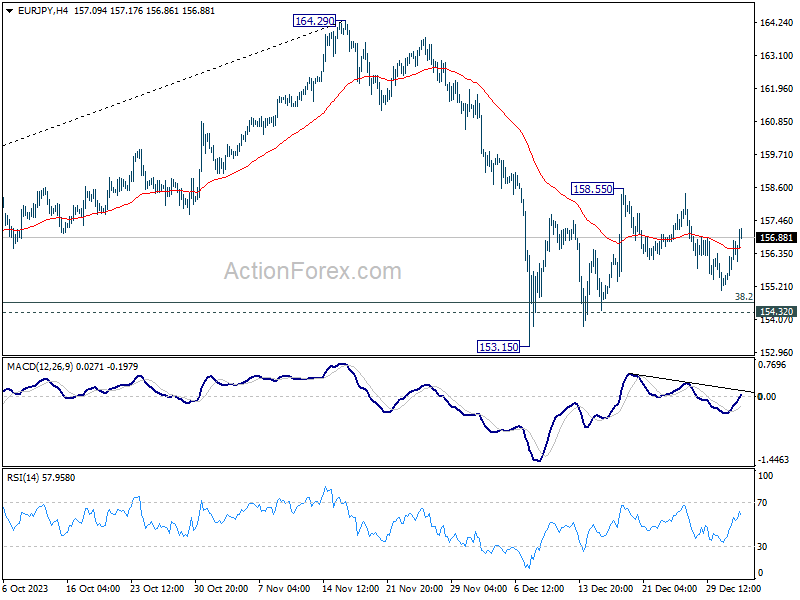

EUR/JPY Daily Outlook

Daily Pivots: (S1) 155.52; (P) 156.15; (R1) 157.15; More...

Range trading continues in EUR/JPY and intraday bias remains neutral. On the upside, above 158.55 will resume the corrective rebound from 153.15. On the downside, break of 153.15 will resume whole fall from 164.39 to 61.8% retracement of 139.05 to 164.29 at 148.69.

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.