Sample Category Title

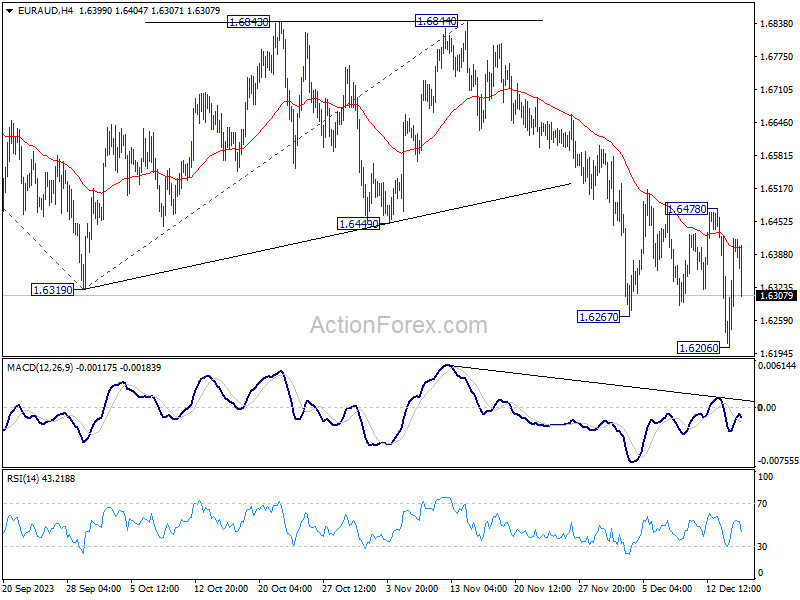

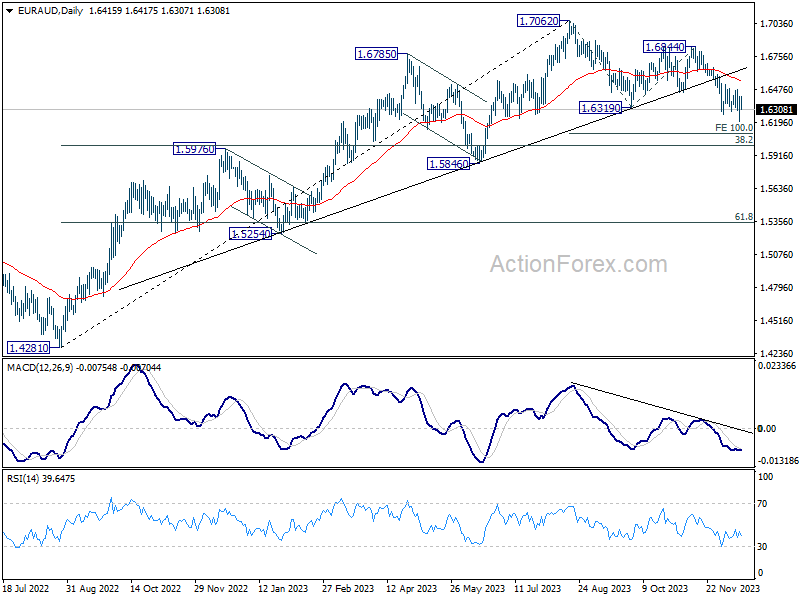

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6272; (P) 1.6346; (R1) 1.6485; More..

Intraday bias in EUR/AUD is turned neutral with current recovery. But outlook remains bearish with 1.6478 resistance intact. Break of 1.6206 will resume larger decline from 1.7062. Next target is 100% projection of 1.7062 to 1.6319 from 1.6844 at 1.6106.

In the bigger picture, fall from 1.7062 medium term top is seen as correcting the whole up trend from 1.4281 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support could be seen there to bring rebound on first attempt. But risk will stay on the downside as long as 1.6844 resistance holds. Sustained break of 1.6000 would bring further fall to 61.8% retracement at 1.5343.

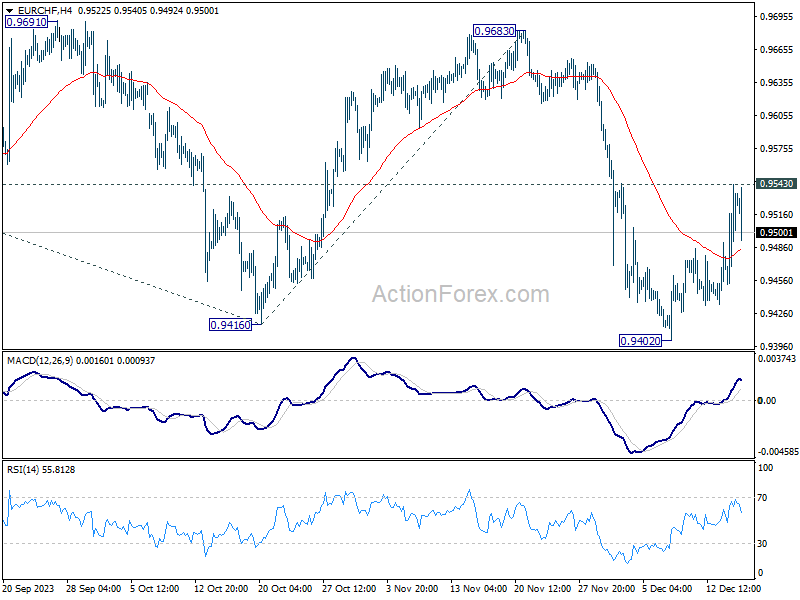

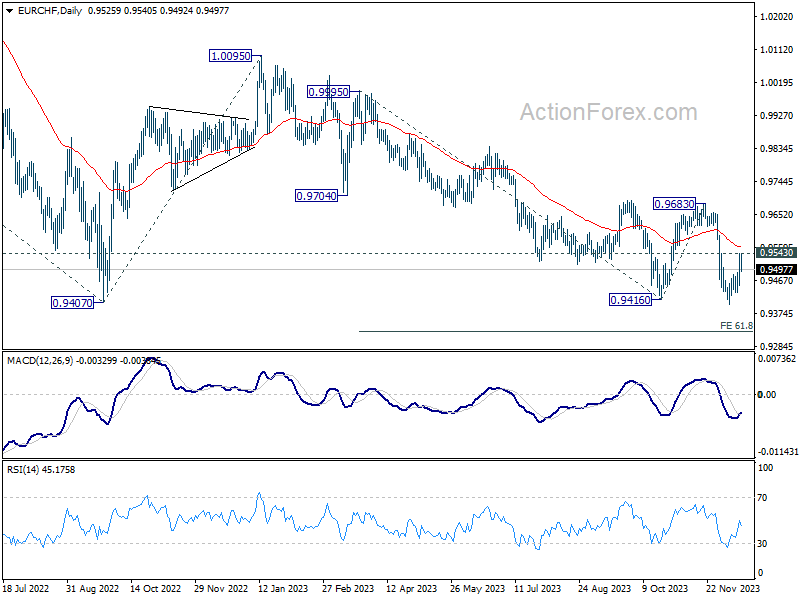

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9479; (P) 0.9512; (R1) 0.9570; More...

While EUR/CHF's recovery from 0.9402 extended higher, it's still capped by 0.9543 resistance. Intraday bias stays neutral and further decline remains in favor. On the downside, decisive break of 0.9407 will confirm larger down trend resumption. Next target is 61.8% projection of 0.9995 to 0.9416 from 0.9683 at 0.9325. However, sustained break of 0.9543 will bring further rally back to 0.9683 resistance instead.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Firm break of 0.9407 (2022 low) will resume long term down trend. Next target will be 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

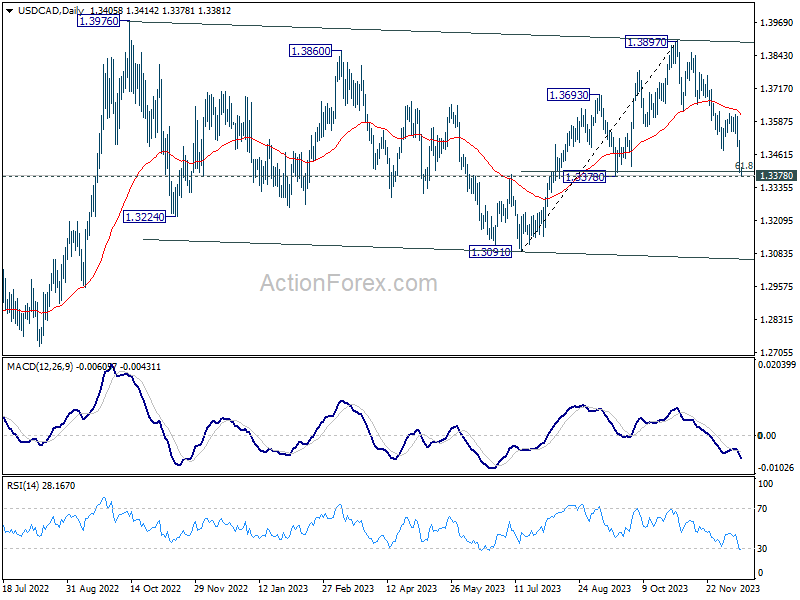

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3473; (P) 1.3540; (R1) 1.3586; More...

Intraday bias in USD/CAD remains on the downside at this point, with focus on 1.3378 support. Decisive break there will argue that whole rise from 1.3091 has completed at 1.3897. Deeper fall should then be seen back to 1.3091, to extend the sideway pattern from 1.3978. On the upside, though, above 1.3479 support turned resistance will turn bias back to the upside for stronger rebound.

In the bigger picture, outlook is mixed up by deeper then expected fall from 1.3897. But after all, price actions from 1.3976 (2022 high) are viewed as a corrective pattern that's in progress. Larger up trend from 1.2005 (2021 low) is still expected to resume at a later stage as long as 1.2947 resistance turned support holds.

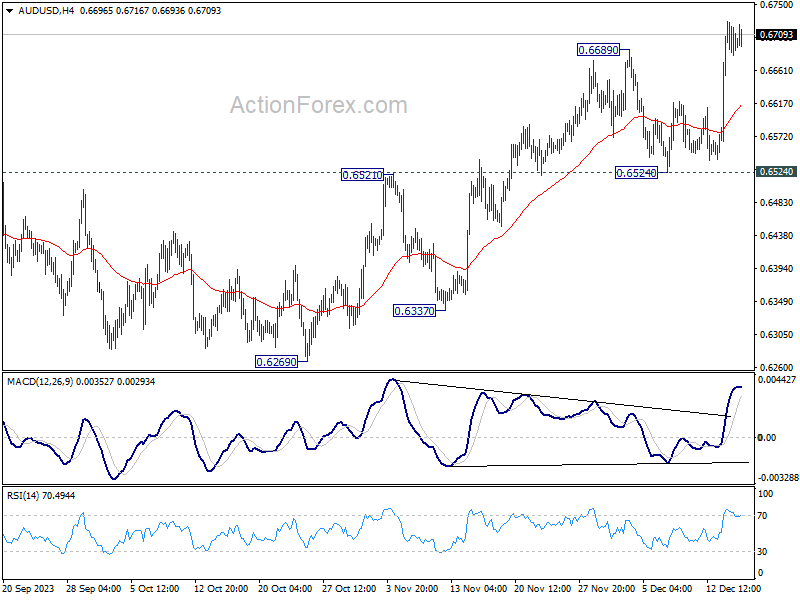

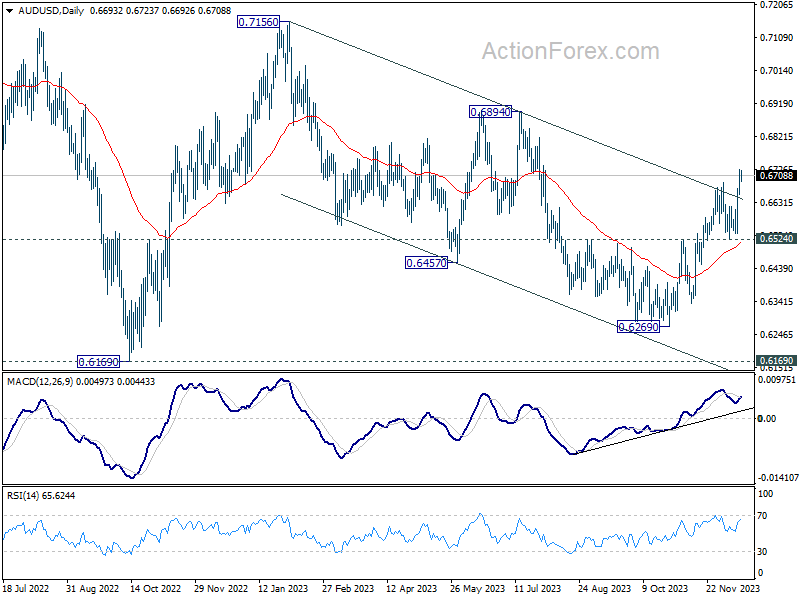

AUD/USD Daily Report

Daily Pivots: (S1) 0.6659; (P) 0.6694; (R1) 0.6733; More...

Intraday bias in AUD/USD remains on the upside for the moment. Current development suggests that whole fall from 0.7156 has completed with three waves down to 0.6269. Further rise should be seen to 0.6894 resistance next. Meanwhile, near term outlook will stay cautiously bullish as long as 0.6524 support holds, in case of retreat.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. Price actions from 0.6169 (2022 low) could be just a medium term corrective pattern. Rise from 0.6269 is seen as the third leg of the pattern. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

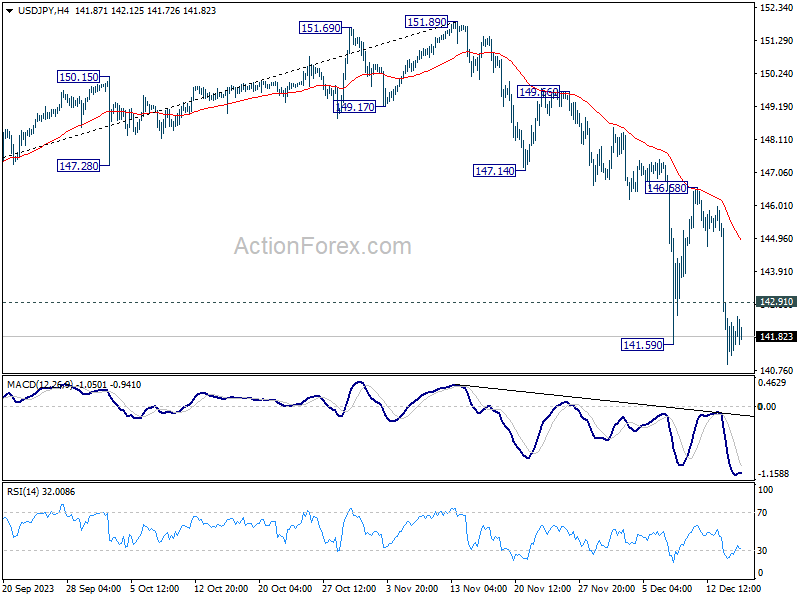

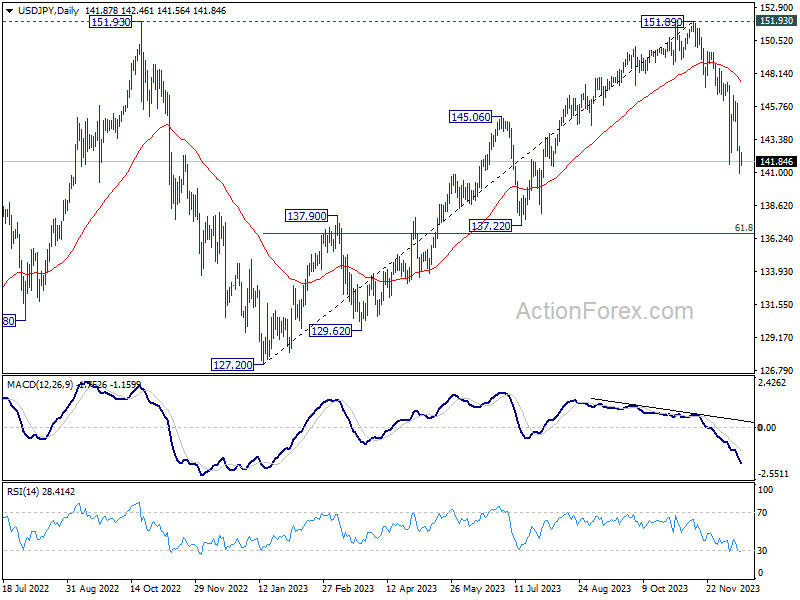

USD/JPY Daily Outlook

Daily Pivots: (S1) 140.92; (P) 141.92; (R1) 142.87; More...

USD/JPY's fall is still in progress and intraday bias stays on the downside. Current decline from 151.89 should target next fibonacci level at 136.63. On the upside, above 142.91 minor resistance will turn intraday bias neutral first. But recovery should be limited well below 146.58 resistance to bring another decline.

In the bigger picture, current fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.

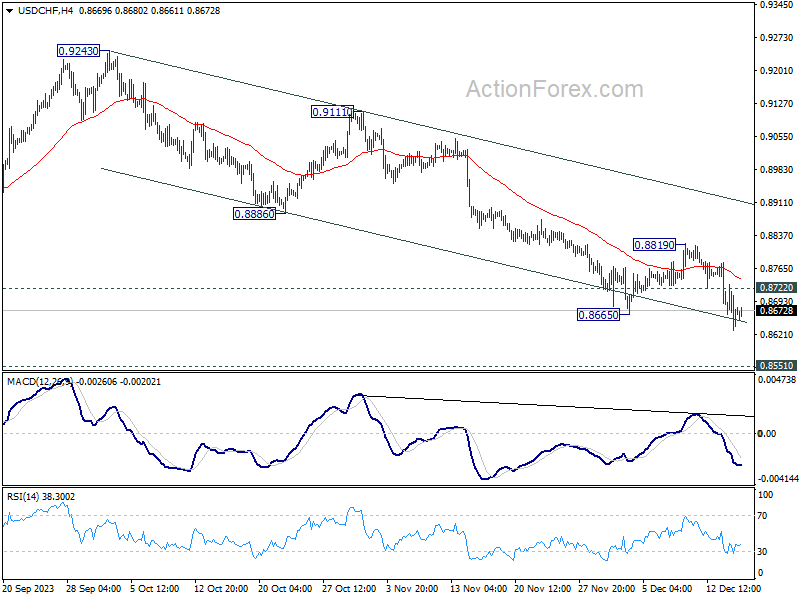

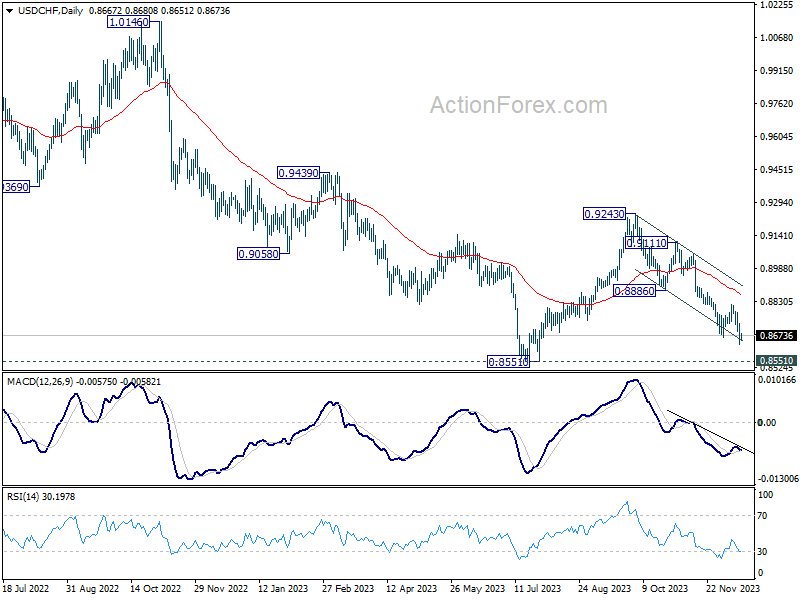

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8627; (P) 0.8680; (R1) 0.8728; More....

USD/CHF's break of 0.8665 support confirm resumption of whole decline from 0.9243. Intraday bias is back on the downside and deeper fall should be seen to 0.8551 key support level. For now, near term outlook will stay bearish as long as 0.8819 resistance holds, in case of recovery.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. Meanwhile, break of 0.9111 resistance will argue that the third leg has started already, and target 0.9243 and above.

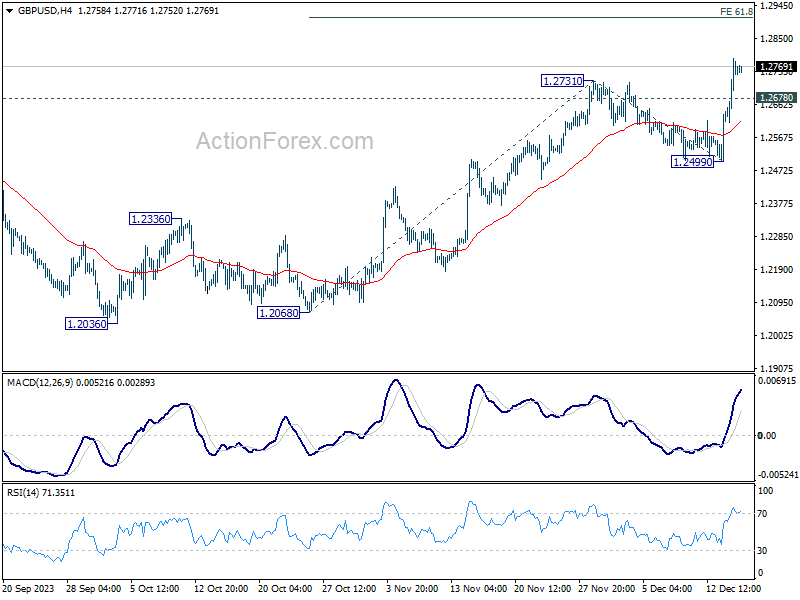

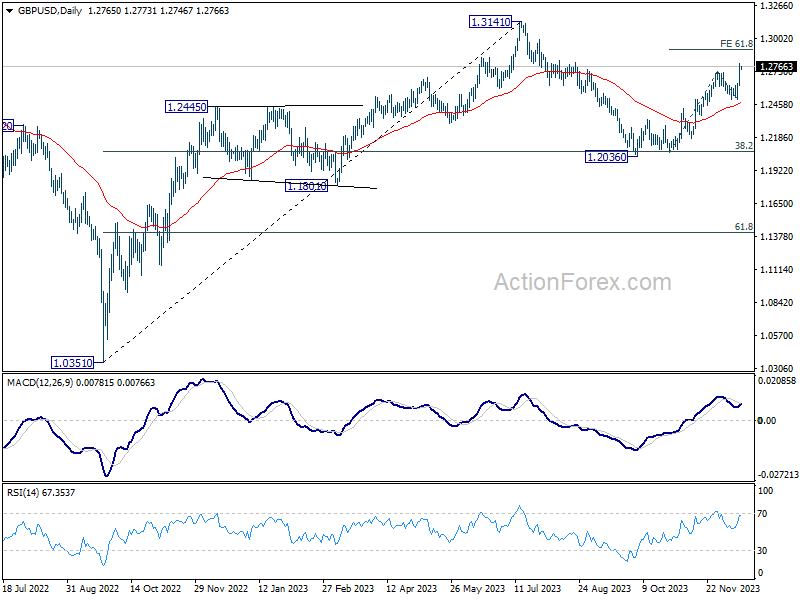

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2653; (P) 1.2724; (R1) 1.2835; More...

GBP/USD's rally is in progress and intraday bias stays on the upside for the moment. Current rise from 1.2036 should target 61.8% projection of 1.2068 to 1.2731 from 1.2499 at 1.2909 next. On the downside, below 1.2678 minor support will turn intraday bias neutral first. But outlook will stay bullish as long as 1.2499 support holds.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to rise from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, that could still extend through 1.2731. But upside should be limited by 1.3141 o bring the third leg of the pattern. Meanwhile, sustained trading below 55 EMA will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again, and possibly below.

After Recent Sharp Decline in Yields, Market Dynamics Might Gradually Change a Bit

Markets

The ECB and the Bank of England yesterday as expected left their policy rates unchanged at respectively 4% and 5.25%. Contrary to the Fed they didn’t ratify aggressive rate cut bets yet. In its new staff projections, the ECB downwardly revised its path inflation for this year (5.4% from 5.6%) and next year (2.7% from 3.2), but it will still take time to bring inflation back to the 2% target (2.1% in 2025; 1.9% in 2026). At the press conference, ECB Chair Lagarde warned that it absolutely wasn’t the time yet to lower the guard on Inflation. Amongst others, the central bank remains concerned on the inflationary impact of wage rises going forward. In this context, there is no ground to talk about rate cuts yet. The ECB also decided to start reducing the PEPP portfolio by €7.5bn/month in H2. It will stop reinvestments at the end of 2024. European yields set intraday lows during the morning session after the dovish Fed U-turn on Wednesday but gradually regained some ground after the ECB decision and press conference. German yields still declined between 10 bps (2-y) and 1.9 bps (30-y). US yields saw further follow-through declines as the Fed openly prepares for 2024 interest rate cuts. Remarkably, bonds with longer maturities outperformed. US yields declined between 3.8 bps (2-y) and 14 bps (30-y). US November retail sales (control group +0.4% M/M) and weekly jobless claims (declining to a low 202k) suggest ongoing economic resilience. Understandably, the data had limited impact. The prospect of Fed easing next year further supported equites with several US and European indices nearing or touching post-Corona top levels. ‘Policy divergence ‘ between the Fed and the likes of the ECB and the BoE kept the dollar in the defensive. EUR/USD tested the 1.10 area, but a break of the 1.1017 end November top didn’t occur yet. At the BoE decision, 3 members of the 9-member MPC still voted for an additional rate hike and the BoE reconfirmed the need to stay restrictive for and extend period of time. Gilts underperformed (2-y -1.9 bps). Sterling gained against the dollar. EUR/GBP whipsawed around the 0.86 big figure (close 0.8611).

Market focus today turns to the preliminary December PMI’s. The US composite PMI is expected to ease slightly from 50.7 to 50.5. The EMU measure is seen improving slightly from 47.6 to 48, but both manufacturing (44.6) and services (49) are expected to stay in contraction territory. After the recent sharp decline in yields, market dynamics might gradually change a bit. Outright weak data could confirm the downtrend in yield. However, (activity) data in line or better than expected might slow the market push for early rate cuts. On FX markets, the dollar is fighting an uphill battle. A break of EUR/USD above the 1.1017 end November top brings the YTD top of 1.1276 on the radar.

News headlines

China’s PBOC offered a record CNY 800bn of one-year loans to commercial lenders today. Combined with the amount to roll-over expiring loans, the amount injected (CNY 1450bn) was the biggest since 2016. Cash injections are often seen as an alternative to the central bank’s reserve requirement ratio to stimulate the struggling economy. While economic data this morning showed industrial production recovering a bit more than expected, retail sales & fixed asset investments underwhelmed while the property (both investment and sales) drag remains substantial. China seeks to keep liquidity ample after the country in a rare move raised the fiscal deficit ratio to a 30-year high in October and allowed the government to sell an additional CNY 1000bn of sovereign bonds within the year. The yuan recovered from opening losses in the meantime, trading close to the USD/CNY 7.10 key support.

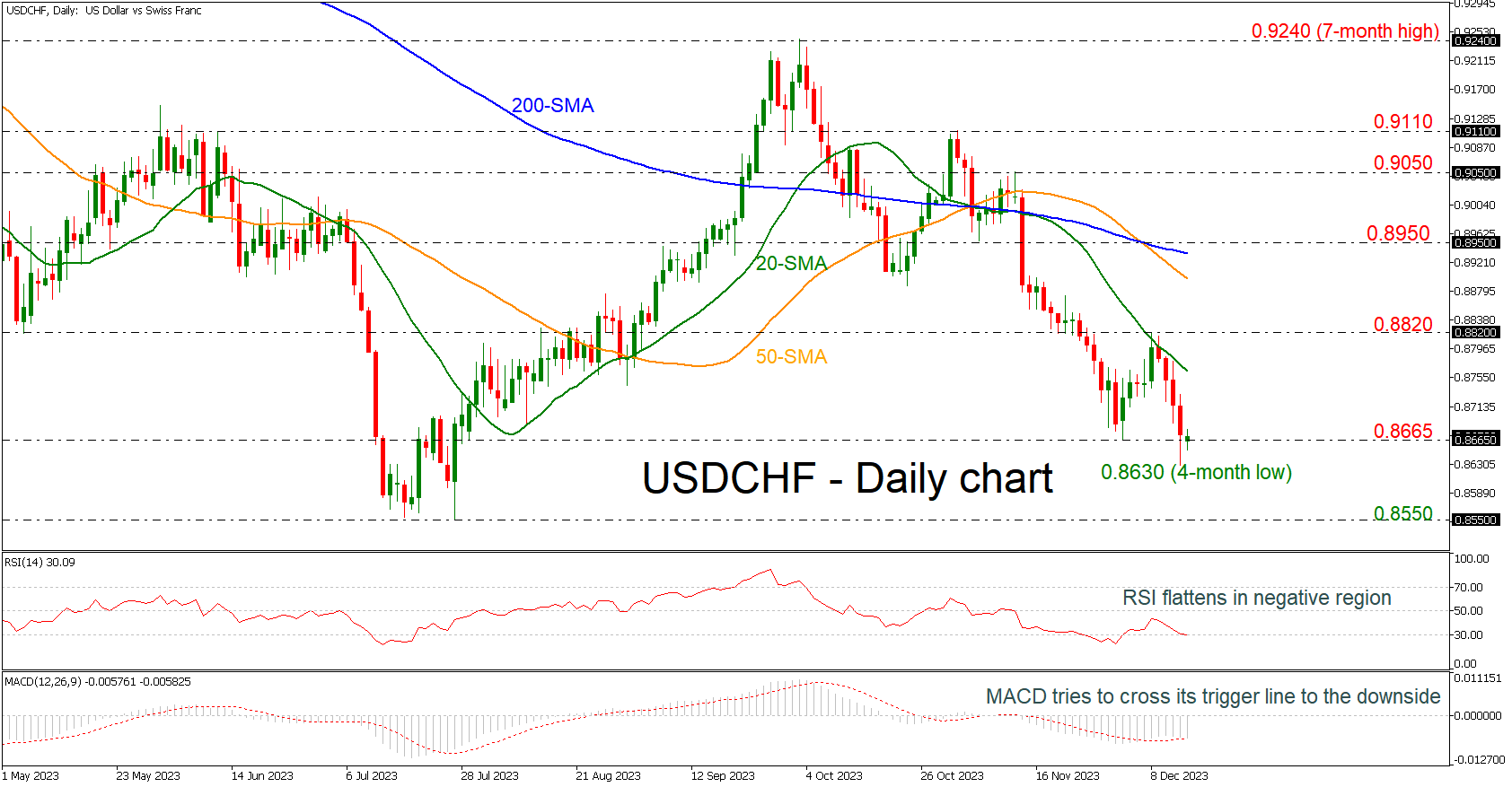

USDCHF Corrects Higher After 4-month Low

- USDCHF ends the week in red

- MACD and RSI in negative region

USDCHF is moving slightly higher after the retreat towards a fresh four-month low of 0.8630. The pair failed to have a closing day beneath the 0.8665 barrier, which is acting as a significant support level.

Technically, the RSI is flattening near the 30 level, while the MACD is extending its bearish momentum beneath its trigger line.

Should the bulls return, they will first push for a move above the 20-day simple moving average (SMA) at 0.8765. Then, they will fight for a breakout above 0.8820. If efforts prove successful, the pair may advance towards the 50-day SMA at 0.8900 ahead of the 200-day SMA at 0.8933.

Nevertheless, any additional declines could remain attractive to traders unless the price exits the 0.8665 support level. If that bearish scenario unfolds, the pair could tumble towards the 0.8550 base, taken from the low on July 27.

In brief, USDCHF is heading for a negative weekly close, but as long as it trades above 0.8665, buying the dip could be a favorable play.

Norges Bank Defies the Tide

In focus today

Today we get PMIs out of the big Western economies.

In the euro area, we expect continued modest contraction in the service sector while the downward trend in manufacturing becomes gradually less steep. We will also keep an eye on the price indices, which moved higher in November. Particularly the IFO survey showed German service businesses' price expectations increased markedly in November.

The 60 second overview

Norges Bank: Norges Bank was the major outlier in a string of monetary policy holds from the ECB, SNB and BoE yesterday. Norges Bank decided to hike its policy rate by 25bp to 4.50% and signal a 20% probability of another hike in March. Heading into the decision, most analysts - ourselves included - had called for unchanged policy rates while markets had priced a small hike probability (+4bp). Following the decision, we postponed our first rate cut from March to June, but lifted the number of expected rate cuts next year from 4 to 5.

ECB/BOE: Apart from Norges Bank, central bank decisions were in line with expectations. ECB kept the deposit rate at 4% and lowered its projections for growth and inflation next year. Lagarde struck a dovish tone with no clear intention to push back on the aggressive market pricing for next year. ECB will start reducing the PEPP portfolio in H2/24 and terminate reinvestments by the end of 2024. We stick to our call of the first cut being delivered at the June meeting, though risks are tilted towards an earlier start. The BoE also left the rate unchanged at 5.25%, though the communication was hawkish in an attempt to counter the easing of financial conditions seen recently. As for the ECB, we expect the first cut from BOE in June.

US: US retail sales surprised to the upside in November, rising by 0.3% m/m after the decline of 0.2% m/m in October. US consumers remain on a solid footing, not least due to the strong labour market. In that respect, initial claims data from last week came in better than expected at 202.000, the lowest level since mid-October.

Japan: Overnight, composite PMI data from Japan rose from 49.6 to 50.4 in December after declining for most of H2. The move was driven by improving activity among services providers, while manufacturing ticked further down below the 50 mark separating expansion from contraction. Focus now turns towards the BoJ meeting on Tuesday.

Equities: What a day in equities! European and Nordic stocks rallied in catch-up to the US session. However, US continued higher too with small cap Russell2000 adding another 3%. This takes small cap Russell 2000 a staggering +7% higher for the week vs Nasdaq +3%. It is clear that the rally is benefitting not only large cap tech. Small caps, REIT, regional banks, lower quality balance sheet and consumer cyclicals were the place to be this week. Value beating growth. Same story in the Nordics with real estate rallying double digit together with rate sensitive stocks like EQT and Nibe. This summed up to S&P 500 0.3%, Nordics 1.3% and Stoxx 600 0.9%. US futures are higher, again, this morning.

FI: Yesterday morning, European yields caught up with the significant decline in US yields following the FOMC meeting on Wednesday. The ECB statement and Lagarde's press conference pushed short-end rates a bit higher, though most of the rally had already faded prior to the ECB decision. Markets still expect ECB to cut rates by around 150bp next year. 10Y Bund yields ended the day down by 6bp, while 10Y UST yields extended the rally from Wednesday night by dropping an additional 11bp. The 10Y BTP/Bund spread tightened following the release of the PEPP schedule, as the planned reduction of EUR7.5bn/month in H2/2024 was less hawkish than feared.

FX: EUR/USD moved sharply higher following yesterday's ECB monetary policy announcement, trading close to the 1.10 mark. The Bank of England (BoE) yesterday decided to keep the Bank Rate unchanged at 5.25% and coupled with a hawkish tilt in communication, this initially sent EUR/GBP lower. However, the move was fully retraced following the ECB announcement, in line with our expectation. Yesterday Norges Bank surprised markets by hiking policy rates by 25bp including the sight deposit rate to 4.50% providing support for NOK. The SNB kept the policy rate unchanged at 1.75% yesterday and delivered a dovish message, which ultimately sent EUR/CHF notably higher. SEK faced headwinds from lower than expected inflation.

Credit: Credit spreads tightened massively, with iTraxx Xover closing 24bp tighter, taking the index to 329bp, while Main compressed 4.6bp and closed in 59.5bp.

Nordic macro

Market is expecting a slight increase in LFS November unemployment to 8.0 % SA. Take this data with a pinch of salt. We rely more on PES registries.