Sample Category Title

US Jobs Data a Setback But No Game Changer

The first US jobs report of the year was an early reminder to investors that things don't always go their way, despite the experience of the last couple of months.

Whether it was just exuberant festive cheer or something more, investors bounced into the end of 2023 full of hope that not only is the tightening cycle behind us, but 2024 will be the year of the soft landing and more rate cuts than you can count on one hand.

That may be proven to be correct, perhaps even not bullish enough, but it was going to be tough to sustain that positioning and build upon it early in the new year. We effectively needed all of the economic indicators to fall kindly from the off which was a big ask.

Today has, along with the FOMC Minutes on Wednesday, brought an early setback. But I don't think either ultimately changes anything as far as the rest of the year is concerned. The labor market is still slowing gradually and while wages were a little stronger, the broader trend remains very promising.

Perhaps that would explain the response in the markets, with the dollar initially spiking as the report dropped before giving back those gains to trade lower than it did pre-release. US yields also reversed the initial gains while gold hit a new high for the day. None of this suggests traders are suddenly worried.

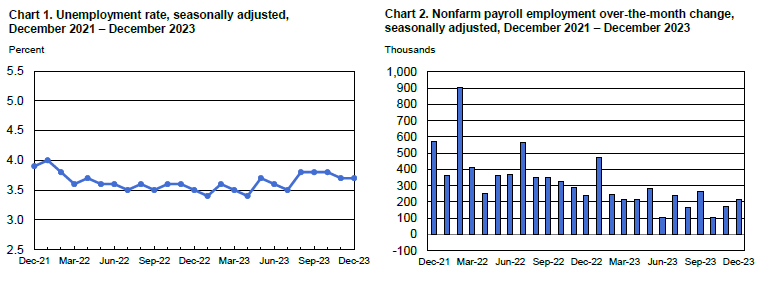

US: Job Growth Picks Up to End 2023, But Unemployment Rate Unchanged

Non-farm payroll employment jumped by 216k in December, comfortably ahead of expectations calling for a gain of 175k. However, that strength is tempered by downward revisions to October and November of 45k and 26k, respectively.

- Hiring over the last three-months averaged 165k jobs per-month, down from the 180k averaged between September-November and below the 225k per month average pace for 2023 as a whole.

Private payrolls rose by 164k – building on the 136k reported in October. The service sector led the way (+142) with healthcare & social assistance (+58.9k) and leisure & hospitality (+40k) once again making large contributions. The bulk of the job losses were concentrated in transportation & warehousing – pulling back 22.6k last month. Goods-producing industries (+22k) were lifted by a healthy print in the construction sector (+17k). The public sector added another 52k jobs with state and local government payrolls finally matching their pre-pandemic totals.

In the household survey, the unemployment rate was unchanged at 3.7%, as the drop in employment (-683k) was offset by 676k fewer people in the labor force. The participation rate fell by 0.3 percentage points to 62.5% - the lowest reading since February 2023.

Wage growth picked up a bit in December, with average hourly earnings were up 0.4% month-on-month and 4.1% on a 12-month basis. The more truncated thee-month annualized rate of change ticked up to 4.3% (from 3.6% in October).

Key Implications

Quite the surprise from the U.S. labor market as job gains blew past expectations for the month. But December's upward surprise must be weigh against the 71k downward revisions to the prior two months. The trend is still the Fed's friend as the pace of hiring continues to slow, particularly for the private sector. The overall picture is one of restrictive monetary policy continuing to work through the economy and cool labor demand.

Longer-term treasury yields have been rising for a week now and today's report will add some more pressure on bonds. This has come as market expectation for the timing of the first Fed cut has shifted from March to May. With inflation still simmering below the surface and the labor market continuing to crank out new jobs, we continue to expect any easing of policy to come in the second half of the year.

Canada’s Labour Market Ends 2023 on a Dull Note

The Canadian labour market added 0.1k positions in December, with full-time employment down 23.5k and part-time employment up 23.6k.

The unemployment rate held steady at 5.8% and the participation rate fell 0.2 percentage points to 65.4%.

Employment by sector showed gains in professional, scientific and technical services (+46k), health care and social assistance (+16k), and other services (+12k). Declines were led by wholesale and retail trade (-21k) and manufacturing (-18K).

Lastly, total hours worked rose 0.4% month-on-month and wages were up 5.4% year-on-year (from 4.8% in November).

Key Implications

The Canadian jobs market ended 2023 with a shrug. The flat headline print occurred alongside diverging underlying details. Negative one month, positive the next was a theme of this report. Hours worked jumped higher after falling significantly last month, while job losses in manufacturing and construction occurred after big gains last month. Same goes for hiring of full-time and part-time workers. While this gives us little direction, some trends remained, with Canada's working-age population having increased by 74k in December, the number of unemployed workers continued to rise, clocking in at +202k in 2023.

All told, today's report does little to change the BoC's thinking. The overall trend in the Canadian economy has been that of gradual weakness. The Canadian consumer has pulled back in the face of high interest rates and businesses have slowed the pace of hiring. With underlying inflation moving towards the BoC's target, an April policy rate cut remains in view.

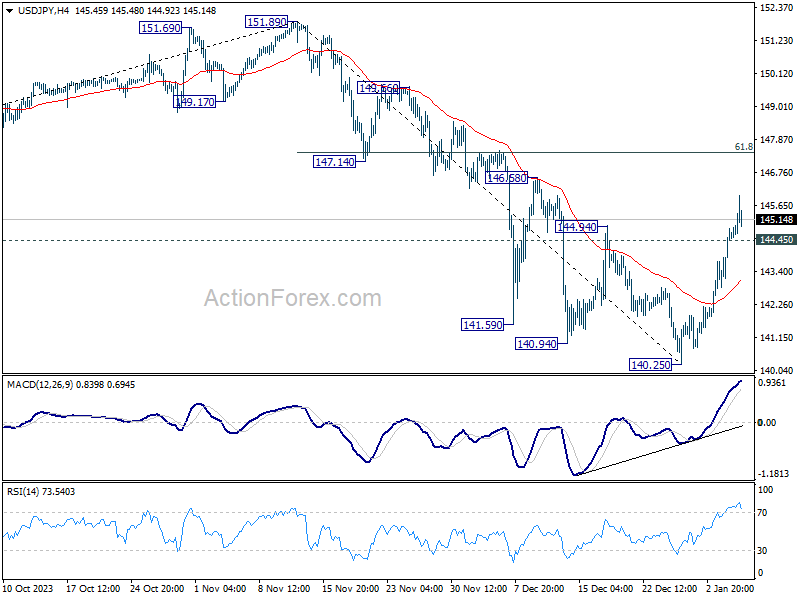

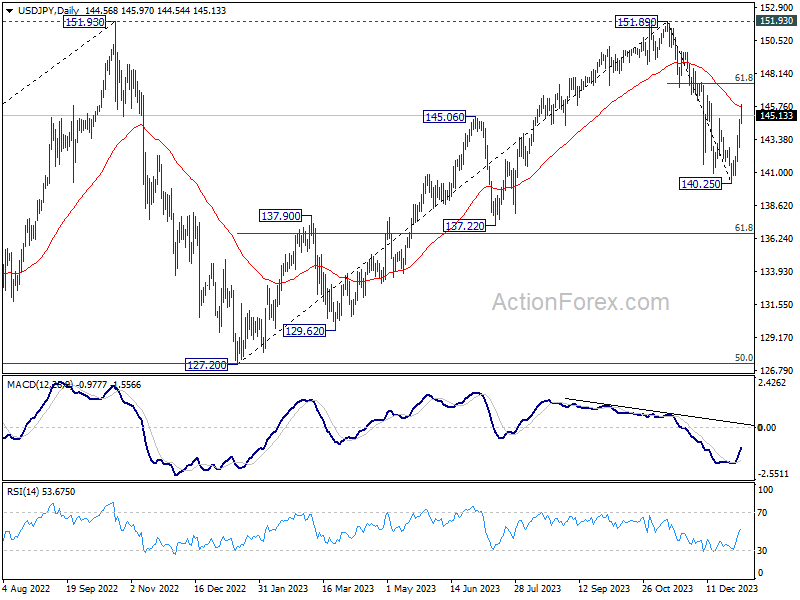

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.38; (P) 144.11; (R1) 145.37; More...

Intraday bias in USD/JPY remains on the upside at this point. Rise from 140.25 is in progress for 61.8% retracement of 151.89 to 140.25 at 147.44, even as a corrective move. On the downside, below 144.45 minor support will turn intraday bias neutral first. But risk will now stay on the upside as long as 55 4H EMA (now at 143.05) holds.

In the bigger picture, stronger than expected rebound from 140.25 is mixing up outlook. On the upside, sustained trading above 55 D EMA (now at 145.72) will argue that fall from 151.89 is merely a correction to the up trend from 127.20 (2022 low). This rally is still in progress for 151.93 and above at a later stage. Nevertheless, break of 140.25 will revive the case that corrective pattern from 151.93 has already started the third leg, back towards 127.20.

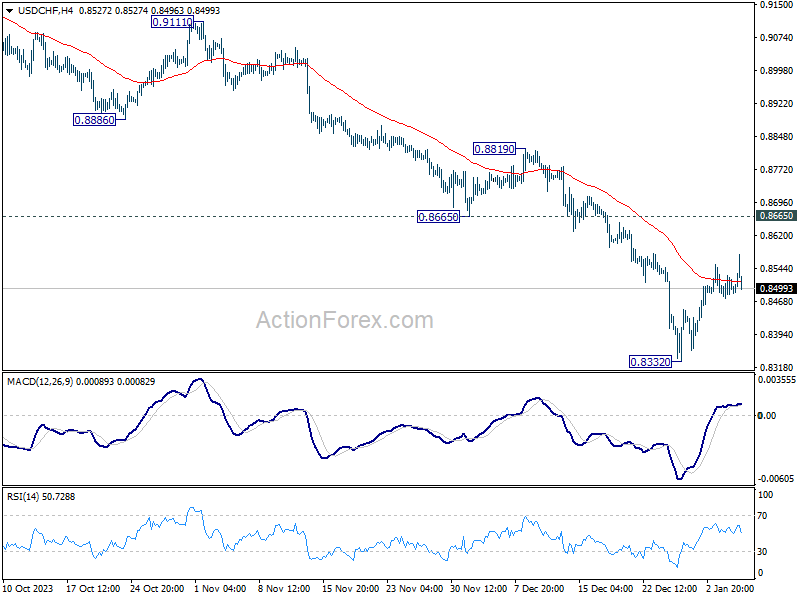

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8477; (P) 0.8503; (R1) 0.8528; More....

USD/CHF's outlook is unchanged as price actions from 0.8332 are still seen as a corrective pattern only. Intraday bias stays neutral and outlook remains bearish with 0.8665 support turned resistance intact. On the downside, break of 0.8332 will resume larger fall from 0.9243 to 0.8257 projection level.

In the bigger picture, break of 0.8551 support indicates resumption of whole decline from 1.0146 (2022 high). Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

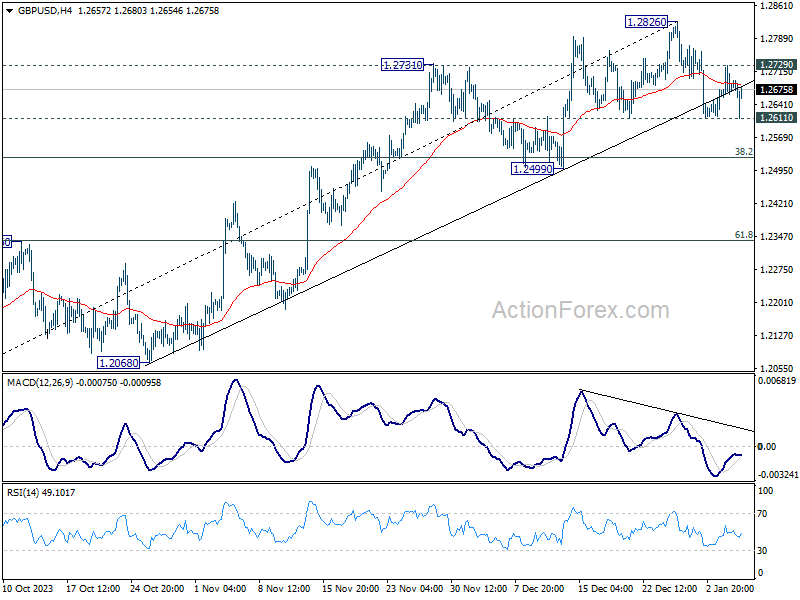

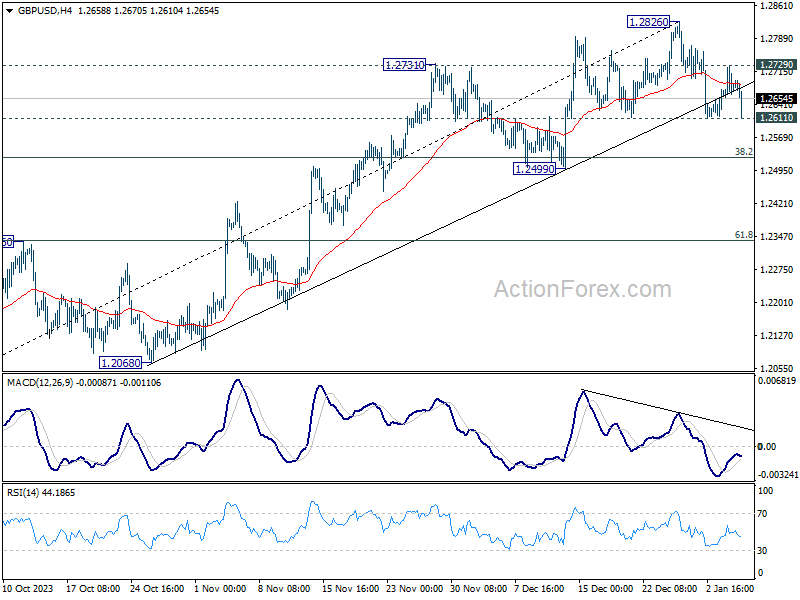

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2650; (P) 1.2690; (R1) 1.2723; More...

GBP/USD is still bounded in range of 1.2611/2826 and intraday bias remains neutral first. On the downside, break of 1.2611 will indicate short term topping, and turn bias back to the downside for 1.2499 support. On the upside, however, above 1.2729 will bring retest of 1.2826 first. Firm break there will resume whole rally from 1.2036.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to rise from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

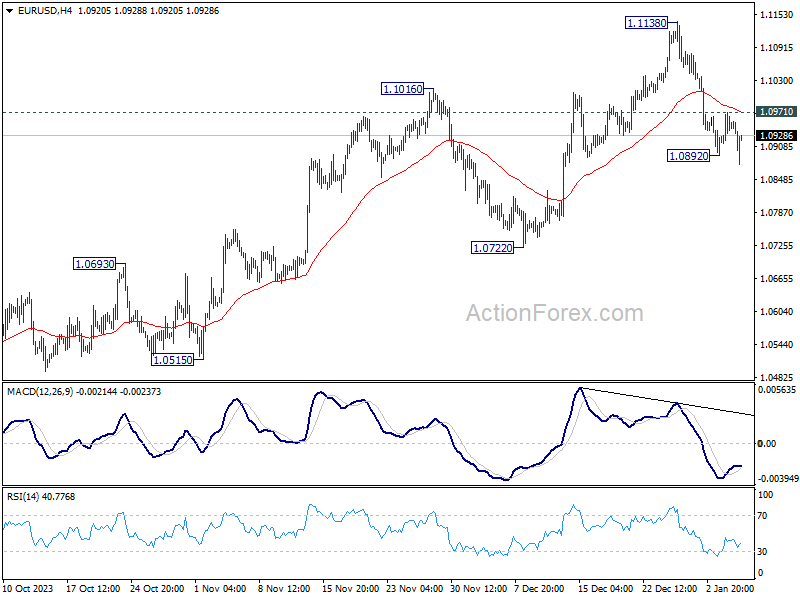

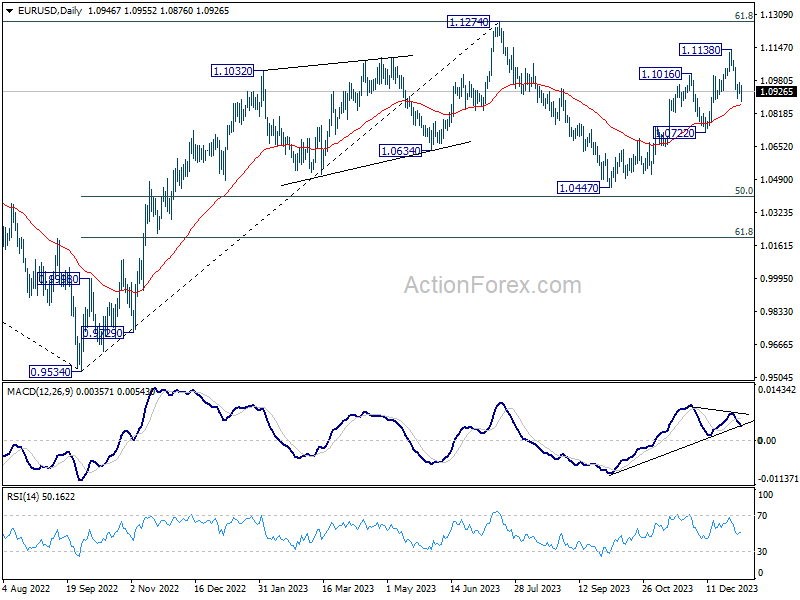

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0917; (P) 1.0944; (R1) 1.0974; More...

EUR/USD's fall from 1.1138 short term top is trying to resume by breaking 1.0892 temporary low. Intraday bias is back on the downside for 1.0722 support first. Sustained break there will argue that whole rise from 1.0447 has completed, and break deeper fall back to this support. On the upside, however, break of 1.0971 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

Dollar Rises on Robust NFP, But Gains Tempered by Hesitation

Dollar rises broadly in early U.S. session, spurred by a robust set of job data that surpassed expectations in all key areas including headline employment growth, unemployment rate, and wage growth. This robust data also propelled 10-year treasury yield further above 4% mark, while concurrently driving stock futures lower. However, while Dollar's gains against Yen and Australian Dollar are pronounced, there appears to be some hesitation in its performance against European majors. This hesitance raises the question of whether the greenback will require additional momentum from the upcoming US CPI report next week.

Japanese Yen remains the weakest performer, largely due to the rally in US and European yields. Australian and New Zealand Dollars are also underperforming for the day, influenced by prevailing risk-off sentiment. Meanwhile, Canadian Dollar, despite a miss in employment data, is emerging as the second strongest currency. Euro and British Pound are displaying mixed performance, with Euro showing minimal reaction to lower-than-expected headline CPI reading from Eurozone.

Technically, conditions are there for a deeper correction in GBP/USD , with break of trend line support, as well as bearish divergence condition in 4H MACD. However, it's still defending 1.2611 support despite the dive in early US session. On the downside, sustained break of 1.2611 will bring deeper fall to 38.2% retracement of 1.2036 to 1.2826 at 1.2524. On the upside, however, break of 1.2729 will maintain near term bullishness for a test on 1.2826 high first. Let's see which way it goes.

In Europe, at the time of writing, FTSE is down -0.82%. DAX is down -0.76%. CAC is down -1.06%. Germany 10-year yield is up 0.067 at 2.190. UK 10-year yield is up 0.064 at 3.795. Earlier in Asia, Nikkei rose 0.27%. Hong Kong HSI fell -0.66%. China Shanghai SSE fell -0.85%. Singapore Strait Times rose 0.32%. Japan 10-year JGB yield fell -0.0215 to 0.606.

US NFP rises 216k, unemployment rate unchanged at 3.7%

US non-farm payroll employment grew 216k in December, above expectation of 168k. Unemployment rate was unchanged at 3.7%, below expectation of a rise to 3.8%. Participation rate fell from 62.8% to 62.5%. Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Over the past 12 months, average hourly earnings increased 4.1% yoy.

Canada's employment rises 0.1k in Dec, vs exp 13.2k

Canada's employment rose 0.1k in December, well below expectation of 13.2k. Employment rate fell -0.2% to 61.6%. Unemployment rate was unchanged at 5.8%. Participation rate fell -0.2% to 65.4%. Total hours worked rose 0.4% mom , 1.7% yoy. Average hourly wages rose 5.4% yoy.

Eurozone CPI rises to 2.9% yoy in Dec, core CPI down to 3.4% yoy

Eurozone CPI reaccelerated from 2.4% yoy to 2.9% yoy in December, below expectation of 3.0% yoy. Core CPI (excluding energy, food, alcohol & tobacco) slowed from 3.6% yoy to 3.4% yoy, matched expectations.

Looking at the main components, food, alcohol & tobacco is expected to have the highest annual rate in December (6.1%, compared with 6.9% in November), followed by services (4.0%, stable compared with November), non-energy industrial goods (2.5%, compared with 2.9% in November) and energy (-6.7%, compared with -11.5% in November).

Eurozone PPI down -0.3% mom, -8.8% yoy in Nov

Eurozone PPI was down -0.3% mom, -8.8% yoy in November, versus expectation of -0.1% mom, -8.7% yoy. For the month, industrial producer prices, decreased by -0.8% for energy, by -0.5% for intermediate goods and by -0.1% for both capital goods and durable consumer goods, while prices remained stable for non-durable consumer goods. Prices in total industry excluding energy decreased by -0.2%.

EU PPI was down -0.2% mom, -8.1% yoy. The largest monthly decreases in industrial producer prices were recorded in Slovakia (-3.0%), Portugal (-2.3%) and Spain (-2.1%), while the highest increases were observed in Sweden (+4.1%), France (+2.4%) and Bulgaria (+0.7%).

Japan's PMI services finalized at 51.5, steeper increase in inflationary pressures

Japan's PMI Services was finalized at 51.5 in December, up slightly from November's 50.8, signaling a modest but positive growth in the sector. Composite PMI also improved, reaching the neutral mark at 50.0, up from 49.6 in the previous month.

Usamah Bhatti of S&P Global Market Intelligence attributed this growth to an increase in new orders and customer numbers. This uptick in business activity led firms to end the year with a more positive outlook. Service providers also expressed confidence about future activity, driven by expectations of economic recovery and plans for long-term business expansion.

However, Bhatti noted "steeper increase in inflationary pressures", mainly from escalated costs for raw materials, fuel, and labor. This resulted in the highest increase in service output charges since August.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0917; (P) 1.0944; (R1) 1.0974; More...

EUR/USD's fall from 1.1138 short term top is trying to resume by breaking 1.0892 temporary low. Intraday bias is back on the downside for 1.0722 support first. Sustained break there will argue that whole rise from 1.0447 has completed, and break deeper fall back to this support. On the upside, however, break of 1.0971 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Dec | 7.80% | 9.00% | 8.90% | |

| 05:00 | JPY | Consumer Confidence Index Dec | 37.2 | 36.6 | 36.1 | |

| 07:00 | EUR | Germany Retail Sales M/M Nov | -2.50% | -0.50% | 1.10% | |

| 09:30 | GBP | Construction PMI Dec | 46.8 | 46.1 | 45.5 | |

| 10:00 | EUR | Eurozone CPI Y/Y Dec P | 2.90% | 3.00% | 2.40% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Dec P | 3.40% | 3.40% | 3.60% | |

| 10:00 | EUR | Eurozone PPI M/M Nov | -0.30% | -0.10% | 0.20% | 0.30% |

| 10:00 | EUR | Eurozone PPI Y/Y Nov | -8.80% | -8.70% | -9.40% | |

| 13:30 | USD | Nonfarm Payrolls Dec | 216K | 168K | 199K | 173K |

| 13:30 | USD | Unemployment Rate Dec | 3.70% | 3.80% | 3.70% | |

| 13:30 | USD | Average Hourly Earnings M/M Dec | 0.40% | 0.30% | 0.40% | |

| 13:30 | CAD | Net Change in Employment Dec | 0.1K | 13.2K | 24.9K | |

| 13:30 | CAD | Unemployment Rate Dec | 5.80% | 5.90% | 5.80% | |

| 15:00 | USD | ISM Services PMI Dec | 52.7 | 52.7 | ||

| 15:00 | USD | Factory Orders M/M Nov | 2.30% | -3.60% | ||

| 15:00 | CAD | Ivey PMI Dec | 55 | 54.7 |

Canada’s employment rises 0.1k in Dec, vs exp 13.2k

Canada's employment rose 0.1k in December, well below expectation of 13.2k.

Employment rate fell -0.2% to 61.6%. Unemployment rate was unchanged at 5.8%. Participation rate fell -0.2% to 65.4%. Total hours worked rose 0.4% mom , 1.7% yoy. Average hourly wages rose 5.4% yoy.

US NFP rises 216k, unemployment rate unchanged at 3.7%

US non-farm payroll employment grew 216k in December, above expectation of 168k. Unemployment rate was unchanged at 3.7%, below expectation of a rise to 3.8%. Participation rate fell from 62.8% to 62.5%. Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Over the past 12 months, average hourly earnings increased 4.1% yoy.