Sample Category Title

ECB maintains interest rates, lowers inflation forecasts

ECB kept interest rates unchanged, maintaining the main refinancing rate at 4.50% and the deposit rate at 4.00%, as was widely anticipated. In a significant update, ECB substantially lowered its headline inflation forecast for 2024 from 3.2% to 2.7%. Additionally, core inflation forecasts for 2024 were slightly revised downward from 2.9% to 2.7%.

The new economic forecasts paint a picture of moderating inflation and subdued growth in the coming years. Headline inflation is expected to average 5.4% in 2023, then decrease to 2.7% in 2024, 2.1% in 2025, and 1.9% in 2026. These projections mark a notable adjustment from the September forecasts, which anticipated 5.6% in 2023 and 3.2% in 2024.

Core inflation is also expected to follow a similar downward trajectory, averaging 5.0% in 2023, 2.7% in 2024, 2.3% in 2025, and 2.1% in 2026, comparing to previous forecasts of 5.1% in 2023, 2.9% in 2024, and 2.2% in 2025

On the growth front, ECB's projections indicate modest economic performance, with growth averaging 0.6% for 2023, 0.8% for 2024, and 1.5% for both 2025 and 2026. These figures represent a downward revision from September forecasts, which predicted 0.7% growth in 2023 and 1.0% in 2024, but 2025 was unchanged at 1.5%.

The central bank reiterated that the current interest rates are positioned to substantially contribute to bringing inflation back to its target, provided they are "maintained for a sufficiently long duration." The ECB plans to continue following a "data-dependent approach" to determine the "level and duration" of policy restrictions.

(ECB) Monetary policy decisions

The Governing Council today decided to keep the three key ECB interest rates unchanged. While inflation has dropped in recent months, it is likely to pick up again temporarily in the near term. According to the latest Eurosystem staff projections for the euro area, inflation is expected to decline gradually over the course of next year, before approaching the Governing Council's 2% target in 2025. Overall, staff expect headline inflation to average 5.4% in 2023, 2.7% in 2024, 2.1% in 2025 and 1.9% in 2026. Compared with the September staff projections, this amounts to a downward revision for 2023 and especially for 2024.

Underlying inflation has eased further. But domestic price pressures remain elevated, primarily owing to strong growth in unit labour costs. Eurosystem staff expect inflation excluding energy and food to average 5.0% in 2023, 2.7% in 2024, 2.3% in 2025 and 2.1% in 2026.

The past interest rate increases continue to be transmitted forcefully to the economy. Tighter financing conditions are dampening demand, and this is helping to push down inflation. Eurosystem staff expect economic growth to remain subdued in the near term. Beyond that, the economy is expected to recover because of rising real incomes – as people benefit from falling inflation and growing wages – and improving foreign demand. Eurosystem staff therefore see growth picking up from an average of 0.6% for 2023 to 0.8% for 2024, and to 1.5% for both 2025 and 2026.

The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. Based on its current assessment, the Governing Council considers that the key ECB interest rates are at levels that, maintained for a sufficiently long duration, will make a substantial contribution to this goal. The Governing Council's future decisions will ensure that its policy rates will be set at sufficiently restrictive levels for as long as necessary.

The Governing Council will continue to follow a data-dependent approach to determining the appropriate level and duration of restriction. In particular, its interest rate decisions will be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission.

The key ECB interest rates are the primary tool for setting the monetary policy stance. The Governing Council also decided today to advance the normalisation of the Eurosystem's balance sheet. It intends to continue to reinvest, in full, the principal payments from maturing securities purchased under the pandemic emergency purchase programme (PEPP) during the first half of 2024. Over the second half of the year, it intends to reduce the PEPP portfolio by €7.5 billion per month on average. The Governing Council intends to discontinue reinvestments under the PEPP at the end of 2024.

Key ECB interest rates

The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 4.50%, 4.75% and 4.00% respectively.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The APP portfolio is declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

The Governing Council intends to continue to reinvest, in full, the principal payments from maturing securities purchased under the PEPP during the first half of 2024. Over the second half of the year, it intends to reduce the PEPP portfolio by €7.5 billion per month on average. The Governing Council intends to discontinue reinvestments under the PEPP at the end of 2024.

The Governing Council will continue applying flexibility in reinvesting redemptions coming due in the PEPP portfolio, with a view to countering risks to the monetary policy transmission mechanism related to the pandemic.

Refinancing operations

As banks are repaying the amounts borrowed under the targeted longer-term refinancing operations, the Governing Council will regularly assess how targeted lending operations and their ongoing repayment are contributing to its monetary policy stance.

***

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation returns to its 2% target over the medium term and to preserve the smooth functioning of monetary policy transmission. Moreover, the Transmission Protection Instrument is available to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across all euro area countries, thus allowing the Governing Council to more effectively deliver on its price stability mandate.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:45 CET today.

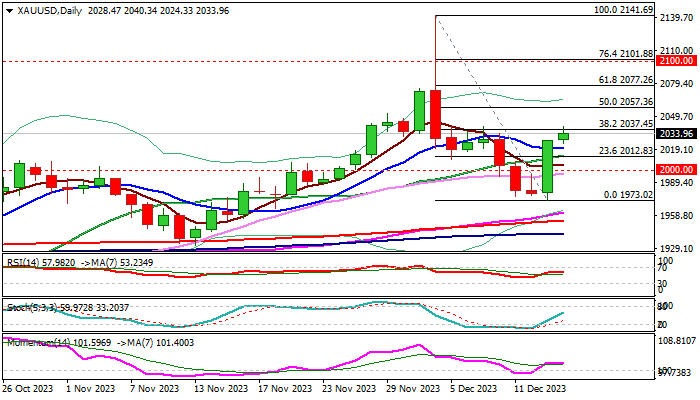

XAU/USD: Gold Price Establishes Above $2000, Lifted by Weaker Dollar

Gold extended recovery on Thursday, following 2.4% rally on Wednesday (the biggest one-day gains since Oct 13), sparked by dovish Fed.

Strong bounce is forming reversal pattern on daily chart and generates initial signal of an end of corrective phase from new all-time high ($2141).

Fresh bulls returned above $2000 and dented pivotal barrier at $2037 (Fibo 38.2% of $2141/$1973 pullback / daily Kijun-sen), close above which will add to positive near-term outlook and expose targets at $2057 and $2077 (Fibo 50% and 61.8% respectively).

Bullish daily technical studies contribute to improved fundamentals after the Fed announced that its tightening cycle is likely over and rate cuts to start in early 2024, with expectations for a total of 150 basis points easing expected next year.

Broken 10DMA ($2020) offers immediate support, which should ideally contain and guard 20DMA pivot ($2012).

Overall bias is expected to remain with bulls while the price stays above $2000 (metal is on track for the third straight weekly close above this level).

Res: 2040; 2057; 2064; 2077.

Sup: 2020; 2012; 2009; 2000.

BoE stands pat, three hawks vote for another hike

BoE kept Bank Rate unchanged at 5.25%, aligning with market expectations. The decision was not unanimous, with a 6-3 vote where Megan Greene, Jonathan Haskel, and Catherine Mann favored a 25 bps hike to 5.50%. This split decision reflects that the hawks remained persistent in their push more tighter monetary policy.

The central bank reiterated its stance that "monetary policy is likely to need to be restrictive for an extended period of time." This suggests continued cautious approach towards easing monetary conditions, likely due to persistent inflationary pressures. The Bank further emphasized that "Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures," indicating readiness to adjust policy should inflation not moderate as expected.

Regarding inflation, BoE forecasts that CPI inflation rate will hover near its current rate around the turn of the year, before gradually declining thereafter. On the growth front, BoE anticipates that GDP growth will be "broadly flat in Q4 and over the coming quarters."

(BOE) Bank rate maintained at 5.25%

Monetary Policy Summary, December 2023

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 13 December 2023, the MPC voted by a majority of 6–3 to maintain Bank Rate at 5.25%. Three members preferred to increase Bank Rate by 0.25 percentage points, to 5.5%.

In the MPC's November Monetary Policy Report projections, conditioned on a market-implied path for Bank Rate that remained around 5¼% until 2024 Q3 and then declined gradually to 4¼% by the end of 2026, GDP was expected to be broadly flat in the first half of the forecast period, in part reflecting relatively weak potential supply, and an increasing degree of economic slack was expected to emerge from the start of next year. In the most likely, or modal, projection, CPI inflation returned to the 2% target by the end of 2025 and fell below the target thereafter. The Committee continued to judge that the risks to its modal inflation projection were skewed to the upside, such that the mean projection for CPI inflation was 2.2% and 1.9% at the two and three-year horizons.

Since the MPC's previous meeting, advanced-economy government bond yields have fallen materially, including at shorter horizons, and risky asset prices have risen. Global GDP growth has been a little stronger than projected in the November Report. Consumer price inflation in the euro area and the United States has declined more quickly than expected. There remain upside risks to inflation given events in the Middle East, although oil and wholesale gas futures prices have fallen.

UK GDP was flat in 2023 Q3, in line with the November Report projection, and fell by 0.3% in October. Based on the latest official and survey data, Bank staff expect GDP growth to be broadly flat in Q4 and over coming quarters. The Committee continues to consider a wide range of data on developments in labour market activity. Employment growth is likely to have softened, and there has been further evidence of some loosening in the labour market.

Relative to the assumptions in the November Report, the fiscal measures in the Autumn Statement are provisionally estimated to increase the level of GDP by around ¼% over coming years. As these measures will probably also boost potential supply to some extent, the implications for the Committee's output gap projection, and hence inflationary pressures in the economy, are likely to be smaller.

Annual private sector regular Average Weekly Earnings (AWE) growth declined to 7.3% in the three months to October, 0.5 percentage points below the November Report projection. That has brought AWE somewhat more into line with other indicators of pay growth, which have fallen below 7%. There remain upside risks to the outlook for wage growth, including from the possible effects of the recently announced increase in the National Living Wage.

Twelve-month CPI inflation fell sharply from 6.7% in September to 4.6% in October. Services price inflation declined to 6.6%, although much of the downside news relative to the November Report reflected movements in components that may not provide a good signal of underlying trends in services prices and of persistence in headline inflation.

CPI inflation is expected to remain near to its current rate around the turn of the year. In particular, services price inflation is projected to increase temporarily in January, related to base effects from unusually weak price movements at the start of this year, before starting to fall back gradually thereafter. The near-term path for CPI inflation is somewhat lower than projected in the November Report, in part reflecting recent declines in energy prices.

The MPC's remit is clear that the inflation target applies at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognises that there will be occasions when inflation will depart from the target as a result of shocks and disturbances. Monetary policy will ensure that CPI inflation returns to the 2% target sustainably in the medium term.

Since the MPC's previous decision, CPI inflation has fallen back broadly as expected, while there has been some downside news in private sector regular AWE growth. However, key indicators of UK inflation persistence remain elevated. As anticipated, tighter monetary policy is leading to a looser labour market and is weighing on activity in the real economy more generally. Given the significant increase in Bank Rate since the start of this tightening cycle, the current monetary policy stance is restrictive. At this meeting, the Committee voted to maintain Bank Rate at 5.25%.

The MPC will continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation. Monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with the Committee's remit. As illustrated by the November Monetary Policy Report projections, the Committee continues to judge that monetary policy is likely to need to be restrictive for an extended period of time. Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures.

Minutes of the Monetary Policy Committee meeting ending on 13 December 2023

1: Before turning to its immediate policy decision, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices.

The international economy

2: UK-weighted global GDP was estimated to have grown by 0.5% in 2023 Q3, a touch stronger than projected in the November Monetary Policy Report. Growth among advanced economies had diverged, with significantly weaker growth in the euro area than in the United States. In Q4, global GDP growth was expected to slow to 0.4%.

3: Euro-area GDP had contracted by 0.1% in the third quarter, just above the November Report projection, and was expected to be flat in 2023 Q4. Near-term indicators such as services and manufacturing output PMIs had stabilised over recent months, albeit at levels indicating a contraction in activity. Industrial production had remained weak, particularly in energy-intensive sectors.

4: By contrast, US GDP had grown by 1.3% in 2023 Q3, stronger than had been expected in the November Report, but was projected to slow markedly in the fourth quarter. Recent data releases had shown signs of softening consumption growth, and both services and manufacturing ISM PMIs had weakened relative to the third quarter.

5: In China, GDP had grown by 1.3% in 2023 Q3. Going forward, growth was expected to slow given relatively weak momentum in recent indicators such as PMIs. Annual consumer price inflation in China had turned negative over recent months, in part accounted for by lower food prices.

6: Since the MPC's November meeting and despite the continuing conflict in the Middle East, the Brent spot oil price had fallen by 17%, to around $75 per barrel, owing to a combination of slowing global demand, evidence of supply increases from non-OPEC countries, less binding OPEC supply cuts than had been anticipated by market participants, as well as healthy US inventory growth. European wholesale gas spot and near-term futures prices had fallen by nearly 30%, as storage levels were almost full going into winter and as forecasts of warmer weather had curbed demand expectations, while supply had been boosted by a re-opening of Israel's production capacity.

7: The Committee discussed the relative extent of disinflation across advanced economies and the risks around the global inflation outlook. Consumer price inflation had declined more quickly in the euro area and the United States over recent months than had been expected in the November Report. According to the flash estimate, annual euro-area headline HICP inflation had fallen to 2.4% in November. Energy and food prices had contributed to the decline, and core goods and services price inflation had also declined such that core inflation had fallen to 3.6%. In the United States, headline CPI inflation had fallen to 3.1% in November, with energy price deflation contributing to the decline. Core CPI inflation had remained more stable in recent months, at 4.0%, as core services price inflation had eased more slowly.

8: Relative to both economies, core inflation had fallen back by less in the United Kingdom, to 5.7% in October, reflecting smaller declines so far in core goods price inflation and more elevated services price inflation. To the extent that they were broadly comparable, measures of wage inflation were also considerably higher in the United Kingdom than elsewhere, even though there were signs of easing in all three economies.

9: Looking forward, domestically generated inflationary pressures in most advanced economies remained elevated and could yet keep headline inflation above central bank targets for some time. There was also a risk that developments in the Middle East could lead to a renewed rise in energy, and potentially other traded goods, prices. Such a shock would push inflation higher once again, and could interact with inflation expectations and lead to second-round effects.

Monetary and financial conditions

10: Since the Committee's previous meeting, government bond yields had fallen materially across major advanced economies, including at shorter horizons. Corporate credit spreads had also declined and equity prices had picked up.

11: Market pricing suggested that policy interest rates in most major advanced economies were at their expected peaks and would remain there for several months. In contrast to developments during much of this year, recent economic news had had less impact on expected peak policy rates, which had remained relatively stable. Instead, recent news had tended to affect, and on net reduce, the length of time policy rates were expected to stay at the peak.

12: In the United Kingdom, all of the respondents to the Bank's latest Market Participants Survey (MaPS) expected Bank Rate to be left unchanged at this MPC meeting. The median MaPS respondent expected Bank Rate to remain at 5.25% until the second half of 2024, before declining gradually. Option-implied market pricing suggested that market participants had increased the probability they placed on Bank Rate remaining at its current level in three months' time. The fall in longer-term UK government bond yields since the previous MPC meeting had been somewhat less pronounced than in the United States and in the euro area. Broadly consistent with this, the sterling effective exchange rate had ended the period around 2% higher.

13: Despite having fallen since the MPC's previous meeting, ten-year government bond yields across major advanced economies remained materially higher than at the start of the current monetary policy tightening cycle, by around 325 basis points in the United Kingdom. There was some evidence that UK long rates had been more sensitive to changes in short rates during this tightening cycle than during the period before the global financial crisis, perhaps because of changes in market participants' perceptions about the level of the neutral rate of interest and about inflation persistence.

14: Medium-term inflation compensation measures in the United Kingdom had fallen slightly relative to the MPC's previous meeting. Although interpreting the level of these measures continued to be difficult, they had remained lower than their peak in March 2022, but above their average levels of the previous decade. The median MaPS respondent's expectation for CPI inflation three years ahead was 2.0% in the latest survey, down slightly relative to the previous survey.

15: Aggregate sterling net lending by banks (M4Lex) had fallen in October, and the twelve-month growth rate had continued to be negative, albeit slightly less so than in September. Within that, annual growth in gross mortgage lending had slowed further. Quoted rates on fixed-rate mortgage products had fallen further since the MPC's previous meeting, largely reflecting the pass-through of reductions in their corresponding risk-free reference rates.

16: The annual growth rate of aggregate sterling broad money (M4ex) had remained negative in October, at around -3%. Within that, annual growth in household deposits had continued to slow, such that the ratio of household deposits to gross disposable income, which had increased sharply during the Covid lockdown period in 2020, had now fallen to just above its pre-Covid level.

Demand and output

17: The level of real GDP had been unchanged in 2023 Q3, in line with expectations at the time of the November Monetary Policy Report, but weaker than the positive growth that had been recorded during the first half of the year. Domestic demand growth had been weaker than expected in Q3, with household consumption estimated to have fallen by 0.4%, and business and housing investment down by 4.2% and 1.3% respectively.

18: Monthly GDP had fallen by 0.3% in October, weaker than had been expected though following a 0.2% increase in September. The declines in output had been broad based across the services, production and construction sectors. Abstracting from volatility in government health services output, market sector activity had fallen to its lowest level since December 2022.

19: Set against that softness, the S&P Global/CIPS UK composite output PMI had risen back above 50 in November, consistent with broadly unchanged GDP. Business survey indicators of future growth had also remained more positive. The latest intelligence from the Bank's Agents suggested that demand had weakened slightly further over recent weeks, however. Overall, Bank staff now expected GDP to be flat in 2023 Q4, compared with the 0.1% positive growth that had been projected in the November Report.

20: Signs of weakening in household consumption had become more evident since the MPC's previous meeting. Real household labour incomes looked to have continued to rise during the second half of the year. Nevertheless, retail sales volumes had declined by 0.3% in October, following a 1.1% fall in September, which had taken spending to its lowest level since the 2021 Covid lockdown period. The Bank's Agents had also reported flat or falling consumer goods volumes compared to a year ago. GfK consumer confidence had risen in November, although it had been broadly flat since the spring at an historically weak level.

21: Alongside continued falls in housing investment, indicators of housing market activity and prices had remained weak. The UK House Price Index had declined by 0.5% in September but that had reversed a similar-sized increase in August, and prices had been broadly unchanged over the previous year. More timely indicators of prices had picked up a little over recent months. A range of indicators of housing construction activity were consistent with a further decline in dwelling investment at the end of this year.

22: The Autumn Statement had taken place on 22 November, accompanied by an Economic and fiscal outlook from the Office for Budget Responsibility (OBR). The OBR had judged that the medium-term fiscal outlook had improved, with receipts being boosted by the interaction of higher nominal earnings and frozen tax thresholds.

23: Additional fiscal measures had been announced in the Statement, including a 2 pence cut in the main rate of employee National Insurance Contributions, a permanent 100% capital allowance for qualifying business investment, and a package of reforms to welfare and health services designed to increase labour market participation. Relative to what had been assumed in the November Report, Bank staff had provisionally estimated that these additional measures could increase the level of GDP by around ¼% over coming years. As the measures would probably also boost potential supply to some extent, the implications for the Committee's output gap projection, and hence inflationary pressures in the economy, were likely to be smaller. A full assessment of this news would be conducted as part of the February Report forecast round.

Supply, costs and prices

24: Reflecting in part the increased uncertainties around the ONS's official labour market activity data, the Committee was continuing to consider a wide range of indicators that collectively pointed to some loosening in the labour market. The ONS was expected to release updated Labour Force Survey (LFS) estimates in January to reflect more recent UK population figures, including higher net migration since 2021.

25: Quarterly employment growth had been slowing, as reflected by the HMRC PAYE Real Time Information measure, and broadly in line with the November Monetary Policy Report projection. Contacts of the Bank's Agents had reported softening labour demand relative to supply over the past year, consistent with surveys such as the REC/KPMG Report on Jobs that had also indicated a continued easing in recruitment difficulties. The ONS's experimental estimate of the unemployment rate, based on the LFS data for June projected forward in line with the claimant count, had remained flat at 4.2% in the three months to October. The vacancies-to-unemployment ratio had fallen to 0.66 in the three months to October, slightly above the levels seen just prior to the pandemic, accounted for mainly by a fall in vacancies.

26: Indicators of pay growth had declined, although they had remained elevated overall. Annual private sector regular Average Weekly Earnings (AWE) growth had been 7.3% in the three months to October, 0.8 percentage points lower than in the three months to July and 0.5 percentage points lower than the November Report projection. This decline had brought the AWE series somewhat more in line with, but still higher than, other indicators of pay that had dipped below 7% in October. Excluding government-related sectors, a Bank staff calculation based on HMRC PAYE Real Time Information suggested that median pay growth had fallen further in November, although these data were early estimates subject to revision.

27: The downward trend in wage growth was broadly consistent with more forward-looking indicators. Expectations for future wage growth from the Decision Maker Panel (DMP) Survey had fallen to 5% in October from around 6% at the start of the year. Early intelligence from the Bank's Agents signalled a fall in average annual pay settlements in 2024. The Committee noted continued upside risks to wage growth forecasts, however. This included the direct and possible indirect effects of the recently announced increase in the National Living Wage, for example if existing pay relativities within businesses were re-established.

28: Twelve-month CPI inflation had fallen sharply from 6.7% in September to 4.6% in October, 0.2 percentage points below the November Report forecast. The latest CPI release had triggered the exchange of open letters between the Governor and the Chancellor of the Exchequer that was being published alongside these minutes.

29: The decline in CPI inflation over recent months could largely be attributed to falls in energy, food, and core goods price inflation, as external cost pressures had continued to abate. Services price inflation had remained elevated, however.

30: The reduction in the Ofgem energy price cap in October had reduced materially the typical household energy bill compared to a year ago. Despite the announced rise in the price cap by around 5% in January, energy was expected to continue to contribute negatively to annual CPI inflation over the next six months, and to a greater extent than had been expected previously, reflecting the recent declines in oil prices as well as in wholesale gas futures prices if sustained.

31: Core goods price inflation was projected to fall further in coming quarters, reflecting base effects and decreasing cost pressures, including from easing global goods price inflation. Contacts of the Bank's Agents anticipated further declines in food price inflation, with a number having revised their estimates lower compared to November.

32: Services price inflation had remained higher than overall CPI inflation at 6.6% in October, a fall of 0.3 percentage points from September and 0.3 percentage points lower than expected in the November Report. This downside news, however, had been accounted for by those components that were not typically reliable indicators of trends in inflationary persistence, such as non-private rents, accommodation and airfares. Excluding these components, services inflation had been more stable at continued high rates, in line with the preceding six months.

33: The S&P Global/CIPS UK services input and output price PMIs had remained below their peaks in early 2022, while Agents' contacts had reported that non-labour cost-pressures were moderating. Although a general easing in services price inflation was therefore anticipated over 2024, a temporary spike was likely in January. Large and unusual falls in a number of services prices at the beginning of 2023 were not expected to be repeated at the start of next year, which would increase mechanically the annual percentage change in services price inflation in January. This positive base effect was expected to increase CPI inflation from just under 4½% at the end of this year to around 4¾% in January, before falling back closer to 4% in February.

34: Inflation expectations for the year ahead had remained at elevated levels, particularly for businesses. Short-term business expectations, as measured in the DMP Survey, had eased slightly, although three-year expectations had been marginally higher. Households' short-term inflation expectations had continued to fall below the peaks seen in 2022. Longer-term household expectations had remained higher, but at close to their historical averages.

The immediate policy decision

35: The MPC sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment.

36: In the MPC's November Monetary Policy Report projections, GDP had been expected to be broadly flat in the first half of the forecast period, in part reflecting relatively weak potential supply. An increasing degree of economic slack had been expected to emerge from the start of next year, although the pace at which that slack emerged would depend on the relative contributions of supply and demand news to developments in activity. The Committee was undertaking a full review of the overall supply capacity of the economy in its regular stocktake ahead of the February Report.

37: As anticipated, tighter monetary policy was leading to a looser labour market and was weighing on activity in the real economy more generally. Based on the latest official and survey data, Bank staff expected GDP growth to be broadly flat in 2023 Q4 and over coming quarters. The Committee would continue to monitor closely the impact on activity and inflation of the significant increase in Bank Rate. It would also consider the impact of recent financial market movements on its macroeconomic projections as part of the forecast round ahead of its next meeting.

38: In the most likely, or modal, November Report projection, conditioned on a market-implied path for Bank Rate that had remained around 5¼% until 2024 Q3 and then had declined gradually to 4¼% by the end of 2026, CPI inflation had been expected to return to the 2% target by the end of 2025 and to fall below the target thereafter. The Committee had continued to judge that the risks to its modal inflation projection were skewed to the upside, such that the mean projection for CPI inflation had been 2.2% and 1.9% at the two and three-year horizons.

39: Since the MPC's previous decision, CPI inflation had fallen back broadly as expected, to 4.6% in October. Key indicators of UK inflation persistence remained elevated. Services price inflation had declined to 6.6%, although much of the downside news relative to the November Report had reflected movements in components that might not provide a good signal of underlying trends in services prices and of persistence in headline inflation.

40: There had been some downside news in private sector regular Average Weekly Earnings growth, but it was important not to over-interpret developments in any one measure, which had to be placed in the context of the evolution of broader pay dynamics. There remained upside risks to the outlook for wage growth, including from the possible effects of the recently announced increase in the National Living Wage. Relative to developments in the United States and the euro area, measures of wage inflation were considerably higher in the United Kingdom and services price inflation had fallen back by less so far.

41: The MPC's remit was clear that the inflation target applied at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognised that there would be occasions when inflation would depart from the target as a result of shocks and disturbances. Monetary policy would ensure that CPI inflation returned to the 2% target sustainably in the medium term. Monetary policy was also acting to ensure that longer-term inflation expectations were anchored at the 2% target.

42: Given the significant increase in Bank Rate since the start of this tightening cycle, the current monetary policy stance was restrictive. The decision whether to increase or to maintain Bank Rate at this meeting was again finely balanced between the risks of not tightening policy enough when underlying inflationary pressures could prove more persistent, and the risks of tightening policy too much given the impact of policy that was still to come through.

43: Six members judged that maintaining Bank Rate at 5.25% was warranted at this meeting. Although some of the news in key data had been to the downside since the MPC's previous decision, economic developments had been relatively limited overall. For most members within this group, it was too early to conclude that services price inflation and pay growth were on a firmly downward path. Both of these metrics of inflation persistence remained higher than in other major advanced economies, possibly reflecting less favourable supply-side developments and stronger second-round effects in the United Kingdom. Second-round effects were likely to be slow to unwind and, with the labour market still tight, the extent to which wage and price-setting would take account of the downward path of CPI inflation was not clear. The risks to CPI inflation in the medium term remained skewed to the upside including from events in the Middle East. For one member, the risks of overtightening policy had continued to build. Lags in the effects of monetary policy meant that sizeable impacts from past rate increases were still to come through.

44: Three members preferred a 0.25 percentage point increase in Bank Rate, to 5.5%, at this meeting. Although current indicators of economic activity had remained subdued, real household incomes had continued to edge up, and forward-looking indicators of output had remained positive. The labour market was still relatively tight, consistent with a rise in the medium-term equilibrium rate of unemployment, and the pace of loosening had been slow. Measures of wage growth had moderated slightly but had remained at rates above those consistent with the inflation target. Underlying services price inflation had remained elevated. These members continued to judge that there was evidence of more persistent inflationary pressures. Financial conditions had eased since the November Report. An increase in Bank Rate at this meeting was necessary to address the risks of more deeply embedded inflation persistence and to return inflation to target sustainably in the medium term.

45: The MPC would continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation. Monetary policy would need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with the Committee's remit. As was illustrated by the November Monetary Policy Report projections, the Committee continued to judge that monetary policy was likely to need to be restrictive for an extended period of time. Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures.

46: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be maintained at 5.25%.

47: Six members (Andrew Bailey, Sarah Breeden, Ben Broadbent, Swati Dhingra, Huw Pill and Dave Ramsden) voted in favour of the proposition. Three members (Megan Greene, Jonathan Haskel and Catherine L Mann) voted against the proposition, preferring to increase Bank Rate by 0.25 percentage points, to 5.5%.

Operational considerations

48: At its September 2023 meeting, the MPC had voted to reduce the stock of UK government bond purchases held for monetary policy purposes by £100 billion over the 12-month period from October 2023 to September 2024, comprising both maturing gilts and sales. The MPC had been briefed on progress on these gilt sales and on the operational arrangements for 2024 Q1, which would be published in a Market Notice at 4.30pm on 15 December.

49: On 13 December, the total stock of assets held for monetary policy purposes was £744 billion, comprising just under £744 billion of UK government bond purchases and £0.4 billion of sterling non‐financial investment‐grade corporate bond purchases.

50: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Ben Broadbent

- Swati Dhingra

- Megan Greene

- Jonathan Haskel

- Catherine L Mann

- Huw Pill

- Dave Ramsden

Sam Beckett was present as the Treasury representative.

US 500 Index Surges to Almost 2-Year High

- US 500 index posts 5-day bullish rally

- Technical oscillators look overbought

The US 500 index (cash) stormed higher after validating the previous high of 4,607. Although, the price jumped to its highest level since January 2022 at 4,728, extending the strong rebound off 4,100 that it has last October.

Technically, the RSI climbed above the 70 level with strong momentum, and the MACD oscillator is crossing above its trigger line well above the zero level. Both indicate an overstretched market and a potential bearish correction.

If the bullish pressures persist, the price could revisit the record high of 4,817, while a jump above this area could take the index into uncharted territory, meeting the next psychological numbers such as 4,900 and 5,000.

Alternatively, should the bears attempt to push the price lower, initial declines could cease at the recent support of 4,607. Diving below that floor, the price may descend towards the 4,540 bottom ahead of the 100- and the 50-day simple moving averages (SMAs) around 4,420. Marginally below these lines, the 4,400 support is standing and then the 4,340 support is coming next. Also, the 200-day SMA at 4,321 is acting as a strong barricade for traders.

In brief, the US 500 index has exhibited strong upside momentum; however technical oscillators are looking overbought.

British Pound Rises after Fed Meeting, BoE Next

- Bank of England expected to pause

- Federal Reserve projects three rate cuts in 2024

The British pound continues to move higher on Thursday. In the European session, GBP/USD is trading at 1.2648, up 0.24%.

The US dollar took a tumble on Wednesday after the Federal Reserve gave the nod to rate cuts in 2024. This helped the pound recover after losing ground in the aftermath of a soft UK GDP report on Wednesday.

Bank of England expected to stand pat

The Federal Reserve created quite a buzz in the financial markets on Wednesday after the Fed signalled that it expected to trim rates in 2024. Will Bank of England Governor Andrew Bailey provide an encore at today’s meeting?

The BoE is widely expected to maintain the cash rate at 5.25% for a third straight time. There is little doubt that the BoE’s aggressive rate-tightening is over, with inflation falling and the UK economy limping along. The key question is whether Bailey will change his stance and signal that rate cuts are on the way, as Fed Chair Powell did at the Fed meeting.

Bailey has been hawkish, saying that rates will remain in restrictive territory for an extended period (“higher for longer”) and that there is more work needed to bring inflation back down to the Bank’s 2% target. Bailey has said that it’s premature to talk about rate cuts, but the markets aren’t buying it and have priced in five quarter-point rate cuts in 2024, up from three cuts just a few days ago. With a pause widely expected at today’s meeting, the rate statement and Bailey’s press conference could provide some drama and shake up the financial markets, if the BoE shifts from its hawkish stance and acknowledges that it plans to cut rates next year.

Powell’s Pivot sends US dollar lower

The Federal Reserve maintained the benchmark rate on Wednesday, as expected. What was somewhat surprising was the Fed Chair Powell’s sharp pivot, as he signalled that the Fed expected to trim rates three times in 2024. This forecast comes less than two weeks after Powell said it would be “premature” to speculate about the timing of rate cuts and that the door was still open to further hikes. The rate statement noted that inflation “has eased over the past year but remains elevated”, suggesting that inflation is moving in the right direction but the battle ain’t over yet.

GBP/USD Technical

- GBP/USD is putting pressure on resistance at 1.2669. Above, there is resistance at 1.2720

- There is support at 1.2585 and 1.2534

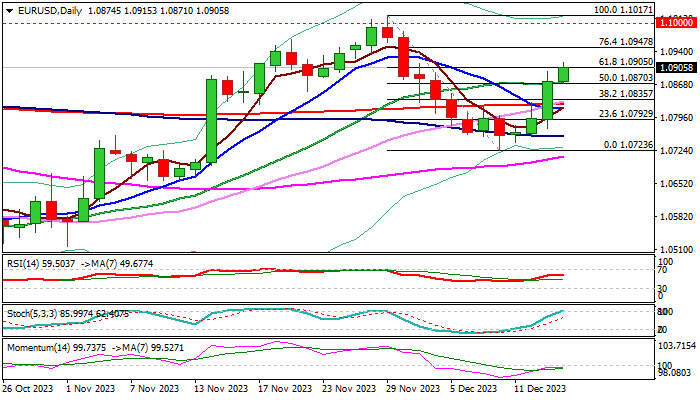

EUR/USD: Stands at the Front Foot Ahead of ECB Policy Decision

The Euro stands at the front foot on Thursday, supported by weaker dollar, which got under increased pressure after the Fed signaled and end of a tightening cycle and rate cuts in 2024.

Extended recovery from 1.0723 (correction low) hit two-week high ahead of today’s key event – ECB policy decision.

The European Central Bank is expected to keep interest rate unchanged at a record 4.5% for the second time, with focus on signals for the future steps, which will provide more details about the ECB’s stance in the near future.

Softer inflation in the Eurozone is supportive factor, however weak economic condition suggest that the ECB is unlikely to further raise interest rates, but will have more cautious approach in current conditions, as the story with fighting inflation is not over yet, but slowing economy is a strong warning.

Technical picture on daily chart has improved, as moving averages turned to bullish configuration, but momentum is still negative and stochastic indicator in overbought territory.

The Euro may rise further if policymakers turn more hawkish, though overall conditions suggest that this is unlikely scenario, while softer than expected tones may deflate the single currency.

Violation of pivotal support at 1.0827 (200DMA) would weaken near-term structure and risk deeper drop.

On the other hand, lift above 1.0947 (Fibo 76.4% of 1.1017/1.0723) would bring bulls fully in play for attack at key 1.1000/17 barriers (psychological / Nov 29 high).

Res: 1.0947; 1.0965; 1.1000; 1.1017.

Sup: 1.0870; 1.0827; 1.0817; 1.0792.

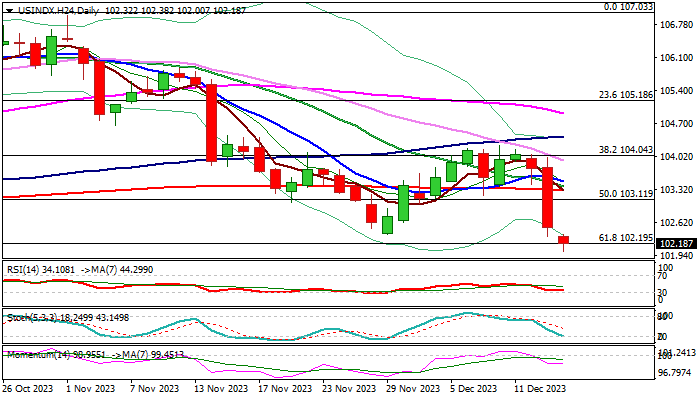

Dollar Index: Hits Four-Month Low, Deflated by Dovish Fed

The dollar index remains firmly in red and holding near fresh four-month low in early trading on Thursday, following post-Fed 1.2% fall on Wednesday (the biggest daily drop since Nov 14).

The greenback was deflated by signals that the Fed’s historic policy tightening cycle is likely over, and projections show that borrowing cost would fall next year, with growing bets for first rate cut in March and expectations for 150 basis points easing in 2024.

Wednesday’s sharp fall has fully retraced 102.36/104.24 corrective leg, with break of former low at 102.36 (Nov 29) signaling continuation of a larger downtrend from 107.03/106.96 double top (2023 highs of Oct 3 / Now 1).

Daily close below 102.36 and 102.19 (Fibo 61.8% of 99.20/107.03) will be needed to confirm signal and open way towards 101.05 (Fibo 76.4%).

Bearish daily studies (MA’s in full bearish setup / 14-d momentum in the negative territory) support the notion, with corrective upticks to be capped under 102.90/103.11 zone (base of thick weekly cloud / falling daily Tenkan-sen) to keep larger bears in play and offer better selling opportunities.

Res: 102.36; 102.90; 103.11; 103.29.

Sup: 102.00; 101.53; 101.05; 100.30.

GBP/USD, EUR/USD, USD/CAD Analysis: Dollar Falls Sharply after Fed Meeting

The American currency, having strengthened after the release of inflation data in the United States, fell sharply against almost all leading currencies yesterday. The reason for the sharp weakening of the dollar was most likely the updated median forecast of FOMC members for the dynamics of interest rates over the next few years, which does not assume a further increase in the base interest rate. As expected, the American regulator left the rate at the same level; in addition, several Fed members expect at least three rate cuts in 2024. On such news, the euro/dollar pair tested 1.0900, the pound/dollar pair consolidated above 1.2600, and the dollar/Canadian pair broke through support at 1.3500.

GBP/USD

The British currency, having tested 1.2500 after the announcement of the results of the Fed meeting, strengthened by more than 100 points in just a few hours. However, today, the situation may change dramatically. At 15:00 GMT+3, there will be a meeting of the Bank of England, at which, according to analysts, the rate will also remain at the same level. Moreover, if it turns out that less than three members of the Bank of England vote for a rate hike, the pair could return to recent lows at 1.2500.

On the daily GBP/USD chart, the price has consolidated above the alligator lines; the pair may rise above the upper fractal at 1.2720 and continue rising. Cancellation of the upward scenario can be considered if it consolidates below 1.2500.

EUR/USD

The single European currency is also awaiting a verdict from the central bank. Today at 16:30 GMT+3, there will be a meeting of the ECB, at which, according to experts, the base rate will be left at the same level of 4.50%. A press conference is scheduled for ECB head Christine Lagarde a little later. Also, important macroeconomic statistics from the eurozone are expected tomorrow. In particular, the index of business activity in the services sector for December will be published, as well as the composite PMI index for the same period.

According to the EUR/USD technical analysis, on the daily timeframe, the price is moving towards the upper fractal at 1.1020. A breakdown of the upward scenario can be considered upon a breakdown of 1.0700.

USD/CAD

The result of yesterday's Fed meeting brought the USD/CAD pair out of a long flat movement in the corridor between 1.3600 and 1.3500. Today at 16:30 GMT+3, the basic US retail sales index for November will be published. Also, at this time, the weekly number of applications for unemployment benefits will be released.

The price confidently consolidated below the alligator lines on all higher time frames. If the current mood in the market continues, a continuation of the downward movement in the direction of 1.3300-1.3200 could happen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.