Sample Category Title

EURUSD Gains in the FOMC Aftermath

- EURUSD reclaims 200-day SMA following dovish Fed signals

- ECB meeting later today could spur some volatility

- Momentum indicators are skewed to the positive side

EURUSD had been experiencing a solid downside correction from its recent three-month peak of 1.1016, which ceased just shy of the 50-day simple moving average (SMA). In the past few sessions though, the pair has been regaining some ground, with the rebound accelerating on the back of the dovish FOMC meeting.

Considering that both the RSI and stochastics are showing signs of strengthening positive momentum, the advance could extend towards the November resistance of 1.0964. Conquering this barricade, the bulls could attack the three-month peak of 1.1016 ahead of the February high of 1.1032. A violation of that region could open the door for the April-May resistance of 1.1094.

Alternatively, if the bears strike back and push the pair lower, initial support could be found at the 200-day SMA, currently at 1.0827. Further retreats could then stall around 1.0765, which served both as support and resistance in September. Failing to halt there, the price may slide towards 1.0693.

In brief, EURUSD has resumed its near-term firm tone following the dovish Fed rhetoric on Wednesday, while investors are eyeing the upcoming ECB meeting for fresh directional impetus.

SNB stands pat, downgrades inflation forecasts

SNB maintained its policy rate at 1.75%, aligning with widespread market expectations. This decision comes alongside a notable downgrade in inflation forecasts, which SNB now expects to remain "within the range of price stability" throughout the forecast period.

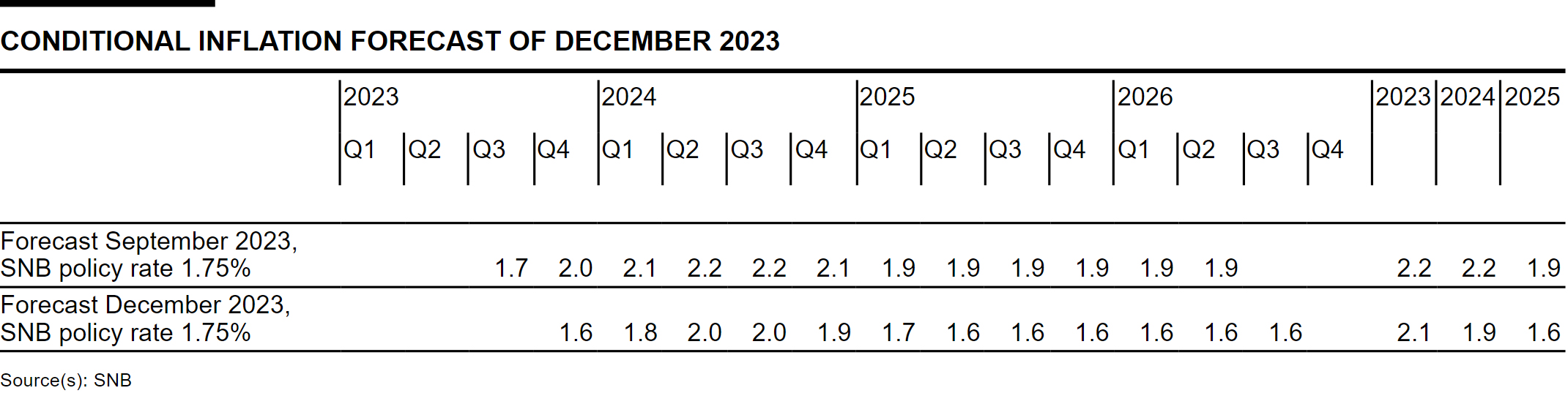

In terms of specific figures, or 2023, average inflation rate is now projected at 2.1%, a reduction from September's forecast of 2.2%. 2024 forecast has been adjusted to 1.9%, down from the previous estimate of 2.2%. Additionally, 2025 inflation prediction has been lowered to 1.6% from the earlier 1.9% projection.

The details of the forecast indicate that inflation is expected to peak in Q2 2024, which is lower than previously anticipated peak at 2.2%. Following this, inflation is projected to decline to 1.6% in Q2 of 2025 and maintain this level until Q3 of 2026.

SNB attributes this downward revision primarily to "recent lower-than-expected inflation" readings. In the medium term, the bank anticipates reduced inflationary pressure from international sources and somewhat weaker second-round effects.

On the growth front, SNB foresees a period of weak economic performance in the upcoming quarters. This outlook is influenced by subdued demand from international markets and tighter financing conditions. The bank's projections for GDP growth are set around 1% for 2023 and between 0.5% and 1% for 2024.

(SNB) Swiss National Bank leaves SNB policy rate unchanged at 1.75%

The Swiss National Bank is leaving the SNB policy rate unchanged at 1.75%. Banks' sight deposits held at the SNB are remunerated at the SNB policy rate up to a certain threshold, and at 1.25% above this threshold. The SNB is also willing to be active in the foreign exchange market as necessary.

Inflationary pressure has decreased slightly over the past quarter. However, uncertainty remains high. The SNB will therefore continue to monitor the development of inflation closely, and will adjust its monetary policy if necessary to ensure inflation remains within the range consistent with price stability over the medium term.

Inflation stood at 1.4% in November, and was thus somewhat lower than in the previous months. The slight decrease was above all attributable to lower inflation on goods and tourism services. However, inflation is likely to increase again somewhat in the coming months due to higher electricity prices and rents, as well as the rise in VAT.

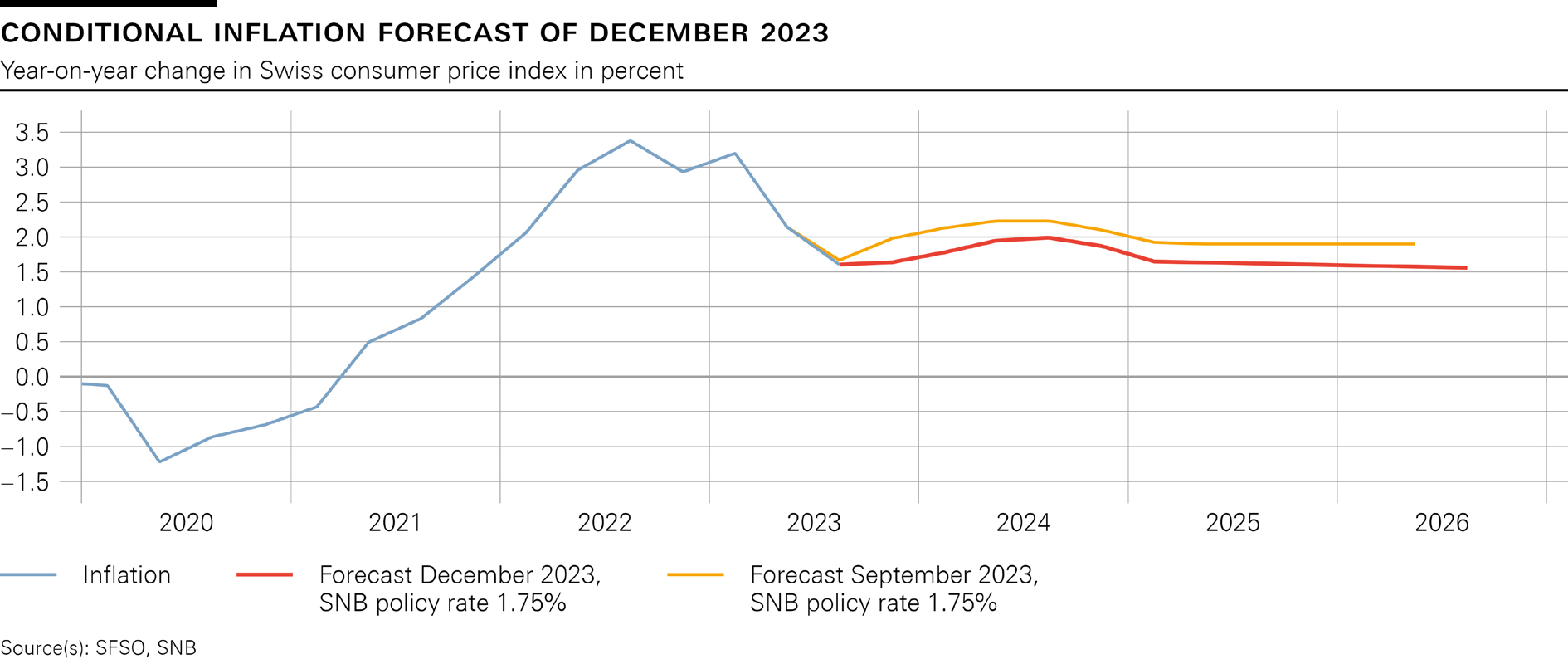

The new conditional inflation forecast is below that of September. In the short term, this is due to the recent lower-than-expected inflation. In the medium term, reduced inflationary pressure from abroad and somewhat weaker second-round effects are resulting in a downward revision. Over the entire forecast horizon, the inflation forecast is within the range of price stability (cf. chart). The forecast puts average annual inflation at 2.1% for 2023, 1.9% for 2024 and 1.6% for 2025 (cf. table). The forecast is based on the assumption that the SNB policy rate is 1.75% over the entire forecast horizon.

Global economic growth was stronger than expected in the third quarter of this year. Inflation has declined significantly in most countries in recent months. Against this backdrop, many central banks have refrained from further monetary policy tightening. With inflation still above the respective targets, monetary policy is likely to remain restrictive in many countries for the time being.

The growth outlook for the global economy in the coming quarters remains subdued. Inflationary pressure is likely to continue to ease.

This scenario for the global economy is still subject to large risks. Inflation could remain elevated for longer in some countries, necessitating a further tightening of monetary policy there. Equally, the energy situation in Europe could deteriorate over the course of the winter, and geopolitical tensions could increase. It therefore cannot be ruled out that global growth momentum will weaken more significantly than assumed.

Swiss GDP growth was moderate in the third quarter of this year. The services sector expanded again, while value added in manufacturing stagnated. Unemployment rose somewhat, and the utilisation of overall production capacity was only slightly above average.

Growth is likely to be weak in the coming quarters. Subdued demand from abroad and the tighter financing conditions are having a dampening effect. Overall, Switzerland's GDP is likely to grow by around 1% this year. For 2024, the SNB currently expects growth of between 0.5% and 1%. In this environment, unemployment is likely to continue to rise gradually, and the utilisation of production capacity should decline somewhat further.

The forecast for Switzerland, as for the global economy, is subject to high uncertainty. The main risk is a more pronounced economic slowdown abroad.

Momentum on the mortgage and real estate markets has weakened noticeably in recent quarters. However, the vulnerabilities in these markets remain.

More detailed information on the monetary policy decision can be found in the introductory remarks of the Governing Board.

Fed Overdelivers – Will ECB and BoE Follow?

The most hotly anticipated central bank meeting of the year did not disappoint on Wednesday, with the Fed potentially delivering this year's Santa rally.

I don't think many will have expected the Fed to go as far as it did in forecasting three rate cuts next year only three months after suggesting the tightening cycle is not over. But clearly, it's not just investors that have been impressed with the data we've seen so far in the fourth quarter and now they're getting more carried away than before.

There's been a lot of debate in recent weeks about whether investors are getting ahead of themselves, too optimistic about how quickly the Fed will cut rates but the message from the central bank is that is not the case. And in typical fashion, investors have now gone further, pricing in six rate cuts next year starting in March.

That's also forced investors to reassess whether they're in fact too pessimistic with other central banks too, with the ECB now expected to cut rates by 150 basis points over the next 12 months and the BoE between 100 and 125 basis points.

Both now have a lot to live up to today and Christine Lagarde, in particular, may not be thanking her US counterparts for whipping investors up into a frenzy right before their announcement and press conference. A repeat performance from the ECB could leave investors going into the end of the year in a much more festive mood.

Oil rebounds off its lows but demand concerns remain

Even oil managed to join in the celebrations, rallying almost 3% from its lows yesterday and it's adding to those gains today. It remains very close to its recent lows but the prospect of deep rate cuts from central banks next year has boosted the global economic prospects and in turn the price of oil. The question now is whether central banks are responding just in time or whether it will prove to be just too late. Oil prices over the coming weeks may offer some insight into market expectations on that.

A Santa rally for Gold?

Gold surged back above $2,000 after the Fed announcement and is once more not too far from the previous record highs. There's still some way to go to reach last week's peak, although that probably wasn't an accurate reflection of gold sentiment at the time. A weaker dollar and lower yields, if sustained, could continue to boost gold at a time when traders are feeling much more optimistic. Perhaps gold could enjoy a Santa rally of its own this year.

Hang Seng Index: Fed’s Dovish Pivot Provides a Temporary Breather

- Short-term technical analysis suggests a potential countertrend rebound with intermediate resistance at 16,890.

- China’s top policymakers’ reluctance to focus on making domestic demand revival a top priority for 2024 is likely to put a damper on positive animal spirits in the long term.

- A focus on making high-tech industrialization a top policy may trigger more headwinds for China and Hong Kong stock markets.

The China and Hong Kong benchmark stock indices have managed to catch a positive feedback loop from yesterday’s risk-on rally triggered by the US Federal Reserve’s dovish guidance.

But overall, their major downtrend phases have remained intact since February 2021 with the Hang Seng Index on track to end 2024 with a fifth consecutive yearly loss (2023 year-to-date loss is at 17% at this time of the writing); its worst performing streak since January 2002.

A similar weak performance is being reflected in the China CSI 300, on sight for a third consecutive yearly loss with a current year-to-date loss of -12.7% for 2023.

The persistent underperformance of China and Hong Kong stock markets against the rest of the world has been driven by past “unfriendly” private sector policies enacted in China, lingering geopolitical tensions with the US, and the right now, heightened deflationary risk spiral due to the liquidity crunch inflicted in the property market where it has a significant wealth effect on China’s society.

China’s top policymakers placed industrialization policy as the top priority for 2024

The recently concluded China’s annual economic work conference attended by the top leadership stated that next year’s priority will be on building a modern industrial system with a focus on developing cutting-edge technologies and artificial intelligence. This year’s priority of boosting domestic demand slipped to second spot for 2024. These 2024 economic goals and initiatives will be formalized and made official during the National People’s Congress, and Chinese People’s Political Consultative Conference (Two Sessions) in March 2024.

Hence, it seems that low odds for a significant and sustainable revival of bullish animal spirits for China and the Hong Kong stock markets in 2024 as policymakers are still reluctant to make a shift away from the current targeted approach to adopting more broad-based stimulus measures coupled with structural moves to remove bad assets from property developers’ balance sheets to reverse the chronic weakness seen in the property market.

US-China geopolitical tension may see an uptick in 2024

Also, making high-tech industrialization a key priority in 2024 is likely to invite more scrutinization from neo-conservative US politicians that may put a strain on the current US-China geopolitical theatrics that have witnessed a tense rivalry between the two superpowers in obtaining cutting-edge semiconductors chips and peripherals.

The US presidential election will be held in November 2024 and in the run-up to election day, there is likely to be intense debate among the presidential candidates and finger-pointing again at China’s current industrialization policy that needs to be “neutralized” due to its potential national security threat to the US. All in all, it is likely to trigger a bout of “uninvestable” narratives on China’s financial markets that may prevent a sustainable recovery from taking shape in 2024 for China and Hong Kong stock markets.

16,100 is the last line of defence for the Hang Seng Index

Fig 1: Hang Seng Index long-term secular trend as of 14 Dec 2023 (Source: TradingView, click to enlarge chart)

The current price actions have managed to retest and held at the long-term secular ascending trendline in place since the Asian Financial Crisis’s August 1998 low now acting as support at 16,100.

The long-term monthly RSI momentum indicator has continued to exhibit bearish momentum reading below key parallel resistance at the 50 level which suggests that the 16,100 key major support is vulnerable to a major bearish breakdown.

A weekly close below 16,100 may trigger a potential multi-month impulsive downleg sequence within its major downtrend phase to expose the next major support at 12,200 (also the Great Financial Crisis’s swing lows area of October 2008/March 2009).

Potential short-term minor countertrend rebound

Fig 2: Hong Kong 33 minor short-term trend as of 14 Dec 2023 (Source: TradingView, click to enlarge chart)

In the lens of technical analysis, price actions do not move in vertical directional movements as market participants adjust their behaviours accordingly to the latest related events and news flow.

The short-term hourly chart of the Hong Kong 33 Index (a proxy of the Hang Seng Index futures) has staged a bullish breakout above the resistance of a minor descending channel from the 23 November 2023 high which increases the odds that a minor countertrend rebound motion may be in progress.

Watch the 16,100 key pivotal support and a clearance above 16,500 may see the next intermediate resistance coming in at 16,890 (the downward sloping 20-day moving average & the 38.2% Fibonacci retracement of the prior down move from 16 November 2023 high to 11 December 2023 low).

However, failure to hold at 16,100 invalidates the countertrend rebound scenario to expose the next intermediate supports of 15,890 and 15,500 in the first step.

Fed Took An Impressive U-turn

Markets

At the final meeting of the Fed took an impressive U-turn from its 2023 approach. 2024 will be different chapter for monetary policy. The Fed left its policy rate unchanged at 5.25%-5.50%. A further rate hike isn’t formally ruled out, but the Fed Chair Powell at press conference and the dots clearly signaled that the Fed is trying to find out when it can start scaling back policy tightening. Inflation, also core, is cooling. That allows the Fed to turn the focus away from inflation and again look to the two sides of its mandate, including growth and the labour market. After a strong performance up until the third quarter of this year, activity now shows signs of slowing and the labour market, while still strong, is coming better into balance. The dots see growth at a below trend 1.4% next year down from 2.6% this year returning back to trend in 2025 (1.8%). Unemployment is seen ticking up to 4.1% (2024-26) from 3.8% currently. Slower demand will push PCE inflation to 2.4% next year and 2.1% and 2.0% respectively in 2024 and 2025. This combination will allow the Fed to make policy less restrictive. The dot plot now ‘guides’ 75 bps of rate cuts by the end of next year. Admittedly, dispersion among the views was big. Even so, the new direction of Fed thinking is obvious. Powell in this respect said that the Fed is well aware of the risk of overtightening. The Fed Chair also didn’t give any sign that the MPC felt uncomfortable with recent easing of monetary conditions. A clear go ahead for recent market positioning and that is exactly what happened. US yields fell off a cliff with the curve bull steepening. The 2-y lost 30.4 bps. The 10-y declines 18.4 bps and currently trades below 4.0%. The 30-y still eased 13.3 bps. Markets now full discount a first rate 25 bps rate cut in March and 1.5% easing end next year. Equities flourished with the Dow, S&P 500 and the Nasdaq all gaining about 1.4%. The Dow even set a new all-time top. The dollar tumbles sharply (DXY 102.87, EUR/USD 1.0874), but in both cases stays above the end November low. This was different for USD/JPY setting a now correction (testing 141 this morning).

The focus today turns to policy decisions of the ECB and, to a lesser extent, the Bank of England. As was the case for the Fed, the ‘guidance’ from the ECB staff projections and the assessment of ECB Chair Lagarde at the press conference will be key. Until now, ECB policymakers showed a more decisive ‘leaning against easing’ bias than the Fed. Questions is whether the ECB inflation forecasts will be reduced enough for Lagarde and Co to already formally open the debate on 2024 rate cuts. Even if the ECB takes a more guarded approach, important spill-over effects from the US will hit European markets. If the ECB takes a less obvious U-turn than the Fed, a retest of EUR/USD 1.10 might be on the cards. We also look out for any communication on the start of the roll-off of the ECB’s PEPP bond portfolio.

News headlines

Australian November employment crushed expectations, adding 61.5k jobs, well above the 11.5k expected. The participation rate hit a new record high of 67.2%. The increased pool of available workers caused the unemployment rate to rise somewhat (3.9%) but it stays well below pre-pandemic levels of around 5%. Head of the Australian Bureau of Statistics’ labour department Jarvis concluded that “We have continued to see employment growth keeping pace with high population growth through 2023.” The strong labour report does little to offset the effect of yesterday’s Fed pivot on markets outside the US though. Australian swap yields did find a bottom shortly after the release this morning. They currently drop 1-3.1 bps. Following the Fed decision, money markets now expect a first RBA rate cut in June compared to September/November just yesterday. The Aussie dollar extends a (mainly USD-driven) surge with AUD/USD now at the highest level since July (0.672).

GDP in New-Zealand unexpectedly contracted in Q3 at -0.3% q/q vs a 0.2% expansion expected, bringing the yearly figure to -0.6% (0.5% consensus). Q2 numbers also were sharply downwardly revised (from 0.9% to 0.5%). The goods producing sector took the brunt in a deceleration (-2.6% q/q) while services still eked out some growth (0.4%). The contraction suggests the Reserve Bank of New Zealand’s tightening is really kicking in. The expenditure approach showed household spending dropping (-0.6%) as well as exports. The RBNZ held the policy rate unchanged at 5.5% since May, signaled the risk of a further hike next year and penciled in no rate cuts until mid-2025. But markets don’t believe one word, especially not after the Fed. A first cut is seen in May. The damage for the kiwi dollar remains contained thanks to a weak USD. NZD/USD even rebounded to the strongest level since July (0.623).

Surprise Dovish Twist

The Federal Reserve (Fed) wraps up the year with a resounding finale. The Fed is not bothered to see the US yields fall in preparation for a rate cut. On the contrary, they endorsed the idea of a policy pivot thanks to an encouraging fall in inflation and sounded way more dovish than everybody expected at their announcement yesterday – which clearly exposed that the policy pivot is coming. This is the major take of the final FOMC meeting of the year, and it was totally unexpected. Jerome Powell still said – just for the sake of saying – that ‘it is far too early to declare victory’ over inflation, but the committee lowered their inflation forecasts for this year and the next, and the so-called dot plot – which plots where the Fed officials see the interest rates going – plotted a 75bp cut in Fed funds rate next year. The median expectation now suggests that the Fed rate will be lowered to 4.6% by the end of next year. And that’s quite a big change compared to last time the Fed President spoke to say that the rates would stay high for long. It now appears that the rates won’t stay high for so long. The first Fed rate cut is now expected to happen in March, with more than 85% probability.

As a result, the US 2-year yield – which captures the Fed rate bets – sank to 4.33% yesterday, and with the dovish message that the Fed sent to the market, the 4.50% level that I saw as a support at the start of this week should now act like a resistance. The US 10-year yield sank below 4%, reflecting the idea that the policy pivot suggests some meaningful slowdown in the US economy. The falling yields sent the S&P500 above the 4700 mark, to the highest levels in almost two years and the Dow Jones Industrial Index hit a record high. There is no reason to stop believing that the S&P500 will soon renew record as well, unless there is a meaningful decline in earnings expectations.

The dovish Fed echoed loudly across the FX markets as well. The US dollar was sharply sold, the EURUSD rebounded back above the 1.09 level, Cable extended gains to 1.2650 and the USDJPY fell almost 1.80% yesterday and slipped below the 141 level this morning. Trend and momentum indicators are comfortably negative, the fundamentals – meaning the narrowing divergence between the more dovish Fed and the more hawkish Bank of Japan (BoJ) – are comfortably positive for the yen, hence price rallies in the USDJPY are now seen as opportunities to strengthen the short USDJPY positions.

Now today, it’s the European Central Bank (ECB) and the Bank of England’s (BoE) turn to give their final policy verdict for this year. And both Mme Lagarde and Mr. Bailey are certainly annoyed to see the Fed go so soft yesterday, as Christine Lagarde had said herself that no reduction in rates should be expected in the next few quarters. It will be interesting to see if ECB and BoE officials feel comfortable about giving up their tough stance. I still believe that Lagarde will repeat that it’s too early to talk about rate cuts, in which case we could see the EURUSD jump above the 1.10 level and finish the year above this level.

Across the Channel, the situation is less obvious. The UK economic outlook is not bright, and wages show signs of slowing. One big argument is that inflation has more than halved in the UK since the start of this year. Yes. But inflation in the UK – though halved – stands at 4.6% which is more than twice the BoE’s 2% target. The latter makes the BoE less inclined to initiate rate cuts compared to the other two major central banks.

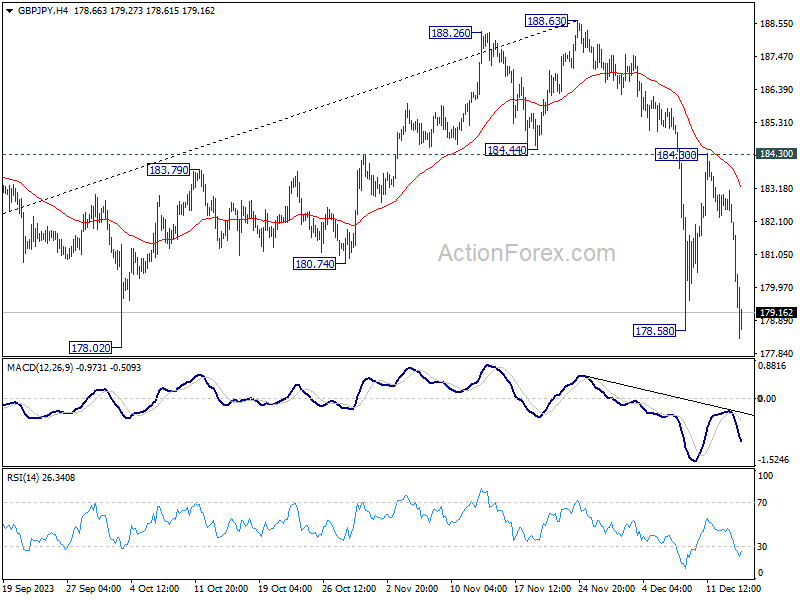

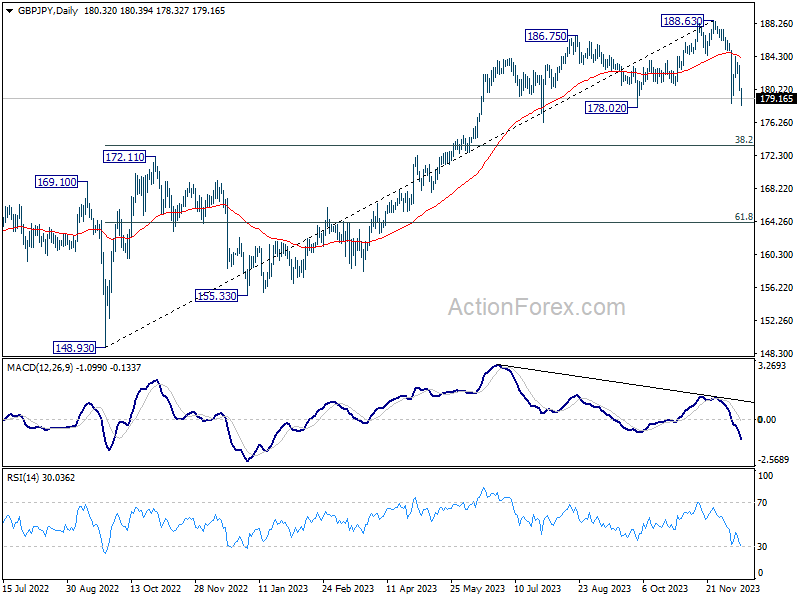

GBP/JPY Daily Outlook

Daily Pivots: (S1) 179.30; (P) 181.22; (R1) 182.25; More...

GBP/JPY's breach of 178.58 support indicates resumption of whole fall from 188.63. Intraday bias is back on the downside. Break of 178.02 support will pave the way to 38.2% retracement of 148.93 to 188.63 at 173.46. For now, risk will stay on the downside as long as 184.30 resistance holds, in case of recovery.

In the bigger picture, while a medium term top is in place at 188.63, there is no clear sign of long term bearish trend reversal yet. As long as 55 W EMA (now at 175.67) holds, price actions from 188.63 are seen as a corrective move only. Larger up trend from 123.94 (2022 low) could resume at a later stage.

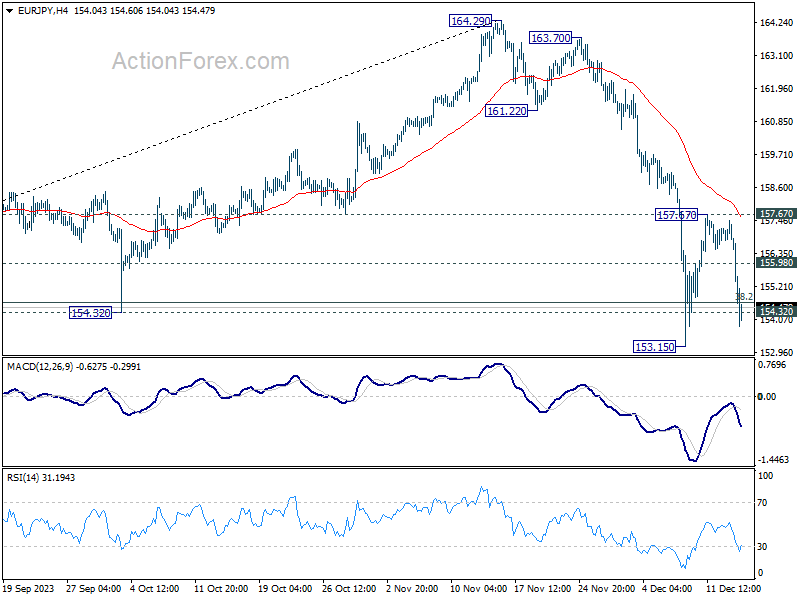

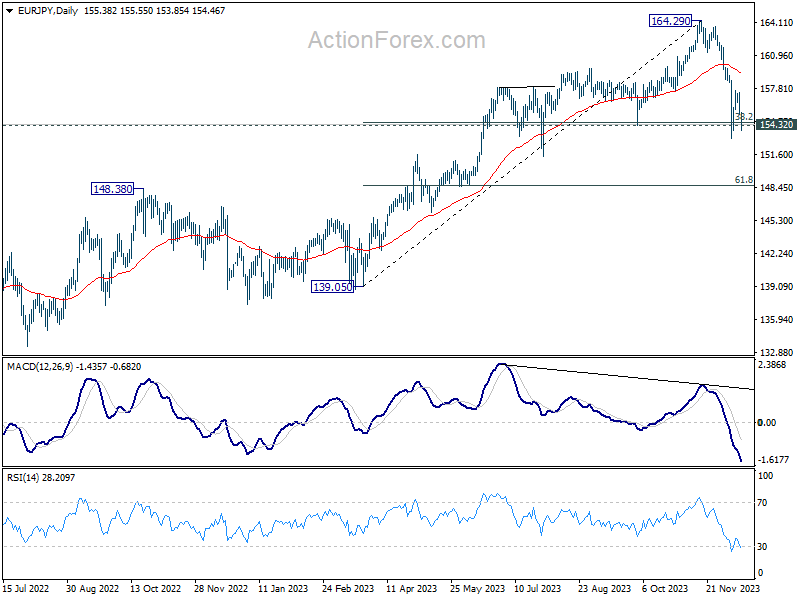

EUR/JPY Daily Outlook

Daily Pivots: (S1) 154.70; (P) 156.09; (R1) 156.79; More..

EUR/JPY's break of 155.98 minor support suggests that recovery from 153.15 has completed at 157.67 already. Intraday bias is back on the downside for retesting 153.15 first. Firm break there will resume whole fall from 164.39 to 61.8% retracement of 139.05 to 164.29 at 148.69. For now, outlook will remain cautiously bearish as long as 157.67 resistance holds, in case of recovery.

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.

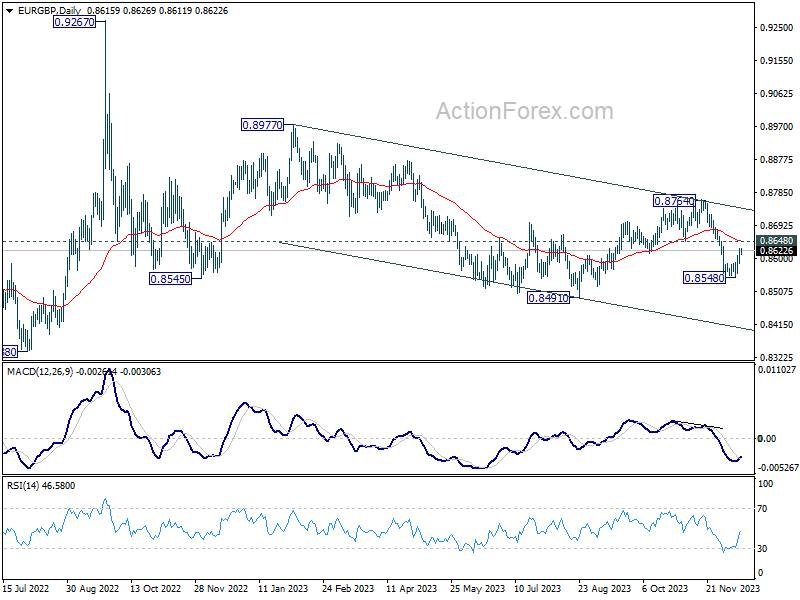

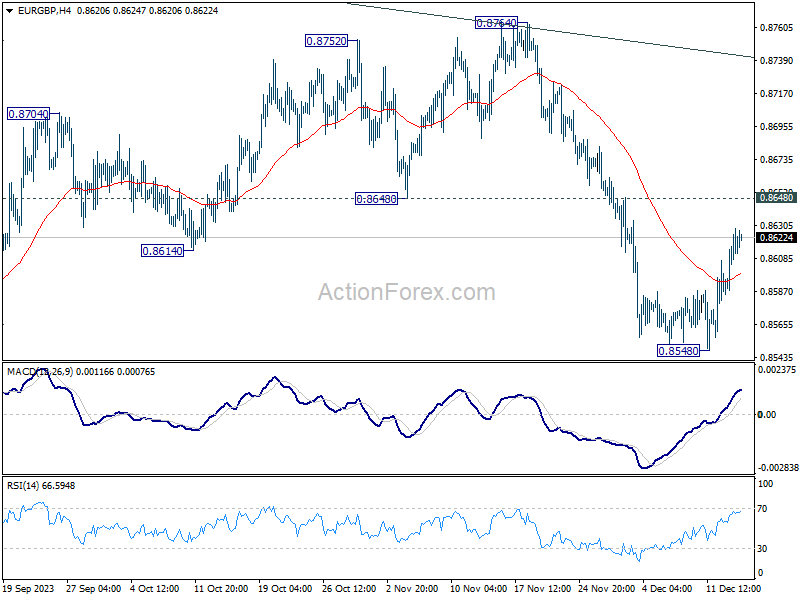

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8594; (P) 0.8612; (R1) 0.8636; More....

Intraday bias in EUR./GBP stays neutral for the moment, and further decline is expected with 0.8648 support turned resistance intact. on the downside, break of 0.8548 will resume the fall from 0.8764 to 0.8491 support next. Firm break there will resume larger down trend. However, sustained break of 0.8648 will turn bias to the upside for stronger rebound.

In the bigger picture, current development suggests that down trend from 0.9267 (2022 high) is still in progress. This decline is seen as the third leg of the pattern from 0.9499 (2020 high). Break of 0.8201 will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969. In any case, outlook will stay bearish as long as 0.8764 resistance holds.