Sample Category Title

AUDUSD: Solid Chinese Data Further Boost Post-Fed Rally

AUD/USD keeps firm bullish tone for the third consecutive, with better than expected China retail sales and industrial production data adding to positive near-term outlook, established after dovish Fed on Wednesday.

The pair is trading near new 4 ½ month high in early Friday, with bullish technical studies contributing to positive fundamentals and continue to underpin the action.

Bulls probe again through Fibo resistance at 0.6713 (50% retracement of 0.7157/0.6270 fall) and pressure top of thin weekly cloud (0.6743) with firm break of these barriers to confirm bullish signal and open way for extension towards next targets at 0.6818/21 (Fibo 61.8% / July 27 spike high).

Formation of bullish engulfing pattern on weekly chart is also contributing to signals of continuation of the uptrend from 0.6270 (2023 low).

However, Friday’s profit-taking and overbought conditions on daily chart may slow bulls for limited consolidation, which should find firm ground above 0.6610 zone (10DMA / broken Fibo 38.2%) to keep larger bulls in play.

Res: 0.6739; 0.6820; 0.6846; 0.6900.

Sup: 0.6692; 0.6654; 0.6610; 0.6575.

Euro Dips on Soft Services PMI

- Eurozone, German Service PMI ease in December

- Euro snaps four-day rally

The euro has snapped a four-day winning streak on Friday. In the European session, EUR/USD is trading at 1.0949, down 0.38%. The euro has enjoyed a strong week, with gains of 1.77%.

Soft Eurozone, German services PMIs weigh on euro

Eurozone Services PMI eased in December, indicating that the economy continues to struggle. The PMI fell from 48.7 to 48.1 and missed the consensus estimate of 49.0. This marked a fifth straight month of contraction in the services sector, with 50 separating contraction from expansion. Germany, the largest economy in the eurozone, also reported a decline, with the PMI falling to 48.4, down from 49.6 in November and short of the consensus estimate of 49.8.

Euro soars after ECB pause

The European Central Bank held the benchmark rate at 4.0% for a second straight time on Thursday. This move was expected, but the central bank pushed back against market expectations for interest rate cuts next year, sending the euro soaring 1.09% against the US dollar after the announcement.

ECB President Christine Lagarde reaffirmed that the Bank would continue its “higher for longer” stance, saying that the Bank was not about to let down its guard and lower rates. Lagarde sounded hawkish even though the ECB lowered its inflation forecast at the meeting. Inflation has fallen to 2.4% in the eurozone, within striking distance of the 2% target. Lagarde acknowledged that inflation was easing but said that domestic inflation was “not budging”, largely due to wage growth.

There is a deep disconnect between the markets and the ECB with regard to rate policy. ECB President Lagarde poured cold water on expectations for rate hikes, arguing that inflation had not been beaten. The markets are marching to a very different tune and have priced in at least in around six rate cuts in 2024 and are confident that Lagarde will have to change her stance, with inflation falling and the eurozone economy likely in recession.

EUR/USD Technical

- EUR/USD is testing support at 1.0957. Below, there is support at 1.0905

- 1.1044 and 1.1096 are the next resistance lines

ECB Villeroy: Rate hikes are over, but that doesn’t mean a quick cut

ECB Governing Council member Francois Villeroy de Galhau, in an Ecorama radio interview, stated, "Barring shocks or surprises, rate hikes are over. However, he emphasized that "doesn't mean a quick rate cut." He further clarified, "We are not guided by a calendar, we are guided by data," and called for "confidence and patience."

Villeroy also commented on the pace of disinflation, noting it is occurring "a little quicker than expected," largely due to the faster-than-anticipated transmission of monetary policy. He concluded, "In other words, monetary policy is effective."

Madis Muller, another ECB Governing Council member, expressed the view that markets might be "a bit optimistic" about the prospects of early rate cuts. This sentiment was echoed by Robert Holzmann, who stated that there were no discussions about rate cuts among policymakers. Holzmann also mentioned that a majority of the Council members perceive upside risks to inflation.

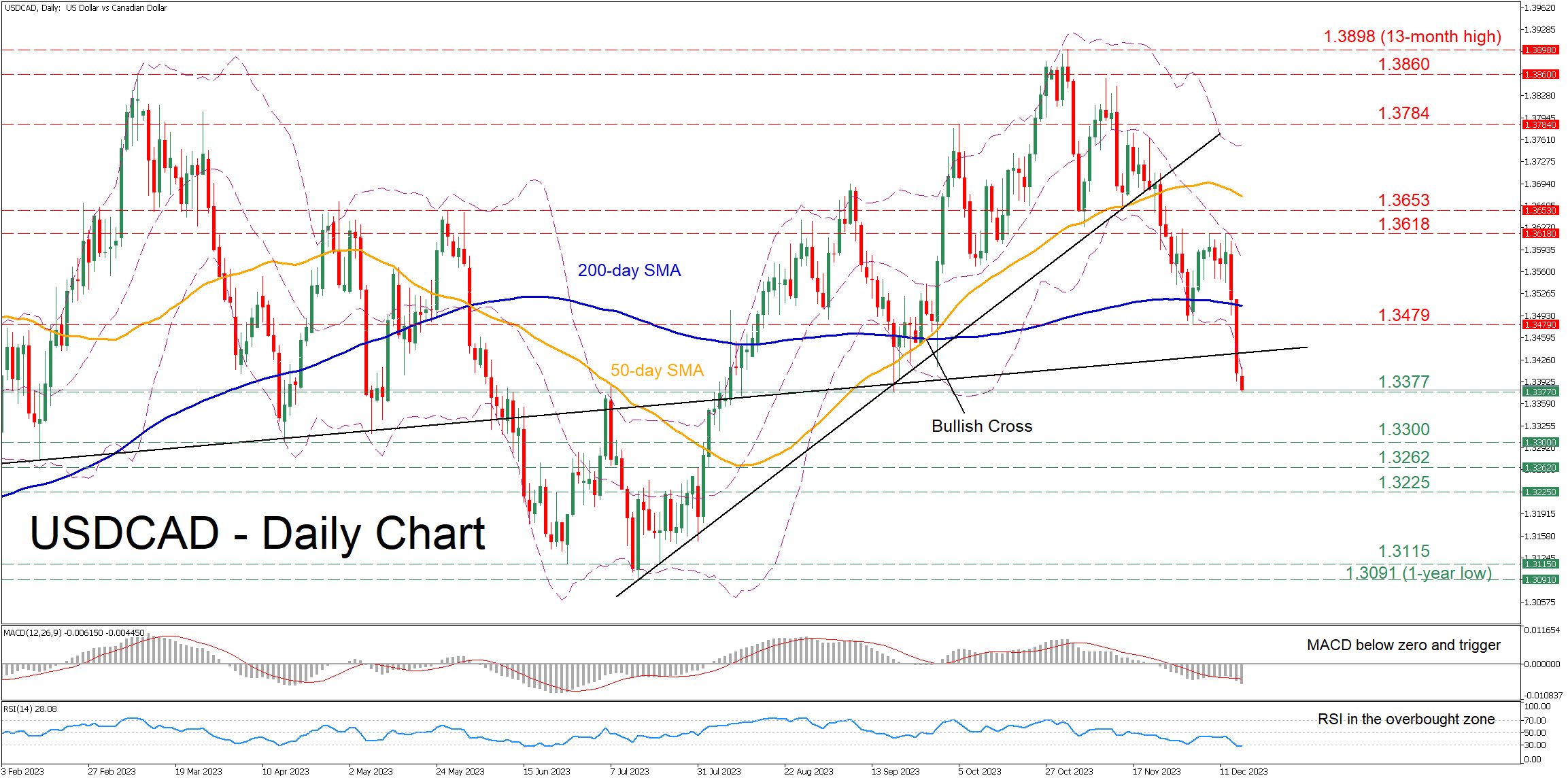

USDCAD Plummets Below Crucial Trendline

- USDCAD posts a fresh 2½-month low in today’s session

- Decline shows no signs of easing after break below 200-day SMA

- Momentum indicators are pointing at an overstretched retreat

USDCAD has been constantly losing ground following its 13-month high of 1.3898 on November 11. Moreover, the pair dropped to its lowest levels in more than two months on Friday, with the bears pushing the price below the crucial ascending trendline that connects a series of higher lows since October 2022.

Should the selloff persist, the September low of 1.3377 could be the first barricade for the price to claim. A violation of that territory could open the door for the April bottom of 1.3300. Failing to halt there, the pair could extend its retreat towards the February low of 1.3262.

On the flipside, if the price reverses higher, the bulls might attack the December support of 1.3479, which could serve as resistance in the future. Surpassing that zone, the pair could face 1.3618, a region that held strong multiple times in December. Further advances may then cease at the April-May resistance of 1.3653.

In brief, USDCAD has been under increasing downside pressures lately, generating a structure of consecutive lower lows. However, traders should not rule out an impending rebound as the short-term oscillators are currently within their oversold zones.

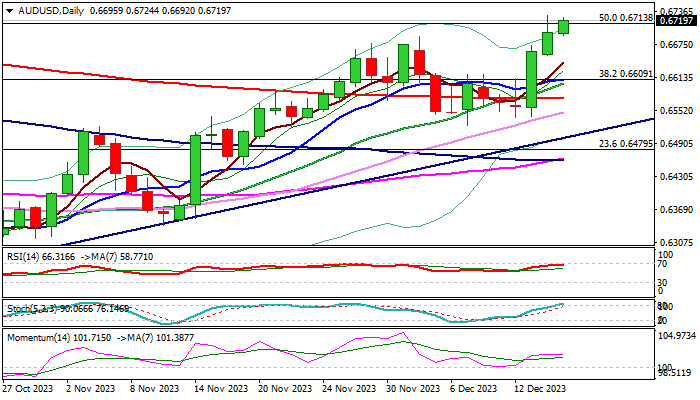

Australian Dollar Extends Gains on Chinese Data

- China industrial production and retail sales accelerate

- Australian dollar extends gains

The Australian dollar has extended its gains on Friday. In the European session, AUD/USD is trading at 0.6713, up 0.23%. It has been an excellent week for the Aussie, which has gained 2.07% on the back of the dovish Fed announcement and strong employment data at home.

The Aussie gained ground on Friday after China posted strong numbers. Industrial production surged 6.6% y/y in November, following a gain of 4.6% in October and above the consensus estimate of 5.6%. This marked the highest level since February 2022. China’s retail sales jumped 10.1% y/y in November, higher than the 7.6% gains in October but shy of the consensus estimate of 12.5%. This marked the 11th straight month of growth and was the fastest expansion since May. The data is an encouraging sign that China’s economy is responding to government stimulus after a rough patch in the third quarter.

Australian job growth sparkled in November, as the economy added 61,500 jobs, crushing the forecast of 11,500. This suggests that the labour market remains resilient despite high interest rates. The Reserve Bank of Australia has reiterated that rate decisions will depend on the data and the strong employment release provides support for the central bank to maintain a tightening bias. With inflation running at 5.4%, well above the 2% target, Governor Bullock has warned that the Bank could continue hiking. The markets, however, aren’t buying it and have priced in about 50 basis points in easing in 2024.

We are also seeing a disconnect between the markets and the Federal Reserve. At the Wednesday meeting, Fed Chair Powell reiterated that rates could move higher if necessary, this seemed little more than lip service as he signalled that the Fed expected to cut rates three times in 2024. The markets are much more dovish and have priced in six cuts next year.

AUD/USD Technical

- AUD/USD is putting pressure on resistance at 0.6733. Above, there is resistance at 0.6768

- 0.6694 and 0.6659 are providing support

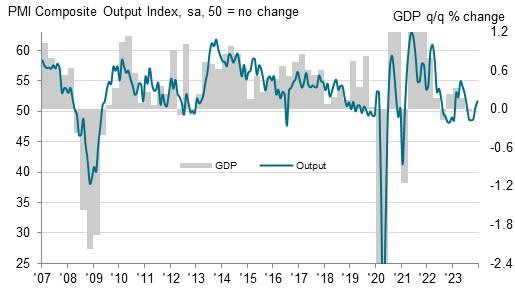

UK services sector boosts PMI composite, averting recession, BoE cut premature

UK PMI Manufacturing fell from 47.2 to 46.4, below the expected 47.5. Conversely, PMI Services rose from 50.9 to 52.7, exceeding expectations of 51.0 and reaching a six-month high. This surge in services also lifted PMI Composite from 50.7 to 51.7, marking another six-month high.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, commented, "The UK economy continues to dodge recession, with growth picking up some momentum at the end of the year to suggest that GDP stagnated over the fourth quarter as a whole." He added that while employment fell for a fourth consecutive month, the decline was marginal and did not significantly impact unemployment.

Williamson also highlighted the dual-speed nature of the UK economy, with manufacturing contracting sharply while services, particularly financial services, showed signs of growth. This growth in services was partly attributed to expectations of lower interest rates in 2024.

The divergence between the two sectors is also evident in inflation pressures. While goods-producing sector showed falling prices, service providers reported persistent and elevated inflationary pressures, often linked to wage growth. Williamson indicated that this could keep inflation above 3% in the coming months.

He added, "The service sector's resilience and sticky inflation picture will add to speculation that it's too early for the Bank of England to be talking about cutting interest rates." However, he also cautioned that the tentative nature of December's growth and the impact of looser financial conditions could raise fears of further policy tightening, potentially leading to economic decline.

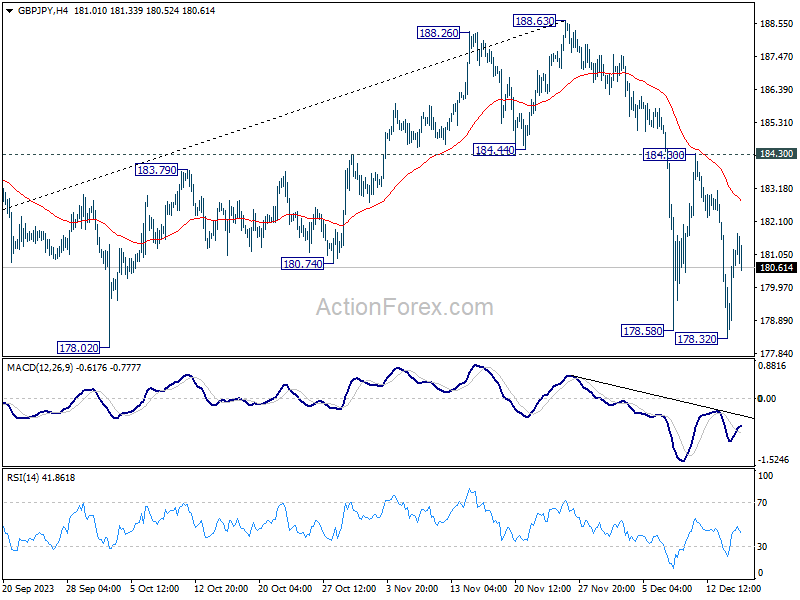

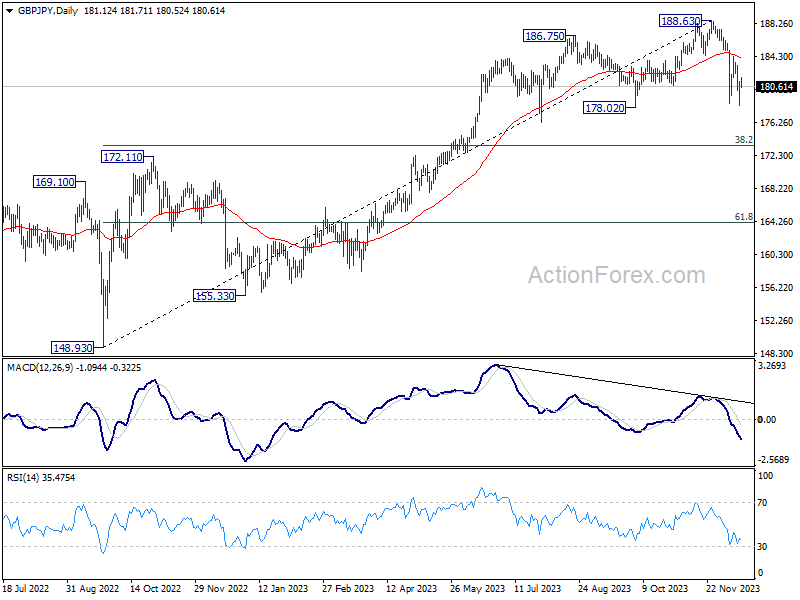

GBP/JPY Daily Outlook

Daily Pivots: (S1) 179.23; (P) 180.22; (R1) 182.10; More...

GBP/JPY recovered after dipping to 178.32 and intraday bias is turned neutral first. Deeper decline is expected as long as 184.30 resistance holds. Break of 178.32 will resume the whole decline from 188.63. Sustained break of 178.02 will pave the way to 38.2% retracement of 148.93 to 188.63 at 173.46.

In the bigger picture, while a medium term top is in place at 188.63, there is no clear sign of long term bearish trend reversal yet. As long as 55 W EMA (now at 175.67) holds, price actions from 188.63 are seen as a corrective move only. Larger up trend from 123.94 (2022 low) could resume at a later stage.

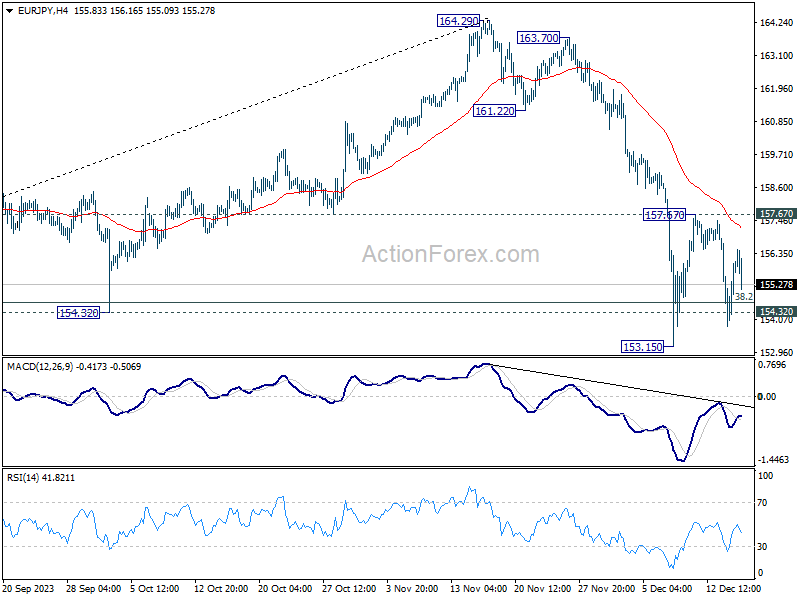

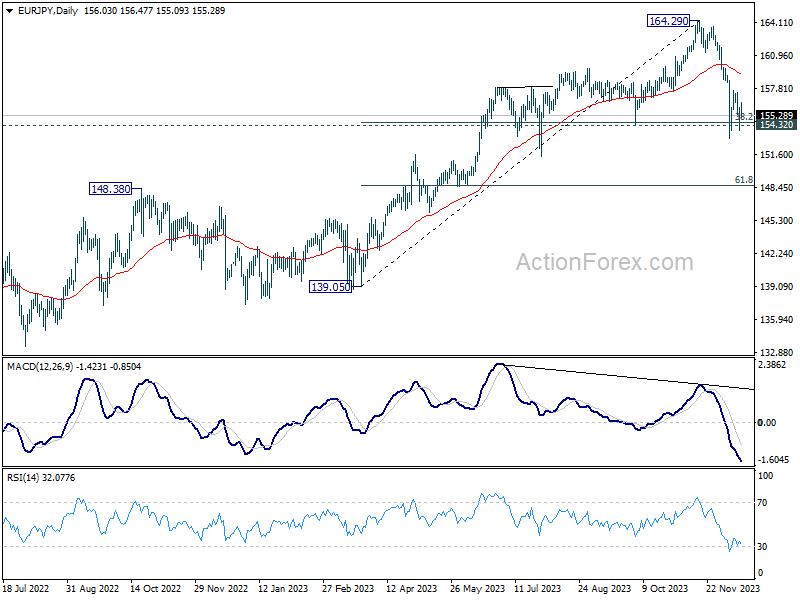

EUR/JPY Daily Outlook

Daily Pivots: (S1) 154.53; (P) 155.29; (R1) 156.72; More..

EUR/JPY recovered ahead of 153.15 support and intraday bias is turned neutral. Near term outlook stay bearish as long as 157.67 resistance intact. On the downside decisive break of 153.15 will resume whole fall from 164.39 to 61.8% retracement of 139.05 to 164.29 at 148.69.

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.

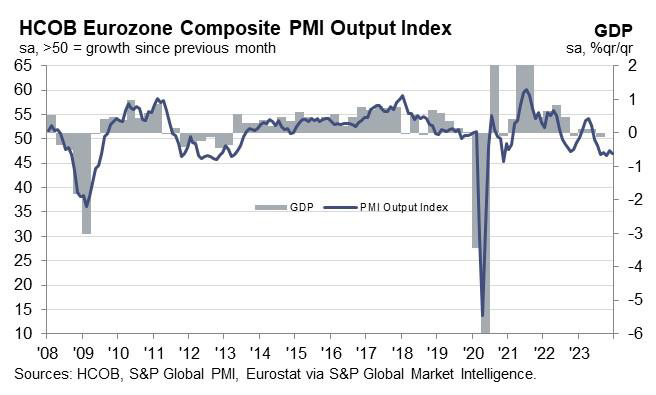

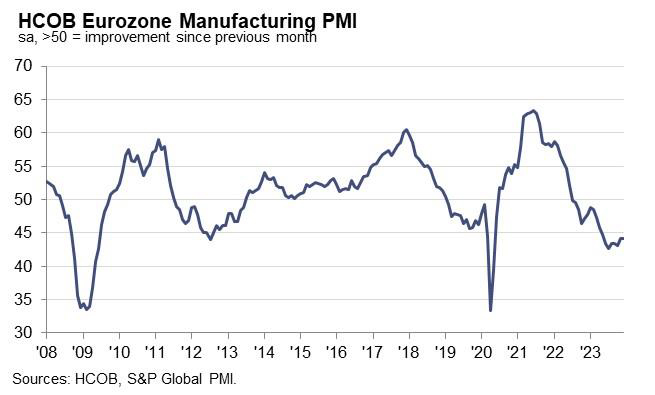

Eurozone PMI composite fell to 47.0, prolonged economic contraction

Eurozone PMI Manufacturing remained unchanged at 44.2 in December, falling short of anticipated 44.5. PMI Services index also declined from 48.7 to 48.1, below expected 49.0. Consequently, PMI Composite index decreased from 47.6 to 47.0.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, provided a critical analysis of these figures. He noted, "Once again, the figures paint a disheartening picture as the Eurozone economy fails to display any distinct signs of recovery. On the contrary, it has contracted for six straight months."

This ongoing contraction underscores the challenges facing the Eurozone economy, with a high likelihood that it has been in a recession since the third quarter.

De la Rubia also observed, "A closer look at the top two economies in the Eurozone reveals a positive comparison for Germany in relation to France, particularly within the service sector." Germany is experiencing a slower contraction in services compared to the more pronounced downturn in France. The manufacturing sector exhibits similar trends, with France facing a faster pace of output decline than Germany.

However, De la Rubia cautioned against any sense of satisfaction from Germany's comparatively better performance, emphasizing, "Obviously, there's no room for 'Schadenfreude' on the German side... the positive comparison does not change the fact that Germany's economy is in a bad shape, in absolute terms."

Also released, France PMI Manufacturing fell from 42.9 to 42.0 in December, a 43-month low. PMI Services fell from 45.4 to 44.3, a 37-month low. PMI Composite fell from 44.6 to 43.7, also a 37-month low. Germany PMI Manufacutring rose from 42.6 to 43.1, a 7-month. PMI Services fell from 49.6 to 48.4. PMI Composite fell from 47.8 to 46.7.

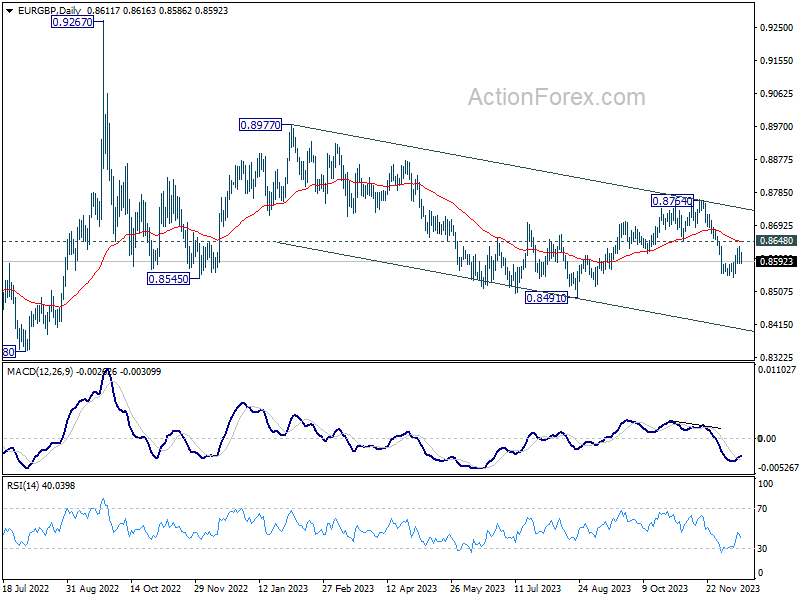

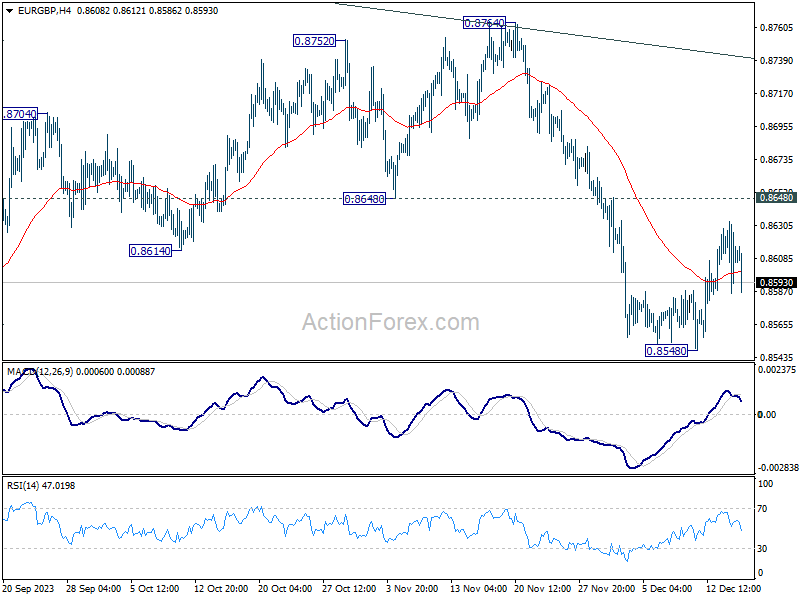

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8587; (P) 0.8611; (R1) 0.8634; More....

While EUR/GBP's recovery from 0.8548 extended, it's capped below 0.8648 support turned resistance. Intraday bias stays neutral and outlook further decline is expected. On the downside, break of 0.8548 will resume the fall from 0.8764 to 0.8491 support next. Firm break there will resume larger down trend. However, sustained break of 0.8648 will turn bias to the upside for stronger rebound.

In the bigger picture, current development suggests that down trend from 0.9267 (2022 high) is still in progress. This decline is seen as the third leg of the pattern from 0.9499 (2020 high). Break of 0.8201 will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969. In any case, outlook will stay bearish as long as 0.8764 resistance holds.