Sample Category Title

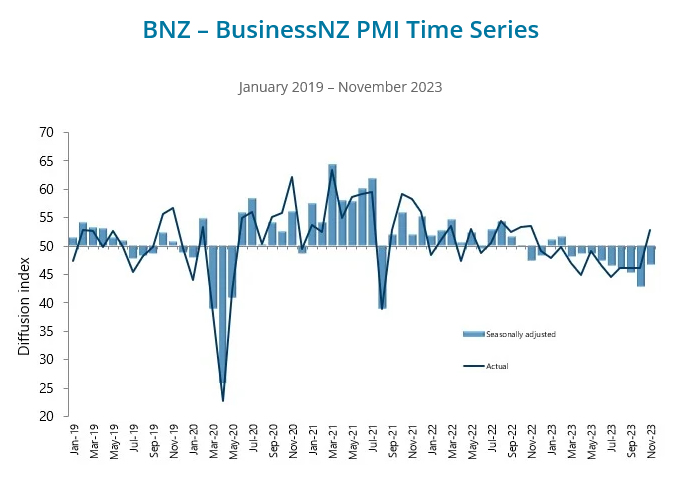

NZ BNZ manufacturing improves to 46.7, ninth month in contraction

New Zealand's manufacturing sector experienced a slight improvement in November, as indicated by the BusinessNZ Performance of Manufacturing Index. The index rose from 42.9 to 46.7, marking its highest level since June. However, it's important to note that the PMI remained in contraction territory (below 50) for the ninth consecutive month.

Breaking down the index, several components witnessed modest improvements. Production increased from 41.6 to 43.6, employment from 43.8 to 47.9, new orders from 44.5 to 47.7, finished stocks from 45.8 to 50.7, and deliveries from 43.3 to 48.0. Despite these gains, the improvements were not strong enough to push the overall PMI into the expansion zone.

The proportion of negative comments from the manufacturing sector was 58.7%, a decrease from 65.1% in October and 68.8% in September. This indicates a slight shift in sentiment, although a significant portion of feedback remains pessimistic. The predominant concerns cited by manufacturers revolved around a general lack of demand and sales, highlighting the primary challenges facing the industry.

BNZ Senior Economist, Craig Ebert, particularly focused on the production index. He noted that despite a slight improvement in November, the production index remained almost 10 points below its long-term average. Ebert emphasized that "That's a big undershoot, in historical context".

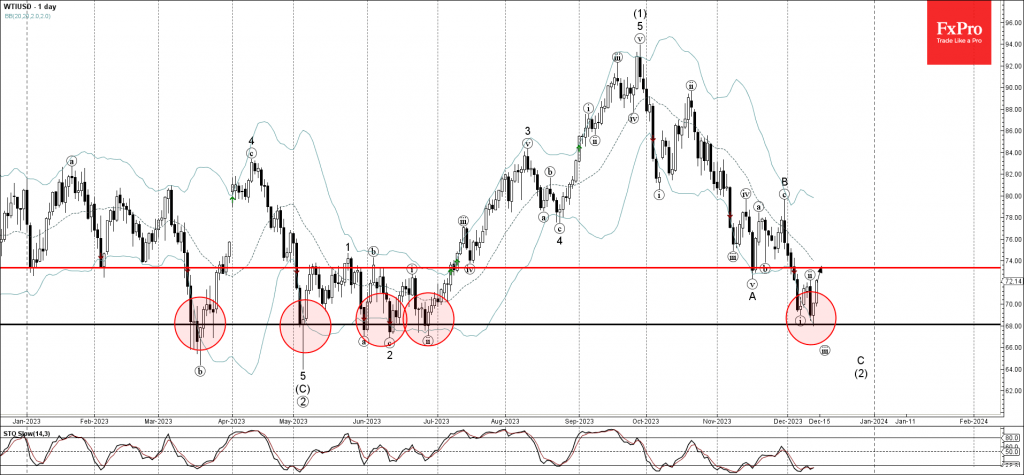

WTI Wave Analysis

- WTI reversed from support level 68.00

- Likely to rise to resistance level 73.35

WTI crude oil recently reversed up from the major long-term support 68.00 (which has been repeatedly reversing the price from March) coinciding with the lower daily Bollinger Band.

The upward reversal from the support 68.00 is likely to form the daily candlesticks reversal pattern Morning Star – strong buy signal for this instrument.

Given the strength of the support 68.00 and the oversold daily Stochastic, WTI crude oil can be expected to rise to the next resistance level 73.35 (former support from November).

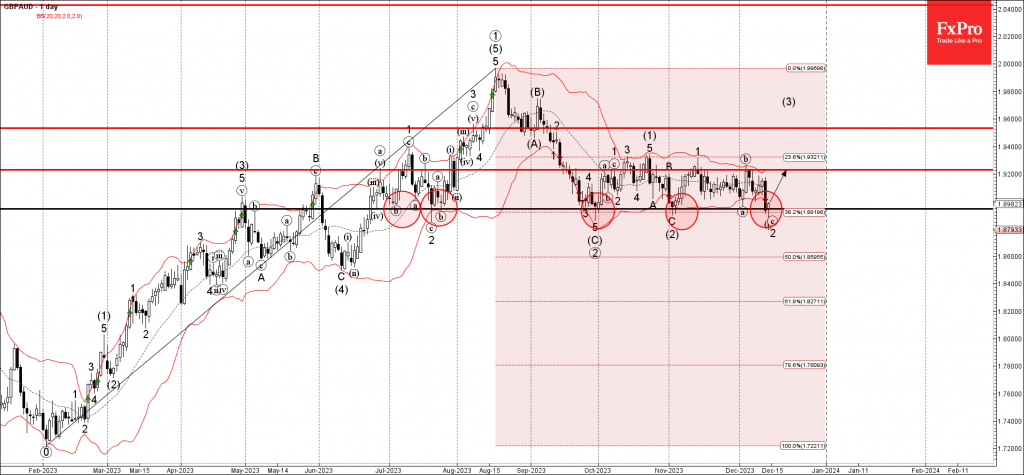

GBPAUD Wave Analysis

- GBPAUD reversed from support level 1.8945

- Likely to rise to resistance level 1.9200

GBPAUD currency pair recently reversed up from the strong support level 1.8945 (which has been repeatedly reversing the pair from the start of July) intersecting with the lower daily Bollinger Band.

The support level 1.8945 was strengthened by the 38.2% Fibonacci correction of the sharp extended uptrend from last February.

Given the clear daily uptrend, GBPAUD currency pair can be expected to rise to the next resistance level 1.9200 (which stopped the previous wave 1 and b).

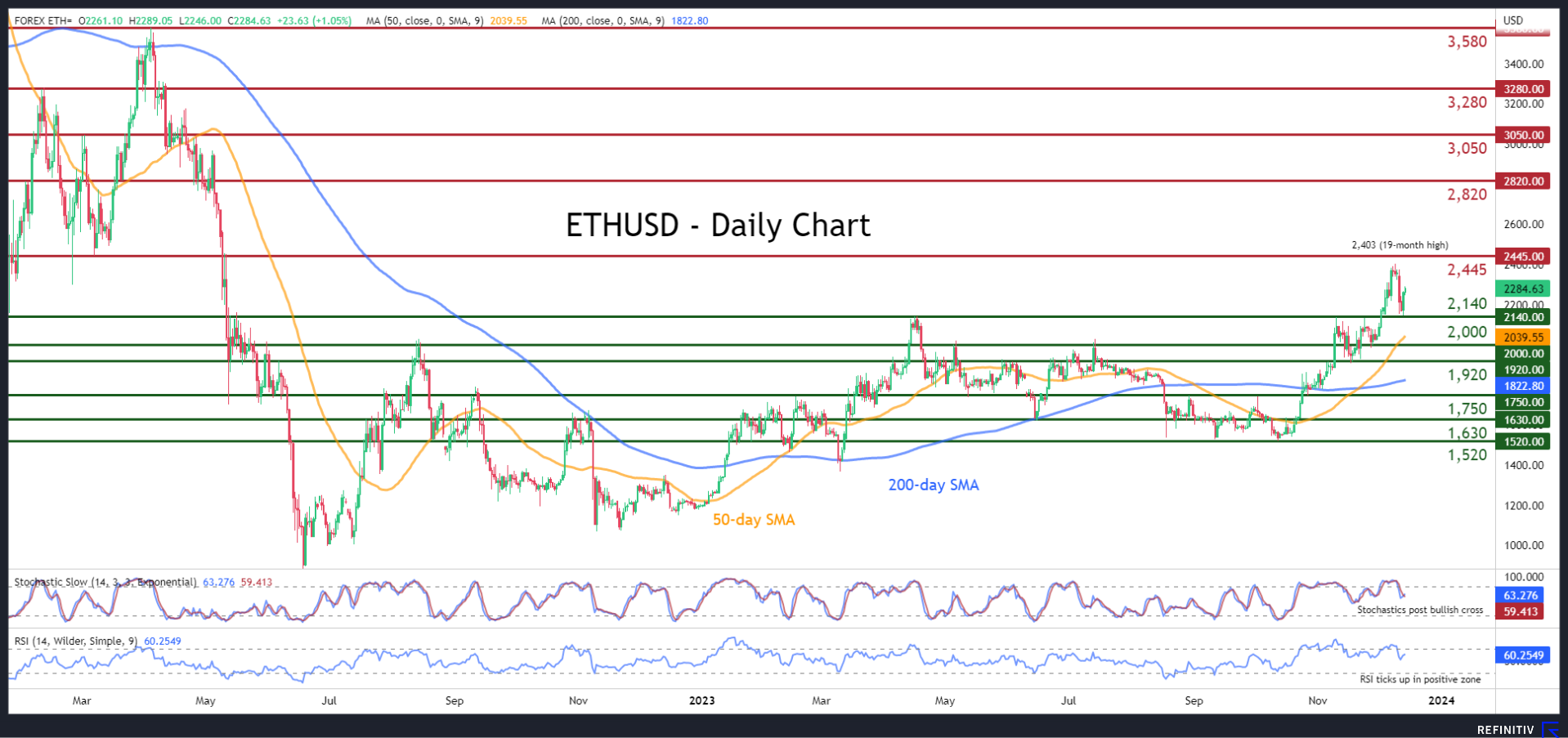

ETHUSD Attempts to Erase Recent Pullback

- Ethereum posts 19-month peak before retracing lower

- But the bulls regain control and recoup some losses

- Momentum indicators point at more gains ahead

ETHUSD (Ethereum) has experienced a strong rally since late October, which propelled the price to a fresh 19-month peak of 2,403 on December 9. Although the latest high was followed by a mild setback, the price seems ready to stage a recovery as both the RSI and stochastics are implying strengthening positive momentum.

Should the rebound extend and the price storms to fresh highs, initial resistance could be met at the March 2022 bottom of 2,445. If that barricade fails, there is no prominent resistance until 2,820, which has acted both as support and resistance during the first half of 2023. Conquering that region, the bulls might then attack the March 2022 hurdle of 3,050.

On the flipside, bearish actions could send the price to challenge the recent support of 2,140, which also held strong both in April and November. Sliding beneath that floor, the altcoin could descend towards the 2,000 psychological mark. A break below the latter may pave the way for the November support of 1,920.

Overall, ETHUSD has been regaining traction in the near term in an attempt to wipe out its latest pullback. Is the price heading towards fresh multi-month highs?

ECB Review: A Conditional Push-Back

- Today's ECB policy meeting saw no changes to the policy rates, as unanimously expected across analysts and market pricing, hence the deposit rate was maintained at 4%.

- The ECB already surprised with an announcement today of its schedule for PEPP reinvestments for next year. ECB decided to end full PEPP reinvestments from H2 24 by EUR7.5bn / month on average and no reinvestments beyond the end of 2024.

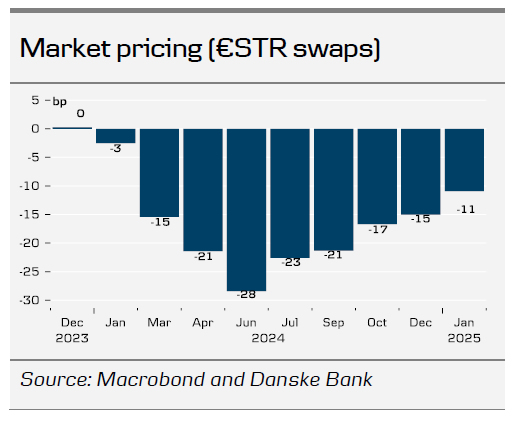

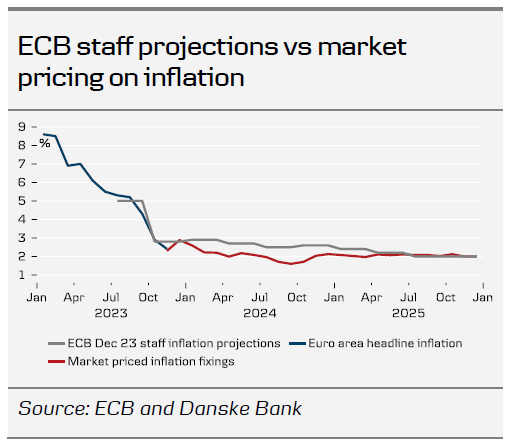

- The staff projections saw a downward revision for 2023 and 2024 in GDP, inflation and underlying inflation. Euro area growth is projected to be around potential from 2025. Lagarde highlighted that the cut-off date of the factors using market pricing was 23 November, which predates the significant bond yield decline, and hence all things being equal would point to higher growth and inflation.

- Lagarde didn't take the opportunity to clearly push back on the current financial conditions, although if data comes in according to their expectation no rate cut should be imminent. We still expect the first rate cut in June 24 as our baseline.

Delinking the PEPP reinvestments scheme and the policy rate path

The ECB decided today to announce the PEPP reinvestment schedule for 2024. While that was earlier than our expectation – which was for the next meeting in January – the calibration of full reinvestments in H1 24 and only EUR7.5bn/m on average is a dovish surprise. Currently, the PEPP redemptions amount to EUR18bn/m on average, which means that in the second half of next year, the ECB will still reinvest more than EUR10bn on average per month. This was also observed with the Italian-German yield spread compression on the back of the announcement. BTPs-Bund spreads are now trading around 167bp.

We judge that the moderate sell-off in rates markets following the ECB decision and through the press conference should be seen as markets getting confirmation of Lagarde not being more dovish than Powell, rather than Lagarde being hawkish as such. According to their expectations, there will not be an immediate cut delivered, but the data dependency weighs higher than the time dependency. Focus will turn to the incoming labour market data. Should data follow according to the staff projections, which saw an upward revision of wage growth for 2024, markets should reprice accordingly.

With the decision to delink the PEPP reinvestments and the policy rate path, the ECB has essentially given markets a green light to trade the narrative they want. Markets have recently repriced policy rate expectations strongly, and Lagarde only gave a conditional push-back in the sense that should data come in according to the ECB's expectations, they also expect markets to reprice accordingly. We continue to like our call for the first rate cut of 25bp coming in June, albeit should data come in weaker than anticipated, particularly wage growth in the early part of next year, the risk is for a rate cut earlier than that.

Weak economic activity lowers staff projections of growth and inflation

Lagarde characterised the current economic environment as a period with weak and slightly negative growth, particularly due to the manufacturing sector. Service sector activity is set to soften due to the lagged effects of monetary tightening, but rising real incomes should underpin growth next year. The labour market is still resilient, although vacancies have fallen in recent months. Base effects and fading fiscal energy support measures imply that inflation will decline more gradually next year compared with this year.

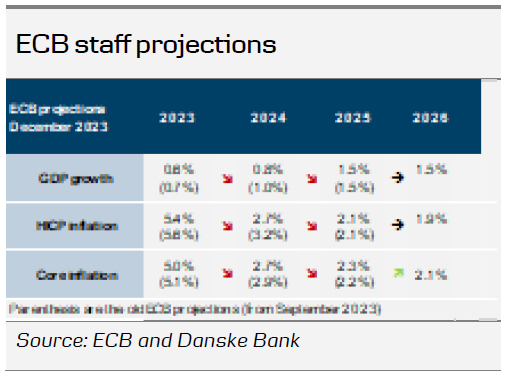

On the back of the economic assessment, new staff projections lowered the inflation forecasts for 2023 and especially 2024, while 2025 was unchanged. Headline inflation is now expected at 5.4% in 2023 (vs 5.6% in September), 2.7% in 2024 (vs 3.2% in September), 2.1% in 2025 (vs 2.1% in September), and 1.9% in 2026. The significant downward revision for 2024 compared with the September projection reflects a lower path for energy prices, the recent downside surprises in inflation, and less underlying price pressure.

The ECB acknowledged that the underlying inflationary pressure has eased recently, albeit it remains high primarily owing to strong growth in labour costs. Wage growth is expected at 4.6% in 2024, up from 4.3% in the September projections. The ECB expects wage growth at 3.8% and 3.3% in 2025 and 2026, respectively. Lagarde stressed that wage growth is the key upside risk for inflation and that the ECB needs to see more data of lower wage growth and that company profit margins can absorb the wage increases before it can start lowering interest rates. The ECB revised down projections for core inflation by 0.1pp for 2023 to 5.0% and by 0.2pp for 2024 to 2.7% due to lower activity, while projections for 2025 increased to 2.3% from 2.2%. In 2026, the ECB expects core inflation at 2.1% as it sees growth at 1.5% in both 2025 and 2026, which is around or just above its estimates of potential growth.

The near-term growth projections were revised down as past interest rate hikes continue to be transmitted forcefully onto the economy. The growth forecast for 2023 was revised down to 0.6% in 2023 (from 0.7% in September) and to 0.8% in 2024 (from 1.0% in September). Tighter financial conditions are damping demand, but the economy is still expected to recover due to rising real incomes and improving foreign demand. Risks to the economic outlook are tilted to the downside due to stronger monetary policy transmission and weak external demand. These two factors pose downward risks to the inflation outlook, while upside risks to inflation include higher than expected energy prices, wage increases and profits.

EUR/USD continues its move higher

EUR/USD moved higher following today's ECB monetary policy announcement, currently trading just below the 1.10 mark and thus close to highs seen at the end of November. Today's move is a continuation of yesterday's sharp uptick higher in response to the dovish FOMC meeting, which included a surprising dovish adjustment in the Fed dot plot. We anticipate USD weakness continuing in the near term due to the recent substantial easing of financial conditions, which should lend support to a general risk-on sentiment in markets. Combined with bearish USD year-end seasonality, this could provide some support to EUR/USD in the next months. Further out, we expect USD to regain strength and see EUR/USD falling towards 1.04 on a 12M horizon. We also remain short EUR/USD via a 6M put spread as part of our FX Top Trades 2024.

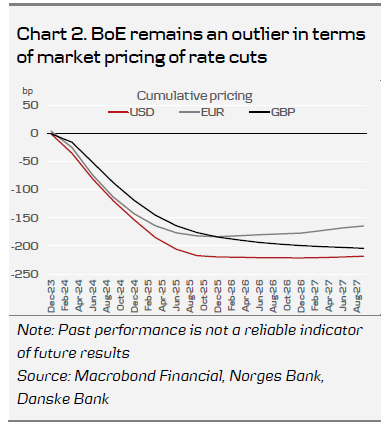

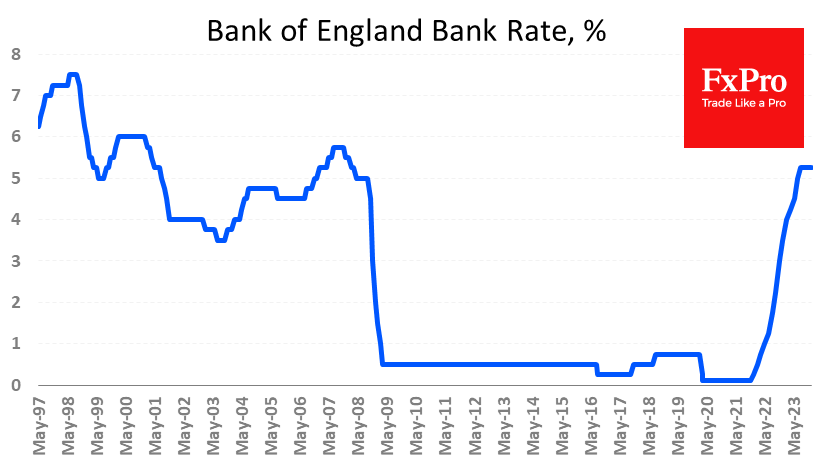

Bank of England Review – Push-Back on Rate Cut Expectations

- At today's monetary policy meeting the BoE left the key policy rate unchanged at 5.25% as widely expected.

- The BoE delivered hawkish communication in an attempt to push-back on markets expectation of rate cuts next year.

- EUR/GBP declined on the back of the statement but fully retraced the move following the ECB meeting, in line with our expectation.

As expected, the Bank of England (BoE) decided to keep the Bank Rate (key policy rate) unchanged at 5.25%. The vote split mirrored that of the November meeting as 6 members voted for an unchanged decision and 3 members voted for an increase of 25bp in the Bank Rate.

The majority of the Monetary Policy Committee (MPC) voted to keep the Bank Rate unchanged citing that, although some news in key data have been to the downside since the MPC's previous decision, changes to the overall outlook look limited. Additionally, the group noted that it was too early to conclude that services price inflation and pay growth were on a firmly downward path, indicating that talks of rate cuts were still premature.

As expected, focus of the statement and minutes, as seen with recent MPC commentary, was to push back expectations on rate cuts in order to prevent financial conditions from easing prematurely. The BoE reiterated that "monetary policy will need to be sufficiently restrictive for sufficiently long" and "is likely to need to be restrictive for an extended period of time". The BoE retained its forward guidance repeating that "further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures". Likewise, in a broadcast interview following the release of the statement, Governor Bailey noted that it is too early to speculate about rate cuts and that he could not definitively say that rates have already peaked.

Overall, we expect the UK economy to show further signs of weakness, inflation to level off and wage growth to have peaked as shown by recent data releases. Coupled with global momentum and more rate cuts being priced in for peers, we expect this to spill over to the BoE pricing (in line with our call).

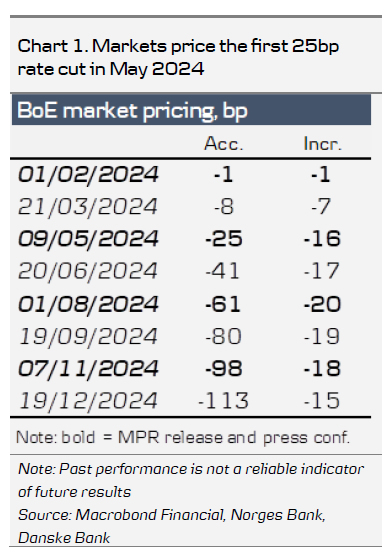

Rates. Overall, the reaction in rates markets was relatively muted. 2Y Gilt yields moved 5bp higher on the statement but remain more than 20bp lower than Monday's highs. While the SONIA-curve inverts from Q1'24 the first 25bp rate cut is not priced before May 2024.

FX. Following the release of the statement, EUR/GBP moved lower, breaching the 0.86 mark but fully retraced the move during the afternoon. Overall, we see relative rates as a negative for GBP and see the recent rebound as attractive levels to sell GBP. We continue to forecast EUR/GBP to move modestly higher the coming year to 0.89.

Our call. We expect the first rate cut of 25bp in June 2024 and subsequently 25bp cuts in the following quarters, totalling of 75bp of cuts for 2024. This is less than current market pricing (110bp). We do not see the BoE deviating from the Fed and ECB by the extent currently priced by markets and expect markets to scale back on expectations from the latter.

Sunset Market Commentary

Markets

No surprise from the ECB today as the central bank kept its deposit rate unchanged at 4%. While inflation has dropped in recent months, it is likely to pick up again temporarily in the near term. New staff projections show downward revisions to inflation forecasts this (5.4% from 5.6%) and next (2.7% from 3.2%) year with the 2025 forecast unchanged (2.1%) and the first estimate for 2026 suggesting a return below the 2% inflation target (1.9%). Underlying core inflation however is projected to remain above 2% over the full policy horizon. ECB staff see growth picking up from an average of 0.6% for 2023 (from 0.7%) to 0.8% (from 1%) for 2024, and to 1.5% for both 2025 (unchanged) and 2026 on rising real incomes and improving foreign demand. Unlike Fed Chair Powell, ECB Lagarde did push back against market expectations of rapid rate cuts: “we should absolutely not lower our guard on inflation”. She suggested that the flatter inflation path was still based on market rates at the end of November cut-off date (3-month forward Euribor curve at least about 25 bps higher) and that wage data aren’t declining yet. She also stressed that there was absolutely no debate or discussion on rate cuts, unlike yesterday’s Powell hints. ECB rates will plateau for some time. Finally, the ECB decided to advance the normalization of its balance sheet by stopping full PEPP reinvestments after H1 2024. Over H2 2024, the central bank intends to reduce the portfolio by €7.5bn/month before discontinuing reinvestments all together at the end of 2024. In a daily perspective, European yields recover from huge, Fed-induced, opening losses. EUR/USD extends yesterday’s rally from 1.09 to 1.0950 while European stock markets trade nice gains for a 0.50% surplus.

he Bank of England kept its policy rate unchanged at 5.25% in a 6-3 vote similar to the one in November. BoE Greene, Haskel and Mann again voted in favour of a 25 bps rate hike but couldn’t tip the “finely balanced” status quo. The MPC nevertheless judged that monetary policy was likely to need to be restrictive for an extended period of time with further tightening being required if there were evidence of more persistent inflationary pressures. BoE governor Bailey confirmed that “there is still some way to go to get inflation all the way back to 2%”. Upward risks to services inflation and wage growth are key in the short term, suggesting inflation won’t repeat the drop from September to October (6.7% to 4.6%), but rather stabilize near to its current rate. BoE staff expect Q4 GDP growth to be flat compared with 0.1% growth in the November Monetary Policy Report. Chancellor Hunt’s fiscal measures announced in the Autumn Statement will increase the level of GDP by around 0.25% over coming years, but boost potential supply to some extent as well and thereby reduce inflationary pressures. The BoE’s tone contrasted with the Fed as well with UK yields showing a similar intraday rebound. EUR/GBP is unchanged near 0.8620.

News & Views

The Swiss national Bank (SNB) left its policy rate unchanged at 1.75%. The SNB statement omitted guidance that further tightening still might be needed. According to the new SNB projections, inflation will be within the 0%-2% target over the policy horizon. SNB governor Jordan at the press conference said that monetary conditions are now adequate. The SNB expects modest growth between 0.5% and 1.% next year. In this environment, unemployment is likely to continue to rise gradually. On further steps (easing), Jordan indicated that the SNB will look very careful at the new forecast in March. The SNB remains prepared to be active in the FX market, but didn’t repeat that this will be in the direction of selling FX. The SNB might even change tactics if the exchange rate makes monetary policy too restrictive. The Swiss franc traded volatile after the meeting and briefly weakened above EUR/CHF 0.95 (currently 0.949). The easing of global conditions clearly mitigates the impact of the change in tone at the SNB.

The Norges Bank (NB) surprised markets by proceeding with a final 25 bps rate hike to 4.5%. The NB acknowledges that the economy is cooling but inflation remains too high. In its new projections, the NB sees inflation cooling from 5.5% this year to 4.4% next year and 2.8% in 2025. However, even at the end of the policy horizon in 2026, inflation is still seen above the 2% target (2.5). The NB now shifts to a more balanced approach and guides that the policy rate will likely remain around 4.5% until autumn, before gradually moving down. Persistent weakness of the krone was an important factor for the NB to proceed with today’s rate hike. The valuation of the currency “could make it more challenging to bring down inflation” governor Ida Wolden Bache said at the press conference. In this respect, today’s rate hike at least yielded some results. EUR/NOK dropped further from the 11.70 area to 11.52 currently.

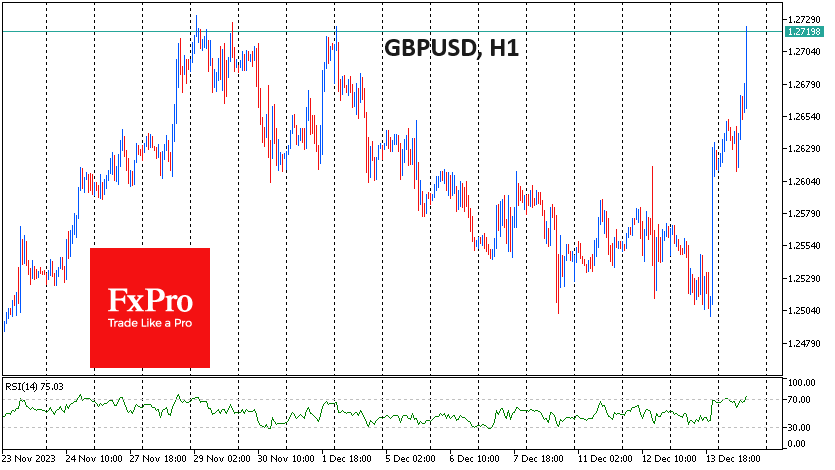

Bank of England Hawks Extend the Pound’s Rally

The Fed’s dovish attitude, for now, hasn’t extended too far into Europe. The Bank of England kept its key rate unchanged at 5.25%, with three of the nine members voting in favour of a quarter-point hike.

In a commentary on the decision, the Bank of England emphasised that it is not yet certain that inflation will return to normal through strong wage growth in the economy and higher prices for services.

The Fed is almost invariably at the forefront of the monetary policy cycle. Hence, the dollar tends to rise against its peers at the start of policy tightening and fall at the first hints of an easing reversal. GBPUSD’s reaction to the Fed and Bank of England meetings is a colourful illustration of this rule.

The willingness to ease the Fed’s policy soon weakens the USD, while the willingness to increase further strengthens the GBP. Both factors worked in the same direction within 16 hours, and as a result, GBPUSD rallied 1.7%, exceeding 1.27 – a sharp return to the highs seen a fortnight ago. The pair has now found itself in the territory of meaningful resistance since August. In addition, the latest rally looks somewhat stretched, and the currency market may go into consolidation or correction mode until the end of the year.

A Hawkish BoE Followed by An Uneventful ECB Announcement

The Bank of England and the European Central Bank both left rates on hold on Thursday but unlike following the announcement of their counterparts in the US, there were no fireworks.

Of course, it's worth noting that the press conference is yet to happen so fireworks may fly when President Lagarde speaks but the announcement and statements that followed it didn't give investors much to get excited about.

The one point of note was the reference to inflation projections being lower than in September "especially for 2024" which may be a precursor to Lagarde insinuating then the next move could be lower in the new year. How early may determine whether markets are forced to pare back very aggressive positioning.

The Bank of England announcement was arguably more notable despite offering no forecasts and there being no press conference after. The voting was unchanged from the last meeting, with three policymakers backing a rate hike, very much running counter to the message from the Fed last night.

Perhaps armed with new projections in February the message from the BoE will be very different but at this moment, that was rather more hawkish than many will have expected. And the statement still referencing higher for an extended period and higher inflation compared with other major advanced economies was clearly more hawkish.