Sample Category Title

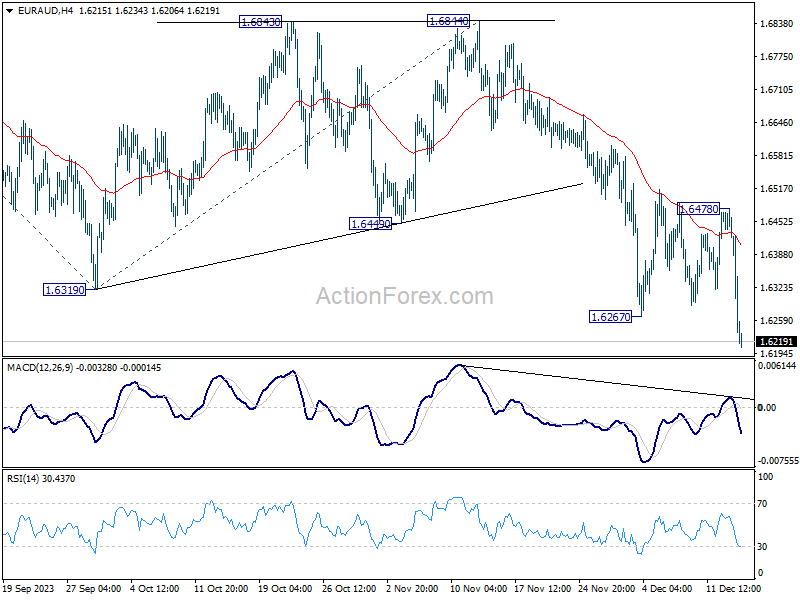

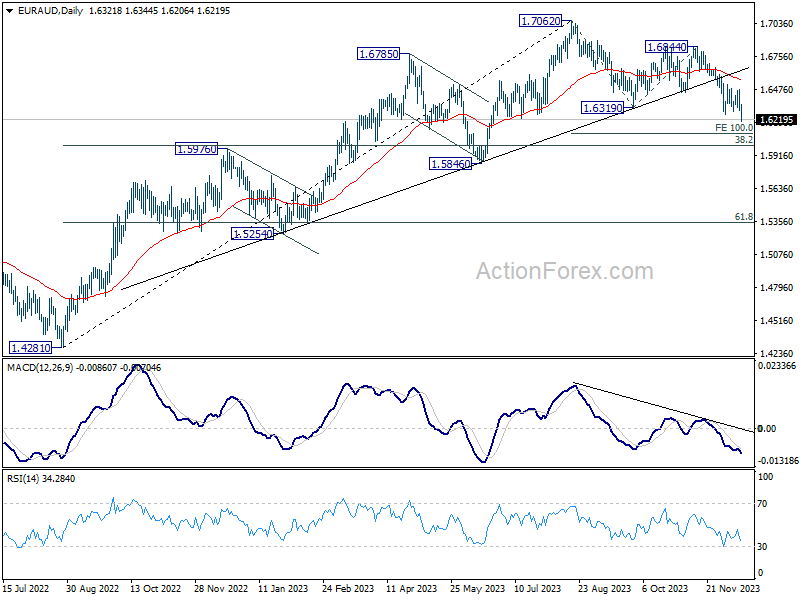

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6261; (P) 1.6371; (R1) 1.6438; More..

EUR/AUD's decline resumed by breaking through 1.6267 support and intraday bias is back on the downside. Current fall from 1.7062 should target 100% projection of 1.7062 to 1.6319 from 1.6844 at 1.6106 next. For now, outlook will remain bearish as long as 1.6478 resistance holds, in case of recovery.

In the bigger picture, fall from 1.7062 medium term top is seen as correcting the whole up trend from 1.4281 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support could be seen there to bring rebound on first attempt. But risk will stay on the downside as long as 1.6844 resistance holds. Sustained break of 1.6000 would bring further fall to 61.8% retracement at 1.5343.

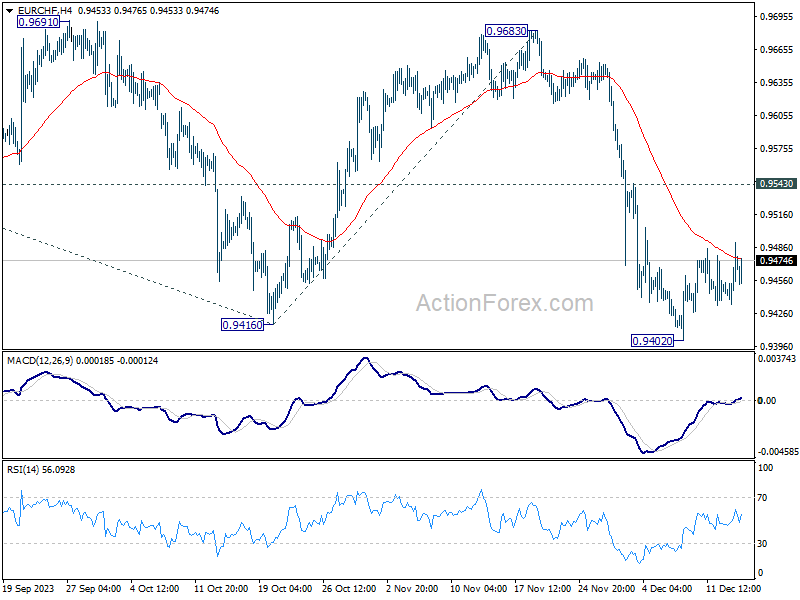

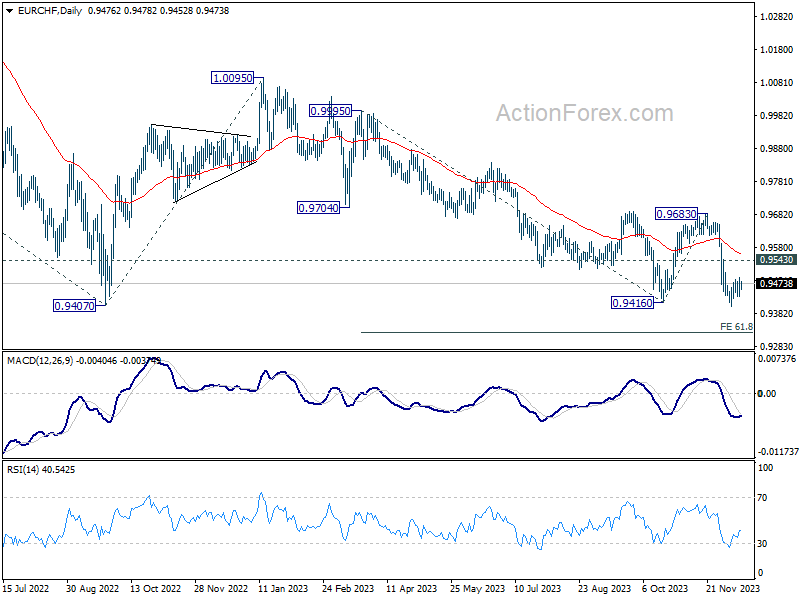

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9447; (P) 0.9469; (R1) 0.9503; More...

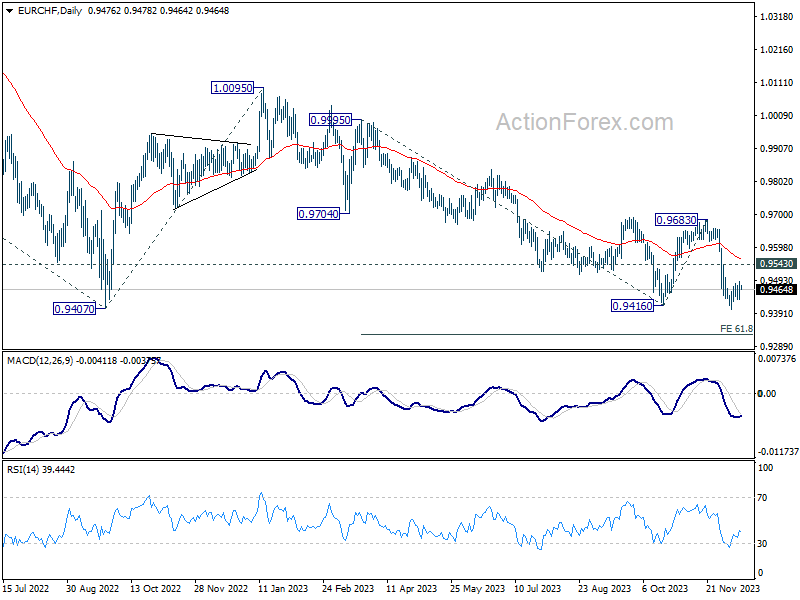

Intraday bias in EUR/CHF remains neutral as consolidation from 0.9402 is extending. Overall outlook stays bearish as long as 0.9543 resistance holds. On the downside, decisive break of 0.9407 will confirm larger down trend resumption. Next target is 61.8% projection of 0.9995 to 0.9416 from 0.9683 at 0.9325.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Firm break of 0.9407 (2022 low) will resume long term down trend. Next target will be 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

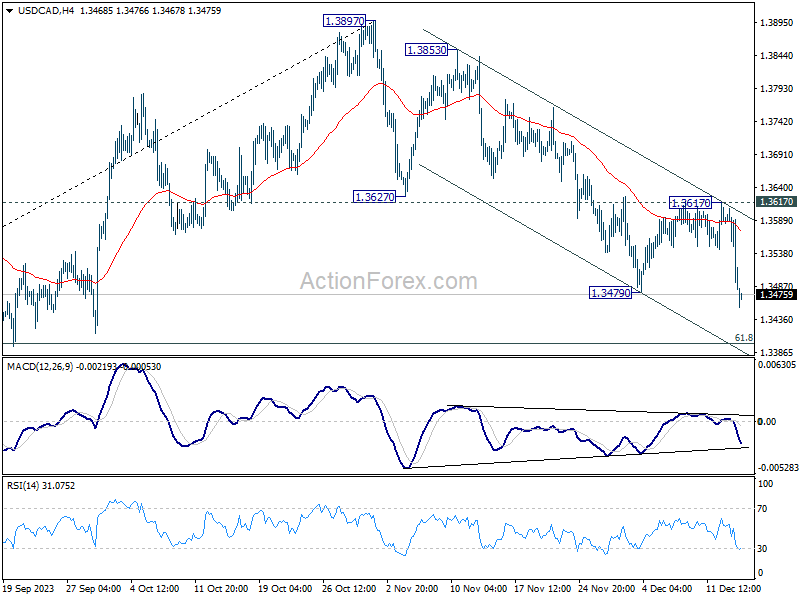

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3473; (P) 1.3540; (R1) 1.3586; More...

USD/CAD's fall from 1.3897 resumed by breaking through 1.3479 support. Intraday bias is back on the downside for 1.3378 support zone. Strong support is expected there to bring rebound. But still, break of 1.3617 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, rise from 1.3091 is seen as the fifth leg of the whole rise from 1.2005 (2021 low). Further rally is expected as long as 1.3378 support holds, to 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. However, decisive break of 1.3378 will dampen this view and bring deeper fall back to 1.3091 instead.

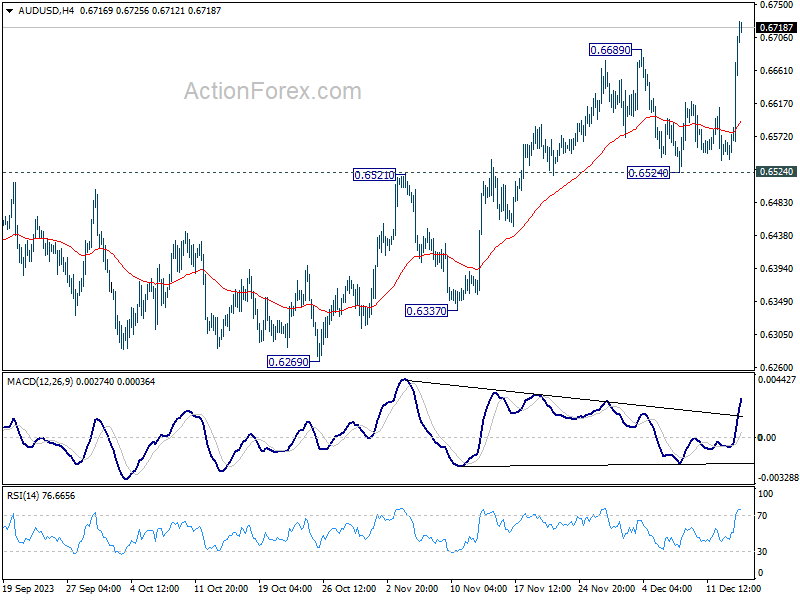

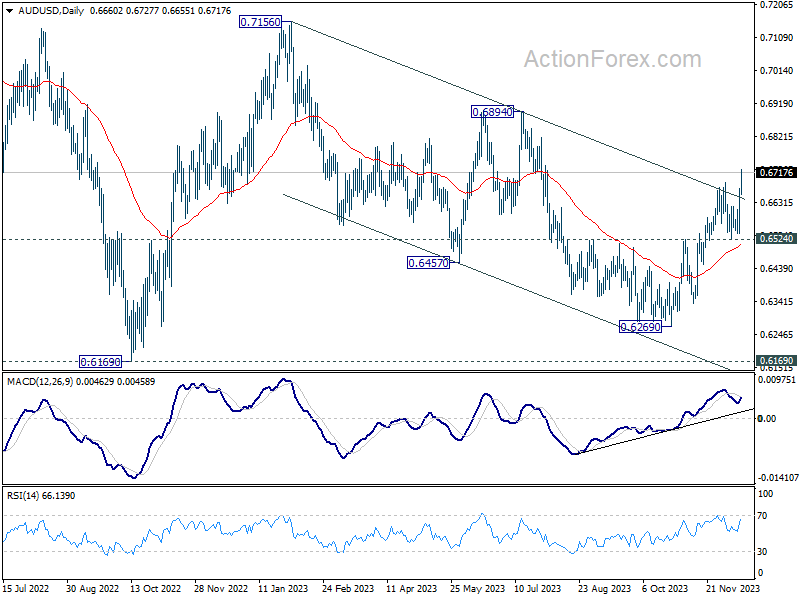

AUD/USD Daily Report

Daily Pivots: (S1) 0.6578; (P) 0.6625; (R1) 0.6709; More...

AUD/USD's rise from 0.6269 resumed by breaking through 0.6689 and intraday bias is back on the upside. Also, the firm break of medium term channel resistance suggests that whole fall from 0.7156 has completed with three waves down to 0.6269. Further rise should be seen to 0.6894 resistance next. Meanwhile, near term outlook will stay cautiously bullish as long as 0.6524 support holds, in case of retreat.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. Price actions from 0.6169 (2022 low) could be just a medium term corrective pattern. Rise from 0.6269 is seen as the third leg of the pattern. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

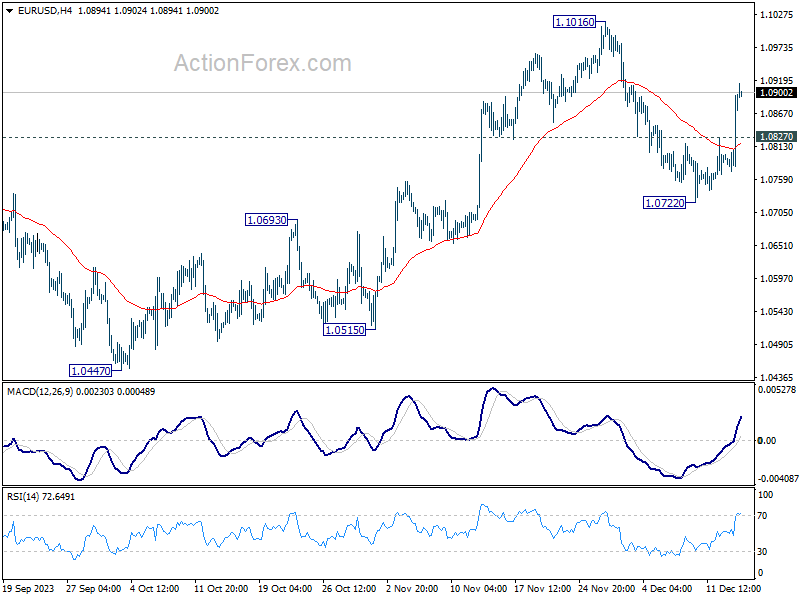

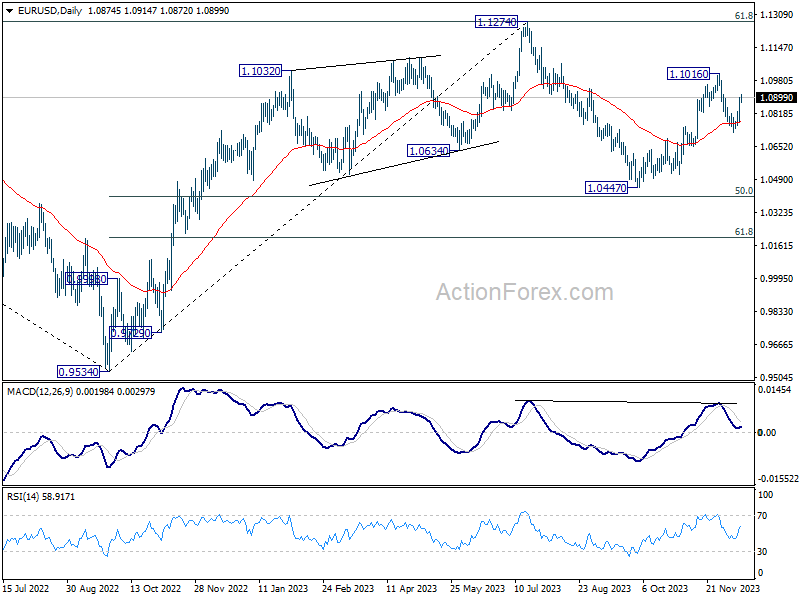

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0800; (P) 1.0848; (R1) 1.0924; More...

EUR/USD's break of 1.0827 minor resistance suggests that pull back from 1.1016 has completed at 1.0722 already, after drawing support from 55 D EMA. Intraday bias is back on the upside for 1.1016 resistance first. Firm break there will resume whole rally from 1.0447 to retest 1.1274 high. On the downside, break of 1.0722 will resume the fall from 1.1016 instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

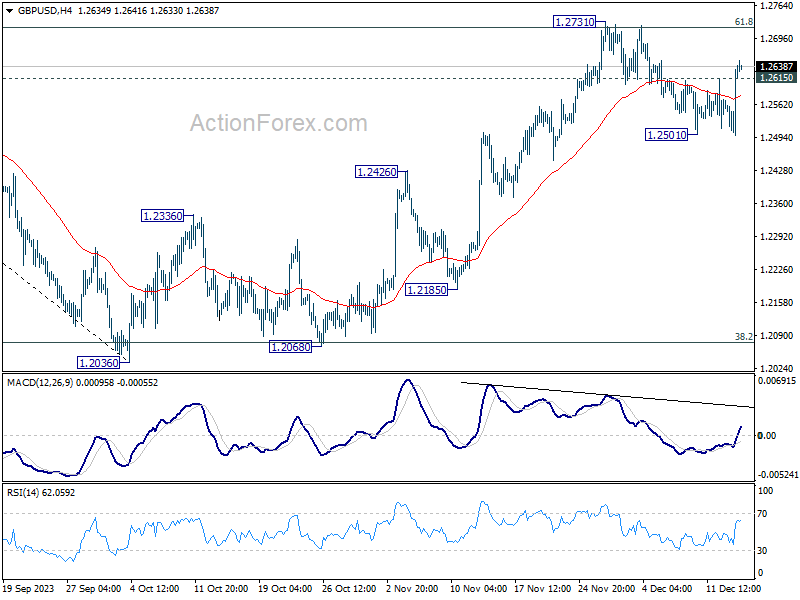

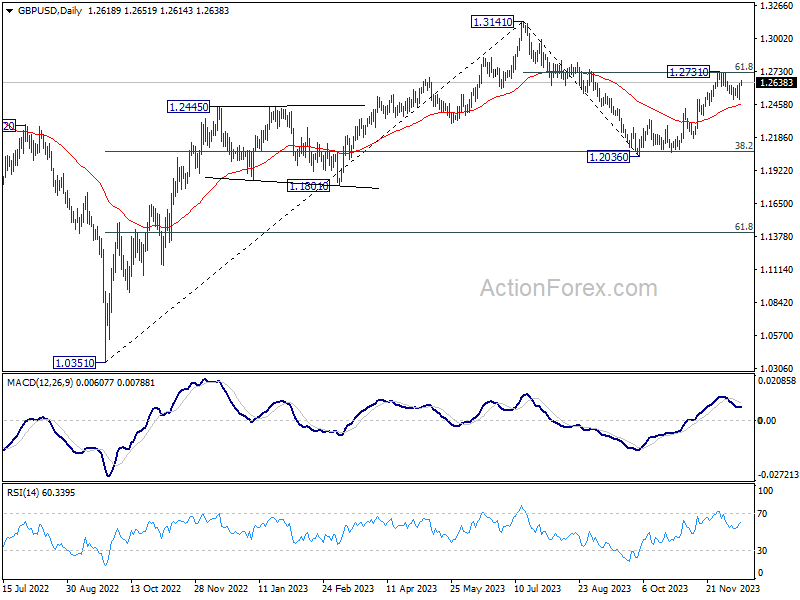

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2534; (P) 1.2585; (R1) 1.2669; More...

GBP/USD's break of 1.2615 minor resistance suggests that pull back from 1.2731 has completed at 1.2501 already. Intraday bias is back on the upside for 1.2731 first. Decisive break there will resume whole rally from 1.2036 for retesting 1.3141 high next. On the downside, break of 1.2501 will resume the pull back to 55 D EMA (now at 1.2462).

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to rise from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, that could still extend through 1.2731. But upside should be limited by 1.3141 o bring the third leg of the pattern. Meanwhile, sustained trading below 55 EMA will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again, and possibly below.

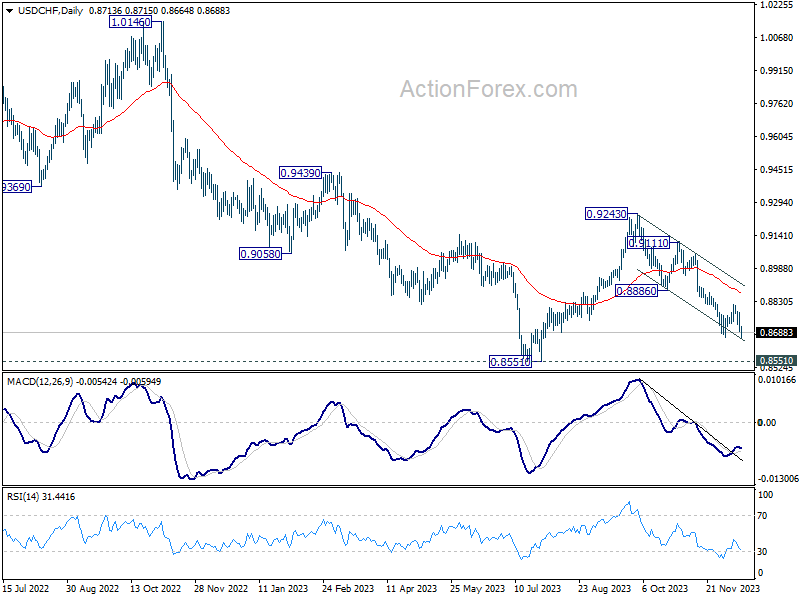

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8679; (P) 0.8729; (R1) 0.8768; More....

USD/CHF's break of 0.8722 minor support argues that recovery from 0.8665 has completed at 0.8819 already. Intraday bias is back on the downside. Firm break of 0.8665 will resume the whole fall from 0.9243 to 0.8551 key support level. On the upside, break of 0.8819 resistance is needed to indicate short term bottom. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. Meanwhile, break of 0.9111 resistance will argue that the third leg has started already, and target 0.9243 and above.

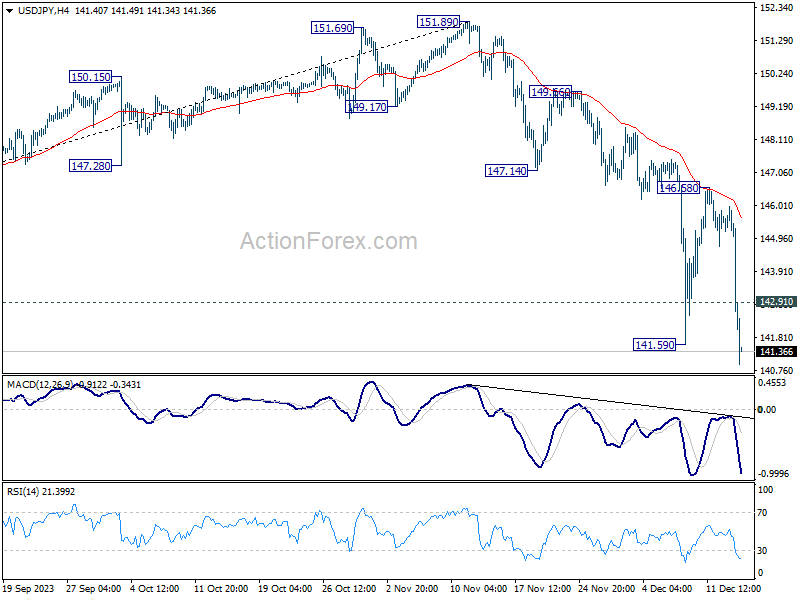

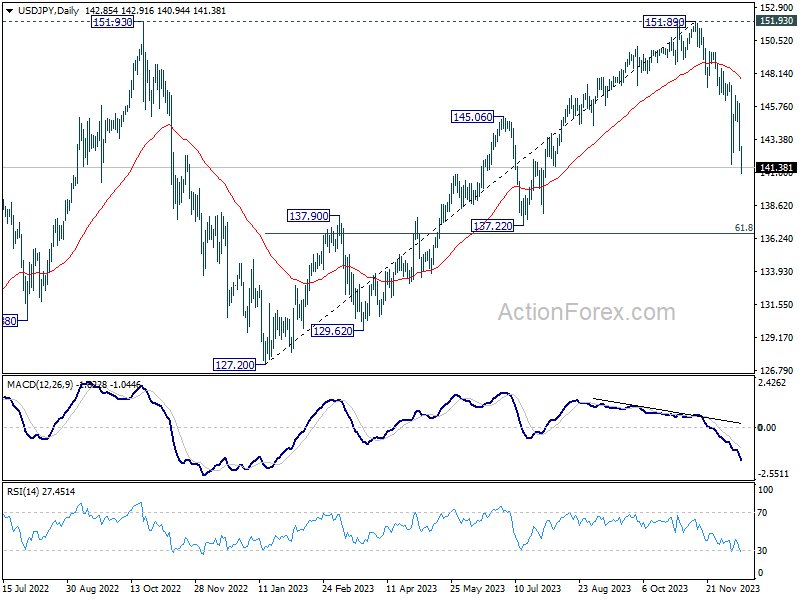

USD/JPY Daily Outlook

Daily Pivots: (S1) 144.74; (P) 145.47; (R1) 146.19; More...

USD/JPY's decline from 151.89 resumed by breaking through 141.59 support. Intraday bias is back on the downside. Further fall should be seen to next fibonacci level at 136.63. On the upside, above 142.91 minor resistance will turn intraday bias neutral first. But recovery should be limited well below 146.58 resistance to bring another decline.

In the bigger picture, current fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.

Dollar Dives after Fed, Yen Leads Gains, Europe Awaits Central Banks Decisions

Investor sentiment was buoyed strongly by Fed's projection of three rate cuts in the upcoming year. This significant dovish turn by the Fed has sparked a wave of investor optimism, propelling the DOW to record-breaking high. This buoyant mood has largely permeated the Asian markets, although Japan has remained an outlier in this trend.

Dollar declined broadly after FOMC announcement, and stays as the worst performer in the week. On the other hand, Yen has capitalized further on the falling treasury yields in the US and Europe, emerging as the strongest performer for the week so far. Australian Dollar also found support in the wake of strong Australian employment data, ranking as the second strongest currency following the Yen.

On the European front, despite making gains against the weakening greenback, both Sterling and Euro have exhibited relative weakness elsewhere. The impending monetary policy decisions from SNB, BoE, and ECB are now the center of attention. In light of Fed's dovish shift, there is heightened speculation among traders and investors that these European central banks might also hint at policy easing in the coming year, thus capping their rallies.

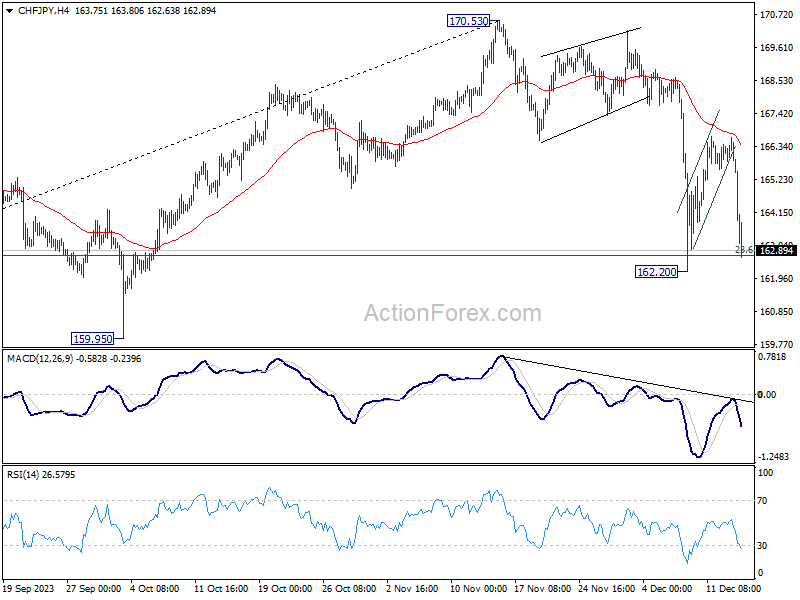

Technically, both USD/JPY and GBP/JPY have breached last week's lows of 141.59 and 178.58, suggesting that Yen might be ready to resume its near term rebound. Focus will turn to corresponding levels in other Yen crosses to confirm, including 153.15 support in EUR/JPY, 104.19 support in CAD/JPY, 93.70 support in AUD/JPY and 162.20 support in CHF/JPY. Concurrent break of these level will set the stage for broad based rally in Yen, leading to next week's BoJ meeting.

In Asia, at the time of writing, Nikkei is down -0.79%. Hong Kong HSI is up 1.02%. China Shanghai SSE is flat. Singapore Strait Times is up 0.76%. Japan 10-year JGB yield is down -0.0066 at 0.683.

Fed signals three rate cuts in 2024, policy easing on discussion table

US stocks surged, with DOW hitting new record, while treasury yields and the Dollar tumbled following Fed's decision to leave interest rates unchanged at 5.25-5.50%. This decision, widely anticipated by the markets, was overshadowed by the Fed's indication of potential rate cuts in 2024. Fed suggested that three 25 bps cuts could be implemented next year, to bring federal funds rate back to 4.50-4.75%.

Fed Chair Jerome Powell, in the post-meeting press conference, acknowledged the emerging discussion within about reducing policy restraint. Powell stated, "The question of when it will be appropriate to begin dialing back the amount of policy restraint in place begins to come into view, and is clearly a topic of discussion out in the world and also of discussion for us at our meeting today." He further noted the general expectation that this issue will be a key focus for Fed going forward.

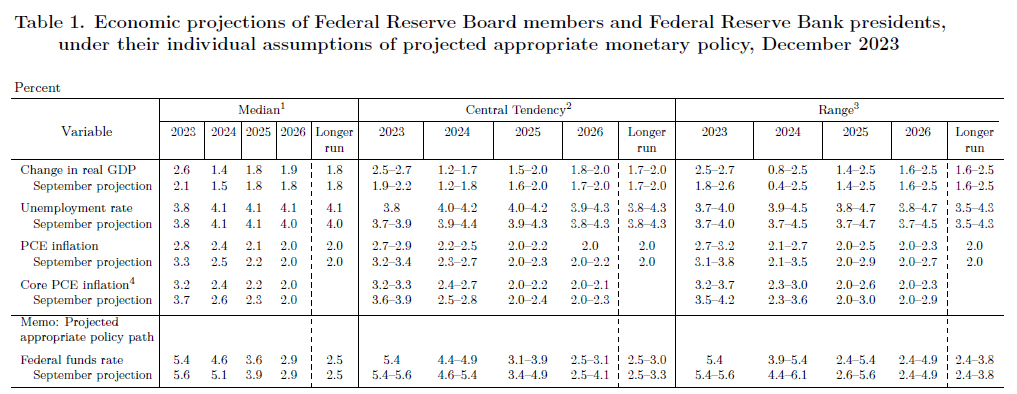

The new economic projections present a detailed outlook. The median forecasts indicate that federal funds rate will decrease from the current 5.4% to 4.6% in 2024, further reducing to 3.6% in 2025, and eventually to 2.9% in 2026. The longer-run federal funds rate is held steady at 2.50%. The central tendency for 2024 is at 4.4-4.9%, suggesting a relatively narrow range, and stable rate expectation.

The projections for GDP growth show a slowdown from 2.6% in 2023 to 1.4% in 2024, followed by a rebound to 1.8% in 2025 and 1.9% in 2026. The unemployment rate is expected to increase from 3.8% in 2023 to 4.1% in 2024 and then stabilize at this level through 2026.

Regarding inflation, headline PCE inflation is forecasted to decrease from 2023's 2.8% to 2.4% in 2024, 2.1% in 2025, and 2.0% in 2026. Similarly, core PCE inflation is projected to slow down from 3.2% in 2023 to 2.4% in 2024, and then to 2.2% in 2025 and 2.0% in 2026.

Some FOMC reviews here.

- December FOMC: Dipping Dots – The Monetary Policy of the Future

- Fed Review: Rising Optimism

- Fed Holds Rates, Signals More Rate Cuts in 2024

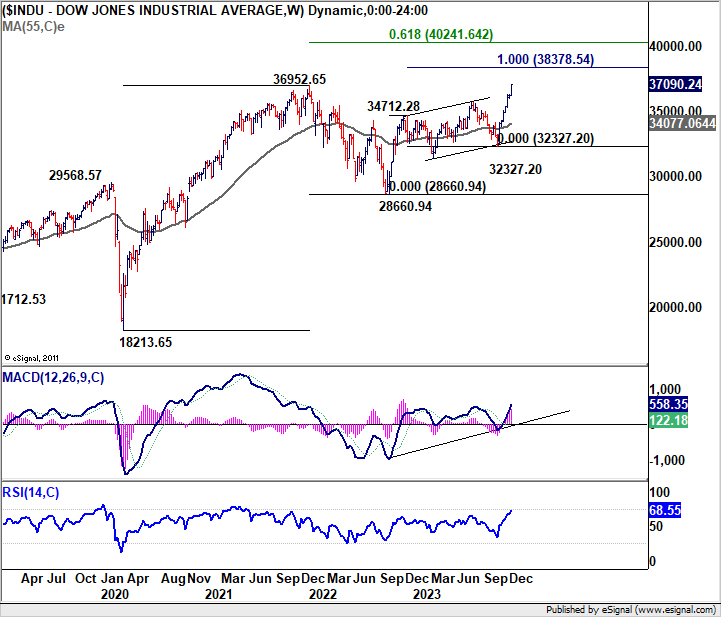

DOW hits new record post-FOMC, 10-year yield presses 4%

DOW surged 1.40% to close at new record high at 37090.24 overnight, after Fed outlined the path for interest rate cuts next year. While some volatility may be expected following this sharp increase, near term outlook will stay bullish as long as 36010.85 support holds. Next near term target is 100% projection of 28660.94 to 34712.28 from 32327.20 at 38378.54.

For the medium term, DOW would be looking at 61.8% projection of 18213.65 (2020 low) to 36952.65 (2022 high) from 28660.94 (2022 low) at 40241.64, which is close to 40k psychological level.

In contrast, 10-year yield lost -0.173 to 4.033, after hitting as low as 4.009, just managed to defend 4% handle. Some support could be seen from current level which is close to 55 W EMA (now at 3.956) and the long term trend line support to bring interim rebound. However, TNX should have completed the five wave rally from 0.398 (2020 low), and a correction to this up trend is underway. Sustainable support might only be found at 3.253 cluster support level, which is close to 38.2% retracement of 0.398 to 4.997 at 3.240.

New Zealand's Q3 GDP falls unexpectedly by -0.3%, manufacturing sector leads decline

New Zealand's GDP unexpectedly contracted by -0.3% qoq in Q3, a significant deviation from the anticipated 0.2% qoq growth. Notably, GDP per capita saw a more pronounced decrease of -0.9%. This downturn in economic activity was primarily led by -2.6% decline in the goods-producing industries. However, there were some positive aspects, with service industries experiencing growth of 0.4%, and primary industries seeing rise of 0.6%.

Ruvani Ratnayake, national accounts industry and production senior manager, pointed out, "All goods producing industries were down this quarter, led by a fall in manufacturing."

Despite the general decline in GDP, there was a silver lining as 8 out of 11 service industries recorded growth during the quarter. The most substantial improvements were observed in healthcare and social assistance, along with rental, hiring, and real estate services.

On the consumer front, household spending decreased by -0.6% during the quarter. This reduction was across all categories, with notable decline in durable goods. The fall in spending on motor vehicles, which came after a period of higher spending, was a significant factor in this overall decrease.

Australia's employment rises 61.5k in Nov, unemployment rate ticks up

Australia's employment sector grew significant by 61.5k in November substantially surpassing the expected 10.0k. This growth was primarily in full-time employment, which saw an increase of 47k, while part-time employment also rose by 14.5k.

Despite these positive developments in job creation, the unemployment rate edged up slightly to 3.9%, against expectations of remaining at 3.8%. Participation rate increased by 0.2% to reach 67.2%, and monthly hours worked were flat at 0.0%.

Bjorn Jarvis, ABS head of labour statistics, stated, "The combination of strong growth in both employment and unemployment in November saw the employment-to-population ratio return to a record high of 64.6 percent and the participation rate reach a new high of 67.2 percent."

Jarvis also noted that the slowing in hours worked suggests that the overall growth rates in employment and hours worked have become more aligned over the past 18 months. This convergence indicates a "less tight" labor market than previously experienced.

Will SNB, BoE, and ECB hint at upcoming rate cuts?

Three major central banks – SNB, BoE and ECB – are set to announce their policy decisions. All three will keep their interest rates unchanged. This comes in the wake of Fed's outlined plans for rate cuts in 2024 in the dot plot released overnight. Now, that raises questions about whether these central banks will follow and signal policy loosening for the next year.

SNB is expected to hold its key policy rate steady at 1.75%. This decision is supported by forecasts from Swiss State Secretariat for Economic Affairs released yesterday, projecting a slowdown in inflation to 1.9% in 2024 and further to 1.1% in 2025. Economic growth in Switzerland is also expected to decelerate to 1.1% in 2024 before rebounding to 1.7% in 2025.

BoE is anticipated to maintain interest rates at 5.25%. Traders have increased their bets on the BoE cutting rates following the unexpectedly sharp contraction in UK's monthly GDP for October. The market has fully priced in 100bps easing in monetary policy for 2024, bringing borrowing costs down to 4.25%. The first rate cut is anticipated in June. Today's voting pattern and accompanying statement from BoE will be under close scrutiny.

Similarly, the ECB is expected to keep its main refinancing rate at 4.50% and deposit rate at 4.00%. The focus will likely be on new DP and inflation forecasts and their implications for the rate path in the coming year. Money markets are currently pricing in almost 150bps of rate cuts for the next year.

In terms of currency performance, Swiss Franc appears to be the firmer one for the near term. As long as 0.9543 resistance holds, outlook in EUR/CHF remains bearish. Decisive break of 0.9402 support will resume larger down trend to 61.8% projection of 0.9995 to 0.9416 from 0.9683 at 0.9325.

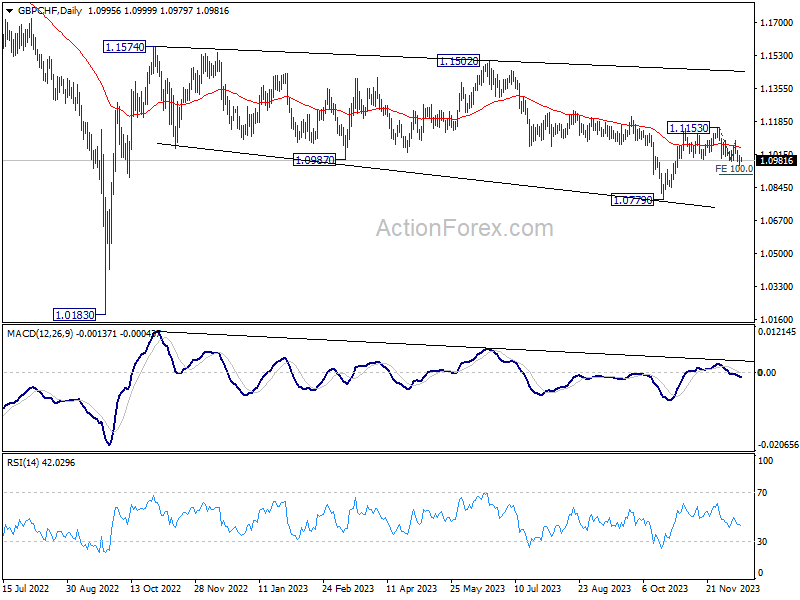

GBP/CHF's fall from 1.1153 resumed this week, and should be on track to 100% projection of 1.1153 to 1.0978 from 1.1085 at 1.0910. Sustained break there could prompt downside acceleration to 1.0779 and below, to resume larger down trend from 1.1574.

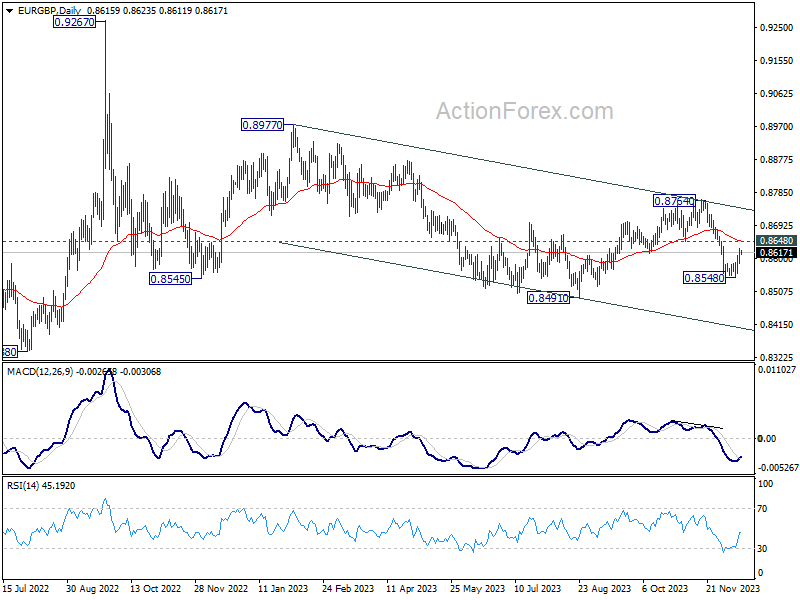

While Euro appears to be light strong then Sterling in the past few days, risk in EUR/GBP remains on the downside as long as 0.8648 resistance holds. Break of 0.8548 will likely bring deeper decline through 0.8491 to resume the medium term down trend.

On the data front

Swiss PPI will be released in European session. Canada wil publish manufacturing sales in North American session. US retail sales, jobless claims, import price index and business inventories will also be featured.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.74; (P) 145.47; (R1) 146.19; More...

USD/JPY's decline from 151.89 resumed by breaking through 141.59 support. Intraday bias is back on the downside. Further fall should be seen to next fibonacci level at 136.63. On the upside, above 142.91 minor resistance will turn intraday bias neutral first. But recovery should be limited well below 146.58 resistance to bring another decline.

In the bigger picture, current fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q3 | -0.30% | 0.20% | 0.90% | 0.50% |

| 23:50 | JPY | Machinery Orders M/M Oct | 0.70% | -0.50% | 1.40% | |

| 00:00 | AUD | Consumer Inflation Expectations Dec | 4.50% | 4.90% | ||

| 00:01 | GBP | RICS Housing Price Balance Nov | -43% | -58% | -63% | |

| 00:30 | AUD | Employment Change Nov | 61.5K | 10.0K | 55.0K | 42.7K |

| 00:30 | AUD | Unemployment Rate Nov | 3.90% | 3.80% | 3.70% | 3.80% |

| 04:30 | JPY | Industrial Production M/M Oct F | 1.30% | 1.00% | 1.00% | |

| 07:30 | CHF | Producer and Import Prices M/M Nov | 0.10% | 0.20% | ||

| 07:30 | CHF | Producer and Import Prices Y/Y Nov | -0.90% | |||

| 08:30 | CHF | SNB Interest Rate Decision | 1.75% | 1.75% | ||

| 09:00 | CHF | SNB Press Conference | ||||

| 12:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | 2--0--7 | 3--0--6 | ||

| 13:15 | EUR | ECB Interest Rate Decision | 4.50% | 4.50% | ||

| 13:30 | CAD | Manufacturing Sales M/M Oct | 0.30% | 0.40% | ||

| 13:30 | USD | Initial Jobless Claims (Dec 8) | 221K | 220K | ||

| 13:30 | USD | Retail Sales M/M Nov | -0.10% | -0.10% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Nov | -0.10% | 0.10% | ||

| 13:30 | USD | Import Price Index M/M Nov | -0.80% | -0.80% | ||

| 13:45 | EUR | ECB Press Conference | ||||

| 15:00 | USD | Business Inventories Oct | 0.00% | 0.40% | ||

| 15:30 | USD | Natural Gas Storage | -60B | -117B |

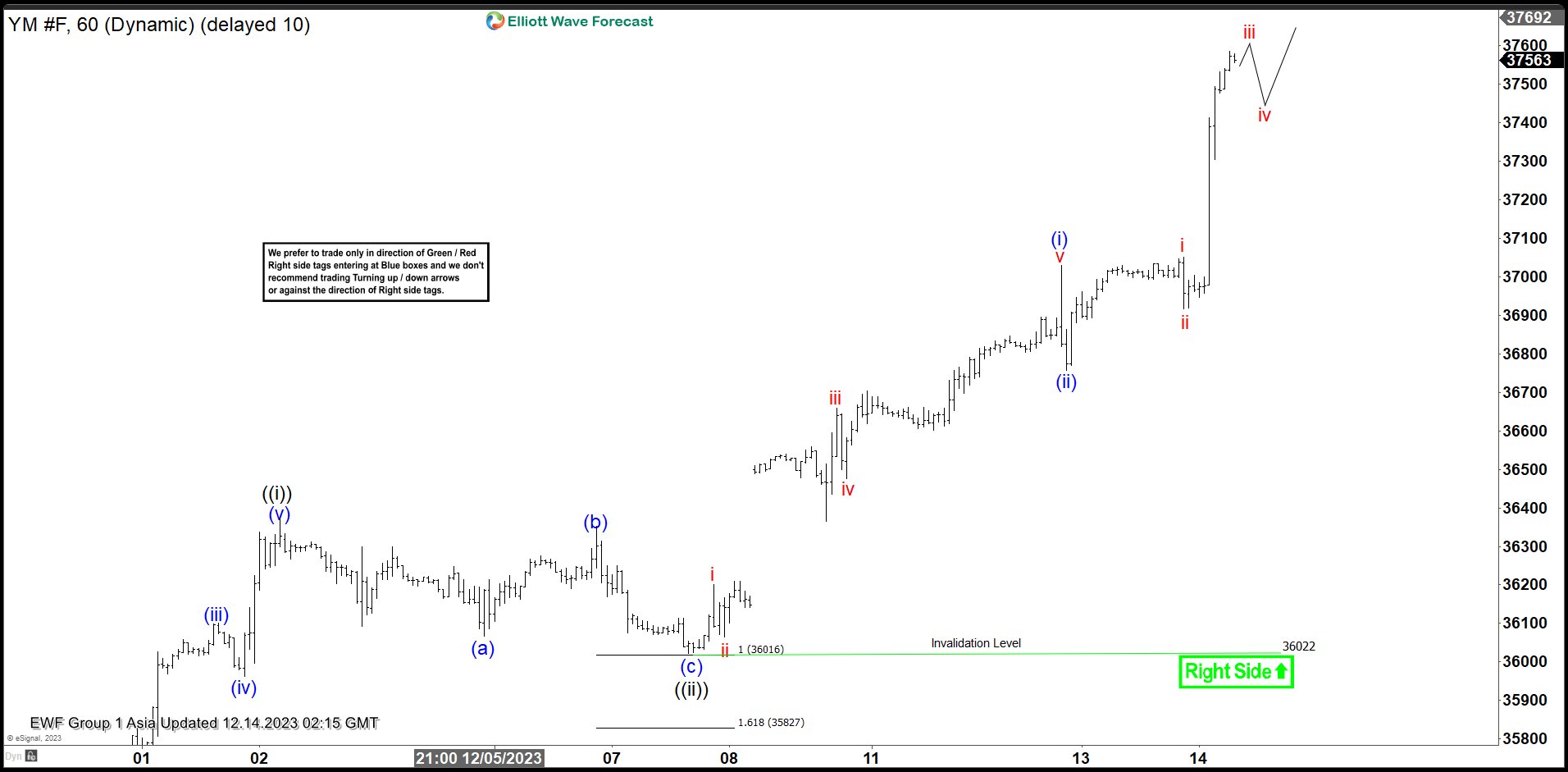

Dow Futures (YM) Breaking to New All-Time High

Dow Futures (YM) has broken to new all-time high, suggesting the trend remains firmly bullish. It also suggests the next bullish cycle has started. Short term, rally from 11.10.2023 low is currently in progress as a 5 waves impulse Elliott Wave structure. Up from 11.10.2023 low, wave ((i)) ended at 36337 and dips in wave ((ii)) ended at 36022. Internal subdivision of wave ((ii)) unfolded as a zigzag structure. Down from wave ((i)), wave (a) ended at 36066, wave (b) ended at 36352, and wave (c) lower ended at 36022. This completed wave ((ii)) in higher degree. Index has resumed higher in wave ((iii)) and broken to new all-time high.

Up from wave ((ii)), wave i ended at 36201 and wave ii ended at 36064. Wave iii higher ended at 36659, wave iv ended at 36476, and wave v higher ended at 37030. This completed wave (i) in higher degree. Pullback in wave (ii) ended at 36758. Index has resumed higher again in wave (iii). Up from wave (ii), wave i ended at 37051 and pullback in wave ii ended at 36917. Expect wave iii to end soon, then Index should pullback in wave iv, and then extend higher again. Near term, as far as pivot at 36022 low stays intact, expect pullback to find support in 3, 7, or 11 swing for further upside.

Dow Futures (YM) 60 Minutes Elliott Wave Chart

Dow Futures (YM) Elliott Wave Video

https://www.youtube.com/watch?v=AnvF2tb7sUY