Sample Category Title

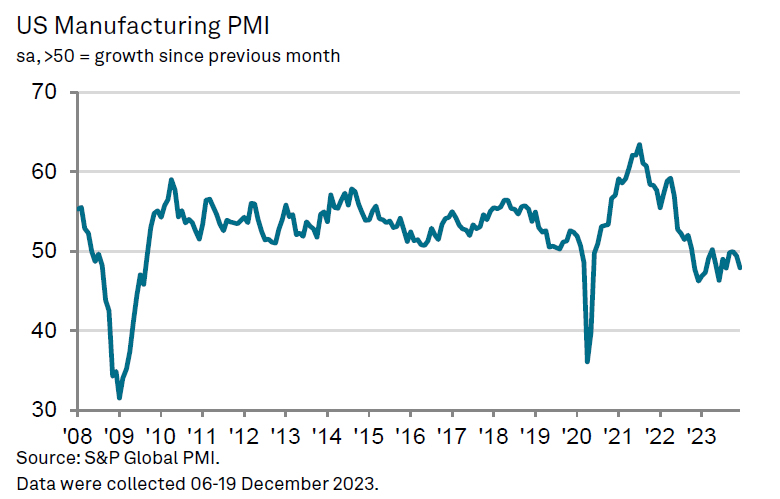

US PMI manufacturing finalized at 47.9, ends the year on a sour note

US PMI Manufacturing was finalized at 47.9 in December, down from November's 49.4.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, said:

"US manufacturers ended the year on a sour note, according to S&P Global's PMI survey. Output fell at the fastest rate for six months as the recent order book decline intensified. Manufacturing will therefore likely have acted as a drag on the economy in the fourth quarter.

"The slowdown is spreading to the labor market. Payrolls were cut for a third month running as increasing numbers of firms grew concerned about the development of excess operating capacity. The fourth quarter has consequently seen factories reduce employment at a pace not seen since 2009 barring only the early pandemic lockdown months.

"With factories also cutting back sharply on their purchases of inputs in December, suppliers were also less busy on average, again hinting at the development of spare capacity.

"While there was some uplift in the rate of both raw material and factory gate selling price inflation, firms' costs notably continued to rise at a pace below the survey's long-run average to hint at historically subdued industrial price pressures.

"Given current order book trends, the overall picture from the survey is one of supply exceeding demand for many goods, which points to downside risks to production, employment and prices as we head into 2024. Potential supply chain disruptions need to be monitored, however, notably in terms of shipping, as the survey has clearly demonstrated in the past how supply chain tensions quickly feed through to higher prices."

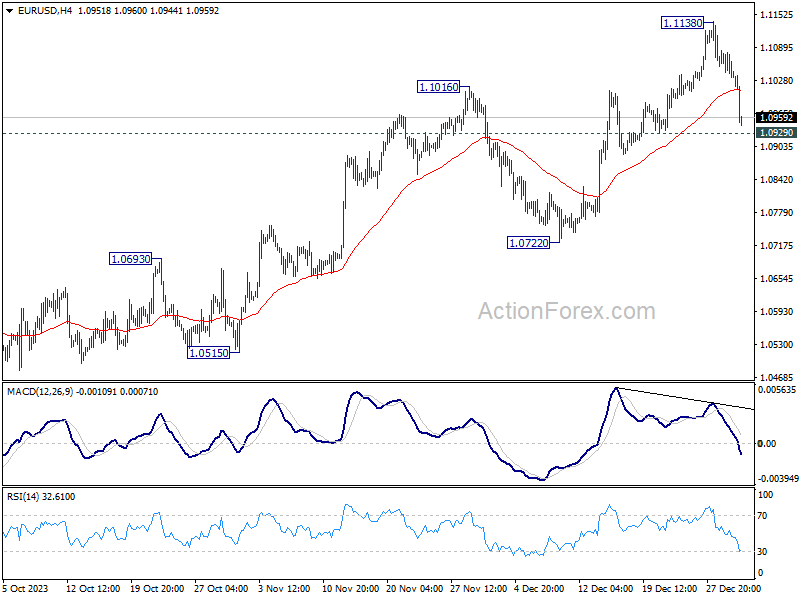

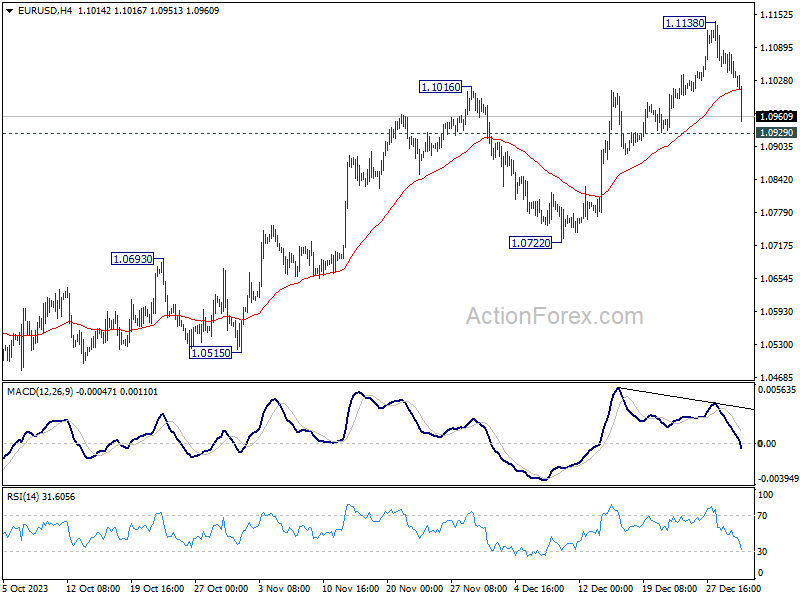

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1020; (P) 1.1052; (R1) 1.1070; More...

While EUR/USD's pull back from 1.1138 extends lower, it's still staying above 1.0929 support. Intraday bias remains neutral at this point. on the upside, break of 1.1138 will resume the rise from 1.0447 to retest 1.1274 high. Meanwhile, break of 1.0929 will indicate short term topping and turn bias back to the downside for 1.0772 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

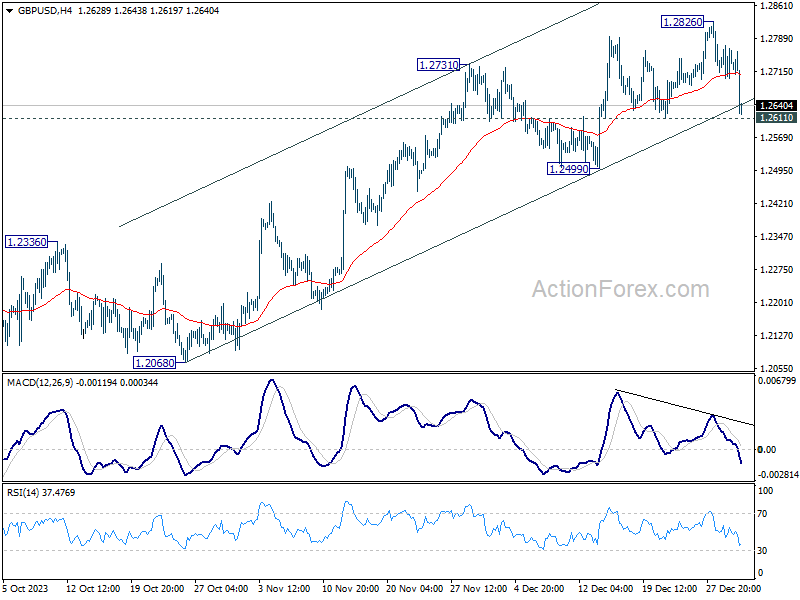

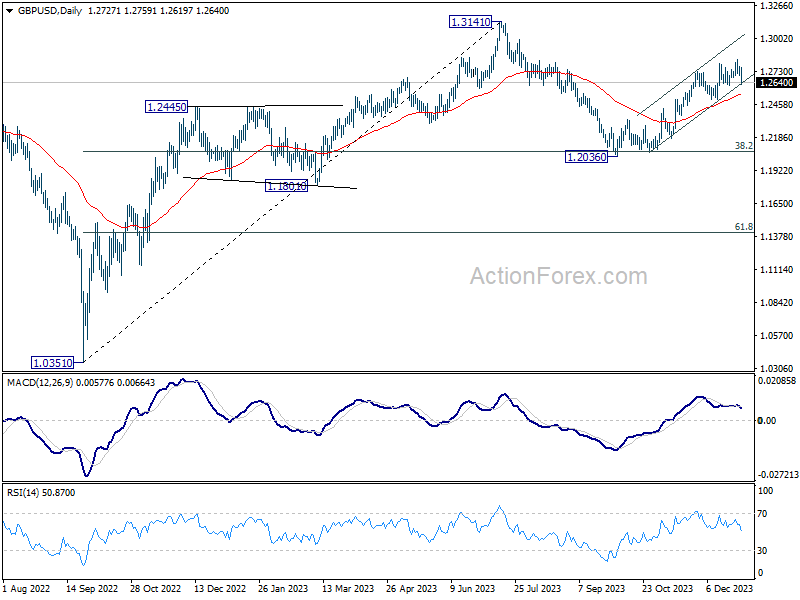

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2698; (P) 1.2735; (R1) 1.2770; More...

While GBP/USD's pull back from 1.2826 extends lower today, it's staying above 1.2611 support so far. Intraday bias remains neutral first. On the upside, break of 1.2826 will resume whole rally from 1.2036. However, break of 1.2611 will indicate short term topping, and turn bias back to the downside for 1.2499 support.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to rise from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

British Pounds Takes a Tumble on Soft Mfg. PMI

The British pound has started the New Year with sharp losses. In the North American session, GBP/USD is trading at 1.2626, down 0.82%.

UK Manufacturing PMI eases lower

The UK manufacturing sector remains in the doldrums. December’s Manufacturing PMI eased to 46.2, below the consensus of 46.4 and shy of the November reading of 47.2, which was a seven-month high. Manufacturing production has now declined for ten straight months. The December decline was driven by weaker demand abroad for UK goods and less optimism from manufacturers about business conditions. The weak UK economy and high borrowing costs continue to dampen manufacturing activity, with no signs that the New Year will bring better tidings.

The UK releases Services PMI on Thursday. The services sector is in better shape than manufacturing although the PMI posted three consecutive declines late in the year. The c consensus for December stands at 52.7, which would indicate slight expansion.

In the US, the markets are in a cheery mood on expectations that the Federal Reserve will start to trim interest rates as soon as March. The Fed surprised the markets at the December meeting when it didn’t push back against rate-cut expectations. Fed Chair Powell signalled that the Fed expected to cut rates three times in 2024, less than the market’s forecast of up to six cuts but more than the two cuts the Fed signalled in September.

The markets have celebrated the apparent end of the rate-tightening cycle, with equities rising and the US dollar retreating. Investors will be keeping a close look at the FOMC minutes on Wednesday, looking for further insights into the Fed’s dovish pivot on rate policy.

GBP/USD Technical

- There is resistance at 1.2753 and 1.2807

- GBP/USD pushed below support lines at 1.2678 and 1.2624 earlier. Below, there is support at 1.2549

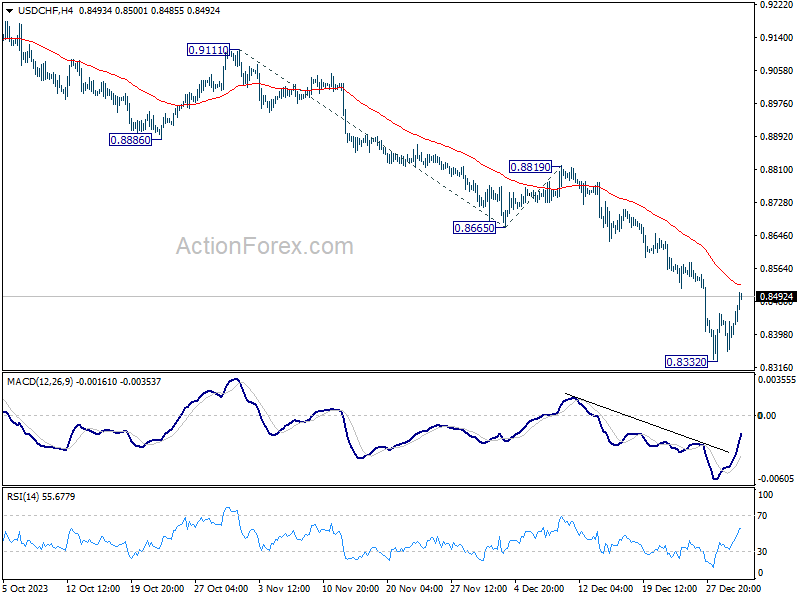

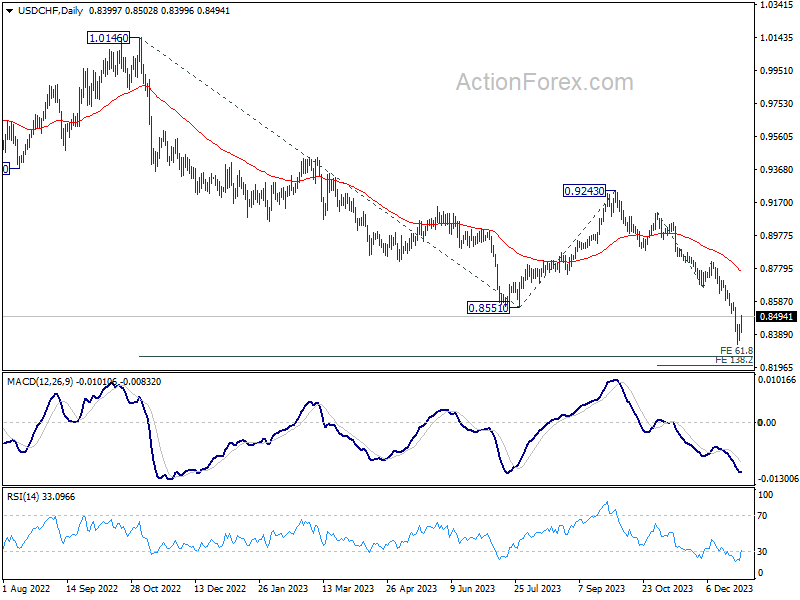

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8363; (P) 0.8409; (R1) 0.8462; More....

Intraday bias in USD/CHF remains neutral for consolidation above 0.8332. While stronger recovery cannot be ruled out, outlook will stay bearish as long as 0.8665 support turned resistance holds. Break of 0.8332 will resume larger fall from 0.9243 to 138.2% projection of 0.9111 to 0.8665 from 0.8819 at 0.8203 next.

In the bigger picture, break of 0.8551 support indicates resumption of whole decline from 1.0146 (2022 high). Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

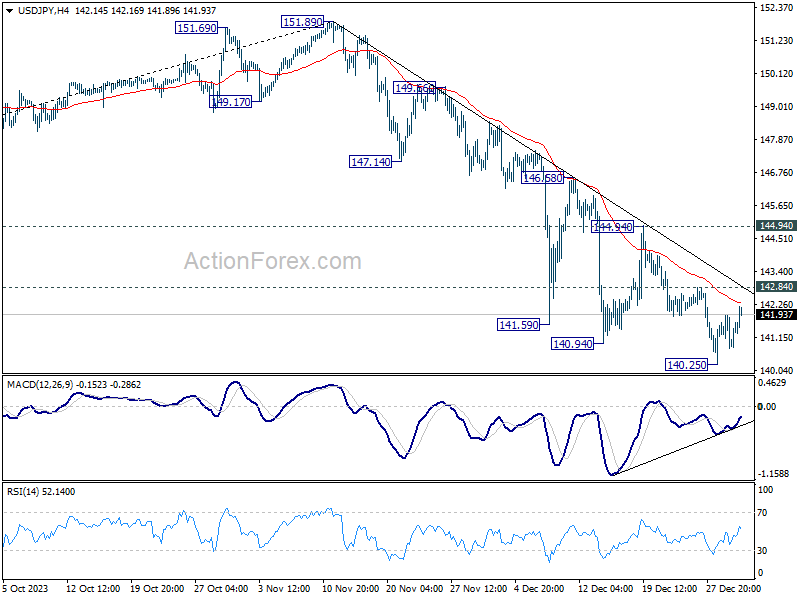

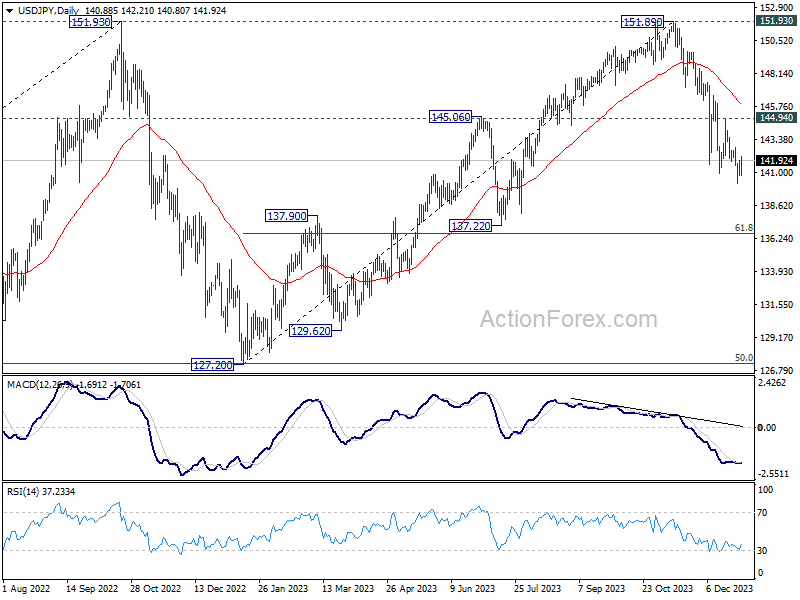

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 140.58; (P) 141.25; (R1) 141.69; More...

Intraday bias in USD/JPY is turned neutral as recovery from 140.25 extends. Further decline will remain in favor as long as 142.84 minor resistance holds. Break of 140.25 will resume fall from 151.89 and target 136.63 fibonacci level. Nevertheless, break of 142.84 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 144.94 resistance holds.

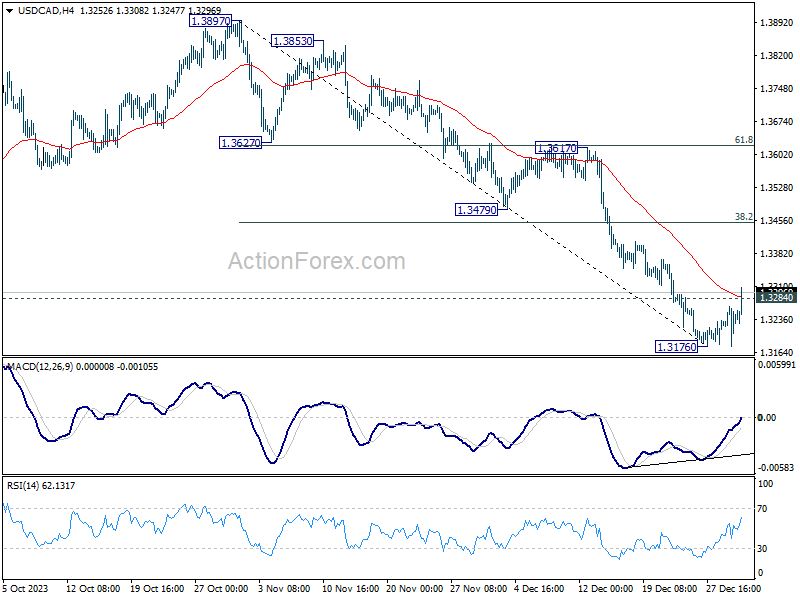

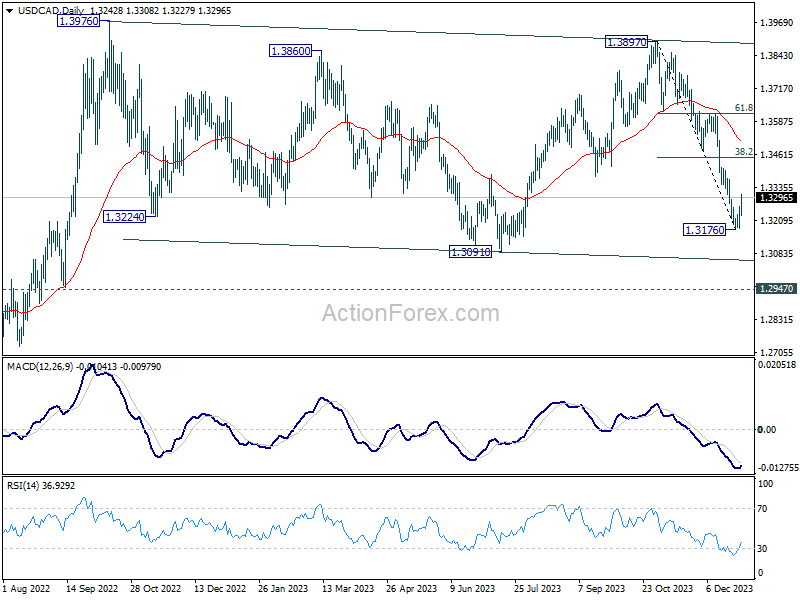

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3196; (P) 1.3230; (R1) 1.3283; More...

USD/CAD's break of 1.3284 minor resistance indicate short term bottoming at 1.3176, on bullish convergence condition in 4H MACD. Intraday bias is back on the upside for 38.2% retracement of 1.3897 to 1.3176 at 1.3451. On the downside, however, break of 1.3176 will resume the fall from 1.3897 to 1.3091 support and possibly below.

In the bigger picture, outlook is mixed up by deeper then expected fall from 1.3897. But after all, price actions from 1.3976 (2022 high) are viewed as a corrective pattern that's in progress. Larger up trend from 1.2005 (2021 low) is still expected to resume at a later stage as long as 1.2947 resistance turned support holds.

Dollar Gains Momentum as 2024 Begins with Global Equities Selloff

As US session commences, Dollar's rebound is gaining additional momentum. This upswing is occurring against a backdrop of intensifying selloff in the equities market, primarily influenced by Apple's downturn following downgrade by Barclays over concerns of weakening sales.

European majors are currently bearing the brunt of the market's shift. The final PMI manufacturing release from S&P Global has fueled this sentiment, suggesting that Eurozone may have already slipped into a recession in the third quarter. This perspective is further compounded by downward revision of UK's PMI manufacturing figures, indicating continued strain on these economies.

In the broader currency markets, Japanese Yen is also showing weakness, a situation likely exacerbated by the powerful earthquake in Japan. This natural disaster has impacted the market at a time when the Japanese stock market remains closed for a public holiday. On the other hand, Canadian and Australian Dollars are showing mild firmness, trailing behind the strengthening greenback.

From a technical analysis perspective, as Dollar's rebound extends, key levels to watch are 1.0929 minor support in EUR/USD and 1.2611 minor support in GBP/USD. Firm breaks below these levels could signify that Dollar's rebound is poised to continue further, potentially until the release of non-farm payroll report on Friday.

In Europe, at the time of writing, FTSE is down -0.45%. DAX is down -0.46%. CAC is down -0.67%. Germany 10-year yield is up 0.0805 at 2.089. UK 10-year yield is up 0.141 at 3.680. Earlier in Asia, Hong Kong HSI fell -1.52%. China Shanghai SSE fell -0.43%. Singapore Strait Times fell -0.32%. Japan was on holiday.

UK PMI manufacturing finalized at 46.2, 17th month of contraction

UK PMI Manufacturing was finalized at 46.2 in December, down from November's 47.2. This marks the seventeenth consecutive month where the index has remained below the neutral 50 threshold, indicating ongoing contraction. According to S&P Global, key aspects such as output, new orders, and employment are all in decline. Additionally, business optimism has reached a 12-month low.

Rob Dobson, Director at S&P Global Market Intelligence, pointed out demand environment remains challenging, with new orders continuing to decline due to difficult conditions in both domestic and key export markets, particularly the European Union.

The downturn is prompting companies to adopt a more cautious approach to costs. There have been notable cutbacks in stock levels, purchasing, and employment as firms grapple with the ongoing challenges.

Eurozone's PMI manufacturing finalized at 44.4, relentless slump continues

Eurozone's PMI Manufacturing was finalized at 44.4 in December, up slightly from November's 44.2. Despite this minor uptick, marking a seven-month high, the index remained below the critical 50.0 threshold, signaling a continued deterioration in operating conditions across the sector.

Country-by-country breakdown of Manufacturing PMI reveals a diverse picture. Greece stands out with a PMI of 51.3, indicating expansion and marking a four-month high. In contrast, other major economies like Ireland, Spain, Italy, the Netherlands, Germany, France, and Austria all recorded PMIs indicative of contraction, with varying degrees of severity. Notably, France registered a PMI of 42.1, a 43-month low. On the other hand, Germany rose to an 8-month high at 433.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, remarked on the "relentless slump" in Eurozone's manufacturing sector, noting that the marginal improvement in the PMI does little to alleviate concerns about the persistent decline in activity and demand for manufactured goods. The consistent sluggishness in new orders was particularly alarming, reflecting a pervasive gloom across the sector.

According to HCOB's Nowcast model anticipates a contraction in the Eurozone's GDP for the fourth quarter. This projection, if realized, indicates that Eurozone may have already entered a recession as early as the third quarter.

China's Caixin PMI manufacturing rises, as NBS PMI shows contraction

December brought mixed signals from China's manufacturing sector, as indicated by two key indices: Caixin PMI and official NBS PMI. Caixin PMI Manufacturing slightly increased from 50.7 to 50.8, surpassing expectations of 50.4, suggesting a marginal yet steady expansion in the manufacturing sector. Notably, Caixin highlighted that both output and new orders are rising at faster rates, indicating increased production and demand within the industry.

However, the same period saw a dip in official PMI Manufacturing, which fell from 49.4 to 49.0. This decline suggests contraction in the sector, contrasting with optimism reflected in Caixin PMI data. The difference between these two indices can be attributed to their varied focus groups; Caixin PMI typically surveys small and medium-sized enterprises, while NBS PMI is more reflective of larger, state-owned companies.

Wang Zhe, Senior Economist at Caixin Insight Group, emphasized the improved economic outlook for the manufacturing sector, with expanding supply and demand, and stable price levels. Yet, he also pointed out significant challenge in employment, highlighting businesses' cautious approach in areas like hiring, raw material purchasing, and inventory management.

On the other hand, NBS PMI Non-Manufacturing showed a slight improvement, rising from 50.2 to 50.4. This marginal increase suggests a modest expansion in China's services sector.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3196; (P) 1.3230; (R1) 1.3283; More...

USD/CAD's break of 1.3284 minor resistance indicate short term bottoming at 1.3176, on bullish convergence condition in 4H MACD. Intraday bias is back on the upside for 38.2% retracement of 1.3897 to 1.3176 at 1.3451. On the downside, however, break of 1.3176 will resume the fall from 1.3897 to 1.3091 support and possibly below.

In the bigger picture, outlook is mixed up by deeper then expected fall from 1.3897. But after all, price actions from 1.3976 (2022 high) are viewed as a corrective pattern that's in progress. Larger up trend from 1.2005 (2021 low) is still expected to resume at a later stage as long as 1.2947 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:01 | GBP | BRC Shop Price Index Y/Y Nov | 4.30% | 4.30% | ||

| 01:45 | CNY | Caixin Manufacturing PMI Dec | 50.8 | 50.4 | 50.7 | |

| 08:45 | EUR | Italy Manufacturing PMI Dec | 45.3 | 44.4 | 44.4 | |

| 08:50 | EUR | France Manufacturing PMI Dec F | 42.1 | 42 | 42 | |

| 08:55 | EUR | Germany Manufacturing PMI Dec F | 43.3 | 43.1 | 43.1 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Dec F | 44.4 | 44.2 | 44.2 | |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Nov | -0.90% | -1% | -1% | |

| 09:30 | GBP | Manufacturing PMI Dec F | 46.2 | 46.4 | 46.4 | |

| 14:30 | CAD | Manufacturing PMI Dec | 47.7 | |||

| 14:45 | USD | Manufacturing PMI Dec F | 48.2 | 48.2 | ||

| 15:00 | USD | Construction Spending M/M Nov | 0.60% | 0.60% |

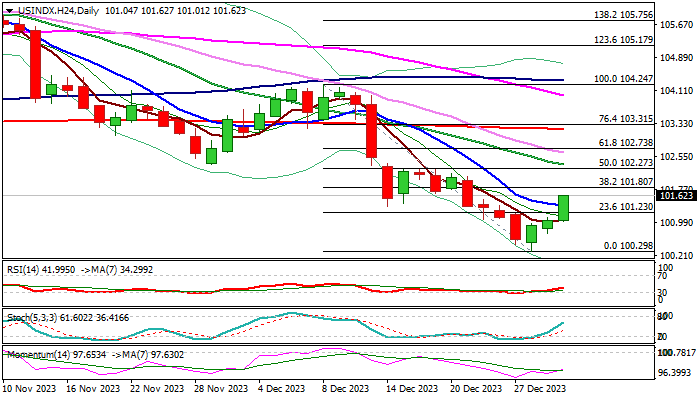

Dollar Index: EU Inflation and US Labor Reports Eyed for Fresh Signals

The dollar index accelerated higher on the first trading day in 2024, extending bounce from five-month low of Dec 28 (100.30) into third consecutive day.

Traders collected some profits from the broader downtrend, pushing the dollar’s price higher and sidelining immediate downside threats, as focus shifts to EU inflation data and US labor report, due to be released later this week and expected to provide more clues about next steps of two central banks.

Larger picture shows the dollar index in a downtrend, with current move higher seen as correction which should provide better selling opportunities.

Fresh bulls eye pivotal barrier at 101.80 (Fibo 38.2% of 104.24/100.30), with strong 101.20/30 resistance zone (base of thick weekly Ichimoku cloud/50% retracement) expected to cap upticks and keep larger bears intact.

Daily technical studies are predominantly bearish (strong negative momentum/MA’s in bearish setup) supporting the notion of limited correction preceding fresh push lower for attack at psychological 100 support and 2023 lows at 99.24/20.

Res: 101.80; 102.20; 102.35; 102.73.

Sup: 101.38; 101.23; 100.73; 100.30.

Euro Extends Losses after Weak PMIs

- Euro slips below 1.10 line

- German and eurozone manufacturing PMIs contract

The euro is down sharply on Tuesday. In the European session, EUR/USD is trading at 1.0969, down 0.62%. The euro hasn’t posted a gain since Wednesday.

The US dollar has hit a rough patch on market expectations that the Federal Reserve will cut rates up to six times this year and that the current rate-tightening cycle is over. The euro has pummelled the US dollar since November 1, falling 5.3%.

German and eurozone Manufacturing PMIs remain in decline

The New Year started with manufacturing releases from Germany and the eurozone earlier today. German manufacturing PMI was revised to 43.3 in December from a preliminary 43.1, compared to 42.6 in November and above the consensus of 43.1. The Eurozone Manufacturing PMI was also revised upwards to 44.4, up from 44.2 in the preliminary estimate and above the consensus of 44.2. The manufacturing sector in Germany and the eurozone is mired in a prolonged slump and hasn’t shown growth since June 2022. There isn’t much to cheer about but there is hope that the worst of the downturn is behind us as we move into 2024.

Germany and the eurozone will post their inflation reports on Thursday. Last week, Spain posted lower-than-expected inflation numbers. Inflation has eased to 3.2% in Germany and 2.4% in the eurozone, as the ECB’s target of 2% is getting closer. If the data shows that inflation eased in Germany and the eurozone as well, it will put pressure on the European Central Bank to cut rates in the first half of 2024.

ECB President Lagarde has pushed back against rate cuts but she may have to shift her hawkish stance or risk tipping the weak eurozone economy into a recession. If the upcoming inflation reports indicate that inflation continues to fall, we can expect the voices in the ECB calling for looser policy to get louder.

EUR/USD Technical

- There is resistance at 1.1069 and 1.1102

- 1.0958 and 1.0887 are the next support lines