Sample Category Title

Weekly Economic & Financial Commentary: A Win for the Doves

Summary

United States: Consumers Maintain Spending Power Amid Slowing Price Growth

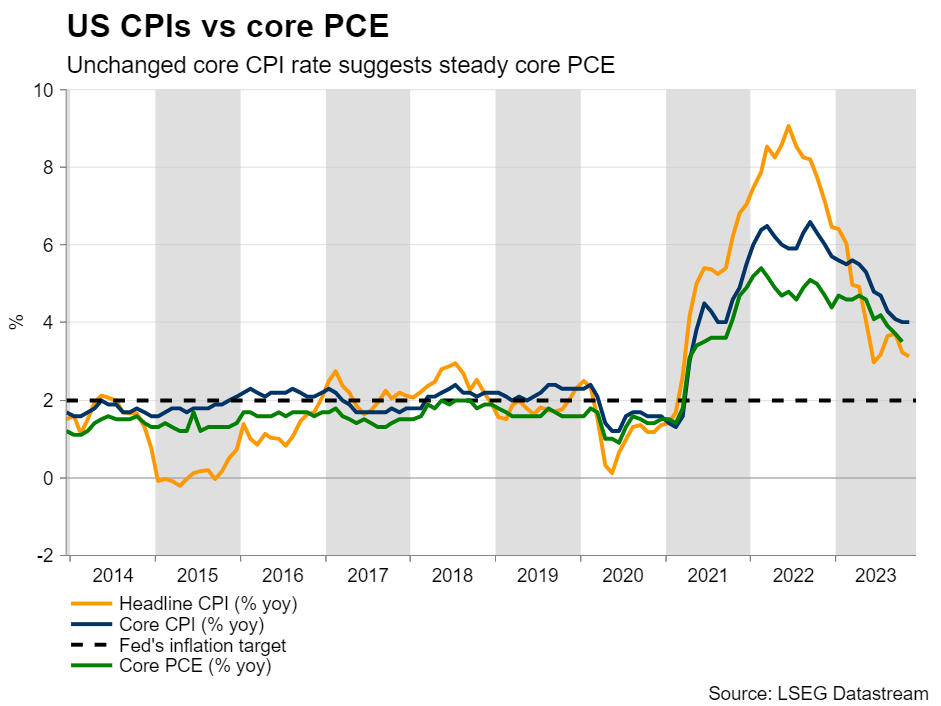

- Data released this week revealed that gradually easing price pressures are promoting consumer resilience, while high financing costs continue to bite producers. Although core CPI remained elevated in November at a 4.0% annual rate, a string of slower monthly prints suggests that disinflation has more room to run.

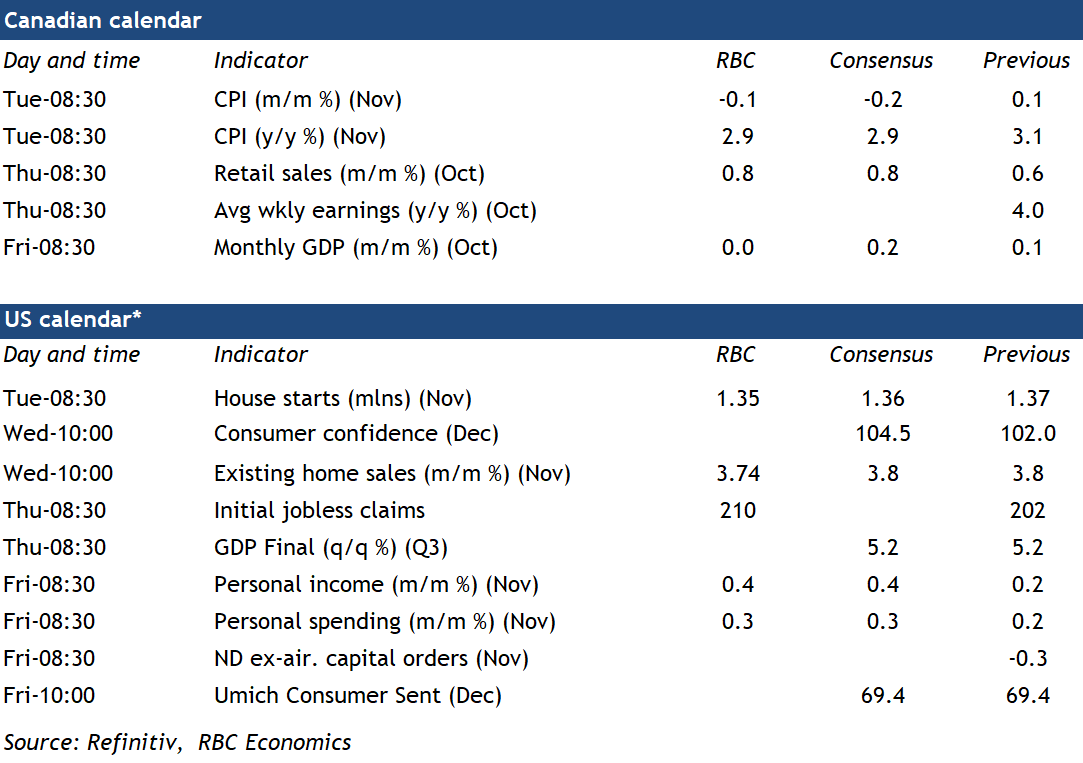

- Next week: Existing Home Sales (Wed.), LEI (Thu.), Personal Income & Spending (Fri.)

International: G10 Central Bank Focus Shifting from Rate Hikes to Rate Cuts

- G10 central banks are in the process of transitioning from rate hikes to rate cuts, with the European Central Bank, Bank of England and the Swiss National Bank holding rates steady this week. In Japan, a relatively sturdy Q4 Tankan survey pointed to a resumption in economic growth. Last, China's latest economic data suggest its economy will end the year on a stable note rather than a strong one.

- Next week: Bank of Japan Policy Rate (Tue.), Colombia Overnight Lending Rate (Tue.), U.K. Consumer Price Index (Wed.)

Interest Rate Watch: A Win for the Doves

- As widely expected, the FOMC left the fed funds target range unchanged at 5.25%-5.50% in a unanimous vote. The decision marked the third consecutive meeting that the Committee held policy steady. While the rate decision came as no surprise, this week's meeting shaped up to be one of the clearest messages yet that the torrid hiking cycle that began in March 2022 has come to an end.

Topic of the Week: The Fiscal Tailwinds Are Still Blowing

- Government hiring and output have accelerated this year even as indicators of private sector economic activity have shown some signs of slowing. In a report published earlier this week, we examined the recent pickup in public sector payroll and production growth and analyzed the outlook for this sector of the economy in 2024 and beyond.

The Weekly Bottom Line: Cuts! The Herald Angels Sing

U.S. Highlights

- The Federal Reserve held the policy rate steady at 5.25-5.5% at its final interest rate announcement of the year.

- However, a markdown in the FOMC’s interest rate projections and little pushback from Chair Powell in the press conference on the recent pull-forward in rate cut timing pressured yields across the curve significantly lower.

- However, with inflationary pressures accelerating in November and retail sales holding up much better than expected through the first month of the holiday shopping season, markets may be getting a bit ahead of themselves expecting rate cuts so soon.

Canadian Highlights

- Shifting central bank tone has given investors an early Christmas present, setting off a Santa Claus rally in both equity and bond markets.

- The real estate market continues to lead Canada’s economic slowdown. Housing sales, prices, and starts all declined, as mortgage rates remain at elevated levels.

- Next week we get a fresh release of Canadian inflation, which is expected to show another deceleration on the back of falling gasoline prices.

U.S. – December FOMC Announcement Comes With ‘Dovish Undertones’

Volatility in the U.S. Treasury market has been a key theme over the past year. This has largely been driven by market participants repeatedly pulling-forward rate cut expectations, only to be reined in by a more cautious Fed concerned of the asymmetric risks of stopping short. That dance is again underway, with markets pulling forward their bets on the timing of the first rate cut to Q1-2024 and pricing for five 25 basis-point (bp) cuts over the course of next year. The only difference this time is policymakers seem less perturbed by the change in view.

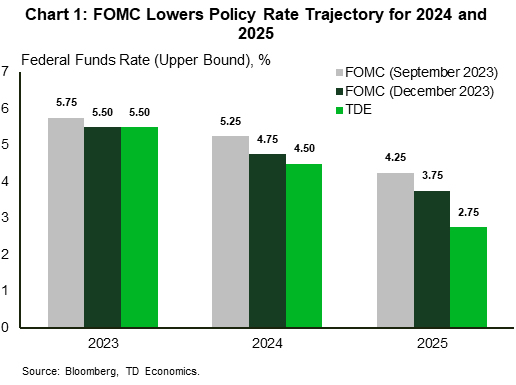

At its final interest rate announcement of the year, the Federal Reserve held the policy rate steady at a range of 5.25%-5.5%. However, both the accompanying statement and the refreshed economic projections had ‘dovish’ undertones. Tweaks to the Fed’s statement suggested that while further tightening remains possible, it’s becoming less probable. This point was reaffirmed in the updated economic projections, which showed 75 bps of rate cuts in 2024 (previously 50 bps), followed by another 100 bps of easing in 2025 (Chart 1). The additional cuts were supported by a more benign inflation outlook, with the FOMC lowering its 2023 and 2024 core PCE forecast to 3.2% (previously 3.7%) and 2.4% (previously 2.6%), respectively. Meanwhile, the 2024 projections for GDP (1.4%) and the unemployment rate (4.1%) were little changed.

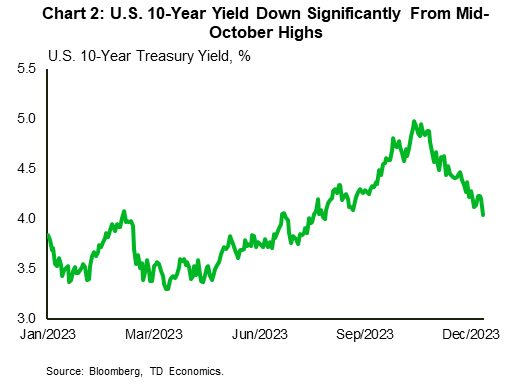

During the press conference, Fed Chair Powell had multiple opportunities to push back on the recent re-pricing in market expectations, but instead opted to play it down the middle. Up until this week, the FOMC had remained emphatic that talks of rate cuts were ‘premature’. However, during the press conference, Powell noted that Committee members were now in the “early stages of that loosening discussion”. Investors used the messaging as reaffirmation of its view of earlier rate cuts, which fueled a rally in equities and put further downward pressure on Treasury yields. At the time of writing, the 10-year yield is down 30 bps for the week and at 3.93%, is now over 100 bps below its cyclical high of 5% reached back in mid-October (Chart 2).

We remain of the view that market pricing has gotten a bit ahead of itself. Data out this week showed that the consumer is still holding up reasonably well, while further progress on the inflation front is likely to come more slowly. Indeed, the November reading of CPI showed an acceleration in core inflation, as continued declines in goods prices were more than offset by stronger service-side price pressures.

While we did see considerable breadth in the number of goods categories showing price declines, further downward pressure seems limited. Retail sales data for November showed demand holding up better than expected through the busy holiday shopping season. Moreover, with spending still tracking a healthy 2.5% for the fourth quarter, retailers will hardly feel pressed to extend recent discounts. This means a further loosening in the labor market will be required to cool demand and maintain further downward pressure on inflation. From that perspective, Fed officials are unlikely to get the confirmation they need to begin easing the policy rate until mid-2024.

Canada – Cuts! The Herald Angels Sing

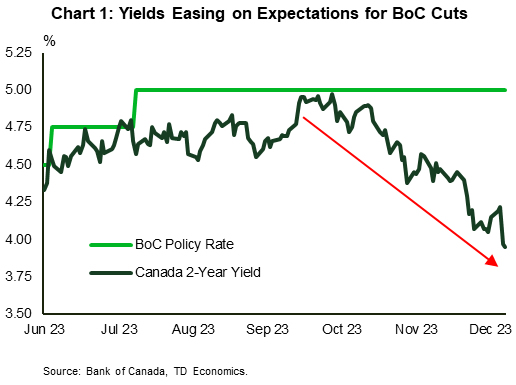

Central banks have given investors an early Christmas present. With economic momentum fading and inflation decelerating more decisively, central banks' tone has shifted dramatically. The higher for longer narrative is being dampened, with expectations for policy rate cuts coming into greater focus (Chart 1). This has set off a Santa Claus rally in both equity and bond markets.

Evidence of Canada's slowing economy keeps coming in. Real estate has been front and center, leading the decline ever since the Bank of Canada (BoC) hiked rates in June and July. Existing home sales data this week showed another drop in sales and prices, leaving resale activity down by 17% from the spring 2023 peak and causing a near 7% correction in house prices. This likely spurred November's big 22% drop in new housing starts data released Friday. The outlook over the next few months doesn’t look favourable either. Mortgage rates have come off their highs, but they are still at elevated levels. And it won't be until the BoC starts to cut rates before we are likely to see a meaningful upturn in housing activity.

The economic slowdown is also coming through in consumer spending. As we highlighted in our note last week, mortgage holders are paring back spending as more borrowers renew/reset at higher interest rates. Household financial data out this week showed that consumers are now allocating a record amount of their income to pay their debts. This is a key reason why consumer spending per capita has been on the decline for most of 2023. Don't expect things to get much better. We find that mortgage holders who are set to renew in 2024 have yet to adjust their spending significantly. If borrowing rates don't come down quickly, expect further weakness in consumer spending.

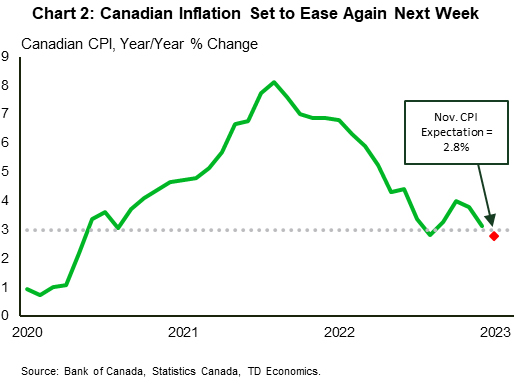

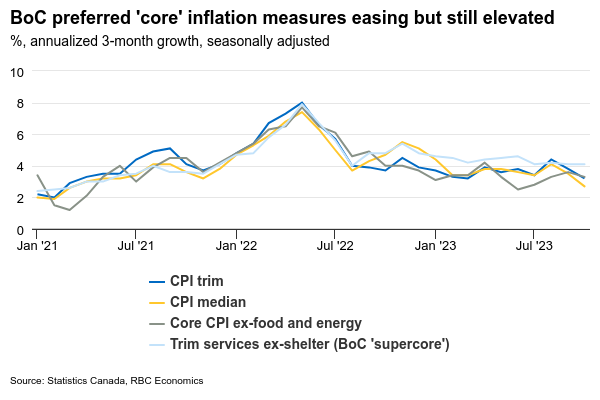

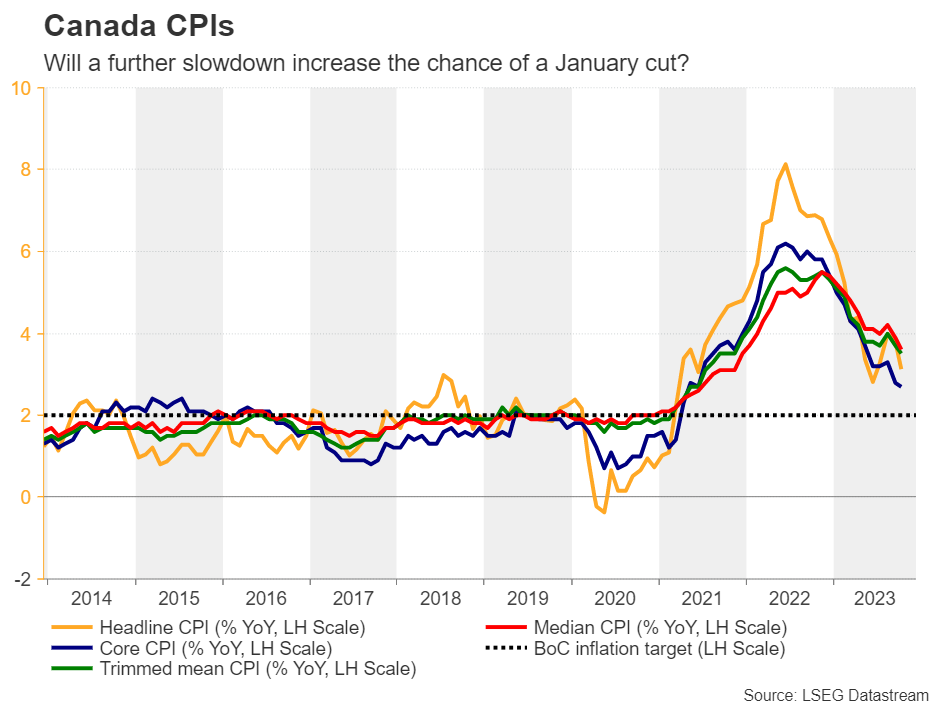

Softer consumer demand has started to force greater discounting amongst retailers. Prices have been cut significantly for goods tied to real estate (furniture and appliances), and now we are seeing discounting for flights and hotels. At the same time, consumers have got some relief from lower gasoline prices. We will get another reading on inflation with the release of Canadian CPI for November next week. We are expecting headline inflation to decelerate again, reaching 2.8% year-on-year (y/y) in November (Chart 2). Importantly, this would bring inflation back into the BoC's 1% to 3% target range.

Easing headline inflation will certainly encourage the BoC, but it will need to see follow through on core inflation. The average of the BoC's core measures is running at 3.6% y/y, which is being driven by services inflation. Employee wage gains are still rolling at close to 5% y/y, so it is no surprise that services inflation has been running at effectively that same rate (4.6% y/y). The Bank will want to see further weakening in the labour market, which should slow the pace of wage gains and raise confidence that core inflation rates will decelerate more decisively going forward. We expect this to occur in early 2024, which would allow the BoC to execute on rate cuts by the spring.

Canadian CPI to Edge Back Below 3% in November

We expect Canadian inflation pressures to have moderated more in November. Headline inflation is expected to have dropped to 2.9% from 3.1% in October reflecting a pullback in retail gasoline prices and further easing in food price growth. That would mark the second time since March 2021 that the reading dips back within Bank of Canada’s 1%-3% target range for inflation after what has been a drawn-out fight between the central bank and very sticky domestic price pressures. We expect price growth excluding food and energy products stayed at 3.4% year-over-year in November, driven by higher shelter costs – more than a third of the rise in ex-food & energy prices in Canada as of October came from mortgage interest costs as higher interest rates continue to flow through to household debt payments with a lag. Both BoC’s preferred core measures – CPI trim and CPI median are also expected to have eased again in November, extending improvements seen in the prior month.

Slowing inflation is following a string of soft economic growth data that we expect also extended into Q4. Canadian GDP has already declined for 5 consecutive quarters on a per-capita basis with Q4 likely to stretch that run to 6. Statistics Canada’s preliminary estimate was that October GDP rose 0.2% month-over-month, but we expect data released since then to point to a softer flat reading. October retail sales appear to have increased, and our own tracking of data of early holiday spending also looked firm in November. But manufacturing and wholesale sale volumes both pulled back (-2.2% and -0.7%, respectively) and total hours worked in October were unchanged before dropping 0.7% in November. We continue to track a small contraction in total GDP in Q4 that will again suggest a bigger decline on a per-capita basis once controlling for still-rapid population growth.

Further softening in the economic backdrop and slower price growth should reinforce that the BoC is done hiking interest rates for this cycle. We don’t expect a pivot to rate cuts right away – central banks will be cautious about declaring victory over inflation too early. We see the BoC to start the easing cycle around the middle of 2024.

Week ahead data watch

November U.S. personal spending likely edged up 0.3% from the prior month, matching retail sales growth in that month. Excluding motor vehicles, sales edged up 0.2%. We look for the U.S. personal income to grow at a faster 0.4% pace in November given a firm round of November labour market data.

StatsCan’s advance estimate showed October retail sales went up by 0.8%, auto sales increased by 1.2% for that month, but that growth was partially offset by a price-related sales decline at gas stations.

Next week’s October SEPH data will be closely watched for more easing in the labour market conditions. We expect job openings will continue to edge lower as separately released LFS showed that the unemployment rate persistently edged higher.

Bank of Japan Meeting: Another Baby Step to Exiting Negative Rates?

- Despite heightened rate hike speculation, BoJ to likely stand pat in December

- No change is anticipated either in yield curve control

- But yen traders will be seeking fresh clues in Tuesday’s announcement

BoJ still to join the rate hike club

The Bank of Japan is the only major central bank that has not yet raised interest rates, as despite inflation running above its 2% target for the past one-and-a-half years, Japan has yet to be declared free of deflation.

Policymakers are keen to see domestically fuelled price pressures like wage growth replacing external drivers such as last year’s energy price shock to be convinced that the inflation rate can be sustained above 2%. Whilst there have been plenty of encouraging signals from the data, there’s yet to be anything conclusive to suggest that inflation has made a permanent comeback in Japan.

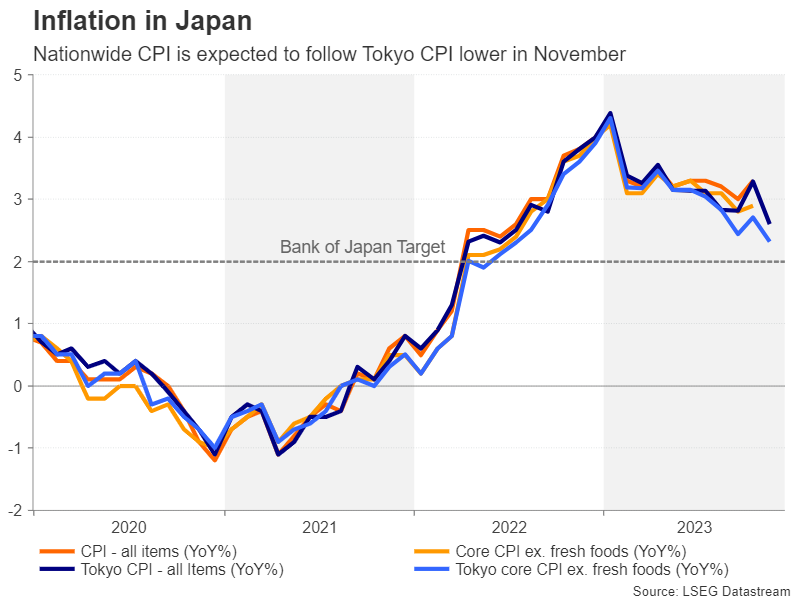

The consumer price index ticked up to 3.3% y/y in October but if the Tokyo CPI numbers, which are leading indicators, are to be believed, the nationwide readings due on Friday likely moderated in November. The GDP data is another one not going in the BoJ’s favour. The Japanese economy contracted more than expected in the third quarter, raising question marks about its strength just as the BoJ is considering exiting negative interest rates.

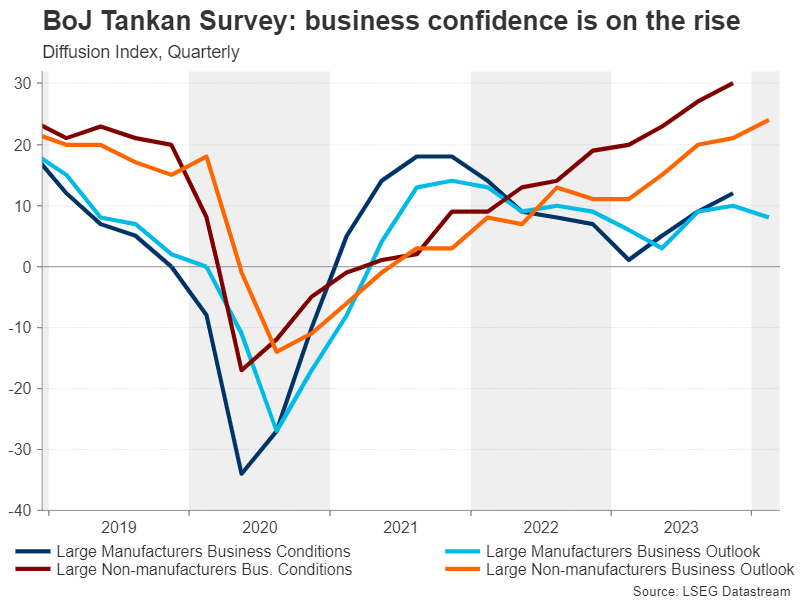

Consumers are spending less but businesses are upbeat

Much of the weakness is down to sluggish household spending. Consumption has fallen sharply in the past two quarters as household budgets have been squeezed by rising prices. It’s an entirely different story for corporate Japan, however, as businesses have been benefiting from the favourable exchange rate that’s seen the yen slump to levels last seen in 1990. Optimism among large Japanese firms has been going from strength to strength this year.

But the outlook is far from clear. The yen’s fortunes have started to change now that the Fed has opened the door to rate cuts and the BoJ is on the verge of scrapping negative rates. Moreover, growth in all the major economies is slowing, thus, this optimism may not last very long.

On the other hand, the Japanese government recently announced a large stimulus package aimed at easing the pain of high inflation on households, so a turnaround in consumer spending is possible in the coming months.

Waiting for the elusive wage acceleration

The muddied economic picture may complicate matters for policymakers, but ultimately, the BoJ will likely base its decision on whether to exit stimulus on what happens to wages. To this effect, next year’s spring wage negotiations will be crucial. Early signs of where the latest round of pay deals are headed are promising.

If the BoJ is satisfied with the outcome, there could be liftoff by April, even if all the other pieces of the jigsaw don’t quite fit properly. The Bank likely recognizes that this may be its best and only opportunity to end the highly unpopular policy of negative rates once and for all.

Will the BoJ give up control of the yield curve?

But what happens to yield curve control (YCC) policy is somewhat less straightforward. Although the BoJ significantly loosened its grip on the yield curve in October when it raised the upper bound of the 10-year yield target to 1.0%, it will probably not want to abandon YCC policy entirely so as to be able to prevent sudden moves in yields.

For investors, however, the immediate priority is the timing of any big policy shift. Some traders are speculating that the BoJ will hike rates as early as the December meeting, if not, in January. A 10-basis-point hike is not fully priced in until June so the consensus view seems to be that the BoJ will remain patient. With sovereign bond yields globally taking a dive lately, there’s also less pressure on policymakers to make any further tweaks to their YCC policy.

Yen on standby for policy hints

Yet, the rhetoric from Governor Ueda suggests some bias towards normalizing policy. Given the BoJ’s history to shock the markets, the risk of a surprise decision in January to either hike rates or end YCC, or both, cannot be dismissed.

However, such a risk is very low for the December meeting so much of the reaction in the markets will depend on any changes in Ueda’s language. Any clues that a rate increase is on the way in early 2024 could fuel the US dollar’s selloff against the Japanese currency.

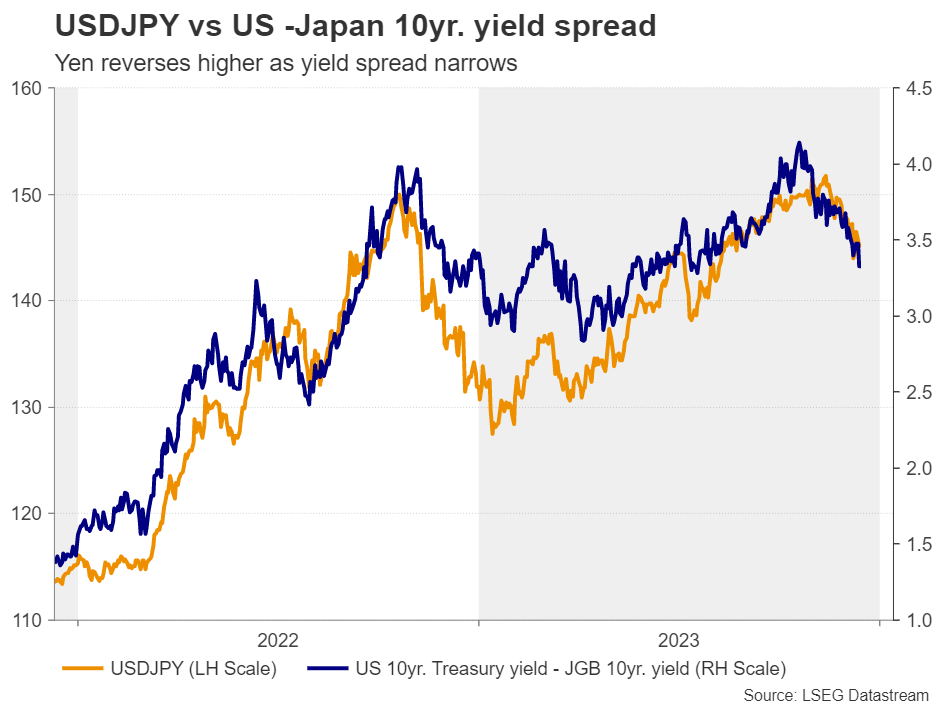

Dollar/yen could extend its slide to the 61.8% Fibonacci retracement of the January-November uptrend at 136.65, which is near where prices troughed in July.

But if the BoJ disappoints by not altering much in its statement and Ueda gives little away in terms of fresh hints on the timing of a possible exit, dollar/yen could stage a rebound. Any upside could initially target the 23.6% Fibonacci of 146.09 before aiming for the 50-day moving average at 148.87.

Week Ahead – BoJ Meets for the Last Time in 2023, US Core PCE and UK CPIs Also On...

- Yen traders await BoJ decision for pivot clues

- US core PCE index the highlight of the US agenda

- UK CPI numbers to be the pound’s next test

- Loonie and aussie await Canada’s CPIs and RBA minutes

Will BoJ policymakers hint at the end of negative rates?

Following a barrage of central bank decisions this week the end credits of major monetary policy decisions for 2023 will roll with the BoJ during the Asian session Tuesday. At their last meeting, policymakers decided to allow 10-year JGB yields to rise above 1%. However, they did not ditch the cap. They just redefined it from a rigid ceiling to a reference bound, meaning they could intervene in the bond market again if deemed necessary. And indeed, this is what they did the day after the decision.

This disappointed investors that were expecting more, with the yen tumbling in the aftermath and the following days, with dollar/yen almost touching its October 2022 high of 151.94 on November 13. That said, it was all downhill thereafter with the fall steepening on December 7 as Governor Ueda talked about the possible options they have on interest-rate targeting once they end their negative interest rate policy.

However, just the next couple of days, two reports hit the wires, saying that his comments were not intended to hint at a potential exit timing and that the Bank sees the cost of waiting for more information as not very high. With that in mind and given the emphasis the BoJ puts on wage growth, policymakers may not opt for an imminent shift at this gathering and perhaps wait for April, after the spring wage negotiations.

That doesn’t mean the meeting will pass totally unnoticed. Yes, Japan’s GDP data revealed that the economy contracted by more than anticipated in Q3, but the National CPIs revealed that inflation continued to accelerate in October which increases the likelihood for businesses and labor unions to agree on another round of strong pay hikes next year. Thus, even the slightest indication that interest rates could exit negative territory in April may add more fuel to the yen’s engines, especially with the market believing that the Fed will cut interest rates by around 150bps next year.

After dovish Fed, dollar traders lock gaze on core PCE index

Speaking about the Fed, it left interest rates unchanged as expected this Wednesday, but revised down its dot plot to indicate that interest rates will end 2024 at 4.6% instead of 5.1% as projected in September. Powell appeared dovish at the press conference following the decision, saying that higher rates “is not the base case anymore.” The outcome pushed Treasury yields and the US dollar lower, while it was cheered by equity and gold traders.

The highlight on the US agenda next week may be the core PCE index for November, the Fed’s favorite inflation gauge, which comes out on Friday alongside the personal income and spending data for the month. On Tuesday, the core CPI rate for the month remained unchanged at 4.0% y/y suggesting that the core PCE price index may have also held steady at 3.5%. This is unlikely to shake expectations regarding the Fed’s future course of action, but a miss could encourage investors to continue selling the dollar and buying stocks. On the other hand, an upside surprise may trigger a counter move, but a mild one, as market participants appear willing to react more to data and headlines validating their view.

Will UK inflation alter the BoE’s thinking?

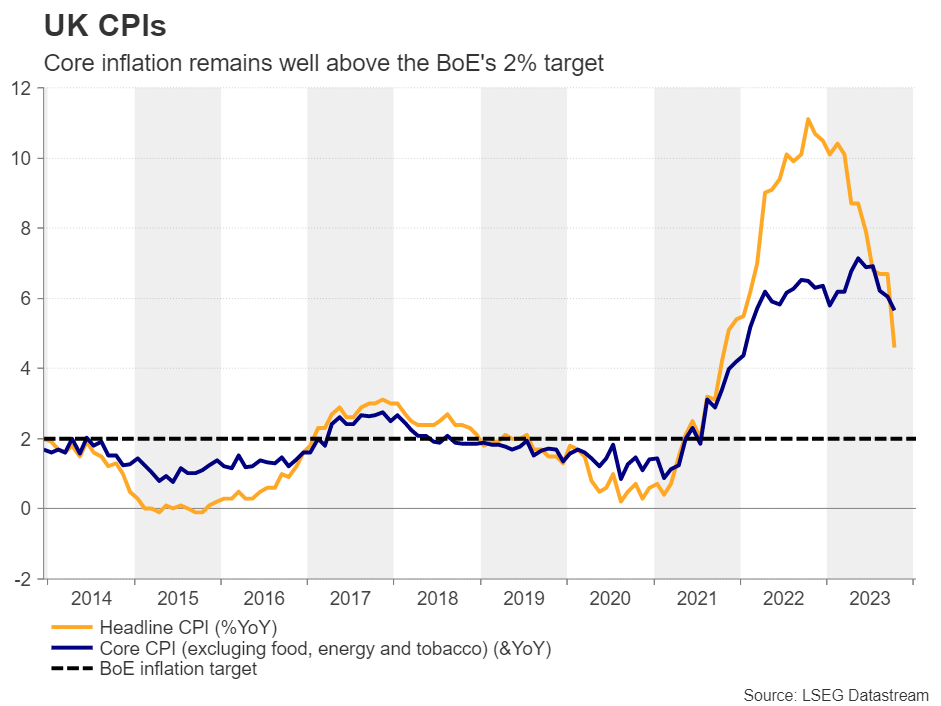

For pound traders, after the BoE’s hawkish hold, attention will now turn to the UK inflation data for November, due to be released on Wednesday. Although slowing, inflation in the UK is much higher than other major economies, with the core rate declining only to 5.7% from 6.1% in October.

With three members of the BoE voting for a rate hike and most of them saying that it is too early to conclude that services inflation and pay growth are on a firmly downward path, some further, but still modest, decline in underlying price pressures may not be a reason for BoE policymakers to change their minds, and is unlikely to severely hurt the pound.

Nonetheless, according to UK overnight index swaps, the market continues to believe that no more hikes are warranted and that around 115bps worth of rate cuts may be needed by next December. Perhaps they are more worried about the performance of the UK economy, which stagnated in Q3, rather than the stickiness of inflation. Therefore, should upcoming growth-related data continue to point to deep economic wounds, the pound’s advance may run out of fuel at some point in the not-too-distant future, as investors insist that some rate reductions may eventually be needed. In that respect, the UK retail sales for November are scheduled to be released on Friday.

Canadian inflation and RBA minutes also on tap

The Canadian inflation numbers for November are also coming out on Tuesday. At its latest gathering, the Bank of Canada held its key overnight rate unchanged at 5% and kept the door open to more tightening, saying that it is still concerned about high inflation, although it acknowledged an easing of price pressures and an economic slowdown.

However, investors were not convinced that another rate hike may be on the horizon. They are actually assigning around a 27% probability for a 25bps cut in January. In October, headline inflation slowed to just a tick above the Bank’s inflation-control target range of 1-3%, while the closely watched trimmed mean rate slid to 3.5% from 3.7%. Therefore, a further slowdown could take the probability of a January rate reduction higher and thereby weigh on the loonie.

Earlier the same day, and a couple of hours ahead of the BoJ decision, the RBA releases the minutes of its December policy meeting, where policymakers kept their benchmark interest rate unchanged, but softened their tightening bias, saying that whether further tightening is required will depend upon the data and the evolving assessment of risks. With the market assigning a small probability of another quarter-point hike by the RBA in February, investors may go through the minutes and see how willing officials are to press the hike button one last time.

Weekly Focus – Central Bankers Boost Christmas Spirit

Repricing continued in the rates markets this week as central bankers did little to talk rates back up. The market is currently pricing in the US short-term rates to fall below 4% by end of next year. In euro area, short-term rates are priced to approach the 2% mark late next year. Optimism about rate cuts arriving sooner rather than later has driven long-term rates lower and equities higher. The US 10y yield has fallen by more than 100bps from late October to below 4% and the S&P500 index is closing in on the all-time high levels.

We agree that rate cuts loom in the horizon but consider market expectations on the pace too optimistic. We also highlight that recent easing in financial conditions poses an upside risk to inflation next year. In this week's meeting, the FOMC cut down its median forecast for core PCE in 2024 while also revising down the dots (now showing a total of 75bps cuts). After the meeting, we were happy to see our long-held call for the first Fed rate cut in March has now become market consensus. Yet, thereafter, we think the market is too aggressive in pricing the pace for cuts. See Research US - Fed review: Rising optimism, 13 December.

For the euro area, the market is fully pricing in the first rate cut by April which we think is premature. In the Governing Council meeting this week, the ECB made no changes on rates as expected but announced it would start scaling back its PEPP portfolio starting H2-2024. The staff economic projections saw a downward revision for 2023 and 2024 in GDP, inflation and core inflation, but Lagarde also highlighted that the cut-off-date for the forecast parameters was prior to the recent fall in rates, which means that growth and inflation could turn out higher. It is true inflation has decelerated faster than expected and December flash PMIs on Friday confirmed that EA economy is slowing down. Yet, we are convinced the ECB wants to see further evidence on core inflation and wage dynamics, and hence, we keep our call for the first ECB rate cut in June 2024. Read more on Flash: ECB review - A conditional push-back, 14 December.

Norges Bank was the major outlier this week in a string of monetary policy holds by other central banks, as also the BOE and SNB kept monetary policy unchanged. Unexpectedly, NB decided to hike its policy rate by 25bp to 4.50% and signalled a 20% probability for another hike. Following the hike, we postponed our first rate cut from March to June, but lifted the number of cuts for next year from 4 to 5. See Reading the Markets Norway - Surprise NB hike paves way for 5 rate cuts in '24, 14 December.

Before Christmas, we still have the Bank of Japan meeting on Tuesday. There has been some speculation whether the BOJ would tighten policies next week. We continue to believe we need more firm conclusions on 2024 wage negotiations before they will feel confident to abandon yield curve control and raise the rate to zero. Next week is quiet on data front, but in the euro area, we are closely following any news from the EU Council regarding an extraordinary meeting about the new fiscal rules. Also, before Weekly focus returns from Christmas break, we will get euro area December inflation data 5 January. In China, focus will be on December PMIs in early January, and in the US, we will receive November PCE print next week, and the December jobs report before our next publication.

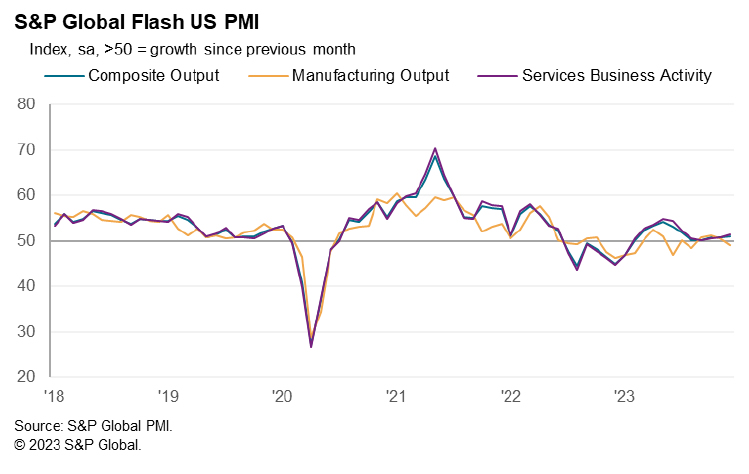

US PMI composite rises to 51.0, picks up a little momentum

US PMI Manufacturing fell from 49.4 to 48.2 in December. PMI Services rose from 50.8 to 51.3. PMI Composite rose from 50.7 to 51.0, a 5-month high.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

"The early PMI data indicate that the US economy picked up a little momentum in December, closing off the year with the fastest growth recorded since July.

"Looser financial conditions have helped boost demand, business activity and employment in the service sector, and have also helped lift future output expectations higher. However, the increased cost of living and cautious approach to spending by households and businesses means the overall rate of service sector growth remains far short of that witnessed during the travel and leisure revival back in the spring and summer.

"Manufacturing meanwhile remains a drag on the economy, with an increased rate of order book decline prompting factories to reduce production, cut back on headcounts and scale back their input buying.

"Despite the December upturn, the survey therefore signals only weak GDP growth in the fourth quarter.

"The survey's selling price gauge, which tends to lead changes in consumer price inflation, remains sticky but at a level which is indicative of CPI running only modestly above 2%. Service sector input cost inflation, a key gauge of core inflation, once again remained notably elevated by historical standards, though even here the average rate of increase in the fourth quarter has been the lowest since mid-2020."

Sunset Market Commentary

Markets

Today’s PMIs marked the end of a busy week. They would either confirm or challenge yesterday’s ECB en BoE case for signaling steady rates for the foreseeable future. It turned out to be the latter for Frankfurt, triggering Bund outperformance vs US Treasuries. German yields currently drop 2.4 (2-y)-9.9 bps (30-y). The 10-y came close to the 2% barrier, more or less this year’s lows. The 10-y swap sniffed at key support at 2.5% which, if broken, opens up another 50 bps of declines from a technical point of view. European PMI business confidence unexpectedly fell in December, from 47.6 to 47. Manufacturing flatlined at 44.2 while services activity (48.1 from 48.7) eased further to its lowest since the early 2021 lockdowns. The overall reduction in business activity again reflected deteriorating order books in both sectors with an only slightly less gloomier outlook not boding well for the future. Backlogs fell consequently while employment, viewed over the past several of months, teetered between marginal increases and decreases, essentially holding steady. S&P Global notes that this is positive for the individual consumer but exacerbates productivity challenges given that it coexists with declining output. Purchasing activity as well as inventories were cut to the lowest levels since around the GFC. Input cost inflation cooled but selling price inflation accelerated, the latter remaining elevated by historical standards. According to the PMI owners, the likelihood of the euro area being in a recession since Q3 remains notably high. It estimates growth of just 0.5% in 2023 and 0.8% next year. The release came the dollar to the rescue as EUR/USD (1.091) called of the test of the 1.10 resistance zone. Fed’s Williams later added some USD strength to it. He pushed back against the recent hefty repositioning prior and after the Fed meeting. He said while that it’s natural to move policy towards a more normal level over time, the FOMC isn’t “really talking about rate cuts right now”. He called the March bets premature. US yields rebounded intraday, turning losses into gains between 0.9-3.6 bps with the front underperforming. In their first comments after the meeting, most ECB officials kept the party line. Villeroy (France) said hikes are over, barring surprises, but warned the ECB needs to be patient. Holzmann (Austria) said policy rates probably have hit their peak but confirmed there was no discussion about rate cuts. He also noted that the council majority still saw upside inflation risks. Centeno (Portugal) struck the unsurprising dovish string with a remark that inflation has come down faster than it rose.

The UK economy finished to 2023 on a more constructive note. The S&P Global/CIPS composite PMI rose from 50.7 to 51.7, the second consecutive reading above the 50 level and coming after three months of sub-50 contraction readings. The December figure indicates the fastest rise in activity in the private sector since June. This was driven by a rebound of activity in the services sector (52.7 from 50.9). Activity in manufacturing declined for the tenth consecutive month. Firms reported a (marginal) increase in total new work for the first time since June. Respondents in this respect mentioned a stabilization in interest rates and hopes of a modest recovery. The improvement in order books was confined to the service economy. Despite better activity and orders, employment declined modestly for the fourth consecutive month. Inflationary tendencies still remain at work. Input cost inflation reaccelerated to the highest since August, mainly on higher wages. Higher cost increases also translate into higher output charges. In this respect, S&P sees little sign of a slowdown in inflationary pressures since the summer. Businesses also turned rather optimistic on their own growth prospects for 2024. S&P concludes that the UK economy probably stagnated over the fourth quarter as a whole. S&P also assess that “the service sector’s resilience and sticky inflation picture will add to speculation that it’s too early for the Bank of England to be talking about cutting interest rates”. UK gilts underperform Bunds but have pared their initial losses since. The front end loses 1-2 but longer maturities drop 4.6-4.7 bps. Sterling outperforms a broadly weaker euro with EUR/GBP falling back below the 0.86 big figure.

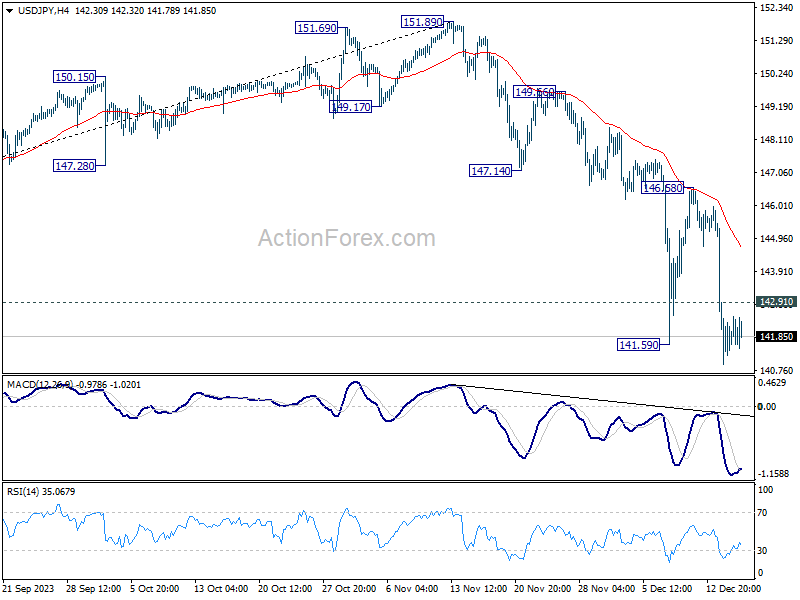

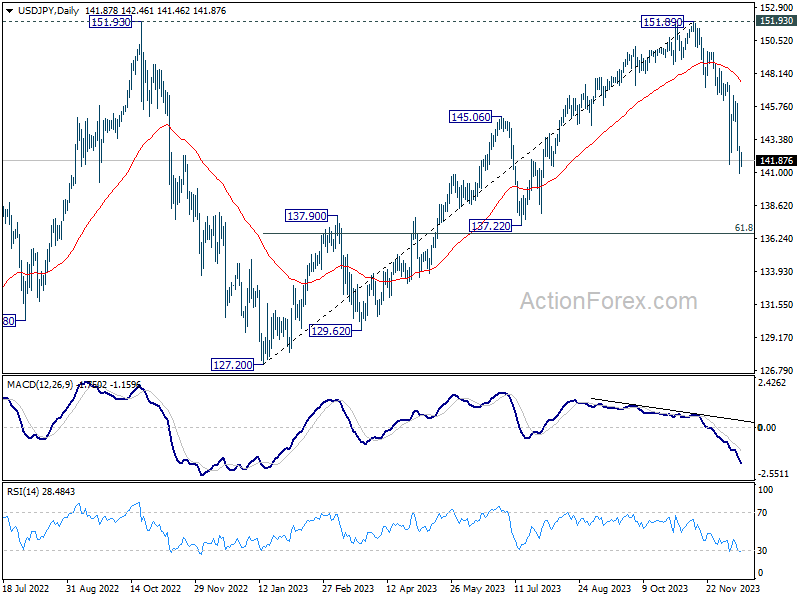

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 140.92; (P) 141.92; (R1) 142.87; More...

Intraday bias in USD/JPY remains mildly on the downside for the moment. Current decline from 151.89 should target next fibonacci level at 136.63. On the upside, above 142.91 minor resistance will turn intraday bias neutral first. But recovery should be limited well below 146.58 resistance to bring another decline.

In the bigger picture, current fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8627; (P) 0.8680; (R1) 0.8728; More....

Intraday bias in USD/CHF remains mildly on the downside for the moment. Current decline from 0.9243 should extend to target 0.8551 key support level. For now, near term outlook will stay bearish as long as 0.8819 resistance holds, in case of recovery.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. Meanwhile, break of 0.9111 resistance will argue that the third leg has started already, and target 0.9243 and above.